Global Surgical Booms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

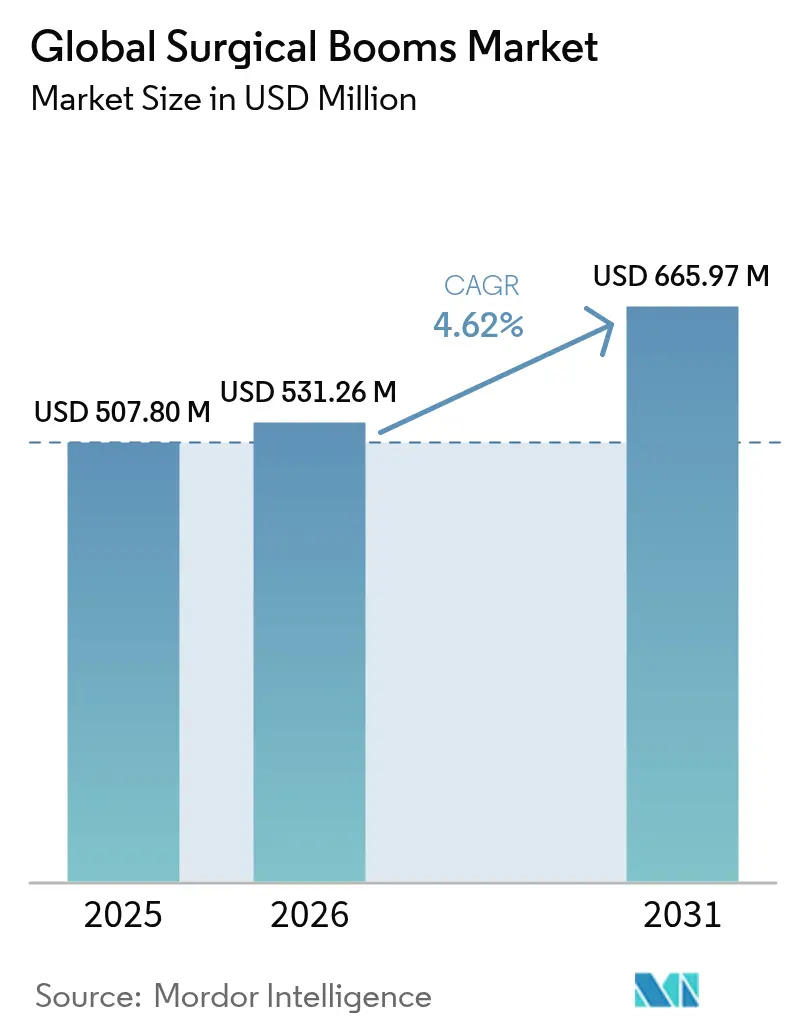

| Market Size (2026) | USD 531.26 Million |

| Market Size (2031) | USD 665.97 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Surgical Booms Market Analysis by Mordor Intelligence

The Surgical Booms market size is expected to grow from USD 507.80 million in 2025 to USD 531.26 million in 2026 and is forecast to reach USD 665.97 million by 2031 at 4.62% CAGR over 2026-2031. Rising adoption of hybrid operating rooms, rapid growth of ambulatory surgery centers, and hospital decarbonization initiatives are together pulling capital toward ceiling-mounted infrastructure. At the same time, IoT-driven predictive-maintenance contracts are shifting service models from reactive repairs to proactive asset management, keeping surgical suites online longer and lowering lifetime ownership costs. Pent-up surgical demand after COVID-19, coupled with persistent clinician preference for minimally invasive procedures, ensures continuous utilization of advanced ceiling systems. Vendors now compete primarily on integration depth with imaging, robotics, and data platforms rather than on headline price, which underscores how technical differentiation is reshaping the Surgical Booms market.

Key Report Takeaways

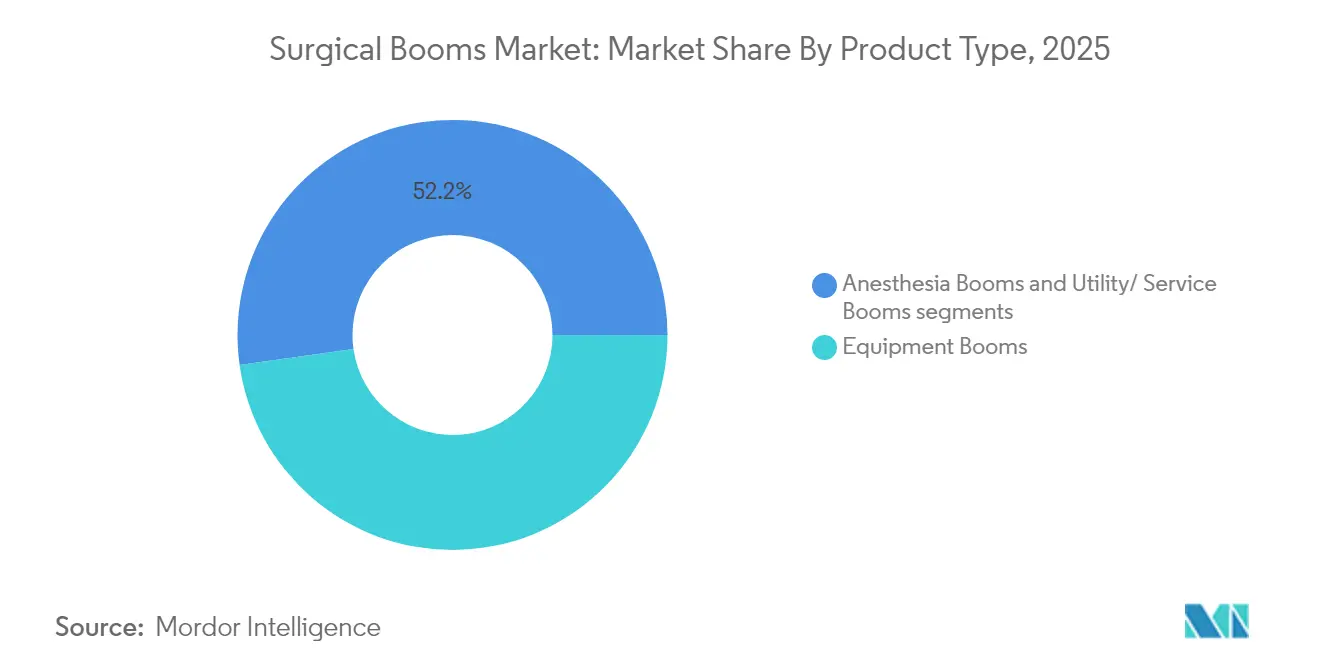

- By product type, Equipment Booms led with 47.78% revenue of the Surgical Booms market share in 2025; Hybrid/Combination Booms are forecast to grow at 4.98% CAGR through 2031.

- By arm type, Single-Arm systems held 53.62% of the Surgical Booms market size in 2025, while Multi-Arm systems are expanding at a 5.67% CAGR through 2031.

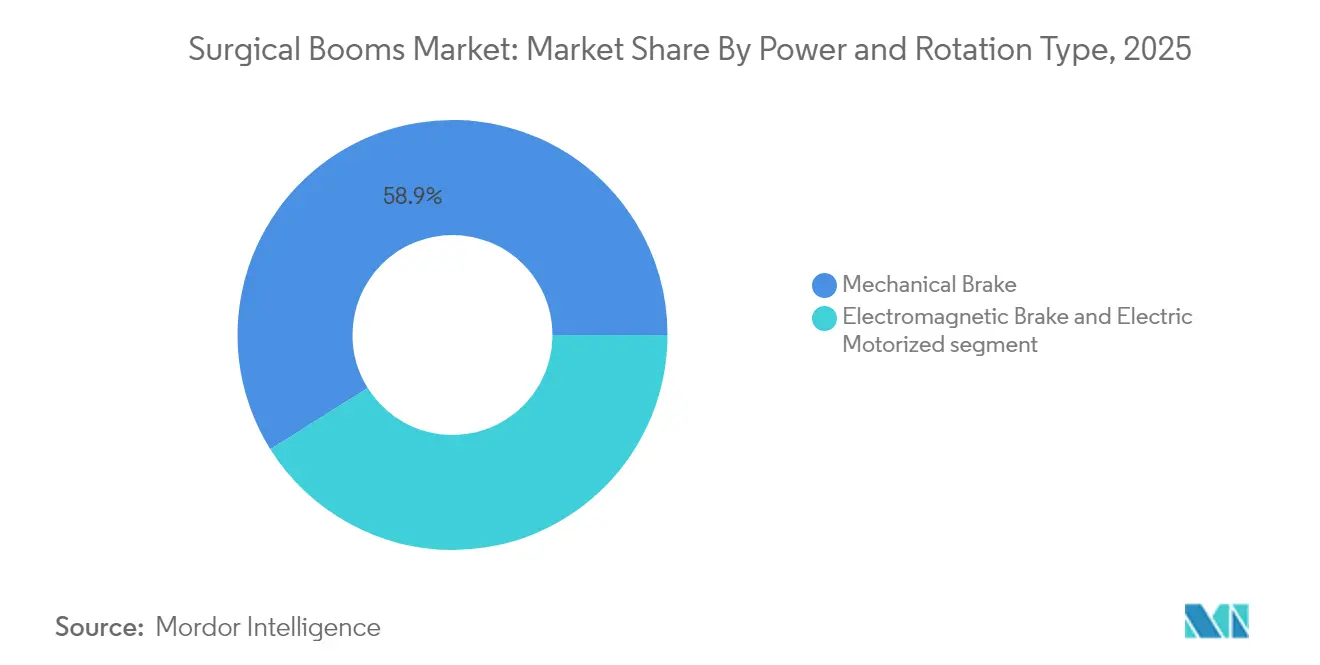

- By power & rotation mechanism, Mechanical Brake units captured 58.91% revenue in 2025; Electric Motorized mechanisms post the fastest growth at a 5.86% CAGR to 2031.

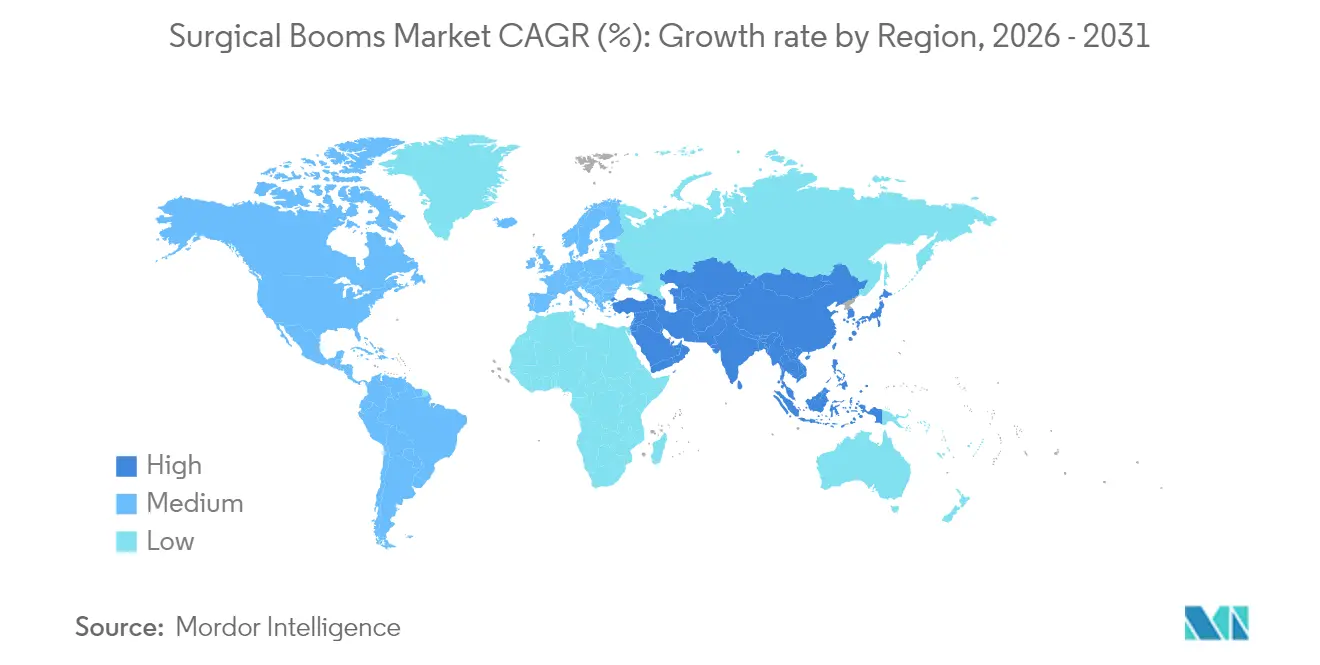

- By geography, North America accounted for 41.88% of the Surgical Booms market in 2025; Asia-Pacific is advancing the fastest at a 6.78% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Booms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hybrid-OR build-outs in tertiary hospitals | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Ambulatory Surgery Center (ASC) proliferation in OECD nations | +0.8% | Global, concentrated in North America | Short term (≤ 2 years) |

| Rising adoption of integrated OR-IT & video routing platforms | +0.7% | Global, led by developed markets | Medium term (2-4 years) |

| Post-COVID backlog driving procedure-room expansion | +0.9% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| IoT-enabled predictive-maintenance contracts for booms | +0.4% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Hospital decarbonization targets favouring modular ceiling utilities | +0.3% | EU & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Hybrid-OR Build-outs in Tertiary Hospitals

Tertiary hospitals are accelerating hybrid suite construction to merge open surgery and advanced imaging. Vancouver General Hospital’s 2025 expansion added 15 rooms and upgraded a hybrid suite, lifting annual cases above 19,000. Virtua Health’s USD 500 million project introduces 10 rooms, two of which are hybrid, specifically supporting high-acuity cardiovascular and gastrointestinal interventions. These spaces need booms that can bear heavier payloads, route complex utilities, and integrate seamlessly with imaging and robotics, driving premium demand across the Surgical Booms market.

Ambulatory Surgery Center Proliferation in OECD Nations

The United States hosted 11,555 ASCs by mid-2024, representing a USD 43.1 billion setting with 2.88 rooms per center. Medicare beneficiaries treated at ASCs climbed to 3.4 million in 2023[1]Source: Medicare Payment Advisory Commission, “March 2025 Report,” medpac.gov . ASC owners prefer ceiling systems that shorten turnover, streamline visualization, and fit lower ceiling heights typical of outpatient builds, underpinning steady intake in the Surgical Booms market.

Post-COVID Backlog Driving Procedure-Room Expansion

Hospitals lost roughly 35% of surgical volume during early 2020, leaving an orthopedic backlog surpassing 1 million cases. Health Sciences Centre in Manitoba launched a USD 100 million program to raise surgical capacity by 25% via new rooms equipped with modern ceiling infrastructure cbc.ca. Clearing backlogs requires efficient, multipurpose rooms, reinforcing procurement momentum for the Surgical Booms market

Rising Adoption of Integrated OR-IT & Video Routing Platforms

Systems such as KARL STORZ OR1 NEO® centralize device control, imaging, and data management through overhead hubs. Sapporo Kashiwabakai Hospital’s SMART suite documented workflow gains once data routing, sterilization bridges, and boom positioning converged in a single ceiling grid Integration raises cabling, network, and structural demands, pushing hospitals to favor advanced booms and enlarging the Surgical Booms market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit cost for brown-field ORs | -0.6% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Extended procurement cycles & facility-planner shortages | -0.4% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Supply-chain bottlenecks in medical-gas connectors & bearings | -0.3% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Limited reimbursement linkage for capital OR fixtures | -0.2% | North America & EU regulatory markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Cost for Brown-field ORs

Renovation consumes 35–55% of new-build budgets, with healthcare construction averaging USD 700-730 per sq ft. St. Francis Hospital’s cardiac unit upgrade cost USD 2.2 million and required temporary closures. Such expense discourages some mature facilities from installing new ceiling platforms, muting a portion of near-term demand inside the Surgical Booms market.

Extended Procurement Cycles & Facility-Planner Shortages

Seventy-one percent of hospitals cite distribution delays, while facility-planning teams operate under staffing gaps that drag out capital approvals. Cross-department coordination now spans HTM, IT, and building engineering, extending order-to-install timelines. These frictions shift revenue recognition outward for suppliers and shave growth points off the Surgical Booms market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Dominance Drives Integration

Equipment Booms retained 47.78% revenue in 2025 because they anchor anesthesia workstations, imaging displays, and surgical lights within compact footprints. Hybrid/Combination Booms, although smaller in base, exhibit a 4.98% CAGR thanks to rising universal-room strategies. Vancouver General Hospital’s build underscores how versatile booms allow any procedure in any room. CleanSuite by Steris illustrates the trend by delivering ISO Class 5 sterility with 40% cost savings and six-fold faster installs. Integration pressure keeps Equipment Booms central to the Surgical Booms market, while combination units promise the headroom for future tech additions.

By Arm Type: Multi-Arm Systems Gain Workflow Advantage

Single-Arm layouts captured 53.62% share in 2025 because they serve cost-sensitive facilities focusing on straightforward cases. Multi-Arm systems rise at 5.67% CAGR as complex minimally invasive procedures require concurrent imaging, suction, and robotics. St. Tammany Health System’s outpatient center runs Da Vinci and Mako robots from multi-arm platforms sttammany.health. This migration improves ergonomics, reduces floor clutter, and heightens room turnover, sustaining momentum in the Surgical Booms market size for the multi-arm class.

By Power & Rotation Mechanism: Electric Automation Transforms Precision

Mechanical Brake designs held 58.91% revenue in 2025; however, Electric Motorized variants track a 5.86% CAGR. BG Klinik’s Ciartic Move self-propelled C-arm highlights automation benefits by eliminating manual alignment. Electric units allow programmable presets, integrate IoT sensors, and maintain tighter infection-control protocols because staff touch fewer surfaces. As hospitals embed digital maintenance suites, Electric systems will claim greater revenue inside the Surgical Booms market.

Geography Analysis

North America generated 41.88% of 2025 revenues, buoyed by well-funded capital budgets and early adoption of surgical robotics. Reimbursement stability allows hospitals to replace ceiling equipment on predictable cycles, and updated building codes mandate higher availability rates—trends that collectively sustain purchasing activity in the Surgical Booms market.

Europe shows mid-single-digit growth anchored by decarbonization directives. The EU’s focus on energy-efficient infrastructure compels facilities to specify modular ceiling utilities compatible with smart HVAC, which raises demand for next-generation booms. Ageing populations further elevate procedure volumes, lending resilience to European contributions within the Surgical Booms market.

Asia-Pacific is advancing at 6.78% CAGR. China’s hospital construction outlays exceed USD 75 billion for 2020-2025, while India’s leading chains intend to add 17,800 beds via ₹14,600 crore programs. Getinge seeks to raise its Indian share from 30% to 45%, illustrating competitive heat. Multilateral funding from the Asian Infrastructure Investment Bank eases capital constraints for public builds, enlarging the addressable Surgical Booms market across emerging Asia.

Competitive Landscape

The Surgical Booms market is moderately consolidated. Stryker, Steris, Getinge, and Drägerwerk emphasize integration depth, cybersecurity, and lifecycle service bundles. Stryker’s USD 4.9 billion purchase of Inari Medical widens its vascular reach and potential boom attach-rate. Steris drives turnkey adoption via CleanSuite, cutting installation times dramatically and pitching ISO-Class sterility in one contract. Getinge’s U.S. Defense Health cybersecurity clearance secures access to large federal tenders.

Emerging players exploit regional procurement models and e-commerce. Mindray’s alliance with Amazon Business lowers transaction friction for mid-tier buyers. Baxter’s voice-activated Voalte Linq signals convergence between communication platforms and ceiling equipment, hinting at future function layers. As autonomous positioning, AI guidance, and predictive analytics proliferate, mechanical engineering alone will not preserve competitive edges, widening the innovation race in the Surgical Booms market.

Global Surgical Booms Industry Leaders

Hill-Rom Services, Inc.

Steris

Amico Group of Companies

Zimmer Biomet

Stryker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stryker completed acquisition of Inari Medical for USD 4.9 billion, adding endovascular capabilities.

- February 2025: SLD Technology AirFRAME Modular Ceiling System – Introduced fully integrated modular ceiling system enabling 3-hour installation for general operating rooms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical booms market as revenue from brand-new, ceiling- or floor-mounted arms that channel medical gases, power, data, monitors, and accessory shelves inside operating rooms in hospitals and ambulatory surgery centers, thereby decluttering floors and supporting advanced imaging or robotic systems. According to Mordor Intelligence, these units are treated strictly as capital equipment instead of consumables.

Scope exclusion: Refurbished systems, basic wall pendants, and mobile carts are purposely left outside the model because they follow different depreciation and pricing paths.

Segmentation Overview

- By Product Type (Value)

- Equipment Booms

- Anesthesia Booms

- Utility / Service Booms

- Hybrid / Combination Booms

- By Arm Type (Value)

- Single-Arm

- Dual-Arm

- Multi-Arm

- By Power & Rotation Mechanism (Value)

- Mechanical Brake

- Electromagnetic Brake

- Electric Motorized

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed biomedical engineers, peri-operative nurses, facility planners, and procurement heads across North America, Europe, and Asia. Their insights on boom penetration ratios, warranty extensions, and expected ASP erosion proved essential to close information gaps and to triangulate final figures.

Desk Research

We combined openly available statistics from bodies such as the World Health Organization, OECD Health Statistics, the American Society of Healthcare Engineers, and multiple national health ministries with technical standards from ECRI and the US FDA device registry to size potential demand and replacement cycles. Company filings, investor decks, and reputable press offered selling-price clues, while paid platforms, D&B Hoovers for company splits and Dow Jones Factiva for contract news, added further granularity. The sources noted here are illustrative; many additional references were consulted to validate every assumption.

Market-Sizing & Forecasting

A top-down build starts with annual surgical procedure volumes and new operating-room projects; these totals are multiplied by validated boom penetration rates and median ASPs, then cross-checked through selective bottom-up supplier roll-ups. Five fingerprint variables, procedure growth, ASC share, hybrid-OR adoption, capital budget per OR, and five-year replacement cadence, feed a multivariate regression that produces a baseline value and a growth rate through the forecast period.

Data Validation & Update Cycle

Outputs run through variance checks against import records and hospital tender data before a three-step analyst review. Reports refresh annually, with interim revisions triggered by regulatory shifts or sizable tender awards, and an analyst reruns key inputs just prior to client release.

Why Mordor's Surgical Booms Baseline Commands Practical Trust

Published values often diverge because firms use different product baskets, regional weights, and refresh schedules. Scope creep, refurbished units, booking one-time installation fees as equipment revenue, or optimistic ASP curves can all inflate or deflate totals.

Mordor Intelligence restricts scope to brand-new booms, anchors ASPs to current tender data, and updates its model yearly, producing the dependable baseline below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 507.8 m (2025) | Mordor Intelligence | |

| USD 433.3 m (2023) | Global Consultancy A | Omits Asia-Pacific hybrid-OR builds; relies on 2021 ASPs |

| USD 444.4 m (2024) | Industry Association B | Bundles refurbished booms and service contracts as hardware |

| USD 388.9 m (2022) | Regional Consultancy C | Uses hospital-start counts without procedure-growth overlay |

The comparison underscores that when scope, current pricing, and timely refresh align, Mordor's disciplined approach offers decision-makers a transparent, reproducible starting point.

Key Questions Answered in the Report

What is the current Global Surgical Booms Market size?

The Global Surgical Booms Market size was USD 531.26 million in 2026 and is projected to register a CAGR of 4.62% during the forecast period (2026-2031)

Who are the key players in Global Surgical Booms Market?

Hill-Rom Services, Inc., Steris, Amico Group of Companies, Zimmer Biomet and Stryker are the major companies operating in the Global Surgical Booms Market.

Which is the fastest growing region in Global Surgical Booms Market?

Asia-Pacific is estimated to grow at the highest CAGR of 6.78% over the forecast period (2026-2031).

Which region has the biggest share in Global Surgical Booms Market?

In 2025, the North America accounts for the largest market share in Global Surgical Booms Market.

What years does this Global Surgical Booms Market cover?

The report covers the Global Surgical Booms Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Surgical Booms Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: