Surgical Stapler Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

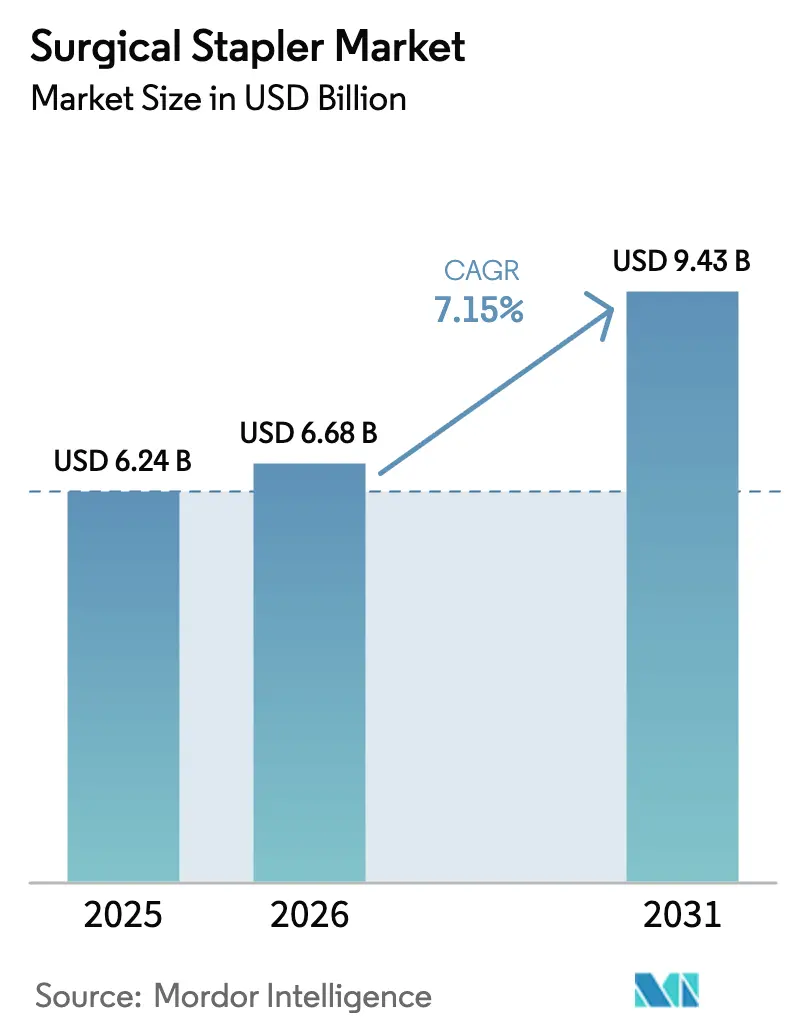

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 9.43 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

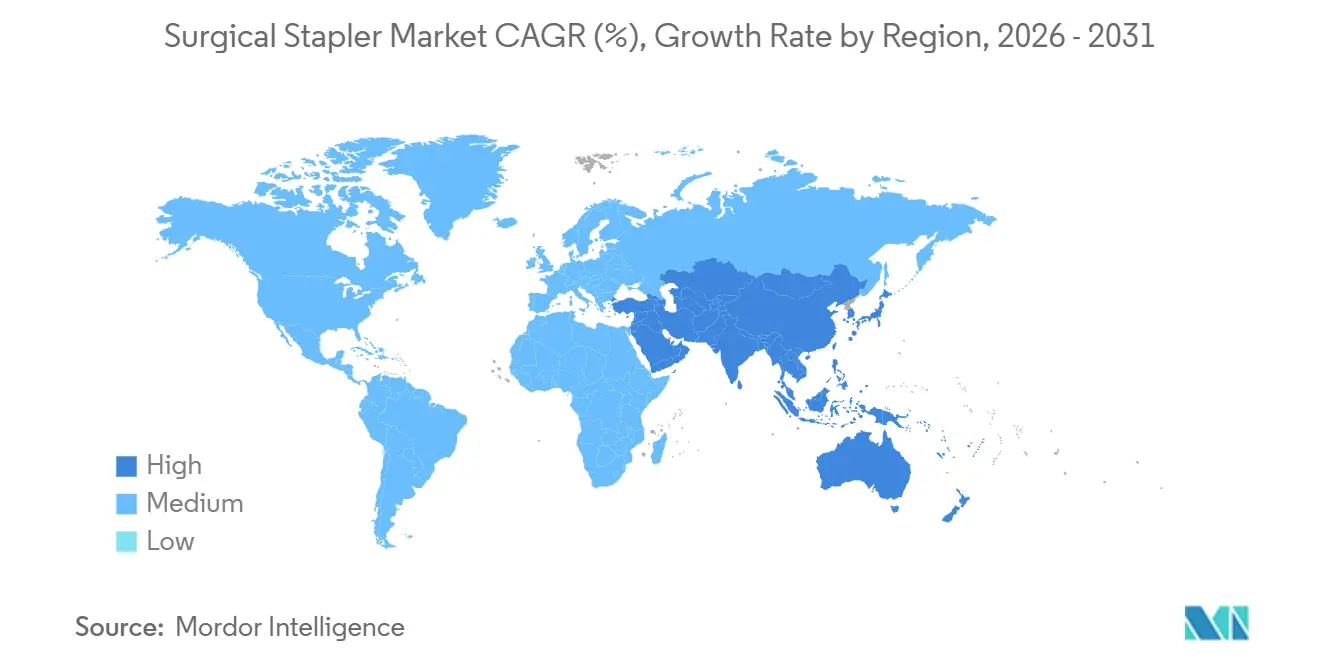

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

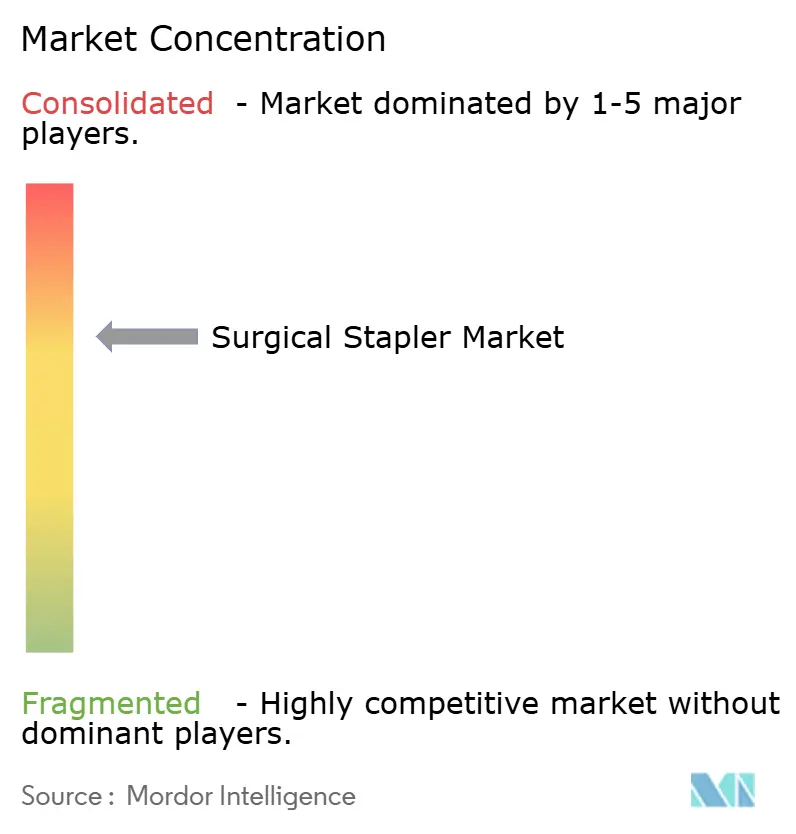

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Stapler Market Analysis by Mordor Intelligence

The Surgical Stapler Market size was valued at USD 6.24 billion in 2025 and is estimated to grow from USD 6.68 billion in 2026 to reach USD 9.43 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031).

Consistent double-digit procedure growth on robotic platforms, the conversion of manual devices to powered formats, and real-time tissue-sensing algorithms are the principal engines behind this expansion[1]Investor Relations Team, “Annual Report 2025,” INTUITIVE.COM. Hospitals are consolidating purchases through multi-year capital contracts that bundle staplers with robotic consoles, while ambulatory surgical centers (ASCs) are absorbing high-volume orthopedic and gastrointestinal cases previously handled in inpatient settings. Environmental, social, and governance (ESG) mandates are reshaping procurement, pulling reusable handle systems into competitive tenders even as infection-control teams defend disposable workflows. Real-time audit logs generated by sensor-rich staplers are lowering litigation risk in high-liability regions, reinforcing the value proposition of intelligence over mechanics. The surgical stapler market, therefore, rewards vendors that combine device performance with data traceability and sustainability credentials.

Key Report Takeaways

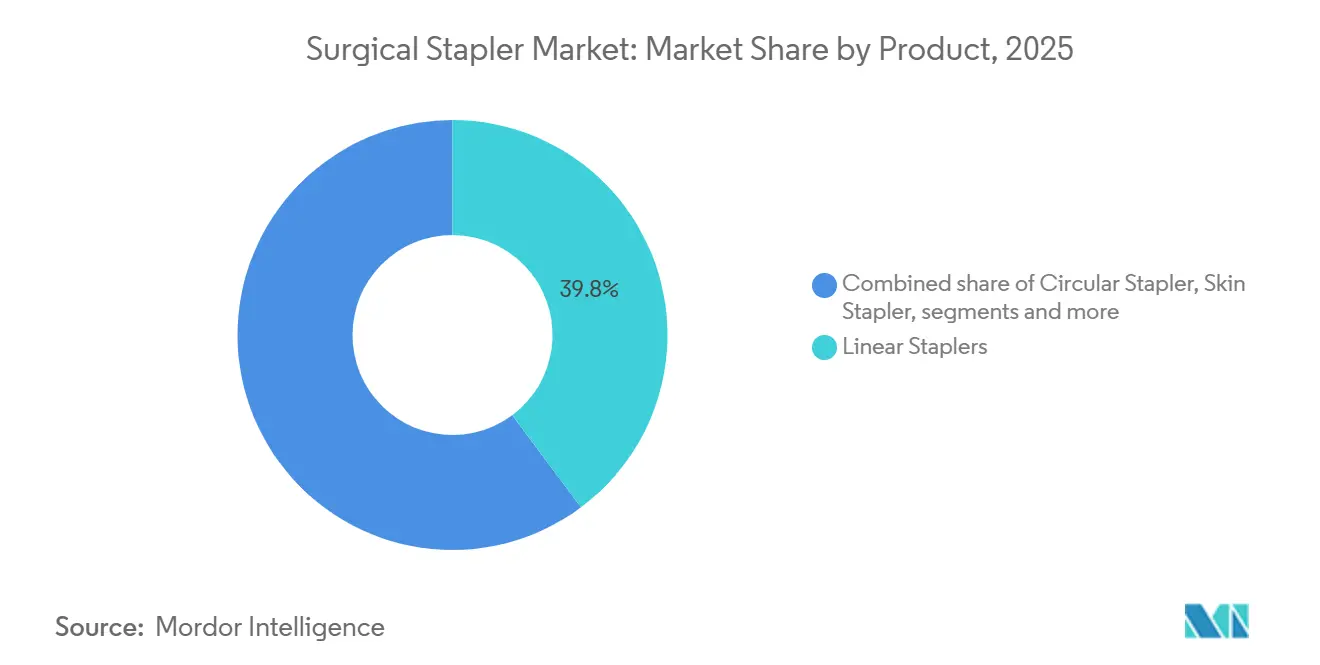

- By product, linear staplers led with 39.8% revenue share in 2025; laparoscopic staplers are forecast to expand at a 8.82% CAGR through 2031.

- By mechanism, manual staplers held 63.2% of the surgical stapler market share in 2025, while powered systems are advancing at a 7.44% CAGR through 2031.

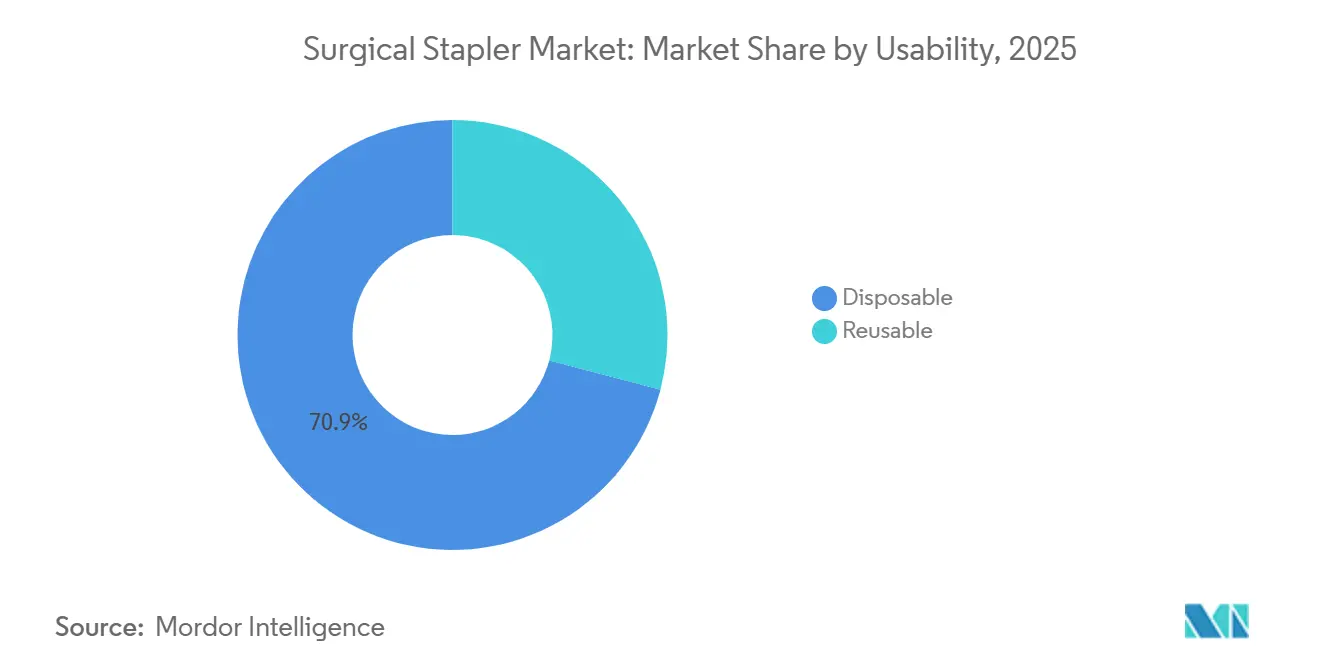

- By usability, disposable cartridges accounted for 70.9% of the surgical stapler market size in 2025, and growing at a 9.12% CAGR through 2031.

- By application, abdominal and gastrointestinal surgery led with 40.1% revenue share in 2025; orthopedic procedures are forecast to expand at an 8.42% CAGR to 2031.

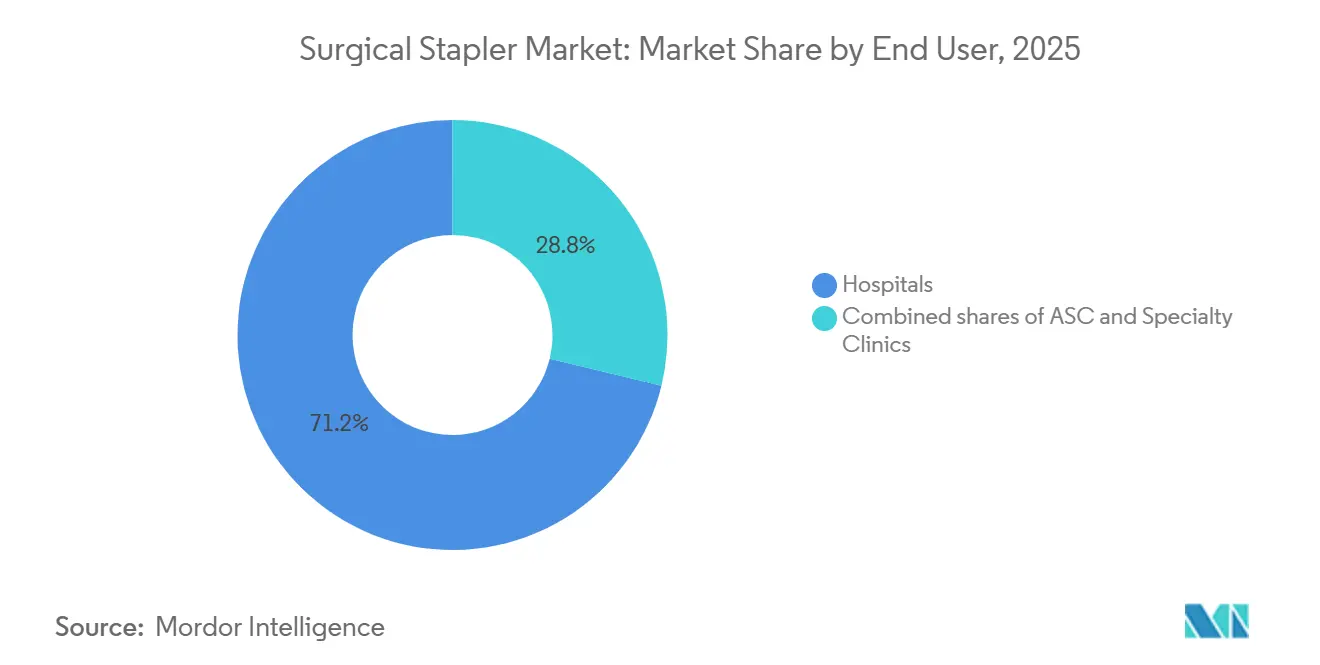

- By end-user, hospitals and clinics controlled 71.2% demand in 2025, whereas ASCs are recording the fastest 8.25% CAGR through 2031.

- By geography, North America commanded a 39.4% share in 2025, but Asia-Pacific is projected to register the highest 8.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Surgical Stapler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration with robotic-assisted surgery platforms | +1.2% | Global, with highest adoption in North America and Western Europe | Medium term (2-4 years) |

| Rapid adoption of powered and reloadable staplers | +1.0% | North America, Europe, and urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Rising preference for minimally-invasive procedures | +1.5% | Global, with accelerated uptake in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Hospital ESG mandates favouring reusable cartridge systems | +0.6% | Europe (NHS net-zero targets), North America (Practice Greenhealth members) | Medium term (2-4 years) |

| AI-driven smart staplers reducing intra-operative error | +0.8% | North America, select European markets with advanced surgical centers | Short term (≤ 2 years) |

| Localized titanium additive-manufacturing cutting logistics cost 30%+ | +0.5% | North America, Germany, Japan (established AM infrastructure) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration With Robotic-Assisted Surgery Platforms

Robotic consoles anchor multi-year purchasing agreements that lock stapler demand into proprietary ecosystems. In April 2025, the SureForm 45 stapler received FDA clearance for exclusive use on da Vinci Xi and X systems, and instruments-and-accessories revenue climbed 19% in 2024 as utilization rose. Hospitals hesitate to introduce third-party staplers because compatibility alerts can void service contracts. Comparable strategies underlie Medtronic’s Hugo platform and Ethicon’s involvement in the Verb collaboration. Regulatory frameworks such as the FDA 510(k) pathway and the EU Medical Device Regulation add high documentation hurdles for every new instrument-platform pairing, reinforcing incumbent advantages. As a result, independent manufacturers face shrinking addressable volume unless they secure robotic partnerships or concentrate on open and laparoscopic niches.

Rapid Adoption of Powered and Reloadable Staplers

Powered devices bring motorized articulation that delivers uniform compression over thick or heterogeneous tissue. Ethicon’s Echelon 4000, introduced in June 2025, shortened firing time significantly in sleeve-gastrectomy trials and lowered incomplete-staple events. Reloadable handles reduce per-case consumable cost significantly and support sustainability targets by limiting full-instrument disposal. Yet strict cleaning validation is mandatory to avoid biofilm accumulation, which deters smaller ASCs without automated reprocessing lines. European chemical-substances disclosure rules further raise compliance overhead, helping large manufacturers that already run comprehensive quality-management systems.

Rising Preference for Minimally Invasive Procedures

Laparoscopic and thoracoscopic approaches shorten inpatient stays and align with value-based reimbursement. CMS added outpatient total knee arthroplasty in 2024, and ASC knee cases almost quadrupled from 2020 to 2023. Compact, articulating staplers such as the 8 mm SureForm 30, cleared in 2024, allow colorectal resections through smaller ports and curb abdominal-wall trauma. Government-funded training programs in Asia and Latin America are accelerating laparoscopic adoption, although domestic price competition there can erode margins. As patient expectations tilt toward smaller scars and faster recovery, powered staplers offering precise articulation gain an adoption edge.

Hospital ESG Mandates Favoring Reusable Cartridge Systems

The United Kingdom National Health Service aims for net-zero emissions by 2040 and operating-room waste forms as much as 30% of total hospital refuse [2]Sustainability Office, “Delivering a Net Zero NHS,” ENGLAND.NHS.UK . Waste reduction is a major focus for United States hospitals, with high percentages of hospitals prioritizing it alongside energy, sustainable products, and operational costs as part of broader sustainability efforts. Reusable handles with disposable cutting cartridges can trim carbon footprints significantly, but strictly validated cleaning cycles are required to achieve a sterility assurance level of 10⁻⁶. Capital outlays for automated washer-disinfectors and real-time monitoring, therefore, influence adoption speed, favoring major academic centers over smaller sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Next-gen bio-adhesive sealants reducing mechanical stapling need | -0.7% | Global, with higher substitution in pediatric and plastic surgery segments | Medium term (2-4 years) |

| Post-operative leakage and infection litigations | -0.5% | North America (high litigation environment), Europe (product-liability directives) | Short term (≤ 2 years) |

| Concentrated titanium supply volatility | -0.4% | Global, with acute impact on manufacturers without diversified sourcing | Long term (≥ 4 years) |

| Centralized procurement in China and EU slashing ASPs 40%+ | -1.0% | China (VBP policies), Europe (joint procurement frameworks) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Next-Gen Bio-Adhesive Sealants Reducing Mechanical Stapling Need

Fibrin sealants, cyanoacrylate glues, and alginate patches are gaining share where tissue tension is low and cosmetic outcomes are paramount. Flexible polymerization accommodates organ motion during lung resections and bowel anastomoses. Clinical trials show cost per procedure can be 30% lower than powered staplers once reprocessing and waste disposal are included. Nonetheless, adhesives lack the tensile strength required for high-pressure closures in bariatric or esophageal surgery. Regulatory pathways vary: the FDA classifies most internal adhesives as Class III devices demanding premarket approval, while European agencies sometimes process them as medicinal products, complicating multinational launches.

Concentrated Titanium Supply Volatility

Titanium sponge capacity is concentrated in a few countries, and the United States has relied entirely on imports since 2020 [3]Mineral Resources Program, “Titanium Mineral Commodity Summary 2024,” USGS.GOV. Spot prices rose nearly 22% between 2023 and 2024, squeezing margins for firms without long-term contracts. High-purity Ti-6Al-4V alloy must meet ASTM F136 standards, and any contamination can hasten in-vivo corrosion, forcing rigorous lot testing. Vertical integration and additive manufacturing relieve some exposure but do not eliminate dependence on upstream sponge supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Laparoscopic Staplers Extend Reach Into Complex Cases

The laparoscopic segment is projected to advance at 8.82% CAGR, eclipsing linear devices that nonetheless maintained 39.8% share in 2025. Intuitive Surgical’s 8 mm SureForm 30 brings colorectal resections through smaller ports, easing recovery times. Circular staplers, critical for end-to-end anastomoses, incorporate adaptive firing to shrink leak rates by 15-20%. Skin staplers face substitution by tissue adhesives that improve cosmesis in elective cases. Penetration of laparoscopic staplers into thoracic and bariatric indications positions this category as the largest contributor to incremental surgical stapler market revenue through 2031.

Low-acuity appendectomy and hernia repairs sustain demand for cost-sensitive linear devices in emerging nations. Yet where robotic consoles dominate, proprietary laparoscopic staplers lock hospitals into closed consumable ecosystems. The surgical stapler market size for laparoscopic systems is expected to approach USD 4 billion by 2031 as reimbursement favors minimally invasive approaches.

By Mechanism: Precision Drives Powered Expansion

Powered systems are projected to generate a 7.44% CAGR through 2031, outpacing the overall surgical stapler market. Manual units still represented 63.2% of the market in 2025 because their lower purchase cost aligns with budget-constrained facilities. Powered devices such as Echelon 4000 feature motorized articulation that keeps compression uniform in tissue exceeding 15 mm thickness. The surgical stapler market share for manual models will erode as litigation concerns intensify; the FDA recorded thousands of misfire complaints attributable to variable hand force. Yet emerging economies that rely on capital-light acquisition strategies will maintain manual demand.

Robotic ecosystems amplify powered uptake. Intuitive Surgical’s SureForm 45 integrates exclusively with da Vinci systems, illustrating how platform bundling anchors consumable sales. Start-ups lacking direct console access must therefore position manual or semi-powered lines where hospitals value cost savings over incremental precision. The surgical stapler industry continues to monitor ISO 13485 usability requirements, which raise entry thresholds for newcomers.

By Usability: Disposable Leadership Faces Sustainability Questions

Disposable cartridges commanded 70.9% of 2025 revenue, confirming their dominance in infection-control protocols. This segment of the surgical stapler market will still advance at a 9.12% CAGR through 2031 as ASCs prefer ready-to-use kits that minimize turnaround time. Reusable handles with single-use cutting tips, however, cut waste up to 80% and reduce per-procedure spend by roughly 25% once sterilization is standardized, aligning with NHS and Practice Greenhealth targets.

Adoption speed hinges on sterile-processing infrastructure. Large academic centers can validate automated washers, while smaller community hospitals and stand-alone ASC chains often lack capital for new equipment. The EU Single-Use Plastics Directive and the SCIP database oblige manufacturers to disclose chemical hazards, bolstering demand for modular hybrid systems that decouple metallic handles from polymer cartridges. Vendors such as Purple Surgical and Grena are exploiting this gap with scalable cartridge programs that satisfy both ESG and infection-control criteria.

By Application: Orthopedic Growth Outpaces Abdominal Core

Abdominal and gastrointestinal surgery accounted for 40.1% of the 2025 surgical stapler market size, reflecting entrenched bariatric, colorectal, and oncologic procedures. Orthopedic and trauma indications, however, will register an 8.42% CAGR through 2031, the fastest in the mix. Bioabsorbable staples now anchor ACL reconstruction, rotator cuff repair, and meniscal fixes, eliminating secondary removal surgeries and appealing to active patients.

Powered staplers tailored for dense cortical bone reduce intra-operative time compared with screws, and sports-medicine case volumes are climbing alongside youth-athletics participation. Meanwhile, sleeve-gastrectomy volumes softened in 2024 as pharmacologic weight-loss therapies entered mainstream reimbursement, tempering abdominal growth. Cardiac and thoracic surgeons continue to specify powered articulating heads for lobectomies and bypass grafting, given the catastrophic consequences of incomplete staple lines. Pediatric and plastic surgeons increasingly substitute bio-adhesive sealants in low-tension closures, further diversifying application-level demand.

By End-User: ASC Migration Alters Demand Centers

Hospitals retained 71.2% purchase share in 2025, yet the fastest 8.25% CAGR resides in ASCs as payers relocate orthopedic, spine, and gastrointestinal cases to lower-cost outpatient settings. Disposable devices dominate ASC preference because of limited reprocessing capacity and high case turnover privilege single-use convenience. Robotic-ready staplers remain concentrated in tertiary hospitals, but smaller articulated manual heads see uptake in high-volume specialty centers for bariatrics and colorectal surgery.

Specialty clinics that rely on consumer self-pay models prioritize powered staplers with embedded sensors to limit revision risk. ESG imperatives are influencing hospital procurement committees, yet infection-control officers still champion disposables for high-acuity oncology resections. The FDA’s Unique Device Identification framework tightens traceability rules across all sites, putting administrative strain on stand-alone centers but improving recall responsiveness.

Geography Analysis

North America maintained a 39.4% share in 2025 through a large installed robotic base, premium pricing on powered devices, and well-funded malpractice coverage that rewards sensor-rich systems. The expansion of outpatient knee replacement eligibility in 2024 is shifting volumes to ASCs, compressing inpatient stapler spend but unlocking new disposable demand. Canada’s single-payer negotiations and Mexico’s medical-tourism niche create divergent sub-regional price points.

Asia-Pacific is projected to post the highest 8.31% CAGR to 2031. China hosts more than 100 domestic robotic-surgery manufacturers, and provincial tenders have reduced device pricing steeply. Local producers like Meril Life Sciences and Grena are leveraging cost advantages to gain share, forcing multinationals to localize production or cede volume. Japan’s regulator subjects new staplers to lengthy clinical audits, moderating near-term growth but protecting established suppliers. India’s dual structure of urban corporate hospitals and rural clinics results in simultaneous demand for powered and manual units.

Europe combines stringent ESG directives with aggressive price consolidation. The EU Medical Device Regulation enforces post-market surveillance that elevates compliance costs, while joint procurement initiatives aggregate buying power and pressure margins. Germany’s diagnosis-related-group system values time-saving powered staplers, whereas U.K. hospitals weigh carbon-footprint metrics heavily in tender scoring. The Middle East and Africa remain early-stage, although Gulf Cooperation Council states fund premium robotic programs aimed at medical tourists. South America shows polarized adoption: public hospitals favor manual devices to manage budgets, while private institutions in Brazil and Chile introduce powered articulating heads for oncology and bariatric procedures.

Competitive Landscape

Johnson & Johnson’s Ethicon, Medtronic, and Intuitive Surgical collectively hold a commanding presence in the surgical stapler market through closed robotic ecosystems, extensive patent portfolios, and service contracts bundling instruments with consoles. Ethicon’s Echelon 4000 and Medtronic’s Signia Circular Stapler both debuted in 2025 with adaptive-firing algorithms that modulate compression in real time, addressing leak-prevention and reducing operating-room time. Intuitive Surgical’s SureForm series remains exclusively compatible with da Vinci platforms, insulating the company from price competition yet concentrating purchasing power in high-volume robotic centers.

Mid-tier players such as B. Braun, Teleflex, and ConMed compete on sustainability features, modularity, and smoke-evacuation integration. Purple Surgical, Lexington Medical, and Reach Surgical focus on reusable handles and single-port laparoscopy, aiming at hospitals constrained by ESG targets. Chinese and Indian entrants leverage local manufacturing to undercut global pricing by 40% to 50%, aided by government incentives favoring domestic suppliers. Bio-adhesive innovators are expanding the competitive set by offering alternatives to mechanical fastening in select procedures.

Technological roadmaps emphasize AI-enabled feedback loops, bioabsorbable materials, and miniaturization for pediatric care. ISO 13485 and FDA 510(k) compliance impose extensive usability and biocompatibility testing that can extend time-to-market for start-ups. Strategic partnerships have proliferated: Johnson & Johnson created a joint venture with MicroPort in 2024 for China, and Stryker’s 2025 investment in titanium additive manufacturing secures supply resilience while trimming logistics costs.

Surgical Stapler Industry Leaders

B. Braun Melsungen AG

ConMed Corporation

Intuitive Surgical Inc.

Johnson & Johnson Services, Inc.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Medtronic launched the Signia Circular Stapler with Adaptive Firing technology, integrating real-time tissue-impedance sensors that cut leak rates by up to 20% in colorectal resections.

- June 2025: Ethicon unveiled the Echelon 4000 powered stapler with motorized articulation that reduces firing time 30% compared with manual predecessors

- April 2025: Intuitive Surgical secured FDA clearance for the SP SureForm 45 stapler for use with the da Vinci SP surgical system in thoracic, colorectal, and urologic procedures.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical stapler market as the total annual sales revenue generated by disposable and reusable manual or powered stapling instruments, together with their reload cartridges, that are used intra-operatively for tissue approximation or transection across open, laparoscopic, and robotic procedures worldwide.

Scope exclusion: ancillary wound-closure adhesives, sutures, and clip appliers are excluded.

Segmentation Overview

- By Product

- Linear Stapler

- Circular Stapler

- Laparoscopic (Endoscopic) Staplers

- Skin Stapler

- By Mechanism

- Manual

- Powered

- By Usability

- Disposable

- Re-usable

- By Application

- Abdominal & Gastrointestinal Surgery

- Bariatric & Metabolic Surgery

- Obstetrics & Gynecology

- Cardiac & Thoracic Surgery

- Orthopedic & Trauma

- Other Surgical Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed gastrointestinal surgeons, peri-operative nurses, and supply-chain managers in North America, Europe, and Asia to verify average selling prices, reload-per-case ratios, power-stapler penetration, and emerging single-port robotic preferences. These discussions filled data gaps and refined our working assumptions before final triangulation.

Desk Research

We began by mapping procedure volumes, import values, and tariff codes from public datasets such as WHO Hospital Care Statistics, UN Comtrade, and the US FDA 510(k) device register, which give hard counts on stapler clearances and trade flows. Country procedure audits from OECD Health Data, bariatric surgery registries, and peer-reviewed journals on stapler misfire incidence helped us gauge adoption ceilings. Supplemental perspectives were drawn from company 10-K filings, investor decks, and D&B Hoovers financial snapshots, while Dow Jones Factiva supplied real-time press on product launches and recalls. The named sources are illustrative; many additional databases and open publications were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

We blended a top-down reconstruction of demand from procedure counts, weighted by stapler usage rates and sterilization cycles, with selective bottom-up supplier roll-ups to validate totals. Key variables in our model include cesarean and bariatric procedure growth, powered unit price erosion, reload utilization per surgery, and hospital capital-budget trends. Forecasts are generated through multivariate regression that links those drivers to historic sales, and the equation is stress-tested under conservative, base, and accelerated care-backlog scenarios that our experts endorsed. Bottom-up gaps, where distributor data were thin, were bridged using median ASP × volume benchmarks from sampled facilities.

Data Validation & Update Cycle

Every intermediate output passes a two-step analyst peer review, followed by anomaly checks against import spikes, FDA recall notices, and quarterly earnings. We refresh models annually, but a material recall or reimbursement change triggers an interim update, ensuring clients always access the latest view.

Why Mordor's Surgical Stapler Baseline Remains the Trusted Benchmark

Published estimates differ because firms choose unequal product mixes, apply distinct ASP ladders, and refresh at varied cadences. Our disciplined scope, yearly refresh, and transparent variable links keep our figure a dependable decision anchor. Key gap drivers include whether reloads are bundled with handpieces, how power-stapler premiums are modeled, currency conversion dates, and the aggressiveness of post-pandemic backlog assumptions, all of which we align to current-year audited evidence before sign-off.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.24 B (2025) | Mordor Intelligence | - |

| USD 5.15 B (2024) | Global Consultancy A | Excludes reload revenue and applies static USD 2023 exchange |

| USD 5.30 B (2023) | Industry Journal B | Uses historic manual-only ASP, no robotic uptake factor |

| USD 5.62 B (2024) | Regional Consultancy C | Limits scope to top five regions and projects linear growth |

Taken together, the comparison shows that once reloads, robotics, and fresh currency baselines are incorporated, Mordor's balanced, traceable model offers the clearest and most reproducible view of the market today.

Key Questions Answered in the Report

What is the expected value of the surgical stapler market by 2031?

The surgical stapler market is forecast to reach USD 9.43 billion by 2031, growing at a 7.15% CAGR.

Which product segment is growing fastest?

Laparoscopic staplers are advancing at a 7.1% CAGR as minimally-invasive techniques expand.

Why are ambulatory surgical centers important for stapler demand?

ASCs are shifting high-volume orthopedic and gastrointestinal procedures out of hospitals, driving an 8.25% CAGR for staplers used in outpatient settings.

How are ESG goals influencing stapler procurement?

Hospitals pursuing waste-reduction targets favor reusable handle systems that cut carbon footprints up to 80% versus single-use devices.

What technologies help reduce stapler-related litigation risk?

AI-enabled staplers with real-time tissue sensing create structured audit logs that document firing conditions and support post-operative reviews.

Which region will see the highest growth?

Asia-Pacific is projected to post the fastest 8.31% CAGR, propelled by aging demographics and an expanding local manufacturing base.

Page last updated on: