Atrial Fibrillation Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

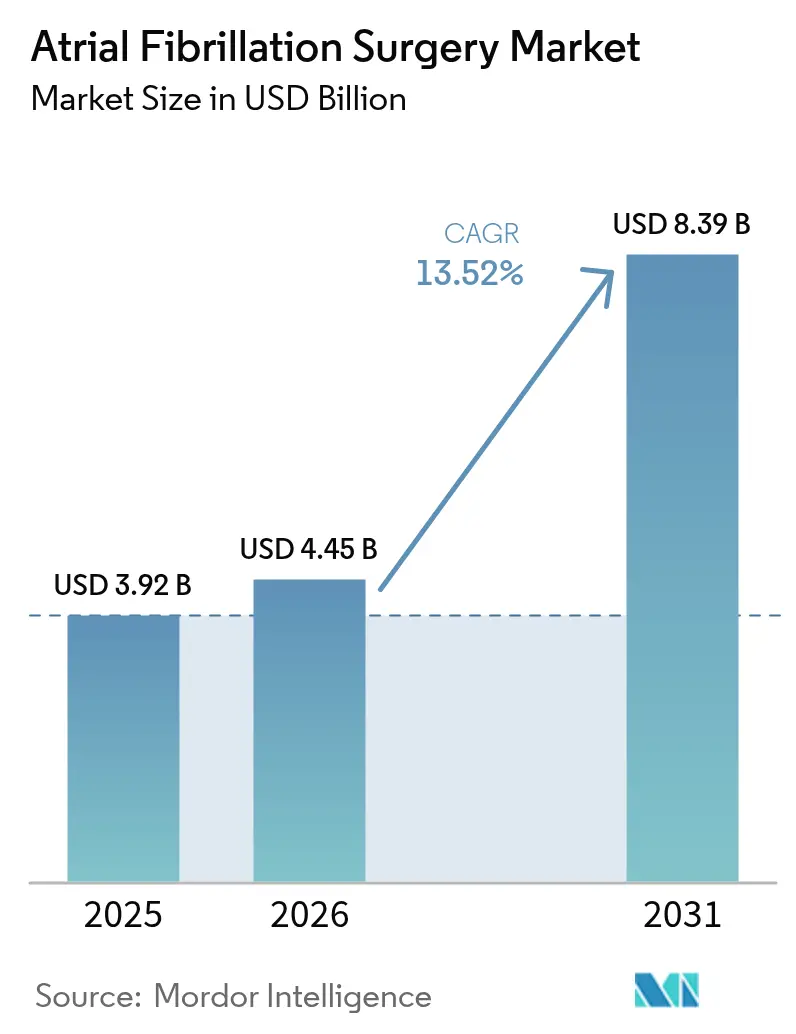

| Market Size (2026) | USD 4.45 Billion |

| Market Size (2031) | USD 8.39 Billion |

| Growth Rate (2026 - 2031) | 13.52% CAGR |

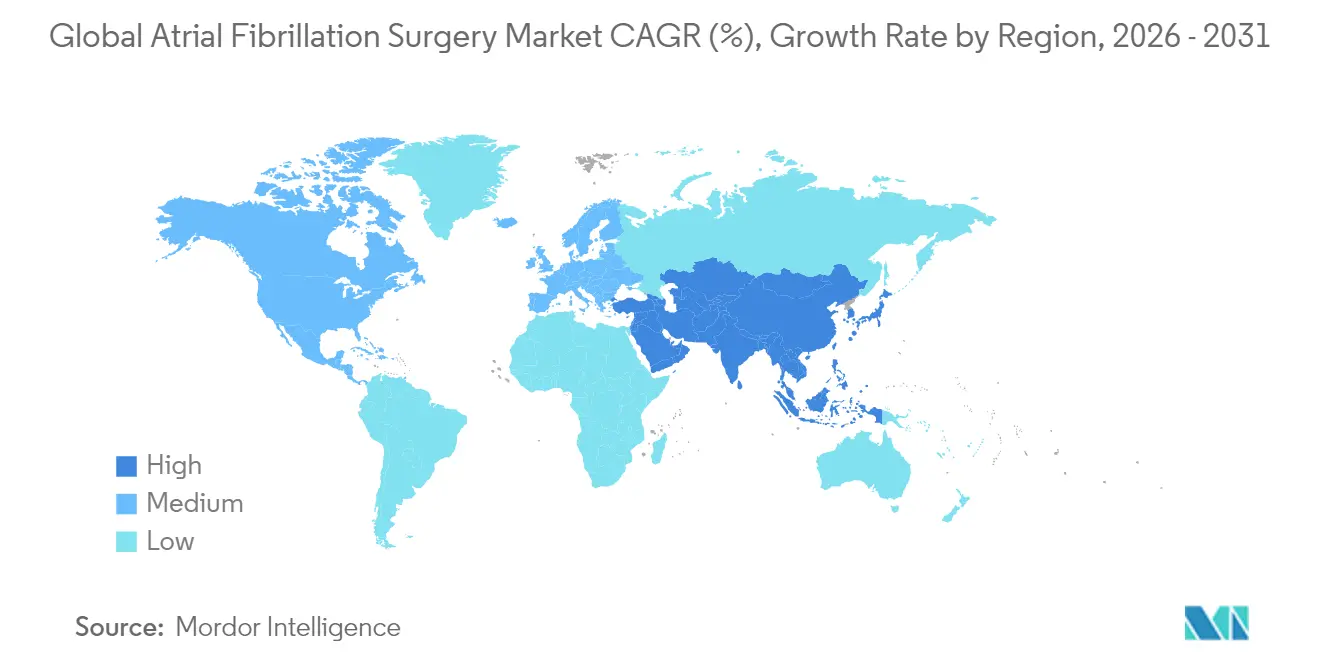

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atrial Fibrillation Surgery Market Analysis by Mordor Intelligence

The atrial fibrillation surgery market size was valued at USD 3.92 billion in 2025 and estimated to grow from USD 4.45 billion in 2026 to reach USD 8.39 billion by 2031, at a CAGR of 13.52% during the forecast period (2026-2031). Rising procedure volumes track sharply higher atrial fibrillation (AF) prevalence, wider availability of elective electrophysiology programs, and rapid migration toward pulsed-field ablation (PFA) systems that shorten procedure times while improving safety. Hospitals keep investing in integrated electrophysiology-hybrid suites even as ambulatory surgical centers (ASCs) draw case volumes through site-neutral payment rules and same-day discharge protocols. Capital flows into innovations such as catheter technology, mapping software, and AI-guided workflow analytics continue to reshape competitive positioning. Meanwhile, reimbursement revisions in the United States and Europe now recognize the complexity of combined left-atrial appendage closure and ablation, supporting revenue expansion for providers.

Key Report Takeaways

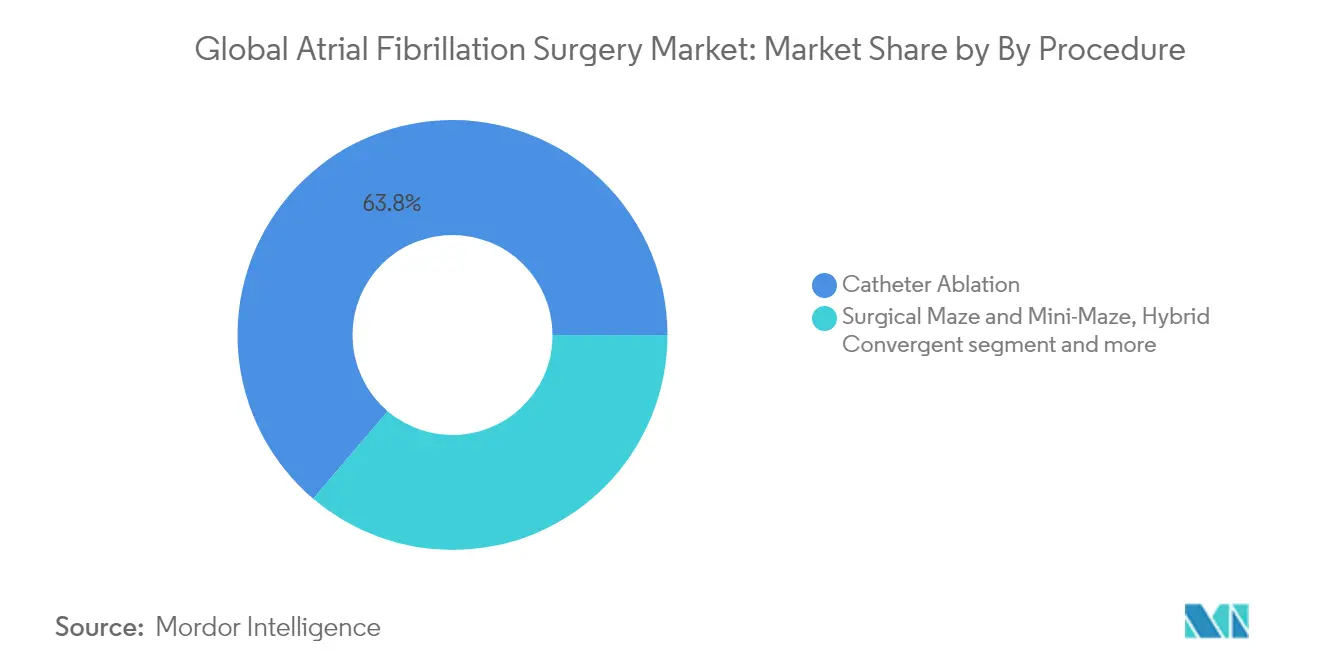

- By procedure, catheter ablation led with 63.78% revenue share in 2025, whereas pulsed-field ablation posts the strongest 14.31% CAGR through 2031.

- By product type, catheter ablation devices accounted for 57.92% of the atrial fibrillation surgery market size in 2025, while PFA systems expanded at a leading 15.02% CAGR to 2031.

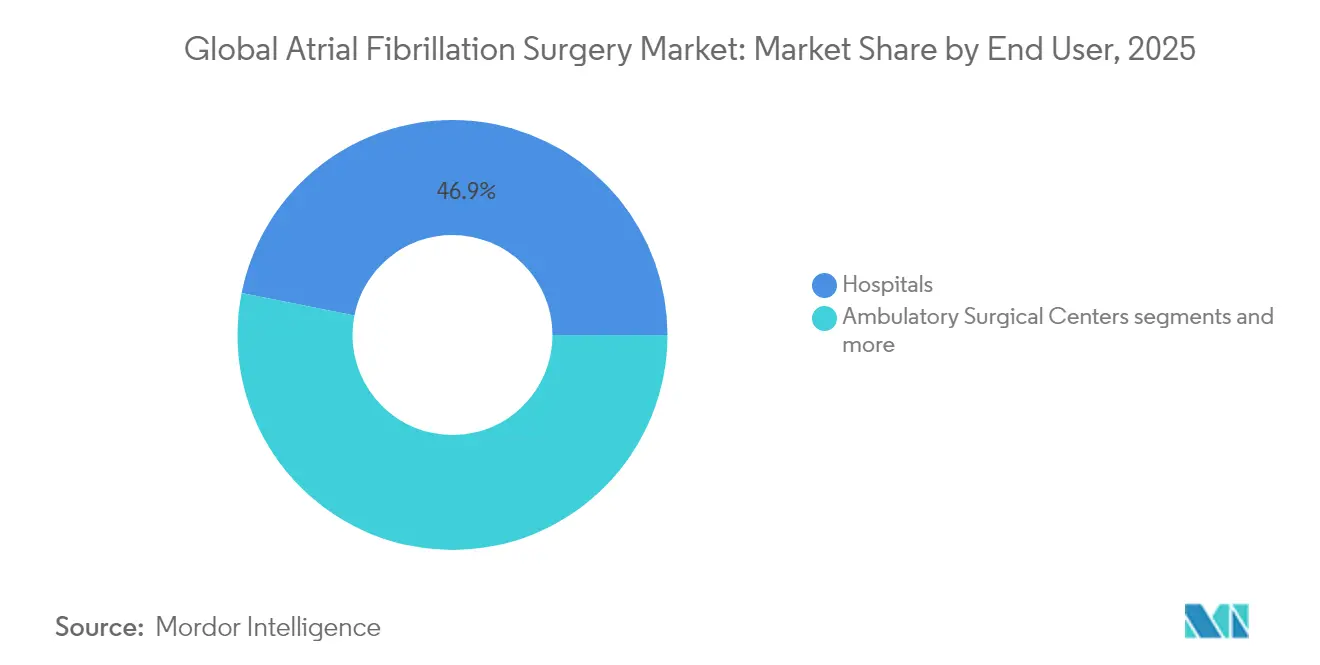

- By end user, hospitals accounted for 46.88% of the 2025 revenue; ASCs represent the fastest-growing setting, with a 15.72% CAGR through 2031.

- By geography, North America captured 38.86% of the 2025 revenue; the Asia-Pacific region delivered the highest 16.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Atrial Fibrillation Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & AF prevalence surge | +3.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rising adoption of minimally-invasive catheter ablation | +2.8% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion of outpatient EP labs & ambulatory centers | +2.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Hospital cap-ex cycle toward single-shot PFA systems | +1.9% | North America & EU core markets | Short term (≤ 2 years) |

| Reimbursement upgrades for same-day discharge AF surgery | +1.6% | US Medicare markets, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing population & AF prevalence surge

Lifetime AF risk climbed from 24.2% for Danes born 2000–2010 to 30.9% for those born 2011–2022, signaling a broad expansion of the treatable patient pool. US prevalence estimates now exceed prior forecasts as remote monitoring uncovers asymptomatic episodes. This demographic pressure intersects with improving detection technologies to lift referral volumes for rhythm-control procedures. Emerging economies mirror the trend; Korean national data reveal similar age-linked incidence curves. Health-system planners therefore frame AF ablation capacity expansion as a long-tail volume growth opportunity.

Rising adoption of minimally invasive catheter ablation

A meta-analysis of 22 randomized trials covering 6,400 patients confirmed that ablation halves AF relapse risk relative to medical therapy and cuts all-cause hospitalization by 43%. Endorsement of same-day discharge by US specialty societies accelerated uptake; Canadian centers reported 79.2% same-day release with negligible readmissions. Cumulative evidence positions ablation earlier in the treatment algorithm, making first-line rhythm control a mainstream option.

Hospital cap-ex cycle toward single-shot PFA systems

Hospitals allocate fresh budgets to PFA after FDA approvals of PulseSelect, VARIPULSE, and Affera systems demonstrated zero esophageal complications in pivotal trials. Administrators highlight predictable learning curves and <90-minute case times that translate to higher lab productivity.

Reimbursement upgrades for same-day discharge AF surgery

The US Centers for Medicare & Medicaid Services created MS-DRG 317 in 2025 for concomitant ablation and appendage closure, boosting average facility payments and validating the clinical resource mix in contemporary AF care[1]Source: Journal of the American College of Cardiology, “Same-Day Discharge After AF Ablation,” jacc.org .

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive hybrid-OR build-outs | -1.8% | Global, particularly emerging markets | Medium term (2-4 years) |

| Shortage of EP-trained surgeons | -2.1% | Global, acute in rural and emerging regions | Long term (≥ 4 years) |

| Long-term durability concerns for PFA | -1.4% | Global, with regulatory focus in US & EU | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Capital-intensive hybrid-OR build-outs

Turn-key electrophysiology–surgical suites cost USD 2–5 million per room, straining rural or small-system budgets and slowing diffusion of advanced energy platforms outside tier-one centers.

Shortage of EP-trained surgeons

Electrophysiology fellowships remain capped relative to demand, and persistent urban clustering of specialists limits access in secondary markets. Workforce gaps complicate adoption of new tools such as dual-energy catheters that require dedicated training modules[2]Source: Johns Hopkins Medicine, “Electrophysiology Training Pathways,” hopkinsmedicine.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure: PFA disrupts thermal dominance

Catheter ablation retained 63.78% revenue in 2025, anchoring the atrial fibrillation surgery market even as pulsed-field ablation logs a breakout 14.31% CAGR to 2031. The atrial fibrillation surgery market size for PFA-based procedures is therefore projected to almost triple within the decade. Balloon-based single-shot systems routinely isolate all pulmonary veins in under 20 minutes, while the MANIFEST-17K registry documented zero esophageal injuries versus historic 1-3% for thermal energy. Clinical validation, such as the ADVENT trial, confirmed non-inferiority on efficacy and superiority on safety against cryoablation, while procedure duration declined by 35%. Although the NEMESIS-PFA registry flagged elevated troponin release, ongoing waveform optimization aims to minimize myocardial stun.

Persistent AF remains challenging; hybrid maze or convergent approaches combine epicardial and endocardial lines to raise single-procedure success, but volumes stay niche. Surgical maze is anchored to valve or coronary bypass cases that already require sternotomy, keeping its share stable. Long-term, industry analysts expect PFA to capture incremental share from both radiofrequency and cryoballoon techniques as operator confidence strengthens and next-generation catheters expand lesion sets beyond pulmonary veins.

By Product Type: Single-shot systems drive innovation

Catheter ablation devices commanded 57.92% of revenue in 2025, yet PFA consoles and catheters post the field-leading 15.02% CAGR on the back of successful US and EU launches. Integrated mapping-plus-ablation platforms such as Medtronic Affera fuse high-density electroanatomical mapping with dual-energy delivery in one catheter, compressing capital costs and simplifying inventories. AI-enhanced mapping from Volta Medical improved durable freedom-from-AF to 88% in the TAILORED-AF study compared with 70% for standard pulmonary vein isolation tctmd.com. Ancillary disposables—including vascular closure, steerable sheaths, and hemostasis valves—benefit from volume growth but face hospital value committee price audits that crimp margin expansion.

PFA technology advantages have sparked new entrants: Kardium’s USD 104 million financing will accelerate Globe mapping and ablation commercialization. Field Medical’s FieldForce platform, backed by USD 40 million Series A, secured US FDA Breakthrough Device designation to explore ventricular arrhythmia use cases. Competitive intensity therefore shifts toward waveform IP, catheter ergonomics, and integrated software rather than commodity pricing.

By End User: ASCs challenge hospital dominance

Hospitals still held 46.88% revenue in 2025 thanks to broad payer contracts and intensive care backup. Yet ASCs register the highest 15.72% CAGR as payers favor lower-cost sites and clinicians embrace outpatient models. The atrial fibrillation surgery market share for ASCs is expected to rise to the mid-30% range by 2031 as Medicare adds complexity adjustments that reward advanced EP procedures outside the hospital. Private equity-backed groups such as Cardiovascular Associates of America now operate more than 149 locations, funneling volume into standardized care pathways that boost device pull-through. Hybrid ownership—hospital plus physician—emerges as a risk-sharing model that preserves inpatient referral streams while capturing ambulatory upside.

Cardiac catheterization laboratories within hospitals bridge the settings gap by offering same-day discharge for low-risk cases, though negative Medicare physician fee schedule updates reduce professional margin. Specialty clinics focusing exclusively on electrophysiology gain visibility in metropolitan hubs where patient density justifies dedicated infrastructure.

Geography Analysis

North America generated 38.86% of 2025 revenue and remains the benchmark for early adoption as payer coverage spans both thermal and pulsed-field technologies. FDA approvals of PulseSelect and VARIPULSE triggered a fresh equipment replacement cycle, while CMS creation of MS-DRG 317 improved facility reimbursement for combined ablation and appendage closure. Market tailwinds include robust ASC roll-outs across Texas, Florida, and California plus capital access that funds hybrid-suite builds. Headwinds are modest: a 2.93% cut in the 2025 Medicare Physician Fee Schedule trims professional income, but throughput gains offset revenue erosion.

Europe positions as the second-largest regional cluster with strong clinical-trial leadership and structured training programs. CE Mark clearance for Abbott’s Volt PFA system in March 2025 unlocked broad commercial use, and the MANIFEST-17K study—largely European—cemented safety credentials. Germany, France, and the United Kingdom anchor procedural volume, while Eastern Europe accelerates from a low base. The United Kingdom’s National Institute for Health and Care Excellence published an analysis indicating that PFA lowers average procedure costs by GBP 743 relative to cryoablation, supporting adoption inside the National Health Service.

Asia-Pacific is the growth engine with a forecast 16.58% CAGR to 2031. Japan validated PFA efficacy in the PULSED-AF trial, creating a template for other regulators. China’s Healthy China 2030 agenda prioritizes chronic disease management and domestic device innovation, prompting local start-ups to co-develop PFA catheters with academic hospitals. India’s middle-class expansion and widening insurance penetration diversify referral channels beyond elite private hospitals. South Korea and Australia function as training hubs for Southeast Asian electrophysiologists. Regional constraints include specialist shortages outside tier-one cities and fragmented reimbursement but remain outweighed by demographic drivers and rapid capital deployment into tertiary cardiac centers.

Latin America and the Middle East & Africa contribute smaller shares but show rising interest in single-shot balloons that shorten general-anesthesia time and fit within limited cath-lab schedules. Multinational vendors often bundle training and warranty packages to reduce ownership cost, easing entry barriers in resource-constrained systems.

Competitive Landscape

Thirteen firms account for the lion’s share of global revenue, reflecting moderate concentration. Medtronic, Boston Scientific, Johnson & Johnson’s Biosense Webster, and Abbott collectively control the platform segment. Each competes on differentiated energy source, catheter design, and data integration rather than price cuts. Medtronic’s USD 925 million acquisition of Affera delivered a dual-energy system and expanded mapping IP. Boston Scientific’s Cortex purchase improved lesion characterization and will feed next-generation FARAPULSE algorithms once FDA approves persistent-AF labeling.

Johnson & Johnson leverages CARTO 3’s installed base for rapid VARIPULSE rollout; however, an FDA Class I recall in February 2025 after elevated stroke events forced protocol tweaks. Abbott emphasizes integrated rhythm-management ecosystems, pairing Volt PFA with its HD Grid mapping catheter and AVEIR leadless pacemakers for comprehensive arrhythmia coverage.

Younger entrants focus on white-space opportunities. Kardium’s Globe integrates 122 electrodes on a single balloon for simultaneous mapping and therapy. Field Medical targets ventricular arrhythmias with its FieldForce waveform library. Volta Medical delivers AI pattern-recognition software now under multicenter evaluation. Private equity aggregates downstream delivery through cardiology ASC platforms that lock in device preferences while guaranteeing procedure volumes. Vendor contracting therefore increasingly incorporates data-analytics dashboards, remote case proctoring, and outcome-based rebates.

Looking forward, competitive advantage will hinge on lesion durability data beyond 3 years, integration with imaging-guided navigation, and algorithms that personalize energy dosing based on tissue impedance signatures. Vendors that bridge hardware, software, and training services should capture disproportionate share of the incremental USD 4.58 billion revenue opportunity forecast between 2025 and 2030.

Atrial Fibrillation Surgery Industry Leaders

Boston Scientific Corporation

Medtronic Plc

Biotronik

AtriCure, Inc.

Cardiofocus, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Medtronic wins FDA clearance for OmniaSecure 4.7F defibrillation lead with 100% acute success.

- April 2025: Boston Scientific reports 73.4% freedom from persistent AF in ADVANTAGE AF phase-2 for FARAPULSE.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the atrial fibrillation (AF) surgery market as all revenue generated from catheter-based and open or minimally invasive surgical ablation procedures that intentionally create atrial lesions for rhythm control in diagnosed AF patients. Devices, consumables, mapping and navigation systems, as well as procedure fees billed by hospitals and ambulatory surgical centers are counted once at the point of care.

Scope Exclusions: Pharmacological therapies, wearable monitors, and left atrial appendage closure implants are left outside the sizing scope.

Segmentation Overview

- By Procedure

- Catheter Ablation

- Surgical Maze & Mini-Maze

- Hybrid Convergent

- Pulsed Field Ablation (PFA)

- By Product Type

- Catheter Ablation Devices

- Surgical Ablation Systems

- PFA Systems

- Mapping & Navigation Systems

- Ancillary Accessories

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Cardiac Catheterization Laboratories

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and short surveys with electrophysiologists, cardiothoracic surgeons, hospital procurement heads, and regional reimbursement experts across North America, Europe, and Asia Pacific help us test prevalence assumptions, procedure mix shifts toward pulsed field ablation, and likely ASP compression through 2030 before final model lock.

Desk Research

We begin with a structured scan of freely available tier 1 datasets such as WHO Global Health Estimates, OECD inpatient procedure files, U.S. CMS hospital discharge records, and Eurostat DRG statistics, all of which clarify treated AF incidence and elective ablation volumes. Trade group releases from the American College of Cardiology, Heart Rhythm Society, and Asia Pacific Heart Rhythm Society provide annual catheter mix and success rate benchmarks. Company 10-Ks, investor decks, and FDA approval summaries reveal average selling prices and upcoming technology shifts. Select paid databases, including D&B Hoovers for provider financials and Questel for ablation catheter patent trends, add depth. The sources listed illustrate, not exhaust, the wider set screened and archived by our analysts.

Market Sizing & Forecasting

A top down reconstruction starts with country level AF prevalence, treatment eligibility ratios, and observed ablation penetration. These volumes are multiplied by blended procedure ASPs that embed device, anesthesia, and facility charges, which are then ground checked through selective bottom up roll ups of leading supplier revenue disclosures.

Core variables include annual ablation volumes, single shot PFA adoption rate, catheter ASP trajectories, same day discharge share, reimbursement tariff revisions, and regional operating theater capacity. Forecasts employ multivariate regression with AF prevalence growth, geriatric population expansion, and technology adoption curves as predictors, backed by consensus ranges gathered during primary research. Where bottom up estimates undershoot or overrun by more than five percent, gap filling follows a weighted average of adjacent country proxies and three year moving averages.

Data Validation & Update Cycle

Outputs pass three analyst reviews, anomaly screens against independent procedure counts, and variance checks with quarterly device revenue. Models refresh annually, while material events, major reimbursement change or first in class approval, trigger interim revisions so clients always receive the latest view.

Why Mordor's Atrial Fibrillation Surgery Baseline Warrants Confidence

Published estimates vary because firms select unlike inclusion criteria, price stacks, and refresh rhythms. Device only counts, hospital charge markups, or historical currency fixes often widen the spread.

Key Gap Drivers here include differing treatment setting coverage (some exclude ASCs), omission of mapping system revenue, and straight line growth on outdated RF volumes that ignore rapid PFA uptake, whereas Mordor analysts embed real world mix shifts and updated tariffs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.92 bn (2025) | Mordor Intelligence | - |

| USD 4.68 bn (2025) | Global Consultancy A | Includes wearable monitors and LAAC devices; uses uniform 10% ASP uplift |

| USD 4.16 bn (2024) | Industry Journal B | Excludes ASC procedures; applies static RF share, underweighting PFA growth |

| USD 1.97 bn (2023) | Regional Consultancy C | Older base year and converts at fixed 2019 exchange rates |

Taken together, the comparison shows that when right sized scope, current tech splits, and live currency bases are applied, Mordor Intelligence delivers a balanced, transparent baseline that decision makers can retrace and replicate without hidden multipliers.

Key Questions Answered in the Report

Q1: How big is the atrial fibrillation surgery market today?

A1: The atrial fibrillation surgery market stands at USD 4.45 billion in 2026 and is projected to reach USD 8.39 billion by 2031 at a 13.52% CAGR during 2026-2031.

Q2: Which procedure type is expanding the fastest?

A2: Pulsed-field ablation is the fastest-growing procedure, advancing at 14.31% CAGR through 2031 as zero esophageal complications and shorter case times propel adoption.

Q3: Why are ambulatory surgical centers important for future growth?

A3: ASCs post a 15.72% CAGR through 2031 because site-neutral reimbursement and same-day discharge protocols lower total episode cost without compromising outcomes, shifting volume from hospitals.

Q4: Which region offers the strongest upside?

A4: Asia-Pacific delivers the highest 16.58% CAGR to 2031 due to aging populations, improving electrophysiology capacity, and supportive regulatory pathways such as Japan’s early PFA approvals.

Q5: What technological trend will shape competition most?

A5: Integration of AI-guided mapping and dual-energy catheters will differentiate platforms by boosting durable success rates and trimming procedure times, creating defensible value propositions for vendors.

Page last updated on: