Philippines Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

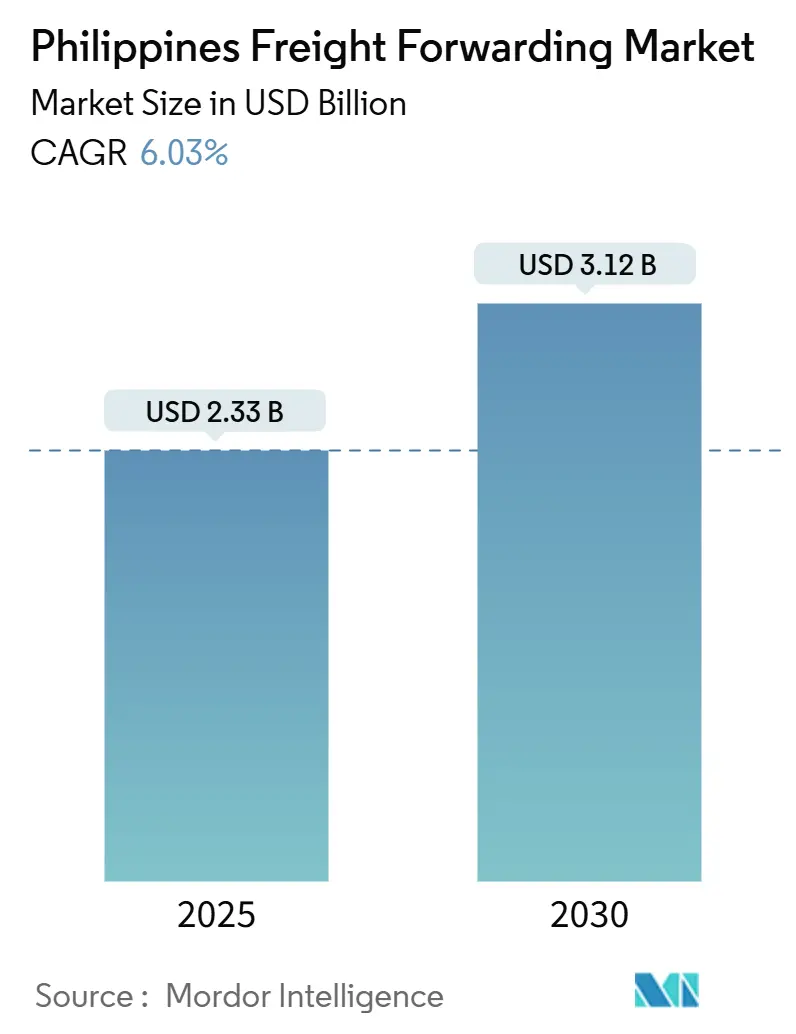

| Market Size (2025) | USD 2.33 Billion |

| Market Size (2030) | USD 3.12 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Freight Forwarding Market Analysis by Mordor Intelligence

The Philippines Freight Forwarding Market size is estimated at USD 2.33 billion in 2025, and is expected to reach USD 3.12 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

Current expansion is anchored in the country’s archipelagic trade flows, strong consumer spending, and ongoing logistics infrastructure upgrades. Sea freight retains scale advantage, but air cargo volumes accelerate as electronic components and e-commerce parcels demand rapid transit. Public spending on ports, airports, and nautical highways steadily improves network capacity, while rising digital adoption pushes shippers toward platform-based booking and real-time visibility solutions. The market also benefits from liberalized foreign-ownership rules that invite fresh capital and global best practices.

Key Report Takeaways

- By mode of transport, sea freight led with a 58.29% share of the Philippines freight forwarding market in 2024; air freight is forecast to expand at a 6.83% CAGR through 2030.

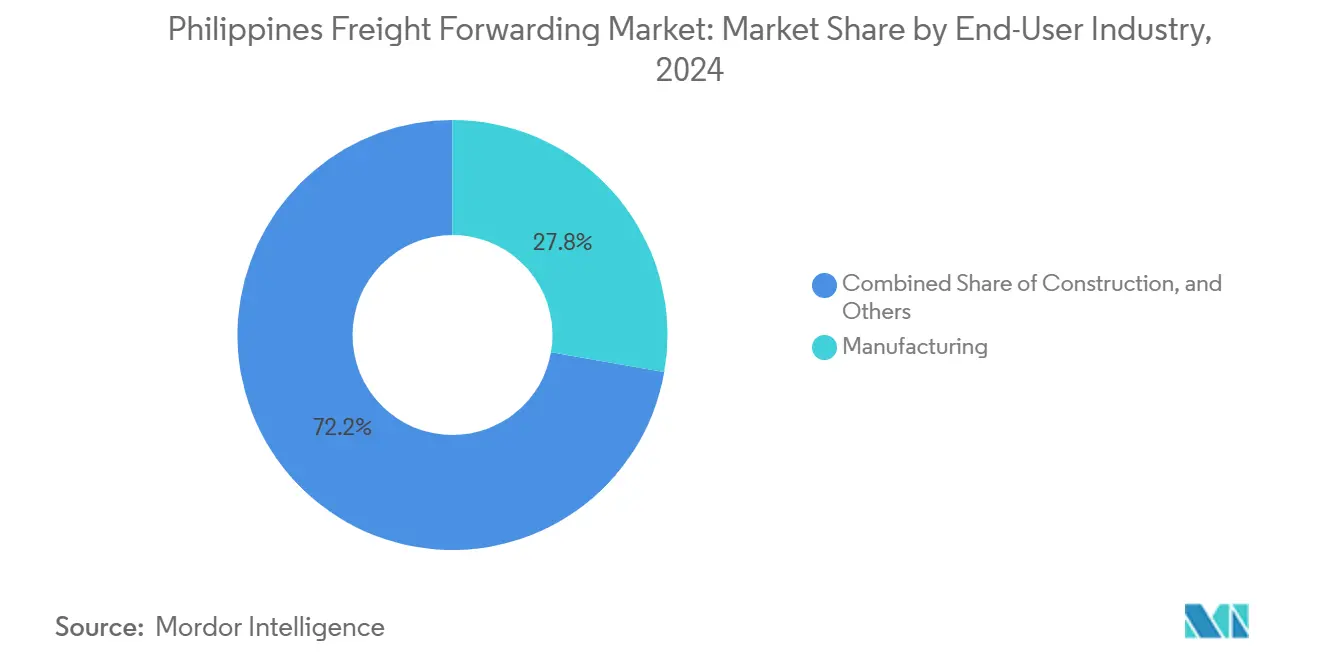

- By end-user, manufacturing accounted for 27.76% of the Philippines freight forwarding market size in 2024, while wholesale and retail trade is advancing at a 6.22% CAGR through 2030.

Philippines Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Build Better More infrastructure program expands port, road, and airport capacity | +1.2% | Nationwide, especially Luzon–Visayas–Mindanao corridors | Medium term (2-4 years) |

| E-commerce boom lifts parcel and express freight demand | +1.8% | Metro Manila, Cebu, Davao with spillover to provinces | Short term (≤ 2 years) |

| ASEAN integration and RCEP implementation foster intra-Asia trade | +0.9% | Major ports and airports | Long term (≥ 4 years) |

| Foreign-ownership liberalization attracts global 3PLs | +0.7% | NCR, CALABARZON, Central Luzon | Medium term (2-4 years) |

| Cross-Border Paperless Trade Framework speeds customs clearance | +0.5% | Principal seaports and airports | Short term (≤ 2 years) |

| Roll-On Roll-Off nautical highways unlock new island corridors | +0.6% | Luzon–Visayas–Mindanao routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Build Better More Infrastructure Program Expands Port, Road, and Airport Capacity

The government’s Build Better More initiative encompasses 198 flagship projects that collectively add substantial freight capacity across ports, highways, and rail links. Inter-modal connectors improve cargo velocity by reducing trans-shipment and dwell times at coastal gateways, while upgrades to nautical highways ease roll-on roll-off operations between the archipelago’s major islands. As new terminals become operational, freight forwarders can negotiate better berthing windows, deploy larger vessels, and shorten door-to-door schedules. Improved hinterland roads also curb truck idling in Metro Manila and decongest key logistics corridors, thereby enhancing asset utilization and driver productivity[1]“Philippines: Tropical Cyclones and Floods Revised Humanitarian Needs and Priorities (Nov 2024 – Apr 2025),” United Nations Office for the Coordination of Humanitarian Affairs, unocha.org.

Explosive B2C E-commerce Demand Lifts Parcel and Express Freight Volumes

Philippine e-commerce revenue climbed 19.6% in 2024 to USD 24.1 billion, driven by higher mobile penetration and digital payment adoption. Marketplace giants and emerging social-commerce players now route bulk parcels through dedicated sort centers and require freight forwarders to provide same-day or next-day delivery solutions. High return ratios and cash-on-delivery preferences add reverse-logistics complexity, spurring demand for integrated fulfillment, payment reconciliation, and track-and-trace services. Provincial growth pockets in Mindanao and Central Visayas further compel providers to expand secondary hubs and align with regional courier partners for extended reach[2]Climate change supercharged late typhoon season in the Philippines,” Imperial College London, imperial.ac.uk.

ASEAN Integration and RCEP Implementation Foster Intra-Asia Trade

Implementation of the Regional Comprehensive Economic Partnership reduces tariffs on a broad spectrum of manufactured and agricultural goods within the bloc. Philippine exporters of electronics, garments, and agri-products gain wider duty-free access to key Asian markets, generating incremental volumetric growth for both full-container-load and less-than-container-load shipments. Simplified rules of origin and digital customs systems lessen border hold-ups, allowing freight forwarders to optimize sailing schedules and block-train departures for east-bound cargo.

Foreign-Ownership Liberalization Attracts Global 3PLs

Amendments to the 2023 Public Service Act now permit 100% foreign ownership in shipping, railways, and telecom assets. Global logistics companies redeploy capital toward dedicated Philippine branches, bringing warehouse automation, data-driven pricing, and multimodal planning tools. Stiffer competition intensifies consolidation pressure on smaller incumbents, prompting joint-ventures, share-swaps, and technology partnerships to keep pace with rising service-level benchmarks.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port congestion and Metro Manila traffic inflate logistics costs | -1.1% | NCR, CALABARZON, Central Luzon | Short term (≤ 2 years) |

| Fragmented, ageing trucking fleet raises maintenance outlays | -0.8% | Nationwide | Medium term (2-4 years) |

| Multi-agency accreditation overlap delays licensing | -0.4% | National | Short term (≤ 2 years) |

| Intensifying typhoon and flood events disrupt operations | -0.9% | Eastern seaboard and northern Luzon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Port Congestion and Metro Manila Traffic Inflate Logistics Costs

High truck density and limited port gate capacity in Manila extend container dwell times beyond regional norms, pushing up demurrage and storage fees. Drivers lose productive hours navigating bottlenecks, and shippers absorb padding charges as forwarders build safety buffers into delivery commitments. New roadworks occasionally narrow lanes, adding short-term pain before capacity gains materialize. For time-sensitive electronics and perishables, these impediments undermine the Philippines freight forwarding market share in premium cargo segments and erode provider margins as overtime and fuel expenditures escalate[3]“PEZA—Service Enterprise Database System,” Philippine Economic Zone Authority, peza.gov.ph.

Intensifying Typhoon and Flood Events Disrupt Operations

Six consecutive typhoons struck the Philippines between October and November 2024, affecting more than 13 million residents and damaging critical transport links. Recurring storm events compel freight forwarders to lift insurance limits, maintain auxiliary warehousing in safer zones, and invest in climate-resilient infrastructure. Shipping lines routinely defer sailings or reroute around storm tracks, forcing forwarders to recalibrate equipment allocation and absorb detention fees. These added costs weigh on profitability and temper volume growth, particularly for small and medium-sized forwarders with limited financial buffers[4]“Philippines—Country Partnership Strategy (2024–2029): Country Climate Investment Plan,” Asian Development Bank, adb.org .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Sea Freight Dominance Faces Air Cargo Acceleration

Sea freight claimed 58.29% of Philippines freight forwarding market share in 2024, reinforced by bulk raw-material flows and inter-island domestic trade lanes. Carriers leverage direct vessel calls to Manila, Subic, and Batangas, while roll-on roll-off ferries support regional loops. Freight forwarders differentiate through contract charters, berth-window negotiations, and end-to-end import processing.

Air freight, though smaller, logged the fastest growth at 6.83% CAGR to 2030 as e-commerce parcels, semiconductor components, and high-value pharmaceuticals migrate to belly-hold capacity. Network carriers expand dedicated freighter frequencies to Clark and Cebu, offering forwarders enhanced uplift options. As customs adopts paperless clearance, transit reliability improves, making air cargo more attractive for just-in-time manufacturers.

Second-tier modes—road, rail, and coastal barge—function mainly as connectors, moving containers between dry ports and gateways. Planned rail corridors under the North–South Commuter Railway will provide long-haul alternatives, enabling the Philippines freight forwarding market to rebalance modal share over the long term. Digital route-optimization platforms help carriers consolidate less-than-truckload shipments, trimming empty mileage and cutting carbon footprints.

By End-User: Manufacturing Leadership Challenged by Retail Trade Surge

Manufacturing held 27.76% of the Philippines freight forwarding market size in 2024, anchored in electronics and semiconductor exports that demand strict lead-time adherence and climate-controlled handling. Multinational assemblers cluster near economic zones in Cavite, Laguna, and Clark, generating predictable inbound component flows and outbound finished-goods consignments.

Wholesale and retail trade posts the steepest trajectory at 6.22% CAGR to 2030 as e-commerce platforms expand reach. Parcel density spikes in peri-urban centers, prompting freight forwarders to co-locate fulfillment hubs near high-volume sort facilities. Reverse-logistics volumes rise in tandem with online returns, nudging providers toward dedicated refurbishment and re-packaging lines.

Construction, agriculture, and extractive industries contribute steady baseline cargo flows, but seasonal demand swings and weight-restricted roads require flexible equipment deployment. Specialized forwarders carve out niches in project cargo, reefer transport, and hazardous materials, further diversifying the competitive field within the Philippines freight forwarding market.

Geography Analysis

Luzon anchors roughly 60% of national freight activity, buoyed by Manila’s twin seaports and Ninoy Aquino International Airport. High container turnover, dense consumer clusters, and extensive industrial parks cement Luzon’s primacy. However, chronic congestion encourages some shippers to reroute via Subic or Batangas, offering forwarders gateway diversification.

Visayas benefits from Cebu’s role as a central nautical crossroads. Upgraded Mactan-Cebu International Airport cargo facilities and deep-water berths extend the reach of international carriers. Regional SME exporters in furniture, garments, and processed food rely on Cebu-based forwarders for consolidation before overseas dispatch.

Mindanao registers the fastest freight throughput expansion as agribusiness, minerals, and e-commerce volumes climb. Completion of Davao Coastal Road and modernization of the General Santos port elevate corridor reliability, attracting forwarders to set up satellite offices. Typhoon exposure remains high on the eastern flank, necessitating adaptive routing, but the region’s growth prospects keep service providers investing in fleet and warehousing.

Inter-island corridors link these island groups through nautical highway spurs, enabling direct truck-on-ferry moves that bypass Manila. As more lanes open, the Philippines freight forwarding market gains cost-efficient domestic connectivity, reducing reliance on empty backhauls and lowering US-dollar cost per ton-kilometer.

Competitive Landscape

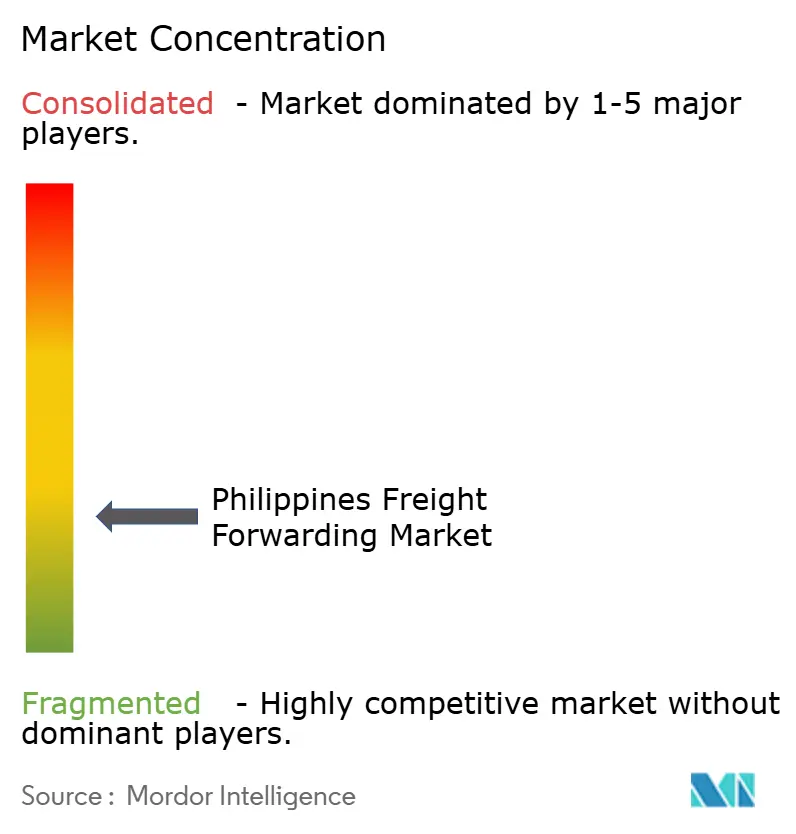

The Philippines freight forwarding market is moderately fragmented; no single firm commands more than a mid-teens revenue share. Multinationals-DHL, UPS, FedEx, and Kuehne + Nagel capitalize on global airlift rights, API-rich booking portals, and integrated brokerage solutions. Domestic champions such as 2GO, LBC Express, and Royal Cargo dominate inter-island shipping, last-mile provincial delivery, and project cargo.

Technology investments shape competitive differentiation. Leading players deploy automated sorters, AI-powered capacity forecasts, and blockchain-enabled document sharing to pare cycle times. Liberalized foreign-ownership rules spur acquisition interest in local license holders, and alliance networks grow as medium-size forwarders seek scale economies.

Service white spaces remain in cold-chain handling, pharma compliance, and island-to-island parcel networks. Providers that bundle warehousing, inventory financing, and omnichannel fulfillment gain stickier customer ties. Market entrants must navigate multi-agency accreditation hurdles, but those with specialty assets temperature-controlled trucks, ISO tanks, or oversized-cargo modules can carve defensible niches.

Philippines Freight Forwarding Industry Leaders

2GO Group

LBC Express Holdings

Royal Cargo

DHL Group

DSV A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: DHL opened a 15,000 m² automated sorting hub in Pasay City to boost express capacity across Metro Manila.

- November 2024: UPS inaugurated an automated package-sorting facility at Clark International Airport with hourly throughput of 15,000 parcels.

- October 2024: C.H. Robinson launched a Manila branch offering cold-chain freight forwarding for pharmaceuticals and perishables.

- September 2024: Maersk earmarked USD 30 million to modernize crane systems and digital tracking at the Port of Manila.

Philippines Freight Forwarding Market Report Scope

| Air |

| Sea |

| Others |

| Oil and Gas, Mining and Quarrying |

| Construction |

| Manufacturing |

| Agriculture, Fishing, and Forestry |

| Wholesale and Retail Trade |

| Others |

| By Mode of Transport | Air |

| Sea | |

| Others | |

| By End-User | Oil and Gas, Mining and Quarrying |

| Construction | |

| Manufacturing | |

| Agriculture, Fishing, and Forestry | |

| Wholesale and Retail Trade | |

| Others |

Key Questions Answered in the Report

How large is the Philippines freight forwarding market in 2025?

It stands at USD 2.33 billion, with a projected 6.03% CAGR to 2030.

Which mode dominates freight forwarding volumes?

Sea freight leads with 58.29% share, driven by bulk and inter-island flows.

What is the fastest-growing service segment?

Air cargo, expanding at 6.83% CAGR through 2030, powered by electronics and e-commerce parcels.

Why is Mindanao a growth hotspot for logistics?

Infrastructure upgrades and rising agribusiness exports push freight volumes higher in the region.

How does foreign-ownership liberalization affect providers?

Global 3PLs can now operate fully owned Philippine entities, intensifying competition and technology transfer.

Page last updated on: