Air Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 99.68 Billion |

| Market Size (2031) | USD 126.55 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

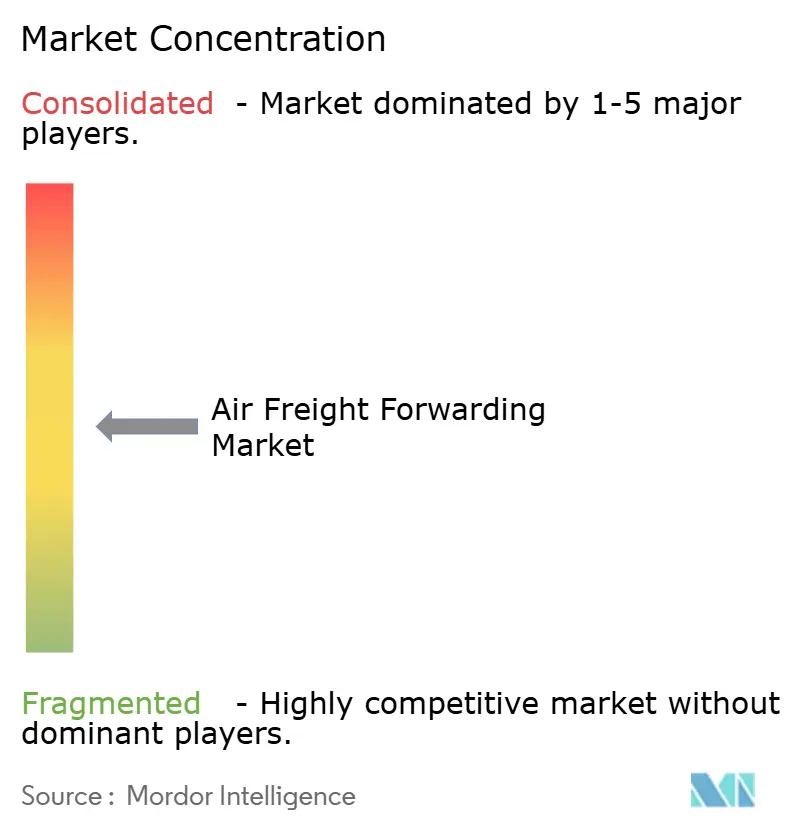

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Freight Forwarding Market Analysis by Mordor Intelligence

The Air Freight Forwarding Market size was valued at USD 95.27 billion in 2025 and is estimated to grow from USD 99.68 billion in 2026 to reach USD 126.55 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031).

This growth path balances fuel-cost volatility, carbon-compliance expenses, and slot scarcity at major hubs against structural tailwinds from cross-border e-commerce, temperature-controlled pharmaceutical logistics, and high-value semiconductor flows that continue to favor speed and reliability. Policy shifts are reshaping parcel routing and compliance, which raises the value of forwarders with global brokerage coverage and shipment-level visibility for customs and sustainability reporting. In healthcare, GDP-certified gateways, validated packaging, and continuous temperature monitoring support a higher-margin mix that cushions rate pressure in general freight. Semiconductor shipments tied to AI infrastructure spending sustain premium yields, with Asia-Pacific production hubs anchoring long-haul traffic into North America and Europe.

Key Report Takeaways

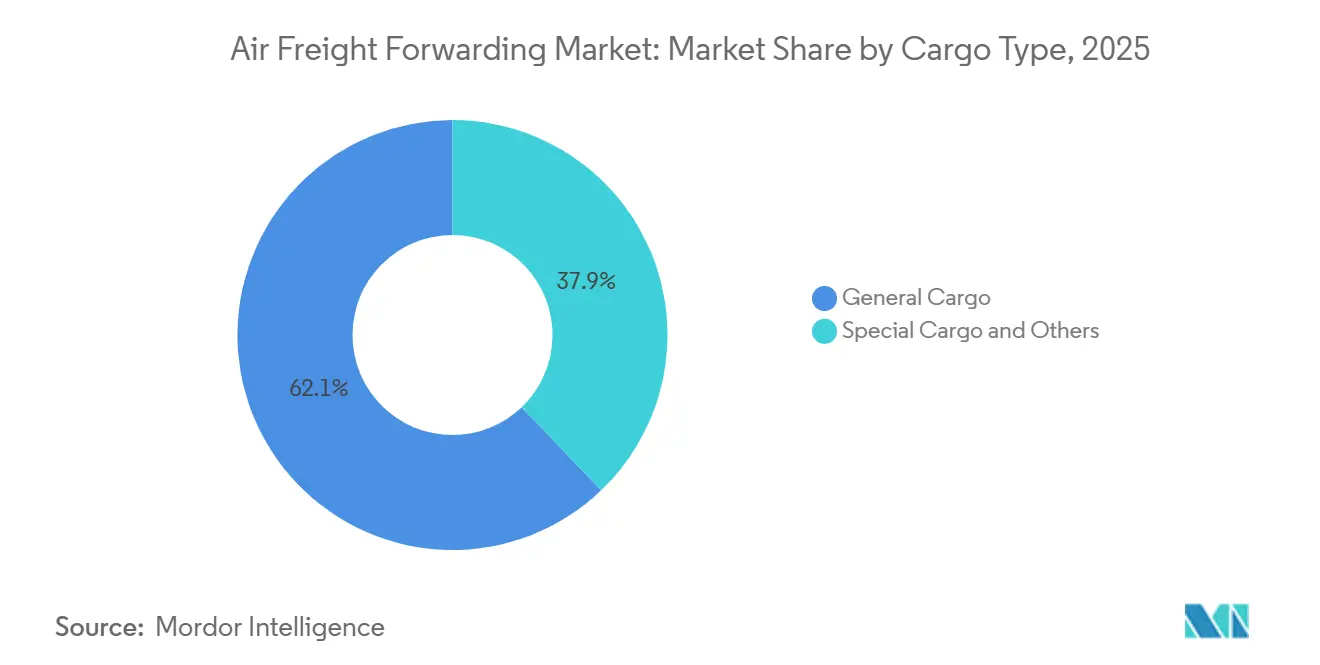

- By cargo type, general cargo led with 62.15% market size of the air freight forwarding market size in 2025, while special cargo is forecast to expand at a 4.18% CAGR through 2031.

- By destination, international routes accounted for 75.45% of market share in 2025 and are projected to grow at a 4.80% CAGR to 2031, outpacing domestic flows.

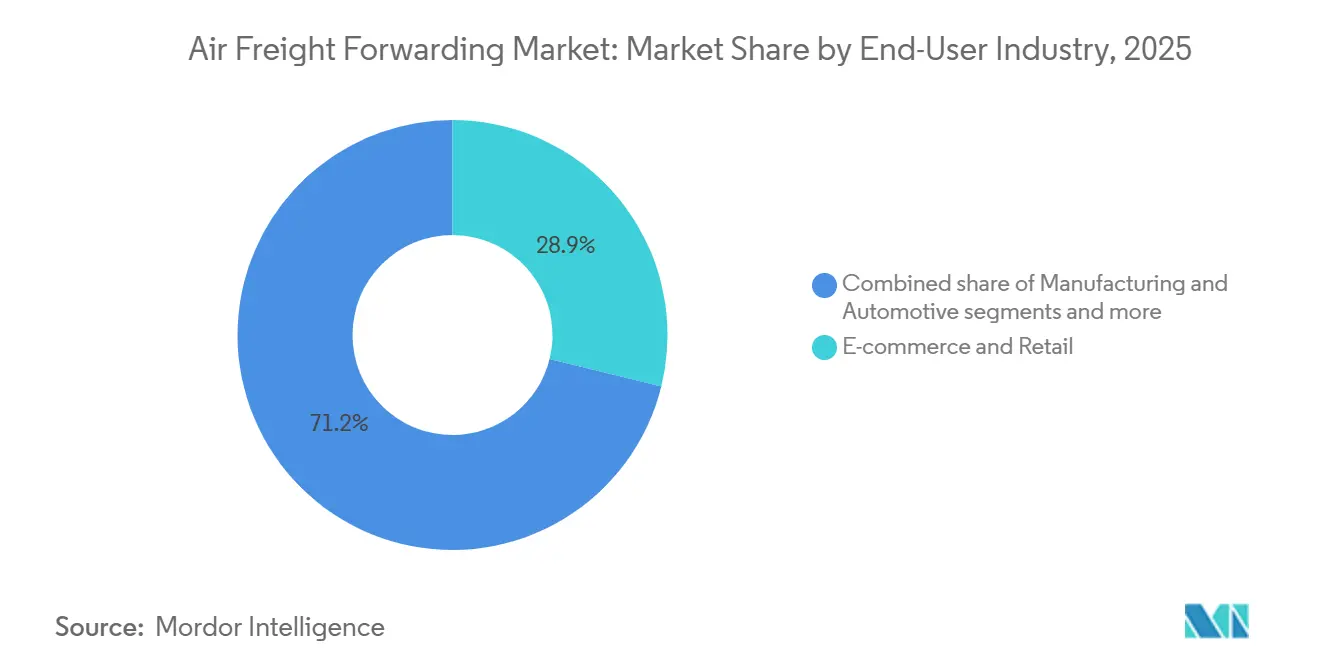

- By end-user industry, e-commerce and retail held the largest share at 28.85% market share of the air freight forwarding market in 2025, and healthcare and pharmaceuticals show the fastest trajectory at a 4.82% CAGR through 2031.

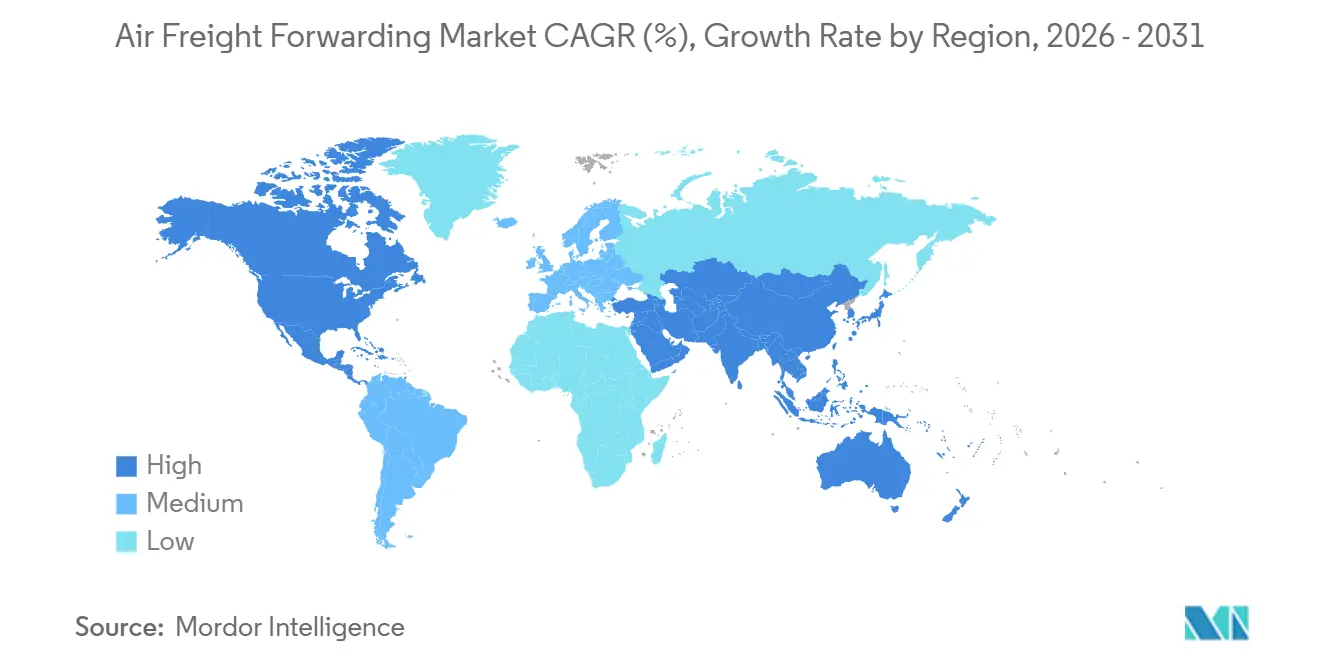

- By region, Asia-Pacific led with a 40.70% market share in 2025 and is forecast to expand at a 7.80% CAGR through 2031, the fastest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom driving express air shipment demand | +1.2% | Global, with early gains in China-Europe corridors, Southeast Asia, and Latin America nearshoring routes | Medium term (2-4 years) |

| Time-critical pharmaceutical and biotech cold chain logistics | +0.9% | North America, Europe, India, with spill-over to emerging APAC and Middle East manufacturing hubs | Long term (≥ 4 years) |

| Growth in high-value electronics and semiconductor trade | +1.0% | APAC core (Taiwan, South Korea, China), with secondary flows to North America and Europe for AI infrastructure | Short term (≤ 2 years) |

| Expansion of dedicated freighter fleets and belly cargo capacity | +0.7% | Global, concentrated in Middle East carriers, Asia-Pacific operators, and European gateways | Medium term (2-4 years) |

| Nearshoring and regionalized supply chains bolster cross-border and intra-regional airflows | +0.6% | North America, especially U.S.-Mexico corridors, and intra-APAC production shifts | Medium term (2-4 years) |

| Digitalization of pricing, booking, and customs accelerates SME adoption | +0.5% | Global, with stronger uptake at major export gateways and across digitally enabled brokerage networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom: Cross-Border Parcel Surge Strains Last-Mile Integration

Cross-border parcel traffic keeps rising and is changing how forwarding networks operate, as small consignments demand faster consolidation, automated customs, and flexible last-mile partnerships that can maintain delivery promises in multiple jurisdictions. The United States suspended the de minimis exemption for China-origin goods in May 2025, which forced platforms to redirect inventory and pushed more parcels into China-Europe gateways where import regimes and duty thresholds remain under review. The European Union’s proposal to abolish the EUR 150 (USD 176.44) low-value thresholds by July 2026 would introduce per-item duties and favor forwarders with digital pre-clearance and harmonized master data across carrier and broker systems. Compliance complexity can become a moat as large forwarders leverage established brokerage networks and standardized data flows, which support sticky customer relationships when routing rules change frequently. Traffic within Asia remained strong through late 2025, and a larger share of e-commerce flows is now using air to protect promised delivery windows even when base rates soften in ocean, which lifts the air freight forwarding market in off-peak months.

Pharmaceutical Cold Chain: Biologics and Cell Therapies Demand GDP-Certified Networks

In the air freight forwarding market, demand for GDP-certified logistics networks is rising due to biologics, cell and gene therapies, and other temperature-sensitive medicines. These shipments require validated temperature ranges, real-time monitoring, a strict chain of custody, and audited facilities, favoring forwarders with standardized life sciences SOPs and global compliance coverage. Capacity control on key healthcare lanes is becoming vital. In February 2026, DHL Group introduced a dedicated Boeing 777F on the Brussels–Cincinnati route, aligned with pharma-focused capacity at BRUcargo. Securing predictable lift through block space or charter programs helps forwarders maintain schedule integrity and protect yields on high-value medical cargo. Regulatory mandates highlight the need for digital integration. The Drug Supply Chain Security Act requires end-to-end serialization and interoperable tracing, benefiting forwarders integrating shipment metadata with manufacturer and distributor systems. India’s Bio-Pharma Shakti initiative is expanding GDP-compliant gateways and boosting biosimilar export readiness, increasing controlled-temperature flows globally. Investments in life sciences infrastructure, certification depth, and validated temperature performance enable forwarders to command premium pricing, offset general freight yield pressure, and sustain growth in the air freight forwarding market.

Electronics and Semiconductors: AI Boom Elevates Taiwan’s Export Trajectory

High-value semiconductor components shipped from Taiwan and South Korea increasingly rely on air freight forwarders to secure priority lift and manage export-control documentation. Export growth from Taiwan, driven by AI orders from leading foundries in 2024, has boosted premium air volumes as time-to-market and inventory velocity outweigh ocean freight cost advantages. This trend continued into 2025, with rising shipments to North America and Europe supporting data center and advanced computing expansions, driving demand for priority air solutions. Export controls on advanced chipmaking equipment have increased regulatory complexity, boosting demand for forwarders skilled in compliant routing, license management, and precise documentation. Meanwhile, South Korean manufacturers have expanded high-bandwidth memory production and long-haul capacities to serve North American server and accelerator clients, strengthening transpacific air corridors. Due to the high value and critical nature of semiconductor shipments, reliability and compliance take precedence over rate sensitivity. This supports yield resilience and positions semiconductor trade flows as a key growth driver for the air freight forwarding market, ensuring steady volumes across economic cycles.[1]Semiconductor Industry Association, “Industry Statistics,” Semiconductor Industry Association, semiconductors.org

Freighter Fleet Expansion: Narrowbody Conversions Fill Widebody Delivery Gaps

Retirements and new-aircraft delays have left a gap that converted narrowbodies are filling, which allows forwarders and carriers to add frequency in secondary markets and align capacity with e-commerce parcel profiles. First deliveries of the A350F shifted to 2027, and the 777-8F timeline was extended further, so operators leaned more on conversions and leased capacity to cover peak seasons and maintain service integrity. Middle East carriers ordered additional freighters to strengthen trunk routes that connect Asia with Europe and North America, which consolidates lift through Dubai and Doha. Large forwarders continued to arrange dedicated charters and long-term leases to gain control in peak months and protect service-level agreements for time-definite cargo. These moves spread across regions and keep the air freight forwarding market anchored even as belly capacity recovers across passenger networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High and volatile aviation fuel costs | -0.8% | Global, with acute pressure on long-haul Transpacific and Europe-Asia routes where fuel represents 30-35% of costs | Short term (≤ 2 years) |

| Environmental regulations and carbon emission pressures | -0.6% | Europe under EU ETS and ReFuelEU, with diffusion to Singapore, Japan, and California by 2027 | Medium term (2-4 years) |

| Aircraft delivery delays and freighter retirements tighten available capacity | -0.5% | Global, with effects felt on peak-season lanes pending A350F and 777-8F entries and 747/MD-11 retirements | Medium term (2-4 years) |

| Geopolitical disruptions and airspace closures reduce effective network throughput | -0.7% | Europe-Asia routings and Middle East adjacency, with network-wide spillovers during prolonged or repeated closures | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fuel Cost Volatility: Geopolitical Shocks Amplify Margin Compression

Jet fuel price swings tighten margins and complicate surcharge recovery during contract lags, especially on long-haul corridors where fuel is a larger share of direct costs. Airspace closures and extended flight paths increase burn and reduce payloads on some lanes, which forces repricing and sharper capacity discipline during peak months. When carriers renegotiate to reflect fuel trends, larger forwarders hold capacity at scale while smaller peers pass through costs more quickly to protect cash, which can shift win rates during competitive bids. Sustainable aviation fuel surcharges add another layer to Europe-origin flights as carriers blend SAF and incur higher input costs that filter through to invoices. SAF prices remain higher than conventional kerosene, which constrains adoption outside compliance mandates and premium-shipping programs, although corporate buyers are beginning to fund SAF pools to meet emissions goals.[2]U.S. Energy Information Administration, “Petroleum & Other Liquids,” U.S. EIA, eia.gov

Environmental Regulations: Carbon Compliance Costs Reshape Competitive Dynamics

Removal of free allowances under the EU Emissions Trading System in 2026 increased cost exposure on EU-departing flights, and airlines pass these costs downstream through carbon-related charges per unit. CORSIA is in its first compliance phase and broadens coverage across international aviation, which encourages shipment-level emissions accounting and data transparency with shippers’ sustainability teams. Dual policy regimes require parallel reporting and verification for emissions, and forwarders need tools that calculate Scope 3 footprints by route and aircraft type to retain enterprise accounts. ReFuelEU Aviation set minimum SAF blends on EU uplift, which hardwires incremental costs into operations and pushes forwarders to offer green service tiers with clear documentation. California’s regulatory path is moving toward EU-style frameworks for aviation, which will extend carbon accounting and surcharge practices to major West Coast gateways that manage Asia-Pacific flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cargo Type: Special Cargo Premiums Offset General-Freight Commoditization

General cargo accounted for 62.15% in 2025, while special cargo is set to grow faster at a 4.18% CAGR through 2031 as pharma, batteries, and aerospace parts expand within the premium mix. This divide reflects standardized goods migrating to digital spot channels and ocean alternatives when time allows, while regulated and temperature-controlled shipments reward certified networks with higher rates and stronger retention. Pharma traffic relies on controlled facilities, validated packaging, and trained handlers that can document compliance at each handoff, which sustains premium yields and improves service resilience. Lithium battery flows focus on dedicated freighters and specialized packaging as operators adhere to Dangerous Goods rules, which limit supply and stabilize pricing for compliant forwarders. Live animals and certain perishables form micro-niches that require specialized stalls, veterinary approvals, and time-definite routings, which add complexity that general cargo networks are unlikely to replicate efficiently.[3]International Air Transport Association, “Dangerous Goods and Live Animals Regulations,” IATA, iata.org

As specialized segments grow, certification programs like IATA CEIV Pharma expand across hubs and raise barriers to entry, which favors incumbents that invested ahead of demand inflection. Perishables remain seasonal with premium peaks during events and holidays, and airline cargo divisions highlight performance on these lanes to secure repeat volumes from growers and distributors. The balance of volumes continues to lean toward general freight in absolute terms, but the rate mix shifts toward controlled and hazardous categories, which supports revenue stability during soft cycles. These dynamics help the air freight forwarding market avoid steep declines in a rate-reset year when pricing for commoditized flows remains under pressure. The interplay between standardized lanes and regulated niches will continue to define how networks allocate capital, training, and technology over the next planning cycles.

By Destination: International Flows Dominate as Nearshoring Rebalances Regional Lanes

International destinations held 75.45% in 2025 and are projected to grow at a 4.80% CAGR to 2031, outpacing domestic flows that maintain a smaller share but serve critical replenishment windows. Recent U.S. de minimis changes altered routing from China to North America and pushed more parcels into China-Europe corridors, where customs, duties, and routing strategies took on greater weight in network design. Nearshoring into Mexico lifted intra-North America traffic, and as manufacturing nodes expanded along the border states, air volumes gained from time-critical flows that feed just-in-time production. Within China, domestic air networks scaled with dedicated freighters to serve tier-2 and tier-3 cities, which shows that domestic lanes still play a role in speed-sensitive retail and replenishment. International complexity, including brokerage and currency, supports stronger margins per shipment than domestic legs, which keeps forwarders focused on cross-border optimization and compliance-led services.

Domestic networks in India grew as UDAN expanded connectivity across underserved airports and improved the economics of short-haul freight on selected lanes. Forwarders continued to develop hybrid routings that mix trucking and air to balance cost with speed as regional supply chains evolved in Asia and the Americas. Digital pre-clearance and automated filings reduce dwell and help sustain service levels on higher-complexity international legs, a shift that supports pricing consistency for multi-country distribution. As international volumes absorb more e-commerce and pharma traffic, the air freight forwarding market size linked to cross-border flows is expected to rise with a broader base of regulated and time-sensitive shipments. These factors keep international corridors central to network planning as nearshoring enriches regional densities rather than replacing long-haul hubs.

By End-User Industry: Healthcare Leads Growth While E-Commerce Anchors Volume

E-commerce and retail represented 28.85% in 2025 and will continue to anchor absolute volumes, while healthcare and pharmaceuticals show the fastest growth at a 4.82% CAGR to 2031 on the back of GDP-compliant expansion and serialization requirements. Healthcare shipments attract premium rates due to strict controls, temperature logging, and contingency planning needed to prevent excursions, which helps protect profitability at the portfolio level. The U.S. DSCSA strengthens traceability expectations and pushes greater data collaboration with carriers and forwarders to confirm custody and integrity for packaged medicines. In parallel, major operators invested in dedicated pharma infrastructure and secured point-to-point capacity to stabilize turn times and integrity during peak months. This momentum allows the air freight forwarding market to rely on a steady base of controlled-temperature traffic even if consumer goods volumes moderate.

High-tech and electronics maintain a significant share of long-haul lanes as semiconductor supply supports server, automotive, and industrial applications with strict delivery timestamps and high value density. Automotive and industrial flows use aircraft-on-ground services when unit shortages threaten assembly lines, which sustains premium add-on services in the broader portfolio. Perishables and fresh produce remain seasonal, and airline cargo divisions refine schedules and cold capabilities to secure repeat contracts with growers and distributors in Latin America and Oceania. Digital-first quoting in e-commerce supports quick tendering but compresses margins on standardized parcels, which shifts emphasis to operational excellence and data-driven visibility for retention. Across end markets, the air freight forwarding market continues to balance volume-heavy retail flows with high-margin healthcare and time-critical industrial traffic that stabilize returns.

Geography Analysis

Asia-Pacific held a 40.70% market share in 2025 and is forecast to grow at a 7.80% CAGR through 2031, led by semiconductor exports from Taiwan and South Korea, rising pharma output across India, and production shifts within Southeast Asia that deepen intra-Asia flows and long-haul links to the West. Taiwan’s exports reflected strong year-over-year growth in 2024 that aligned with AI-related investments, while India’s policy support for biosimilars and biologics reinforced capacity building at major gateways. Intra-Asia demand showed robust momentum into late 2025, which helped smooth seasonality and stabilize load factors on regional services. Following the U.S. de minimis change in May 2025, more cross-border parcels were routed to Europe-bound channels, and operators adjusted consolidation and customs strategies in response. Japan and South Korea maintained premium flows through electronics and automotive components, and airlines invested in lift to support higher memory and display shipments on transpacific lanes.

Europe accounted for an estimated 25% share in 2025, supported by concentrated pharma clusters and strong hubs such as Frankfurt and Paris that process large volumes of long-haul freight. EU air freight volumes grew in 2024 as Eastern Asia trade lanes expanded, and e-commerce parcels redirected to European entry points strengthened the role of BENELUX and German gateways as consolidation platforms for the continent. ReFuelEU Aviation introduced a 2% SAF blend mandate from 2025, which raised operating costs for carriers departing EU airports and added a new dimension to lane economics and customer pricing. The EU ETS removed free allowances in 2026, which increased the carbon cost burden for airlines and filtered into forwarder invoices on both intra-EU and international departures. Investment in airside facilities continued to enhance throughput, as large operators prepared for sustained Asia-Europe flows with capacity, sustainability features, and direct aircraft access to improve turn times.[4]European Commission, “Air Freight Statistics and Policy,” European Commission, europa.eu

North America maintained an estimated 30% share in 2025 as e-commerce consumption, pharma manufacturing scale, and nearshoring into Mexico reinforced cross-border and long-haul traffic. Mexico’s growth in exports to the United States supported higher regional air volumes, while platforms explored distribution models that maintain two- to five-day service levels within tariff and routing constraints. Canada’s throughput increased in 2025, with Vancouver and Toronto acting as anchors for transpacific and pharma traffic despite capacity limits at secondary airports. A 2026 U.S. Supreme Court ruling changed tariff dynamics and introduced short-term refund flows, which added uncertainty to booking patterns and pricing for 2026 while sectoral measures remained in effect for priority categories. Across the broader region, semiconductor demand tied to AI infrastructure continued to lift inbound flows from Asia, which supported the air freight forwarding market during shifts in retail parcel routing.

The Middle East and Africa together held an estimated 9% to 10% share in 2025, with Dubai and Doha leading as transshipment hubs for East-West trunk routes and playing a larger role during rerouting events. Additional freighter orders announced in 2026 by leading Gulf carriers reinforced long-haul connectivity as global airspace disruptions forced alternative routings that preserve cargo integrity. In South America, Brazil anchored regional flows and supported perishables exports that rely on air to protect shelf life during key harvest windows, while new interline agreements improved network coverage. Customs improvements at selected Brazilian airports enhanced predictability for time-sensitive cargo, though bottlenecks persist at other points of entry. Kenya’s horticulture exports kept Africa-Europe lanes active, and efforts to diversify beyond flowers continued as stakeholders sought higher year-round utilization.

Competitive Landscape

The market shows moderate consolidation at the top, with scale benefits in procurement, digital platforms, and controlled capacity underpinning service stability during peak periods and disruptions. DSV completed the acquisition of DB Schenker for EUR 14.3 billion (USD 16.82 billion), targeted DKK 9 billion (USD 1.41 billion) in annual opportunities by 2027, and expanded global reach, which set a benchmark for scale-driven integration within the air freight forwarding market. Nippon Express’ acquisition of CargoPartners and Yusen Logistics’ acquisition of Movianto deepened sector specialization in Europe and enhanced healthcare logistics capacity integrated with global forwarding networks. Incumbents invested in dynamic pricing, visibility, and automation to speed quote-to-book and orchestrate multi-leg routings in real time for time-definite, regulated, and high-value cargo. These moves reinforce stickiness in complex verticals and support premium tiers that defend margins amid base-rate variability.

Tech-focused platforms accelerated direct connections with airlines and brokers to streamline small and medium enterprise bookings and provide transparent pricing in near real time. Airline cargo divisions expanded widebody and regional narrowbody networks that link production hubs to consumption centers, which sharpened competition for enterprise accounts on lanes where predictable lift is critical. Large forwarders increased charter programs and long-term leases to limit exposure to airline allocation cuts and stabilize service for premium customers during Q4 peaks and routing disruptions. The combination of scale, sector specialization, and controlled capacity is central to winning and retaining regulated customers whose products command higher yields and strict service metrics. These dynamics continue to define the air freight forwarding market as contracts that emphasize operational resilience and data transparency.

Sustainability requirements added a new layer to competitive differentiation, with forwarders offering green service tiers that include SAF contributions and shipment-level emissions reporting aligned with corporate climate targets. Kintetsu World Express executed SAF agreements to help reduce Scope 3 emissions in cooperation with airline partners, while expanding its CEIV Pharma footprint to serve high-growth healthcare corridors. DHL launched a dedicated B777 pharma freighter and scaled its health logistics investment to build capacity and control on critical lanes. As regulations expand across regions and stakeholders seek measurable emissions reductions, operators that unify carbon accounting, routing, and capacity planning may retain a durable advantage in bids and renewals. These shifts continue to shape the air freight forwarding market’s path through 2026 and beyond as shippers evaluate partners on reliability, visibility, and verified sustainability outcomes.

Air Freight Forwarding Industry Leaders

DHL Supply Chain & Global Forwarding

Kuehne + Nagel

DSV

UPS Supply Chain Solutions

Expeditors International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group expanded its Airfreight Cold Chain Network with a dedicated Boeing 777 freighter operating Brussels to Cincinnati, integrated with pharma-only zones and a broader EUR 2 billion (USD 2.32 billion) health logistics investment.

- February 2026: Savino Del Bene acquired two Netherlands-based operators to strengthen coverage in Northern Europe and opened a new office in Budapest to serve Central European demand.

- February 2026: LX Pantos acquired a large-scale logistics center in Katowice, Poland, intended to serve as a European hub supporting Korean corporates and future reconstruction logistics.

- December 2025: GEODIS expanded its South American network through an interline agreement with Atlas Air and MAS, improving connectivity in Brazil, Colombia, Panama, Chile, and Costa Rica with direct links from Asia Pacific via Mexico.

Global Air Freight Forwarding Market Report Scope

The Air Freight Forwarding Market Report is Segmented by Cargo Type (General Cargo, Special Cargo, and Others), by Destination (International, Domestic), by End-User Industry (E-Commerce & Retail, Manufacturing & Automotive, Healthcare & Pharmaceuticals, Perishables & Fresh Produce, and More), and by Geography (North America, South America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| General Cargo |

| Special Cargo and Others |

| International |

| Domestic |

| E-commerce & Retail |

| Manufacturing & Automotive |

| Healthcare & Pharmaceuticals |

| Perishables & Fresh Produce |

| High-Tech & Electronics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Cargo Type | General Cargo | |

| Special Cargo and Others | ||

| By Destination | International | |

| Domestic | ||

| By End-user Industry | E-commerce & Retail | |

| Manufacturing & Automotive | ||

| Healthcare & Pharmaceuticals | ||

| Perishables & Fresh Produce | ||

| High-Tech & Electronics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the air freight forwarding market?

The air freight forwarding market size was USD 95.27 billion in 2025 and is forecast to reach USD 126.55 billion by 2031 at a 4.06% CAGR.

Which cargo type is expanding the fastest within air forwarding?

Special cargo is the fastest-growing category with a 4.18% CAGR through 2031, supported by pharma cold chains, lithium batteries, and aerospace components.

How are policy changes affecting cross-border e-commerce flows?

The United States suspension of de minimis for China-origin shipments in 2025 and EU proposals to remove low-value thresholds are shifting routing toward Europe and rewarding forwarders with strong digital customs capabilities.

Which region leads and which grows fastest in air freight forwarding?

Asia-Pacific leads with 40.70% share in 2025 and is also the fastest-growing at 7.80% CAGR through 2031, driven by semiconductors and expanding pharma exports.

What regulations are most influencing costs in 2026?

EU ETS removal of free allowances and ReFuelEU SAF blending requirements increased carbon-related costs on EU departures, which carriers have passed through to shippers and forwarders.

Where are leading forwarders investing for resilience and growth?

Investments focus on pharma-dedicated capacity and facilities, controlled freighter lift and charters, and digital platforms for pricing, visibility, and shipment-level emissions reporting.

Page last updated on: