Belgium Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

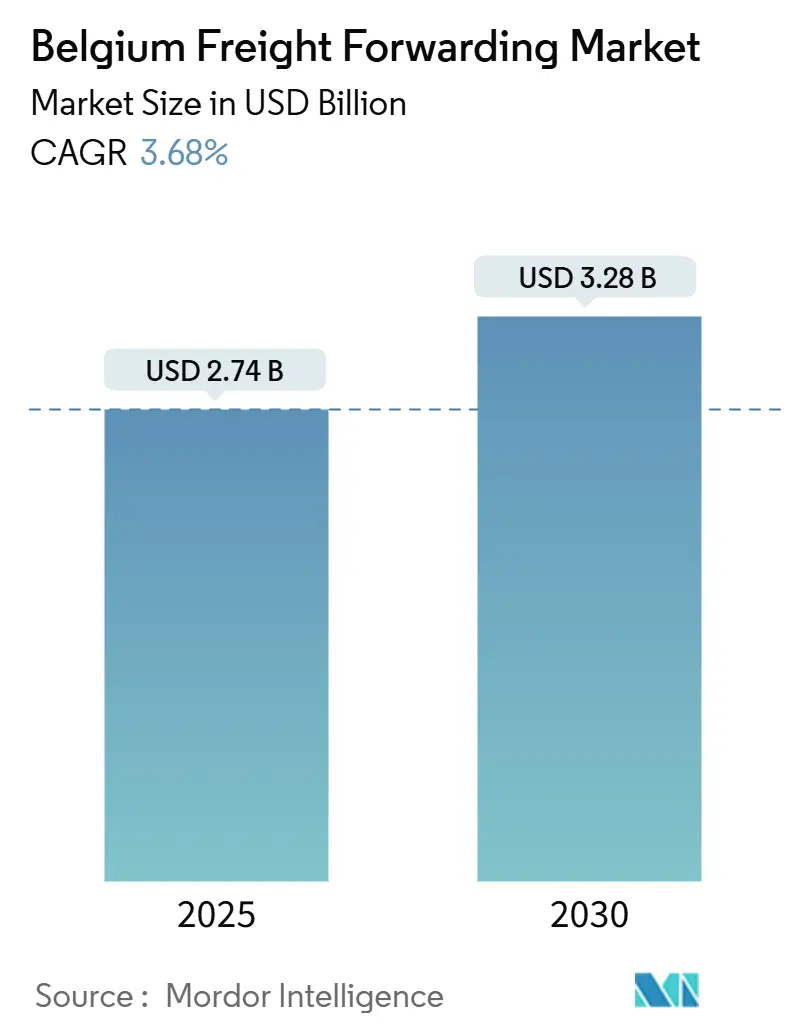

| Market Size (2025) | USD 2.74 Billion |

| Market Size (2030) | USD 3.28 Billion |

| Growth Rate (2025 - 2030) | 3.68% CAGR |

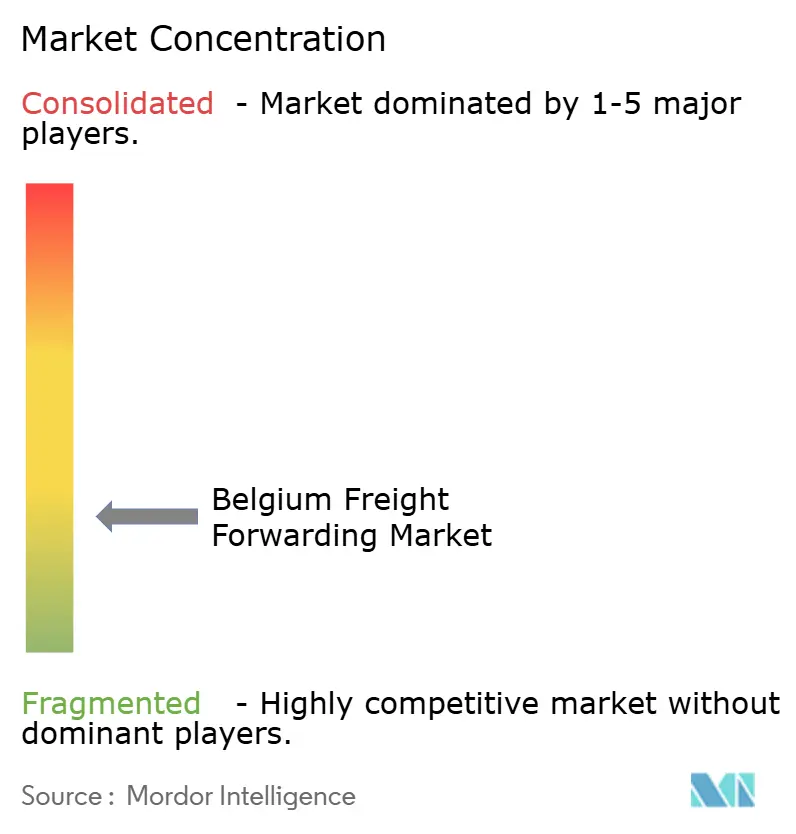

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Freight Forwarding Market Analysis by Mordor Intelligence

The Belgium Freight Forwarding Market size is estimated at USD 2.74 billion in 2025, and is expected to reach USD 3.28 billion by 2030, at a CAGR of 3.68% during the forecast period (2025-2030).

The Belgium freight forwarding market benefits from a location that puts 60% of European purchasing power within overnight trucking distance, sustained container growth at the Port of Antwerp-Bruges, and steady industrial demand for multimodal logistics solutions. The sea freight segment retains its primacy, yet forwarders increasingly deploy rail and barge legs to lower emissions as shippers align with the EU Green Deal. E-commerce volumes originating in neighboring countries expand the customer base for time-definite services, while adoption of digital customs platforms accelerates clearance and frees capacity for higher-value shipments. Consolidation among global third-party logistics providers reshapes competitive positioning as scale economies, data integration, and technology investment become decisive factors for winning new contracts.

Key Report Takeaways

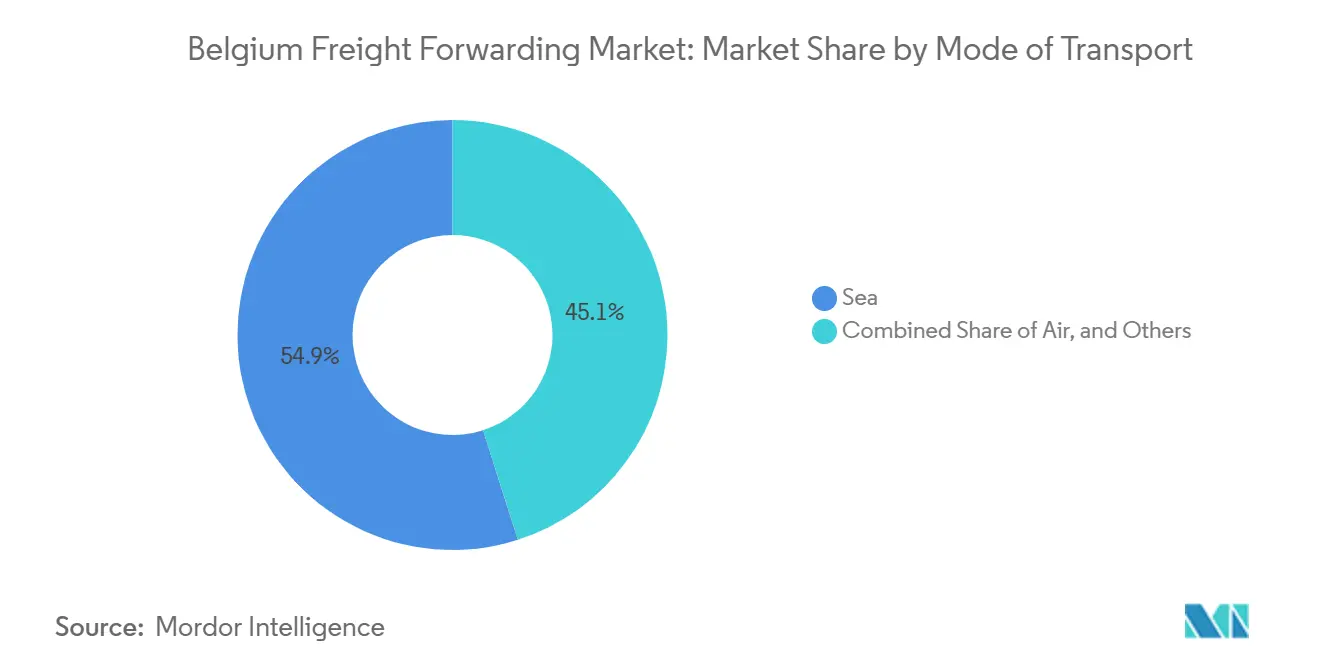

- By mode of transport, sea freight led with 54.92% of the Belgium freight forwarding market share in 2024. By mode of transport, sea freight is projected to post the fastest 3.73% CAGR through 2030.

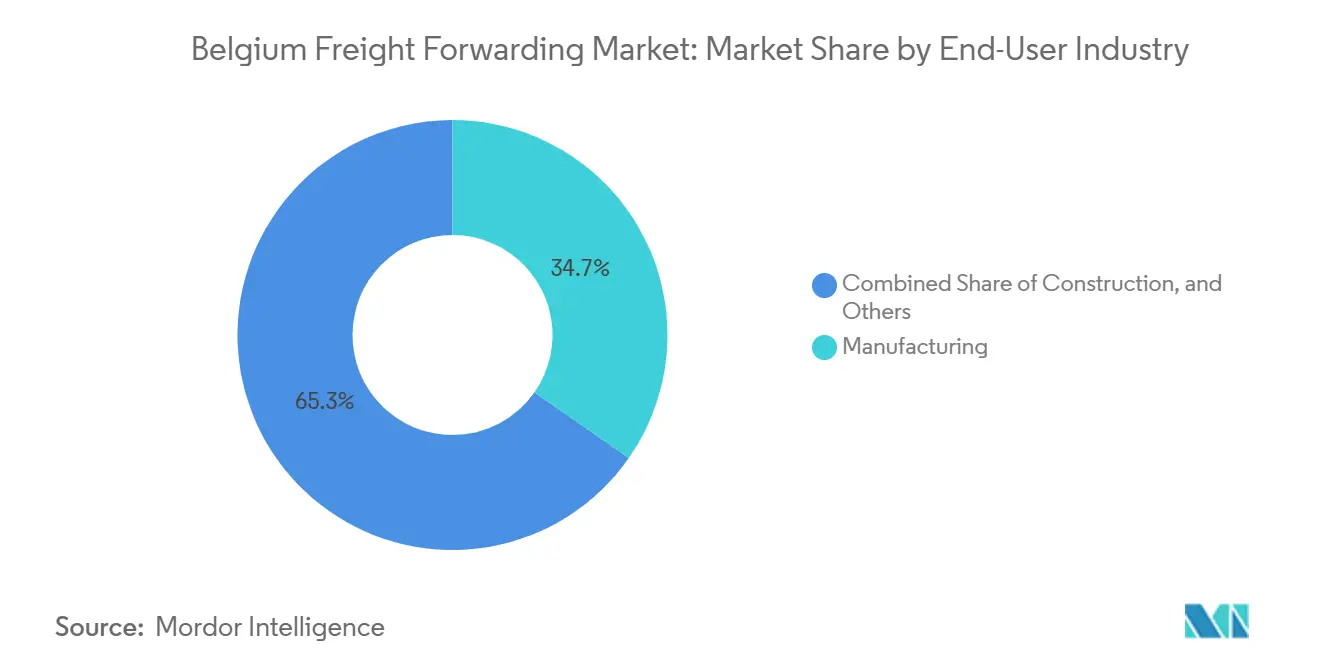

- By end-user, manufacturing commanded 34.70% share of the Belgium freight forwarding market size in 2024. By end-user, wholesale and retail trade is forecast to expand at a 3.84% CAGR to 2030.

Belgium Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic location as EU gateway | +0.8% | Belgium, with spillover to Netherlands and Northern France | Long term (≥ 4 years) |

| Rising container throughput at Port of Antwerp-Bruges | +0.6% | Belgium, primarily Antwerp-Bruges metropolitan area | Medium term (2-4 years) |

| E-commerce boom driving time-sensitive shipments | +0.5% | Belgium, with cross-border EU relevance | Short term (≤ 2 years) |

| EU Green Deal pushing multimodal and low-carbon logistics | +0.4% | EU-wide, early adoption in Belgium | Long term (≥ 4 years) |

| Direct China–Belgium rail corridors expanding | +0.3% | Belgium, connecting to broader European network | Medium term (2-4 years) |

| Digital customs platforms cutting clearance times | +0.2% | Belgium, with EU regulatory alignment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strategic Location as EU Gateway Amplifies Logistics Convergence

Belgium freight forwarding market participants harness a position that places Brussels within a four-hour drive of Paris, Amsterdam, and Frankfurt, giving shippers a single point of entry to multiple consumer hubs. Freight forwarders integrate customs-free Benelux corridors to re-export Asian imports with minimal paperwork, helping electronics and apparel brands collapse regional inventories into Belgian consolidation centers. The Belgium freight forwarding market leverages passenger airports—particularly Brussels and Liege—that maintain belly capacity capable of supporting high-value, time-critical goods under the same distribution footprint as maritime flows, thereby reducing complexity for multinational supply chains. Shippers re-routing traffic from congested North Sea ports in neighboring countries redirect volume through Antwerp-Bruges, reinforcing hub status without large deviations in voyage distance. Ongoing geopolitical realignment encourages near-shoring; Belgium’s ready access to skilled multilingual labor and existing bonded warehousing infrastructure lets forwarders capture incremental trade that might otherwise have landed in Germany or the Netherlands[1]“Belgium as European Logistics Hub,” Belgian Foreign Trade Agency, BELGIANECONOMY.BE.

Rising Container Throughput Drives Modal Integration

Cargo handled at Antwerp-Bruges rose 8.1% in 2024 to 278 million tons, and the port authority earmarked EUR 1.2 billion (USD 1.39 billion) for terminal automation and digitization that cuts crane cycle times and improves berth availability. Forwarders embed these efficiency gains into just-in-time models for automotive and petrochemical clients, using integrated rail lines that now connect Antwerp to 14 European countries on fixed schedules. With dwell time dropping below 36 hours for standard containers, contract logistics providers can synchronize inbound sea freight with outbound barge services along the Scheldt and Albert Canal corridors. As a result, the Belgium freight forwarding market captures orders that combine ocean legs with rail shuttles to inland consolidation points, limiting reliance on long-haul trucking and insulating shippers from driver shortages and fuel price spikes[2]“Cross-border E-commerce Statistics 2024,” European Commission, EC.EUROPA.EU Restraints.

E-commerce Logistics Reshape Time-Sensitive Delivery Models

Belgium’s law mandating two consumer delivery options per transaction, effective March 2024, forces forwarders to add micro-fulfillment sites that handle order-cut-off times as late as 22:00 while still supporting next-day delivery to Luxembourg and northern France. Cross-border orders now represent 55% of Belgian online spending, led by purchases from Germany, France, and the Netherlands. The Belgium freight forwarding market adapts by dedicating capacity on LTL truck runs and line-haul parcel flights, then pooling returns to minimize empty backhauls. Urban consolidation centers located within 30 kilometers of Antwerp, Brussels, and Liège shorten final-mile routes, diminish congestion fees, and meet municipal emission caps. Data-driven routing allows forwarders to present shippers with dynamic pricing tiers that adjust to delivery windows, giving small merchants cost visibility once reserved for enterprise clients.

EU Green Deal Accelerates Multimodal Transport Adoption

The Fit-for-55 package obliges a 55% cut in transport emissions by 2030; Belgian forwarders respond by shifting bulk chemicals, metal coils, and fast-moving consumer goods onto barge and rail lanes that run on renewable traction power. Sea-rail solutions using electric locomotives save shippers up to 260 grams CO₂e per km versus diesel trucks, data that forwarders now certify via blockchain audits to satisfy Scope 3 reporting. Grants for shore-power connections at Antwerp-Bruges further lower well-to-wake emissions, and logistics contracts increasingly include carbon-indexed rate adjustment clauses that reward modal conversion. The Belgium freight forwarding market positions these services as premium yet compliant offerings, leaning on EU funds that offset capital expenditures for low-carbon fleet upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labor and operating costs | -0.4% | Belgium, with EU-wide labor market pressures | Short term (≤ 2 years) |

| Driver shortage and aging workforce | -0.3% | Belgium, reflecting broader European trend | Medium term (2-4 years) |

| Port congestion and hinterland bottlenecks | -0.2% | Belgium, particularly Antwerp-Bruges corridor | Short term (≤ 2 years) |

| Low-water events on inland waterways | -0.1% | Belgium, Rhine-Scheldt basin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortage Constrains Capacity Expansion

Belgium lacks 17,000 truck drivers as of 2024, with an average driver age past 50, mirroring a European shortfall forecast to hit 2.6 million positions by 2030. The Belgium freight forwarding market cannot fully substitute technology for human operators, so capacity tightening pushes spot trucking rates up to 14% higher than the 2023 average. Forwarders invest in warehouse automation, drone yard checks, and simulator-based driver academies, but these mitigations deliver scale only in the medium term. Multimodal routing buffers some exposure, yet first-mile and last-mile legs still rely on truck assets. Higher labor costs compress margins and may curtail small forwarders’ ability to finance digital upgrades, prompting accelerated consolidation[3]“Transport Sector Labor Market Analysis 2024,” Belgian Federal Public Service Employment, EMPLOYMENT.BELGIUM.BE .

Port Congestion Limits Throughput Optimization

Peak-period truck dwell times at Antwerp-Bruges stretch to 45-60 minutes, while hinterland train slots experience 2-4-hour delays, especially on the busy Iron Rhine route. Forwarders must add buffer days to delivery schedules, diluting the benefit of fast ocean transits or customs automation. Shippers paying detention and demurrage charges lean on forwarders to negotiate relief, straining relationships and adding administrative overhead. Planned rail infrastructure, scheduled for completion by 2027, will ease bottlenecks, but present uncertainty still deters some time-critical cargo from routing through Belgium[4]“Manufacturing Sector Overview 2024,” Belgian Investment and Trade Agency, INVESTINBELGIUM.BE.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Sea Freight Dominance Reinforces Hub Strategy

Sea transport held 54.92% of the Belgium freight forwarding market share in 2024 and is projected to rise at a 3.73% CAGR to 2030 as direct Asia-Europe loops favor Antwerp’s deep-water terminals. The Belgium freight forwarding market size in sea freight terms expands as mega-vessels discharge containers scheduled for rapid transshipment onto rail and barge legs. Air freight constitutes roughly 25% of market revenue because pharmaceuticals and automotive electronics tolerate premium lift, though it represents less than 5% of tonnage. Rail and barge gain incremental share when the EU Green Deal prompts shippers to substitute lower-carbon corridors for medium-haul trucking. Transport integrators bundle carbon-offset certificates alongside routing proposals, transforming emissions accounting into a revenue stream.

Operational synergies intensify as the port authority’s digital twin enables synchronized berth planning, fostering collaborative forecasting among terminal operators and forwarders. Antwerp-Bruges’ LNG bunkering and onshore power supply help carriers comply with imminent fuel regulation, driving vessel calls away from ports that lag in alternative energy infrastructure. Consequently, the Belgium freight forwarding market secures long-term capacity agreements that keep base rates competitive despite volatile bunker surcharges. Forwarders also exploit extended gate programs that allow nighttime container pick-ups, minimizing daytime congestion and enabling driver shifts to align with regulated work-hour caps.

By End-User: Manufacturing Leadership Drives Industrial Logistics

Manufacturing contributed 34.70% to the Belgium freight forwarding market size in 2024, anchored by automotive assembly lines in Ghent and Brussels, petrochemical complexes along the Scheldt, and pharmaceutical clusters in Wallonia. The Belgium freight forwarding market integrates vendor-managed inventory programs for these plants, synchronizing inbound raw materials with line-side delivery windows to avoid production stops. Specialized ISO tanks, temperature-controlled containers, and GMP-certified warehouses strengthen the competitive moat for incumbents versed in sector-specific compliance. Although the segment’s growth moderates, its scale and stability underwrite investment in emerging services such as predictive maintenance analytics on reusable packaging assets.

Wholesale and retail trade is emerging as the fastest-growing vertical, expected to generate a 3.84% CAGR up to 2030 as cross-border e-commerce funnels consumer goods through Belgian hubs. Forwarders design omni-channel fulfillment solutions that consolidate SKU-level inventory for Benelux and northern French delivery within 24 hours of order placement. Dynamic slotting and robotic picking inside suburban distribution centers accelerate throughput, while returns management becomes a differentiator given the high return rates in online fashion. Agriculture, forestry, and fisheries add niche value via chilled reefer movements of Belgian chocolates, beer malt, and specialty pork to Asian markets, yet volumes remain limited relative to industrial freight.

Geography Analysis

The Belgium freight forwarding market tilts toward the Flemish region, where Antwerp-Bruges anchors the maritime cluster and intermodal corridors stretch north to Rotterdam and south to the Rhine basin. Proximity allows next-day truck service to Paris, Amsterdam, and the Ruhr Valley, giving forwarders predictable transit times over congestion-controlled routes. Coastal logistics ecosystems integrate petrochemical feedstock imports with export of refined products, generating round-trip flows that stabilize equipment utilization.

Wallonia complements the north by linking Liege’s multimodal center to north-south flows bound for Switzerland and Italy. Air cargo from Liege Airport, specializing in express shipments, entices freight forwarders targeting high-value electronics and e-commerce parcels. Government incentives in the Ardennes attract cold-chain warehouses that receive pharmaceutical cargo from Brussels Airport, distributing it into Germany within a same-day window.

Brussels operates as a specialized hub for diplomatic, aerospace, and medical consignments tied to EU institutions. Customs simplification via the Digital Single Market and NCTS Phase 5 extends Belgium’s reach, letting forwarders process a single electronic transit document for moves into 26 member states. This seamless regime reinforces the Belgium freight forwarding market’s appeal to shippers consolidating intra-EU flows under one logistics service provider.

Competitive Landscape

Global 3PLs dominate tender volumes, yet mid-sized regional forwarders hold niche positions in chemicals, perishables, and project cargo. The 2024 DSV-DB Schenker merger created the largest European logistics network, augmenting Belgian operations with accelerated modal integration and unified IT platforms. DHL Global Forwarding and Kuehne + Nagel compete on digital transparency, rolling out APIs that stream real-time container milestones into shippers’ enterprise resource planning systems. X-press Feeders and Tailormade Logistics cultivate specialized automotive and e-commerce lanes, capitalizing on familiarity with local regulatory nuances.

Technology adoption underpins differentiation: Internet of Things sensors monitor reefer integrity, while AI route engines slash empty miles. Antwerp’s port authority encourages data sharing through the D-HI digital marketplace, enabling forwarders to reserve rail slots two weeks out and synchronize appointment windows across terminals. Financial resilience gained through scale allows larger forwarders to guarantee capacity during peak season, attracting multinational shippers seeking cost certainty.

White-space opportunities persist in pharmaceutical cold chain where stringent GDP compliance narrows the field. H.Essers’ 2024 expansion of its Brussels facility positions the firm to handle temperature-sensitive vaccines, leveraging automated sortation and adjacent airside access. Smaller players, while agile, confront rising cybersecurity requirements and ESG reporting burdens that elevate fixed costs-factors intensifying consolidation prospects across the Belgium freight forwarding market.

Belgium Freight Forwarding Industry Leaders

DHL Group

DSV

GEODIS

H.Essers

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its EUR 14.3 billion (USD 15.6 billion) acquisition of DB Schenker, creating Europe’s largest logistics network with expanded Belgian coverage.

- March 2025: H.Essers expanded its Brussels healthcare logistics site by 15,000 sqm and announced a EUR 45 million (USD 52.21 million) terminal in the Netherlands to channel Belgian import flows.

- December 2024: Manuport Logistics invested EUR 25 million in automated container handling at Antwerp-Bruges, lifting throughput capacity by 30%.

- February 2024: Kuehne + Nagel introduced a dedicated China–Belgium rail service via Welkenraedt, offering 16-day transit from Shanghai.

Belgium Freight Forwarding Market Report Scope

| Air |

| Sea |

| Others |

| Oil and Gas, Mining and Quarrying |

| Construction |

| Manufacturing |

| Agriculture, Fishing, and Forestry |

| Wholesale and Retail Trade |

| Others |

| By Mode of Transport | Air |

| Sea | |

| Others | |

| By End-User | Oil and Gas, Mining and Quarrying |

| Construction | |

| Manufacturing | |

| Agriculture, Fishing, and Forestry | |

| Wholesale and Retail Trade | |

| Others |

Key Questions Answered in the Report

How large will Belgium freight volumes become by 2030?

The Belgium freight forwarding market size is forecast to reach USD 3.28 billion by 2030, up from USD 2.74 billion in 2025, delivering a 3.68% CAGR.

Which transport mode is growing fastest?

Sea freight leads both in scale and growth, expanding at a 3.73% CAGR through 2030 as Antwerp-Bruges captures Asian and intra-EU flows.

What segment offers the best growth prospect for forwarders?

Wholesale and retail trade, propelled by cross-border e-commerce, is projected to grow at 3.84% CAGR, outpacing traditional industrial sectors.

How is Belgium addressing the driver shortage?

Forwarders invest in automation, launch driver academies, and shift more tonnage to rail and barge corridors to mitigate the 17,000-driver shortfall.

Why are customs clearance times falling?

The April 2025 Inbound Release Platform automates document checks, cutting average clearance from 24 hours to 4 hours and enabling real-time status updates.

What role does sustainability play in contract awards?

Shippers increasingly mandate carbon-efficient routing; multimodal solutions and emissions-tracked services give Belgian forwarders a competitive edge under EU climate goals.

Page last updated on: