Market Overview

| Study Period | 2020 - 2031 |

|---|---|

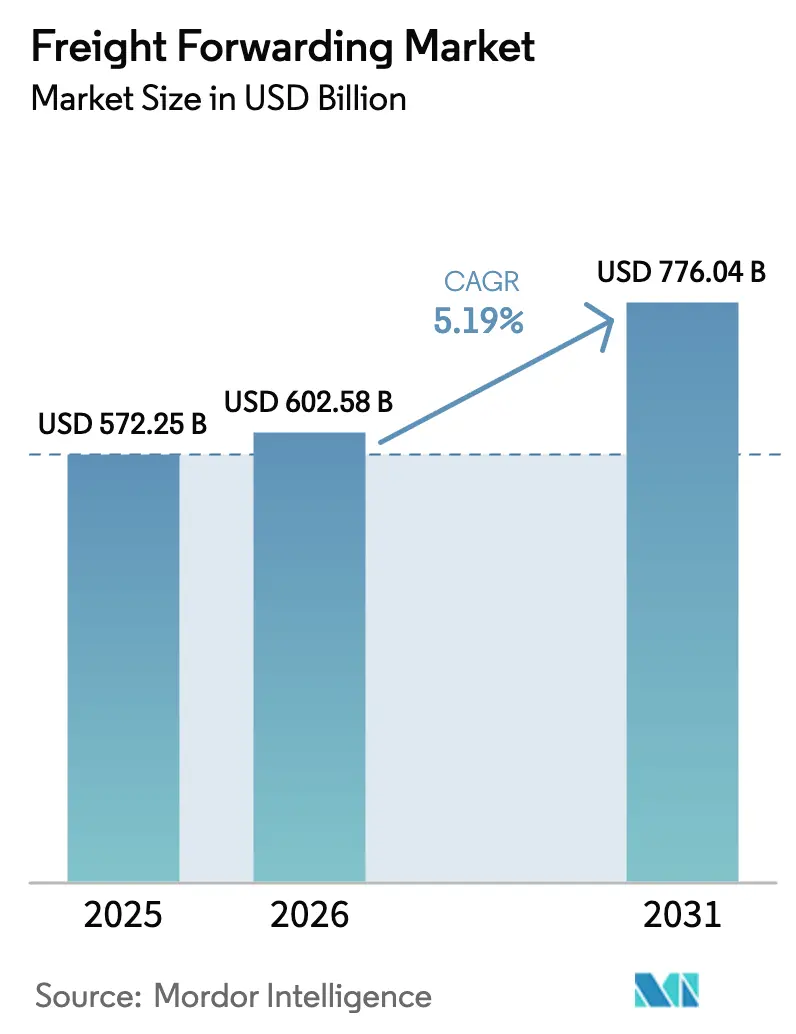

| Market Size (2026) | USD 602.58 Billion |

| Market Size (2031) | USD 776.04 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freight Forwarding Market Analysis by Mordor Intelligence

The Freight Forwarding Market size is expected to grow from USD 572.25 billion in 2025 to USD 602.58 billion in 2026 and is forecast to reach USD 776.04 billion by 2031 at 5.19% CAGR over 2026-2031.

Growth stems from the cross-border e-commerce parcel boom that fragments container loads, accelerating near-shoring mandates that compress lead times and expanding cold-chain corridors for biologic drugs and fresh food. Multimodal demand is widening as shippers combine ocean, rail, and air to bypass chokepoints, while digital-first platforms deliver instant quoting and transparency that reshapes carrier selection. Labor shortages in trucking and warehousing inflate execution costs in North America and Europe, but Asia-Pacific hubs continue to gain prominence as manufacturing shifts toward Vietnam, India, and Indonesia. Forwarders that blend asset-light networks with real-time visibility and carbon dashboards are positioned to unlock premium pricing and capture share in high-growth healthcare and e-commerce verticals.

Key Report Takeaways

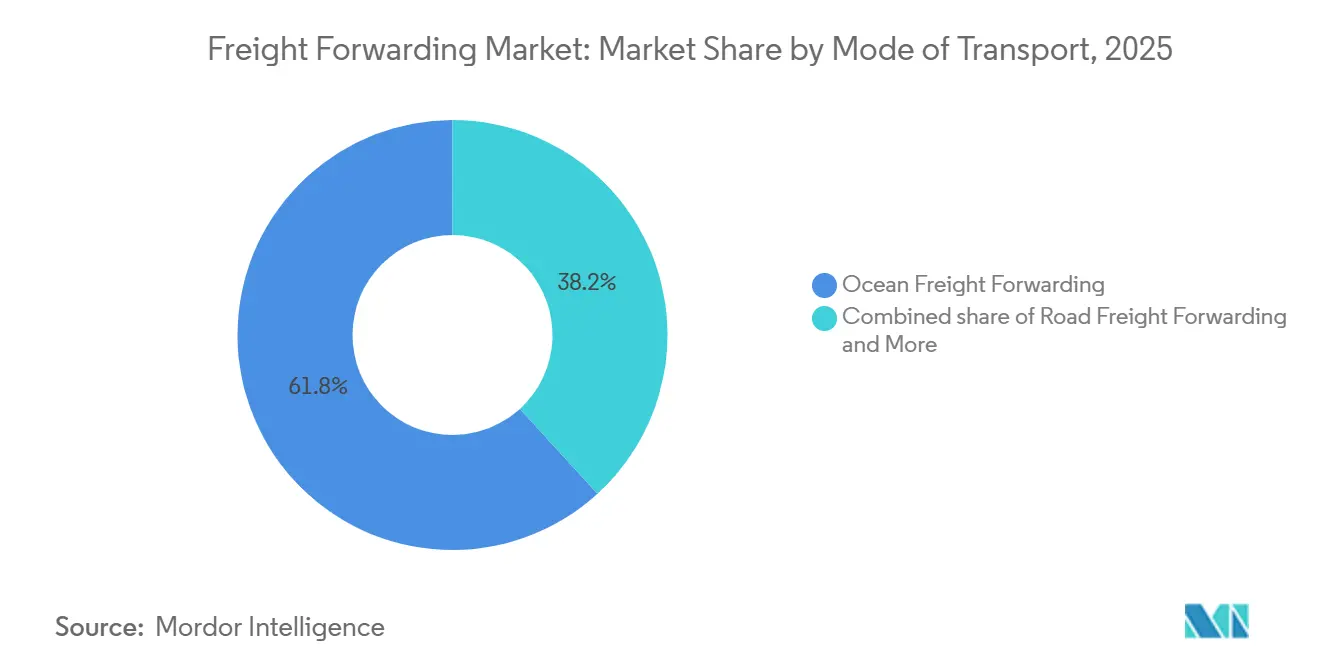

- By mode of transport, ocean freight forwarding held 61.77% of the freight forwarding market share in 2025, while multimodal and intermodal forwarding is advancing at a 6.40% CAGR between 2026-2031.

- By enterprise size, large enterprises accounted for 68.50% of the freight forwarding market size in 2025, yet small and medium enterprises are expanding at a 6.53% CAGR between 2026-2031.

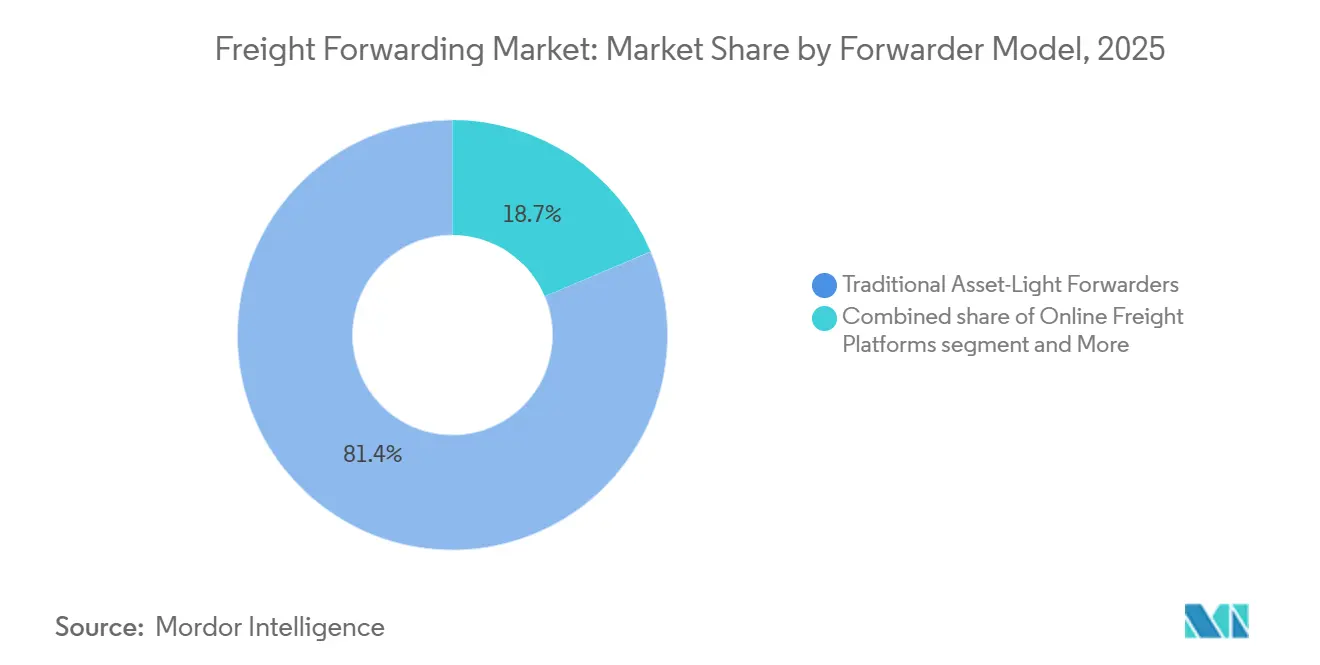

- By the forwarder model, traditional asset-light players retained 81.35% of revenue in 2025, whereas digital-first platforms are growing at a 17.84% CAGR between 2026-2031.

- By end-user industry, retail and e-commerce contributed 29.52% of 2025 demand, while healthcare and pharmaceuticals are the fastest-growing segment with an 8.50% CAGR between 2026-2031.

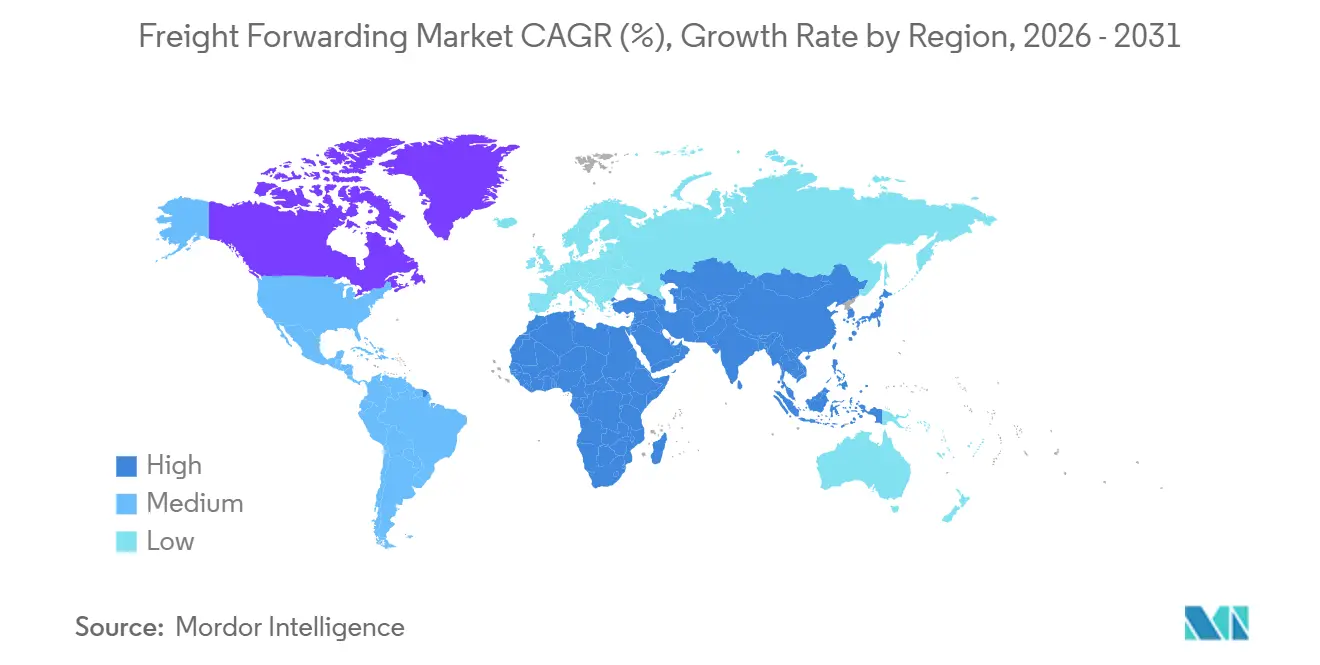

- By geography, Asia-Pacific controlled 36.49% of forwarding revenue in 2025 and is forecast to improve at a 7.80% CAGR between 2026-2031, outpacing North America and Europe.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Freight Forwarding Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border e-commerce parcel boom | +1.2% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| End-to-end shipment visibility adoption | +0.7% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Near-shoring and China-plus-one trade shifts | +0.9% | Asia-Pacific core with spill-over to Mexico and Central America | Long term (≥ 4 years) |

| Cold-chain investment for pharma and food | +0.6% | Global, led by North America and Europe | Medium term (2-4 years) |

| Shipper ESG targets and carbon pricing | +0.5% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Generative-AI dynamic load matching | +0.8% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-Border E-Commerce Parcel Boom

Global cross-border parcels reached 2.1 billion in 2024 and are expected to exceed 3 billion by 2027, fragmenting full-container traffic into small consignments that need rapid consolidation. Forwarders now build parcel hubs and last-mile alliances to uphold 48-hour delivery windows in Southeast Asia. Regulatory frameworks such as the World Customs Organization’s cross-border e-commerce standard drive investment in automated duty calculation that trims clearance delays. Providers unable to furnish real-time inventory visibility risk displacement by digital-native competitors. The freight forwarding market is therefore tilting toward flexible, data-rich operators that can optimize cost and speed simultaneously[1]“Cross-Border E-Commerce Framework,” World Customs Organization, wcoomd.org .

End-to-End Shipment Visibility Adoption

More than 12 million IoT container sensors were active in ocean trade by early 2025, feeding control-tower platforms that predict port congestion and customs holds. Machine-learning analytics help shippers re-route cargo before delays escalate, an advantage that cuts detention fees in temperature-sensitive pharma lanes. Blockchain bills of lading shorten letter-of-credit cycles and deter documentation fraud, yet widespread adoption is slowed by the need for carrier and customs interoperability. Forwarders that integrate these tools enhance trust and command premium rates in the freight forwarding market[2]“Pharmaceutical Logistics Outlook 2024,” International Air Transport Association, iata.org.

Near-Shoring and China-Plus-One Trade Shifts

Vietnam attracted USD 20.3 billion in manufacturing FDI during 2024, and India drew USD 84 billion in the same period, underscoring diversification away from single-country sourcing. Longer ocean transits are motivating multimodal solutions that blend ocean and rail to compress lead times. Inland depots in Vietnam and India allow pre-clearance that lowers dwell times and detention costs. Rail corridors such as the China-Europe Railway Express moved 1.8 million TEUs in 2024, supplying a middle-ground option between air speed and ocean cost. The freight forwarding market is reallocating capacity toward nodes that can pivot quickly as sourcing footprints evolve.

Cold-Chain Investment for Pharma and Food

Global cold-chain capacity added 23 million cubic meters in 2024, with pharmaceuticals accounting for 38% of new space. Biologic drugs, mRNA vaccines, and cell therapies require GDP-certified facilities and validated packaging, raising operational barriers and enabling price premiums. Fresh-produce exporters in Latin America and Africa depend on sub-5 °C corridors to uphold shelf life for avocados, berries, and seafood. IoT sensors feed blockchain audit trails to satisfy EU GDP and United States FSMA rules that demand continuous temperature records. Specialized providers, therefore, capture high-margin lanes within the freight forwarding market.

Restraints Impact Analysis of Freight Forwarding Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port congestion and container imbalances | -0.9% | Global, acute in North America, Europe, and Asia | Short term (≤ 2 years) |

| Global driver and warehouse labor shortage | -0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Geopolitical flashpoints and route risk | -0.8% | Global, concentrated in Red Sea, Suez Canal, and Black Sea | Short term (≤ 2 years) |

| Tightening de-minimis thresholds and compliance burden | -0.4% | North America and Europe, spill-over to Asia-Pacific e-commerce hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Port Congestion and Container Imbalances

Average dwell times at Los Angeles and Long Beach climbed to 6.2 days in early 2025, up from 4.8 days in 2023, while empty-container repositioning costs rose 22% in 2024. Structural imbalances create surplus boxes in import-heavy regions and scarcity in export zones, driving up detention fees. Inland depots and container-sharing pacts mitigate some expense, yet chassis shortages and rail yard congestion remain persistent bottlenecks that weigh on the freight forwarding market[3]“Port Performance Statistics,” Port of Los Angeles, portoflosangeles.org .

Global Driver and Warehouse Labor Shortage

The United States faced a deficit of 78,000 truck drivers in 2024, a shortfall expected to reach 160,000 by 2030. Warehouse turnover exceeded 40% in North America and Europe, spurring wage inflation and forcing investment in robotics that only large hubs can justify. Last-mile delivery is hit hardest, imperiling same-day promises for e-commerce parcels. Smaller forwarders without capital for automation remain exposed, limiting service quality in the freight forwarding market[4]“Driver Shortage Forecast,” American Trucking Associations, trucking.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Freight Forwarding Market Segment Analysis

By Mode of Transport:

Multimodal Solutions Accelerate FlexibilityOcean freight forwarding retained a 61.77% freight forwarding market share in 2025, driven by cost efficiency on dense lanes. Yet multimodal and intermodal forwarding is advancing at a 6.40% CAGR (2026-2031) as shippers balance speed, cost, and carbon impact. Less-than-container load volumes increase with e-commerce fragmentation, widening consolidation complexity. Road forwarding connects last-mile nodes, but driver shortages and fuel volatility tilt inland moves toward rail where infrastructure allows. Air forwarding protects semiconductor and pharmaceutical supply lines, although capacity caps and carbon surcharges temper growth. Rail corridors such as the China-Europe Railway Express offer 15- to 20-day transits that fill the gap between air and ocean.

The freight forwarding market is restructuring networks to blend ocean trunk haul with rail or air final legs, reducing buffer inventory without incurring full air premiums. Digital cost-time simulators guide mode selection based on stockout penalties and inventory carrying costs. Regulatory pressure from the IMO Carbon Intensity Indicator spurs modal shifts toward lower-emission combinations, especially for non-urgent cargo. Forwarders that orchestrate seamless handoffs and provide unified visibility capture share as shippers exit single-mode contracts.

By Enterprise Size:

Digital Platforms Propel SME PenetrationLarge enterprises contributed 68.50% of forwarding revenue in 2025, leveraging volume to negotiate contract rates, but SMEs are expanding at a 6.53% CAGR (2026-2031) as digital tools democratize access. Historically, SMEs lacked the scale to secure competitive pricing or manage customs intricacies. Platforms such as Flexport aggregate fragmented demand, provide instant quotes, and automate documentation, removing broker dependency and helping SMEs expand faster.

As the freight forwarding market evolves, large shippers still prize tailored solutions and account teams, yet they pilot digital dashboards to benchmark incumbent service. A two-tier dynamic emerges: SMEs value transparency and speed, whereas large accounts prioritize relationship continuity. Providers that deliver self-service portals alongside white-glove expertise can span both clusters, capturing incremental volumes without diluting service quality.

By Forwarder Model:

Digital Disruption Challenges Legacy BrokersTraditional asset-light forwarders controlled 81.35% of revenue in 2025, but digital-first platforms are rising at a 17.84% CAGR (2026-2031), offering API-driven pricing and real-time capacity. Online players automate quote-to-book processes, freeing shippers from email chains and manual phone calls. Hybrid asset-enabled forwarders balance owned warehouses and trucks with digital interfaces, providing service guarantees that pure brokers cannot match.

Legacy IT systems slow incumbent progress, yet investments in proprietary platforms such as C.H. Robinson’s Navisphere show determination to protect share. The freight forwarding market rewards operators that fuse long-standing carrier relationships with digital agility, while those who delay modernization suffer margin squeeze as transparency becomes a universal expectation.

By End-User Industry:

Healthcare Drives High-Margin ExpansionRetail and e-commerce generated 29.52% of forwarding revenue in 2025, still the largest slice of the freight forwarding market. However, healthcare and pharmaceuticals lead growth with an 8.50% CAGR (2026-2031), fueled by biologic approvals and cell-therapy commercialization that demand a stringent cold chain. Industrial manufacturing remains stable, relying on predictable ocean and rail services for just-in-time production. Food and beverage volumes grow on Latin American and African exports that must uphold sub-5 °C integrity. Automotive forwarding stabilizes as electric-vehicle battery moves to gain hazmat complexity. Chemical cargo faces capacity limits because of regulatory hurdles.

Forwarders specializing in healthcare deploy GDP-certified sites, validated packaging, and continuous monitoring, commanding higher yields. Others pursue volume strategies in retail, accepting thinner margins. Segment divergence drives strategic focus within the freight forwarding market as players weigh specialization against scale.

Geography Analysis

APAC Freight Forwarding Market

Asia-Pacific generated 36.49% of forwarding revenue in 2025 and is set to grow at a 7.80% CAGR between 2026-2031, the quickest regional climb in the freight forwarding market. China remains the largest single origin, yet Vietnam, India, and Indonesia collect rising investment under China-plus-one diversification. Singapore and Hong Kong anchor regional consolidations thanks to superior port efficiency and trade finance ecosystems. Japan and South Korea ship high-value electronics and automotive parts, while Australia ships bulk commodities and absorbs e-commerce imports.

North America Freight Forwarding Market

North America remains an import-heavy destination, but chronic port congestion and labor scarcity inflate handling costs. Shippers divert to Gulf and East Coast gateways and expand cross-border rail through Mexico under USMCA provisions. Canada’s forwarding flows align with energy and automotive trade, while Mexico benefits from near-shoring that relocates parts of electronics and auto production from Asia.

EMEA and South America Freight Forwarding Market

Europe holds a mature forwarding base centered on Germany, the Netherlands, and the United Kingdom. Brexit-induced customs friction and warehouse labor shortages moderate growth. Scandinavia and Central and Eastern Europe gain niche volumes through specialized corridors such as pharma and automotive parts. South America, the Middle East, and Africa account for smaller slices but rise as infrastructure upgrades and trade pacts improve connectivity, enlarging the freight forwarding market.

Regulatory Landscape

Freight forwarding is shaped by cross-border data, security, and transport rules that affect documentation, routing, and carrier selection across modes. In customs and trade facilitation, the World Customs Organization (WCO) provides global anchors through the SAFE Framework of Standards (2025 edition) and ongoing work on the WCO Data Model and e-commerce package tools, which push forwarders toward standardized electronic data exchange, risk management, and tighter supply-chain security controls for high-volume cross-border parcels.

On the transport and sustainability side, maritime compliance tightened with International Maritime Organization (IMO) rules entering into force from 1 January 2026, adding operational reporting and training requirements relevant to ocean-forwarding execution and carrier onboarding. National programs also influence forwarding flows and investment decisions: Japan approved its Comprehensive Physical Distribution Policy Outline (FY2026-FY2030) to promote logistics standardization and DX/GX, the United States Department of Transportation issued 2026 guidance on Multimodal State Freight Plans and State Freight Advisory Committees (via the Federal Register), and Vietnam adopted Decision 2229/QD-TTg (October 2025) setting a strategy for logistics services development that supports infrastructure and service modernization across key corridors.

Value Chain Analysis

The freight forwarding value chain starts with shippers (manufacturers, retailers, healthcare firms, and SMEs) defining service needs such as lead time, temperature control, and compliance. Forwarders then design and orchestrate the shipment across ocean, air, road, rail, and multimodal options, bundling carrier capacity procurement, consolidation (FCL/LCL and air consolidation), documentation, customs brokerage, cargo insurance facilitation, and value-added supply-chain services. Execution depends on an operating network that includes ocean carriers and airlines, trucking and rail operators, ports and terminals, bonded facilities, depots, and technology providers for booking, tracking, and data exchange.

Value capture concentrates in network design, carrier negotiations, compliance, and exception management, especially for fragmented e-commerce consignments and GDP or temperature-controlled healthcare moves that require validated processes and audit-ready records. Bottlenecks and cost leakages often show up at handoffs and nodes, including port and terminal operations, inland drayage capacity, and schedule reliability, which raises demand for multimodal routing and control-tower capabilities. As digital-first platforms spread, and as IoT tracking and standardized data sharing become more common, forwarders increasingly function as integrators that connect carriers, terminals, and customs processes into a single service layer.

Competitive Landscape

The top 10 forwarders captured an estimated 35% to 40% of global revenue in 2025, indicating a low-concentration freight-forwarding market. Competition intensifies as digital entrants leverage venture funding to scale carrier APIs and visibility tools, courting SMEs and mid-market shippers that prefer transparency over legacy relationships. DSV’s USD 15.1 billion purchase of DB Schenker in 2024 illustrates consolidation by incumbents seeking scale to match online rivals.

Forwarders deploy generative AI for dynamic load matching, optimizing container utilization, and forecasting port delays. C.H. Robinson processed 19 million shipments through its AI-enabled Navisphere in 2024, reinforcing that technology is now the primary differentiator. Shipper ESG goals spur investment in carbon dashboards and Sustainable Aviation Fuel contracts, forging a premium green tier within the freight forwarding market.

Incumbents holding multinational contracts defend share with global branch networks and customs expertise, while digital-first movers attract rapid-growth SMEs. The landscape therefore bifurcates into relationship-centric and technology-centric battlegrounds.

Freight Forwarding Industry Leaders

Kuehne+Nagel

DHL Group

C.H. Robinson

Expeditors International of Washington, Inc.

DSV A/S

- *Disclaimer: Major Players sorted in no particular order

Freight Forwarding Market Companies Covered in this Report

- A.P. Moller - Maersk

- C.H. Robinson

- CIMC Wetrans Logistics

- CMA CGM Group (including CEVA Logistics)

- DACHSER

- DHL Group

- DSV A/S

- Expeditors International of Washington, Inc.

- FedEx

- GEODIS

- Hellmann Worldwide Logistics

- Kerry Logistics Network, Ltd.

- Kintetsu World Express

- Kuehne+Nagel

- Lineage, Inc.

- LX Pantos

- Nippon Express Co., Ltd.

- Rhenus Logistics

- Sinotrans, Ltd.

- Toll Group

- Uber Freight LLC

- United Parcel Service of America, Inc.

- XPO, Inc.

- Yusen Logistics Co., Ltd.

Market Opportunities and Future Outlook

Standardized, interoperable cargo-data exchange is creating a modernization path for forwarders still reliant on email-driven workflows and duplicated data entry. In January 2026, IATA introduced the ONE Record standard to provide a common data framework across airlines, freight forwarders, and partners, and implementation activity is moving from pilots toward production-grade exchange. As these standards and broader e-documentation efforts mature, forwarders that connect operations to ONE Record and complementary eBL workflows can streamline document handling, strengthen shipment visibility, and improve exception management for high-value, time-critical air freight.

AI-enabled procurement and selling tools are also opening a whitespace for forwarders competing for SME and mid-market share while managing margins in volatile ocean and air markets. In May 2026, Yusen Logistics implemented cargo.one across global air freight sales and procurement operations, highlighting how digital operating systems can centralize rate management, automate quote-to-book workflows, and broaden access to carrier capacity. The same capability-based differentiation is broadening in specialized lanes including healthcare cold chain, secure transport for high-value goods, and multimodal corridors that align with China-plus-one sourcing shifts into Vietnam, India, Indonesia, and Mexico, where forwarders can bundle compliance, visibility, and controlled-handling services into higher-yield offerings.

Recent Industry Developments in Freight Forwarding Market

- June 2026: The acquisition of DeSpir Logistics by C.H. Robinson closed, adding secure transportation and cargo escort services for high-value freight in North America. This move expands mission-critical handling capabilities and broadens service breadth beyond standard brokerage moves.

- March 2026: The European Commission approved the joint venture between DHL eCommerce and Correios de Portugal (CTT), integrating DHL eCommerce Portugal operations into CTT Expresso and establishing cross-shareholdings in Iberia. The structure tightens last-mile and cross-border e-commerce connectivity in Spain and Portugal, a key demand center for parcel-driven forwarding and related value-added services.

- July 2024: The proposed acquisition by DSV of DB Schenker was announced for USD 15.1 billion, a major consolidation move among global forwarding incumbents. The transaction strengthens scale in air and ocean forwarding networks and increases competitive pressure on mid-sized forwarders through broader coverage and deeper procurement leverage.

Freight Forwarding Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the freight forwarding market is defined as the gross revenue earned by intermediaries that arrange cargo movement across ocean, air, road, rail, and multimodal routes, along with related coordination services like documentation, consolidation, and customs brokerage.

Scope exclusions: Dedicated parcel and CEP networks, pure trucking or warehousing-only contracts, and in-house shipper logistics teams are not counted in this market size.

Segments Covered in This Report

- By Mode of Transport

- Ocean Freight Forwarding

- Full Container Load (FCL)

- Less-Than-Container Load (LCL)

- Road Freight Forwarding

- Full Truck Load (FTL)

- Less-Than-Truck Load (LTL)

- Air Freight Forwarding

- Rail Freight Forwarding

- Multimodal and Intermodal Forwarding

- Ocean Freight Forwarding

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Forwarder Model

- Traditional Asset-Light Forwarders

- Digital-First / Online Platforms

- Hybrid Asset-Enabled Forwarders

- By End-user Industry

- Industrial and Manufacturing

- Retail and E-commerce

- Healthcare and Pharmaceuticals

- Oil, Gas and Energy

- Food and Beverages

- Automotive

- Chemicals

- Other End-users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Vietnam

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand and supply context for freight movement so later assumptions do not float without support. We review public trade and transport signals such as UN Comtrade, International Air Transport Association air cargo summaries, International Maritime Organization publications, and World Trade Organization trade statistics, followed by national customs and port authority throughput releases where available.

Next, the model is anchored with company disclosures and sector commentary that help interpret how forwarding revenue is formed and reported. Sources such as annual reports, investor presentations, association sites like FIATA, and credible business press are used to cross-check service mix trends (air vs ocean, and multimodal) and rate cycle narratives. Where needed, we also consult paid databases for company financials and intelligence, shipment-level import and export records, and global contracts and tenders to validate directionally. Examples are illustrative only, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk indicators cannot fully explain, especially how freight rates pass through into forwarder revenue and how much of total value comes from value-added services across different trade lanes. We spoke with freight forwarding executives, lane managers, and operations leaders across key shipper industries and major corridors, and then used their feedback to tune growth drivers and prevent double counting between forwarding and carrier services.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 17% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Our core build uses a top-down and bottom-up mix, where trade and transport activity is reconstructed by mode and major corridors and then translated into forwarding revenue using mode-level rate proxies and typical fee structures. To keep it grounded, the totals are corroborated with selective bottom-up approximations, such as sampled forwarder revenue roll-ups, channel checks on service mix, and volume times average revenue-per-shipment sanity tests for air and ocean.

Key inputs that were tracked include global merchandise trade value direction, container throughput and FCL vs LCL mix, air cargo ton-kilometers, capacity tightness indicators that influence spot and contract rate movement, and the share of time-sensitive shipments that usually lift air forwarding revenue. We also reflect adoption of multimodal forwarding and value-added services since documentation, brokerage, and consolidation can move differently than pure transport coordination.

For forecasting, scenario analysis is used alongside short time-series smoothing on the main activity indicators, and then the resulting revenue outlook is adjusted using expert consensus from interviews on rate normalization timing and lane rebalancing. Where bottom-up checks are incomplete (for example, limited disclosures in smaller geographies), gaps are handled through regionally consistent ratios tied back to trade flows and verified through follow-up calls.

Data Validation & Update Cycle

Validation is done in layers so one data series does not dictate the outcome. We compare the modeled market totals against independent signals like container and air cargo growth, trade value direction, and rate cycle movement, and then investigate any sharp variances before internal sign-off.

If a result looks off, assumptions that usually cause it, such as mode mix, currency conversion timing, or a step-change in forwarding take rates, are rechecked and corrected, followed by targeted re-contact with interviewees when needed. The report is refreshed annually, with interim updates made when material events occur, and a final pre-delivery review completed so clients receive the latest adjusted view.

Mordor Intelligence's Freight Forwarding Market Size Compared With Other Published Estimates

Published market sizes for freight forwarding can vary because teams do not always count the same revenue pool, and the same year label can hide different base assumptions. Differences usually come from what is included around brokerage and value-added services, whether parcel networks are counted, and how the freight rate cycle is treated in the base year.

By tracking trade and cargo activity by mode and refreshing how forwarding revenue links to rate and service-mix shifts, Mordor Intelligence avoids counting parcel and CEP networks and also keeps pure trucking and warehousing-only contracts outside the market total, which can materially change the reported number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 602.58 B (2026) | |

| Industry Publisher A | USD 229.80 B (2025) | Uses a smaller base-year capture that can reflect a narrower forwarding revenue pool, and its service buckets can overlap with transportation and warehousing lines, which affects comparability across years. |

| Research Publisher B | USD 192.50 B (2021) | Anchors on an earlier base year when freight rates and volumes were at a different point in the cycle, and broad service groupings can blend forwarding with adjacent logistics services, shifting the stated market value. |

The spread across sources is mostly explained by what revenue streams are counted as forwarding and how rate-cycle conditions are reflected in the base year. When the totals are tied back to mode activity indicators and checked with practical bottom-up sanity tests, the resulting market size is easier to replicate during annual refreshes.

Key Questions Answered in the Report

What is the projected value of the freight forwarding market in 2031?

The freight forwarding market is forecast to reach USD 776.04 billion by 2031, growing at a 5.19% CAGR (2026-2031).

Which mode of transport is expanding quickest within forwarding?

Multimodal and intermodal forwarding is the fastest-growing mode, advancing at a 6.40% CAGR between 2026-2031.

Why are SMEs gaining ground in forwarding spend?

Digital platforms aggregate SME shipments, provide instant quotes, and automate documentation, lowering barriers to entry and enabling 6.53% CAGR (2026-2031) growth among SMEs.

Which end-user segment shows the highest growth potential?

Healthcare and pharmaceuticals lead with an 8.50% CAGR (2026-2031) due to biologic and cell-therapy cold-chain requirements.

How is Asia-Pacific influencing global forwarding flows?

Asia-Pacific accounts for 36.49% of revenue and is expanding at a 7.80% CAGR (2026-2031) as production shifts toward Vietnam, India, and Indonesia under China-plus-one strategies.

What technology trends are reshaping competitive dynamics?

Generative AI for load matching, real-time shipment visibility platforms, and carbon-accounting dashboards are becoming essential differentiators among forwarders.

Page last updated on: