Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 51.43 Billion |

| Market Size (2031) | USD 118.12 Billion |

| Growth Rate (2026 - 2031) | 18.09% CAGR |

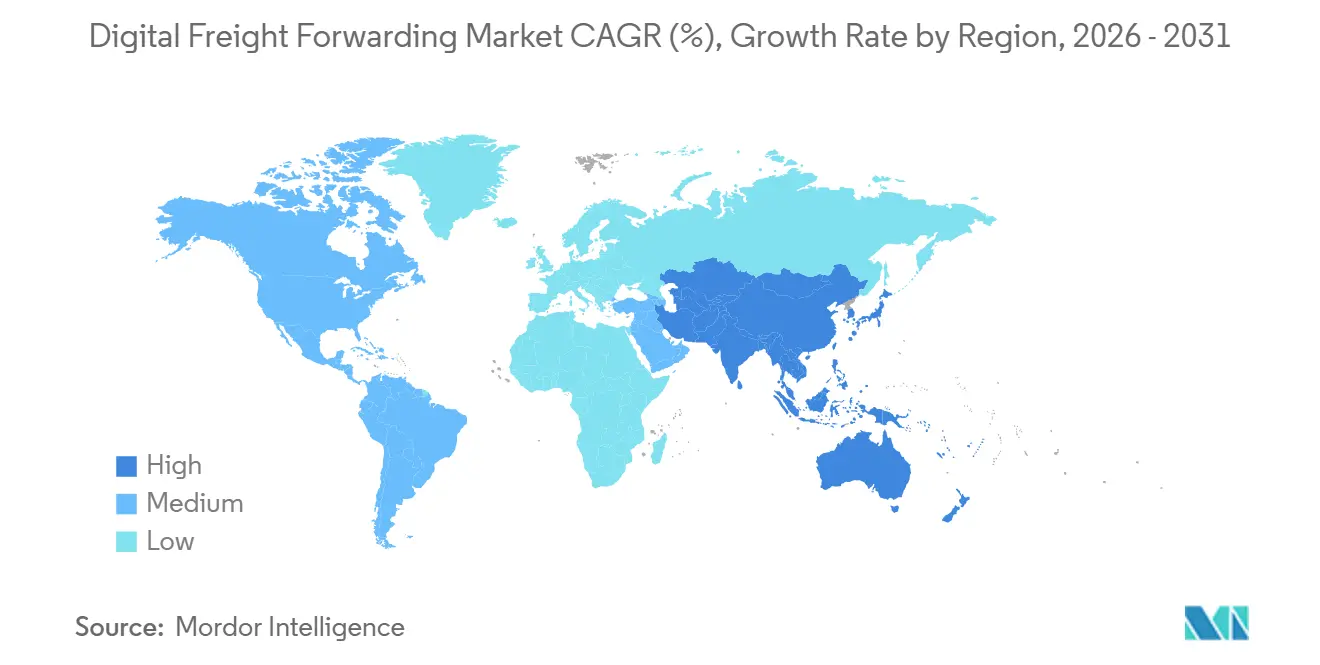

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digital Freight Forwarding Market Analysis by Mordor Intelligence

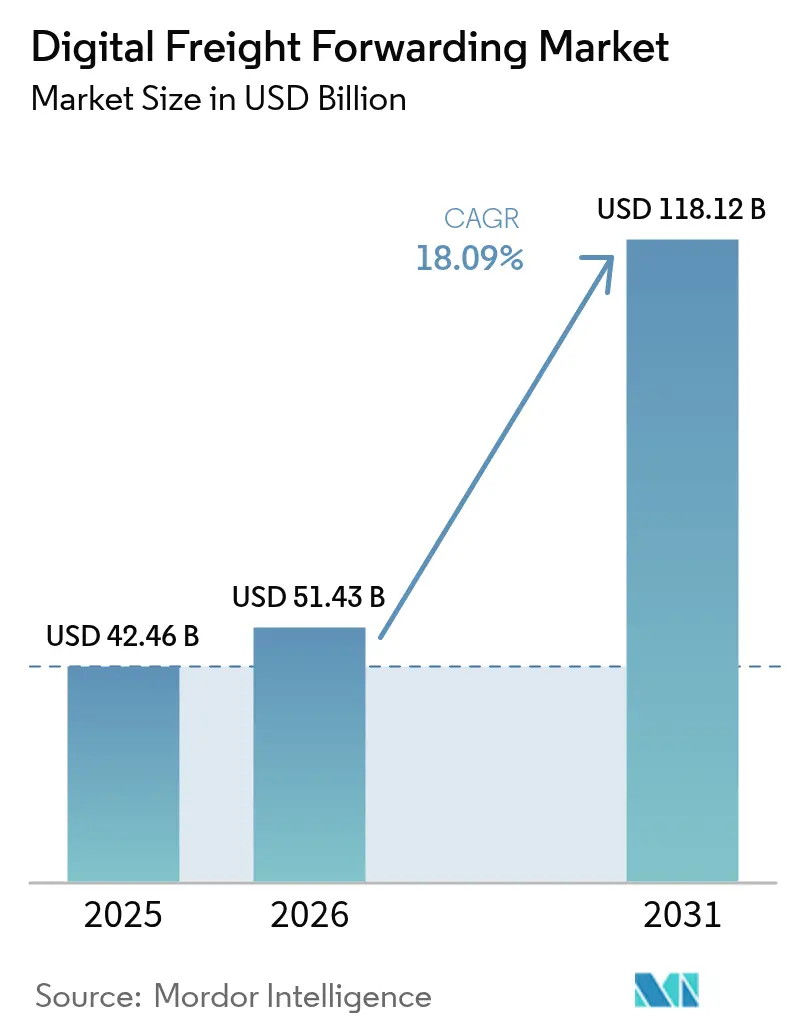

The Digital Freight Forwarding Market size is expected to increase from USD 42.46 billion in 2025 to USD 51.43 billion in 2026 and reach USD 118.12 billion by 2031, growing at a CAGR of 18.09% over 2026-2031.

Demand is moving toward platforms that solve visibility, documentation, and compliance gaps rather than pure mode switching, and that shift favors providers that automate workflows across booking, tracking, and customs. Small and mid-sized enterprises are accelerating adoption because subscription software and pooled capacity overturn scale disadvantages in pricing and process control. Regional momentum is strongest in Asia-Pacific, where infrastructure programs and multi-modal corridors create network effects for digital orchestration, while North America and Europe advance through nearshoring, intermodal hubs, and regulatory digitization. Functional differentiation is concentrated in value-added layers such as customs, sustainability reporting, and trade finance, which turn compliance into a repeatable service that complements transportation execution.

Key Report Takeaways

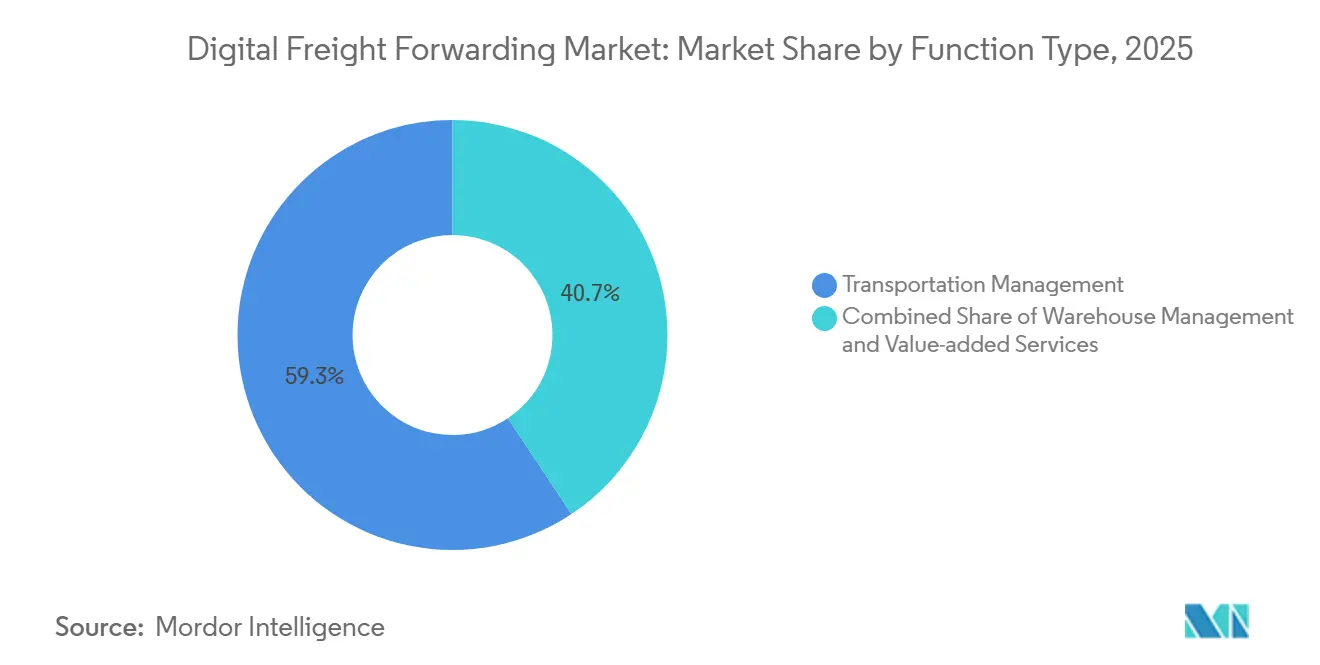

- By function, Transportation Management dominated the digital freight forwarding market share with 59.34% revenue in 2025, while Value-Added Services is projected to expand at a 16.21% CAGR through 2026-2031.

- By end-users, Retail and E-commerce accounted for a 35.64% share in 2025, reinforcing their strong position in the Digital Freight Forwarding Market Size.

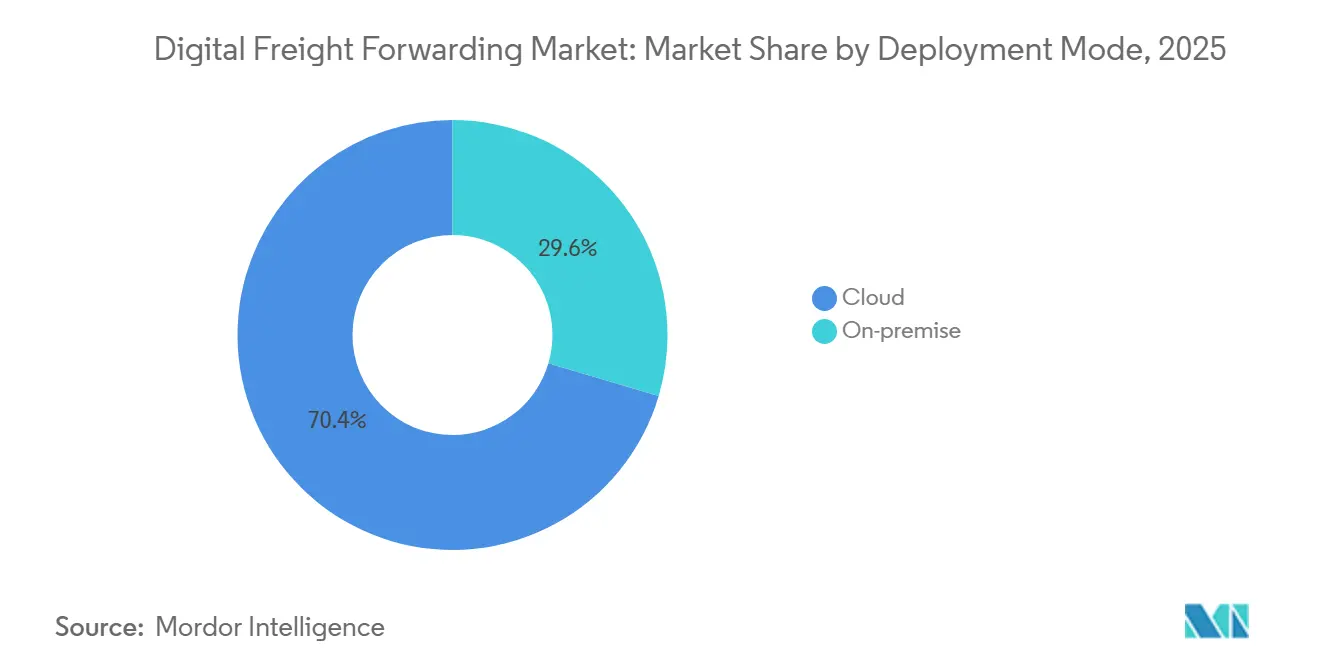

- By deployment mode, Cloud captured 70.43% share in 2025, while On-Premise is set to record a 19.23% CAGR through 2026-2031.

- By firm type, SMEs held a 60.27% share in 2025 and are projected to grow at a robust 17.45% CAGR from 2026 to 2031.

- By geography, Asia-Pacific led with 40.24% share in 2025 and is the fastest growing region at a 19.48% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for real-time visibility and tracking | +3.2% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Post-pandemic contactless logistics operations | +2.8% | Global core, residual gains in Southeast Asia and Latin America | Short term (≤ 2 years) |

| Blockchain-enabled transparency solutions | +2.5% | North America, EU, and tier-1 APAC markets | Long term (≥ 4 years) |

| Sustainability mandates and carbon reporting | +3.5% | EU leadership with spillover to North America and select APAC | Medium term (2-4 years) |

| Integration with multi-modal networks | +3.1% | Central Asia corridors, APAC-Europe lanes, North American intermodal hubs | Medium term (2-4 years) |

| Rising SME adoption of digital platforms | +2.9% | Global, led by EU, South Africa, and Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Real-Time Shipment Visibility and Tracking

Shippers expect continuous status updates and predictive exception alerts, which push platforms to deliver milestone-level tracking and proactive intervention for delays or disruptions. Visibility has moved from a customer service add-on to a core requirement that drives routing decisions, carrier selection, and contract renewals in the Digital Freight Forwarding market. As procurement teams standardize on API access to shipment events and estimated times of arrival, providers with granular data capture outperform peers that rely on manual updates. This focus expands the use of platform integrations across carriers, terminals, and customs systems to close gaps at mode handoffs. The result is wider adoption of control-tower architectures that centralize status, exceptions, and workflows for internal and external users in one place.

Post-Pandemic Acceleration of Contactless Logistics Operations

Digital booking, automated documentation, and self-service portals became standard in the pandemic phase and are now embedded in everyday operations. Companies that scaled these tools realized faster quoting cycles and fewer manual errors, which improved customer satisfaction and repeat bookings. In Vietnam, logistics firms reported sustained digital transformation between 2020 and 2024, including higher adoption of transportation and warehouse management systems that reduced process frictions. This experience reinforced the value of remote-ready workflows that uphold service levels during disruptions while lowering the burden on customer support teams. The same pattern appears in enterprise roadmaps where remote audits, electronic records, and digital signatures align with compliance and data-protection requirements.

Blockchain-Enabled Supply Chain Transparency Solutions

Tamper-resistant records for documents, milestones, and custody changes help reduce disputes and fraud exposure in high-value lanes such as pharmaceuticals and electronics. The technology’s role is expanding from proof-of-origin and bill-of-lading validation to near-real-time dashboards that link shipment events to sustainability and quality metrics. As multiple stakeholders share a synchronized ledger, billing and settlement processes shorten because discrepancies surface early and are supported by cryptographic evidence. The performance and cost profile still limits deployment to use cases where the value of trusted data is high and coordination complexity is acute. Over time, interoperability standards and integration maturity will lower barriers, making blockchain modules an option within broader freight platforms rather than standalone systems.

Integration With Multi-Modal Transportation Networks

Digital orchestration across ocean, air, rail, and road reduces re-keying and closes visibility gaps that often occur during transloads and border crossings. Shippers favor partners that manage trade-offs among transit time, price, reliability, and emissions for each leg of the journey, especially on Asia-Europe and North America cross-border corridors. Platform features like dynamic slot booking, schedule synchronization, and automated documentation raise on-time performance and reduce accessorials. Emerging air mobility and unmanned systems expand the definition of multi-modal for urgent and niche payloads, which calls for software that coordinates new feeder networks with conventional modes.[1]"ITS America, “Multimodal Technology Integration,” ITS America, itsa.org These capabilities increase the value of control towers and analytics that anticipate delays and re-plan routings in real time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment in technology infrastructure | -1.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Resistance from traditional incumbents | -1.2% | Fragmented markets such as U.S. and Southern Europe | Medium term (2-4 years) |

| Regulatory compliance complexity across jurisdictions | -1.5% | Cross-border corridors with differing rules | Long term (≥ 4 years) |

| Limited digital infrastructure in emerging markets | -1.0% | Sub-Saharan Africa, Central Asia, and tier-2/3 APAC cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment in Technology Infrastructure

Investment in TMS replacements, integration layers, and data foundations can strain mid-sized organizations that lack external funding sources. Companies often prioritize incremental rollouts that deliver targeted gains while deferring full-stack modernization. Evidence from Vietnam shows a wide distribution of digital investments with many firms deploying smaller budgets, which indicates phased adoption rather than single-step transformation. Parallel integrations with carriers, customs, and customers can inflate costs when standards vary by corridor and counterpart. This makes vendor selection and roadmap planning central to balancing near-term improvements with longer-term platform consolidation.

Resistance From Traditional Freight-Forwarding Incumbents

Cultural inertia and legacy processes can delay decision-making even when platforms demonstrate operational and financial benefits. Organizations that reward revenue capture over process efficiency can underinvest in digitization, which holds back automation of quoting, documentation, and exception workflows. Change programs succeed when leadership aligns incentives and training with new tools, so teams see direct gains in customer retention and margin. Firms that integrate digital modules into proven operations tend to advance faster because they leverage existing relationships and scale while raising service quality. The divide between adopters and holdouts shapes competitive dynamics in the Digital Freight Forwarding market as customers favor partners with consistent data and dependable service windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Platform-Orchestrated Logistics Supersedes Pure Transport

Transportation Management held the largest share at 59.34% in 2025, while Value-Added Services is the fastest-growing function at a 16.21% CAGR through 2031, indicating that margin pools are shifting toward compliance, brokerage, and financial workflows that wrap around core execution. The Digital Freight Forwarding market rewards platforms that layer customs brokerage, sustainability dashboards, and trade finance onto booking and tracking. This mix creates differentiation that pure carrier-rate arbitrage cannot sustain as pricing becomes transparent and standardized. Ocean remains the volume anchor within Transportation Management, while air gains when customers need shorter lead times, and land nodes support final-mile and cross-border complexity that demands orchestration. Warehouse Management benefits from real-time inventory monitoring and software-defined operations that connect robots and sensors with enterprise systems.

Value-Added Services scale as regulations and customer policies require documented emissions, quality checks, and traceability locked to each shipment. The fastest growth sits where compliance risk and coordination effort run high, which supports premium pricing for predictable execution. As functions converge into unified platforms, users prefer tools that keep documents, milestones, and exceptions in one workflow rather than across disconnected systems. The Digital Freight Forwarding market, therefore, ties transport planning to landed cost, compliance, and service-level adherence in a continuous cycle that is visible to all parties. This direction makes multi-functional orchestration a defining capability for leaders through the forecast period.

By End-Users: E-Commerce Volumes Plateau, Healthcare Margins Strengthen

Retail and E-commerce accounted for 35.64% of end-user demand in 2025, while Healthcare and Pharma are the fastest-growing end-users at an 11.12% CAGR as cold chain, quality, and traceability standards drive premium service needs. E-commerce is a large but price-sensitive category where providers win on network design, inventory positioning, and real-time tracking across final-mile nodes. Healthcare and Pharma require carefully validated processes and temperature monitoring tied to shipment records, which aligns with digital platforms that track every milestone. Manufacturing and Automotive contribute steady volume, but shifting production footprints and regulatory changes increase the value of digital customs and pre-clearance workflows.

Digital orchestration also supports sector-specific compliance, such as quality documentation in life sciences and traceability records in food and beverage. The Digital Freight Forwarding market continues to align productized workflows to the needs of each end-user group rather than one-size-fits-all tracking. Retail brands push for branded tracking and harmonized returns, while industrial shippers emphasize predictable transit and duty accuracy. Providers that standardize capabilities across these profiles at scale gain both cross-sell opportunities and higher renewal rates. This segmentation pattern reinforces how vertical context shapes adoption and spending.

By Deployment Mode: Cloud Dominance With On-Premise Resurgence in Regulated Verticals

Cloud captured 70.43% of deployments in 2025 and remains the default choice for scalability and time-to-value, while On-Premise is growing at a 19.23% CAGR, where data residency and audit control are non-negotiable. Cloud deployments lower upfront costs, accelerate upgrades, and standardize integrations with carriers and customs systems. These traits make cloud attractive for Retail and E-commerce as well as many mid-market shippers that prioritize speed and flexibility. In contrast, On-premises fits regulated environments such as defense or clinical logistics, where isolation, validation, and fine-grained control outweigh run-rate savings.

Hybrid approaches are also rising as firms place customer portals and visibility layers in the cloud while keeping core planning near enterprise systems for performance and compliance. The Digital Freight Forwarding market reflects this nuance as vendors build modular architectures that let customers mix cloud and on-premise by workflow. Over time, privacy and cybersecurity frameworks will influence deployment splits, but the need for configuration depth will ensure that on-premise remains relevant in select use cases. The main selection criteria will continue to be time-to-value, compliance assurance, and integration scale.

By Firm Type: SMEs Outpace Large Enterprises Through Platform Democratization

SMEs held 60.27% share in 2025 and are advancing at a 17.45% CAGR because pooled capacity and subscription pricing help them match the capabilities of larger incumbents without comparable capital budgets. Cloud-native tools deliver real-time rate shopping, automated documentation, and emissions reporting that customers now expect as standard features. Evidence from South Africa shows that logistics IT strengthens network effects and improves timeliness, which validates the SME case for adoption. As procurement criteria expand to include technical integration and sustainability, SMEs rely on platforms to satisfy these requirements and win larger contracts.

Large enterprises still control complex projects and sensitive cargo, yet they also contend with legacy systems and longer implementation cycles. This creates room for two-speed strategies that add modern TMS and visibility layers beside existing ERP and finance platforms. The Digital Freight Forwarding market supports this split with APIs and pre-built connectors that speed up onboarding and data exchange. Over the forecast period, SME momentum remains tied to accessible features and predictable pricing, while enterprise progress depends on modernization programs that consolidate tools without service disruption.

Geography Analysis

Asia-Pacific led with a 40.24% share in 2025 and is projected to grow at a 19.48% CAGR through 2031, supported by infrastructure programs, diversified trade lanes, and rising platform penetration that reinforce network effects in the Digital Freight Forwarding market. North America follows with demand shaped by nearshoring to Mexico and the need to orchestrate rail, road, and port capacity across cross-border nodes. Europe advances on the strength of regulatory digitization and sustainability mandates that formalize data capture and reporting in everyday logistics. Middle East and Africa and Latin America add growth from a lower base, with leading hubs investing in ports, free zones, and customs digitization to attract transshipment and regional distribution flows.

Within the Asia-Pacific region, adoption patterns vary by market maturity. China scales digital-forwarding platforms for large volumes while India’s fragmentation creates room for aggregators that unify trucking and intermodal capacity. Southeast Asian economies benefit from industrial shifts and regional agreements that encourage standardized customs processes and greater uptake of single-window systems. Japan and South Korea maintain high digitization with conservative change management, and Australia moves early on compliance reporting that supports platform-led transparency. These dynamics translate into consistent upgrades to tracking coverage, document automation, and platform integrations for cross-border moves.

North American dynamics concentrate on intermodal hubs and cross-border orchestration, where congestion and variability favor predictive planning and automated documentation. European markets balance cost pressures with investment in rail, inland waterways, and green corridors that reduce emissions and dependence on specific chokepoints. In each region, platforms that integrate bookings, tracking, and compliance into unified workflows help shippers standardize service and reduce exceptions. As these capabilities spread, the Digital Freight Forwarding market continues to shift share toward providers that bring reliable data into planning and execution decisions at scale.

Competitive Landscape

Competition features digital-native platforms that emphasize algorithmic pricing, API connectivity, and automation alongside incumbents that leverage global networks and relationships to retain high-complexity cargo. Platform-led differentiation centers on real-time visibility, automated customer workflows, and embedded compliance that improve service predictability and decrease manual exceptions. This split encourages hybrid models where incumbents invest in modular software and automation to match digital peers in everyday execution quality.

Evidence of platform scaling also appears in captive and partner-led ecosystems. Samsung SDS reported Cello Square subscriber growth to 24,625 companies across 36 countries in 2025 alongside strong platform revenue, underscoring how embedded demand can accelerate third-party expansion when capabilities meet market needs.[2]Samsung SDS, “Samsung SDS Financial Results,” Samsung SDS, samsungsds.com Select road-freight consolidators such as Sennder increased European scale by acquiring a large surface-transport operation in 2024, which reflects ongoing efforts to aggregate fragmented capacity in key lanes. These moves align with customer requirements for consistent coverage, standardized data, and unified service across borders.

Technology partnerships remain a core lever for speed and scale. Collaboration announcements in 2026 included managed transportation platforms that integrate real-time visibility and AI-driven workflows to improve planning and response, which is aligned with customer priorities across sectors.[3]Turvo, “Collaborative Transportation Management Enhances Supply Chains,” Turvo, turvo.com In parallel, leading carriers and integrators publish logistics insights that highlight the value of multi-carrier and intermodal orchestration, signaling continued demand for digital coordination across extended networks. Over the forecast horizon, the Digital Freight Forwarding market will reward participants who pair process reliability with configurable tools for compliance, emissions, and analytics at the shipment level.

Digital Freight Forwarding Industry Leaders

-

Flexport

-

Twill (Maersk)

-

Forto

-

Cello Square

-

InstaFreight

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung SDS showcased the ongoing expansion of its Cello Square digital logistics capabilities, with 2025 results reporting 24,625 company subscribers across 36 countries and strong platform revenue momentum

- February 2026: Alpha Zero Global Logistics partnered with Turvo to power a next-generation managed transportation platform featuring real-time visibility, automated workflows, and AI-integrated insights.

- December 2025: Maersk published intermodal and multi-carrier logistics trends for 2026, including the continued relevance of digital transformation for decision-makers and the growing role of integrated platforms in multi-modal optimization

- April 2025: DSV completed the acquisition of DB Schenker, creating the world’s largest freight forwarder with projected annual synergies and an accelerated integration timeline that now targets end-2026.

Global Digital Freight Forwarding Market Report Scope

Digital Freight Forwarding Market report provides insights on the market like Market Overview, Market Dynamics, Value Chain / Supply Chain Analysis, Investment Scenarios, Government Regulations and Initiatives, Technology Development in Online Freight Forwarding and Digital Platforms, Overview on E-commerce Logistics and Freight Forwarding, Value Propositions of E-platforms Vs Competitors and Industry Attractiveness - Porter's Five Forces Analysis. The report also covers geopolitical impact analysis on the market.

Furthermore, the report also provides company profiles with leading market players to understand the competitive landscape of the market.

By Function

| Transportation Management | Land |

| Sea | |

| Air | |

| Warehouse Management | |

| Value-added Services |

By End-users

| Retail and E-commerce |

| Manufacturing |

| Healthcare and Pharma |

| Automotive |

| Others |

By Deployment Mode

| Cloud |

| On-premise |

By Firm Type

| SMEs |

| Large Enterprises and Government Entities |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Function | Transportation Management | Land |

| Sea | ||

| Air | ||

| Warehouse Management | ||

| Value-added Services | ||

| By End-users | Retail and E-commerce | |

| Manufacturing | ||

| Healthcare and Pharma | ||

| Automotive | ||

| Others | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| By Firm Type | SMEs | |

| Large Enterprises and Government Entities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Digital Freight Forwarding market?

The Digital Freight Forwarding market size reached USD 42.46 billion in 2025 and is projected to reach USD 118.12 billion by 2031 at an 18.09% CAGR. These figures reflect strong adoption of platform-led orchestration and compliance-centric services.

Which regions are leading and growing fastest in Digital Freight Forwarding?

Asia-Pacific leads with 40.24% share in 2025 and is the fastest growing region at a 19.48% CAGR, supported by infrastructure programs and multi-modal corridors. North America and Europe also grow through intermodal upgrades and regulatory digitization.

Which customer segments are shaping demand most in Digital Freight Forwarding?

Retail and E-commerce accounts for 35.64% of 2025 demand, while Healthcare and Pharma shows the fastest expansion at an 11.12% CAGR due to cold chain needs and traceability requirements.

How are deployment choices evolving in Digital Freight Forwarding?

Cloud remains dominant with 70.43% share in 2025 due to scalability and faster rollout, while On-Premise is expanding at a 19.23% CAGR in regulated and latency-sensitive environments that require stronger data control.

What differentiates leading platforms in Digital Freight Forwarding?

Leaders integrate transportation execution with value-added services like customs, emissions reporting, and trade finance, and they offer unified visibility, API connectivity, and configurable compliance workflows that reduce exceptions and speed decisions.

Why are SMEs advancing faster than large enterprises in Digital Freight Forwarding?

SMEs benefit from subscription pricing, pooled capacity, and pre-built integrations that match large-enterprise capabilities without heavy capital budgets, which supports faster adoption and steady share gains within their lanes.

Page last updated on: