West Africa Freight And Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

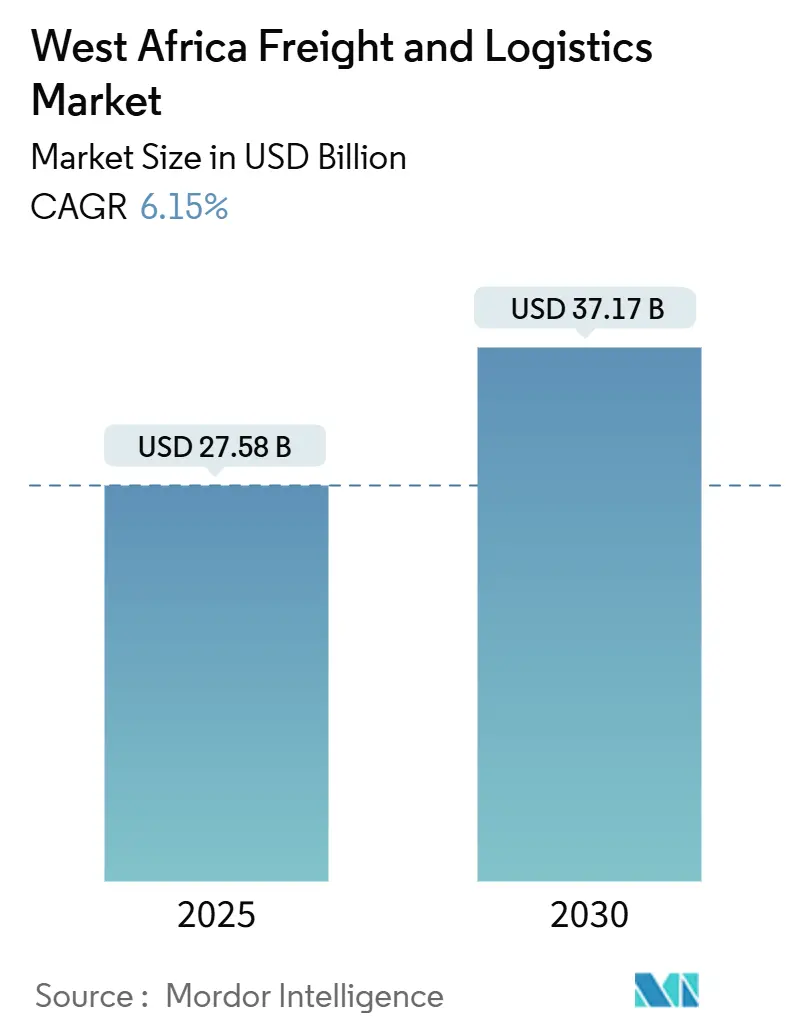

| Market Size (2025) | USD 27.58 Billion |

| Market Size (2030) | USD 37.17 Billion |

| Growth Rate (2025 - 2030) | 6.15% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

West Africa Freight And Logistics Market Analysis by Mordor Intelligence

The West Africa Freight And Logistics Market size is estimated at USD 27.58 billion in 2025, and is expected to reach USD 37.17 billion by 2030, at a CAGR of 6.15% during the forecast period (2025-2030).

The expansion reflects sustained infrastructure spending, AfCFTA-driven trade liberalization, and diversification of end-user demand across agriculture, retail, and petrochemicals. Nigeria anchors the region’s freight flows through its rehabilitated ports and the fully operational Dangote refinery, while Ghana’s petroleum hub and Tema-Ouagadougou corridor position it as the fastest-growing national market. Freight transport retains dominance due to the breadth of regional road networks, yet express delivery outpaces all other logistics functions as e-commerce penetration rises. Temperature-controlled warehousing records the highest facility investment momentum, mirroring the rise in agri-food exports and stringent quality requirements. Competitive differentiation increasingly hinges on digital freight platforms, multimodal service offerings, and strategic placement along the Abidjan-Lagos corridor.

Key Report Takeaways

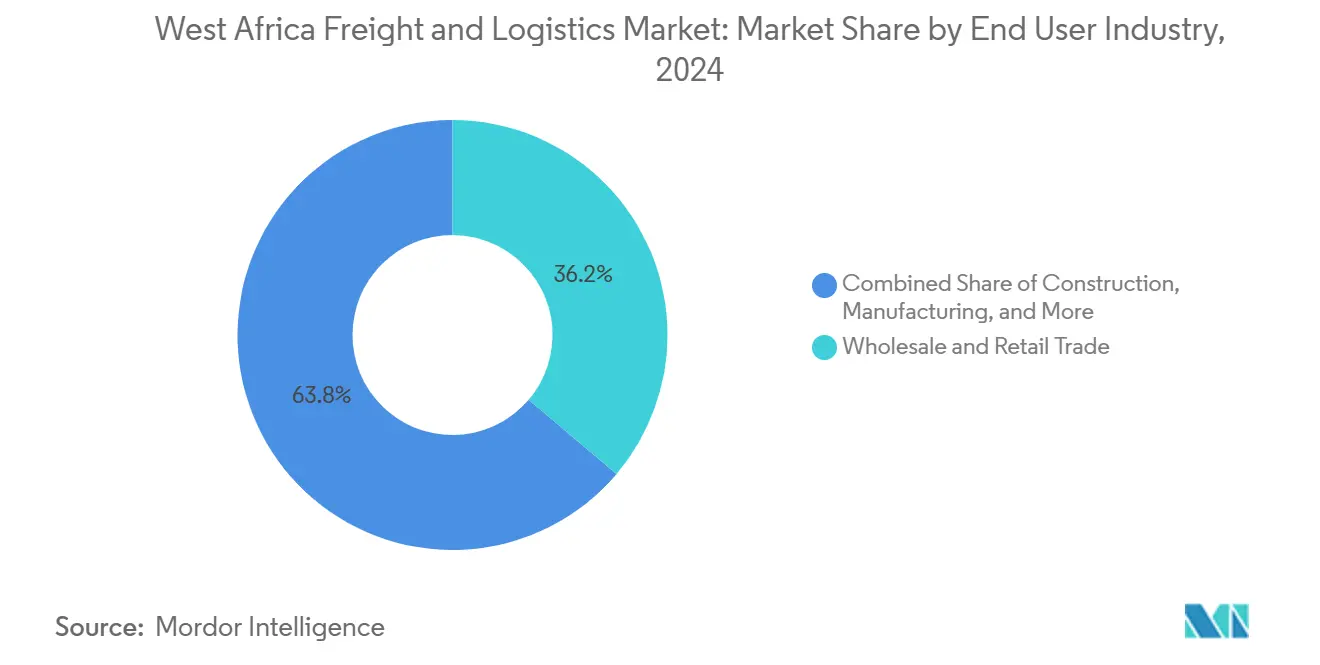

- By end-user industry, wholesale and retail trade commanded 36.19% of the West Africa freight and logistics market share in 2024 and is projected to grow at a 6.39% CAGR to 2030.

- By logistics function, freight transport held 61.22% of the West Africa freight and logistics market size in 2024; courier, express, and parcel services are advancing at a 6.88% CAGR to 2030.

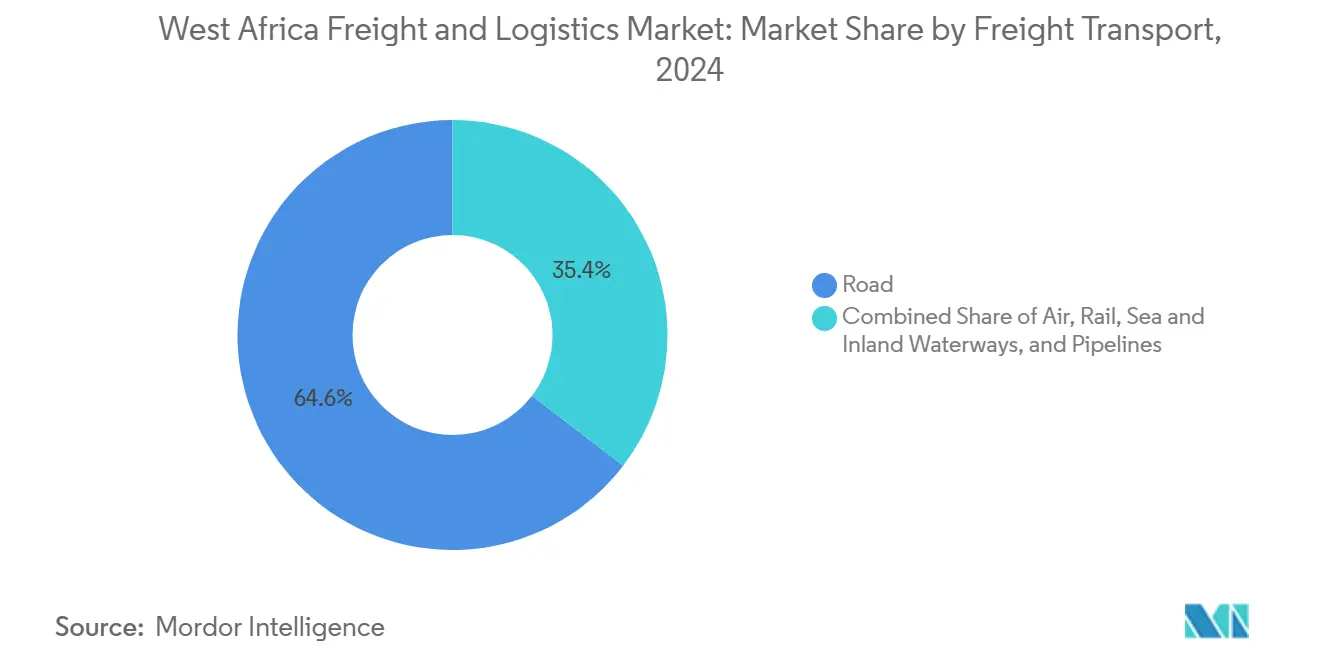

- By freight transport mode, road accounted for 64.58% of the West Africa freight and logistics market share in 2024, whereas air transport is poised to rise at a 6.61% CAGR through 2030.

- By CEP service, domestic deliveries controlled 64.12% of the West Africa freight and logistics market share in 2024, while international CEP is set to register a 6.82% CAGR between 2025 and 2030.

- By warehousing type, non-temperature-controlled facilities captured 91.38% of the West Africa freight and logistics market share in 2024, whereas temperature-controlled warehouses are growing at a 6.93% CAGR through 2030.

- By freight forwarding mode, sea and inland waterways freight forwarding contributed 61.29% of 2024 revenue and is expected to advance at a 6.33% CAGR between 2025-2030.

- By country, Nigeria led with 37.44% of the West Africa freight and logistics market share in 2024, while Ghana is forecast to expand at a 6.19% CAGR through 2030.

West Africa Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming intra-regional e-commerce | +1.2% | Nigeria, Ghana, Senegal | Short term (≤ 2 years) |

| AfCFTA-aligned infrastructure funding surge | +1.0% | Regional corridors, port cities | Medium term (2-4 years) |

| Petro-chemical project backlog clearance | +0.8% | Nigeria, Ghana, Senegal | Medium term (2-4 years) |

| Road corridor digital-tolling rollout | +0.6% | ECOWAS highway networks | Long term (≥ 4 years) |

| Cold-chain expansion for agri-food exports | +0.5% | Coastal exporters, inland producers | Medium term (2-4 years) |

| Gulf of Guinea port community systems uptake | +0.4% | Lagos, Tema, Dakar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming Intra-Regional E-Commerce

West Africa freight and logistics market benefits directly from surging digital commerce, which raises demand for last-mile delivery solutions and cross-border parcel flows. Mobile payment platforms processed USD 3 billion in 2024, providing seamless settlement infrastructure for merchants and logistics providers. Venture funding accelerated as logistics start-ups raised USD 50 million, led by OnePort 365’s EUR 4.7 million (USD 4.9 million) fundraising to digitize freight forwarding across Nigeria and Ghana[1]TechCrunch Reporter, “OnePort 365 raises €4.7 million,” TechCrunch, techcrunch.com. Improved urban road projects shorten delivery times, while integration of ride-hailing fleets into parcel networks optimizes asset utilization.

Surge in AfCFTA-Aligned Infrastructure Funding

The African Development Bank approved USD 170 million in 2024 for trade integration initiatives, catalyzing further public–private partnerships across key corridors[2]African Development Bank Communications, “AfDB approves US $170 million to boost AfCFTA,” AfDB, afdb.org. Flagship projects include the USD 15.6 billion Abidjan-Lagos highway, aimed at cutting transit times by 40% once completed in 2027. Railway upgrades such as Guinea’s USD 2.8 billion Conakry-Kankan line and Nigeria’s USD 1.3 billion Kano-Maradi link improve bulk freight economics. Funding inflows lift demand for heavy-lift forwarding, equipment leasing, and multimodal coordination services. The multiplier effect spans warehousing, road haulage, and ocean freight, reinforcing freight transport’s 61.22% share of the West Africa freight and logistics market size.

Petro-Chemical Project Backlogs Clear Post-COVID-19

Full start-up of Nigeria’s Dangote refinery in 2024 has reconfigured regional fuel trade lanes and created new offtake volumes for trucking and pipeline carriers[3]Reuters Staff, “Nigeria's Dangote refinery starts gasoline production,” Reuters, reuters.com. Ghana’s USD 12 billion petroleum hub adds further refining capacity, while Senegal’s offshore developments and the Greater Tortue Ahmeyim LNG venture inject specialized break-bulk and project cargo into coastal ports. Rising output bolsters the oil and gas, mining and quarrying end-user vertical, which is increasingly reliant on technically capable freight forwarders and temperature-controlled storage for petrochemical derivatives. Pipeline transport inches upward within the modal mix as refined-product movements shift from informal trucking to regulated networks.

Road Corridor Digital-Tolling Rollout

ECOWAS countries accelerate electronic tolling to improve fiscal capture and traffic flow, with Nigeria’s National Single Window reducing port clearance times[4]Nigeria Customs Service, “National Single Window Platform,” customs.gov.ng. Ghana’s TradeNet boosts customs integration, while Senegal digitizes Dakar port community systems to streamline gate throughput. Digital infrastructure supports real-time fleet tracking, predictive maintenance, and route optimization, amplifying road transport’s share of freight movements. Enhanced data visibility enables shippers to consolidate loads and reduce empty miles, reinforcing cost leadership for incumbents in the West Africa freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic port congestion & dwell times | –0.9% | Lagos, Tema, Dakar | Short term (≤ 2 years) |

| Fragmented customs regimes across ECOWAS | –0.7% | Border crossings, trade corridors | Medium term (2-4 years) |

| High transport-fuel subsidy volatility | –0.5% | Road transport operators | Short term (≤ 2 years) |

| Under-insurance of cargo and assets | –0.3% | Cross-border, high-value freight | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Port Congestion & Dwell Times

Average container dwell time at Lagos hits 21 days, seven times the global best practice, inflating freight forwarding costs. Tema and Dakar confront similar backlogs despite phased capacity upgrades. Vessel queues translate into demurrage surcharges, prompting shippers to favor transshipment hubs outside the region. Inefficiencies cascade into warehouse overflows and trucking delays, tempering the growth trajectory of the West Africa freight and logistics market.

Fragmented Customs Regimes Across ECOWAS

Disparate inspection protocols and documentation rules create clearance delays of 3–5 days at border posts. Non-interoperable IT systems force freight forwarders to duplicate data entry, eroding scale efficiencies. International CEP operators face service-level variability that undermines brand reliability, restraining the otherwise robust 6.82% CAGR in cross-border express parcels. Full ECOWAS Customs Union functionality is improbable before 2027, prolonging compliance friction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale Trade Drives Diversification

Wholesale and retail trade captured 36.19% of West Africa freight and logistics market share in 2024 and is projected to grow at a 6.39% CAGR through 2030 as modern retail formats expand across urban centers. Supermarket chains like Shoprite and Game increased outlet counts, generating demand for integrated distribution centers and frequent replenishment cycles. Manufacturing follows, buoyed by Ghanaian textile clusters and Nigerian FMCG plants seeking streamlined inbound raw-material flows and outbound finished-goods distribution. Agriculture, fishing, and forestry account for a rising portion of West Africa freight and logistics market size, propelled by increasingly stringent export quality protocols that necessitate cold-chain infrastructure.

Continued economic diversification under AfCFTA encourages vertical integration among logistics providers, enabling one-stop solutions that bundle warehousing, freight forwarding, and cross-border trucking. Integrated offerings resonate with wholesale distributors navigating complex regional sourcing patterns. The interplay between manufacturing output and retail demand reinforces steady volume growth across the ambient and cold chains, cementing wholesale trade’s leadership in the West Africa freight and logistics market.

By Logistics Function: Express Services Reshape Traditional Freight

Freight transport held 61.22% of the West Africa freight and logistics market size in 2024, supported by bulk commodity and containerized flows over road, sea, rail, and pipeline networks. Yet courier, express, and parcel services are expected to record the highest CAGR at 6.88%, reflecting e-commerce-driven small-parcel demand and corporate outsourcing of time-critical deliveries. International CEP grew 6.82% as uniform AfCFTA documentation protocols shortened clearance times. Warehousing and storage upgraded via automation and cold-chain investments, with temperature-controlled units expanding at a 6.93% CAGR.

Other services such as customs brokerage and supply-chain consulting evolve in response to regulatory complexity, adding higher-margin revenue streams for integrated players. Digitalization blurs functional boundaries: freight forwarders integrate online booking portals, CEP operators deploy trucking fleets for heavyweight parcels, and warehouse operators embed value-added kitting and labeling. Players able to orchestrate multimodal flows and provide end-to-end visibility stand to consolidate their share in the West Africa freight and logistics industry.

By Courier, Express, and Parcel: Cross-Border Growth Accelerates

Domestic CEP controlled 64.12% of segment revenue in 2024, propelled by urban e-commerce and on-demand delivery ecosystems across Lagos, Accra, and Dakar. Local players such as Red Star Express expand service reach through technology upgrades and strategic alliances, including partnerships with global air integrators. International CEP logs the highest CAGR at 6.82%, capturing business document flows and small-parcel cross-border trade.

Harmonized electronic customs filings reduce transit variability, while improved air connectivity boosts network reliability. Emerging digital freight marketplaces facilitate duty and tax calculations upfront, enhancing customer experience and accelerating shipment volumes within the West Africa freight and logistics market.

By Warehousing and Storage: Cold-Chain Revolution Unfolds

Non-temperature-controlled facilities comprised 91.38% of warehousing space in 2024, supporting consumer goods, construction materials, and industrial inputs. Yet temperature-controlled capacity is scaling fastest at 6.93% CAGR as exporters meet stringent quality and traceability standards for horticulture, seafood, and dairy. ColdHubs’ solar-powered units and LMI Holdings’ EDGE-certified warehouses illustrate localized and large-scale solutions alike.

Proximity to airports and processing zones optimizes turn-around for perishables, while value-added services such as blast freezing and ripening chambers create new revenue lines. Adoption of WMS and IoT sensors improves inventory accuracy and temperature compliance, reinforcing warehouse operators’ critical role in the expanding West Africa freight and logistics market.

By Freight Transport: Air Cargo Gains Despite Road Dominance

Road retained a 64.58% share within freight transport in 2024, leveraging the flexibility of ECOWAS highway networks and the ongoing USD 15.6 billion Abidjan-Lagos corridor construction. Sea and inland waterways followed, handling mineral exports and container traffic through Lagos, Tema, and Dakar. Rail’s revival—anchored by Guinea’s 1,400 km Conakry-Kankan line—improves the competitiveness of bulk commodity corridors.

Air transport, although smaller in volume, is forecast to grow at a 6.61% CAGR to 2030 on the back of perishables, pharmaceuticals, and high-value electronics. Pipeline transport capitalizes on refinery capacity, moving refined products across borders and easing road congestion.

By Freight Forwarding: Maritime Services Lead Integration

Sea and inland waterways made up 61.29% of freight forwarding revenue in 2024 and are projected to rise at a 6.33% CAGR as digitized port community systems drive efficiency. Air forwarding serves high-yield segments, benefiting from the region’s expanding cargo-dedicated apron space at Lagos, Accra, and Dakar airports. Multimodal and project cargo forwarding in the “Others” category grows alongside mining developments and large-scale infrastructure schemes.

Technology adoption—exemplified by OnePort 365’s end-to-end booking portal—bolsters transparency, helping shippers compare schedules and rates in real time. Forwarders integrating customs brokerage and inland trucking services reduce handoff points, mitigating border delays and compliance risks. This holistic approach supports scale advantages and reinforces maritime forwarding’s leading contribution to the West Africa freight and logistics market size.

Geography Analysis

Nigeria represented 37.44% of the West Africa freight and logistics market share in 2024, anchored by the Lagos port complex, which handles a significant portion of the national marine trade. The USD 1 billion port rehabilitation and the high-capacity Dangote refinery have created sustained inbound and outbound cargo demand. The USD 1.3 billion Kano-Maradi rail link further integrates northern Nigeria with Niger, enabling modal diversification and positioning the country as a regional logistics pivot.

Ghana records the fastest national CAGR at 6.19% through 2030 on the back of a USD 12 billion petroleum hub and the completed 97 km Tema-Mpakadan rail line, which improves hinterland connectivity for Burkina Faso’s trade. Port expansions at Tema raise container capacity, while economic diversification into manufacturing and services upgrades logistics sophistication.

Senegal and Guinea emerge as next-tier growth stories. Dakar port’s modernization and Senegal’s offshore hydrocarbon finds drive specialized freight and warehousing investments, aided by digital PCS deployment. Guinea’s 1,400 km Conakry-Kankan railway underpins bauxite exports, necessitating high-capacity transshipment yards and bulk-handling terminals. Côte d’Ivoire, Togo, and Benin collectively benefit from the Abidjan-Lagos corridor, enhancing cross-border trucking efficiency and contributing incremental volume to the West Africa freight and logistics market.

Competitive Landscape

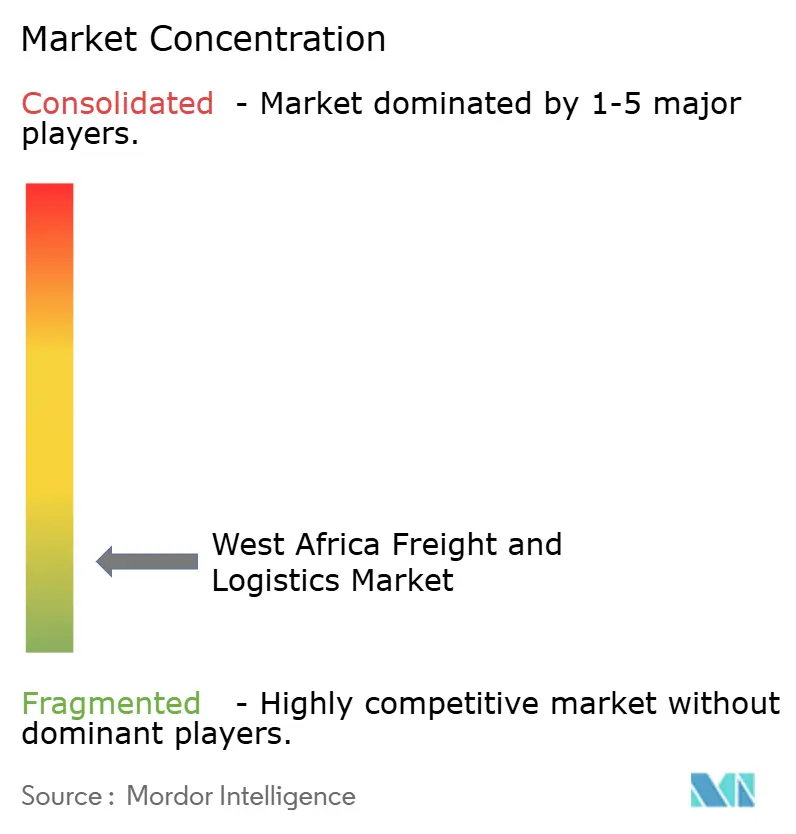

The West Africa freight and logistics market is fragmented, with national champions competing against global integrators that provide advanced IT and multimodal reach. Regional players leverage market intimacy, regulatory fluency, and localized assets, while international incumbents deploy scale and technology. Partnerships—such as SIFAX Group’s LCL collaboration with ECU Worldwide—demonstrate hybrid strategies blending local presence with global networks.

Digital freight platforms, warehouse automation, and track-and-trace solutions differentiate service offerings. Express operators upgrade sortation hubs and invest in electric delivery vans to meet urban emission mandates. Maritime forwarders integrate port community systems, while trucking fleets adopt telematics for fuel optimization.

Competitive intensity rises along the Abidjan-Lagos and Tema-Ouagadougou corridors, where traffic density offers economies of scale. Players capable of end-to-end orchestration and real-time visibility emerge as preferred partners for multinational shippers, shaping consolidation dynamics in the West Africa freight and logistics industry.

West Africa Freight And Logistics Industry Leaders

AGL (Africa Global Logistics)

DHL Group

CEVA Logistics

GIG Logistics

Sifax Global Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Red Star Express upgrades training facilities to enhance employee skill development, supporting service quality improvements.

- April 2025: DHL and Temu announce the rollout of joint fulfillment centers in Lagos and Accra to expedite cross-border deliveries.

- July 2024: CEVA completes Bolloré Logistics acquisition, enlarging its footprint in African air and ocean freight operations.

- June 2024: GIG Logistics teams with Travelstart to launch combined air-and-road ticketing, facilitating multimodal passenger and parcel transport.

West Africa Freight And Logistics Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| Nigeria |

| Ghana |

| Guinea |

| Senegal |

| Others |

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

| By Country | Nigeria | ||

| Ghana | |||

| Guinea | |||

| Senegal | |||

| Others | |||

Key Questions Answered in the Report

What is the current value of the West Africa freight and logistics market?

The market is valued at USD 27.58 billion in 2025.

Which country contributes the largest share to regional freight flows?

Nigeria holds 37.44% of regional market share due to its port capacity and refinery output.

Which logistics function is expanding most rapidly?

Courier, express, and parcel services are growing at 6.88% CAGR through 2030.

How fast is temperature-controlled warehousing expanding?

Cold-chain facilities are forecast to grow at a 6.93% CAGR between 2025 and 2030.

What corridor project will most influence future freight patterns?

The USD 15.6 billion Abidjan-Lagos highway aims to cut transit times by 40% once completed in 2027.

Which end-user industry currently drives the most logistics demand?

Wholesale and retail trade leads with 36.19% share of logistics spending.

Page last updated on: