Mexico Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.98 Billion |

| Market Size (2026) | USD 12.62 Billion |

| Market Size (2031) | USD 16.39 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

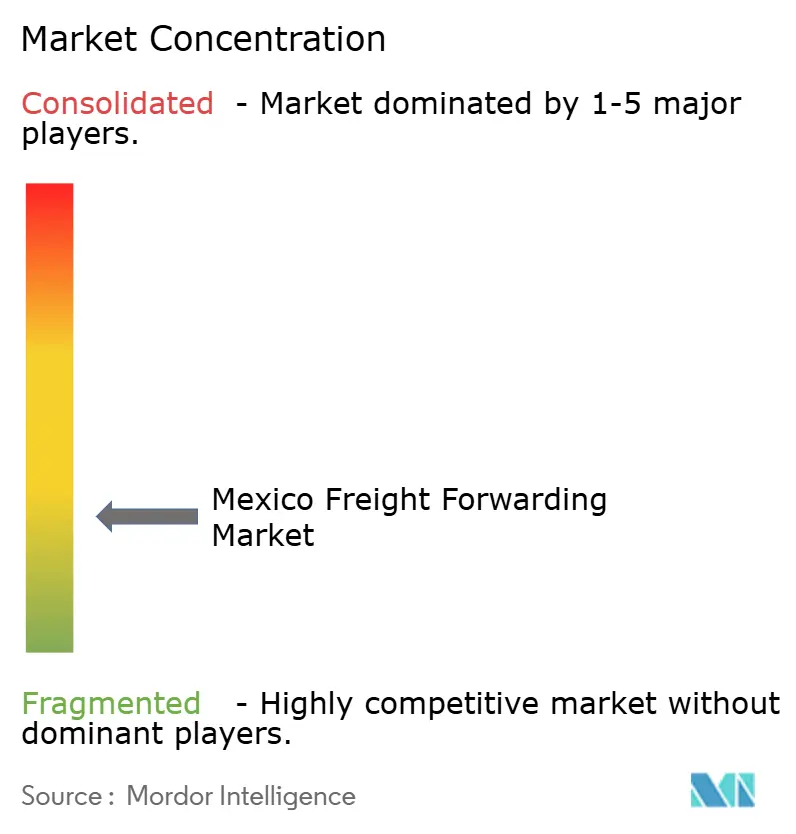

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Freight Forwarding Market Analysis by Mordor Intelligence

Mexico Freight Forwarding Market size in 2026 is estimated at USD 12.62 billion, growing from 2025 value of USD 11.98 billion with 2031 projections showing USD 16.39 billion, growing at 5.35% CAGR over 2026-2031.

Nearshoring-led manufacturing inflows, cross-border e-commerce acceleration, and continuing infrastructure upgrades across sea, air, road, and rail corridors underpin this market size expansion. Mexico became the United States’ largest trading partner in 2024, and the resulting freight volume growth is reinforcing competitive investment around Pacific gateways, Northern border intermodal hubs, and Bajío production corridors. Currency volatility, driver shortages, and rail congestion temper growth but do not outweigh structural demand stemming from OEM relocation, customs digitization, and regulatory incentives. Together, these elements sustain an environment in which technology-enabled forwarders deepen scale advantages while niche operators capture specialized opportunities.

Key Report Takeaways

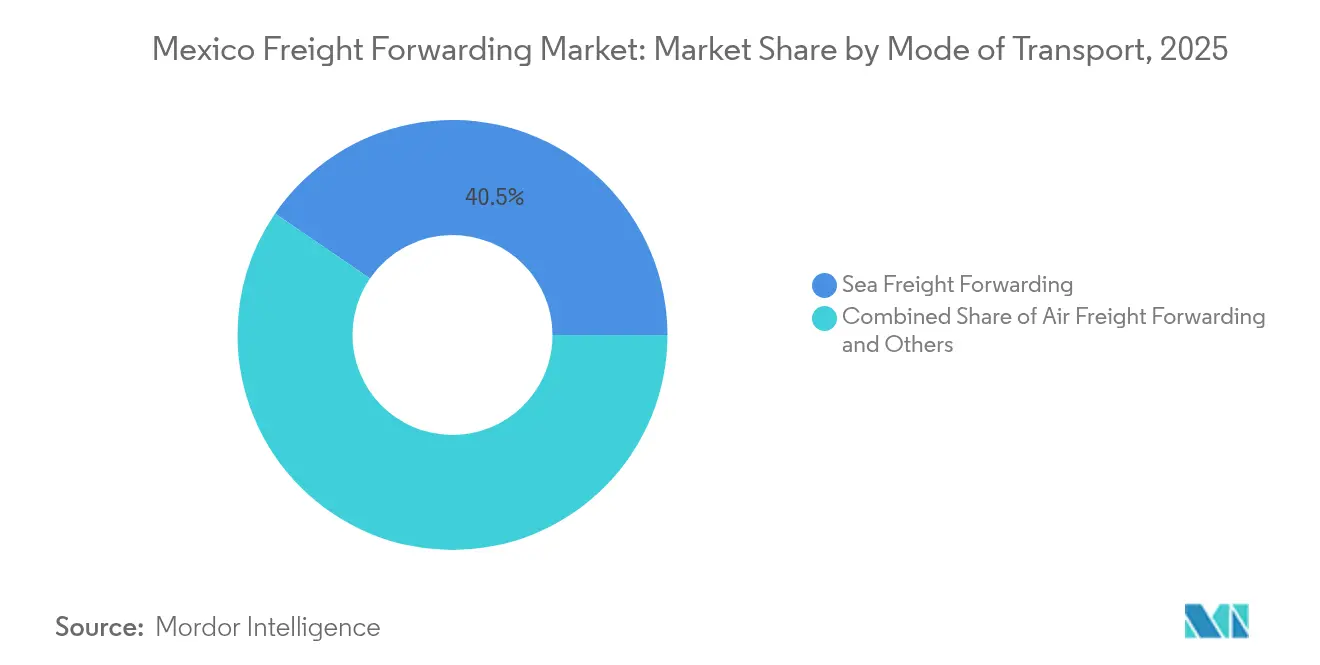

- By mode of transport, sea freight forwarding led with 40.45% market share of the Mexico freight forwarding market in 2025, while air freight forwarding is projected to grow at the fastest 5.38% CAGR through 2031.

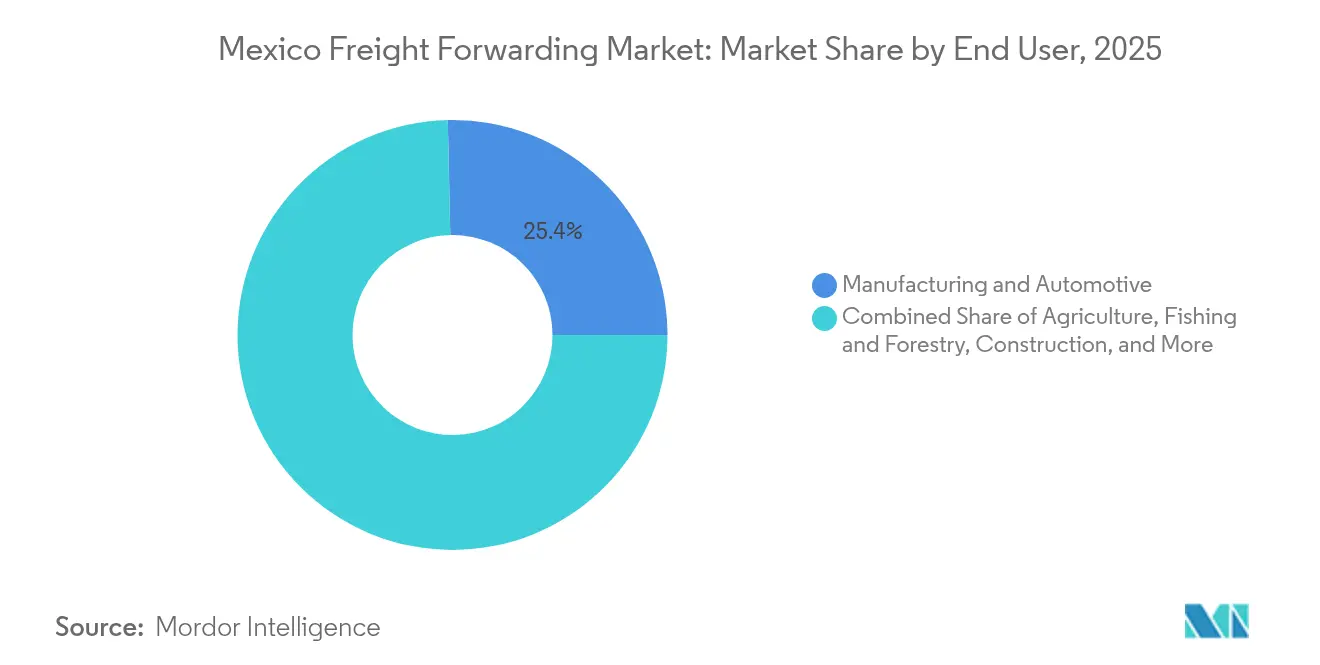

- By end user, manufacturing & automotive accounted for 25.35% share of the Mexico freight forwarding market size in 2025, whereas healthcare & pharmaceutical demand is advancing at a 4.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring driven export rebound | +1.8% | National, with concentrations in Bajío, Northern border states | Medium term (2-4 years) |

| USMCA-aligned customs reforms | +1.2% | US-Mexico border crossings, Pacific ports | Short term (≤ 2 years) |

| E-commerce parcel boom (cross-border) | +0.9% | Major urban centers, border logistics hubs | Short term (≤ 2 years) |

| OEM relocation of Tier-1 auto suppliers | +0.8% | Automotive corridors: Bajío, Nuevo León, Sonora | Medium term (2-4 years) |

| Multimodal corridors (Pacific ports to Bajío) | +0.6% | Pacific Coast, Central Mexico manufacturing zones | Long term (≥ 4 years) |

| Government green-freight incentives | +0.4% | National, with priority in industrial development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Near-shoring Driven Export Rebound

Manufacturing migration from Asia to Mexico is reshaping North American supply chains and underpinning a persistent rise in freight forwarding volumes. Investment commitments above USD 60 billion are scheduled to enter operation by 2027, and more than 450 new companies have opened facilities since 2024. Auto parts output, of which 87% is exported, relies on reliable just-in-time corridors that favor multimodal solutions bridging Pacific ports, Bajío plants, and U.S. assembly lines. Automotive production represented 21.7% of Mexico’s manufacturing GDP in 2024, and Tesla’s USD 5 billion Monterrey complex illustrates the scale of projects anchoring future flows. Freight forwarders with bonded warehousing and certified customs expertise are positioned to secure long-term contracts as OEMs and Tier-1 suppliers intensify local sourcing[1]Automotive Logistics, “Mexican powerhouse poised to grow,” automotivelogistics.media.

USMCA-Aligned Customs Reforms

The Complemento Carta Porte 3.0 mandate and IMMEX 4.0 certification scheme shorten clearance cycles and simplify documentation, enabling same-day inspections at Manzanillo and Lázaro Cárdenas. Automated risk profiles and electronic consignment tracking lower compliance costs and encourage modal diversification. Companies deploying API-based brokerage platforms now clear border entries in hours instead of days, translating into working-capital savings and higher trailer utilization. These gains reinforce market share for digital-first forwarders while compelling traditional brokers to accelerate technology upgrades.

E-commerce Parcel Boom (Cross-border)

Online retail spending surged in 2024, catalyzing double-digit parcel shipments across the U.S.–Mexico border. DHL’s USD 120 million Querétaro hub expansion created Latin America’s largest DHL Express center, lifting throughput capacity for next-day deliveries by 35%. Vertical logistics parks in Mexico City cut fulfillment lead times by 70%, and tariff-free thresholds under USMCA encourage rising small-parcel imports. Fulfillment providers are partnering with freight forwarders to integrate middle-mile capacity, linking airfreight uplift with local distribution in a single platform. These dynamics sustain premium yield growth, especially for time-definite air lanes.

OEM Relocation of Tier-1 Auto Suppliers

Vehicle output reached 3.8 million units in 2024, with 3.3 million exported. BMW’s San Luis Potosí plant sources from 250 regional suppliers using predictive scheduling and cross-docking analytics, cutting line-side inventory by 23%. Relocated Tier-1 suppliers trigger incremental cargo of batteries, interiors, and electronics, each requiring temperature, security, or hazardous-goods compliance. Freight forwarders that integrate insurance, origin consolidation, and bonded drayage capture higher-margin contracts, while carriers invest in specialized equipment fleets. The transition to electric vehicles intensifies demand for certified lithium-ion storage facilities and ADR-trained staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail network bottlenecks at border crossings | -0.8% | US-Mexico border crossings, key rail corridors | Medium term (2-4 years) |

| Driver shortage & high turnover | -1.1% | National, with acute impact in Tijuana, Ciudad Juárez, Monterrey | Short term (≤ 2 years) |

| FX-linked fuel-surcharge volatility | -0.6% | National, affecting cross-border operations | Short term (≤ 2 years) |

| Limited cold-chain infrastructure outside Tier-1 cities | -0.4% | Secondary cities, rural distribution networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rail Network Bottlenecks at Border Crossings

Eagle Pass and Laredo remain overwhelmed as rail volumes outstrip siding capacity. Average dwell times have risen by 18 hours year-on-year despite Kansas City Southern de México’s capital programs. The Green Eagle Railroad proposal, a 1.335-mile extension in Maverick County, still awaits multi-agency approvals, delaying relief. Delays ripple through just-in-time automotive chains, forcing expensive truck diversion. Forwarders build buffer stock in near-border warehouses, raising inventory carrying costs and complicating schedule reliability[2]Railway Age, “Petition for Exemption,” railwayage.com.

Driver Shortage & High Turnover

An estimated 56,000 long-haul driver vacancies persist across North America, and Mexico’s mandated 108% wage hike, effective March 2025, escalates cost pressure on small carriers. Higher pay has yet to curb attrition, with turnover topping 25% in Monterrey fleets. Insurance premiums, checkpoint delays, and rising fuel expenses squeeze margins, causing smaller operators to exit. Forwarders with captive or brokered capacity hedge risk through dedicated contracts and multimodal routing, but overall trucking elasticity remains tight, restraining market CAGR upside[3]Mexico Business News, “Mexico Trucking Faces Disruption After 108% Driver Salary Hike,” mexicobusinessnews.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Sea Freight Maintains Scale, Air Freight Accelerates

Sea freight retained a 40.45% Mexico freight forwarding market share in 2025, underlining its dominance in high-volume flows between Asia and Pacific ports. LCL solutions are gaining traction among mid-sized firms exploiting nearshoring benefits, whereas FCL remains steady for established manufacturers with predictable output. Carrier alliances introduced express Shanghai-Manzanillo loops with 15-day transits, providing a viable middle ground between air and traditional ocean schedules.

On the air side, network carriers expanded belly capacity at Mexico City Felipe Ángeles International Airport, while integrators invested in Querétaro uplift, propelling air lanes to the fastest 5.38% CAGR across 2026-2031. E-commerce parcels, high-value electronics, and urgent automotive components anchor demand, encouraging forwarders to negotiate block-space agreements and to deploy consolidation charters. Rail-truck multimodal, classified under “Others,” benefits from cross-border intermodal corridors and customs pre-clearance pilots that shave hours off door-to-door cycles. Collectively, these developments ensure modal diversity within the Mexico freight forwarding market and encourage integrated service offerings.

By End User: Manufacturing Leads While Healthcare Gains Momentum

Manufacturing & automotive captured 25.35% of the Mexico freight forwarding market size in 2025, driven by 3.8 million vehicle output and the relocation of Tier-1 suppliers to Bajío and northern clusters. Specialized freight, including tiered sequencing and just-in-time cross-dock, translates into higher revenue per kilogram versus commodity cargo. Plant expansions by Tesla, BMW, and Kia require consolidated inbound flows, propelling consistent demand for bonded transloading at border zones. Oil & gas, mining, and quarrying retain steady volume through heavy-lift equipment and bulk mineral exports, although energy diversification moderates long-term growth.

Healthcare & pharmaceuticals are forecast to outpace all peers at a 4.62% CAGR (2026-2031), thanks to multinational firms diversifying supply chains and stricter Good Distribution Practice enforcement. Cold-chain capacity shortages outside Tier-1 cities support premium pricing for validated lanes. Construction demand is tied to large-scale projects such as the Mayan Train, requiring inbound cement, steel, and machinery. Distributive trade, including wholesale, FMCG, and e-tailers, adds volatility but high frequency, benefiting forwarders that combine less-than-truckload, parcel, and returns management into unified contracts. Emerging telecom and renewable-energy cargoes inject oversize and high-value movements, increasing insurance and compliance complexity within the Mexico freight forwarding industry.

Geography Analysis

Pacific Coast hubs account for the bulk of maritime throughput, with Manzanillo handling 3.5 million TEU in 2024 and set to reach 10 million TEU by 2030 following its USD 3 billion upgrade. Lázaro Cárdenas operates Mexico’s largest customs facility and semi-automated quay cranes, delivering same-day inspections and absorbing spillover from Asian shipping routes. Together, these ports underpin regional sea-rail solutions that feed Guadalajara and Bajío factories, lowering inland freight costs by up to 12%.

Northern border states register the fastest growth trajectory within the Mexico freight forwarding market, buoyed by nearshoring and cross-border assembly. Laredo, El Paso, and Eagle Pass concentrate truck and rail intermodal flows, while new dry ports in Nuevo León integrate bonded warehousing with value-added services. Vacancy in Class A industrial parks along the Monterrey–Saltillo corridor fell below 2% in 2024, reflecting sustained demand for export-oriented logistics real estate. Rail congestion remains a bottleneck, however, prompting forwarders to diversify routing through smaller crossings and to leverage expedited drayage programs.

Competitive Landscape

Global integrators and multinational forwarders continue to deepen scale through acquisition and technology investment. UPS’s purchase of Estafeta adds domestic parcel density, while Hub Group’s partnership with Easo creates North America’s largest US-Mexico intermodal offering. Deutsche Post DHL Group, Kuehne + Nagel, and DSV reinforce positions in premium air and express sectors by deploying predictive analytics, IoT tagging, and automated brokerage. Regional specialists such as Solistica and Traxión counter by focusing on automotive sequencing, last-mile e-commerce, and time-critical shipments, often through joint ventures with OEMs or retailers.

Technology adoption differentiates service propositions. Digital platforms integrating rate quotation, cargo visibility, and customs compliance deliver cost transparency and reduce administrative cycles. Companies investing in blockchain for document verification and in machine learning for capacity forecasting report lower detention and demurrage charges. Forwarders lacking capital for digital transformation face margin compression as shippers migrate toward data-rich providers. Cold-chain expansion beyond Tier-1 metros remains a white-space opportunity; firms with multimodal temperature-controlled networks can command premium yields while benefiting from sparse competition.

Market fragmentation persists, yet consolidation accelerates as rising compliance costs pressure smaller brokers. Private-equity interest in freight tech start-ups fuels innovation around real-time multimodal marketplaces, dynamic routing, and embedded financial products. Still, regulatory hurdles—CTPAT certification, Mexico’s Authorized Economic Operator (OEA) program, and evolving hazardous-materials rules—create barriers that insulate established players. Overall, the Mexico freight forwarding market exhibits moderate concentration, balanced between global incumbents and agile regional operators.

Mexico Freight Forwarding Industry Leaders

Deutsche Post DHL Group (DHL Global Forwarding)

Kuehne + Nagel International AG

DSV A/S

Traxión

Expeditors International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Grupo Traxion acquired Solistica for MXN 4.04 billion (USD 213.3 million), strengthening domestic 3PL capabilities.

- July 2025: DP World opened a freight forwarding hub in Mexico City to meet surging cross-border demand.

- June 2025: Kuehne + Nagel inaugurated a 363,000-sq-ft consolidation facility in El Paso to streamline El Paso-Juárez flows.

- April 2025: DHL completed a USD 120 million expansion of its Querétaro air hub, now the largest DHL Express center in Latin America.

Mexico Freight Forwarding Market Report Scope

Freight forwarding is the strategic planning and execution of logistics for the international movement of commodities on behalf of shippers. A freight forwarder, for example, will handle freight rate negotiations, container tracking, customs documentation, and freight consolidation, among other things.

The Mexico freight forwarding market is segmented by mode of transport (air freight forwarding, ocean freight forwarding, road freight forwarding, rail freight forwarding), by customer type (B2C and B2B), and by application (industrial and manufacturing, retail, healthcare, oil and gas, food and beverages and other application).

The report offers market size and forecast values (USD) for all the above segments.

| Air Freight Forwarding | |

| Sea Freight Forwarding | Full-Container-Load (FCL) |

| Less-than-Container-Load (LCL) | |

| Others |

| Manufacturing & Automotive |

| Oil & Gas, Mining & Quarrying |

| Agriculture, Fishing & Forestry |

| Construction |

| Distributive Trade (Wholesale/Retail, FMCG) |

| Other End Users (Telecom, Pharmaceutical, etc.) |

| By Mode of Transport | Air Freight Forwarding | |

| Sea Freight Forwarding | Full-Container-Load (FCL) | |

| Less-than-Container-Load (LCL) | ||

| Others | ||

| By End User | Manufacturing & Automotive | |

| Oil & Gas, Mining & Quarrying | ||

| Agriculture, Fishing & Forestry | ||

| Construction | ||

| Distributive Trade (Wholesale/Retail, FMCG) | ||

| Other End Users (Telecom, Pharmaceutical, etc.) | ||

Key Questions Answered in the Report

How large is the Mexico freight forwarding market in 2026?

It is valued at USD 12.62 billion and is forecast to reach USD 16.39 billion by 2031 at a 5.35% CAGR.

Which mode of transport holds the biggest share in Mexican forwarding?

Sea freight leads with 40.45% revenue share, supported by rising Asia–Pacific container flows through Manzanillo and Lázaro Cárdenas.

What end-user sector drives the greatest forwarding demand?

Manufacturing & automotive contributes 25.35% of market value thanks to robust vehicle and components exports to the United States.

Why are air lanes growing faster than other modes?

Cross-border e-commerce parcels and time-critical automotive components are raising airfreight volumes, supporting a 5.38% CAGR for air forwarding.

What is the main infrastructure project to watch?

The USD 3 billion Manzanillo port expansion will quadruple capacity to 10 million TEU by 2030, reshaping Pacific gateway dynamics.

How is nearshoring influencing the forwarding landscape?

Relocation of OEMs and Tier-1 suppliers from Asia to Mexico is driving sustained export growth and spurring investment in multimodal corridors and customs digitization.

Page last updated on: