Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 31.62 Billion |

| Market Size (2026) | USD 33.13 Billion |

| Market Size (2031) | USD 41.86 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Freight Forwarding Market Analysis by Mordor Intelligence

The ASEAN Freight Forwarding market size is expected to grow from USD 31.62 billion in 2025 to USD 33.13 billion in 2026 and is forecast to reach USD 41.86 billion by 2031 at 4.78% CAGR over 2026-2031.

Cost-competitive manufacturing, rapidly expanding cross-border e-commerce, and the region’s robust port infrastructure are combining to pull larger volumes of merchandise through Southeast Asia’s logistics corridors. China’s export diversification into ASEAN continues to accelerate, pushing containerized volumes higher on the east-bound legs while creating fresh backhaul demand on the return routes. Government-backed digital customs programs such as the ASEAN Single Window compress clearance cycles and lower compliance costs, enabling freight forwarders to shorten door-to-door lead times[1]EU–ASEAN Cooperation, “Digitalising and Simplifying Customs in ASEAN: The ASEAN Customs Transit System,” euinasean.eu. Multimodal economic corridors under construction in the Greater Mekong Subregion and the Indonesia-Malaysia-Thailand Growth Triangle are unlocking previously underserved production zones.

Key Report Takeaways

- By mode of transport, sea freight forwarding accounted for 54.60% of the ASEAN freight forwarding market share in 2025; air freight is expected to record the fastest modal expansion at a 5.12% CAGR through 2031.

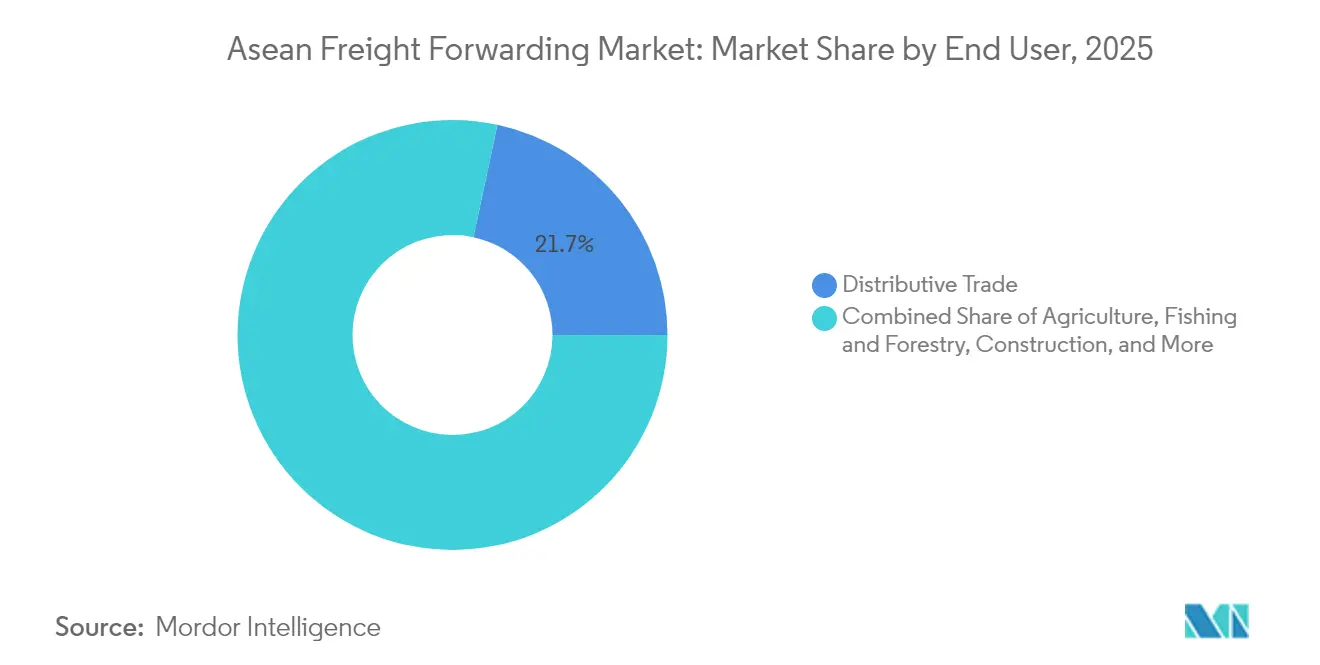

- By end user, distributive trade captured 21.65% of the ASEAN freight forwarding market size in 2025 and is forecast to register a 4.95% CAGR between 2026 and 2031.

- By country, Singapore held a 27.05% share of the ASEAN freight forwarding market in 2025, while Vietnam is poised to post the highest national CAGR at 5.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid intra-ASEAN manufacturing re-shoring | +1.8% | Vietnam, Thailand, Malaysia, Indonesia | Medium term (2-4 years) |

| E-commerce mini-hubs powering cross-border parcel volumes | +1.5% | Singapore, Thailand, Malaysia, Vietnam | Short term (≤ 2 years) |

| Free-trade corridor build-outs (GMS, IMT-GT) | +1.2% | Thailand, Malaysia, Vietnam, Laos, Cambodia | Long term (≥ 4 years) |

| Near-real-time port community systems deployment | +0.9% | Singapore, Malaysia, Thailand, Indonesia | Medium term (2-4 years) |

| Widespread third-party carbon-offset programs by shippers | +0.7% | Global, with focus on Singapore, Thailand, Malaysia | Medium term (2-4 years) |

| ASEAN digital customs single-window rollout | +0.6% | All ASEAN members, led by Singapore, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Intra-ASEAN Manufacturing Re-shoring Accelerates Regional Trade Flows

Production networks for electronics, automotive, and consumer durables are steadily migrating from coastal China into Vietnam, Thailand, and Malaysia. Contract manufacturers that once operated single-country plants now run multi-site footprints across ASEAN to hedge geopolitical exposure and tap 15% lower wage structures. The dispersion of tier-1 and tier-2 component suppliers multiplies intra-regional cargo legs, requiring freight forwarders to synchronize plant-to-plant movements under tight just-in-time parameters. Dedicated corridors linking Thailand’s Eastern Economic Corridor to Vietnamese assembly clusters are already handling higher-frequency, less-than-container-load shipments, while Indonesia’s Batam and Java industrial parks are feeding supplemental feeder volumes into Singapore’s transshipment streams. Customs transit guarantees under the ASEAN Customs Transit System allow sealed trucks to move across borders without repeated inspections, trimming border dwell times to under four hours.

E-commerce Mini-hubs Transform Cross-border Parcel Logistics Architecture

Online marketplaces across Southeast Asia now push order cut-off times deeper into the evening and promise next-day delivery even for cross-border purchases. To honor those service levels, freight forwarders and platform operators have rolled out micro-fulfillment nodes in Johor, Batam, and Songkhla, keeping inventory within a four-hour line-haul of major metro areas. Small parcels clear customs in bulk at bonded consolidation centers before being injected into last-mile networks, reducing per-item brokerage costs and smoothing daily volume spikes. Blockchain-enabled track-and-trace services give sellers and buyers near-real-time status updates, while automated duty assessment engines pre-calculate landed costs at checkout to improve cart-conversion rates. The mini-hub model increases shipment frequency, compresses average consignment size, and lifts demand for time-definite air cargo uplift on high-density lanes such as Kuala Lumpur–Ho Chi Minh City.

Free-trade Corridor Build-outs Unlock Multimodal Connectivity Gains

The North-South, East-West, and Southern Economic Corridors now link manufacturing zones in Laos and northeast Thailand to deep-water terminals in Vietnam and Myanmar, shaving two days off previous route options[2]Asian Development Bank, “Review of Configuration of the Greater Mekong Subregion Economic Corridors,” adb.org. Harmonized axle-weight limits and unified vehicle-telematics standards allow Thai and Vietnamese trucking fleets to operate seamlessly across borders, lowering empty-backhaul ratios. Rail investments, such as the Vientiane–Bangkok freight shuttle, open new block-train opportunities that reduce carbon footprints versus road haulage. Freight forwarders are introducing door-to-door packages that combine rail for long-haul trunk legs with bonded trucking for the first and final miles. Cargo owners in landlocked provinces access direct sailing schedules out of Da Nang and Laem Chabang, bypassing the congestion historically associated with transshipment at Singapore or Port Klang.

Near-real-time Port Community Systems Enhance Operational Transparency

Singapore’s Tuas Mega Port now integrates 5G IoT sensors, automated quay cranes, and an AI-driven Vessel Traffic Management System that predicts berth clashes 48 hours in advance[3]GovInsider, “How Singapore’s Maritime and Port Authority is crafting the vessel management system of the future,” govinsider.asia. Port Klang and Laem Chabang mirror these capabilities through cloud-based platforms that funnel secure API feeds to brokers, customs, and shipping lines. Forwarders access live container status, customs release timestamps, and truck slot reservations from a single dashboard, enabling exception management before costly dwell fees accrue. Blockchain-backed smart bills of lading cut document turnaround from three days to under six hours, while predictive analytics highlight chassis imbalances so equipment pools can be re-positioned proactively. These digital ecosystems translate directly into shorter transit times and higher schedule reliability, reinforcing the competitiveness of maritime-centric supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented truck ownership raising last-mile costs | -0.8% | Indonesia, Philippines, Vietnam, Thailand | Short term (≤ 2 years) |

| Chronic container equipment imbalance | -1.1% | Global, with acute impact on Vietnam, Thailand, Malaysia | Short term (≤ 2 years) |

| Non-harmonised dangerous-goods codes among members | -0.5% | All ASEAN members, particularly cross-border corridors | Medium term (2-4 years) |

| Shortage of FIATA-certified freight professionals | -0.4% | Regional, with acute impact in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Truck Ownership Structure Constrains Last-mile Efficiency

Owner-drivers operate over 70% of commercial vehicles in Indonesia and the Philippines, limiting telematics penetration and consistent service quality. Freight forwarders juggling hundreds of micro-carriers face elevated administrative overhead, while inconsistent maintenance standards inflate roadside-breakdown risks. Consolidation remains slow because small fleets rely on informal lending circles, making capital-intensive upgrades to Euro VI or electric trucks financially out of reach. As e-commerce pushes delivery frequency higher, the shortage of scalable line-haul partners forces forwarders to pay rate premiums during peak seasons, eroding margins.

Chronic Container Equipment Imbalance Disrupts Service Reliability

Export-heavy hubs such as Ho Chi Minh City and Hai Phong routinely grapple with 40-foot shortages that trigger Container Imbalance Charges ranging from USD 85 on 20-foot boxes to USD 170 on 40-foot equipment. Longer voyage times around the Cape of Good Hope divert boxes from Asia for as much as two extra weeks, tying up global pool capacity[4]HCargo, “Container Imbalance Charge: What you need to know,” hcargovn.com. Forwarders incur additional repositioning fees and scramble for substitute routes like feeder loops into Laem Chabang or Penang, adding days and extra transshipment risk. Cargo owners hedge by over-booking allotments, further distorting demand visibility and exacerbating port-side congestion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Maritime Dominance Drives Regional Integration

Sea freight’s 54.60% share underscores its role as the backbone of the ASEAN freight forwarding market, funneling containerized exports of electronics, apparel, and automotive parts through the Straits of Malacca and the South China Sea. Within the broader ASEAN freight forwarding market size, full-container-load movements benefited most from manufacturing reshoring, while less-than-container-load volumes captured rising intra-bloc trade. Air freight, though smaller in tonnage, is scaling at a 5.12% CAGR (2026-2031) as e-retailers route high-value smartphones, pharmaceuticals, and fashion items via Bangkok, Kuala Lumpur, and Singapore. Service innovations such as time-definite cross-border parcel flights and temperature-controlled ULDs reduce spoilage risks on life-science cargo and underpin premium yields.

Hybrid routing strategies are spreading as shippers blend ocean for base-load replenishment with scheduled charters for inventory top-ups. The International Maritime Organization’s decarbonization rules push carriers toward LNG and methanol-ready newbuilds, prompting freight forwarders to market low-emission lanes at modest rate premiums. Road-rail combinations in the Greater Mekong Subregion extend sea-rail intermodal options, letting cargo skip coastal detours and shave 400 kilometers off certain Hanoi-to-Bangkok routings. These offerings increase operational resilience amid climate-linked weather disruptions and periodic berth congestion.

By End User: Distributive Trade Leads Multi-sector Expansion

Distributive trade’s 21.65% slice of the ASEAN freight forwarding market size in 2025 reflects supermarkets, FMCG importers, and omnichannel retailers stocking multi-country hubs in Johor and Batam to reach 600 million consumers within two-day transit windows. Demand climbs further as lifestyle and beauty brands pursue direct-to-consumer strategies that require pick-and-pack capabilities in free-trade zones. Manufacturing and automotive clients remain bedrock shippers, leveraging bonded shuttle lanes from Thai and Malaysian auto clusters to Vietnamese final assembly lines. Oil, gas, and mining volumes stabilize as green transition policies redirect capital toward LNG and downstream petrochemicals, necessitating project forwarding skills for oversized modules and hazardous cargo paperwork.

Infrastructure megaprojects such as Indonesia’s new capital city and the Philippines’ Build Better More program spur construction-related freight, boosting steel and heavy-equipment moves. Agriculture exports of durians, mangosteens, and frozen shrimp fortify cold-chain demand, while forestry exports from Kalimantan feed China’s pulp and paper industry. Telecommunications gear and pharmaceuticals register double-digit volume growth, sustained by 5G rollouts and expanded healthcare coverage. Regulatory certification—GDP for pharma or ISPS for dangerous goods—confers pricing power on forwarders that invest early in compliance.

Geography Analysis

Singapore remains the epicenter of the ASEAN freight forwarding market, handling 27.05% of regional throughput in 2025 thanks to unrivaled port efficiency, bonded warehousing capacity, and a deep bench of licensed customs brokers. The USD 20 billion Tuas Mega Port, slated to reach full phase by 2040, consolidates existing terminals into a single automated nexus capable of 65 million TEU annually, reinforcing Singapore’s first-mover edge in AI-enabled berthing and paperless cargo release. Thailand and Malaysia occupy the next tier, each leveraging strong industrial linkages and aggressive smart-port roadmaps. Laem Chabang’s integrated Port Community System and Port Klang’s blockchain-secured container gate operations extend end-to-end visibility to regional hauliers and freight forwarders.

Vietnam is expected to post the region’s fastest expansion at a 5.05% CAGR to 2031, fueled by preferential trade agreements and escalating electronics exports. The country’s northern ports tap new double-stack rail connections into China, while the south benefits from Ro-Ro links serving automotive supply chains. Indonesia offers vast domestic potential but battles archipelagic logistics challenges, prompting investments in feeder networks and roll-on/roll-off routes to unify Java, Sumatra, and Kalimantan. The Philippines, though island-fragmented, experiences parcel-volume spikes as mobile-first consumers embrace pan-ASEAN marketplaces.

Regulatory Landscape

Freight forwarding in ASEAN operates under a layered regime of national licensing rules and region-wide trade facilitation frameworks. The ASEAN Trade Facilitation Framework anchors initiatives such as the ASEAN Single Window, the ASEAN Trade Repository, and self-certification, which collectively support paperless trade and more consistent border procedures across Member States.

For cross-border land movements, the ASEAN Framework Agreement on the Facilitation of Goods in Transit (AFAFGIT) and the ASEAN Customs Transit System (ACTS) provide a structured mechanism for transit movements where duties and taxes are not paid at intermediate borders and formalities are finalized at destination. At the national level, compliance requirements continue to tighten in some markets; for example, the Philippines Department of Trade and Industry issued Department Administrative Order No. 24-09 for sea freight forwarding, including capitalization-related compliance requirements effective by January 1, 2025. This raises the bar for smaller operators and contributes to greater market formalization.

Value Chain Analysis

The ASEAN freight forwarding value chain typically starts with shipper procurement and order management, followed by freight forwarder planning (routing, consolidation, documentation, and risk management), and then execution through carriers and terminal operators across sea, air, and road-rail legs. Forwarders coordinate origin services (pickup, export customs filing, warehousing and consolidation), main carriage (ocean and air linehaul, including feeder connections), and destination services (import clearance, deconsolidation, bonded storage, and last-mile delivery), supported by enablers such as customs brokers, insurers, inspection bodies, and digital platforms that connect port community systems with shipper visibility tools.

Capacity and reliability depend heavily on infrastructure nodes and corridor programs that reduce fragmentation across borders. Policy-led upgrades, such as the Framework on ASEAN Supply Chain Efficiency and Resilience adopted in October 2024, emphasize digital technology application and regional coordination, while country initiatives also shape local execution, including Viet Nam's Decision 2229/QD-TTg (approved October 2025) that sets a 2025-2035 logistics services strategy. On the physical side, inland port and rail-linked developments influence network design and modal mix, such as Malaysia's Perlis Inland Port plan (reported March 2025) to add 300,000 TEUs of annual handling capacity and strengthen rail connectivity with China and Thailand, alongside corridor efforts like the Singapore-Kunming Rail Link and emerging smart logistics hubs.

Competitive Landscape

Industry consolidation reshapes the competitive map as global integrators pursue scale, technology, and end-to-end capabilities. DSV’s USD 14.3 billion takeover of DB Schenker is the headline act, vaulting the combined group to the top of the global rankings and injecting large contract logistics volumes into ASEAN gateways. DHL Global Forwarding expands regional footprint through a EUR 60 million (USD 62.5 million) automated gateway in Kuala Lumpur that doubles cross-border parcel capacity. Kuehne+Nagel’s alliance with Microsoft injects AI into route optimization, fueling 5% cycle-time improvements on Singapore–Jakarta lanes and reinforcing its differentiation on data-driven reliability.

Local champions fight back by leveraging nuanced regulatory knowledge and domestic distribution muscle. YCH Group’s Vietnam SuperPort links blockchain settlement tools with Vietnam Post’s last-mile reach, creating an SME-friendly platform that bundles duty computation, financing, and doorstep delivery. GEODIS folds Keppel Logistics’ 200,000 m² warehouse estate into its ASEAN road network, enabling port-to-door temperature-controlled services that appeal to pharmaceuticals and high-tech manufacturers. PSA International’s earlier purchase of BDP International aligns port assets with freight management, providing shipper visibility from container berth to factory gate.

Technology adoption distinguishes leaders from laggards. Top-tier forwarders deploy digital twins of warehouse and transport assets to model cost-to-serve, predict disruptions, and pre-book capacity. IoT-enabled road fleets feed live telemetry to control towers, lowering empty-run kilometers. Sustainability moves also count: DSV’s commitment to sustainable aviation fuel blends and Kuehne+Nagel’s offset marketplace allow shippers to track scope 3 emissions. Barriers to entry rise as dangerous-goods compliance, GDP certification, and cybersecurity protocols demand heavier investment, nudging sub-scale operators toward merger talks or niche specialization.

ASEAN Freight Forwarding Industry Leaders

Deutsche Post DHL Group (DHL Global Forwarding)

Kuehne + Nagel International AG

DSV A/S

Sinotrans Ltd

Kerry Logistics Network Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated where ASEAN is turning trade facilitation and infrastructure programs into faster, more transparent door-to-door execution across multiple countries. Digitally enabled cross-border movements that rely on the ASEAN Single Window and ACTS create room for forwarders to standardize documentation, rules-of-origin workflows, and duty and tax calculations across lanes, while also integrating port community systems data into shipper-facing tracking. The push for higher schedule reliability supports premium offerings in time-definite air and multimodal services as manufacturing footprints diversify across Viet Nam, Thailand, Malaysia, and Indonesia.

New and reactivated logistics nodes also create additional entry points for consolidation, bonded processing, and rail-sea interchange. In June 2026, Malaysia reactivated Segamat Inland Port to support rail freight with on-site Customs clearance, strengthening inland distribution options beyond coastal gateways and supporting forwarder-led hub-and-spoke designs. Port and corridor projects support specialized services as well: PSA Singapore field-tested next-generation Intelligent Guided Vehicles at the Tuas Living Lab in April 2026, highlighting automation at a key transshipment node, while Cambodia's Sihanoukville Autonomous Port is advancing a phased expansion program supported by Japan with a stated target of about 2.5 million TEUs per year by 2029. That expansion increases the need for feedering, transshipment planning, and integrated customs and documentation services.

Recent Industry Developments

- July 2026: DSV expanded its Asia-Pacific headquarters in Hong Kong to support Greater China and regional operations. The expansion improves control-tower capabilities for customers routing freight through ASEAN gateways and aligns the network for larger, multi-country contracts following ongoing industry consolidation.

- June 2026: DHL Global Forwarding launched dedicated transpacific air cargo flights from Hanoi and Bangkok to North American hubs, including Cincinnati and Chicago, using Boeing 777 freighters. The added controlled capacity supports time-definite export lanes for electronics and e-commerce-related uplift from Southeast Asia and reshapes peak-season procurement for forwarders and shippers.

- April 2026: Kuehne+Nagel advanced its Thailand road-logistics upgrade by rolling out another batch under its prime mover fleet investment program. The added tractor capacity improves cross-border linehaul performance on key mainland Southeast Asia corridors and supports higher-frequency LTL and consolidated truck movements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the ASEAN freight forwarding market is defined as the revenue earned from arranging and managing the movement of goods across modes, including shipment planning, carrier coordination, documentation, and cross-border handling services across ASEAN.

Scope exclusions: Excludes pure asset-based transport and infrastructure revenues (such as trucking fleet operations, airline/ship operator line-haul revenue, and port or terminal handling fees) when they are not billed as part of a forwarding service.

Segmentation Overview

- By Mode of Transport

- Air Freight Forwarding

- Sea Freight Forwarding

- Full-Container-Load (FCL)

- Less-than-Container-Load (LCL)

- Others

- By End User

- Manufacturing & Automotive

- Oil & Gas, Mining & Quarrying

- Agriculture, Fishing & Forestry

- Construction

- Distributive Trade (Wholesale/Retail, FMCG)

- Other End Users (Telecom, Pharmaceutical, etc.)

- By Country

- Singapore

- Thailand

- Malaysia

- Indonesia

- Vietnam

- Philippines

- Rest of ASEAN (Myanmar, Laos, Cambodia, Brunei)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand backdrop for ASEAN trade and freight flows, then mapping how forwarding revenues typically get generated by mode and corridor. We rely on public data such as ASEAN Secretariat trade statistics, UN Comtrade, World Bank logistics and trade indicators, IMF macro series, and national statistics offices and customs agencies across key member states.

To keep the model grounded in real pricing and mix, we also review sources such as company annual reports, investor presentations, and port and airport authority publications, plus reputable press coverage on capacity, disruptions, and route changes. Where needed, a paid subscription focused on company financials and another focused on shipment-level trade flows were referenced to confirm corridor directionality and to sanity-check rate movements. These examples are not exhaustive, and other sources were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary discussions were used to verify how forwarding revenue is recognized by mode, what services are commonly bundled (customs clearance, consolidation, basic warehousing), and how cross-border demand shifts between air and sea in different cycles. We spoke with forwarders, carriers and agents, and large shipper-side logistics teams across ASEAN, so corridor-level realities, yield trends, and the share of outsourced forwarding could be cross-checked against what they see operationally.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | |

| Mid tier: 61% | Functional/Unit leaders: 35% | |

| Smaller Players: 14% | Managers: 52% |

Market-Sizing & Forecasting

The core sizing uses a top-down build where trade and freight activity across ASEAN is reconstructed by mode and key corridors, then translated into forwarding revenue using service penetration and typical fee intensity. Once the first total is formed, it is corroborated through selective bottom-up checks using sampled price per shipment, volume by mode, and country-level rollups from a set of visible operators, then adjusted when the two views do not align.

Inputs used in the model include ASEAN import and export values, containerized throughput indicators, air cargo tonnage signals, cross-border manufacturing and electronics shipment momentum, and corridor-specific rate direction (spot and contract) as reported by market participants. Because full country-by-country disclosure is uneven, gaps are handled by applying proxy relationships between trade value, mode split, and forwarding fee ranges that were validated in interviews.

For forecasting, scenario analysis is applied around trade growth, capacity additions, and rate normalization, then a simple multivariate regression is used as a cross-check on the base case using GDP, merchandise trade, and air and sea activity indicators. Assumptions are reviewed with respondents so the forward view reflects what operators expect in contract renewals, shipment mix, and service bundling.

Data Validation & Update Cycle

Outputs are checked against independent signals such as merchandise trade growth, container and air cargo trends, and major corridor disruption events, so the final totals do not drift away from observed activity. Variances are reviewed step-by-step, starting with unit checks and currency timing, followed by country and mode reconciliation, and then a second analyst review before sign-off.

If an outlier is found, we re-contact relevant experts to confirm whether it is explained by rate spikes, mix shifts, or a temporary policy change. The report is refreshed annually, and interim updates are made when material events occur (for example, major capacity changes or trade policy shifts). Before delivery, the latest data pass is done so clients receive an updated view.

Mordor Intelligence's Asean Freight Forwarding Market Sizing Compared With Other Published Estimates

Published market sizes for ASEAN freight forwarding can look far apart because each publisher sets its own service boundary, base year, and rate assumptions, then refreshes those inputs on different timelines. Differences also come from whether some numbers reflect a surge year for freight rates, while others smooth rates over a longer cycle.

Ocean carrier line-haul revenue and port or terminal handling charges sit outside Mordor Intelligence's scope, which is why our value can be lower than figures that fold in a wider logistics spend bucket alongside forwarding fees. Another driver is how fee intensity is treated, since some estimates apply a single percent-of-freight assumption across modes, while our model separates air and sea forwarding economics and then pressure-tests the totals with corridor checks and interview-led validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.62 B (2025) | |

| Market Research Publisher A | USD 45.50 B (2024) | Often presented as a broader service basket, which can include adjacent logistics revenues beyond forwarding, and it uses an earlier base year that may reflect a different rate cycle and currency timing. |

| Industry Research Outlet B | USD 32.80 B (2026) | Uses a different forecast window and can embed stronger growth and higher fee progression assumptions, with less visibility on how mode mix and corridor-level rate shifts were validated in the base build. |

Across the three figures, the spread is mainly explained by what gets counted as forwarding versus adjacent logistics charges, and by the year chosen for the starting value when rates were moving quickly. By keeping the demand pool tied to trade and mode activity, then checking fee intensity with practitioner inputs, we end up with a number that is easier to trace back to clear, repeatable drivers.

Key Questions Answered in the Report

What is the current value of the ASEAN freight forwarding market?

The ASEAN freight forwarding market size is USD 33.13 billion in 2026 and is projected to climb to USD 41.86 billion by 2031.

Which transport mode holds the largest share in Southeast Asia’s forwarding sector?

Sea freight accounts for 54.60% of shipments, reflecting the region’s heavy reliance on maritime corridors.

Why is Vietnam the fastest-growing national market?

Vietnam’s 5.05% CAGR is driven by manufacturing migration from China and preferential trade agreements that lift export volumes.

How are digital customs systems improving logistics efficiency?

The ASEAN Single Window enables paperless clearance across member states, cutting border processing times and associated costs.

What impact does container imbalance have on forwarders?

Shortages trigger Container Imbalance Charges of up to USD 170 per 40-foot box and force costly repositioning strategies.

Which recent merger has reshaped the competitive landscape?

DSV’s acquisition of DB Schenker added USD 41.6 billion in global revenue and elevated the combined entity to the top of the freight forwarding rankings.

Page last updated on: