Logistics

30th MayUnlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

The Intra-Asia Freight Forwarding Market Report is Segmented by Mode of Transport (Air Freight Forwarding, Sea Freight Forwarding, and Others), End User (Manufacturing & Automotive, Oil & Gas, Mining & Quarrying, Agriculture, Fishing & Forestry, Construction, and More), Trade Lanes (China and Vietnam, China and South Korea, Japan and Vietnam, China and Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

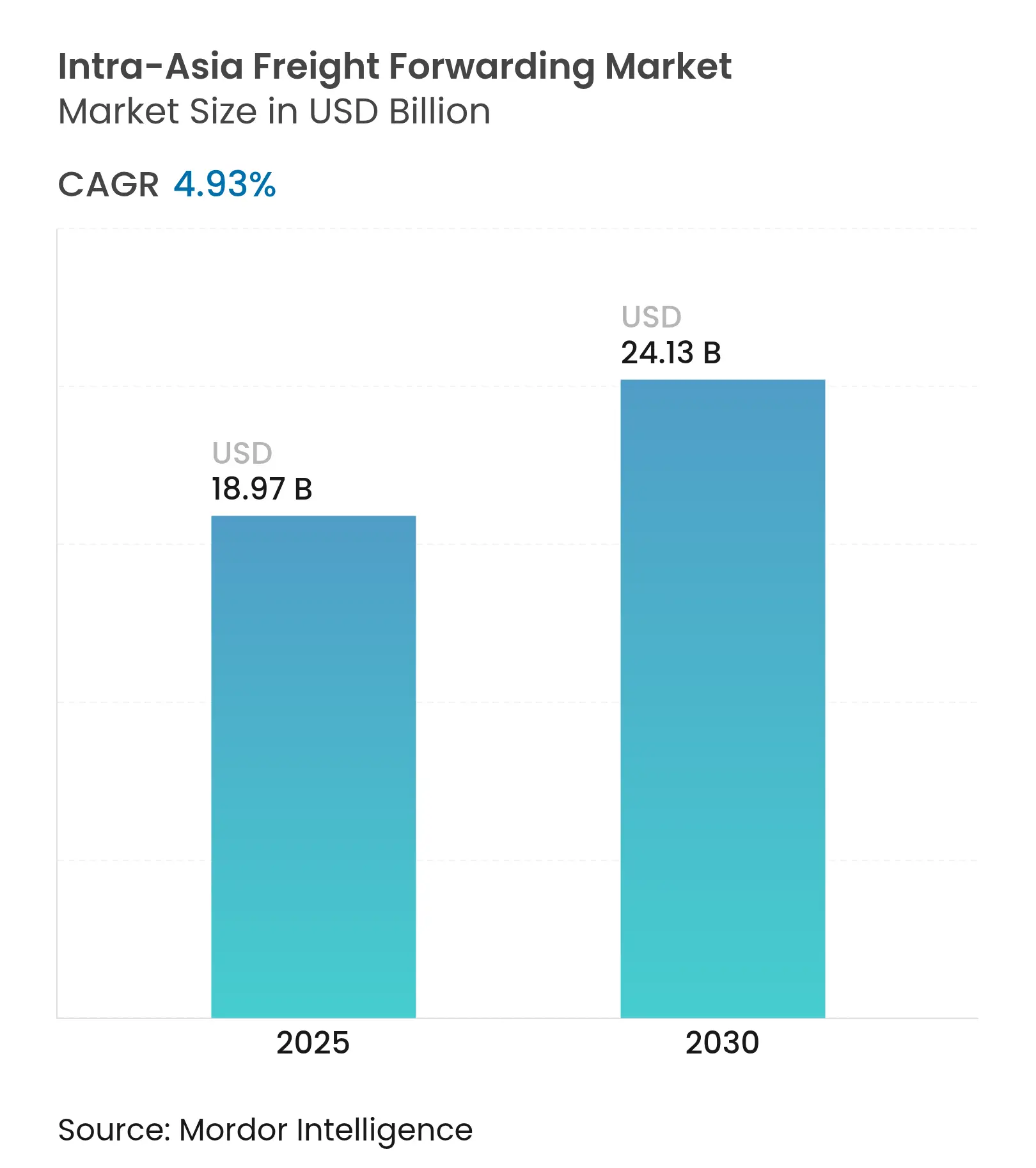

| Market Size (2025) | USD 18.97 Billion |

| Market Size (2030) | USD 24.13 Billion |

| Growth Rate (2025 - 2030) | 4.93 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Robust e-commerce expansion, RCEP-driven tariff reductions, and relocation of manufacturing to Southeast Asia are boosting cargo volumes and intensifying demand for integrated logistics. Sea freight remains the preferred mode for containerized goods, yet air freight is expanding swiftly as shippers of temperature-sensitive pharmaceuticals and high-value parcels seek time-critical options. Digitalization, encompassing AI-based freight audit and blockchain-enabled document flows, is redefining service expectations, while ongoing port automation across China, Singapore, and Vietnam is lifting throughput and lowering unit costs. Simultaneously, geopolitical uncertainty and periodic port congestion oblige forwarders to diversify routing, implement multimodal solutions, and actively manage capacity.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge in intra-Asian e-commerce volumes Surge in intra-Asian e-commerce volumes | +1.2% | Core APAC, spill-over to Southeast Asia | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Core APAC, spill-over to Southeast Asia | Impact Timeline:Medium term (2-4 years) |

RCEP liberalization RCEP liberalization | +0.8% | RCEP members, China–ASEAN corridor | Long term (≥ 4 years) | |||

China + 1 manufacturing shift China + 1 manufacturing shift | +1.0% | Vietnam, Thailand, Malaysia | Medium term (2-4 years) | |||

Expansion of regional port infrastructure Expansion of regional port infrastructure | +0.7% | China, Singapore, Vietnam | Long term (≥ 4 years) | |||

Multi-leg consolidation hubs Multi-leg consolidation hubs | +0.5% | Singapore, Hong Kong | Short term (≤ 2 years) | |||

Rise in temperature-controlled pharma trade Rise in temperature-controlled pharma trade | +0.6% | Japan, South Korea, Australia | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Intra-Asian E-commerce Volumes

Cross-border e-commerce is transforming cargo flows as Asian consumers increasingly purchase within the region rather than from Western sellers. Chinese merchants recorded strong export gains to RCEP partners, spurring specialized last-mile networks and demand for end-to-end visibility platforms. Forwarders are scaling fulfillment centers near consumption hubs and investing in cold-chain assets so that food and pharmaceutical parcels meet stringent shelf-life and compliance requirements. High-frequency shopping events trigger peak-season surcharges, prompting small and mid-size enterprises to book less-than-container-load (LCL) capacity through digital marketplaces. As a result, more than one-third of new business inquiries received by leading forwarders in 2025 originate from regional online sellers seeking multichannel distribution, underscoring e-commerce’s structural role in sustaining the Intra-Asia freight forwarding market.

Regional Comprehensive Economic Partnership (RCEP) Liberalization

RCEP has created the world’s largest free-trade zone, covering 28% of global GDP and simplifying customs through a single set of rules of origin[1]Lisandra Flach, Hannah Hildenbrand, Feodora Teti, “The Regional Comprehensive Economic Partnership Agreement and Its Expected Effects on World Trade,” Intereconomics, intereconomics.eu. The diagonal cumulation mechanism now lets manufacturers source inputs across 15 member states and still claim preferential tariffs, which in turn directs freight toward intra-regional corridors. Academic studies confirm a positive correlation between shipping-liner connectivity and trade volumes under the agreement. Forwarders benefit from reduced documentation cycles and faster customs release, yet they must also re-engineer routing models to accommodate diverted flows that bypass non-member countries.

Manufacturing Shift from China to Southeast Asia (“China + 1”)

Escalating tariffs and geopolitical tension have accelerated the relocation of electronics, apparel, and automotive production to Vietnam, Thailand, and Malaysia[2]Z2Data, “Why ‘China Plus One’ Has Become ‘Anywhere but China’,” z2data.com. U.S. imports from China face duties as high as 20%, incentivizing multinationals to carve out alternate factories while retaining select operations in coastal China for domestic sales. This dual-sourcing model multiplies multi-leg shipments that move intermediate goods between the Pearl River Delta and emerging ASEAN hubs before final export to North America or Europe. Freight forwarders with consolidation expertise capture value by stitching together sea-air routes, cross-border trucking, and regional warehousing.

Expansion of Regional Port Infrastructure

Smart-port investments are unlocking new capacity throughout Asia. Qingdao’s automated terminal averages 60.6 container moves per crane-hour—double legacy benchmarks—while China’s FAST coastal service trimmed Shanghai-Guangzhou logistics costs by 65%[3]CGTN, “Chinese Ports Get Smarter With Automation Push,” cgtn.com. DP World has earmarked USD 2.5 billion for terminal upgrades and multimodal parks that streamline transshipment. Southeast Asian governments, buoyed by Belt and Road financing, are upgrading secondary ports such as Brunei’s Muara to handle post-Panamax vessels. These enhancements shorten dwell times and enable forwarders to offer more reliable sailing schedules.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Port congestion in key Asian hubs Port congestion in key Asian hubs | -0.8% | Shanghai, Singapore, Port Klang | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Shanghai, Singapore, Port Klang | Impact Timeline:Short term (≤ 2 years) |

Geopolitical & trade-policy uncertainty Geopolitical & trade-policy uncertainty | -1.1% | China–U.S., Taiwan Strait, ASEAN corridors | Medium term (2-4 years) | |||

Logistics labor shortages Logistics labor shortages | -0.6% | Japan, South Korea | Long term (≥ 4 years) | |||

Emerging carbon-pricing schemes Emerging carbon-pricing schemes | -0.4% | EU–Asia, global shipping | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Port Congestion in Key Asian Hubs

In April 2025, 134 vessels queued outside the Shanghai–Ningbo complex with average anchorage delays nearing two days, while Port Klang’s yard utilization surpassed 85% despite improved berth productivity. Vietnam’s Cai Mep terminal recorded five-day vessel waits during peak export season, eroding schedule reliability and elevating demurrage risk. Typhoon-induced closures further magnify disruption, causing forwarders to secure buffer stockpiles and reroute transit-time-sensitive cargo through Busan or Laem Chabang. These contingency measures raise operating costs and squeeze margins.

Geopolitical & Trade-Policy Uncertainty

U.S.–China trade volumes declined more than 20% in 2024, yet Chinese exports to ASEAN jumped 16.6% year on year[4]South China Morning Post, “China Presses Ahead With Southeast Asia Port Expansion,” scmp.com. Washington’s tariff review could lift Vietnam’s average duty from 3.4% to 46%, exposing supply chains to pricing volatility. Forwarders manage uncertainty via dual-sourcing strategies, multi-currency contracts, and “friends-shoring” of inventory, but insurance premiums and compliance overhead remain elevated.

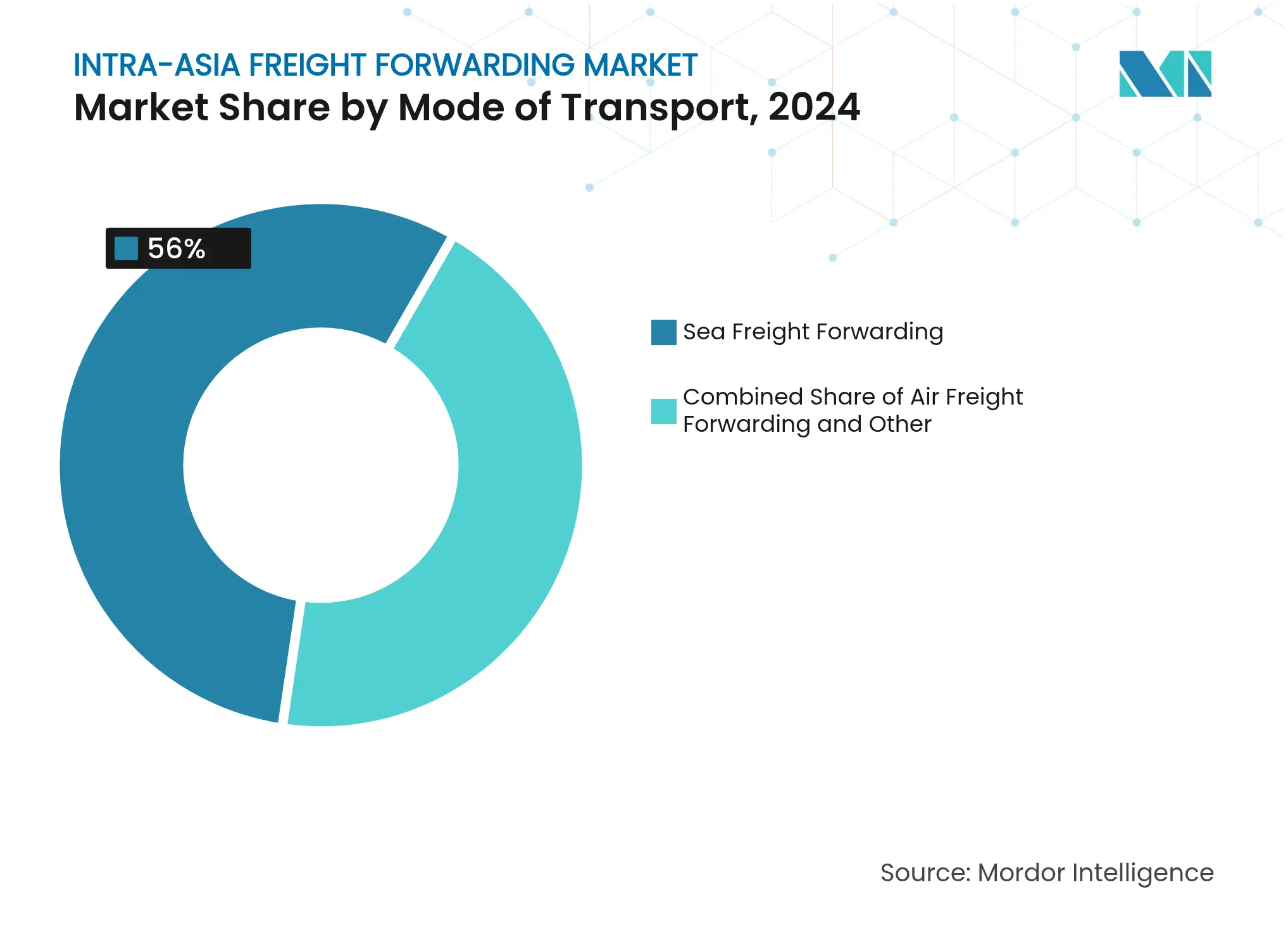

By Mode of Transport: Sea Freight Dominance Amid Air Growth

Sea freight generated 56% of the total 2024 value, underscoring its cost-efficiency for mass-market manufacturing goods that move in container lots across dense Asian corridors. The segment benefits from tight-knit carrier alliances—Premier Alliance and Gemini Cooperation now control 80% of global capacity—allowing forwarders to negotiate slot commitments across multiple weekly sailings. Air freight, while only a minor revenue share, is projected to post a 4.50% CAGR as e-commerce parcels and bio-pharma consignments demand next-day or two-day delivery across megacity pairs. High-speed rail pilots between China and Southeast Asia are also carving a niche by offering 20% faster transit than trucking at comparable costs, broadening shipper choices.

Forwarders differentiate sea-freight offerings through guaranteed equipment availability, real-time container tracking, and carbon-offset booking options. Less-than-container-load growth is particularly vibrant; SMEs leveraging consolidation hubs in Singapore and Hong Kong can save up to 18% on logistics spend compared with origin-stuffed FCL shipments. Meanwhile, airports including Ezhou Huahu are being purpose-built for freight, providing all-cargo runways and bonded warehousing that slash dwell time to six hours. Such upgrades position air cargo as the fastest-growing service line in the Intra-Asia freight forwarding market.

Note: Segment shares of all individual segments available upon report purchase

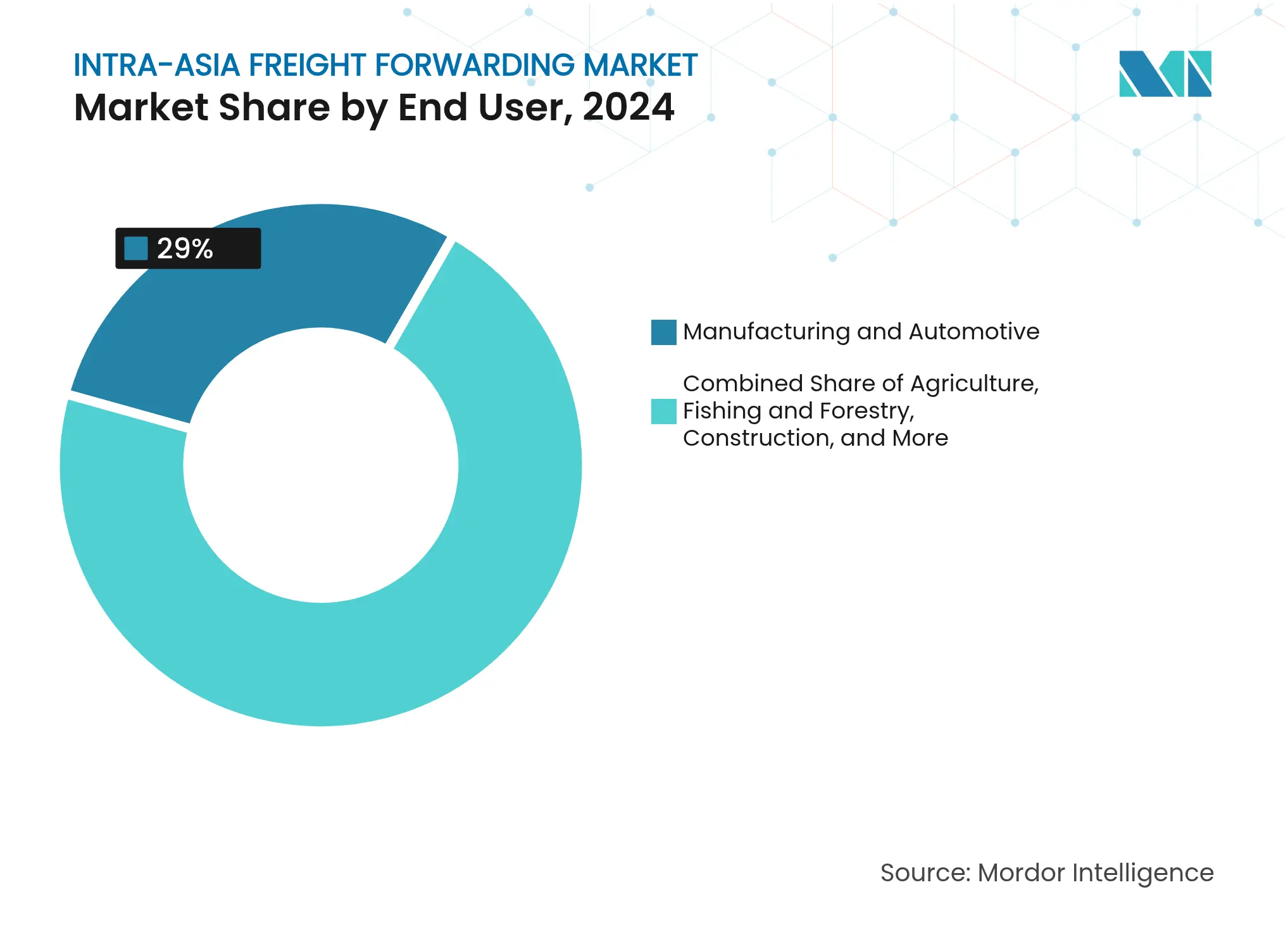

By End User: Manufacturing Leadership with Distributive Trade Acceleration

Manufacturing & automotive retained a 29% share of 2024 revenue, buoyed by Chinese vehicle exports surging 33.62% in Q1 2025 as OEMs leveraged rail-sea links and expanded port connectivity. The segment favors multimodal chains that blend inland waterways, feeder vessels, and block trains to minimize landed cost. Automotive tiers increasingly demand just-in-sequence deliveries to ASEAN assembly plants, prompting forwarders to establish cross-dock platforms adjacent to industrial parks.

Distributive trade—covering wholesale, retail, and FMCG activities—is forecast for a 5.50% CAGR to 2030, propelled by intra-regional consumer spending and venture-backed marketplace expansion. Platforms such as J&T Express lifted parcel volumes 24% year on year, generating downstream demand for pick-and-pack, returns processing, and seller-fulfilled prime services. Other verticals display mixed fortunes: oil & gas faces emissions-driven scrutiny, mining & quarrying wrestles with volatile commodity prices, while agriculture benefits from stable food-security policies. Forwarders customizing sector-specific value-added services capture superior yields within the Intra-Asia freight forwarding industry.

Note: Segment shares of all individual segments available upon report purchase

By Trade Lanes: China–Vietnam Leadership with Japan Corridor Growth

The China–Vietnam lane delivered 13.50% of 2024 market revenue, reflecting Vietnam’s ascent as a near-shore manufacturing hub and its seamless integration into Pearl River Delta supply chains. Bilateral trade is forecast to exceed USD 750 billion by 2030, sustaining dense feeder and cross-border trucking rotations. China–Japan, although a mature route, is set for the fastest 4.10% CAGR as electric-vehicle components and semiconductor equipment shuttle between Suzhou, Nagoya, and Osaka ports.

Supplementary corridors such as China–South Korea remain critical for electronics; China–Singapore serves transshipment re-export flows; and Singapore–Indonesia grows on the back of omni-channel retail fulfillment. Kerry Logistics, for example, has shortened Asia–Europe lead times by instituting Singapore-based sea-air solutions that bypass Middle-East congestion. Fragmentation across emerging routes provides an opportunity for forwarders deploying digital freight-matching tools to stitch together capacity and secure competitive pricing.

Southeast Asia is the fastest-advancing sub-region as relocation of factories doubles export volumes toward 2030. Vietnam capitalizes on preferential access to both Chinese upstream suppliers and Western buyers, while Thailand and Malaysia leverage established automotive and electronics clusters to attract incremental FDI. Port automation in Laem Chabang and Tanjung Pelepas accelerates throughput, enhancing regional competitiveness.

Northeast Asia commands sophisticated infrastructure but grapples with aging workforces and tight trucking capacity. Japan’s overtime limits compel shippers to adopt proximity sourcing, repositioning inventory nearer to end markets, and raising demand for value-added warehousing in Osaka and Tokyo Bay. South Korea continues to pioneer digital customs clearance and 5G-enabled terminal operations, yet must contend with wage inflation and driver shortages.

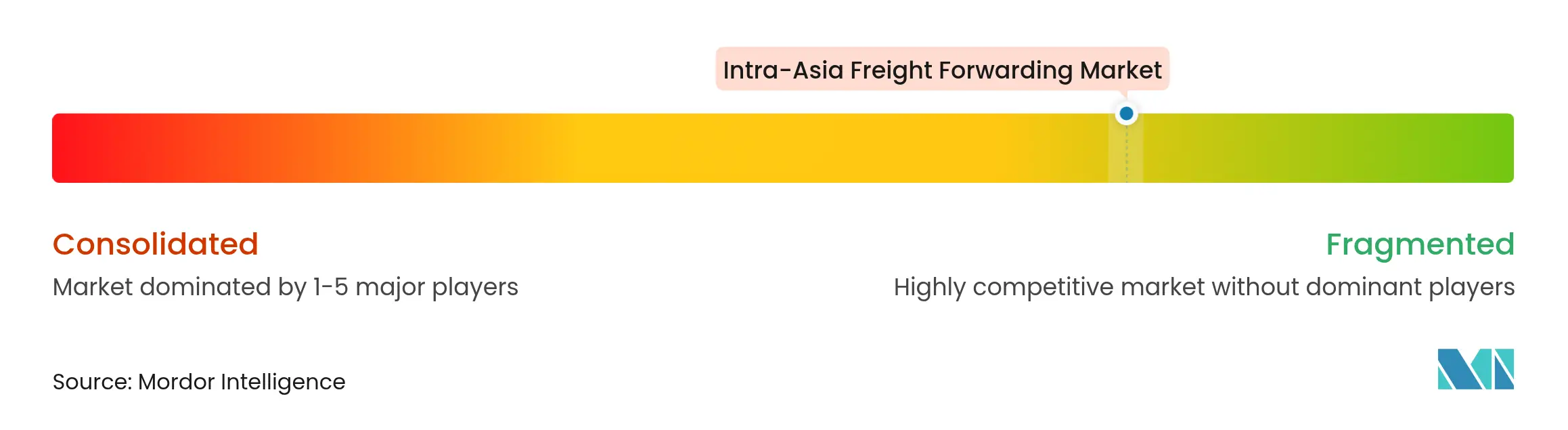

Market Concentration

The market is moderately fragmented; however, DSV’s EUR 14.3 billion (USD 14.9 billion) acquisition of DB Schenker in April 2025 pushed the combined entity’s sales to EUR 41.6 billion (USD 43.3 billion), creating the world’s largest player and sharpening focus on multimodal benefits. DHL Express, by contrast, strengthened its Asia-Pacific network through new gateways in Singapore and Kuala Lumpur and by launching dedicated Hong Kong–Jakarta freighters that trim transit times for e-commerce shippers.

Technology adoption remains a decisive differentiator. Portcast joined Google’s AI-First Startups Program to refine algorithms that spot invoice anomalies and automate contract management, potentially reducing billing errors by 80%. UPS deployed its Gateway Technology Automation Platform, harvesting USD 24 million in 2024 savings via predictive routing and robotic induction at Worldport. Regional specialists such as Sinotrans and Nippon Express pair local-market know-how with investments in cross-border digital corridors, enabling rapid customs clearance and in-country distribution.

Strategic alliances also shape competition. NYK partnered with Sembcorp in October 2024 to explore green-ammonia shipping and to advance digital freight visibility, aligning fleets with decarbonization mandates. GEODIS completed its purchase of Keppel Logistics in June 2024, reinforcing Southeast Asian contract-logistics reach. Such moves underscore an arms race for network density, sustainability credentials, and data-rich customer interfaces within the Intra-Asia freight forwarding market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Freight forwarders are an important part of the supply chain. They act as middlemen between the company that ships the goods and the place where the goods will end up.It is the coordination and shipment of goods from one place to another via single or multiple carriers via air, marine, rail, or highway. The report provides a complete background analysis of the global freight forwarding market, which includes an assessment of the economy, a market overview, market size estimations for key segments, emerging trends in the market, market dynamics, and key company profiles. The report also covers the impact of COVID-19 on the market.

The Intra-Asia Freight Forwarding Market is segmented by mode of transport (air freight forwarding, ocean freight forwarding, road freight forwarding, and rail freight forwarding), by customer type (business-to-business (B2B)), by application (industrial and manufacturing, retail, healthcare, oil and gas, food and beverage, and other applications), and by geography (China, Japan, South Korea, India, and the Rest of Asia). The Intra-Asia Freight Forwarding Market report offers market size and forecast values (in USD billion) for all the above segments.

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.