Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

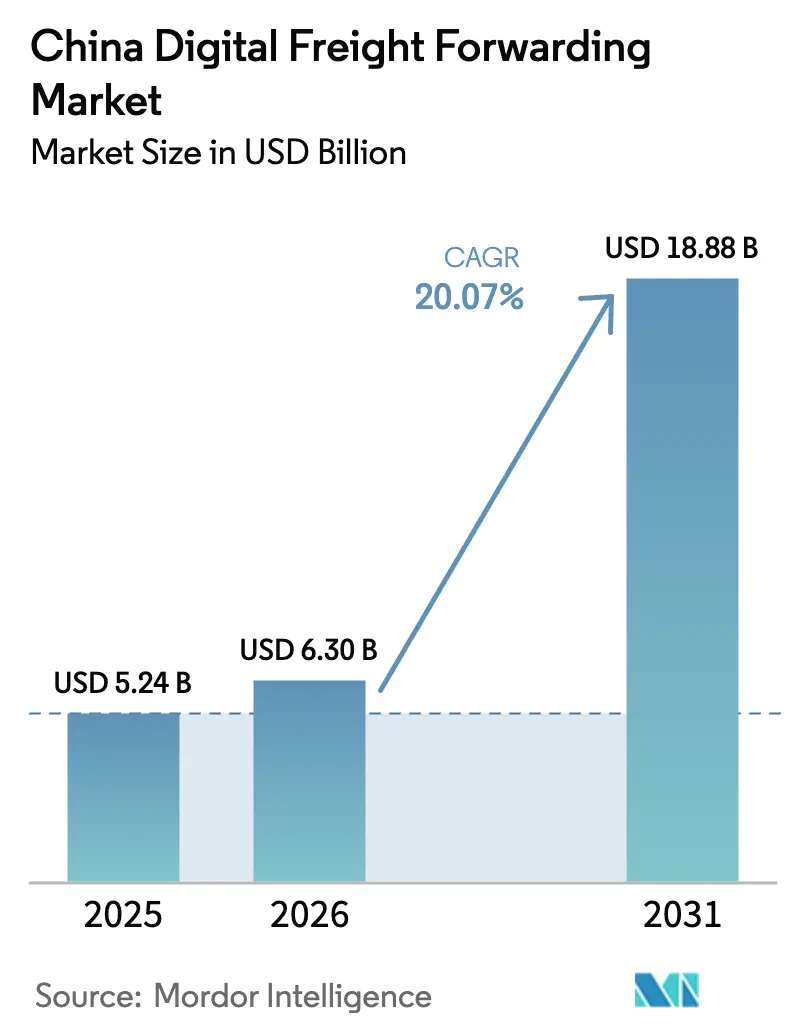

| Base Year Market Size (2025) | USD 5.24 Billion |

| Market Size (2026) | USD 6.30 Billion |

| Market Size (2031) | USD 18.88 Billion |

| Growth Rate (2026 - 2031) | 20.07% CAGR |

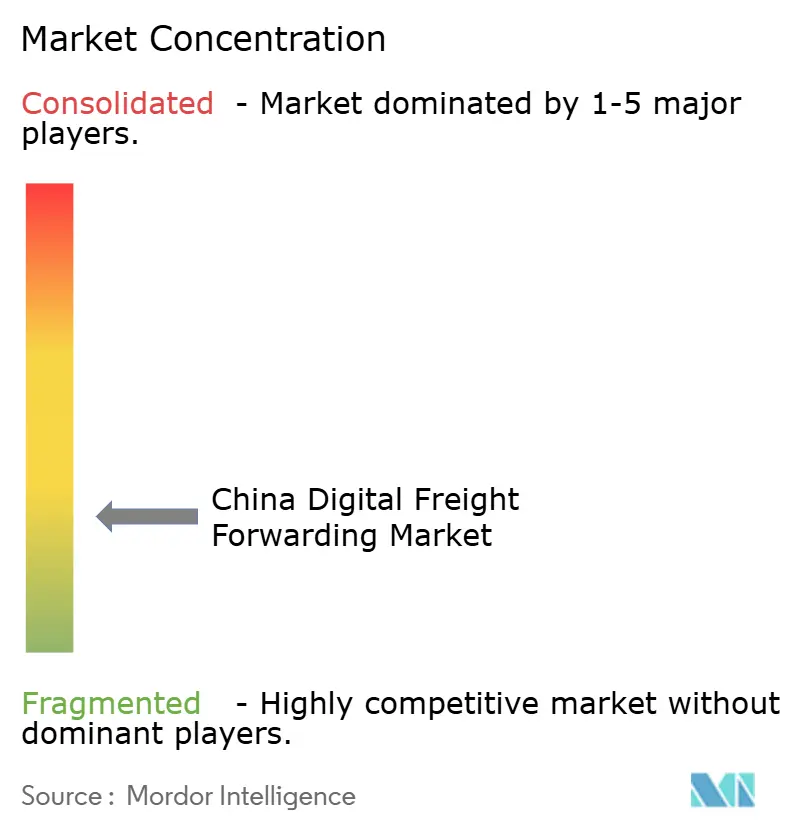

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Digital Freight Forwarding Market Analysis by Mordor Intelligence

The China Digital Freight Forwarding Market size is projected to expand from USD 5.24 billion in 2025 and USD 6.30 billion in 2026 to USD 18.88 billion by 2031, registering a CAGR of 20.07% between 2026 and 2031. The transition away from paper‐based processes, combined with widespread ESG procurement mandates and digital-yuan escrow pilots, is redefining contracting norms and compressing payment cycles. Sea freight continues to anchor volumes, yet platform-enabled air cargo is scaling quickly, helped by Latin American e-commerce flows and easier e-CNY settlement. Small and medium exporters now enjoy real-time visibility and pooled capacity once reserved for large multinationals, while cloud deployment lowers entry costs and speeds regulatory upgrades. Geographic momentum is shifting inland as the New International Land-Sea Trade Corridor opens new rail and river routes, even as coastal depots struggle with congestion. Competitive pressure intensifies as pure-play platforms battle asset-heavy logistics groups that blend owned fleets with booking apps, each racing to absorb rising cyber-risk compliance costs.

Key Report Takeaways

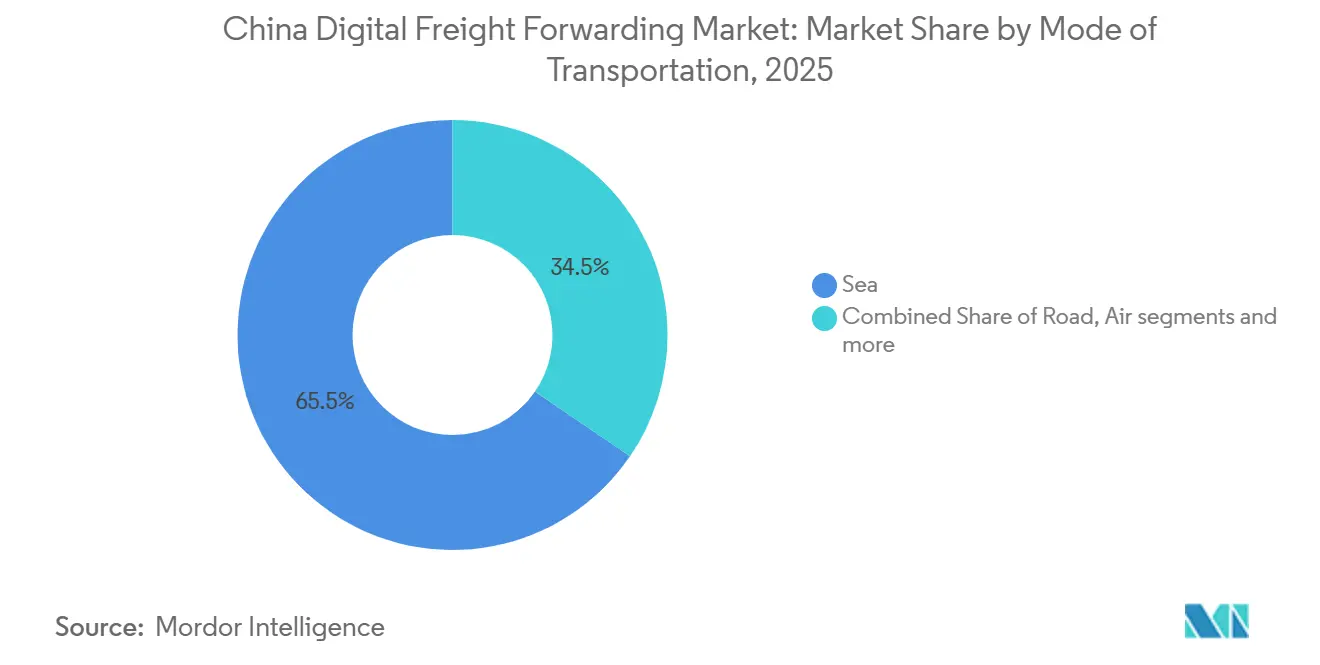

- By mode of transportation, sea freight led with 65.46% revenue share of the China digital freight forwarding market in 2025, while air cargo posted the highest projected CAGR at 23.27% through 2031.

- By enterprise size, small and medium enterprises held 60.14% of the China digital freight forwarding market share in 2025 and are advancing at a 23.00% CAGR to 2031.

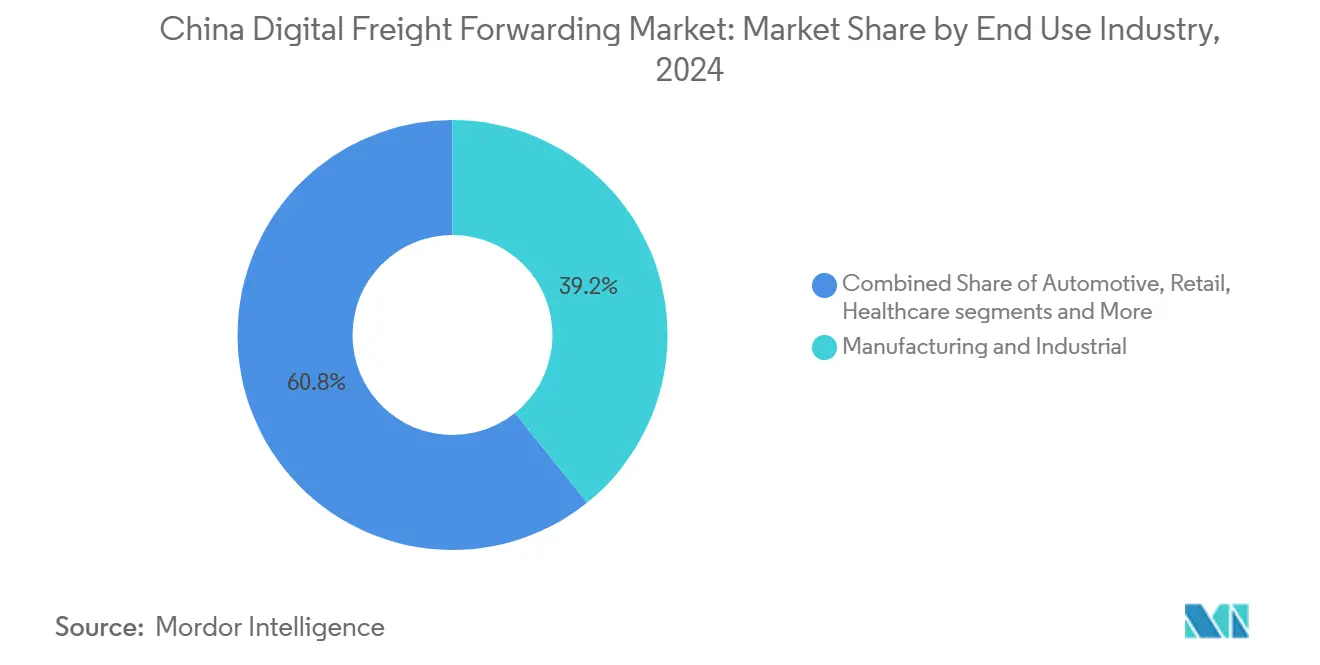

- By end-use industry, manufacturing and industrial users accounted for a 39.24% share of the China digital freight forwarding market size in 2025, while retail and e-commerce are expanding at a 24.25% CAGR to 2031.

- By deployment model, cloud platforms captured 80.09% share in 2025 and are growing at a 21.52% CAGR to 2031.

- By geography, East China commanded 41.38% share in 2025, whereas Southwest China recorded the strongest 21.84% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Digital Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory ESG-linked freight procurement is accelerating platform adoption | +3.6% | National, with early traction in tier-1 cities and state-owned enterprise supply chains | Medium term (2-4 years) |

| Nationwide roll-out of electronic Bills of Lading (eBL) under MoT guidelines | +3.2% | Coastal provinces initially, expanding to inland dry ports by 2028 | Long term (≥ 4 years) |

| Port community system integration providing live berth & container data to forwarders | +2.8% | East and South China coastal hubs, with limited inland penetration | Short term (≤ 2 years) |

| Beidou-enabled asset tracking enhances multimodal shipment visibility | +3.4% | National coverage, with the highest adoption in cross-border rail and road corridors | Medium term (2-4 years) |

| Rapid growth in China–LATAM cross-border e-commerce fuelling digital air-cargo bookings | +3.9% | Originating from East and South China, destination-focused on Brazil, Mexico, and Chile. | Short term (≤ 2 years) |

| Pilots of e-CNY smart-contract escrow shortening settlement cycles for SME shippers | +2.8% | Pilot zones in Shenzhen, Suzhou, and Chengdu, with a gradual national rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESG-Linked Freight Procurement Accelerating Platform Adoption

Corporate purchasing policies now demand auditable emissions data, steering shippers toward platforms that integrate carbon calculators and route optimization tools. China’s dual-carbon pathway obliges state-owned groups to track Scope 3 logistics emissions, prompting faster onboarding to digital dashboards that allocate loads to lower-carbon rail or coastal feeder options. The Shanghai Environment and Energy Exchange launched voluntary logistics carbon credits in 2025, letting forwarders monetize efficiency gains and rebate value to customers, reinforcing loyalty. Platforms that cannot certify emissions face exclusion from high-value automotive and electronics tenders exposed to EU carbon border rules. Early adopters report premium pricing tolerance for verified low-carbon routes, signaling durable demand growth.

Nationwide Roll-out of Electronic Bills of Lading Under MoT Guidelines

The Ministry of Transport made electronic Bills of Lading mandatory in 2025, cutting average settlement from ten days to under forty-eight hours. Blockchain registries protect title integrity, lowering documentary fraud and opening access to cheaper working-capital finance. Digital freight forwarders embed eBL issuance directly into booking flows, allowing exporters to combine shipment creation, financing, and title transfer in one interface. Interoperability through the ICC Digital Standards Initiative means Chinese eBLs are now recognized in eighty-seven jurisdictions. Smaller regional carriers still lag on IT readiness, creating a two-speed market in which tech-enabled operators attract premium cargo.

Port Community System Integration Providing Live Berth & Container Data to Forwarders

Shanghai Port linked its community system to freight platforms in 2025, granting live berth and yard visibility over 42 million TEU of throughput. Forwarders can divert loads before congestion builds, trimming demurrage that once cost Chinese shippers USD 2-3 billion a year. National rollout to thirty-four ports by 2027 is planned, though some authorities resist data sharing that could reveal commercial secrets. Platforms with privileged API access quote tighter lead times, capturing contracts from exporters tired of opaque legacy fee structures.

Beidou-Enabled Asset Tracking Enhancing Multimodal Visibility

Beidou’s global coverage now powers centimeter-level tracking across road, rail, and inland waterway legs. Over 1.2 billion logistics devices will use the constellation by the end of 2025. Short-message functionality keeps containers visible even when cellular service drops, a critical advantage on cross-border rail corridors. Digital platforms subsidize device installs for SME carriers to close network gaps, and insurers reward participants with lower cargo-damage premiums. Beidou regulation under the Belt and Road Initiative effectively sets a domestic standard that disadvantages non-compatible foreign systems[1]China Satellite Navigation Office, “Beidou Navigation Satellite System,” BEIDOU.GOV.CN.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inland container-depot congestion is undermining schedule reliability for digital bookings | -2.6% | Yangtze River Delta and Pearl River Delta transshipment hubs | Short term (≤ 2 years) |

| Escalating cyber-insurance premiums for logistics SaaS providers | -1.8% | National, with an acute impact on cloud-based platform operators | Medium term (2-4 years) |

| Provincial protectionism favouring local trucking alliances over national platforms | -2.4% | Central and Western provinces with entrenched state-owned logistics operators | Long term (≥ 4 years) |

| Ambiguous VAT rebate rules for cross-border digital services are eroding profit margins | -1.9% | Cross-border e-commerce corridors, particularly impacting air-cargo platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inland Container-Depot Congestion Undermining Schedule Reliability for Digital Bookings

Depots in Ningbo and Shanghai frequently operate above 95% capacity, forcing trucks to idle six to eight hours, which breaks the predictive ETAs promised by booking algorithms. Shippers lose confidence and revert to legacy forwarders that buffer delays through relationships rather than data. Despite port automation, the China Ports and Harbours Association logged an 18% rise in average dwell times during 2025. Platforms lack the authority to prioritize their boxes or finance new yard capacity, limiting influence over this chokepoint.

Escalating Cyber-Insurance Premiums for Logistics SaaS Providers

Premiums for logistics SaaS rose 40-60% over 2024-2026, reflecting ransomware spikes and tighter Personal Information Protection Law penalties. Insurers now demand ISO 27001 certifications, penetration tests, and air-gapped backups that add up to USD 2 million in annual overhead for mid-size firms[2]Cyberspace Administration of China, “Data Protection Regulations,” CAC.GOV.CN. Net margins, already at 8-12%, come under strain, forcing trade-offs between security spend and product R&D. Smaller platforms risk shutdown if a breach triggers fines of up to 5% of revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transportation: Sea Freight Dominates While Air Cargo Scales Fast

Sea freight accounted for 65.46% of the China digital freight forwarding market share by mode of transportation in 2025, underpinning the China digital freight forwarding market through consolidated container flows that platforms stitch together from smaller loads. The China digital freight forwarding market size for air services is forecast to expand at 23.27% CAGR as eBLs lift administrative bottlenecks. Platforms gain margin by filling outbound capacity and securing discounted backhauls[3].Ministry of Transport of the People’s Republic of China, “Digital Freight and Transport Data,” MOT.GOV.CN

Live rate-shopping and instant booking help SME exporters convert faster. Rail’s share inches up as China Railway Express adds cold-chain wagons, yet customs fragmentation across twelve countries tempers adoption. Road freight stays essential for first- and last-mile connectivity; Beidou tracking narrows the visibility gap with containerized modes, cutting empty kilometers by double digits.

By Enterprise Size: SMEs Lead Both Volume and Growth

SMEs contributed 60.14% share of the total China digital freight forwarding market size by enterprise size in 2025 and are forecast to outpace large enterprises at a 23.00% CAGR, reflecting platforms’ ability to pool shipments and democratize trade finance. The China digital freight forwarding market share of SME users rises steadily because cloud dashboards and mobile apps are limited to in-house logistics resources.

E-CNY smart-contract escrow reduces working-capital lockup, improving SME cash flow and lowering dependence on expensive factoring. Large enterprises maintain direct carrier contracts but now use platforms for spot overflow loads and peripheral trade lanes. The Chinese digital freight forwarding industry increasingly supports hybrid procurement, blending long-term carrier deals with agile digital bookings to cover peaks.

By End-Use Industry: Manufacturing Base Meets Retail Acceleration

Manufacturing and industrial clients held 39.24% of 2025 demand, drawn by end-to-end visibility that supports lean inventory. The China digital freight forwarding market size for manufacturing cargo will expand with dual-carbon monitoring tools that satisfy EU carbon border checks.

Retail and e-commerce show the fastest 24.25% CAGR as cross-border sellers bypass wholesalers and need agile fulfillment. Apparel, electronics, and consumer goods makers rely on dynamic routing that matches flash-sale order spikes. Healthcare and pharma cargo grows steadily through GDP-compliant cold-chain features, while agriculture benefits from temperature alerts that cut spoilage. Automotive exporters leverage ESG dashboards to document Scope 3 cuts demanded by global OEMs.

By Deployment Model: Cloud Platforms Sustain Leadership

Cloud solutions owned 80.09% of 2025 deployments and are projected to grow at 21.52% CAGR, keeping the China digital freight forwarding market firmly cloud-first. Multi-tenant architecture lowers unit costs and speeds feature releases such as AI-based demand forecasts[4].Cyberspace Administration of China, “Cloud Computing and Data Infrastructure Development,” CAC.GOV.CN

The China digital freight forwarding industry still hosts on-premise systems among state enterprises with classified cargo or strict data-residency rules. Yet cross-border data flow reforms under the Multi-Level Protection Scheme v2.0 eased perceived risks, triggering migration roadmaps even among conservative shippers. Shared security layers help cloud users mitigate the surge in cyber-insurance premiums.

Geography Analysis

East China retained 41.38% share in 2025 thanks to Shanghai, Ningbo, and Qingdao ports and dense expressway grids that shorten truck drays. Real-time port community data feeds allow platforms in the region to promise tighter schedule accuracy, sustaining exporter loyalty despite yard congestion. ESG-linked purchasing among coastal electronics clusters accelerates digital uptake as firms chase verified carbon savings.

Southwest China shows the highest 21.84% CAGR through 2031, powered by the New International Land-Sea Trade Corridor that funnels Chongqing exports directly to Qinzhou Port on the Gulf of Tonkin. Provincial pilot zones there test Beidou asset tracking across river–rail interchanges and waive platform licensing fees, cutting barriers to entry. Yet local trucking cooperatives enjoy preferential subsidies that still lock out national players unless they form joint ventures.

Central and North China post healthy growth, benefiting from manufacturing expansion along the Zhengzhou-Wuhan axis and better China Railway Express links to Europe. Inland dry ports integrate customs and bonded warehousing, reducing diversion to congested coastal ports and raising the China digital freight forwarding market's presence inland. Northeast China lags slightly due to slower industrial momentum, but gains from Dalian’s shipping hub development. Northwest China trails as sparse population reduces freight densities, though Belt and Road investments slowly build baseline volumes.

Competitive Landscape

The China digital freight forwarding market remains low fragmented. National platforms offer multimodal coverage and embedded finance, while regional players focus on single corridors or commodities. Data advantages accrue to leaders that ingest port community feeds, Beidou pings, and carbon metrics into pricing engines, enhancing quote precision and lane profitability.

Vertical integration is a defining theme. Full Truck Alliance now bundles trade-finance and driver carbon accounts, locking in shippers that value ESG evidence. Cainiao and SF Express deploy dedicated freighters and warehouses, giving hybrid digital-physical control that few pure tech startups can match. JD Logistics pushes stable-coin experiments to compress cross-border payment cost and latency.

Fragmentation persists where provincial rules favor local fleets or where niche cargoes require specialized compliance. New entrants pursue micro-segments such as hazardous chemicals or project cargo that command premium yields. Consolidation is expected as cybersecurity costs outstrip the capital of smaller apps, prompting tie-ups with asset owners eager for algorithmic capability.

China Digital Freight Forwarding Industry Leaders

Flexport

DHL

Full Truck Alliance

Kuhene+Nagel

SF Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group and JD.com signed a Memorandum of Understanding to build end to end logistics solutions for German and European brands selling into China through JD’s platforms, including preferential customs duties and VAT schemes for B2C parcels from Europe to China.

- February 2026: DHL Group supported new UK-China trade facilitation developments, enabling easier SME access to China. Enhances DHL’s positioning in cross-border freight forwarding and advisory services for China-bound trade.

- January 2026: DHL Group supported new UK–China trade facilitation developments, enabling easier SME access to China. Enhances DHL’s positioning in cross-border freight forwarding and advisory services for China-bound trade.

- September 2025: Maersk outlined its Greater China strategy focusing on integrated end to end logistics solutions (ocean, air, intermodal, warehousing, and supply chain management) tailored to local industry needs, including contract logistics and value added services around its Lin Gang, Shanghai flagship fulfilment facility that integrates warehousing, customs, and distribution with real time inventory visibility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China digital freight forwarding market as the gross fees earned by online-native or fully software-enabled forwarders that arrange ocean, air, road, and rail shipments while providing instant quotes, paperless documentation, and live tracking to shippers. Revenue from traditional 3PLs is counted only when the entire booking to proof-of-delivery cycle runs through an integrated digital workflow.

Shipments handled solely through phone, fax, or email without a front-end platform are excluded.

Segmentation Overview

- By Mode of Transportation

- Ocean

- Air

- Road

- Rail

- By Enterprise Size

- Small & Medium Enterprises

- Large Enterprises

- By End-use Industry

- Manufacturing & Industrial

- Retail & E-commerce

- Automotive

- Electronics & High-Tech

- Healthcare & Pharmaceutical

- Agriculture & Perishables

- Others

- By Deployment Model

- Cloud-Based Platforms

- On-Premise Solutions

- By Geography

- East China

- South China

- Central China

- North China

- Northeast China

- Southwest China

- Northwest China

Detailed Research Methodology and Data Validation

Primary Research

We interviewed digital platform founders, port community managers, and export-oriented SME shippers across East, South, and Southwest China. Their insights on adoption rates, average shipment values, and margin trends closed data gaps and confirmed desk estimates before we finalized assumptions.

Desk Research

We pulled macro trade and logistics indicators from the National Bureau of Statistics, General Administration of Customs, Ministry of Transport, and China Internet Network Information Center to size freight pools, SME counts, and internet reach. Policy circulars from the China Federation of Logistics & Purchasing and provincial smart-logistics pilots mapped regulatory stimuli and funding. Company filings, investor decks, and high-circulation business press clarified platform take-rates and operating costs. Our analysts also tapped D&B Hoovers for private financial clues and Factiva for deal alerts, sharpening benchmarks. These references are illustrative; many additional sources supported data gathering, validation, and clarification.

Market-Sizing & Forecasting

We built a combined top-down and bottom-up model. National cargo volumes, freight spend, and SME counts were filtered through verified digital adoption ratios and then checked against sampled platform revenue (average selling price multiplied by shipment volume) for consistency. Core inputs include e-commerce gross merchandise value growth, TEU throughput at Shanghai and Ningbo-Zhoushan, smartphone penetration, cloud TMS usage, and RMB-USD exchange rates. Multivariate regression with ARIMA smoothing projects values to 2030, while scenario analysis gauges tariff or fuel shocks. Lane-level gaps were bridged with calibrated proxies from comparable corridors.

Data Validation & Update Cycle

Model outputs face peer review, variance screens, and, when needed, follow-up calls. Mordor analysts refresh the dataset each year, with interim updates triggered by material events so clients always receive the latest view.

Why Mordor's China Digital Freight Forwarding Baseline Merits Confidence

Published estimates often differ because providers select varying revenue buckets, adoption factors, and refresh cadences. By limiting scope to truly digital workflows and re-checking drivers every twelve months, Mordor Intelligence narrows this spread.

Key gap drivers at other publishers include the addition of courier brokerage, use of static digital-share multipliers, and infrequent field validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.24 B (2025) | Mordor Intelligence | - |

| USD 8.80 B (2024) | Global Consultancy A | Adds courier brokerage and shipment insurance to digital forwarding revenue |

| USD 30.00 B (2024) | Industry Analytics Firm B | Blends traditional forwarding turnover and applies fixed 20% digital share without field validation |

The comparison shows that our disciplined variable selection, recurring primary checks, and transparent calculations give decision-makers a balanced baseline they can trust.

Key Questions Answered in the Report

What growth rate is expected for China’s platform-based freight forwarding between 2026 and 2031?

A compound annual growth rate of 20.07% is forecast, taking value from USD 6.30 billion in 2026 to USD 18.88 billion by 2031.

Which transport mode currently brings in the most platform revenue?

Sea freight contributes 65.46% of the 2025 platform revenue because containerized exports dominate China’s trade mix.

Why are small and medium exporters adopting digital freight platforms fastest?

Platforms pool capacity, offer automated trade finance, and now clear e-CNY escrow payments within one day, easing cash strain for SMEs.

Which region shows the quickest market expansion?

Southwest China is advancing at a 21.84% CAGR thanks to the New International Land-Sea Trade Corridor and supportive pilot zones.

How do electronic Bills of Lading affect transaction speed?

EBLs cut settlement windows from up to ten days to under forty-eight hours by enabling instantaneous, blockchain-backed title transfer.

What is the main cybersecurity challenge for logistics SaaS firms?

Rapidly rising cyber-insurance premiums force platforms to invest heavily in certifications and backups, squeezing profit margins.

Page last updated on: