Middle East Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 21.81 Billion |

| Market Size (2030) | USD 28.60 Billion |

| Growth Rate (2025 - 2030) | 5.56% CAGR |

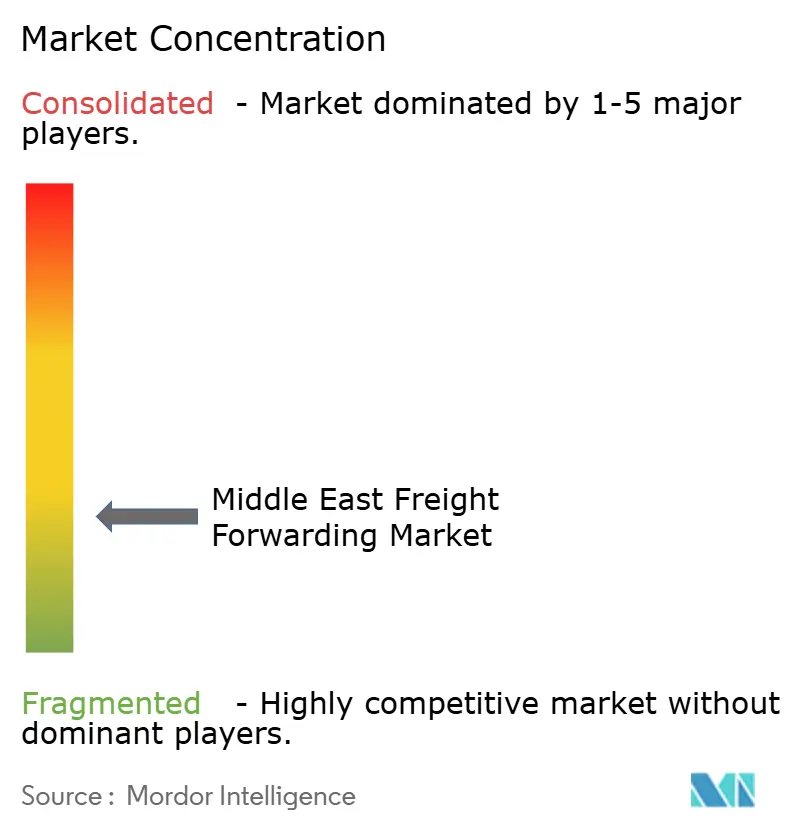

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Freight Forwarding Market Analysis by Mordor Intelligence

The Middle East Freight Forwarding Market size is estimated at USD 21.81 billion in 2025, and is expected to reach USD 28.60 billion by 2030, at a CAGR of 5.56% during the forecast period (2025-2030).

This trajectory stems from the region’s role as a bridge linking Asia, Europe, and Africa, combined with Vision 2030 infrastructure programs, multimodal investments, and fast-scaling e-commerce. Saudi Arabia, the United Arab Emirates, and Turkey channel capital into ports, airports, and rail corridors that shorten transit times and lower total landed costs. Digital freight platforms gain ground, allowing real-time tracking, automated customs clearance, and predictive routing. Heightened sustainability mandates motivate shippers to favor providers offering carbon-neutral solutions, while ongoing Red Sea routing shifts redistribute volumes toward Gulf gateways.

Key Report Takeaways

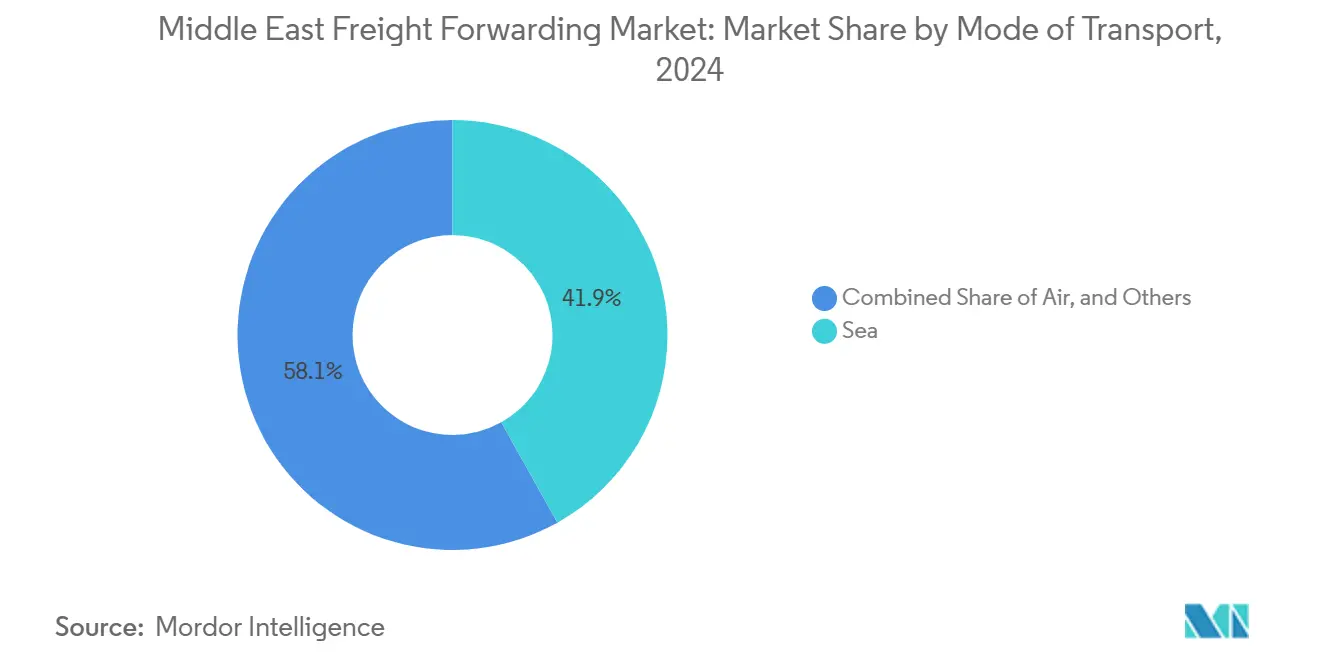

- By mode of transport, sea freight held 41.89% of the Middle East freight forwarding market share in 2024. Air freight forwarding is forecast to expand at a 6.12% CAGR to 2030.

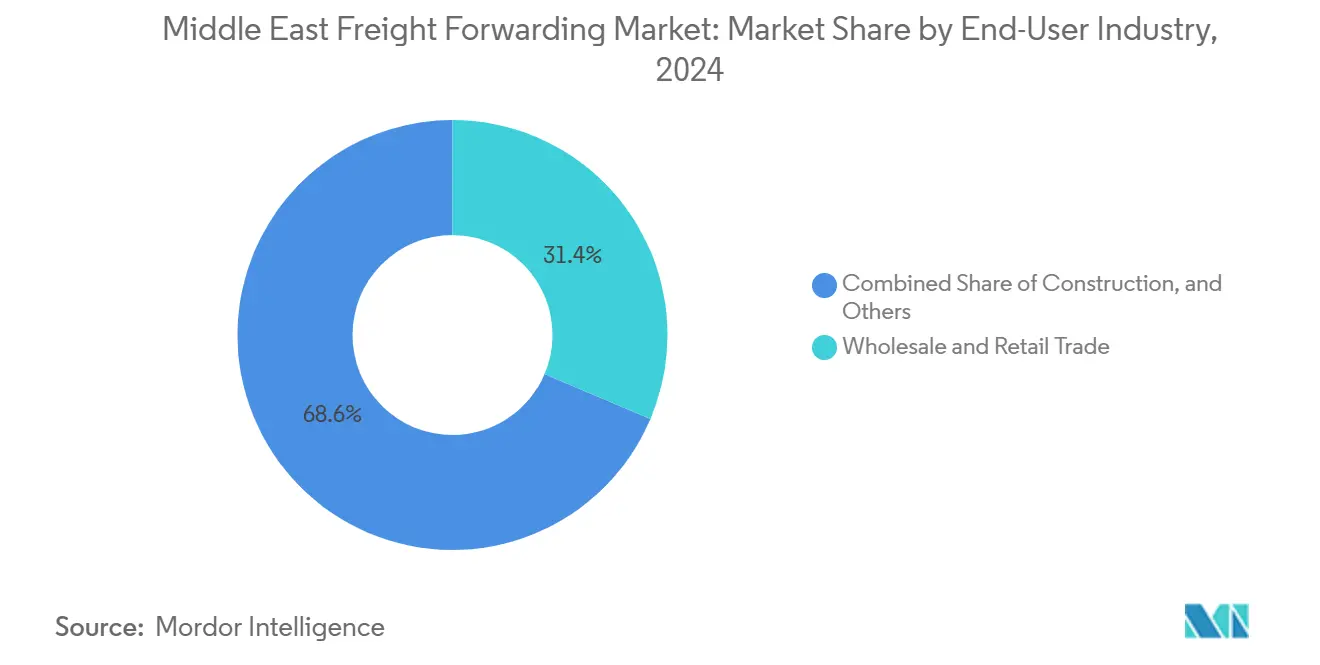

- By end-user, wholesale and retail trade commanded 31.38% share of the Middle East freight forwarding market size in 2024 and is advancing at a 6.29% CAGR through 2030.

- Saudi Arabia led with 39.30% revenue share in 2024, while the United Arab Emirates records the highest projected CAGR at 5.95% through 2030.

Middle East Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid GCC e-commerce boom | +0.8% | GCC core, spillover to Egypt and Turkey | Medium term (2-4 years) |

| Post-pandemic nearshoring of inventories | +0.7% | Global, with concentration in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Multimodal infrastructure investments (Vision 2030 programs) | +0.7% | Saudi Arabia and UAE primary, regional spillover | Long term (≥ 4 years) |

| Digital freight platform adoption | +0.5% | UAE leading, expanding to Saudi Arabia and Qatar | Medium term (2-4 years) |

| Green shipping mandates pushing 3PL outsourcing | +0.4% | Global impact, early adoption in UAE and Saudi Arabia | Long term (≥ 4 years) |

| Growing trade corridors with Asia and Africa | +0.6% | Regional hub focus in UAE, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid GCC e-commerce boom

Online retail sales in the Gulf Cooperation Council are set to reach USD 50 billion by 2025, expanding at 12.7% annually. Surging parcel volumes require dense urban fulfillment networks, flexible last-mile options, and robust reverse-logistics. Saudi Arabia’s e-commerce turnover leaped 35% in 2024, forcing freight forwarders to integrate cross-border clearance with domestic distribution. Retailers seeking end-to-end visibility contract providers that offer API-based booking, dynamic routing, and real-time proof-of-delivery. The scale of consumer demand accelerates warehouse automation, cargo flights, and bonded-zone utilization[1]“Vision 2030 Strategic Objectives,” Saudi Vision 2030, vision2030.gov.sa .

Post-pandemic nearshoring of inventories

Multinational firms rebalanced safety stocks into Gulf free zones to buffer supply shocks, with 40% establishing distribution centers in 2024 surveys. UAE and Saudi clusters provide duty-free re-exports, bonded storage, and single-window customs that cut order-to-delivery cycles. Electronics, pharma, and automotive firms channel deferred assembly and labeling to regional hubs, raising demand for temperature-controlled storage, value-added services, and multi-country consolidation. Freight forwarders enlarge contract logistics footprints inside Jebel Ali Free Zone and Riyadh Integrated Logistics Park to meet resilient supply planning[2]“Middle East Air Cargo Market Analysis 2024,” International Air Transport Association, iata.org .

Multimodal infrastructure investments

Vision 2030 programs commit more than USD 500 billion to airports, ports, and rail. King Salman International Airport targets 3.5 million tons of annual cargo by 2030. The Saudi Landbridge rail line will link Jeddah with Dammam in under 18 hours, enabling Asia-Europe cargo to bypass the Suez Canal. UAE’s Etihad Rail network integrates with Khalifa Port to allow direct block trains to free zones. Such projects let forwarders design cost-efficient sea-rail solutions, reduce overland emissions, and diversify corridors amid Red Sea unrest.

Digital freight platform adoption

GCC governments champion paperless trade; Dubai aims for 50% of transactions via blockchain by 2025. AI-driven platforms match shippers with capacity, forecast dwell-time, and automate insurance issuance. Regional forwarders launch cloud portals that provide instant quotes and milestone alerts, compressing booking cycles from days to minutes. Early adopters convert data insights into lane optimization and predictive maintenance, winning long-term contracts from omnichannel retailers and pharma majors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical flashpoints disrupting trade routes | -0.8% | Regional, with acute impact on Red Sea and Persian Gulf routes | Short term (≤ 2 years) |

| Customs harmonization gaps among Middle East countries | -0.5% | Regional, particularly affecting cross-border trade flows | Medium term (2-4 years) |

| Driver shortages and rising labor costs | -0.4% | GCC core, expanding to other regional markets | Medium term (2-4 years) |

| Limited cold-chain capacity for perishables | -0.3% | Regional, with acute gaps in secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical flashpoints disrupting trade routes

Red Sea security incidents pushed freight rates on the Asia-Europe lane up by 15-20% in 2024. Rerouted vessels lengthened transit times by up to 10 days, heightening demand for alternative Gulf gateways and air-sea solutions. Forwarders absorbed higher war-risk premiums and fuel costs while arranging contingency paths via Dammam, Khor Fakkan, and Salalah. Contract negotiations now embed escalation clauses and multimodal redundancy, increasing complexity and working-capital exposure[3]“Digital Economy Strategy 2025,” UAE Ministry of Economy, moec.gov.ae.

Customs harmonization gaps among Middle East countries

The GCC Customs Union remains only partly implemented, leaving divergent duty codes, HS interpretations, and clearance documents. Shippers face inconsistent inspection regimes that prolong border dwell and inflate compliance costs. Forwarders maintain teams specialized in each country’s e-manifest and VAT rules, limiting scalability. Absence of unified risk-management platforms postpones full digital-border rollouts, delaying potential savings from truck-train interlining and bonded transshipment[4]“GCC Customs Union Implementation Status,” GCC Secretariat, gcc-sg.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Sea Freight Retains Scale Advantage as Air Cargo Climbs

Sea freight secured 41.89% of the Middle East freight forwarding market share in 2024 on the strength of cost-efficient bulk movements and deepwater hubs. Jebel Ali, King Abdullah Port, and Sohar continue to add berths for ultra-large container vessels. The Middle East freight forwarding market size tied to maritime volumes is poised to expand along Asia-Africa corridors as shippers substitute Suez transits with Gulf discharge and feeder networks. Forwarders bundle port trucking, cross-docking, and value-added packaging to capture margin beyond ocean freight.

Air freight, though smaller, posts the fastest gains with a 6.12% CAGR through 2030. IATA projects a 12.3% rise in Middle East air cargo tonnage in 2024 amid surging demand for express e-commerce parcels, time-critical spares, and biomedical shipments. Gulf carriers exploit 5th-freedom rights to link East-West routes, while new dedicated freighters at Al Maktoum International Airport open overnight Middle East-Europe lanes. Digital booking portals that quote dynamic all-in rates help medium-sized shippers switch to air during disruption, reinforcing growth momentum.

By End-User: Wholesale and Retail Trade Sets the Pace

Wholesale and retail trade accounted for 31.38% of 2024 revenue, the largest slice of the Middle East freight forwarding market size, and leads growth at a 6.29% CAGR. Mall operators, grocery chains, and online marketplaces require omnichannel fulfillment, inventory visibility, and last-mile orchestration. The rise of cross-border fashion and electronics sales through GCC duty-paid models spurs demand for bonded warehousing, multi-country consolidation, and returns management.

Energy, construction, and manufacturing segments collectively generate steady volumes tied to regional infrastructure spending and industrial diversification. Project cargo linked to NEOM, hydrogen plants, and solar farms drives heavy-lift charters and out-of-gauge trucking. Pharmaceutical and agrifood verticals, while smaller, command premium yields for temperature-controlled and GDP-compliant handling. ISO 9001 and GDP certification increasingly influence tender awards as shippers tighten quality metrics.

Geography Analysis

Saudi Arabia’s 39.30% share of the Middle East freight forwarding market stems from Vision 2030 programs that pour billions into ports, airports, and rail. King Salman International Airport will process 3.5 million tons of cargo annually by 2030, rivalling Dubai World Central. NEOM’s Oxagon logistics cluster offers automated warehouses, hyper-loop feasibility trials, and hydrogen-powered trucks. Landbridge rail cuts Jeddah-Dammam transit to under 18 hours, enabling sea-rail solutions that bypass congested chokepoints.

The United Arab Emirates posts the region’s fastest expansion at a 5.95% CAGR. Jebel Ali remains the Gulf’s top container gateway, while Khalifa Port and Al Maktoum International Airport provide incremental capacity. Dubai Customs’ blockchain platform reduces declaration time to under 10 minutes, trimming clearance overhead. Abu Dhabi’s industrial drive in aluminum, biopharma, and clean energy pulls specialized cargo flows requiring GDP-certified storage and project-cargo engineering.

Turkey, Egypt, and a cluster of smaller Gulf states add geographic depth. Turkey’s customs-union ties with the EU foster just-in-time automotive and textile flows linking Bursa and Gaziantep to Leipzig and Milan. Egypt’s Suez Canal Economic Zone combines bonded manufacturing and port handling, keeping east-west relay traffic even as shippers hedge Red Sea risk. Qatar, Bahrain, Kuwait, and Oman carve niches in LNG, petrochemicals, and cruise-linked perishables, sustaining demand for tailored 3PL services.

Competitive Landscape

The market is fragmented, keeping competition moderate and opportunity broad. Global integrators such as DHL, DSV, and CEVA leverage end-to-end networks and multi-country brokerage to secure enterprise contracts. Regional specialists like Aramex and GAC differentiate through local knowledge, customs expertise, and Arabic-language customer service. Digital entrants deploy asset-light marketplaces that connect shippers to under-utilized capacity, offering instant booking and milestone alerts.

Strategic moves center on automation and sustainability. DHL earmarked USD 750 million for robotic sorters and extra freighters through 2027, aiming to cut transit times for e-commerce exports. DP World’s USD 2.2 billion port-terminal acquisitions extend its controlled berth count by 40%, enabling integrated sea-land corridors. Aramex launched a blockchain-based freight platform targeting SMEs requiring simplified documentation. Patent filings tracked by WIPO reveal rising R&D in automated container handling and electric drayage trucks. Providers that bundle visibility, compliance reporting, and green-logistics options win long-term contracts from pharmaceuticals and high-tech manufacturers.

Middle East Freight Forwarding Industry Leaders

DHL Group

Aramex

Almajdouie Logistics

Al-Futtaim Logistics

Bahri Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DHL Group announced a USD 750 million Gulf expansion plan, including automated sort centers in Riyadh and expanded air-freight capacity at Dubai International Airport.

- December 2024: DP World completed a USD 2.2 billion acquisition of port terminals in Egypt and Turkey, lifting regional handling capacity by 40%.

- November 2024: Aramex launched “Aramex Connect,” an AI-powered digital freight platform in the UAE and Saudi Arabia.

- October 2024: DSV merged with Gulf Logistics Solutions, creating a USD 1.8 billion regional entity.

Middle East Freight Forwarding Market Report Scope

| Air Freight Forwarding |

| Sea Freight Forwarding |

| Others |

| Oil and Gas, Mining and Quarrying |

| Construction |

| Manufacturing |

| Agriculture, Fishing, and Forestry |

| Wholesale and Retail Trade |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Turkey |

| Egypt |

| Qatar |

| Bahrain |

| Kuwait |

| Oman |

| Rest of Middle East |

| By Mode of Transport | Air Freight Forwarding |

| Sea Freight Forwarding | |

| Others | |

| By End-User | Oil and Gas, Mining and Quarrying |

| Construction | |

| Manufacturing | |

| Agriculture, Fishing, and Forestry | |

| Wholesale and Retail Trade | |

| Others | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| Qatar | |

| Bahrain | |

| Kuwait | |

| Oman | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the projected value of the Middle East freight forwarding market by 2030?

The market is expected to reach USD 28.60 billion by 2030, reflecting a 5.56% CAGR.

Which mode currently leads the market in revenue terms?

Sea freight leads, holding 41.89% of 2024 revenue.

Which segment is the fastest-growing end user?

Wholesale and retail trade is advancing at a 6.29% CAGR through 2030.

Which country shows the highest growth rate?

The United Arab Emirates posts the fastest national CAGR at 5.95% between 2025 and 2030.

How are Red Sea disruptions affecting logistics costs?

Freight rates on some Asia-Europe corridors rose by 15-20% during 2024 due to rerouting.

What technological trends are reshaping the sector?

Digital freight platforms using AI and blockchain enable instant booking, customs automation, and predictive routing.

Page last updated on: