Philippines Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

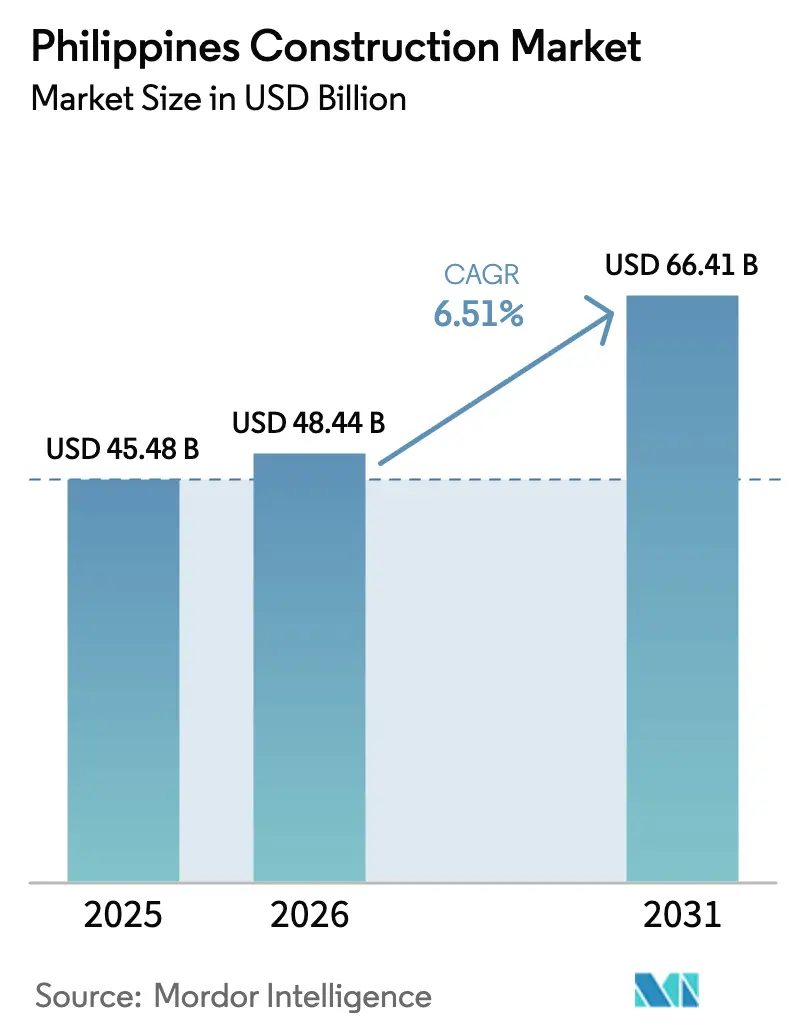

| Base Year Market Size (2025) | USD 45.48 Billion |

| Market Size (2026) | USD 48.44 Billion |

| Market Size (2031) | USD 66.41 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Construction Market Analysis by Mordor Intelligence

The Philippines Construction Market size is projected to be USD 45.48 billion in 2025, USD 48.44 billion in 2026, and reach USD 66.41 billion by 2031, growing at a CAGR of 6.51% from 2026 to 2031.

Consistent public infrastructure outlays, accelerating urban in-migration, and the early adoption of prefabricated modules are keeping the Philippines construction market on a steady upswing. Government programs such as “Build Better More,” combined with an expanding pipeline of township estates and data-center campuses, are anchoring contractor backlogs despite short-term typhoon disruptions. Private developers are pivoting toward mixed-use estates and logistics hubs, moves that balance the historical dominance of public spending and enhance cash-flow visibility for suppliers. At the same time, modular techniques, digital scheduling, and building information modeling are improving cost certainty and compressing hand-over times, an important hedge against material-price volatility and skilled-labor gaps.

Key Report Takeaways

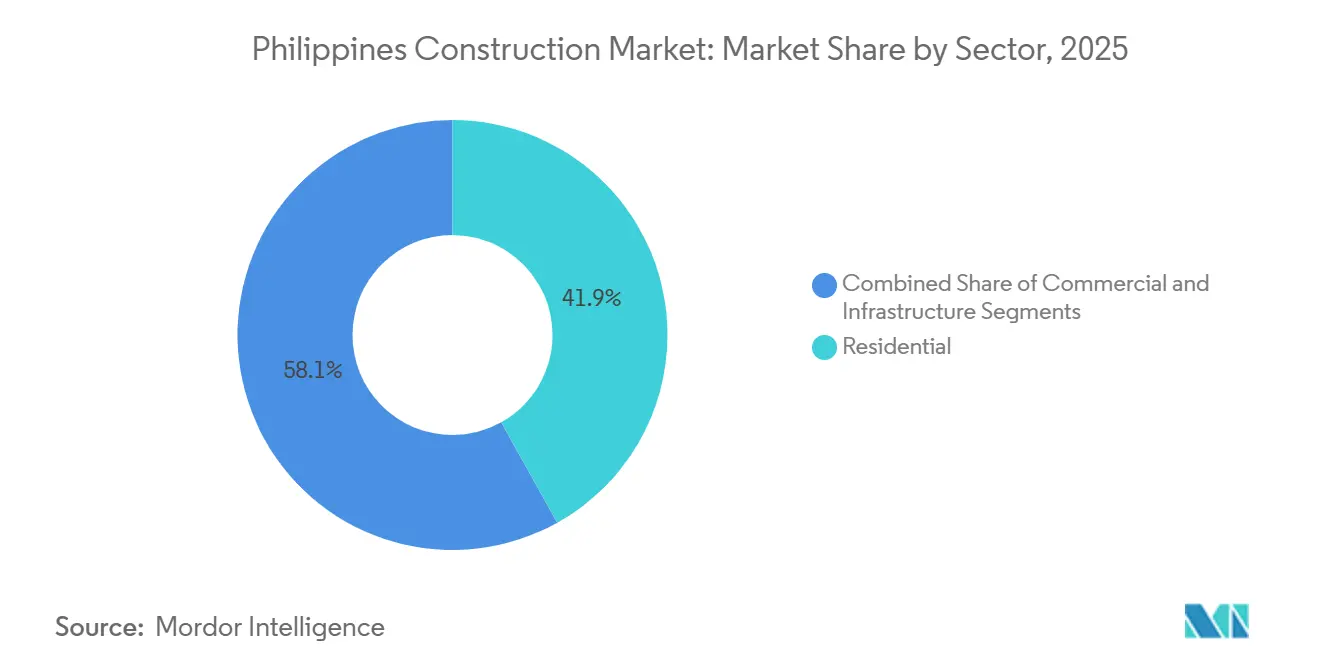

- By sector, residential captured 41.9% of the 2025 value, while infrastructure is projected to grow at a 6.95% CAGR through 2031

- By construction type, new builds accounted for 77.8% of 2025 spending, and renovation is forecast to advance at a 7.11% CAGR over 2026-2031.

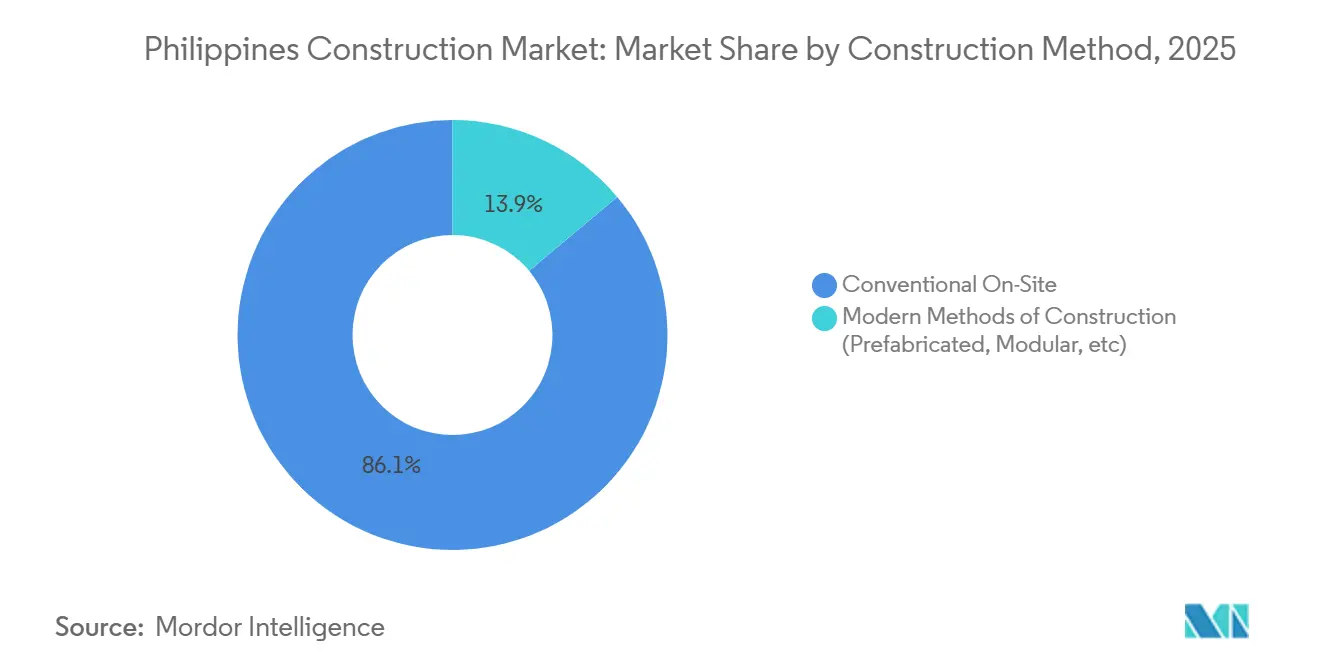

- By construction method, conventional on-site techniques held 86.1% in 2025, whereas modern modular systems are rising at a 7.09% CAGR to 2031.

- By investment source, public funding supplied 65.2% of the 2025 work, yet private investment is expected to expand at a 7.32% CAGR through 2031.

- By geography, Metro Manila held a 40.4% share in 2025, while Central Luzon is pacing all regions with a 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure rollout is sustaining demand for transport, utilities, and public works contractors | +2.1% | National, especially NCR, Calabarzon, and Central Luzon | Long term (≥ 4 years) |

| Rapid urban housing demand is increasing residential and township project launches | +1.8% | NCR, Calabarzon, Central Luzon, Cebu, Davao | Medium term (2-4 years) |

| Industrial and logistics expansion boosting warehouses, manufacturing parks, and port-linked builds | +1.3% | Calabarzon, Central Luzon, Cebu, Davao | Medium term (2-4 years) |

| Disaster-resilient rebuilding programs are driving retrofit and reconstruction activity | +0.9% | Visayas, Bicol, Eastern Mindanao | Short term (≤ 2 years) |

| Growth in tourism and commercial developments supporting hotels, malls, and mixed-use construction | +0.7% | NCR, Cebu, Boracay, Palawan, Clark | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Rollout Sustaining Demand for Transport, Utilities, and Public Works Contractors

Annual public works spending equal to about 6% of gross domestic product guarantees a multiyear construction queue for the Philippines construction market [1]Department of Public Works and Highways, “Infrastructure Program 2026,” dpwh.gov.ph . Signature projects include the 32-kilometer Bataan–Cavite Interlink Bridge, the 147-kilometer North-South Commuter Railway, and seismic upgrades on key Metro Manila bridges, all of which are already under contract. Energy packages are equally active: Aboitiz Power is adding 3,400 megawatts of solar, wind, and battery storage; Meralco PowerGen is erecting a 1,200 MW gas-fired plant in Batangas; and the Department of Energy has awarded 3,644 MW of renewable capacity in recent Green Energy Auctions[2]Department of Energy, “Green Energy Auction Results,” doe.gov.ph . These overlapping project streams keep heavy-equipment fleets fully deployed and underpin contractor hiring plans, even as rights-of-way disputes occasionally stall individual segments. Because each package is financed through a blend of official loans and domestic bond issues, payment risk is low, which helps local banks extend working-capital lines on favorable terms.

Rapid Urban Housing Demand Increasing Residential and Township Project Launches

Metro Manila packs more than 20,000 residents into every square kilometer, and planners expect 70% of Filipinos to live in urban areas by 2030[3]National Economic and Development Authority, “Urbanization Outlook 2030,” neda.gov.ph . To relieve pressure, the Department of Human Settlements and Urban Development (DHSUD) is rolling out the Pambansang Pabahay Para sa Pilipino program, targeting one million affordable units a year. Pilot projects in San Juan, Cebu, and Davao Oriental already use factory-built modules that cut on-site work from 18 to 6 months. Private developers have responded at scale: Megaworld committed USD 8.9 billion to 30 township estates between 2024 and 2028, while Ayala Land is pushing Vertis North, Arca South, and Vermosa to full build-out. Although the Philippine Statistics Authority logged a 27.3% slide in office-permit issuances during 3Q 2024, that lull is being offset by sustained condominium launches and community retail strips that feed residential absorption.

Industrial and Logistics Expansion Boosting Warehouses, Manufacturing Parks, and Port-linked Builds

Near-shoring and e-commerce fulfillment continue to enlarge the warehouse footprint across Luzon and the Visayas. International Container Terminal Services finished a 1.5 million-TEU terminal in Batangas in 2024, triggering auxiliary builds for cold-chain depots and truck yards. Philippine Economic Zone Authority approvals for semiconductor and electronics plants in Laguna, Cavite, and Clark are likewise driving purpose-built factory shells with redundant power and fiber links. Developers such as Filinvest are scaling innovation parks, while Maersk launched a reefer facility aimed at automotive components. Right-of-way clearances and environmental checks still add 12 to 18 months in many corridors, but most operators bake those delays into pro-formas, given the long-dated demand outlook and the Philippines construction market’s strategic position in regional trade flows.

Disaster-Resilient Rebuilding Programs Driving Retrofit and Reconstruction Activity

With roughly 20 typhoons striking the archipelago each year, mandated retrofits have become a permanent revenue line for structural specialists. The Department of Public Works and Highways is upgrading more than 21,000 public buildings to the National Structural Code of the Philippines, and the Department of Education has earmarked USD 179 million for storm-resilient schools in Catanduanes, Albay, and Eastern Samar. Leyte’s 12-kilometer storm-surge wall, co-financed by the World Bank and Japan, exemplifies the specialized civil-works skills now in demand. UNESCO programs in Vigan further illustrate how heritage facades can be braced with contemporary materials without compromising authenticity. These projects attract contractors able to combine geotechnical analysis, composite materials, and cultural-resource management, a niche that offers higher margins than commodity civil packages.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High material costs and import exposure are increasing project budgets and bid prices | -1.2% | National, strongest in island provinces | Short term (≤ 2 years) |

| Permitting, right-of-way, and land acquisition delays extend project timelines | -0.9% | National, especially NCR, Calabarzon, and Central Luzon | Medium term (2-4 years) |

| Skilled labor shortages and contractor capacity limits are slowing execution and raising costs | -0.7% | National, acute in Visayas and Mindanao | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Material Costs and Import Exposure Increasing Project Budgets and Bid Prices

Roughly 60% of cement clinker, 80% of steel rebar, and nearly all heavy machinery are imported, leaving builders exposed to exchange swings and freight spikes. The wholesale index for core materials climbed 4.2% year-on-year in December 2025, while a 10% safeguard tariff on cement added USD 3 per 40-kilogram bag. Ocean freight rose sharply after Red Sea diversions and Panama Canal droughts, tacking USD 15–20 a ton onto landed steel in Manila. Financing conditions remain tight, with the Bangko Sentral ng Pilipinas holding its key rate at 6.25% through 2025. Contractors are now inserting price-adjustment clauses, stockpiling steel during low-season months, and substituting fly-ash binders to temper cement demand, but margins on provincial projects remain thin because inter-island shipping premiums hit 20–30%.

Permitting, Right-of-Way, and Land Acquisition Delays Extending Project Timelines

The Accelerated Right-of-Way Act, signed in September 2025, promises quicker expropriations, yet local implementation lags. Metro Manila Subway’s inaugural section slipped from 2028 to 2032 after land title disputes in Quezon City, and North-South Commuter Railway packages are on hold until 18 Laguna and Cavite parcels clear litigation. The Commission on Audit flagged USD 232 million in unused Bicol road budgets for similar reasons. Private deals also suffer: a USD 21 million Cebu market redevelopment idled 14 months over zoning appeals. Industry groups want a centralized ROW office inside the public-works agency, but budget authorization is still pending, meaning scheduling buffers remain a hard-baked necessity in the Philippines construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Dominates as Infrastructure Accelerates

Residential work captured 41.9% of the 2025 value, buoyed by the 4PH social-housing push and steady condominium launches in Metro Manila, Cebu, and Davao. Demand is strongest for mid-rise towers that balance affordability, seismic resilience, and proximity to transit lines. Infrastructure, however, is the fastest-growing slice of the Philippines construction market, logging a 6.95% CAGR on the back of rail, bridge, and flood-control megaprojects. Contractor mobilization on the North-South Commuter Railway and Bataan–Cavite Bridge is already lifting equipment rentals and steel shipments, and those programs will keep the steel mills in full production through 2031.

Apartments and condominiums set the urban tone, yet landed housing still appeals to middle-income buyers in Calabarzon and Central Luzon, where land costs are lower. Commercial builds are selective: the 27.3% slide in 2024 office permits signaled caution, but warehouse and data-center shells remain fully booked for Clark, Batangas, and Laguna corridors. Energy packages are another growth pocket as 3,644 MW of auctioned renewables move into civil works mode. All told, infrastructure’s share of the Philippines construction market size for public contracts is widening each year, a pivot that buffers cyclical dips in private high-rise starts.

By Construction Type: New Builds Command Spending While Renovation Gains Pace

New builds accounted for 77.8% of the 2025 volume, reflecting an economy still adding railways, power plants, and greenfield townships. Renovation, though, is picking up at a 7.11% clip as public-school retrofits, heritage upgrades, and adaptive-reuse office conversions enter contractor pipelines. The seismic makeover of 21,000 government facilities alone assures steady demand for structural engineers and specialty trades through the decade.

Commercial landlords in Makati and Ortigas are installing fiber, variable-refrigerant air-conditioning, and flexible floor plates to retain business-process-outsourcing tenants at competitive rents. Hotel owners, led by New Coast Manila’s USD 36 million facelift, are repositioning older stock for meetings and conferences. This dual-track market lets general contractors hedge volumes: megaproject teams chase greenfield rail viaducts, while in-city specialists focus on retrofit packages where return on labor is higher, and material scope is narrower. The combined effect supports a balanced Philippines construction market share across greenfield and brownfield segments.

By Construction Method: Conventional Techniques Prevail, Modular Systems Accelerate

Conventional on-site pouring and rebar tying still held 86.1% of 2025 spend, but modern methods of construction are expanding at a 7.09% CAGR. The DHSUD’s modular rollouts in San Juan, Cebu, and Davao cut site labor by 60% and showcase how offsite fabrication can meet one-million-unit housing goals. DoubleDragon’s Hotel101 used precast panels to stay on schedule during 2024 typhoon weeks, underscoring private-sector appetite for predictable timelines.

Large bridges and rail viaducts will remain cast-in-place domains because segmental launches and cable stays need specialized formwork and heavy cranes. Still, regional plants for precast girders, tunnel linings, and bathroom pods are starting to open, often in partnership with Japanese or Chinese engineering firms that share design templates. As these facilities ramp up, the Philippines construction market size for modular units is expected to top USD 3 billion by 2031, easing the skill-gap crunch flagged by the Technical Education and Skills Development Authority.

By Investment Source: Private Sector Momentum

Public coffers funded 65.2% of 2025 activity, a level in line with the administration’s pledge to keep infrastructure allocations near 6% of GDP. Even so, private commitments are now growing faster at 7.32% a year, aided by the CREATE MORE tax regime and a revised public-private-partnership code that clarifies tariff recovery and arbitration rules. Megaworld’s USD 8.9 billion township pipeline, Ayala Land’s estate rollouts, and the USD 2.2 billion Maharlika Investment Fund are cornerstones of that rebound.

Foreign direct investment climbed to USD 8.9 billion in 2024 as global funds hunted for exposure to renewable energy and data-center shells. Public money remains concentrated in transport: the Department of Transportation alone manages more than USD 35 billion in active rail corridors. The blend of sovereign, pension, and corporate balance-sheet cash ensures that the Philippines construction market share between state and private sponsors will converge over the forecast window, diversifying order books and lowering macro-volatility risk.

Geography Analysis

The construction industry in the Philippines is witnessing strong regional expansion. Metro Manila retained a 40.4% slice of the 2025 value, thanks to transit-oriented condos, bridge retrofits, and the early civil packages for the Metro Manila Subway. Vacancy in premium offices reached 18%, yet residential pre-sales in Bonifacio Global City and Quezon City remained firm, helped by Overseas Filipino Worker remittances and flexible payment schedules. Right-of-way clearances under the new ARROW Act should unlock USD 8.9 billion in stalled projects, reinforcing the capital’s near-term dominance even as land prices cap further greenfield sprawl.

With in the Philippine construction industry, Calabarzon ranks second in spend volume, propelled by expressways such as the Cavite–Laguna Expressway and the C5 Link that trim truck travel times into Manila ports. EEI’s USD 357 million contract book in the corridor spans both roads and residential towers, and ICTSI’s Batangas terminal has catalyzed adjacent warehouse parks. Central Luzon, home to the Clark Freeport Zone, is the fastest-growing area at 7.86% through 2031, buoyed by a confluence of solar farms, casino resorts, and industrial estates that serve automotive wiring-harness exports.

Visayas and Mindanao, combined, are often labeled “Rest of the Philippines” and are leveraging landmark connectors such as the Panay–Guimaras–Negros bridges and the Mindanao Railway to integrate fragmented supply chains. Cebu’s fourth Mactan bridge and its bus rapid-transit lanes are already reshaping land use, while Davao’s coastal bypass unlocks formerly isolated barangays for mid-rise housing. Although inter-island shipping premiums inflate cement and steel costs by up to 30%, the DPWH has ring-fenced USD 5.4 billion for regional roads and bridges in 2026, preserving project viability and drawing Manila-based contractors to set up provincial depots.

Competitive Landscape

A core quartet of conglomerates—Ayala Corporation, San Miguel, Metro Pacific, and Aboitiz—continues to dominate multibillion-dollar rail, toll-road, and estate concessions, leveraging vertically integrated subsidiaries for design, build, and operate functions. Their one-stop capabilities and balance-sheet depth ensure front-of-queue status on big-ticket auctions, yet they now face disciplined bids from Chinese and Japanese engineering giants that bring modular fabrication and volume pricing.

Mid-tier specialists such as EEI, Megawide, DMCI, and First Balfour provide the execution backbone on EPC packages. First Balfour’s USD 536 million backlog spans data centers, geothermal plants, and bridge retrofits executed with AI-enabled project-controls software that trims rework rates by double digits. These firms chase ISO 9001, 14001, and 45001 certifications to score technical points in public tenders and assure lenders of strong governance standards.

White-space niches are opening in mid-rise social housing, provincial cold-chain depots, and renewable balance-of-plant works where local contractors’ lower overhead and municipal relationships offset foreign rivals’ scale. Companies able to embed drones, BIM, and digital quantity surveying into daily workflows are capturing these pockets at attractive margins. The market reality is a measured coexistence: conglomerates secure long-dated concessions, foreign EPCs supply advanced methods, and local specialists execute granular packages, an equilibrium that underpins a stable yet moderately competitive Philippines construction market.

Philippines Construction Industry Leaders

DMCI Holdings Inc.

Megawide Construction Corp.

EEI Corporation

Makati Development Corp. (Ayala)

San Miguel Infrastructure

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Department of Energy awarded 1,800 MW of solar capacity under Green Energy Auction III, triggering immediate EPC bids for substations and access roads.

- November 2025: The Accelerated Right-of-Way Act took effect, pledging 30% faster land acquisitions for national infrastructure packages.

- August 2025: DHSUD completed 110 modular housing units in San Juan City, the first batch under its one-million-unit annual target.

- August 2025: Hann Resort started a USD 268 million expansion in Clark, adding 500 rooms and a convention hall to tap the MICE segment.

Philippines Construction Market Report Scope

| Residential | Apartments / Condominiums |

| Villas / Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial & Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, Others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc.) |

| Public |

| Private |

| NCR (Metro Manila) |

| Calabarzon |

| Central Luzon |

| Rest of the Philippines |

| By Sector | Residential | Apartments / Condominiums |

| Villas / Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial & Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, Others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc.) | ||

| By Investment Source | Public | |

| Private | ||

| By Region | NCR (Metro Manila) | |

| Calabarzon | ||

| Central Luzon | ||

| Rest of the Philippines | ||

Key Questions Answered in the Report

What is the projected value of the Philippines construction market by 2031?

Forecasts place the sector at USD 66.41 billion by 2031, reflecting a CAGR of 6.51% from 2026.

Which segment currently controls the largest share of spending?

Residential construction led with 41.9% of the 2025 value, supported by the national social-housing drive.

Which region is expected to grow fastest?

Central Luzon shows the quickest trajectory, tracking a 7.86% CAGR on the back of Clark and solar-farm builds.

How are material-cost pressures being managed?

Contractors negotiate escalation clauses, pre-buy steel during low demand, and substitute fly-ash cement to offset price spikes.

What role do modular methods play in future growth?

Modern modular systems are expanding at a 7.09% CAGR as public housing and select hotels shift to offsite fabrication.

Page last updated on: