Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

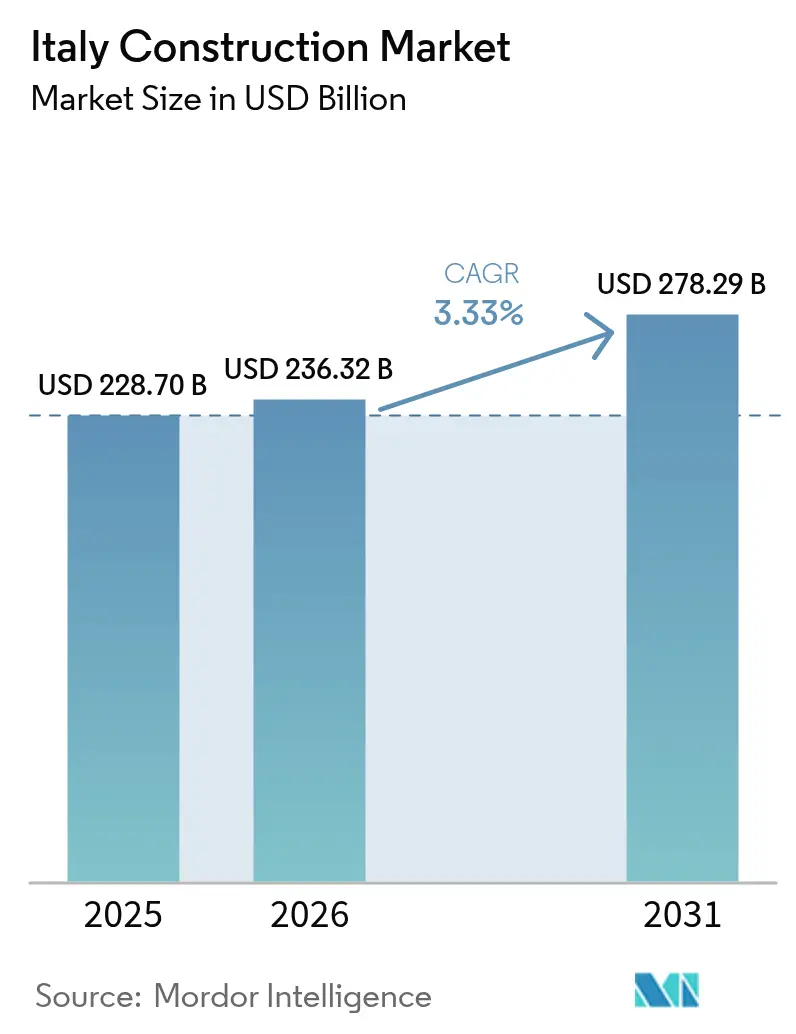

| Base Year Market Size (2025) | USD 228.70 Billion |

| Market Size (2026) | USD 236.32 Billion |

| Market Size (2031) | USD 278.29 Billion |

| Growth Rate (2026 - 2031) | 3.33% CAGR |

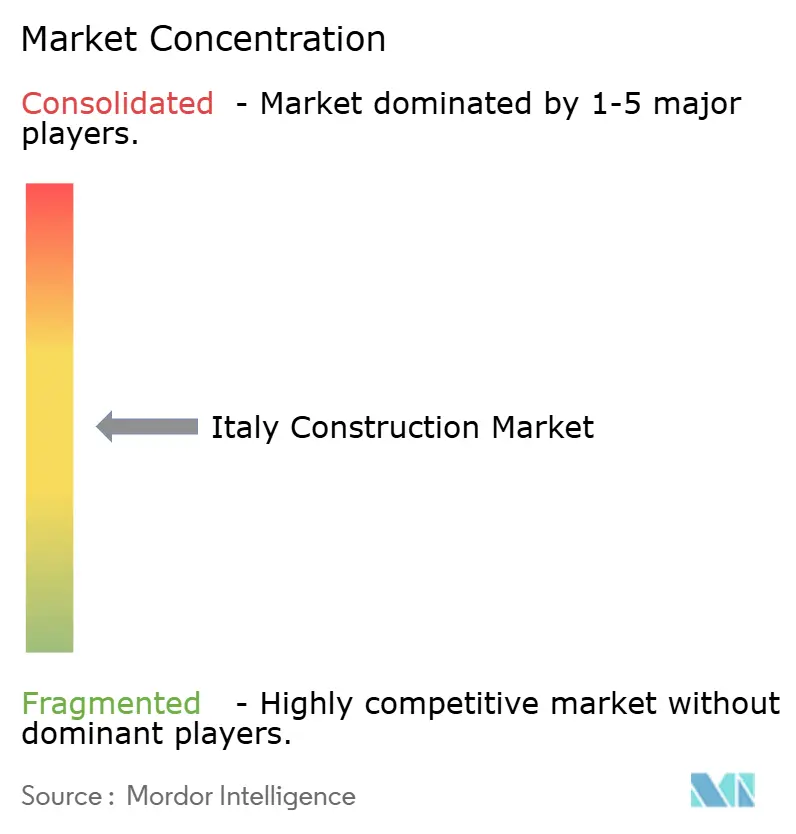

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Construction Market Analysis by Mordor Intelligence

The Italy Construction Market size is expected to grow from USD 228.70 billion in 2025 to USD 236.32 billion in 2026 and is forecast to reach USD 278.29 billion by 2031 at 3.33% CAGR over 2026-2031. A surge in public infrastructure spending, large-scale energy-efficiency upgrades, and the rebound of private commercial investment are reshaping short-term demand patterns. Infrastructure work, from high-speed rail corridors to national grid enhancements, is expanding at a pace that outstrips overall growth, pulling specialist contractors and equipment suppliers into new regional clusters. Meanwhile, regulatory deadlines set by the Energy Performance of Buildings Directive (EPBD) are redirecting renovation strategies toward deep-retrofit packages, sparking innovation in materials and digital construction workflows. Companies able to blend traditional capabilities with modular techniques and data-driven project controls are capturing a widening share of contracts as clients demand shorter delivery times, lower carbon footprints, and rigorous cost certainty.[1]European Commission, “Economic forecast for Italy"

Key Report Takeaways

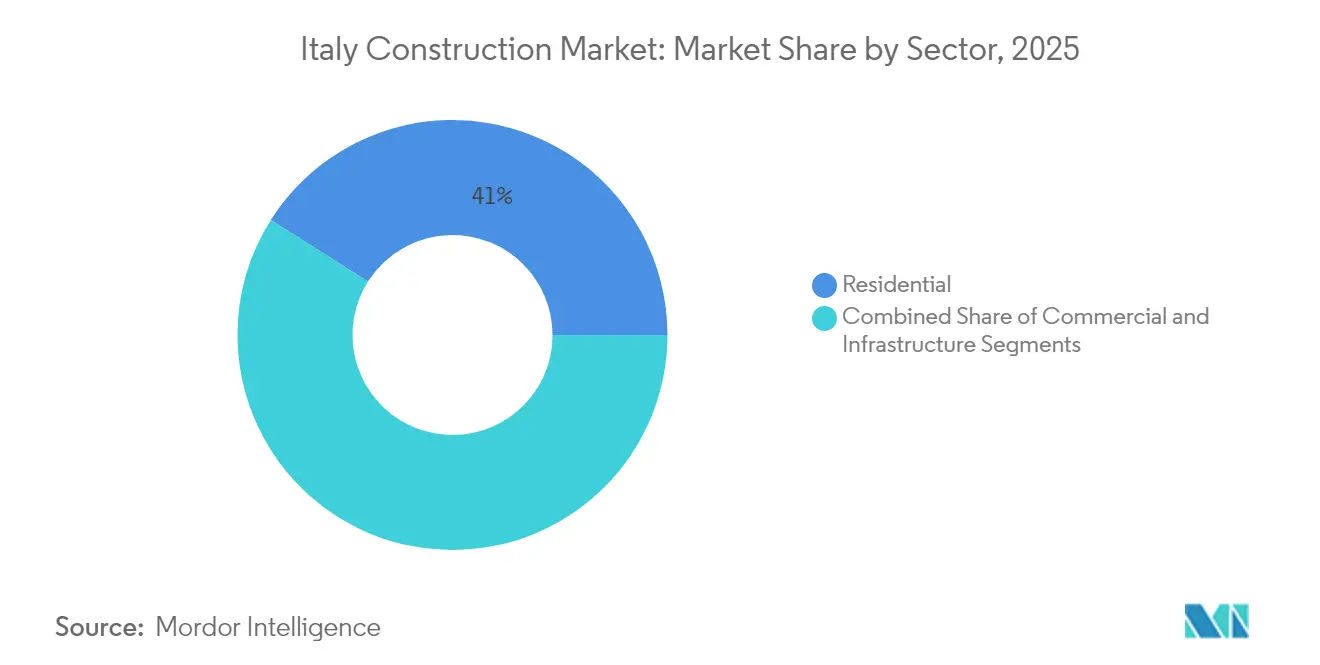

- By sector, Residential captured 41.02% of the Italy construction market share in 2025. Italy construction market size for residential is projected to grow at a 3.38% CAGR between 2026-2031.

- By construction type, New construction captured 54.62% of the Italy construction market share in 2025. Italy construction market size for new construction is projected to grow at 3.74% CAGR between 2026-2031.

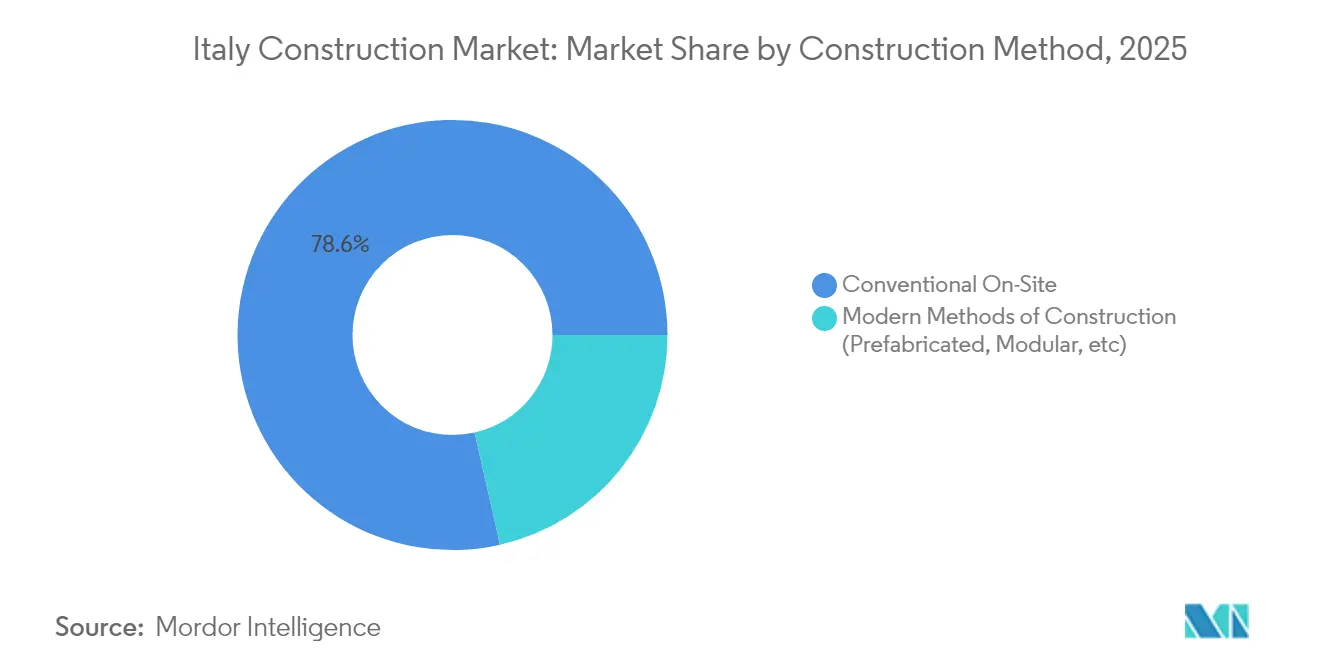

- By construction method, Conventional on-site techniques captured 78.55% of the Italy construction market share in 2025. Italy construction market size for conventional on-site techniques is projected to grow at 3.36% CAGR between 2026-2031.

- By investment source, Private capital captured 62.05% of the Italy construction market share in 2025. Italy construction market size for private capital is projected to grow at 4.14% CAGR between 2026-2031.

- By geography, Milan captured 26.22% of the Italy construction market share in 2025. Italy construction market size for Rest of Italy is projected to grow at 3.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large-scale public infrastructure modernization | +1.2% | National, high in Southern Italy | Medium term (2-4 years) |

| Energy-efficiency driven deep-retrofit renovations | +0.9% | National, higher in North & Center | Long term (≥4 years) |

| High-speed rail & urban mobility expansion | +0.7% | National, focus on South & urban nodes | Medium term (2-4 years) |

| Utility-scale renewable energy construction | +0.5% | South & Islands | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Large-scale Public Infrastructure Modernization Under National and EU Stimulus Plans

Massive funding under the NRRP allocates USD 217 billion for 2021-2026, channeling USD 78 billion toward ecological transition and infrastructure upgrades. Public works spending rose 13.7% in 2024 as transport, water and digital projects broke ground, cushioning weakness in residential starts. Southern provinces, long constrained by connectivity gaps, posted construction growth of 0.9% in 2024 versus 0.7% in the North, illustrating how targeted outlays are recalibrating the Italy construction market. These projects, including the Brenner Base Tunnel and the Tyrrhenian Link, embed resilience standards that require advanced digital design and low-carbon materials. Contractors with integrated engineering, procurement and environmental compliance capabilities are winning multi-year frameworks that provide predictable backlog and technology transfer opportunities.

Structural Shift Toward Residential Energy Efficiency and Deep-Retrofit Renovations

The EPBD mandates every residential building reach energy class D by 2033, a target that affects nearly 60% of Italy’s housing stock currently labeled G or F. Lombardy and Piedmont alone would need USD 135 billion in upgrades, equal to 20.2% of regional GDP. Although the “Superbonus” scheme is being phased out, heightened consumer awareness and stricter resale requirements are propelling demand for heat-pump installations, triple glazing and smart metering. Specialized design-build firms that bundle energy modelling, subsidy advisory and performance guarantees are scaling rapidly, often in partnership with utilities and fintech platforms that tailor mortgage-linked retrofit loans.

Expansion of High-Speed Rail and Urban Mobility Networks for Sustainable Transport

Ferrovie dello Stato plans USD 215.6 billion of rail investment over the next decade, expanding capacity 20% and trimming Genoa-Milan travel to 1 hour. The Naples-Bari corridor demonstrates the broader multiplier: rural towns along the route are recording higher land values and ancillary construction contracts, pointing to spillovers into hospitality, retail and light industrial builds. Urban metros in Rome, Milan and Turin are synchronising extensions with last-mile electric bus fleets, opening tender packages that require rolling-stock depots, signaling systems and TOD (transit-oriented development) opportunities. This cluster of mobility projects is steering the Italy construction market toward integrated design and prefabricated viaduct segments that compress onsite schedules.

Accelerated Growth in Utility-Scale Renewable Energy Construction Projects

Battery-equipped solar farms and offshore wind arrays are scaling fast, led by a 354 MWp storage portfolio co-developed by Emeren Group and Nuveen Infrastructure slated for mid-2025 groundbreaking. Terna’s USD 26 billion grid plan allocates funds to connect renewable clusters via the Tyrrhenian and Adriatic Links.[2]Terna, “2025 Development Plan for the national electricity grid” EPC contractors with HVDC expertise and modular substation solutions are well positioned as utility clients prioritize rapid interconnection. Southern regions and the Islands supply optimal solar irradiance and wind speeds, making them epicenters for hybrid generation-storage complexes that require sizable civil works for foundations, access roads and port upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated input costs & supply chain disruptions | -0.7% | National, acute in North | Short term (≤2 years) |

| High interest rates reducing mortgage access | -0.5% | Urban centers nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Construction Input Costs Due to Global Supply Chain Disruptions and Energy Prices

The Construction Cost Index hit multiyear peaks as steel, cement and bitumen prices surged, squeezing contractor margins. Northern regions, home to steel-intensive industrial builds, face steeper cost spikes. Firms are responding by stockpiling bulk materials, forging long-term supplier alliances and broadening recycled-content procurement to hedge volatility. Digital marketplaces offering live price feeds and AI-powered forecasting are gaining traction, allowing mid-tier builders to negotiate index-linked contracts and mitigate risk.

High Interest Rate Environment Reducing Mortgage Access and Private Residential Investment

Although the ECB has initiated cuts, cumulative rate hikes have already cooled housing permits, with developers in Milan and Rome shelving large projects amid weaker presales. Affordability gaps widen as wages lag home prices, pushing demand toward smaller units or co-living options. Developers are recalibrating pro-formas via modular designs and mixed-use schemes that unlock alternative revenue streams. Once rates normalise, the backlog of deferred household demand could trigger a supply crunch, placing upward pressure on construction capacity and land values.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Outpaces Traditional Segments

Infrastructure work generated the fastest growth, advancing at a 3.94% CAGR from 2026 to 2031 as rail corridors, grid links and water projects dominate procurement schedules. Terna’s USD 26 billion programme and Webuild’s high-speed rail packages illustrate how long-cycle assets are anchoring order books. The Italy construction market size for transportation alone is projected to climb steadily as EU corridors intersect domestic freight upgrades. Conversely, the residential segment—despite holding 41.02% of 2025 revenue—faces mixed signals; energy-efficient demand gains are countered by tapering tax credits. Commercial builds are bifurcated, with data centres and logistics sheds filling pipelines while traditional offices retrench.

Infrastructure contracts are structured around multi-stakeholder frameworks that require granular ESG reporting and digital twin integration, altering bid-evaluation priorities. Residential players emphasize net-zero ready designs, stimulating uptake of prefabricated façades and heat-pump systems. Commercial asset classes see investor scrutiny around embodied carbon, pushing contractors to validate material sourcing and lifecycle emissions. Collectively, these shifts ensure the Italy construction market remains sensitive to policy and capital-market requirements, steering growth toward sectors that marry resilience and digital performance.

By Construction Type: Renovation Gains Strategic Importance

New builds retained 54.62% of Italy construction market share in 2025 and are forecast to rise at 3.74% CAGR as high-profile schemes such as the Strait of Messina bridge (USD 15.3 billion) progress toward procurement. Visibility on long-duration public projects gives tier-one contractors revenue certainty, while private industrial and logistics builds secure pre-lease agreements that underpin financing.

Renovation commands 45.38% of spending and is evolving from reactive maintenance to strategic retrofits driven by EPBD deadlines. Deep-retrofit packages that achieve class D or better are gaining traction, supported by building-integrated photovoltaics and phase-change insulation panels. Energy-performance contracting models shift upfront capital risks onto ESCOs, widening market access for asset owners. This regulatory momentum places renovation at the heart of decarbonisation, reinforcing its value proposition within the Italy construction market.

By Construction Method: Modern Techniques Gain Momentum

Conventional on-site processes still accounted for 78.55% of 2025 output, underpinned by Italy’s intricate architectural heritage and bespoke civil works. This share, however, hides incremental gains in low-carbon concrete mixes, robotic rebar tying and drone-based site analytics that squeeze waste out of legacy workflows. Builders use BIM-driven clash detection to curtail rework, signalling an evolutionary path rather than wholesale disruption.

Modern methods of construction (MMC) are advancing at a 4.29% CAGR, propelled by the need to halve delivery times and address labour shortages. Modular classrooms, healthcare units and student housing lead adoption, often financed via performance-based PPP contracts. Digital design libraries, coupled with IoT sensors embedded in prefabricated modules, enable near-real-time commissioning, improving asset-handover quality. Successful pilots in Lombardy and Emilia-Romagna are reducing perceived quality stigma, clearing a pathway for wider MMC penetration within the Italy construction market.

By Investment Source: Private Capital Drives Market Dynamics

Private outlays represent 62.05% of Italy construction market size and are expected to grow at 4.14% CAGR to 2031, buoyed by data-centre pipelines such as AWS’s USD 1.2 billion expansion that underscores appetite for digital-economy assets. Logistics portfolios remain in favour as e-commerce penetration climbs, generating stable income streams for pension funds and sovereign wealth vehicles.

Public investment, 37.95% of spending, concentrates on transformative infrastructure. The Medium-Term Fiscal-Structural Plan shields capital budgets despite deficit pressures, relying on PPP structures to mobilise private liquidity. Italy’s proposed USD 227 billion facility that leverages USD 19 billion public funds typifies this blended-finance approach. Such mechanisms expand the Italy construction market’s investable universe, particularly for renewable energy transmission corridors and resilient transport nodes.

Geography Analysis

In 2025, Milan commands 26.22% of Italy's national construction activity, spearheading the country's urban redevelopment with initiatives like the Porta Romana Olympic Village and the MIND Milano Innovation District. The city is a magnet for institutional capital, especially in ESG-compliant commercial and residential assets. Its prime location enhances cross-border logistics, and the adaptive reuse of industrial sites is fast-tracking the creation of high-performance buildings with a focus on reduced embodied carbon.

Rome stands at the forefront of heritage-centric construction and infrastructure rejuvenation. The city's ambitious USD 2.32 billion (EUR 2 billion) Jubilee 2025 initiative is not only modernizing metro stations but also enhancing public spaces to better serve the influx of visitors. The restoration of Rome's classical buildings artfully marries seismic retrofitting with traditional conservation techniques, bolstered by advanced digital tools like scan-to-BIM. With land at a premium in the historic center, developers are turning to vertical expansions and sub-grade engineering to make the most of the urban landscape.

The rest of Italy is emerging as the most vibrant growth hub in the national construction arena, eyeing a projected CAGR of 3.74% from 2026 to 2031. Northern regions, especially Emilia-Romagna and Veneto, lead the charge in logistics and brownfield redevelopment. Central Italy thrives on cultural preservation and transport-related hospitality projects. In the South, initiatives like Special Economic Zones (SEZs) and funding from the National Recovery and Resilience Plan (NRRP) are catalyzing significant investments in industrial parks, ports, and renewable energy. Concurrently, Sicily and Sardinia are bolstering their tourism infrastructure and offshore wind projects, with a growing inclination towards modular construction to tackle seasonal workforce challenges and ferry logistics.

Competitive Landscape

Industry concentration is moderate; a handful of national champions such as Webuild SpA, Saipem SpA and Astaldi SpA alongside thousands of niche contractors. Strategic consolidation is gathering pace as large players absorb specialist firms to deepen design-build-operate propositions; Webuild’s USD 567 million note issue funds a USD 72.6 billion backlog dominated by sustainable assets. Technology acquisitions are rising: Accenture’s purchase of the 450-person IQT Group expands engineering depth for net-zero projects, signalling non-traditional entrants’ influence.

Competitive differentiation pivots on digital prowess and ESG credentials. Contractors deploy drone photogrammetry, AI-led safety analytics and low-carbon material chains to secure premium margins in the Italy construction market. Public procurers increasingly assign weighted scores for carbon intensity and circular-economy plans, nudging firms toward recycled aggregates and bio-based insulation. Innovators such as the Italgas-I3P “NewGen Construction Site” programme showcase successful pilots using IoT wearables and predictive maintenance, highlighting collaboration across utilities, startups and academia.

White-space opportunities emerge in modular housing, energy-efficient retrofits and infrastructure maintenance. Mid-cap specialists with smart-sensor offerings win framework agreements for motorway condition monitoring, while finance providers deepen niche lines such as surety bonds; PIB Group’s purchase of Elleti Broker exemplifies insurance segment expansion aligned with construction surety demand. Against this backdrop, strong order backlogs and stable public pipelines underpin revenue visibility despite input-cost volatility.

Italy Construction Industry Leaders

Webuild SpA

Saipem SpA

Astaldi SpA

Salcef Group SpA

Maire Tecnimont SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Webuild S.p.A. issued USD 533 million in 4.875% notes due 2030 to bolster a EUR64 billion sustainable project backlog.

- March 2025: ASTM recorded USD 4.9 billion turnover for 2024, investing USD850 million (EUR781.8 million) in motorway network upgrades.

- March 2025: Terna released its 2025 Development Plan, earmarking USD25 billion to integrate renewables and expand grid capacity.

- February 2025: PIB Group acquired Elleti Broker S.p.A., strengthening surety bond capacity linked to NRRP projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian construction market as the full on-site value of building, civil engineering, and major renovation works completed within Italy's borders during a calendar year. It spans new housing, commercial towers, factories, rail lines, highways, utilities, and deep-retrofit upgrades that raise energy performance.

Scope Exclusions: Temporary site rentals, sales of construction equipment, and brokerage or notary fees linked to property transactions sit outside this boundary.

Segmentation Overview

- By Sector

- Residential

- Apartments/Condominiums

- Villas/Landed Houses

- Commercial

- Office

- Retail

- Industrial and Logistics

- Others

- Infrastructure

- Transportation Infrastructure (Roadways, Railways, Airways, others)

- Energy & Utilities

- Others

- Residential

- By Construction Type

- New Construction

- Renovation

- By Construction Method

- Conventional On-Site

- Modern Methods of Construction (Prefabricated, Modular, etc)

- By Investment Source

- Public

- Private

- By Region

- Milan

- Rome

- Turin

- Rest of Italy

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with general contractors, regional engineering consultants, supplier associations, and municipal permit officers in Milan, Rome, Naples, and Turin. Interviews clarify average project budgets, payment lags, NRRP funding flows, and the likely pace at which energy-efficiency incentives restart, filling gaps left by published statistics and guiding assumption ranges.

Desk Research

We begin with structured searches across authoritative public sources such as ISTAT's national accounts, Eurostat production indices, the Ministry of Infrastructure and Transport's project databases, and FIEC investment dashboards. Industry journals, trade-license records, municipal building-permit files, and company 10-K filings enrich the sector view. For company-level splits and historic deal values, analysts access D&B Hoovers and Dow Jones Factiva. These sources establish baseline activity, price trajectories, and policy triggers. The sources listed are illustrative; many additional outlets were reviewed to ground and validate every data point.

Our team then collates macro indicators (GDP, gross fixed capital formation), project pipelines, and commodity inputs (structural-steel and cement price indices) that influence construction spend. Cross-checks against customs data for key materials confirm import exposure and cost pass-through trends.

Market-Sizing & Forecasting

A top-down model converts national construction output tables and NRRP disbursement schedules into current-year market value, which is then corroborated through selective bottom-up roll-ups of sampled residential and infrastructure projects. Key variables like building-permit floor area, average project cost per square meter, mortgage interest rates, public-tender awards, and structural-steel prices drive year-on-year shifts. Forecasts to 2030 deploy multivariate regression with ARIMA overlays; the equation weights macro demand signals and cost factors that our primary respondents judge to be most predictive. Where bottom-up estimates diverge, variance caps and segment-specific escalation factors realign totals.

Data Validation & Update Cycle

Every draft model passes anomaly checks, peer review, and senior analyst sign-off. Outputs are reconciled with external trade and labor metrics before publication. Reports refresh each year, and we reopen models whenever policy shocks or material price swings exceed predefined thresholds.

Why Our Italy Construction Baseline Commands Reliability

Published values differ because firms select distinct scopes, price concepts, and refresh cadences. By anchoring on investment actually executed on site and by adjusting for informal renovation and inflation, Mordor delivers a balanced midpoint clients can trust.

Key Gap Drivers stem from whether estimates include plant assembly, exclude maintenance, or mingle construction with real-estate services; currency treatment and forecasting windows also reshape totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 228.70 B (2025) | Mordor Intelligence | - |

| USD 311.72 B (2025) | Global Consultancy A | Includes industrial installation revenues and applies one macro multiplier without segment validation |

| EUR 193 B (2024) | Industry Association B | Captures only capital investment, omitting maintenance and informal renovation activity |

| EUR 317.4 B (2023) | Data Aggregator C | Uses turnover that merges construction and property development, with no inflation adjustment |

Taken together, the comparison shows that when scope breadth or price bases shift, totals swing widely. Mordor's disciplined mix of clearly bounded scope, multi-indicator modeling, and annual refresh gives decision-makers a dependable reference line for strategy and budgeting.

Key Questions Answered in the Report

What is the current value of the Italy construction market?

The Italy construction market stands at USD 236.32 billion in 2026 and is forecast to reach USD 278.29 billion by 2031.

Which sector is growing the fastest within the market?

Infrastructure leads growth with a 3.94% CAGR for 2026-2031, buoyed by high-speed rail, grid upgrades and water projects.

How important are renovation projects under new energy rules?

Renovations hold 45.38% of spending in 2025 and are becoming mandatory as the EPBD pushes buildings to achieve at least class D by 2033.

What share of investment is private versus public?

Private capital accounts for 62.05% of 2025 revenue, while public spending remains crucial for large transport and energy works.

Which region is forecast to expand the quickest?

The rest of Italy is expected to post a 3.74% CAGR between 2026 and 2031, supported by Special Economic Zones and EU funding.

How are rising material costs affecting builders?

Elevated input prices reduce margins, prompting contractors to adopt recycled materials, long-term supply deals and digital procurement to manage cost volatility.

Page last updated on: