Singapore Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

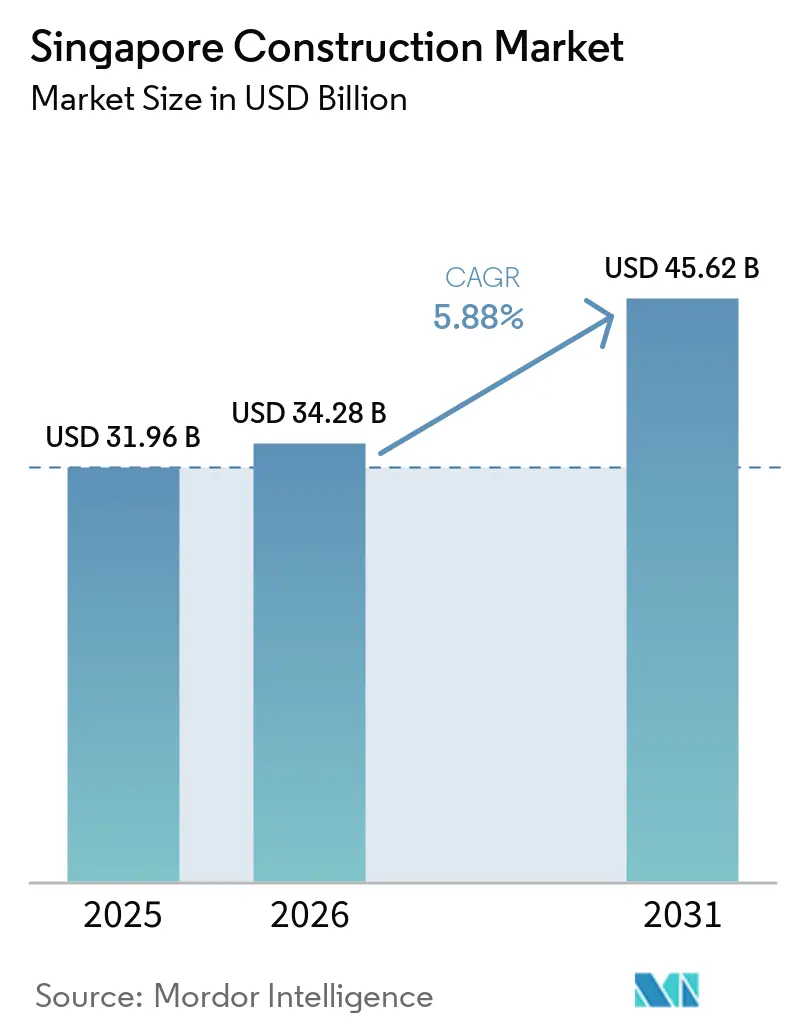

| Base Year Market Size (2025) | USD 31.96 Billion |

| Market Size (2026) | USD 34.28 Billion |

| Market Size (2031) | USD 45.62 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

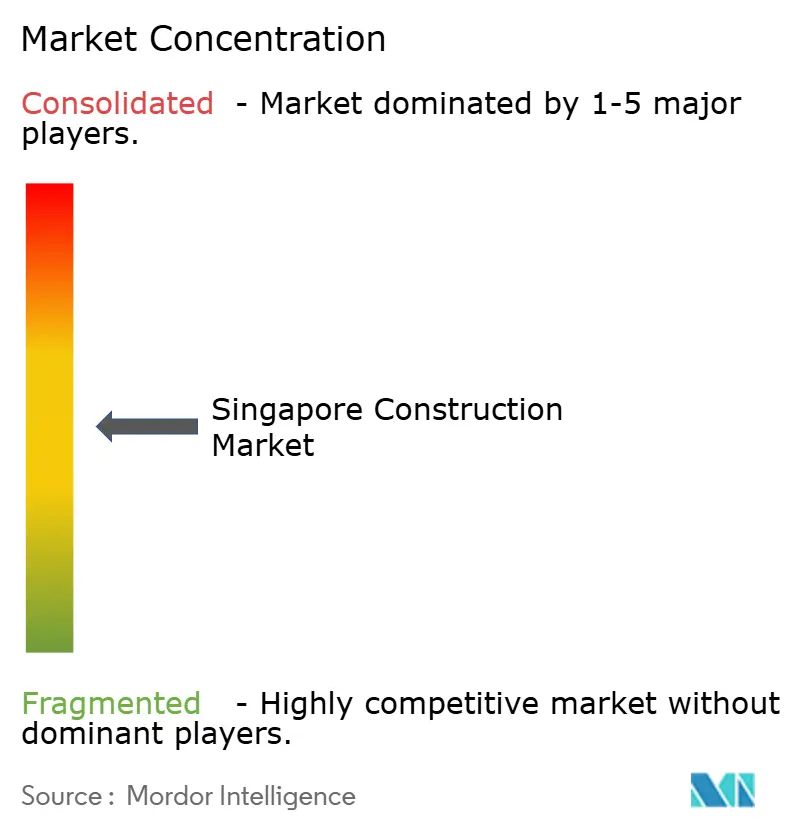

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Construction Market Analysis by Mordor Intelligence

The Singapore construction market size was valued at USD 31.96 billion in 2025 and estimated to grow from USD 34.28 billion in 2026 to reach USD 45.62 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031). Robust public-sector infrastructure projects, steady private housing demand, and policy-led sustainability targets underpin this trajectory. Megaprojects at Tuas Port and Changi Terminal 5 anchor a long civil-works pipeline, while the Housing Development Board’s (HDB) Build-To-Order (BTO) programme keeps residential activity resilient. Mandatory Green Mark 2021 rules are accelerating low-carbon design, and the mid-2024 lifting of a data-centre moratorium is opening a new pocket of high-specification demand. The Singapore construction market, therefore, balances near-term housing delivery with long-term logistical and digital infrastructure needs, creating opportunities for both conventional contractors and modern-method specialists.

Key Report Takeaways

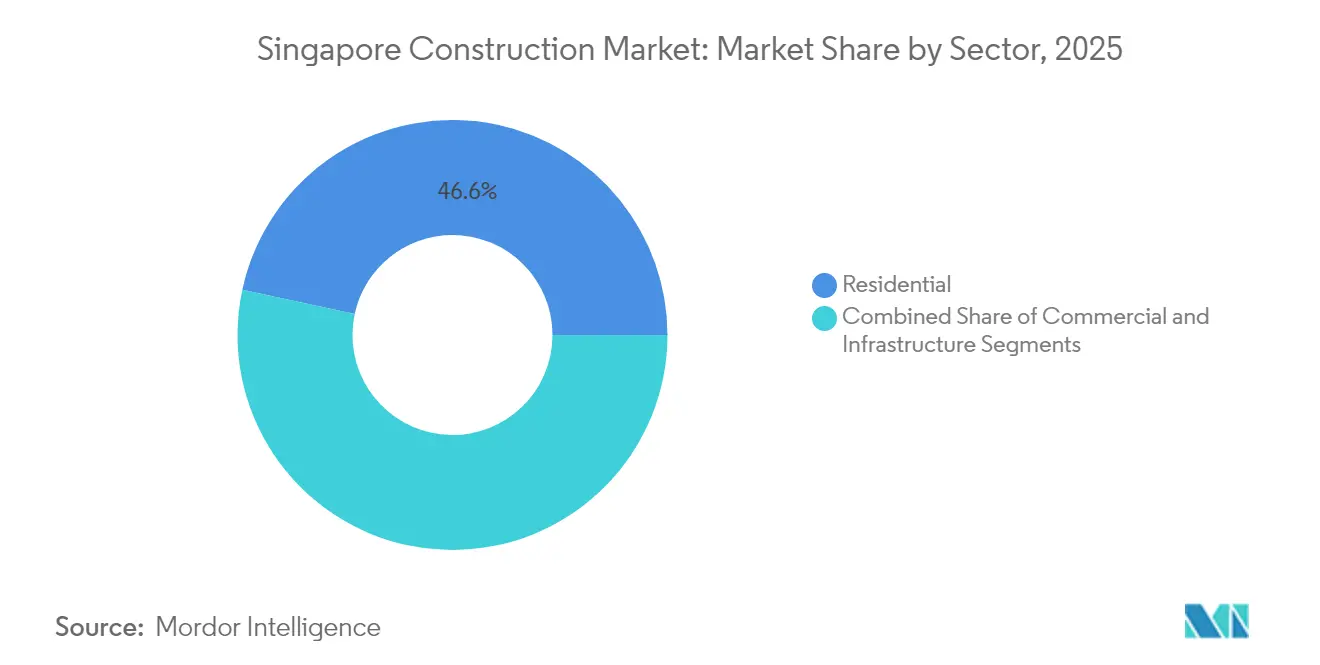

- By sector, residential construction held a 46.62% share of the Singapore construction market in 2025, while infrastructure is projected to post the fastest growth at a 5.72% CAGR between 2026 and 2031.

- By construction type, new projects accounted for 62.35% of 2025 output; renovation and retrofit work is forecast to record a 5.83% CAGR to 2031.

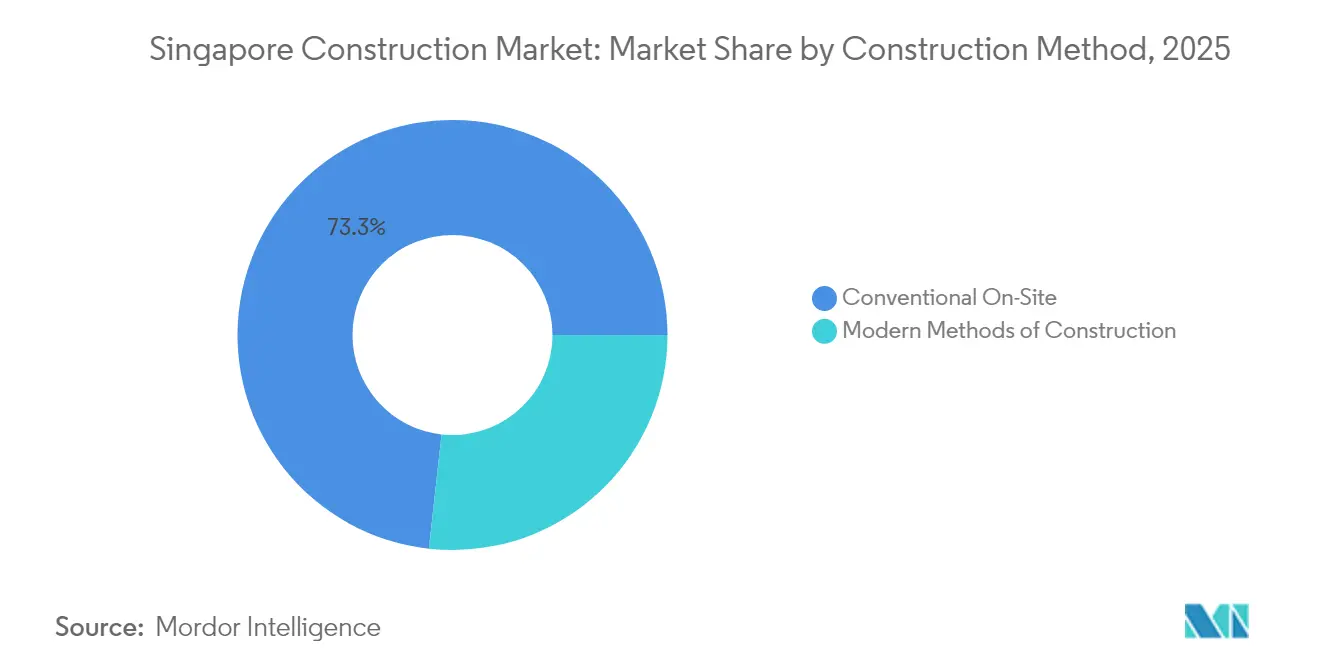

- By construction method, on-site conventional techniques dominated with a 73.25% share in 2025; modern methods are advancing at a 6.02% CAGR through 2031.

- By investment source, private investment represented 58.30% of spending in 2025, whereas public-private partnerships are set to expand at a 5.76% CAGR over the forecast horizon.

- By geography, the Outside Central Region captured 39.45% of 2025 activity and is expected to lead growth at a 5.84% CAGR, reflecting suburban township rollout.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tuas Port & Changi T5 megaprojects | +1.2% | Nation-wide, with main works in western and eastern corridors | Long term (≥ 4 years) |

| Accelerated BTO housing pipeline | +0.9% | Country-wide, strongest in Outside Central Region | Short term (≤ 2 years) |

| Public-sector Green Mark procurement | +0.8% | Concentrated in Core and Rest of Central Regions | Medium term (2-4 years) |

| New hyperscale data-centre permits | +0.6% | Industrial estates and Punggol Digital District | Medium term (2-4 years) |

| Mandatory Integrated Digital Delivery (IDD) | +0.5% | Early uptake on public projects across Singapore | Medium term (2-4 years) |

| Neighbourhood Renewal retrofits | +0.4% | Mature estates island-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tuas Port and Changi T5 megaprojects anchor the infrastructure pipeline

Tuas Port reclamation is 75% complete and will scale from 11 to 18 berths by 2027 before reaching 65 million TEUs capacity in the 2040s. At the other end of the island, construction on Changi Terminal 5 started in 2025 after USD 3.56 billion in substructure and airside contracts were awarded. Complex marine, tunnelling, and aviation packages are lifting demand for specialist engineering services, robotics, and large-format precast elements. With a combined public investment of around USD 15 billion, these flagship projects secure a decade-plus workload for heavy civil contractors and their supply chains.

Housing Development Board’s accelerated BTO programme sustains residential demand

HDB plans to launch 25,000 new flats in 2025, pushing the total 2021-2025 supply above 102,000 units. The programme introduces Standard, Plus, and Prime flat categories that deepen affordability and shorten waiting times, while half of all BTO sites now deploy painting and plastering robots that cut labour hours by 30%. Large suburban sites in Tengah and Mount Pleasant are embedding centralised cooling and solar installations, keeping the construction industry in Singapore aligned with national climate goals.

Public-sector Green Mark procurement drives sustainable construction standards

The Green Mark 2021 framework became compulsory for all new government buildings in June 2024, linking contract eligibility to energy-use intensity and embodied-carbon thresholds. Contractors now compete on low-carbon materials and design credentials, and guaranteed energy-savings contracts are locked in over a building’s life cycle. The approach aligns with global ESG benchmarks and boosts demand for prefabrication, recycled aggregates, and smart-building sensors. Private developers are following suit to secure green financing, broadening the standard’s commercial reach. As a result, firms with proven sustainability expertise enjoy stronger bid pipelines and margin resilience[1]Singapore Green Building Council, "Embodied Carbon Assessment Framework for Buildings," sgbc.sg.

Hyperscale data-centre expansion follows moratorium lift

The Green Data Centre Roadmap, released in May 2024, frees 300 MW of additional capacity, with two-thirds ring-fenced for operators using renewables. Vacancy sat at only 2% in 2024, so Equinix and other colocation players have moved quickly to secure permits for AI-ready facilities that will open by 2027. New resilience guidelines on cybersecurity and business continuity add layers of MEP complexity, creating premium opportunities for builders versed in mission-critical construction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight foreign-worker quotas | -1.1% | Nationwide, especially labour-intensive trades | Short term (≤ 2 years) |

| Scarce land and vertical-build complexity | -0.7% | Most acute in Core and Rest of Central Regions | Long term (≥ 4 years) |

| Volatile imported-material prices | -0.6% | Island-wide due to re-export hub exposure | Medium term (2-4 years) |

| Rising workplace-safety compliance costs | -0.3% | High-risk activities throughout Singapore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight foreign-worker quotas constrain labour supply

The dependency ratio ceiling remains at 83.3%, limiting firms to five Work-Permit holders for each local employee, while S-Pass salary minimums rose to USD 2,475 in 2025. Levies will climb to USD 488 by September 2025, and new capital requirements for contractor registration add a further hurdle. These rules inflate total labour costs and encourage heavier reliance on automation, but smaller firms may struggle to fund the transition, risking project delays.

Scarce land drives vertical-build complexity and risk

Singapore’s 728 km² land area forces projects to stack functions, adopt deeper basements, and rely on heavier cranes. Tall-slender designs are sensitive to wind load and require thicker cores, raising material usage and programme risk. With premium sites concentrated in the downtown core, design changes and neighbour-management obligations can prolong approval phases and erode developer returns.

Scarce Land Drives Vertical Construction Complexity and Project Risks

Singapore's limited land area of 728 square kilometers necessitates increasingly complex vertical construction projects, elevating technical risks and project costs across the construction sector. The government's strategic land recycling initiatives, including the Selective En bloc Redevelopment Scheme and upcoming Voluntary Early Redevelopment Scheme, create opportunities for higher-density developments but require sophisticated engineering solutions for deep excavations and high-rise construction. Projects like Changi Terminal 5's underground connections and the Cross Island Line's 50-meter deep King Albert Park station exemplify the technical complexity required to maximize land utilization while minimizing surface disruption. Land constraints drive premium pricing for construction services, as contractors must invest in specialized equipment, advanced safety systems, and highly skilled personnel capable of executing complex vertical projects. The scarcity factor intensifies competition for prime development sites, leading to aggressive bidding that can compromise project margins and increase financial risks for contractors. Heat stress projections indicating potential economic losses exceeding USD 1.5 billion by 2035 further compound land utilization challenges, as outdoor construction activities face productivity constraints during increasingly frequent extreme weather events.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Gains Momentum While Residential Leads Overall Activity

Residential work held 46.62% of the Singapore construction market share in 2025, fuelled by the BTO pipeline and steady private condominium launches. Infrastructure, although smaller, is set to record the fastest 5.72% CAGR to 2031, reflecting long-cycle port, rail and airport expansions.

Rising population density sustains apartment demand, while energy-efficient designs and prefab components help developers meet Green Mark targets. On the infrastructure side, Phase 2 of the Cross Island Line began in 2025, and Tuas Port’s next berth tranche requires heavy caisson fabrication. The Singapore construction market size tied to transport corridors will therefore outpace other segments as the nation reinforces its role as a trans-shipment and aviation hub.

By Construction Type: Renovation Activity Accelerates in an Ageing Building Stock

New builds made up 62.35% of 2025 output, underpinned by greenfield housing and megaprojects. Renovation earns the top growth slot at a 5.83% CAGR as mature estates enter cyclical upgrade programmes.

CORENET X digital approvals shorten design cycles for new towers, but brownfield retrofits enjoy tailwinds from mandated energy improvements and universal-design upgrades. As many commercial offices head for repositioning to retain tenants, capital spending shifts towards façade recladding, low-energy HVAC, and structural strengthening. These trends enlarge the Singapore construction market size for fit-out and M&E contractors through 2031.

By Construction Method: Modern Techniques Target Productivity Gaps

Conventional on-site processes controlled 73.25% of the 2025 volume, yet modern approaches will expand at a 6.02% CAGR. Labour scarcity and safety penalties push builders to prefabricated pre-finished volumetric construction (PPVC) and large-panel precast.

HDB now deploys PPVC in most high-rise blocks, cutting man-hours and raising site safety. Private developers adopt hybrid systems combining PPVC bathrooms with conventional slabs to balance cost and flexibility. The Singapore construction market share for modern methods will therefore widen as supply-chain capacity and regulatory familiarity grow.

By Investment Source: Public-Private Partnerships Emerge as a Growth Lever

Private developers funded 58.30% of the 2025 project value, attracted by stable yields and transparent land tenders. PPP structures, however, are on track for a 5.76% CAGR as the state taps private expertise to deliver complex assets such as integrated resorts and waste-to-energy plants.

Las Vegas Sands broke ground on its USD 8 billion Marina Bay Sands expansion in July 2025 under a government-supported development agreement. Similar risk-sharing frameworks are under study for solar farms and district-cooling networks, offering financiers long-duration cashflows tethered to public service needs.

Geography Analysis

The Outside Central Region led the Singapore construction market in 2025 with a 39.45% share and is forecast to grow at 5.84% CAGR through 2031. Early phases of Tengah, an eco-smart township featuring centralised cooling and autonomous shuttle trials, dominate permit volumes. Planned Chencharu projects near Khatib MRT will add 10,000 homes, 80% of which are public flats, reinforcing suburban momentum.

The Rest of the Central Region retains a balanced mix of renewal and new-build schemes. Mature estates in Ang Mo Kio and Queenstown are in line for lift upgrades, façade repainting, and greenery enhancements under the Neighbourhood Renewal Programme. Meanwhile, parts of the Cross Island Line Phase 2 tunnel beneath Bukit Timah and Clementi will spur station-linked retail clusters. Investors note that repositioned offices and life-science labs in One-North enjoy rapid take-up, signalling latent demand for adaptive-reuse projects.

In the Core Central Region, flagship developments sharpen Singapore’s international profile. The NS Square, a 30,000-seat waterfront venue, integrates rooftop solar arrays and an elevated pedestrian loop, setting bar-raising sustainability benchmarks. The USD 8 billion Marina Bay Sands expansion adds a 55-storey hotel tower and 15,000-seat arena, reinforcing tourism competitiveness. Land scarcity keeps supply tight, but premium rents justify complex engineering such as deep basements and slender towers.

Competitive Landscape

Competition sits at a moderate level, with incumbents like Woh Hup, Hyundai E&C and Obayashi Singapore holding long reference lists while nimble tech-led entrants vie for niche mandates. Major public tenders favour joint ventures able to meet hefty bonding and digital-delivery requirements, as shown by the China Communications Construction–Obayashi win for the USD 2.85 billion Changi T5 substructure[3]Competition and Consumer Commission of Singapore, "Construction Industry Market Study 2024," cccs.gov.sg.

Technology adoption has become a key differentiator. Contractors are rolling out drones for progress tracking, 4D BIM for clash detection, and robotics for labour-intensive tasks. Obayashi’s Construction-Tech Lab, launched in 2024, pilots remote-controlled excavators and AI-driven safety analytics, giving the firm a head start in productivity contests. Local proptech platform Podium, backed by Autodesk and Lendlease, offers automated model-generation tools that shrink design timelines for mid-rise buildings.

Sustainability credentials influence bid success. Firms with Environmental Product Declarations and circular-material supply chains earn bonus points under Green Mark 2021 scoring. Hwa Seng Builder secured the USD 712 million Changi T5 airside job partly due to its track record in low-carbon asphalt and electrified equipment fleets. As carbon-pricing tightens, the market is likely to tilt further towards contractors able to document cradle-to-gate emissions.

Singapore Construction Industry Leaders

-

Woh Hup (Private) Ltd.

-

Obayashi Singapore Pte. Ltd.

-

Dragages Singapore Pte. Ltd.

-

Penta-Ocean Construction Co., Ltd. (Singapore)

-

Lum Chang Building Contractors Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Las Vegas Sands began the USD 8 billion Marina Bay Sands expansion featuring a 55-storey hotel and 15,000-seat arena, targeting completion by Jun 2030.

- July 2025: The Land Transport Authority started building Cross Island Line Phase 2, adding 15 km and six underground stations with daily ridership of 600,000 by 2032.

- May 2025: Changi Airport Group awarded USD 3.56 billion in contracts for Terminal 5 foundations and USD 712 million for airside infrastructure.

- March 2025: HDB offered 10,622 flats in the Feb 2025 BTO and Sale of Balance exercises, the largest release to date.

Singapore Construction Market Report Scope

| Residential | Apartments / Condominiums |

| Villas and Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation / Retrofit |

| Conventional On-Site |

| Modern Methods of Construction |

| Public |

| Private |

| Public-Private Partnership (PPP) |

| Core Central Region (CCR) |

| Rest of Central Region (RCR) |

| Outside Central Region (OCR) |

| By Sector | Residential | Apartments / Condominiums |

| Villas and Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation / Retrofit | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction | ||

| By Investment Source | Public | |

| Private | ||

| Public-Private Partnership (PPP) | ||

| By Region | Core Central Region (CCR) | |

| Rest of Central Region (RCR) | ||

| Outside Central Region (OCR) | ||

Key Questions Answered in the Report

What is the current size of the Singapore construction market?

The Singapore construction market size stood at USD 34.28 billion in 2026 and is projected to reach USD 45.62 billion by 2031.

Which segment is growing the fastest?

Infrastructure construction is forecast to record the quickest growth, with a 5.72% CAGR through 2031, driven by port, rail and airport megaprojects.

How big is the residential share of activity?

Residential work accounted for 46.62% of total output in 2025, underpinned by the Housing Development Board’s BTO programme.

Why are modern construction methods gaining traction?

Prefabrication and robotics help offset tight foreign-worker quotas and can lift productivity by up to 40%, supporting faster, safer project delivery.

What role do public-private partnerships play?

PPPs are the fastest-expanding funding model at a 5.76% CAGR through 2031, bringing private capital and expertise into large public assets such as airport terminals and integrated resorts.

How will labour policies affect project costs?

Foreign-worker quotas and higher levies are pushing firms to automate and upskill, and these measures are expected to add short-term cost pressure but long-term efficiency gains.

Page last updated on: