Philippines Building System Components Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

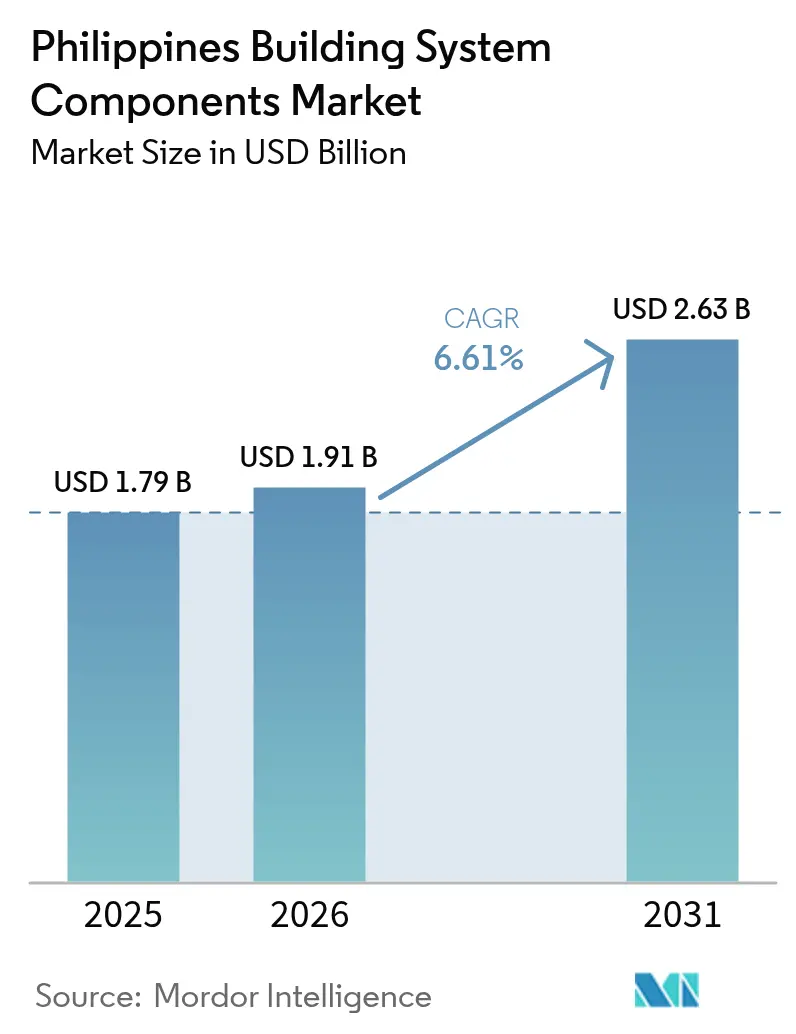

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Philippines Building System Components Market Analysis by Mordor Intelligence

The Philippines Building System Components Market size is projected to be USD 1.79 billion in 2025, USD 1.91 billion in 2026, and reach USD 2.63 billion by 2031, growing at a CAGR of 6.61% from 2026 to 2031.

Robust public infrastructure spending, a still-buoyant residential pipeline, and escalating demand for wind-rated and typhoon-resilient products underpin growth, while digital design tools are cutting waste and accelerating bid decisions. Contractors that package structural, mechanical, and electrical assemblies now win more tenders because they shorten site labor, a decisive advantage amid skilled-worker shortages. Demand is also migrating toward certified green materials as BERDE and LEED compliance moves from niche to baseline specification in NCR office towers, industrial cold-chains, and data centers. Finally, the archipelago’s chronic exposure to 20 tropical cyclones a year is hard-coding disaster-resilient standards into the procurement playbook, a change that is elevating reputable suppliers over generic imports.

Key Report Takeaways

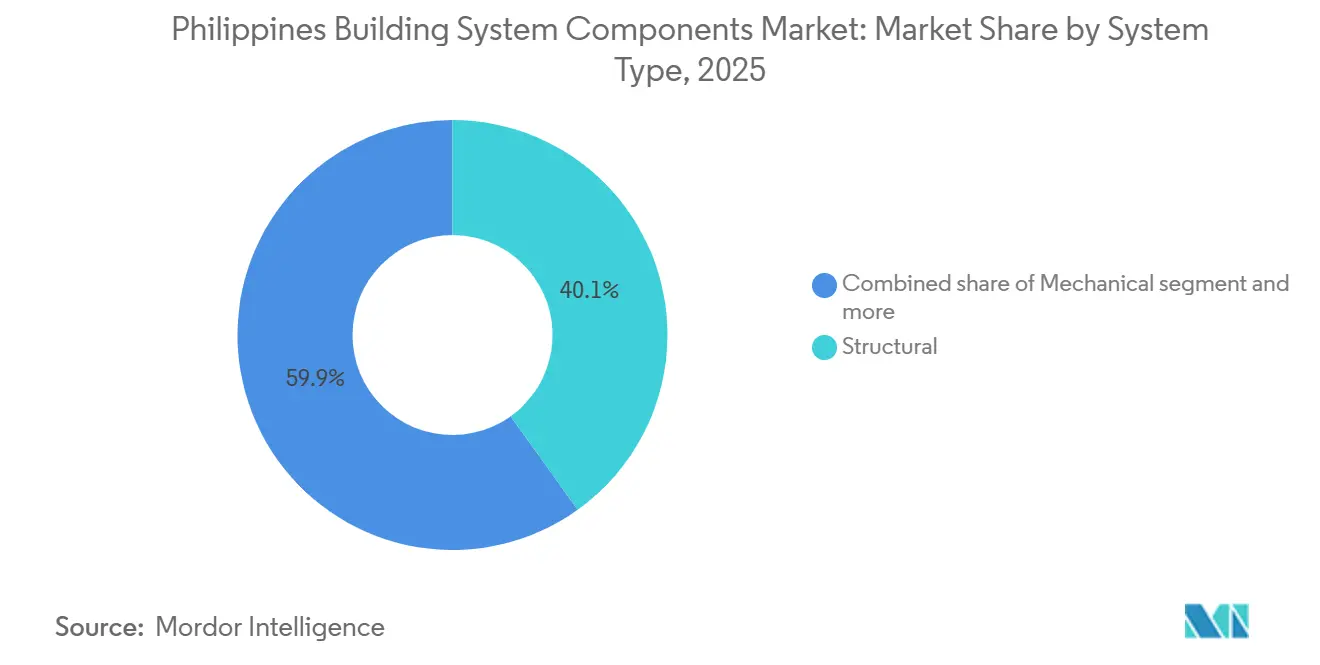

- By system type, structural systems held 40.1% of the Philippines building system components market share in 2025; mechanical components are forecast to expand at a 7.21% CAGR through 2031.

- By end user, residential buildings accounted for 47.2% of demand in 2025, whereas industrial and logistics facilities are set to grow at a 7.36% CAGR to 2031.

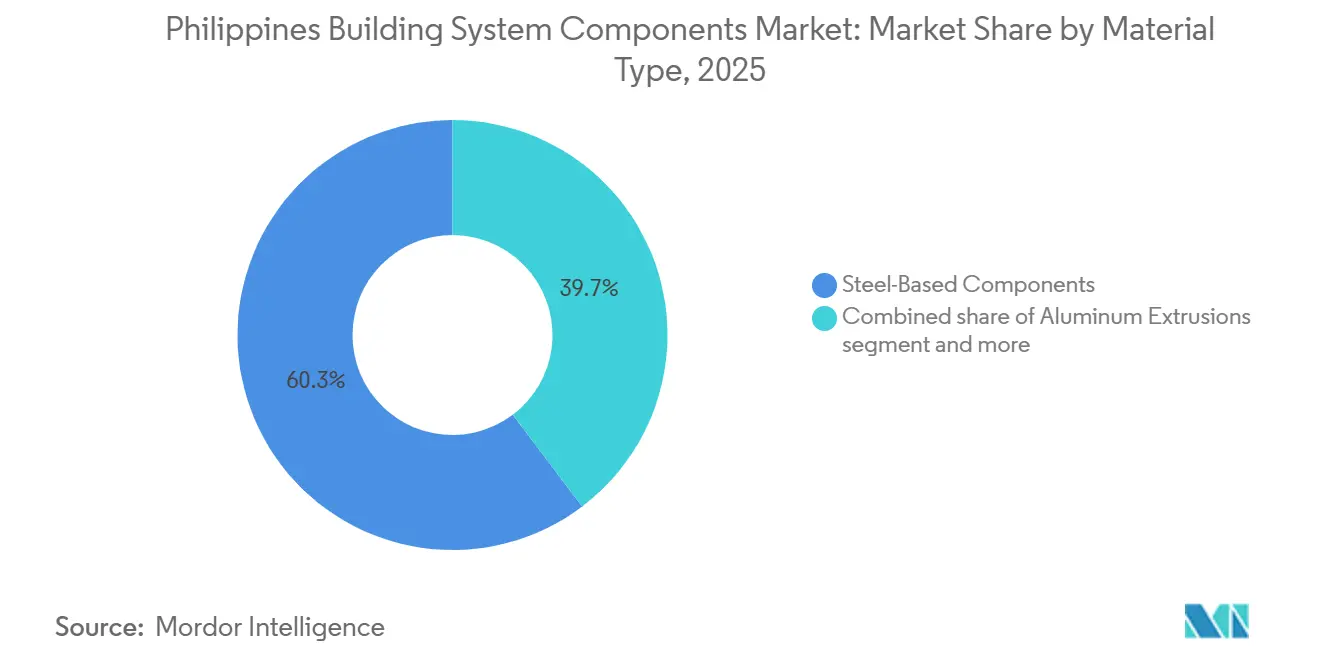

- By material, steel-based components captured 60.3% of the Philippines building system components market size in 2025, while gypsum and drywall boards are advancing at a 7.41% CAGR to 2031.

- By region, NCR (Metro Manila) contributed 40.9% of 2025 revenue, and Central Luzon is on track for a 7.71% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Building System Components Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure expansion is increasing demand for standardized building components | +1.8% | National, led by NCR, Calabarzon, Central Luzon | Medium term (2-4 years) |

| Strong residential construction pipeline boosting consumption of roofing and structural systems | +1.5% | Nationwide, early traction in NCR, Calabarzon, Davao | Short term (≤ 2 years) |

| Rising adoption of prefabricated and modular systems to reduce build time | +1.2% | NCR, Calabarzon, Cebu metros | Medium term (2-4 years) |

| Need for disaster-resilient construction is increasing the uptake of durable structural components | +1.1% | Coastal provinces, Eastern Visayas, Bicol, Northern Luzon | Short term (≤ 2 years) |

| Growing green building compliance is driving demand for insulation and high-performance materials | +0.9% | NCR, Makati, Bonifacio Global City, Cebu IT parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Expansion Increasing Demand for Standardized Building Components

The Department of Public Works and Highways’ FY 2026 budget of PHP 881.31 billion (USD 15.4 billion) prioritizes arterial roads, bridges, and flood-control projects that specify factory-certified steel trusses, precast tunnel rings, and modular drainage lines[1]Department of Public Works and Highways. "FY2026 Budget and Infrastructure Programs." DPWH, 2025. https://www.dpwh.gov.ph. Suppliers able to show Philippine National Standards certification and deliver repeatable batches on tight schedules are taking share from mom-and-pop fabricators. Public-private-partnership contracts for the Metro Manila Subway and Mindanao Railway further embed performance bonds and third-party inspections, forcing contractors to document traceability back to the mill. By reducing design variability, government buyers negotiate volume pricing and cut structural-steel lead times from eight to four weeks. As a result, integrated plants such as Steel Asia’s forthcoming Bulacan melt shop can lock multi-year supply agreements at scale.

Strong Residential Construction Pipeline Boosting Consumption of Roofing and Structural Systems

The 4 Pillars of Housing (4PH) program issued 143,301 Licenses to sell between January and September 2024, sustaining the procurement of pre-painted metal roofs, engineered trusses, and galvanized purlins[2]Philippine Statistics Authority. "Construction Statistics and Housing Data." PSA, 2024-2025. https://psa.gov.ph. Developers now favor 24-gauge, 40-year-warranty roof sheets, lifting average selling prices 8%–12% above commodity alternatives. Metro verticalization is redirecting demand toward composite floor decks and cold-formed studs that trim structural dead load and enable taller footprints on constrained lots. Remittance inflows, which reached USD 3.2 billion in December 2025, are buttressing down payments despite elevated mortgage rates. Mega wide Construction’s PHP 6.5 billion (USD 113 million) 2024 earnings highlight how modular roof cassettes—complete with insulation and gutters—are moving from pilot to mainstream adoption.

Rising Adoption of Prefabricated and Modular Systems to Reduce Build Time

Contractors that switch to bathroom pods, HVAC plenums, and pre-wired risers are compressing project schedules by up to 30%, an edge when penalty clauses bite after the first missed milestone. The Department of Human Settlements used modular shelters post-Typhoon Odette, giving the private sector proof of concept for factory-built quality and speed[3]Department of Human Settlements and Urban Development. "Modular Shelter Programs." DHSUD, 2024-2025. https://www.dhsud.gov.ph. Labor scarcity magnifies the value proposition: Metro Manila carpenter and welder wages jumped 15% in 2024 as infrastructure mega-projects absorbed crews. Data-center builders chasing 9-month commissioning windows are installing packaged rooftop units with factory-installed controls, while Kingspan and Lindab open Luzon distribution to bridge last-mile gaps. Adoption remains highest in NCR and Calabarzon, where crane fleets and lay-down yards enable safe module handling.

The need for disaster-resilient construction is increasing the uptake of durable structural components

With roughly 20 typhoons a year and frequent quakes, local codes now push wind-rated steel frames, impact-resistant cladding, and reinforced concrete that meet the National Structural Code of the Philippines. Coastal areas in Eastern Visayas, Bicol, and Northern Luzon enforce 250 km/h wind ratings for public assets, steering builders toward pre-engineered metal systems that ride out extreme weather. DHSUD’s modular shelters survived Category 4 winds without major repairs, giving factory solutions a real-world endorsement. Insurers now discount premiums up to 15% for NSCP-certified buildings, offsetting the 15%–20% price bump on resilient components. Steel Asia, Union Galva Steel, and panel specialists like Kingspan are capitalizing by offering mill-tested members and engineered fastening kits ready for high-wind zones.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependence on imported materials exposes costs to currency volatility | –1.3% | Nationwide, acute in steel, aluminum, gypsum | Short term (≤ 2 years) |

| Logistics and inter-island transport constraints are increasing delivery timelines | –0.8% | Visayas, Mindanao, and remote islands | Medium term (2-4 years) |

| Raw material price fluctuations are pressuring contractor margins | –0.7% | National, affects fixed-price contracts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Dependence on Imported Materials Exposing Costs to Currency Volatility

Philippine steel imports totaled 7.0-7.5 million metric tons in 2024, and January 2026 arrivals hit USD 497.35 million—up 17.84% year on year—magnifying peso swings that can erase 10% of margin in a quarter. Aluminum extrusions from China and Malaysia climbed 12% in early 2025 on energy surcharges, while gypsum inputs faced 30% freight surges during late-2024 Red Sea diversions. Steel Asia’s USD 1.1–1.4 billion melt-shop should supply 2.75 million tons of crude steel, yet start-up is still years away, so reliance on imports persists. Small and mid-size contractors rarely hedge currency risk, driving contractual fights over escalation clauses that slow approvals.

Logistics and Inter-Island Transport Constraints Increasing Delivery Timelines

Hauling building components through an archipelago of 7,640 islands lifts landed costs 10%–20% and adds one to three weeks to schedules outside Luzon. Port congestion at Manila and Batangas routinely delays roll-on/roll-off loadouts by up to a week, forcing contractors to pad programs or incur liquidated damages. Prefabricated pods need special crating and marine insurance, hiking logistics overhead 15%–25% relative to mainland routes. Remote provinces such as Palawan depend on secondary ports with shallow drafts, restricting vessel size and raising per-ton rates. EEI’s strategy of pre-positioning inventory in Cebu and Davao shelters projects from the worst delays but locks working capital into warehouses that deliver no margin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Mechanical Systems Capture Momentum in the Digital Economy

Mechanical assemblies—HVAC, chilled-water lines, and fire suppression—are expanding at a 7.21% CAGR, eclipsing the broader Philippines building system components market. Structural systems still dominated 40.1% of 2025 revenue, thanks to standardized frames for housing and public works. Surge capacity is now shifting to mechanical packages as hyperscale operators, including Microsoft and Google, are readying cloud regions that demand N+1 cooling redundancies. Integrated design-build contractors are bundling mechanical, electrical, and plumbing (MEP) into single-source agreements, slashing interface risk and giving ABB and Schneider Electric clear room to upsell IoT switchgear. Over the forecast window, mechanical upgrades become unavoidable for data sovereignty, vaccine cold chains, and agri-food exports, supporting premium pricing even as steel frames reach commodity status.

Project owners consider total-cost-of-ownership instead of capex alone. Factory-tested air-handling units with digital twins cut commissioning time by half and reduce early-life failures that plague site-built systems. Lenders financing data centers now stipulate performance guarantees that only modular mechanical vendors can meet, accelerating the share pivot. By 2031, the Philippines' building system components market size for mechanical segments is on track to push USD 0.85 billion, while structural share erodes as prefabrication saturates.

By End-User: Fulfillment Hubs Push Industrial and Logistics to the Front

Residential construction delivered 47.2% of 2025 turnover, but industrial and logistics facilities are the growth engine with a 7.36% CAGR through 2031. E-commerce giants Lazada, Shopee, and TikTok Shop are signing leases of up to 1 million sq ft a year in Calabarzon, each warehouse asking for 30-foot clear heights, wide column grids, and dock-levelers that pre-engineered steel buildings deliver on a 20% faster timeline. Cold-storage is another spur: grocery platforms and vaccine logistics need –25 °C environments, propelling demand for insulated metal panels and high-capacity evaporative condensers.

Commercial towers keep a steady baseline of orders for curtain walls and smart-lighting kits, especially in Makati and Bonifacio Global City, where multinational tenants bid for BERDE Gold space. Yet rent growth lags warehousing, so capital is tilting toward logistics parks that hit 12%–15% yields. Industrial land in Bulacan trades at 30%–50% discounts to NCR plots, widening margin headroom and reinforcing the pivot. The Philippines' building system components market will see industrial share climb five percentage points by 2031 as omnichannel retail and near-shoring reshape the landscape.

By Material Type: Drywall Surges as Developers Chase Speed and Sustainability

Steel held 60.3% of material demand in 2025, reflecting entrenched use of rebar, decking, and studs, but gypsum and drywall boards are registering a 7.41% CAGR on the back of condominium interiors and fast-cycle office refurbishments. Drywall lets developers turn over units weeks earlier because boards arrive cut-to-length and require no curing. The Philippines building system components market size for gypsum solutions is slated to exceed USD 0.32 billion by 2031, powered by Knauf, Saint-Gobain Gyproc, and USG Boral, each extending distribution into Visayas and Mindanao.

Aluminum extrusions for thermally broken façades are also advancing as BERDE compliance tightens. However, spiking ingot prices threaten margins, pushing contractors to value-engineer hybrid façades that pair steel mullions with fiberglass pressure plates. Composite panels and engineered wood sit in the “other” bucket, serving acoustic and aesthetic niches. Steel remains unbeatable for heavy infrastructure and high-seismic zones, but residential and hospitality segments are tilting to drywall because lower mass and fewer wet trades translate into cleaner, quieter sites that please city neighbors.

Geography Analysis

NCR dominated with 40.9% of 2025 receipts thanks to vertical residences, premium offices, and marquee civil works, yet sky-high land at USD 5,200 per square meter and chronic congestion are tipping new capital to satellite provinces. Developers now deploy prefabricated bathrooms, packaged HVAC, and unitized façades to trim site labor and dodge traffic-driven overtime. BERDE adoption is most pronounced in Makati towers, where owners secure 15% rent uplifts for green space, supporting higher-spec insulation and advanced glass. Infrastructure outlays—anchored by the USD 15.4 billion FY 2026 DPWH budget—keep structural steel and precast suppliers busy, but right-of-way disputes still stretch timelines.

Central Luzon, by contrast, offers land at half Manila’s cost and direct port access via Subic and Manila North Harbor, propelling a 7.71% CAGR until 2031. Logistics operators erect one-million-square-foot sheds with 30-foot clears in Bulacan, and data-center investors shortlist Clark, where dual-feed power and fiber islands reduce downtime risk. Cement, rebar, and panel plants are clustering to shave haul-miles, slicing 5%–7% off delivered cost and reinforcing a self-feeding ecosystem.

Calabarzon, bounded by Cavite, Laguna, and Batangas, maintains momentum on semiconductor fabs and mid-income housing, supported by expressway links that guarantee two-hour door-to-door deliveries to NCR sites. The wider Philippines still battles fragmented supply chains; Visayas resorts and Mindanao agro-export cold-stores order modular kits but factor in two-week marine transit buffers. Post-Odette shelter deployments proved industrialized building methods can conquer distance, suggesting that once logistics bottlenecks ease, provincial penetration will accelerate.

Competitive Landscape

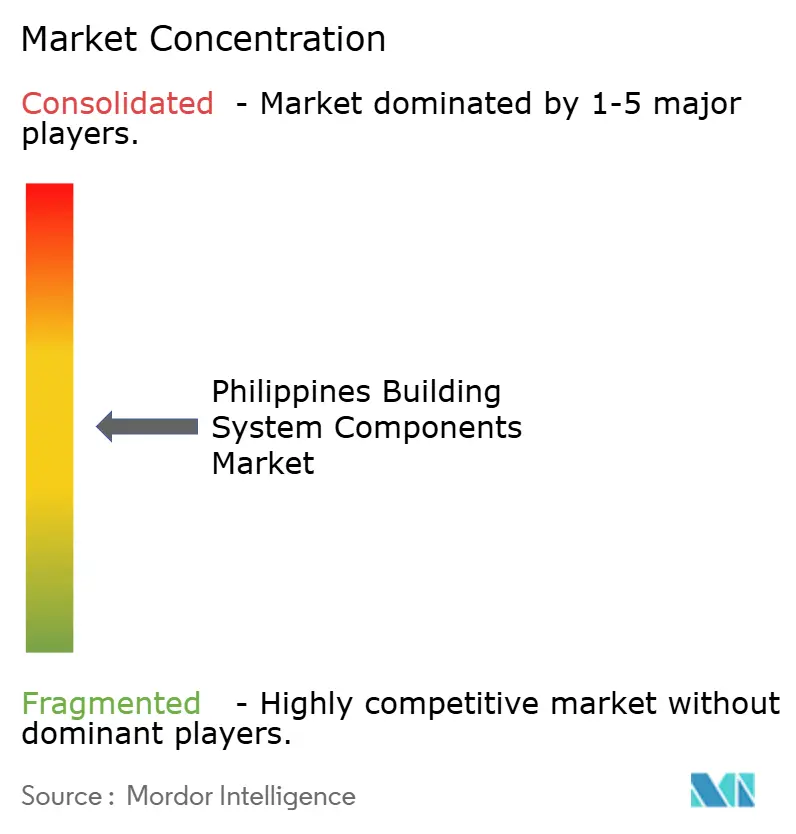

Competition is moderate, with multinationals Holcim, Saint-Gobain Gyproc, and Knauf squaring off against domestic stalwarts Steel Asia, Union Galva Steel, and JEA Steel. Scale players exploit broad catalogs and robust QA systems to clinch DPWH and PPP contracts that mandate traceable mill certificates. Integrated system bundles—structural skeletons plus pre-wired electrical and mechanical assemblies—are now a default tender requirement on subway stations and data halls, crowding out single-trade subcontractors. BIM is the battlefield for differentiation: suppliers that furnish parametric objects and live inventory feeds win early design lock-in and cut RFIs by double digits.

Strategic capex is reshaping supply. SteelAsia’s USD 1.1–1.4 billion melt-shop aims at 2.75 million tons annual output, a hedge against peso volatility and import quotas. Holcim’s USD 84 million Bulacan line adds infrastructure-grade cement capacity minutes from the North Luzon corridor. Kingspan and Zamil promote pre-engineered buildings to logistics developers chasing 20% faster completion and 12% IRR. ABB and Schneider Electric ride the data-center wave with IoT switchgear and digital substations, embedding service contracts that deepen switching costs.

Niche players carve defensible ground in disaster-resilient and cold-chain envelopes. ENERCON and Ultra Insulated Panels focus on –25 °C cleanrooms where polymeric facings and cam-lock joints trim downtime. Kirby Building Systems intensifies outbound sales to Visayas, where port capacity is rising, while EEI pre-positions steel and drywall inventory in Cebu and Davao to counter shipping choke points. Over the forecast horizon, accelerating compliance spend, digital tooling, and capex intensity favor well-capitalized incumbents, implying mild consolidation but leaving room for specialists with proprietary IP.

Philippines Building System Components Industry Leaders

-

USG Boral (Building Products)

-

Knauf Philippines

-

Saint-Gobain Gyproc Philippines

-

Etex Group

-

SteelAsia Manufacturing Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Steel Asia confirmed that its USD 1.1–1.4 billion melt-shop will lift crude-steel capacity to 2.75 million tons, trimming import exposure and feeding Build Better More megaprojects.

- December 2025: Holcim Philippines finalized a USD 84 million Bulacan plant expansion, adding high-spec cement lines for Metro Manila rails and bridges.

- November 2025: Mega wide posted USD 113 million 2024 earnings and earmarked new modular warehouses to capture Calabarzon e-commerce demand.

- October 2025: EEI logged USD 625 million in 2024 revenue and began staging inventory in provincial hubs to blunt inter-island delays.

Philippines Building System Components Market Report Scope

| Structural |

| Mechanical |

| Electrical |

| Plumbing |

| Residential Buildings |

| Commercial Buildings |

| Industrial and Logistics |

| Others |

| Steel-Based Components |

| Gypsum / Drywall Boards |

| Aluminum Extrusions |

| Other Materials (Composite, Wood, etc.) |

| NCR (Metro Manila) |

| Calabarzon |

| Central Luzon |

| Rest of Philippines |

| By System Type | Structural |

| Mechanical | |

| Electrical | |

| Plumbing | |

| By End-User | Residential Buildings |

| Commercial Buildings | |

| Industrial and Logistics | |

| Others | |

| By Material Type | Steel-Based Components |

| Gypsum / Drywall Boards | |

| Aluminum Extrusions | |

| Other Materials (Composite, Wood, etc.) | |

| By Region | NCR (Metro Manila) |

| Calabarzon | |

| Central Luzon | |

| Rest of Philippines |

Key Questions Answered in the Report

What was the value of the Philippines' building system components market in 2025?

It stood at USD 1.79 billion in 2025 and is projected to reach USD 2.63 billion by 2031.

Which segment is growing fastest within the sector?

Mechanical systems, driven by data centers and cold-storage builds, are advancing at a 7.21% CAGR through 2031.

Why is Central Luzon attracting so many new projects?

Land is 30%–50% cheaper than Metro Manila, yet it retains port and expressway access, enabling warehouses and factories to serve NCR consumers quickly.

How are BERDE rules influencing material choices?

They mandate higher R-values and low-e glass, pushing demand for insulated panels and thermally broken façades despite higher upfront cost.

What is the biggest supply-chain bottleneck?

Inter-island shipping can add up to three weeks and 20% to costs for Visayas and Mindanao sites, making local inventory hubs a competitive edge.

How are contractors coping with peso volatility on imported steel?

Many now include escalation clauses or pursue dual-currency bids, while large firms explore hedging once order books justify the fees.

Page last updated on: