Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

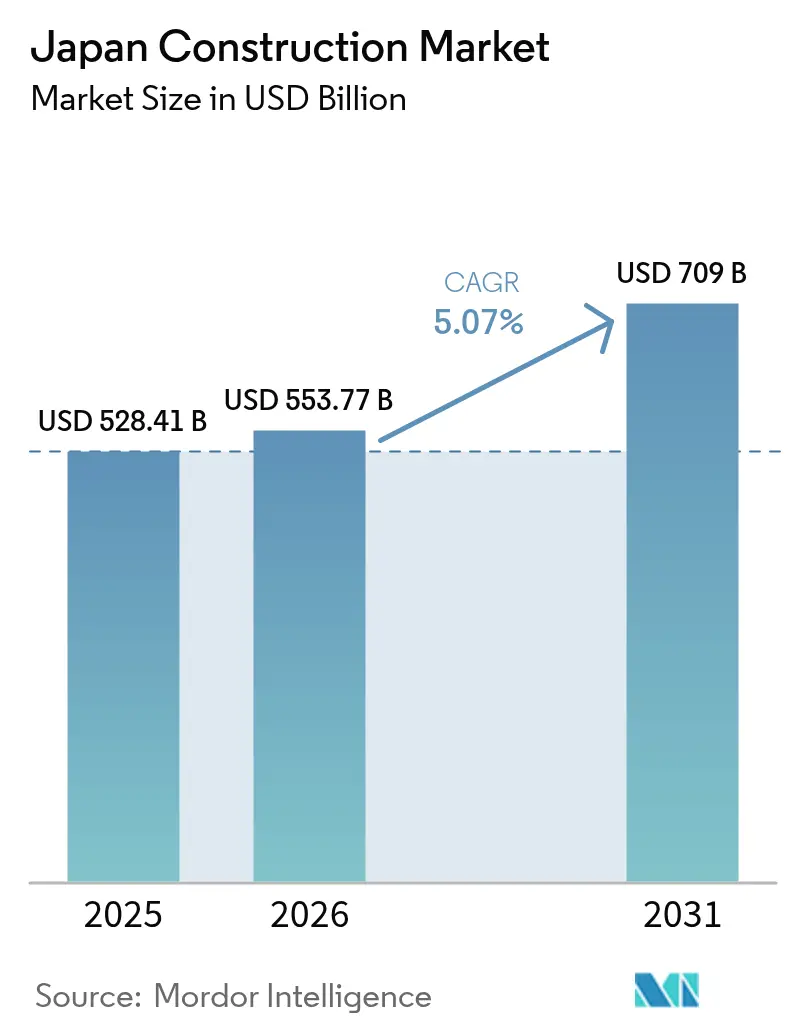

| Base Year Market Size (2025) | USD 528.41 Billion |

| Market Size (2026) | USD 553.77 Billion |

| Market Size (2031) | USD 709 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Construction Market Analysis by Mordor Intelligence

The Japan construction market size reached USD 528.41 billion in 2025 and USD 553.77 billion in 2026 and is projected to reach USD 709 billion by 2031 at a 5.07% CAGR, supported by steady public works spending, policy-led seismic retrofits, and an expanding pipeline for renewables and semiconductors. Labor scarcity and higher input costs pressured margins in 2025 as labor unit prices rose across public-works design schedules and materials costs remained elevated, keeping bid pricing and delivery schedules under strain. Government measures that preserved disaster-resilience budgets and tightened procurement standards sustained work volumes, while the Construction Business Act amendments in 2025 reinforced price-adjustment clauses and wage fairness. Policy signals on BIM and digital twins increased compliance requirements and shifted capability advantages to firms with integrated design-to-site workflows. The offshore wind program, data-center investments, and incentives for domestic semiconductor capacity anchored the medium-term order book, though cost volatility and permitting timelines require balanced risk allocation in contracts.

Key Report Takeaways

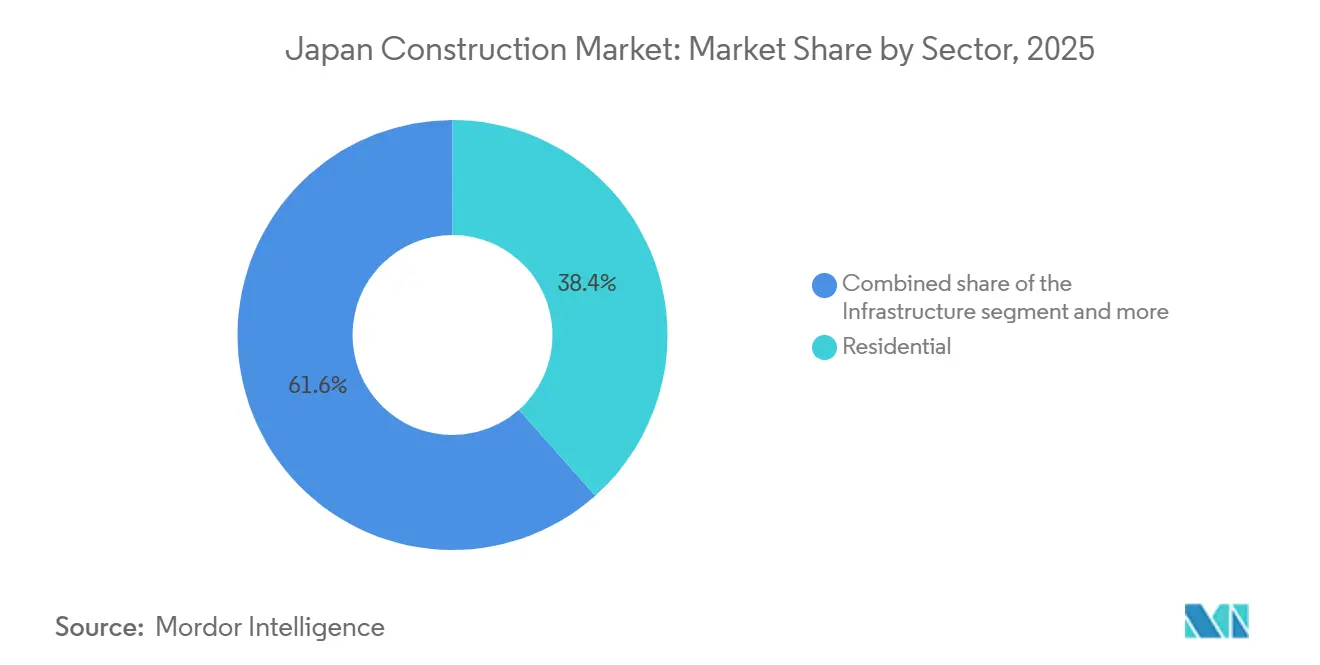

- By sector, residential accounted for 38.44% of Japan’s construction market size in 2025, and infrastructure is set to grow at a 6.12% CAGR by 2031.

- By construction type, new construction held 81.22% of Japan’s construction market share in 2025, while renovation is anticipated to advance at a 6.55% CAGR by 2031.

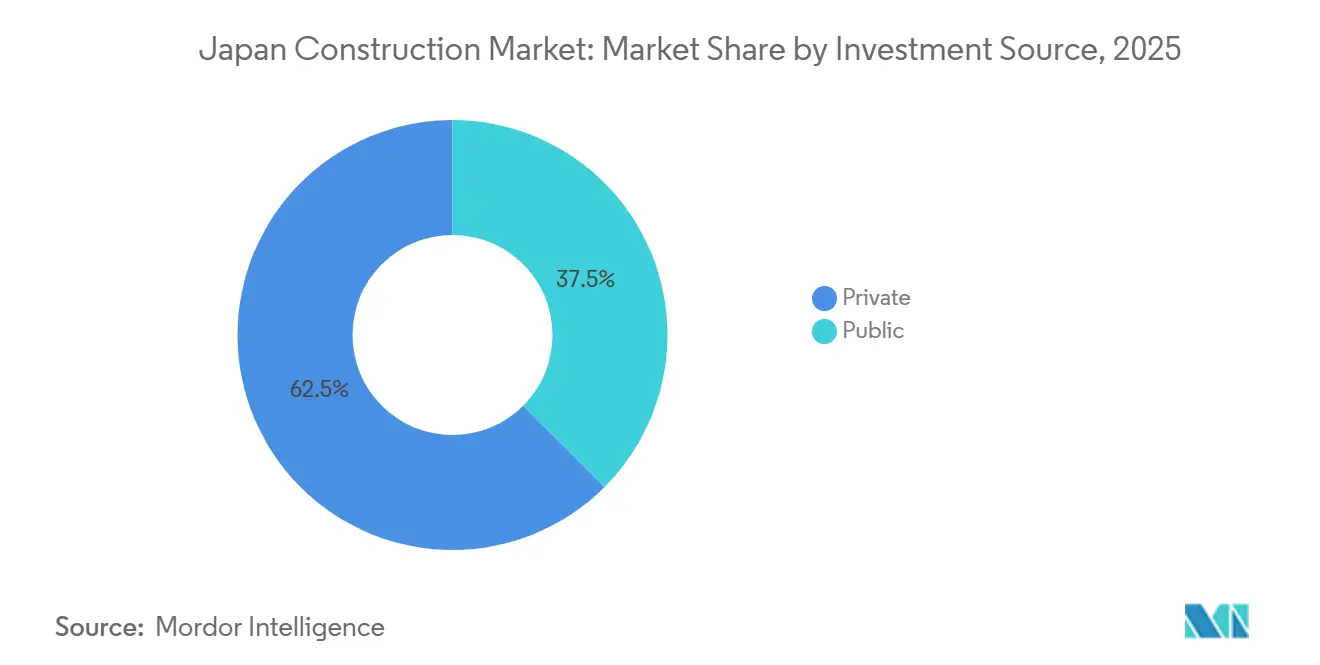

- By investment source, private investment represented 62.50% of Japan’s construction market size in 2025, and public spending is expected to rise at a 6.33% CAGR through 2031.

- By construction method, conventional on-site captured 66.45% of Japan’s construction market share in 2025, whereas modern methods are likely to register a 7.10% CAGR through 2031.

- By geography, Kanto recorded 35.44% of Japan’s construction market size in 2025, and Hokkaido is poised to grow at a 6.99% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy project pipeline (offshore wind, solar) | +1.2% | Hokkaido, Aomori, Akita, Yamagata | Medium term (2-4 years) |

| Government stimulus & public-works spending | +0.9% | National | Medium term (2-4 years) |

| BIM & digital-twin mandate (MLIT 2026) | +0.8% | National | Short term (≤ 2 years) |

| Seismic retrofitting & urban-redevelopment wave | +0.7% | Kanto, Kansai, major metropolitan areas | Long term (≥ 4 years) |

| Tokyo metropolitan housing-demand pressure | +0.6% | Kanto (Tokyo) | Short term (≤ 2 years) |

| Wood-based high-rise subsidies (CLT, timber skyscrapers) | +0.5% | National, with early gains in urban cores | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-energy project pipeline (offshore wind, solar)

In Hokkaido, Aomori, Akita, and Yamagata, Japan's renewable energy initiatives are set to boost the construction market by a modest ~1.2% over the next 2–4 years, with offshore wind and solar energy leading the charge. Offshore wind projects, especially those spearheaded by JERA in Akita and Aomori Prefectures, are advancing towards construction, following government-sanctioned auction rounds. Starting in 2026, these projects will drive demand for marine civil works, turbine foundations, port enhancements, and grid connections, solidifying offshore wind's status as a premium infrastructure segment in northern Japan. Meanwhile, solar PV development is actively unfolding in Hokkaido and Aomori. This momentum is bolstered by established assets like the SoftBank Tomatoh Abira Solar Park and the addition of mid- to large-scale projects. Solar initiatives are consistently engaging in EPC, electrical, and grid upgrades, with a gradual uptick in battery storage integration. In summary, while solar ensures stable construction activity in the short term, offshore wind is poised to fuel infrastructure growth in the medium term.

Government stimulus & public-works spending

Public-works expenditure held near JPY 6,085.8 billion (USD 43.5 billion) in FY2025, with allocations weighted to disaster prevention and national resilience initiatives that sustained construction backlogs even as overall fiscal space remained tight[1]Ministry of Finance Japan, “Japanese Public Finance Fact Sheet FY2025,” Ministry of Finance. Within that envelope, spending on seismic retrofitting, flood-control systems, and bridge renewal was prioritized after the 2024 earthquake season underscored the need to upgrade older assets. The December 2025 amendments to the Construction Business Act embedded standard labor costs and price-adjustment norms into contracting practices, signaling an intent to improve wage pass-through and stabilize procurement in Japan's construction market. Digital directives on BIM and CIM for public works continued to shape qualification thresholds in bidding and changed delivery models in favor of integrated contractors with stronger design-management systems[2]Ministry of Land, Infrastructure, Transport and Tourism, “Summary of the White Paper on Land, Infrastructure, Transport and Tourism in Japan, 2025. While the policy stance provides visibility for civil and resilience projects, supply-side constraints, including labor caps and higher financing costs since early 2025, have put a premium on productivity and modularization in the Japan construction market.

BIM & digital-twin mandate (MLIT 2026)

Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT) is set to roll out a mandate for BIM and digital twins by 2026. This initiative is poised to give the national construction market a modest boost of approximately 0.8% over the next two years. The mandate aims to broaden the adoption of Building Information Modeling (BIM) in public infrastructure and building projects. It emphasizes integrating digital design, managing lifecycle data, and improving collaboration among contractors, designers, and asset owners. This move aligns with Japan's overarching i-Construction initiative, which aims to boost productivity and address labor shortages. In the immediate future, the mandate is expected to lead to heightened investments in digital design services, software enhancements, training, and data infrastructure by contractors across the nation. While the mandate doesn't directly spur new construction projects, it does hasten the modernization of processes, curtail rework and cost overruns, and bolster project transparency. As the mandate takes effect in national and public works projects, firms that have already embraced BIM and digital twin technologies will likely find themselves at a competitive edge in both bidding and execution.

Seismic retrofitting & urban-redevelopment wave

Urban resilience programs advanced as Tokyo updated its resilience plan, focusing on structural retrofits and flood defenses, reflecting long-horizon risk planning for earthquakes and typhoons. Authorities cite the high probability of a major seismic event for the capital in the coming decades, which supports sustained demand for retrofitting of pre-1981 building stock in the Japan construction market. Codes and implementation frameworks put greater emphasis on mandatory checks for older buildings and on quality assurance during complex renovations in dense districts. Large cities increased investments in multi-layered protection that pairs levees and underground reservoirs with early-warning and resident training measures, broadening the range of projects beyond heavy civil works alone. This convergence of public and private actions positions seismic upgrade work as a durable driver for the Japan construction market into the 2030s.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortage & aging workforce | -1.3% | National, acute in rural areas | Long term (≥ 4 years) |

| Imported-material inflation & weak yen | -0.8% | National | Medium term (2-4 years) |

| Zoning reforms favor renovation over new-builds | -0.4% | Tokyo, Osaka, regional cities | Medium term (2-4 years) |

| Carbon-footprint approval bottlenecks | -0.3% | Urban cores, MLIT-regulated zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-labor shortage & aging workforce

Japan’s construction workforce continued to age through 2025, which constrained effective capacity even before accounting for new overtime caps that limit hours per worker and required firms to rebalance staffing and schedules in the Japan construction market. Industry plans now lean on modularization, automation, and accelerated training to close skill gaps, with BIM and CIM integration shifting manual coordination to digital preconstruction. Professional bodies have flagged multi-year deficits in skilled trades if productivity does not improve fast enough, which pushes general contractors to standardize designs and expand off-site fabrication. Policy discussions also include routes for longer-term residency and skill-tier progression for foreign workers to stabilize site teams, though language and safety training needs remain binding constraints. The labor profile is therefore a central factor in delivery risk, pricing, and the uptake of modern methods in the Japan construction market.

Imported-material inflation & weak yen

Import-cost pass-through lifted producer prices during 2024 and 2025 while a weaker yen amplified the local-currency cost of inputs, keeping pressure on construction material indices and project estimates. Industry metrics reported cumulative increases in key material baskets since 2021, combined with labor unit-price revisions for public works, which together lifted total project costs and tightened bid margins in the Japan construction market. Central bank rate adjustments in January 2025 modestly raised financing costs, affecting contractors with larger working-capital needs and heightening diligence around payment milestones. The 2025 contracting reforms sought to formalize risk-sharing for material volatility and to prohibit unreasonably low bids, but the transition placed new administrative demands on firms and clients while the pricing environment stayed firm. Cost-certainty has therefore become a deciding factor in both public and private decisions, favoring standardized designs and supply chain integration in the Japanese construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Gains Momentum on Renewable Push and Semiconductor Revival

Residential accounted for 38.44% of the Japan construction market size in 2025, reflecting Kanto’s pull and stable replacement demand for older housing stock, while infrastructure’s 6.12% CAGR through 2031 positions it as the fastest-moving component through the forecast horizon. Priority programs include resilience upgrades for bridges and flood control, offshore wind site preparation and ports, and utility reconfiguration around new grid and storage assets that support clean power deployment. Commercial demand benefited from logistics and data center expansions targeting power-secure locations and fiber connectivity, which are reshaping site selection and building standards in the Japan construction market. The offshore wind buildout advanced with Round-3 awards for Aomori and Yamagata, which share June 2030 commercialization goals and reinforce the civil and electrical balance-of-plant pipeline. Semiconductor localization added specialized cleanroom and MEP demand as the Rapidus IIM-1 pilot line in Hokkaido moved into operation in 2025, positioning related industrial builds as a near-term construction theme.

The residential segment wrestled with an April 2025 code revision that increased the complexity of timber structural calculations, which temporarily lowered starts among smaller firms before activity normalized later in the year. Demand for energy-efficient homes remained resilient as owners prioritized insulation, rooftop solar readiness, and lower lifetime operating costs in the Japan construction market. Infrastructure will likely keep trending higher on elevated resilience budgets and offshore wind execution, with the civil-heavy mix boosting order coverage for top-tier general contractors. On the commercial side, data center projects, including the 300 MW-class site in Tomakomai, Hokkaido, are reshaping local supply chains and construction logistics around power availability and renewable sourcing models in the Japan construction market. This sector balance sets a stable base for 2026 with diversification across housing, logistics, energy, and critical manufacturing as key anchors.

By Construction Type: Renovation Surges as Zoning Incentives Shift Capital Allocation

New construction accounted for 81.22% of the Japan construction market size in 2025, yet renovation is forecast to grow at 6.55% CAGR through 2031 as policies steer capital to asset renewal and life extension, where risk-adjusted returns are attractive. Bridge and tunnel assets that cross age thresholds will require inspection and reinforcement, which supports steady maintenance contracts and improves asset safety profiles in the Japan construction market. Urban owners are also upgrading offices to align with energy targets and to refresh tenant experiences, with ZEB pathways a priority for projects that can benefit from digital modeling from design to commissioning. Renovation profiles also show faster cycle times when prefabricated elements can be integrated, which suits an environment with overtime caps and scarce skilled labor. Public program support for BIM adoption and city-scale digital twins is helping to reduce discovery risk and to enhance construction sequencing across complex brownfield sites in the Japan construction market.

The Japanese construction industry is also rebalancing toward refurbishment in districts where greenfield development faces disaster risk or zoning limits, thereby raising the value of structural strengthening, envelope upgrades, and building-systems modernization. Renovation leaders are standardizing solutions and harnessing BIM libraries to reduce design time and field rework, which can offset higher wage floors and materials volatility. Owners who prioritize lifecycle carbon are also turning to renovation when embodied-carbon advantages are clear and when permitting for demolition-rebuild is more involved. The combined effect is a healthier mix of traditional new builds and renovations that spreads risk and improves asset performance in the Japan construction market. The combined effect is a healthier mix of traditional new builds and renovations that spreads risk and improves asset performance in the Japan construction market. This shift is expected to hold as more cities integrate digital-twin layers into planning and as code trajectories continue to lift energy and safety standards.

By Investment Source: Public Spending Accelerates on Disaster Resilience and Semiconductor Incentives

Private investment held a 62.50% share in 2025, while public spending is set to record the faster 6.33% CAGR to 2031 as resilience, offshore wind, and industrial policy continue to command budget priority in the Japan construction market. Public-works expenditures stayed near JPY 6 trillion (USD 42.9 billion) in recent years and reached JPY 6,085.8 billion (USD 43.5 billion) in FY2025 to safeguard critical networks and accelerate upgrades that reduce disaster losses over time. Within that plan, a large allocation targeted disaster prevention and national resilience, including flood-control measures and seismic retrofits for high-priority assets across large metropolitan regions in the Japan construction market. Funding routes also encompass support for strategic industries, including semiconductors, where facility builds, and associated utilities require specialized cleanroom and MEP capabilities[3]Kajima Corporation, “Integrated Report 2025,” Kajima. The policy mix gives larger general contractors a steadier runway for civil-heavy work, with collaboration models and PPP structures applied where appropriate.

Private capital remains active across data centers and logistics, which includes a 300 MW-class hyperscale development in Hokkaido that underscores the importance of proximity to renewables and grid capacity for site selection in the Japan construction market. Corporate strategies and RE100 commitments are also guiding developments that prioritize operational efficiency and lower emissions in new commercial stock. Monetary policy conditions shifted in early 2025 with a rate increase, although funding remained accommodative by global standards and continues to support investment where returns are underwritten by long contracts or strong tenant demand. Public investment is likely to grow faster than private over the forecast due to mandated maintenance backlogs and long-dated clean power targets, which stabilizes the base for the Japan construction market through 2031. This balance favors contractors with cost-control systems, compliance readiness, and the ability to integrate BIM-driven processes into procurement and delivery.

By Construction Method: Modular and Prefabricated Approaches Gain Traction Amid Labor Constraints

Conventional on-site construction accounted for 66.45% of activity in 2025, while prefabricated and modular approaches are forecast to post a 7.10% CAGR through 2031 as contractors shift labor off-site and industrialize assembly in the Japan construction market. Integrated housing majors pair design and factory manufacturing to deliver standard modules with tighter tolerances and lower rework rates, which helps offset higher wage floors and tighter overtime rules at job sites. Hybrid mass timber and prefabricated elements are moving into select mid-rise schemes as codes evolve and as tenant demand favors low-carbon buildings in premium clusters. For large projects, modularization is advancing in plant rooms, bathroom pods, and façade systems, compressing critical-path work and reducing exposure to site labor variability in the Japan construction market. The digital layer acts as the enabler, with BIM standards and content libraries that simplify coordination and more predictable interfaces between factory-made components and on-site trades.

The Japanese construction industry is also piloting low-emission equipment and site automation, which complement factory-first production and support quieter, safer operations in dense neighborhoods. Policy frameworks such as i-Construction 2.0 aim to boost productivity and streamline verification, aligning with modular workflows and reducing administrative friction in public tenders. Timber design standards and the April 2025 code update are shaping where and how prefabrication can scale in multi-story residential and office projects, especially as owners weigh energy, carbon, and resilience together in siting decisions. Equipment innovations such as automated lifting coordination and heavy-plant telematics are being embedded into major sites to cut idle time and improve safety outcomes in the Japan construction market. These shifts are gradual but compound with every design cycle as more owners and public agencies specify modular readiness and digital deliverables.

Geography Analysis

Kanto dominated the Japan construction market in 2025 with a 35.44% share, while Hokkaido is expected to record the fastest growth at a 6.99% CAGR through 2031, reflecting emerging investments in renewable energy and digital infrastructure. Kanto’s 2025 leadership reflects a strong foundation in residential and commercial redevelopment, supported by transit corridor investments and urban-district upgrades that keep general contracting and specialty trades in steady rotation in the Japan construction market. Tokyo’s large pipeline includes premium office and mixed-use towers, where tenant demand for energy performance standards raises the specification level for façades, HVAC, and controls. Climate resilience priorities continue to support flood-defense improvements and seismic retrofits, spreading work across multiple subtrades and consulting disciplines in the Japan construction market. Within the Kanto metro, housing starts normalized after code-driven adjustments in mid-2025, with large housebuilders regaining schedule predictability and smaller firms recalibrating to new structural and insulation rules. Public works procurement in the region is also shaped by BIM-readiness requirements, which add a capability filter to tender participation in the Japan construction market.

Hokkaido’s trajectory is anchored by renewable energy and digital infrastructure, which creates demand for marine civil works, substation builds, and high-capacity transmission, alongside large-scale site development for data centers. The designation of promotion zones for offshore wind has set the stage for multi-year construction schedules and port modernization, with contractors aligning vessel access, laydown areas, and fabrication bases to project designs in the Japan construction market. Tomakomai’s hyperscale computing cluster exemplifies how renewable proximity, local-government collaboration, and land availability can attract power-intensive builds, which in turn draw supplier ecosystems and workforce pipelines. As these programs mature, the regional mix of projects should widen to include storage, grid upgrades, and industrial facilities that leverage cleaner electricity in the Japan construction market.

Kansai, Chubu, and Tohoku offer complementary demand. Kansai includes signature urban redevelopments and post-Expo legacies that sustain interior and fit-out works through 2026 in the Japan construction market. Chubu’s manufacturing base supports expansions and modernizations in automotive and adjacent sectors, while Tohoku benefits from clean-energy growth that aligns with long-term reconstruction plans. Across the rest of Japan, logistics hubs and industrial parks continue to be refreshed and expanded where transport corridors and land banks support multi-tenant facilities. The overall geographic spread is balanced, with energy and resilience policies shaping tallied volumes where local regulations and grid availability allow investment to scale in the Japan construction market.

Competitive Landscape

Competitive intensity is moderate, with the top general contractors capturing a significant portion of very large civil, infrastructure, and complex building packages, while residential and small commercial work remains fragmented among regional specialists in the Japan construction market. Strategic expansions emphasize data centers, semiconductors, and renewables, where MEP content, cleanroom standards, and marine engineering are differentiators for scale players. In October 2025, Obayashi acquired U.S.-based GCON Inc., expanding its reach in critical-environment construction that serves data-center and semiconductor clients across multiple states. Kajima reported overseas revenue milestones in FY2024 and is executing semiconductor-linked facilities such as the Rapidus IIM-1 pilot line, which demonstrates its process and cleanroom build capabilities in the Japan construction market. Shimizu has added interior fit-out capacity in Asia and North America to target hotel and tenant-improvement demand, aligning with workflow integration goals across markets.

Technology programs are central to productivity plays. Obayashi is rolling out site-management and lifting-coordination systems to improve crane operations and reduce idle time, while also piloting alternative-power equipment to help decarbonize heavy operations at construction sites in the Japan construction market. Kajima has deployed automated-mobility systems for tunneling and is scaling BIM content and workflows to drive down errors in complex fit-outs. Shimizu’s logistics and industrial builds are targeting ZEB standards, supported by standardized design modules that accelerate delivery. Across the peer set, digital compliance and execution capability are becoming prerequisites for public tenders, which channels volume toward firms with strong back-office and engineering stacks in the Japan construction market. These moves collectively improve resilience to input-cost swings and labor constraints.

Capital allocation in 2025 and 2026 also features targeted M&A and partnerships. Daiwa House’s U.S. expansion through Stanley Martin and Windsor Homes adds scale and procurement advantages relevant to industrialized housing workflows in the Japan construction market. ITOCHU made moves to strengthen its construction-materials value chain by adding a general contractor affiliate and pursuing bolt-ons in related product lines. Taisei’s medium-term plan includes real estate alliances and renewable energy allocations that build optionality for steady income and development opportunities. On the energy side, policy reforms after 2024 made offshore wind more investable and saw zero-premium awards at JPY 3.00 (USD 0.021) per kWh in Round-3 selections, which nudged expectations for cost curves and vendor strategies in the Japan construction market. The still-fragmented tail of residential, interiors, and small civil packages remains active and price competitive, especially outside major metros.

Japan Construction Industry Leaders

Obayashi Corporation

Kajima Corporation

Shimizu Corporation

Taisei Corporation

Takenaka Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Obayashi conducted Japan’s first on-site proof-of-concept test of a hydrogen fuel-cell powered hydraulic excavator at an active construction site, advancing zero-emission machinery adoption for heavy works.

- January 2026: INPEX and partners commenced commercial operations at the Goto City Offshore Wind Power Project, a 16.8 MW floating offshore wind facility approved by METI, validating deeper-water technology pathways.

- October 2025: Obayashi acquired 100% of GCON Inc., a U.S. contractor focused on data centers and semiconductor-related MEP, expanding its critical-environment footprint.

- September 2025: Daiwa House, through Stanley Martin Homes, acquired Windsor Homes in North Carolina to scale U.S. single-family deliveries beyond 10,000 by 2026.

Japan Construction Market Report Scope

Construction refers to building commercial, institutional, or residential infrastructures like bridges, buildings, roads, and other structures. The different materials used in modern-day construction include clay, stone, timber, brick, concrete, metals, and plastics, among others.

Japan's construction market is segmented by sector (residential, commercial, industrial, infrastructure (transportation), and energy and utilities).

The report offers the market sizes and forecasts in value (USD) for all the above segments. The report also covers the impact of COVID-19 on the market.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Hokkaido |

| Tohoku |

| Kanto (Tokyo) |

| Chubu (Nagoya) |

| Kansai (Osaka) |

| Rest Of Japan |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Hokkaido | |

| Tohoku | ||

| Kanto (Tokyo) | ||

| Chubu (Nagoya) | ||

| Kansai (Osaka) | ||

| Rest Of Japan | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan construction market?

The Japan construction market size was USD 528.41 billion in 2025 and is projected to reach USD 709.00 billion by 2031 at a 5.07% CAGR, supported by resilience programs, renewables, and semiconductor-linked builds.

Which segments are expected to grow fastest in Japan’s construction through 2031?

Infrastructure is the fastest-growing sector at a 6.12% CAGR, renovation leads by construction type at 6.55% CAGR, and modern methods of construction are projected at 7.10% CAGR, supported by policy and productivity needs.

How are government policies affecting the Japan construction market?

Public-works budgets emphasize disaster prevention and resilience, BIM and CIM mandates shape procurement, and 2025 contracting reforms support wage fairness and price adjustments, which stabilize delivery in the Japan construction market.

What is driving regional differences in construction activity across Japan?

Kanto leads due to metropolitan redevelopment, while Hokkaido’s growth is propelled by offshore wind and 300 MW-class data center projects that align with local renewable energy resources .

How are material costs and labor conditions influencing bids and schedules?

Import-driven inflation and a weaker yen increased material and producer prices, while labor unit-price revisions and overtime caps tightened schedules, pushing contractors toward prefabrication and digital delivery.

What technologies are contractors adopting to manage productivity and compliance?

Contractors are scaling BIM content libraries, digital twins for planning, automated lifting coordination, and low-emission equipment trials to raise productivity and meet procurement standards in the Japan construction market.

Page last updated on: