Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

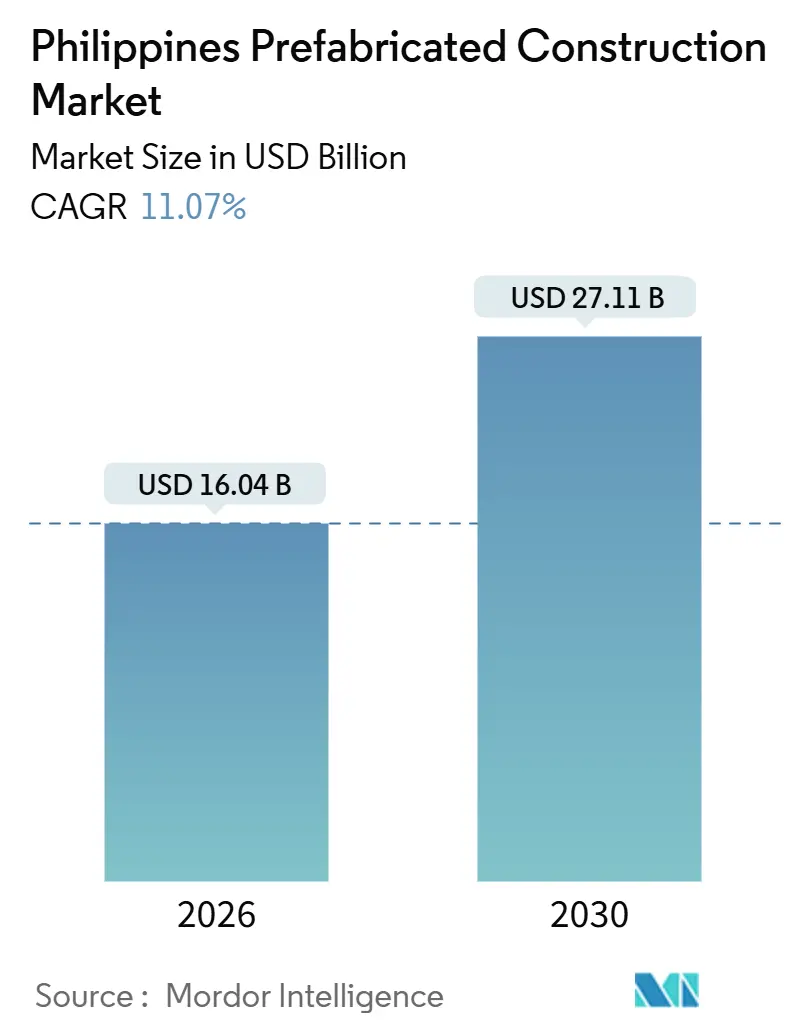

| Market Size (2026) | USD 16.04 Billion |

| Market Size (2031) | USD 27.11 Billion |

| Growth Rate (2026 - 2030) | 11.07% CAGR |

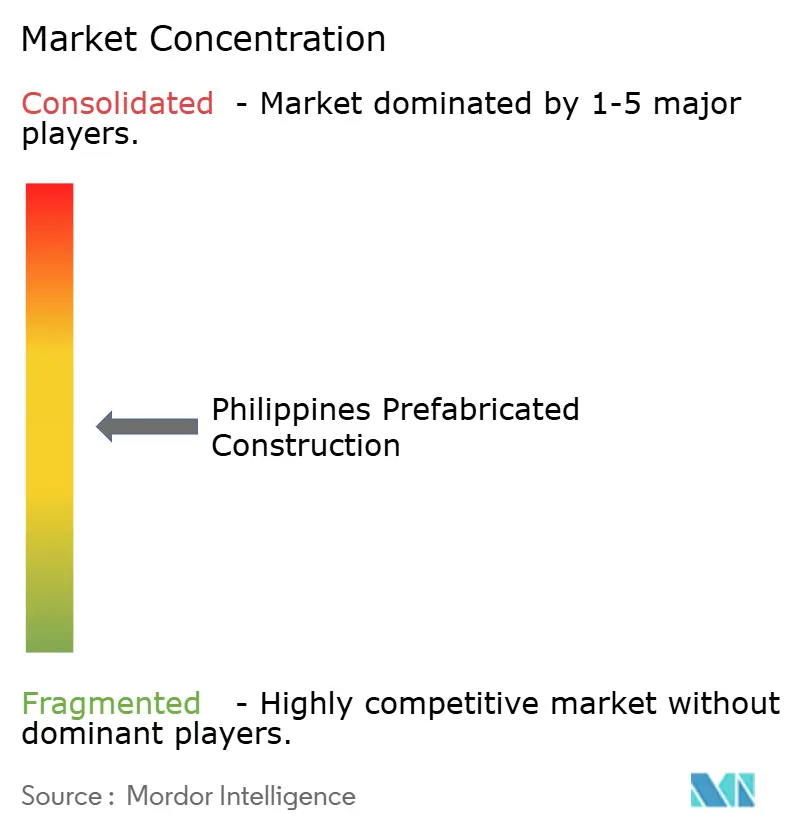

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Prefabricated Construction Market Analysis by Mordor Intelligence

The Philippines Prefabricated Construction Market size is estimated at USD 16.04 billion in 2026, and is expected to reach USD 27.11 billion by 2031, at a CAGR of 11.07% during the forecast period (2026-2031). A USD 44.5 billion public-private-partnership pipeline, a 6.94 million-unit housing shortfall, and a disaster-response framework that pre-qualifies modular suppliers are combining to intensify demand. Archipelago logistics that reward kit-based assembly, plus a tourism-and-BPO expansion that values speed to occupancy over artisanal finishes, further anchor growth. Domestic steel additions of USD 1.5 billion through 2027 aim to shave 15% off structural-frame costs, narrowing the import gap. At the same time, Pag-IBIG’s USD 5.3 billion in 2024 housing-loan releases support entry-level buyers when prefabrication compresses labor hours and material waste. Altogether, these forces keep the Philippines' prefabricated construction market on a double-digit trajectory.

Key Report Takeaways

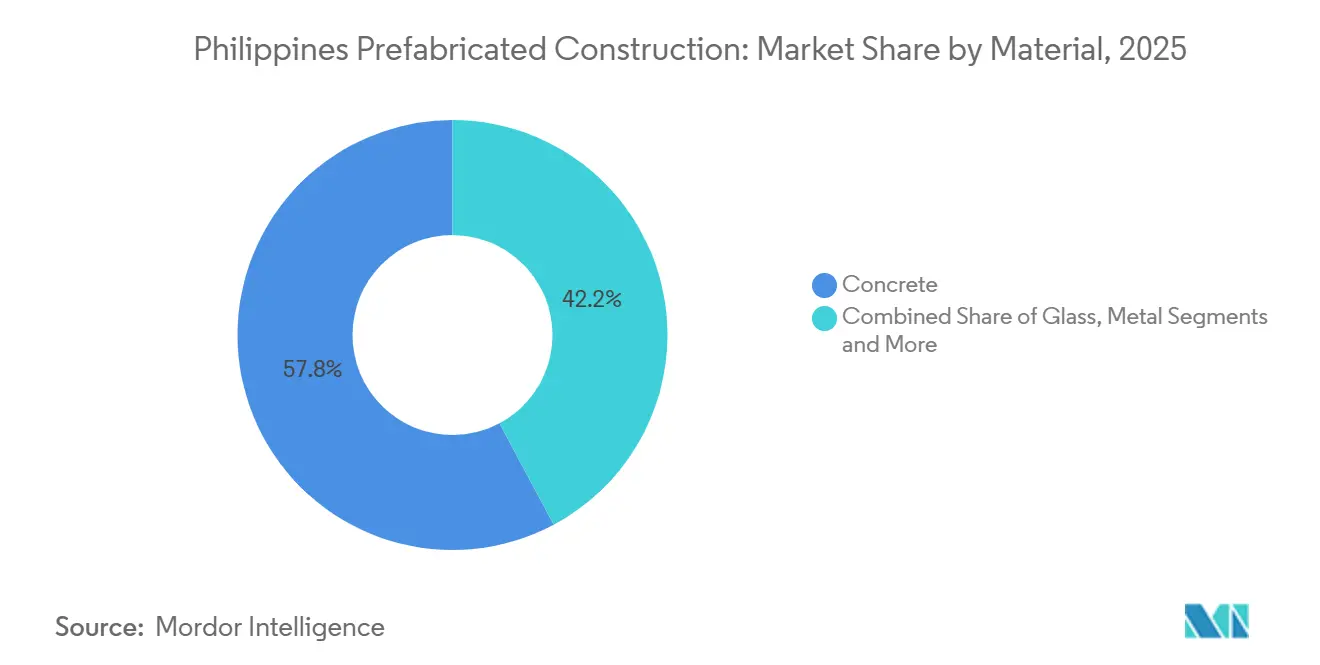

- By material, precast concrete led with 57.8% of the 2025 Philippines prefabricated construction market share, while FSC-certified timber is forecast to post an 11.81% CAGR to 2031.

- By application, residential captured 63.1% of the 2025 value; commercial is set to expand at an 11.71% CAGR through 2031.

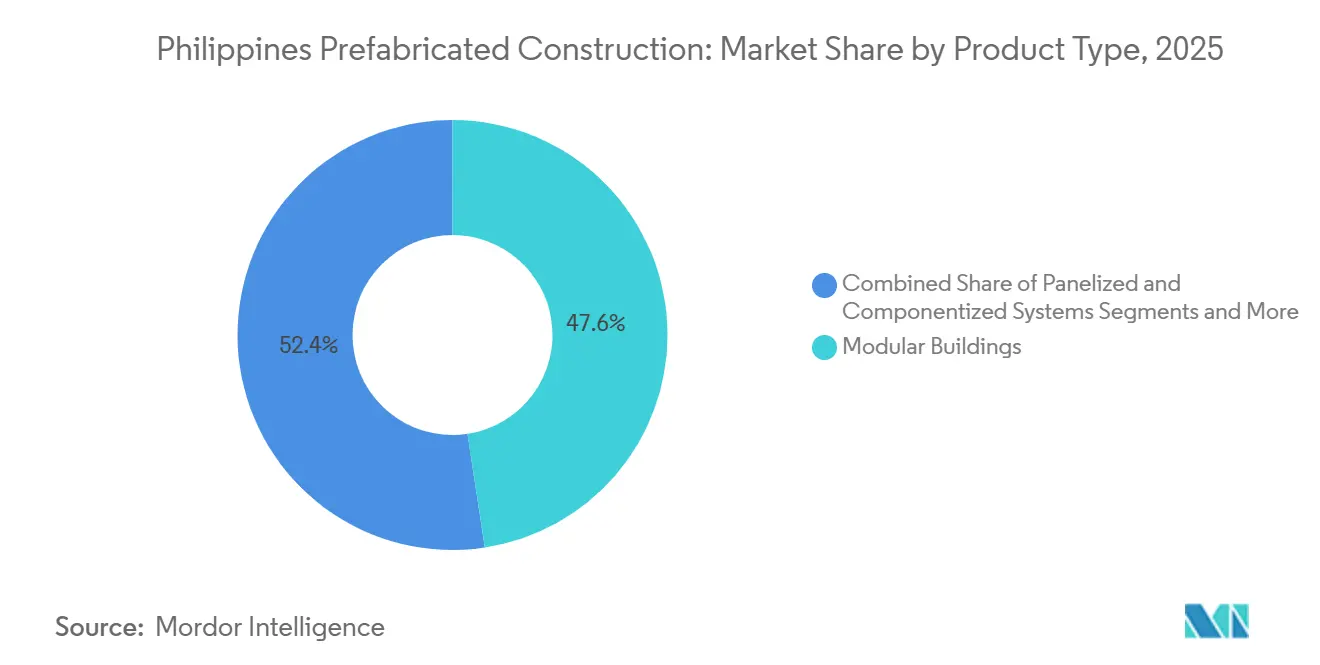

- By product type, modular buildings commanded 47.6% of 2025 revenue and are projected to grow at a 12.41% CAGR to 2031.

- By region, the National Capital Region held 49.1% of 2025 revenues, but the Rest of the Philippines is projected to register a 12.61% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and classroom/clinic backlogs | +2.8% | National, acute in NCR, Calabarzon, Central Luzon | Medium term (2-4 years) |

| Disaster resilience needs (typhoon/quake) | +2.3% | National, the highest in Visayas, Bicol, and Mindanao coastal zones | Short term (≤2 years) |

| Tourism and BPO/industrial growth | +2.1% | NCR, Calabarzon, Clark Freeport, Cebu, Boracay | Medium term (2-4 years) |

| Public programs and PPPs specifying off-site | +1.9% | National, concentrated in Build Better More projects | Medium term (2-4 years) |

| Archipelago logistics benefits | +1.6% | Island provinces, Mindanao, Palawan, Eastern Visayas | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Classroom/Clinic Backlogs Drive Fast, Scalable Delivery

A 6.94 million-unit housing deficit running through 2028 forces local governments to favor solutions that can be finished within one election cycle. Prefabricated packages trim foundation-to-turnover schedules from 18 months to 9 months, aligning ribbon-cutting dates with political calendars. The Department of Education’s 9,000-classroom target for 2024 and the Department of Health’s plan for 700 rural health stations through 2028 both specify repeatable modular designs that can be copied across remote sites without re-engineering. Pag-IBIG’s USD 43,200 average housing loan pushes developers to cut waste and labor costs so homes remain under that threshold. Commercial builders also tap prefabrication to secure Philippine Green Building Code compliance, because factory runs spread certification fees across large volumes.

Disaster Resilience Needs Favor Modular, Code-Compliant Systems

Under Presidential Decree 1096 Chapter 15, prefabricated units must clear third-party tests for wind load and seismic capacity before occupancy permits are issued, giving compliant suppliers an instant go-ahead once a calamity hits. The Post-Disaster Shelter Recovery Framework keeps a roster of firms able to roll out 500 dwellings within 60 days, a capability activated after Typhoon Odette and again in 2024 for Cebu and Leyte. Average typhoon landfalls of 8-10 per year sustain recurring orders for relocatable health-care and classroom modules. The National Structural Code’s 40-millimeter concrete cover and Grade 275 rebar rules are easier to hit in a factory than on a rain-soaked site, so insurers now discount premiums for certified modular assets. Together, these factors steer replacement budgets toward suppliers with documented factory quality logs.

Tourism and BPO/Industrial Growth Support Hotels, Dorms, and Light-Industrial Prefab

PEZA cleared 159 new projects in 2024 worth USD 4.27 billion and will add 14 economic zones in January 2026, each needing dormitories, canteens, and light-assembly buildings that volumetric kits can finish in 12 months instead of the usual 24. The IT-BPM workforce climbed to 1.57 million in 2024 and is tracking a 2 million target by 2028, translating into roughly 400,000 m² of new office and support space every year in cities like Iloilo, Bacolod, and Davao where contractor pools are thin. Tourism adds another pull: 5.45 million arrivals in the first ten months of 2024 support a 12 million-visitor goal for 2028, leaving a 15,000-room gap that developers are filling with modular mid-rises; Hilton Manila Bay and Fairmont Manila both opened in 2025 after precast cores shaved six months off schedule. Radisson RED Cebu and Dusit Thani Mactan Cebu, launched in 2024, relied on bathroom pods and balcony modules to dodge skilled-labor shortages in the Visayas. Clark Freeport’s USD 1.15 billion 2024 inflow, including a USD 91.8 million Korean plant, follows the same pattern—pre-engineered metal frames that hit 18-month commissioning—while Republic Act 7916 adds a 5% gross-income tax and duty-free equipment that make imported prefab even more cost-effective.

Public Programs and PPPs Increasingly Specify Offsite for Speed and Cost Certainty

The USD 44.5 billion PPP roster logged in 2024 gives bid points for methods that guarantee schedule compression and fixed costs, tilting awards toward factory builds. New 4 Pillars Housing rules require that 30% of the one-million-unit target be modular to hit the 2028 deadline. Republic Act 7916 grants PEZA firms duty-free equipment and a 5% gross-income tax, incentives that make imported prefab economical for the 159 projects worth USD 4.3 billion approved in 2024. Build Better More funding at 5-6% of GDP prefers milestone-based contracts and transparent cost curves, both natural fits for factory-made components[2] Department of Public Works and Highways, “National Building Code, Department Order 221 s.2024,” dpwh.gov.ph. Developers such as Ayala Land and Megaworld are locking multiyear output from precast plants, anchoring the volume base needed for specialized lines.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliance on imported materials/systems | -1.4% | National, acute for high-rise and specialty glass | Short term (≤2 years) |

| Fragmented permitting and standards enforcement | -1.1% | Provincial LGUs outside Metro Manila | Medium term (2-4 years) |

| Affordability constraints and limited manufacturing depth | -0.9% | National, sharpest in Mindanao and Eastern Visayas | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Reliance on Imported Materials and Systems Raises Costs and Lead-Time Risk

Philippine builders imported 5.9 million t of steel worth USD 4.2 billion in 2023, exposing project budgets to exchange-rate swings and container delays that can stretch procurement by 8-12 weeks. Although SteelAsia’s USD 1.5 billion plant pipeline will cover H-beams and sheet piles by 2027, niche items such as insulated panel cores and low-e glazing still rely on foreign factories. A pending safeguard investigation on steel dumping could lift duties and squeeze fixed-price contracts. Even ASEAN tariff perks come with logistics lags: pre-engineered kits from Vietnam need 10-14 days at sea plus a week to clear Manila ports, forcing contractors to pad schedules. Lead-time anxiety often keeps developers anchored to conventional methods until financing and permits finish their own slow march[3]Department of Trade and Industry, “Steel Import Statistics 2023,” dti.gov.ph.

Fragmented Permitting and Standards Enforcement Slow Adoption

Building permits rest with 145 cities and 1,488 municipalities, each free to put its own spin on Chapter 15 of the National Building Code. Identical drawings can sit 30-90 days longer in one town than in the neighboring city. Advisory circulars from the National Building Code Development Office are only persuasive, not binding, and the absence of a digital portal forces manufacturers to repeat document kits for every jurisdiction. DPWH Department Order 221 sets uniform concrete rules, yet random site tests occur in fewer than one-third of provincial jobs, eroding the quality edge promised by factory production. Developers also juggle zoning conversions from the Housing and Land Use Regulatory Board, which does not synchronize code enforcement, leaving a maze of local bans on certain claddings or height profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Precast Concrete Anchors, Typhoon Markets, Timber Rides Resort Premiums

Concrete secured 57.8% of the 2025 Philippines prefabricated construction market share. That dominance rests on DPWH rules that specify hollow-core slabs and load-bearing wall panels for disaster housing and public schools. The segment is projected to grow at a 10.9% CAGR through 2031 as SteelAsia’s new mills lower structural steel cost, encouraging hybrid concrete-steel frames that slash import bills by 15%. ISO-certified Frey-Fil’s supply to elevated expressways demonstrates how factory casting guarantees consistent strength even during monsoon months.

Timber starts from a smaller base yet is expected to rise at an 11.81% CAGR, the fastest among materials. Resort developers in Palawan, Boracay, and Siargao pay premiums for Forest Stewardship Council-certified plywood that boosts eco-branding credibility. PERI Philippines, which imports kiln-dried lumber to meet chain-of-custody rules, illustrates how specialty suppliers fill the gap while domestic sawmills catch up. Metal maintains steady demand as Kirby Building Systems exploits ASEAN duty waivers, funneling kits from its 40,000 t per-year Vietnam plant to Mindanao projects where local fabricators remain scarce.

By Application: Socialized Housing Volume Meets BPO Speed-to-Lease Urgency

Residential projects accounted for 63.1% of the 2025 value in the Philippines' prefabricated construction market. The government’s 4 Pillars program aims for 1 million socialized units, and Pag-IBIG’s USD 5.3 billion in 2024 loan releases keep entry-level buyers active. Megaworld’s USD 158 million purchase of a 49% Empire East stake secures a land bank that precast suppliers can serve via multi-year contracts.

Commercial is the fastest-growing application at an 11.71% CAGR to 2031. PEZA cleared USD 4.3 billion in fresh investments during 2024, with many projects insisting on modular offices that reach lease-up in 12 months instead of 24. Ayala Land’s ARCA South Tower 3 and Megaworld’s Iloilo Business Park both switched to panelized envelopes to satisfy BPO tenants demanding quick handover. Light-industrial sheds in new Mindanao economic zones and panelized hotel wings in Cebu further widen the commercial funnel.

By Product Type: Volumetric Modules Bypass Thin Contractor Pools

Modular buildings held 47.6% of 2025 revenues and are predicted to advance at a 12.41% CAGR. Fully finished boxes avoid the multi-trade coordination that often stalls panel jobs in provinces with shallow contractor rosters. DHSUD re-engaged vetted suppliers in 2024 to drop 500-unit shelter batches within 60 days after storms, reinforcing volumetric credibility.

Panelized and component systems, while smaller, still grow at a near 10.5% CAGR, catering to mid-rise formats that seek layout flexibility. Hybrid approaches-site-cast podiums topped by factory frames-remain niche but essential for towers above 10 stories where pure modules struggle with lift shaft alignment or lateral bracing.

Geography Analysis

The National Capital Region captured 49.1% of 2025 receipts, reflecting dense BPO towers, hospitality builds, and mid-rise condos that prioritize nine-month completion targets. Taguig alone logged more than USD 540 million in permit value in early 2024, and partnerships such as Ayala-Mitsubishi’s USD 630 million mixed-use play at Arca South channel steady work to precast yards.

Calabarzon follows as structural-steel capacity rises. SteelAsia’s USD 324 million Lemery upgrade and USD 540 million Candelaria line will anchor H-beam output, trimming freight costs for builders in Batangas and Laguna. Central Luzon benefits from Clark Freeport’s USD 1.15 billion investment inflow, where Korean and Japanese tenants specify pre-engineered metal buildings to hit 18-month commissioning windows.

Outside Luzon, the Rest of the Philippines segment is forecast to clock a 12.61% CAGR, the fastest in the country. Fourteen new economic zones launching in January 2026 highlight Mindanao and Visayas, spurring demand for dormitories and canteens that arrive as flat-packs or volumetric pods. Tourism goals of 12 million international arrivals by 2028 require 15,000 extra hotel keys, steering precast suites toward secondary islands. Kirby Building Systems’ new Davao office positions the firm for industrial sheds tied to these zones.

Competitive Landscape

The Philippines’ prefabricated construction market is moderately concentrated: a handful of leading players—SteelAsia, Kirby Building Systems, Zamil Steel, Frey-Fil, and Megaworld’s precast partners—account for a sizable share of total supply. SteelAsia’s USD 1.5 billion multiyear program to open five mills aims to undercut imports by 15-20% on frame cost, potentially compressing margins for import-dependent rivals.

Kirby Building Systems leverages 0-5% ASEAN tariffs to funnel 40,000 t per year of kits from Vietnam. A Davao branch opened in June 2024, allowing the firm to chase Mindanao agro-industrial parks that local fabricators cannot reach. Zamil Steel’s twin Vietnam hubs ship 8,500 t per month of building frames that enter the Philippines under the same duty edge, allowing head-to-head bids on logistics warehouses and PEZA plants.

Developers also shape competition. Megaworld’s USD 158 million Empire East stake secures a captive residential pipeline, giving its favored precast suppliers visibility on multi-year volumes. Meanwhile, incoming ASEAN suppliers such as Dongguan Toppre or Teak Bali test waters with 10-15% cheaper quotes but face after-sales and brand hurdles, especially where local governments reward track records in typhoon compliance.

Philippines Prefabricated Construction Industry Leaders

iSteel Inc

USG Boral Building products

Frey - Fil Corporation (FFC)

Revolution Precrafted

Smarthouse Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PEZA rolls out 14 new economic zones worth an expected USD 2.7 billion, many sited in Mindanao and Visayas to decentralize industrial growth.

- December 2025: SteelAsia schedules mid-2027 commissioning for its USD 540 million Candelaria plant to manufacture wide-flange beams

- October 2025: DHSUD revises the 4 Pillars Housing guidelines, requiring 30% of the 1 million-unit target to use prefabrication.

- July 2025: Hilton Manila Bay and Fairmont Manila open six months ahead of baseline after adopting precast core-and-shell designs

- June 2024: Kirby Building Systems opens a Davao office to back-stop Mindanao contracts with kits from Vietnam

Philippines Prefabricated Construction Market Report Scope

A prefabricated building is a building or part of a building that has been manufactured in advance and can be easily transported and assembled.

The Philippine's prefabricated buildings market is segmented by material type (concrete, glass, metal, timber, and other material types) and by application (residential, commercial, and other applications). The report offers market size and forecasts for the Philippines prefabricated buildings industry in value (US) for all the above segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Region

| NCR (Metro Manila) |

| Calabarzon |

| Central Luzon |

| Rest of Philippines |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Region | NCR (Metro Manila) |

| Calabarzon | |

| Central Luzon | |

| Rest of Philippines |

Key Questions Answered in the Report

What is the current value of the Philippines' prefabricated construction market?

The market is valued at USD 16.04 billion in 2026 and is projected to reach USD 27.11 billion by 2031.

Which material dominates prefabricated builds in the Philippines?

Precast concrete holds 57.8% of the 2025 market share because it meets wind-load and fire-rating codes.

Why are volumetric modules gaining traction over panelized systems?

Fully finished modules bypass trade-coordination delays in provinces with limited contractor pools, driving a 12.41% CAGR through 2031.

Which region is growing fastest for prefabricated construction?

Mindanao, Visayas, and outer Luzon, collectively labeled “Rest of Philippines,” are forecast to expand at a 12.61% CAGR as 14 new economic zones open.

How will SteelAsia’s capacity additions influence the market?

Five new mills worth USD 1.5 billion are expected to trim structural-steel costs by up to 20%, encouraging hybrid prefabricated frames.

What policy change is propelling prefab adoption in socialized housing?

The 2025 update to the 4 Pillars program mandates that at least 30% of the one-million-unit goal rely on prefabricated or modular systems.

Page last updated on: