Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

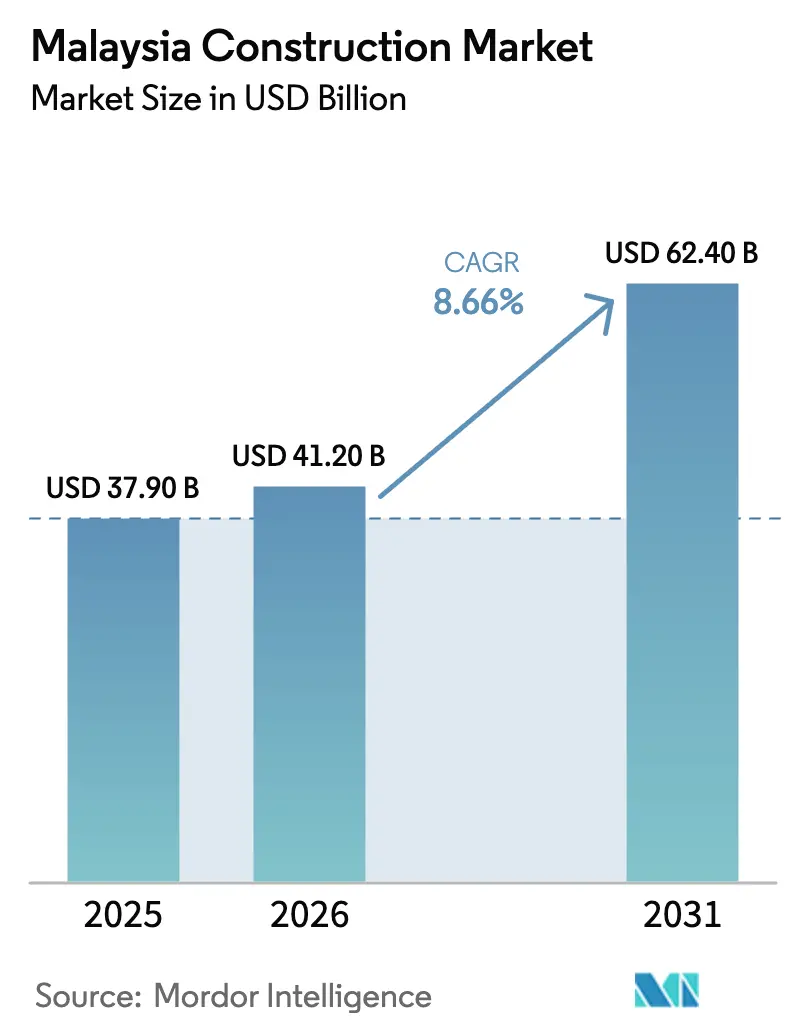

| Base Year Market Size (2025) | USD 37.90 Billion |

| Market Size (2026) | USD 41.20 Billion |

| Market Size (2031) | USD 62.40 Billion |

| Growth Rate (2026 - 2031) | 8.66% CAGR |

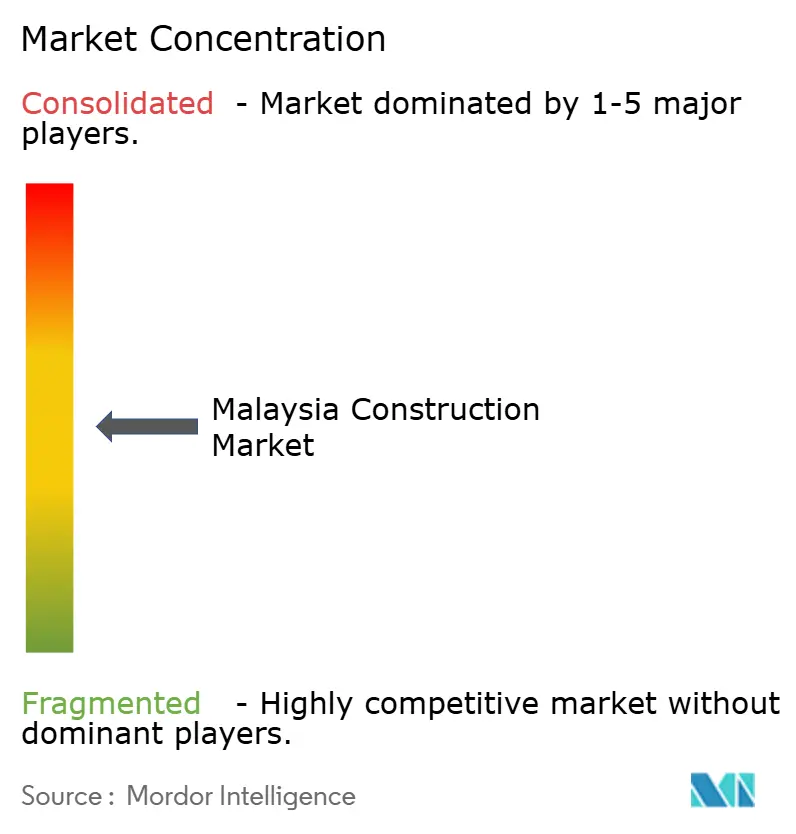

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Construction Market Analysis by Mordor Intelligence

The Malaysia construction market size is valued at USD 41.2 billion in 2026 and is projected to reach USD 62.4 billion by 2031, reflecting an 8.66% CAGR. A pipeline of federally backed mega-projects - led by the East Coast Rail Link nearing 89% completion, the USD 2.9 billion to USD 3.8 billion Penang Light Rail Transit Mutiara Line, and the Pan Borneo Highway Sabah upgrade - anchors long-cycle visibility. Parallel private commitments from Microsoft and Google surpass USD 4 billion for hyperscale data centers, while more than USD 5.5 billion flows into the Johor-Singapore Special Economic Zone (JS-SEZ). These initiatives spur contractors to adopt prefabrication and modular methods, with the aim of reaching 70% penetration in public projects. Momentum is reinforced by Budget 2025’s USD 5.0 billion flood-mitigation envelope, rising foreign direct investment in industrial facilities, and a minimum-wage hike that accelerates mechanization. Against this backdrop, the Malaysia construction market is navigating raw-material price swings, diesel-subsidy phase-outs, and land-acquisition delays, yet overall demand signals remain solid.

Key Report Takeaways

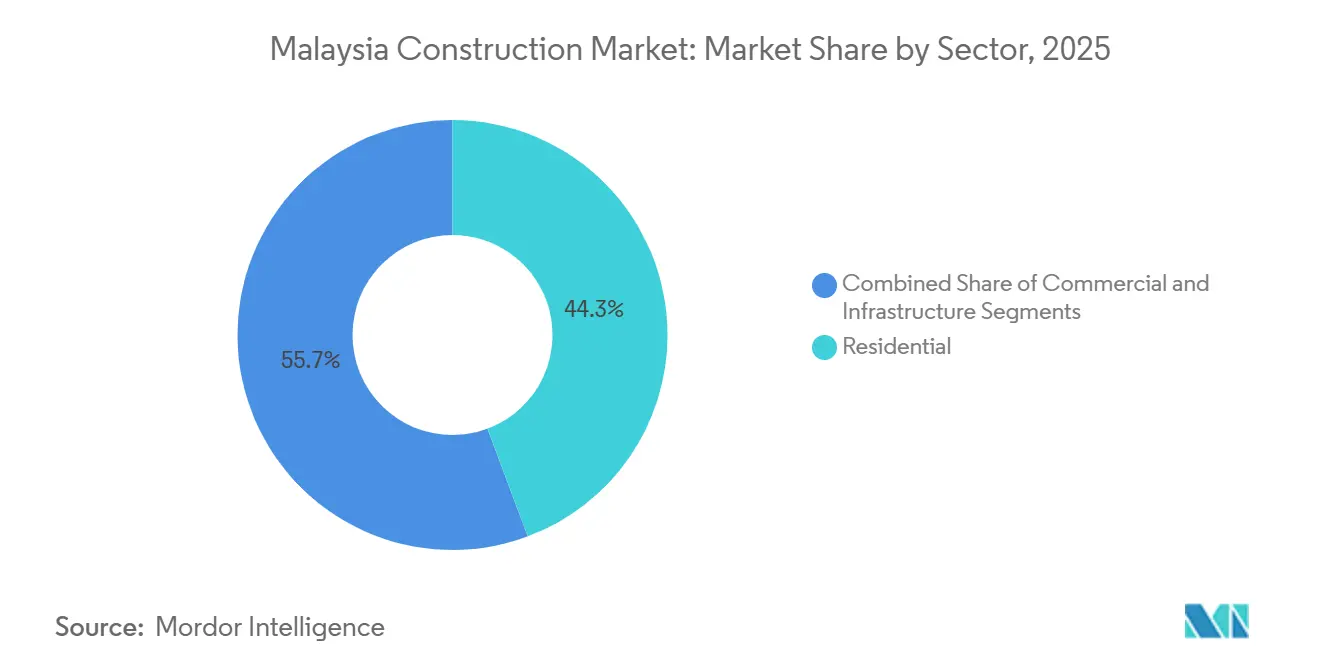

- By sector, residential led with 44.3% revenue share in 2025; infrastructure is advancing at a 9.88% CAGR through 2031

- By construction type, new works accounted for 75.4% of the Malaysia construction market size in 2025, whereas renovation is growing at an 8.10% CAGR to 2031

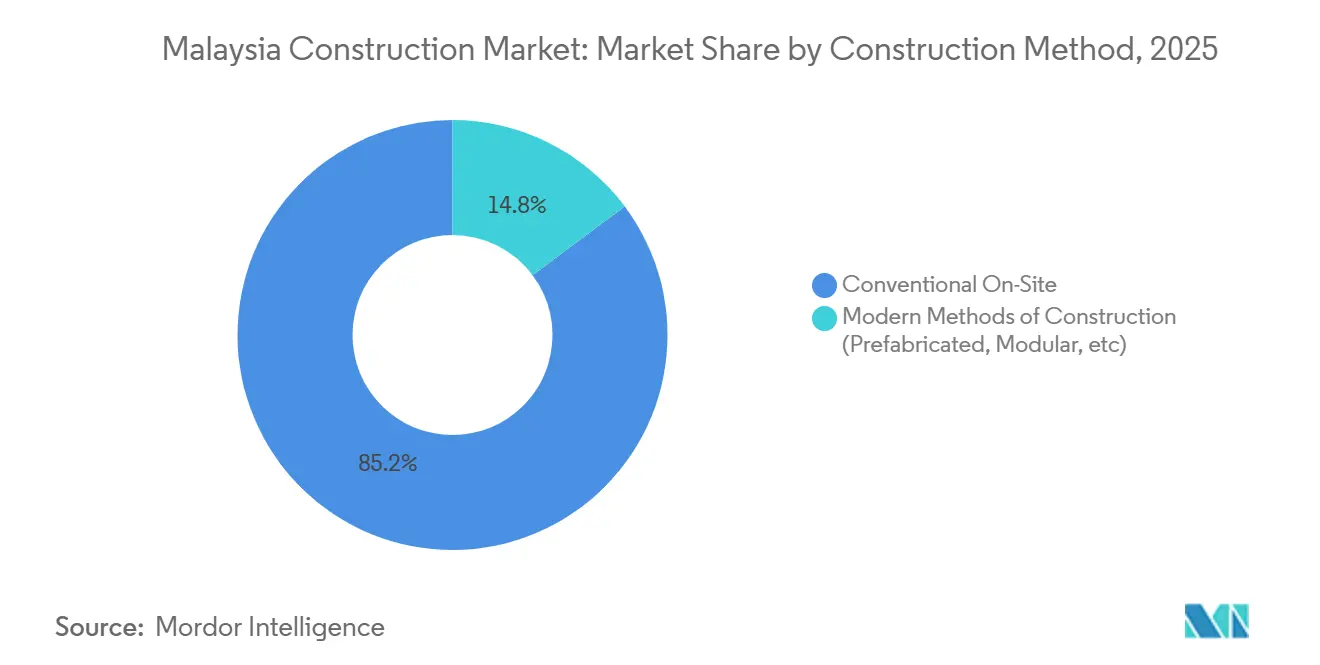

- By construction method, conventional on-site work represented 85.2% of Malaysia's construction market share in 2025; modern methods of construction are rising at an 11.05% CAGR through 2031

- Private investors command 62.2% of Malaysia’s 2025 construction value and will widen their advantage at an 8.99% CAGR through 2031

- By geography, Selangor held 23.5% of Malaysia's construction market share in 2025, while the Rest of Malaysia is expanding at an 11.10% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mega-infrastructure pipeline (ECRL, MRT 3, Pan-Borneo, Penang LRT) | +2.8% | National, with concentration in Pahang, Kelantan, Terengganu (ECRL); Penang (LRT); Sabah, Sarawak (Pan Borneo) | Long term (≥ 4 years) |

| Public-private partnership funding and Budget-2025 flood-mitigation allocations | +1.5% | National, early gains in Selangor, Penang, Johor river-basin zones | Medium term (2-4 years) |

| Surge in FDI-led industrial and logistics facilities | +1.4% | Selangor (Sepang, Shah Alam), Johor (Iskandar Malaysia), Penang (Batu Kawan) | Short term (≤ 2 years) |

| Affordable-housing push for urban middle-income households | +1.2% | Selangor, Wilayah Persekutuan, Johor urban corridors | Medium term (2-4 years) |

| Hyperscale data-centre and 5G infrastructure build-out | +1.0% | Selangor (Cyberjaya, Sepang), Johor (Nusajaya) | Short term (≤ 2 years) |

| Johor-Singapore SEZ catalysing cross-border projects | +0.9% | Johor (Johor Bahru, Iskandar Malaysia), spill-over to southern Pahang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mega-Infrastructure Pipeline (ECRL, MRT 3, Pan-Borneo, Penang LRT)

Flagship rail and highway projects underpin a multiyear civil-works surge. The 665-kilometer East Coast Rail Link targets January 2027 revenue service and already stimulates warehousing around Kuantan Port. The USD 2.9 billion to USD 3.8 billion Penang LRT, awarded in 2024, enters intensive land-acquisition phases that lock in steady subcontracting through 2030. Pan Borneo Highway, Sabah, received a fresh USD 373 million allocation, enabling accelerated earthworks on the 35-kilometer Keningau–Tambunan stretch. Collectively, these corridors shelter infrastructure workloads from cyclical residential swings and justify the segment’s 9.88% CAGR.

Public-Private Partnership Funding and Budget-2025 Flood-Mitigation Allocations

Budget 2025 allocates USD 5.0 billion to flood-control structures, with early packages structured as availability-payment concessions. Private consortia bear construction and 15-year maintenance risk in return for CPI-indexed annuities, drawing in balance-sheet strength from Sunway Construction and WCT Holdings. Procurement for Klang Valley retention basins began in January 2026, and financial close is expected mid-year. Mandatory compliance with ISO 14001 and MSMA design standards raises technical thresholds, favoring incumbents and reinforcing medium-term growth signals.

Affordable-Housing Push for Urban Middle-Income Households

The Rumah Mampu Milik Wilayah program targets 150,000 units priced below USD 67,000, diverting developer focus from luxury condominiums toward compact transit-oriented apartments. Sime Darby Property’s Elmina Valley 2, launched in March 2025, dedicates 40% of its 3,200-unit pipeline to this bracket, using industrialized building systems to cut delivery to 18 months. PR1MA’s restructured tenders in Kuala Lumpur’s Sentul and Cheras corridors hand over the first phases in late-2026, guaranteeing predictable volume but capping gross margins at 12%–15%. Scale efficiency and MMC adoption, therefore, become critical profitability levers.

Surge in FDI-Led Industrial and Logistics Facilities

Manufacturing approvals climbed to USD 73.6 billion in 2024, dominated by electrical and electronics. Infineon’s USD 5.4 billion silicon-carbide wafer plant and BYD’s auto-component campus require a combined 430,000 square meters of built-to-suit space by 2027. JS-SEZ incentives compress permitting to 90 days, drawing DHL and Kuehne+Nagel to pre-lease half a million square meters of grade-A warehouses. Steel-frame and tilt-up contractors such as Kimlun and Gadang therefore enjoy a near-term order-book uplift.[1]https://www.mida.gov.my/mida-news/malaysia-records-highest-ever-fdi-in-2024/

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cement and steel costs | -1.3% | National, acute in Selangor, Johor, Penang, high-activity zones | Short term (≤ 2 years) |

| Skilled-labour shortages and rising wage floor | -1.1% | National, most severe in the Klang Valley and Johor Bahru metro areas | Medium term (2-4 years) |

| Land-acquisition and permitting delays | -0.7% | Penang, Selangor (urban TOD parcels), Sabah/Sarawak (native-title negotiations) | Medium term (2-4 years) |

| Diesel-subsidy rationalisation inflating haulage costs | -0.5% | National, disproportionate impact on rural infrastructure projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages and Rising Wage Floor

CIDB cites a 180,000-worker skilled-trade shortfall against project pipelines through 2028. The February 2025 wage floor moved from USD 337 to USD 382 per month, and foreign-worker levies climbed 15%. These pressures accelerate industrialized building system adoption, cutting on-site labor by 30%–40%. Gamuda’s Sepang precast plant, operating at 85% utilization, demonstrates how capital-intensive off-site fabrication mitigates labor scarcity but widens capability gaps between tier-one and regional players.

Land-Acquisition and Permitting Delays

The Penang LRT alignment still negotiates 42 parcels, pushing final transfers to late-2026 and risking the 2030 opening date. Similar friction at Kwasa Damansara MRT precinct stalled affordable-housing starts by 14 months. Native-title claims added 18 months to Pan Borneo Highway realignments in Sabah. Although early stakeholder engagement can shorten cycles, no comprehensive reform yet guarantees timeline certainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Velocity Outpaces Residential Volume

Residential construction commanded 44.3% of Malaysia construction market share in 2025, reflecting sustained demand from 150,000 planned affordable apartments and private condominium launches. Its growth moderates to about 7.5% CAGR as urban affordability caps expansion. Infrastructure, while smaller, leads future momentum with a 9.88% CAGR on the back of the East Coast Rail Link, Penang LRT, and Pan Borneo Highway. Each megaproject funnels civil packages, precast demand, and specialized MEP opportunities to large contractors. Industrial-and-logistics subsegments ride the USD 73.6 billion FDI wave, accounting for roughly 40% of 2025 commercial activity. Office builds remain tepid amid 18% Kuala Lumpur vacancy, whereas retail pivots toward experiential refurbishments.

Combined, these dynamics illustrate how the Malaysia construction market remains two-speed: large-volume residential keeps laborers engaged, but infrastructure and industrial projects drive higher-margin, technology-intensive work. The interplay shapes materials sourcing—cement and steel weigh heavily in civil jobs—while encouraging contractors to spread risk across sectors. As data-center and grid-reinforcement schedules intensify from 2026 onward, infrastructure revenues will likely surpass residential by early next decade.[2]https://www.nst.com.my/business/insight/2024/01/1004042/madani-framework%C2%A0strategic-action-plans-%C2%A0restructuring-national

By Construction Type: Renovation Gains Momentum

New builds captured 75.4% of 2025 spending in the construction industry in Malaysia, yet renovation is advancing at an 8.10% CAGR as Kuala Lumpur’s average commercial building age reaches 28 years. Energy-efficiency retrofits—exemplified by Sunway Construction’s USD 40 million Menara Sunway upgrade—deliver quick paybacks through energy savings and rental premiums. Suburban malls adopt similar strategies, swapping anchor tenants for dining, entertainment, and fulfillment zones. Government policy amplifies the trend: MGTC now requires Green Building Index certification for federal buildings above 10,000 square meters, offering grants that cover half of incremental retrofit costs.

The construction sector in Malaysia continues to be shaped by new construction, which still dominates because megaprojects, affordable housing, and factory builds involve greenfield civil works. However, land scarcity in urban cores and slower permitting tilt incremental value toward high-spec renovations. Contractors with MEP and facade engineering expertise, such as Kerjaya Prospek and WCT Holdings, increasingly position retrofit divisions to capture this growing slice of the Malaysia construction market.

By Construction Method: Prefabrication Disrupts On-Site Dominance

Conventional methods held 85.2% of Malaysia construction market share in 2025, yet modern methods of construction will expand at an 11.05% CAGR - nearly triple traditional growth. CIDB’s 70% IBS content mandate on public projects compresses schedules 20%–25% and cuts labor 30%–40%. Gamuda’s Sepang facility, running near full tilt at 12,000 cubic meters monthly, supplies MRT 3 and Penang LRT beams and walls. Minimum-wage hikes plus skilled-labor shortages reinforce adoption economics, delivering 15%-20% labor savings despite an 8%-12% premium on precast components.

Modular techniques flourish in worker dorms and affordable apartments; Kimlun’s Johor Bahru project delivered 1,200 modular units six months faster than stick-built approaches. Infrastructure still leans on site-specific casting, but precast bridge segments and tunnel liners are penetrating Pan Borneo and ECRL work scopes. By 2031 IBS and modular could command 25%-30% of Malaysia construction market size, reshaping supply chains and contractor qualification norms.[3]https://theedgemalaysia.com/

By Investment Source: Private Capital Sustains Momentum

Private players generated 62.2% of 2025 activity and will grow at an 8.99% CAGR, edging out public outlays. Sime Darby Property’s USD 268 million Elmina Valley 2 and YTL-Nvidia’s USD 500 million edge-data-center JV illustrate how presales and private equity accelerate projects unhindered by fiscal ceilings. Public expenditure remains critical for high-capex undertakings such as the USD 9.8 billion ECRL and USD 5.0 billion flood-mitigation plan, but spending is lumpy and exposed to budget cycles.

Hybrid PPP structures blur lines: twelve flood-control contracts bundle private financing with 15-year annuity streams from the federal treasury, combining efficiency with sovereign credit. Consequently, the Malaysia construction industry continues to rely on private agility for quick-turn housing and industrial jobs, while public-sector megaprojects deliver durable base-load demand.

Geography Analysis

Selangor generated 23.50% of 2025 construction value, buoyed by USD 4 billion in hyperscale data centers, middle-income housing around Setia Alam, and USD 491 million in flood-mitigation basins. Its growth moderates to roughly 8.0% CAGR as industrial land tightens and developers scout cheaper corridors in Nilai and Bangi. Johor’s trajectory accelerates under the JS-SEZ; UEM Sunrise’s Gerbang Nusajaya already pre-leased 60% of phase-one plots, while logistics giants DHL and Kuehne+Nagel secure 500,000 square meters of warehouses for 2027 delivery. Affordable apartments in Johor Bahru complement luxury villas catering to Singaporean buyers, making the state the fastest-growing peninsular market.

Federal Territory activity centers on transit-oriented developments like Kwasa Damansara and green retrofits such as the Menara Sunway overhaul, yet office oversupply limits new high-rise starts, holding growth near 7.2% CAGR. Elsewhere, the Rest of Malaysia segment—Sabah, Sarawak, Penang, Pahang—advances at an 11.10% CAGR, propelled by the USD 373 million Pan Borneo Highway segment, the USD 3.8 billion Penang LRT, and USD 179 million warehouse clusters near Kuantan Port. Native-title negotiations and rugged terrain raise execution risk in East Malaysia, but budget allocations continue to flow as part of inclusive development priorities.

Regulatory Landscape

Malaysia's construction sector is primarily governed by the Construction Industry Development Board (CIDB), established under Act 520. The framework requires registration for local and foreign contractors and classifies firms from G1 to G7 by tender capacity. CIDB also administers quality and safety assessment frameworks such as QLASSIC and SHASSIC (aligned to Malaysian Construction Industry Standards) and manages construction product and material compliance via the Certification of Construction Product and Material (CCPM) listing for prescribed items.

Regulatory emphasis has shifted toward design-led safety management and measurable quality outcomes. The Occupational Safety and Health (Construction Work) (Design and Management) Regulations 2024 came into operation on 1 June 2024, setting out explicit pre-construction and construction-stage duties for designers and contractors. In February 2026, the Ministry of Works launched the Construction Action Plan 2030 (CAP30) as a five-year roadmap under the National Construction Policy (NCP) 2030, linking sector execution to targets such as 100% compliance with construction design management standards, higher QLASSIC/SHASSIC performance benchmarks, and wider green certification requirements for larger building projects.

Value Chain Analysis

Malaysia's construction value chain runs from project origination (federal and state ministries and agencies, local authorities, and private developers) through funding structures (public budgets, PPP concessions, and private capital), into design and procurement (architects, engineers, quantity surveyors), main contracting, specialist subcontractors (civil, MEP, facade, foundations), and building materials and equipment suppliers. Oversight and professional gatekeeping are shared across bodies such as the Ministry of Works and CIDB, alongside professional boards including the Board of Engineers Malaysia (BEM), Board of Architects Malaysia (LAM), and the Board of Quantity Surveyors Malaysia (BQSM). Infrastructure delivery interfaces with agencies such as the Malaysian Highway Authority (LLM).

Operating conditions show the chain scaling while adapting to productivity and labor constraints. The value of construction work rose to RM158.8 billion in 2024 and reached RM178.6 billion in 2025, and the sector had about 1.1 million registered personnel as of December 2024. Policy programs including the Construction 4.0 Strategic Plan (2021-2025) and the NCP 2030 push digital workflows and industrialization, increasing the role of IBS or precast manufacturers, BIM-enabled consultancies, and equipment rental and automation providers. At the same time, compliance expectations around quality, safety, and sustainable construction delivery are tightening.

Competitive Landscape

The Malaysia construction industry competition is moderately fragmented: the top five firms—Gamuda, IJM, Sunway, MRCB, UEM Sunrise—control under one-third of Malaysia construction market share, leaving ample scope for regional specialists. Tier-one players reinforce vertical integration by investing in precast plants, BIM platforms, and MEP subsidiaries; Gamuda’s BIM on MRT 3 trimmed design clashes 40% and shaved six weeks off coordination. Mid-tier contractors such as Kerjaya Prospek and Econpile focus on high-margin niches—facades and foundations—to dodge head-to-head confrontations on megaproject bids.

Foreign entrants add external pressure. China Communications Construction dominates ECRL civil works, while several Singaporean groups eye JS-SEZ industrial parcels, injecting advanced quality benchmarks. Regulatory levers are light—CIDB grade classifications govern eligibility, but enforcement varies by state, so technology becomes the main differentiator. IBS mandates make in-house precast a prerequisite for public tenders, nudging smaller companies toward consortium models that compress margin yet broaden capability.

Green retrofits, modular housing, and rural infrastructure appear as white spaces. Fewer than 15% of Kuala Lumpur’s legacy towers have pursued deep energy renovations despite MGTC grants. Early movers exploiting this gap could lock in multi-year revenue while honing ESG credentials. Consolidation is likely as capital-light regional firms seek partners with IBS capacity; acquisitions may accelerate once MMC adoption crosses the 25% threshold around 2031, reshaping competitive contours.

Malaysia Construction Industry Leaders

Gamuda Berhad

IJM Corporation Berhad

YTL Corporation Berhad

UEM Group Berhad

Malaysian Resources Corporation Berhad (MRCB)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-linked compliance and industrialization are creating clear white spaces for contractors, consultants, and suppliers that can deliver measurable quality, safety, and sustainability outcomes. The February 2026 launch of CAP30 as a five-year roadmap under NCP 2030 elevates demand for capabilities tied to construction design management compliance, QLASSIC/SHASSIC performance improvement, and green certification delivery on larger projects, favoring firms with robust QA/QC systems, digital site management, and ESG-ready design and MEP packages.

PPP structuring and industrial-driven facility builds broaden addressable demand beyond traditional public works. CIDB-reported main contractor contract awards totaled RM85.4 billion in the first five months of 2026, pointing to active tendering for qualified players across civil, rail, and utilities packages. In-scope pipelines and programs, including the Johor-Singapore SEZ industrial build-out, federally backed flood-mitigation packages, and hyperscale data center investments, support opportunities for fast-track industrial and logistics construction, high-spec MEP and power distribution works, and more standardized worker-accommodation and modular solutions where compliance requirements and delivery speed are key differentiators.

Recent Industry Developments

- July 2026: Hartanah Kenyalang Berhad, via Hartanah Construction Sdn Bhd, secured a contract from JKR Sarawak to build Wisma JKR Sarawak in Kuching. The award reinforces the visibility of public-sector building demand in East Malaysia and supports a steadier pipeline for local contractors and supply networks tied to government facilities.

- May 2026: Gamuda Berhad announced its joint venture secured the Kaohsiung Metropolitan MRT Xiaogang-Linyuan Line in Taiwan. The deal strengthens Gamuda's regional rail credentials and adds external order-book diversification that can support technology transfer and procurement scale for complex urban transit works.

- October 2024: A Gamuda-led consortium secured the Penang LRT Mutiara Line contract. It advances multi-year rail civil and systems works in Penang and accelerates demand for precast, MEP, and specialist subcontracting aligned with Malaysia's push toward industrialized construction methods.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Malaysia construction market is defined as the value of construction activity tied to delivering buildings and civil infrastructure. This includes project planning and design through construction, and it also covers repair and maintenance, upgrades, and eventual decommissioning where it is part of construction work.

Scope exclusions: Real estate transactions and pure property ownership income are not counted unless they directly relate to construction services and project execution.

Segmentation Overview

- By Sector

- Residential

- Apartments / Condominiums

- Villas / Landed Houses

- Commercial

- Office

- Retail

- Industrial & Logistics

- Others

- Infrastructure

- Transportation Infrastructure

- Roadways

- Railways

- Airways

- Others

- Energy & Utilities

- Others

- Transportation Infrastructure

- Residential

- By Construction Type

- New Construction

- Renovation

- By Construction Method

- Conventional On-Site

- Modern Methods of Construction

- By Investment Source

- Public

- Private

- By Geography

- Selangor

- Johor

- Wilayah Persekutuan

- Rest of Malaysia

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public construction output and macro series so our assumptions sit on a realistic national activity baseline. We typically rely on sources such as the Department of Statistics Malaysia for sector value added and activity signals, Bank Negara Malaysia for credit and rate direction, and Ministry of Finance budget documents for public development allocations.

To ground the demand pipeline, we also review materials from agencies and bodies such as CIDB Malaysia for industry outlook views, the Economic Planning Unit for plan priorities, and procurement and tender notices that indicate timing and project readiness. Company annual reports, investor presentations, and reputable business press are used to understand order books and execution pace, and subscription financial datasets plus an import-export shipment level database are used selectively when we need to cross check revenue exposure and materials movement. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification during research.

Primary Interviews and Surveys

Primary work is used to confirm what is really getting built, what is being delayed, and how costs are moving across residential, commercial, industrial, and infrastructure projects. We spoke with a mix of contractors, project consultants, materials and equipment stakeholders, and institutional participants across Malaysia so the model could be adjusted for tender conversion, execution constraints, and price pass through.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | |

| Mid tier: 45% | Functional/Unit leaders: 36% | |

| Smaller Players: 18% | Managers: 47% |

Market-Sizing & Forecasting

Sizing is built mainly through a top-down approach, where Malaysia construction activity is reconstructed using national indicators and then allocated across major work types. Inputs that matter here include public development spending direction, tender announcements and award momentum, visibility into the large-project pipeline, building materials price movement (as a proxy for cost inflation), and financing conditions that influence private starts.

Those totals are then cross checked with selective bottom-up approximations, such as sampled contractor revenue exposure to Malaysia work, channel checks on typical project ticket sizes, and value per square meter or per kilometer benchmarks for common build categories. When a bottom-up view is incomplete, gaps are handled by using execution rates and typical subcontracting splits discussed in interviews, and then the results are adjusted back to align with the top-down control totals.

For forecasting, we mainly use scenario analysis supported by simple multivariate regression checks, where project starts and award conversion are linked to budget cycles, private investment tone, and construction cost inflation. In years where policy or mega project timing shifts, assumptions are refreshed and re-validated with local experts before the forecast is finalized.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers do not move only because one data series changes. We compare the modeled market value against independent signals like construction value added trend direction, tender award pace, and observed cost inflation, then we review large variances to confirm whether they are real shifts or data timing effects.

If an anomaly is found, the assumptions are re-opened and respondents may be re-contacted to confirm what changed on the ground, such as project delays, scope reductions, or faster execution. Each report goes through step-by-step analyst reviews before sign-off, and it is refreshed annually, with interim updates when material events occur. Before delivery, a fresh pass is completed so clients receive the most up to date view available at that time.

Mordor Intelligence's Malaysia Construction Market Size Versus Other Published Estimates

It is normal to see different market sizes for Malaysia construction because publishers do not always count the same work scope, the same year timing, or the same treatment of renovations versus new builds. Differences also come from how firms translate local currency activity into USD and whether their forecast assumes steady execution or a faster mega project ramp.

By tracking award momentum, materials cost inflation, and execution pace through primary checks, Mordor Intelligence anchors the 2025 value to construction activity that is actually delivered, instead of widening the scope into adjacent real estate income or counting early pipeline at full value. When estimates lean higher, it is often because more categories like broad property related services are bundled in, or because aggressive timing is applied to large infrastructure programs. When estimates lean lower, it is commonly tied to narrower coverage that focuses on selected subsectors or uses conservative conversion from announced pipeline to realized work.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 37.90 B (2025) | |

| Industry Association A | USD 41.85 B (2025) | The estimate appears to use a broader view of construction market value in 2025 without clearly separating delivered work from early stage pipeline, and scope notes on inclusions like maintenance or decommissioning are not explicit in the published summary. |

| Trade Journal B | USD 83.40 B (2025) | This figure is presented as a construction output number in MYR converted to USD and can reflect a different measurement basis (real terms output or total spending), which can inflate the USD value when compared with a market value definition tied to delivered construction activity. |

The spread is mainly explained by boundary choices and timing, especially around how pipeline is treated and how currency conversion is applied. Our approach stays repeatable because each step is tied to observable indicators and then pressure tested with interviews, which keeps the final total aligned with what is executed in Malaysia during the year.

Key Questions Answered in the Report

How large is the Malaysia construction market in 2026?

The Malaysia construction market size stands at USD 41.2 billion in 2026 with an 8.66% CAGR outlook to 2031.

Which sector is growing fastest?

Infrastructure shows the highest velocity, set to expand at a 9.88% CAGR thanks to rail, highway, and grid projects.

Why are modern methods of construction gaining share?

Wage hikes, skilled-labor shortages, and CIDB’s 70% IBS mandate make prefabrication 15%–20% cheaper on labor and 20% faster on schedules.

What role does the Johor-Singapore SEZ play?

The SEZ streamlines customs and standards, unlocking USD 5.5 billion in early commitments and driving rapid industrial build-out in Johor.

How are material-price swings affecting contractors?

Cement and steel volatility trimmed margins by up to 280 basis points for firms on fixed-price contracts, pushing demand for escalation clauses and hedging.

Which companies hold the most market share?

Gamuda, IJM, Sunway, MRCB, and UEM Sunrise collectively account for about 30% of contract value, leaving a sizable share to regional players.

Page last updated on: