Russia Construction Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

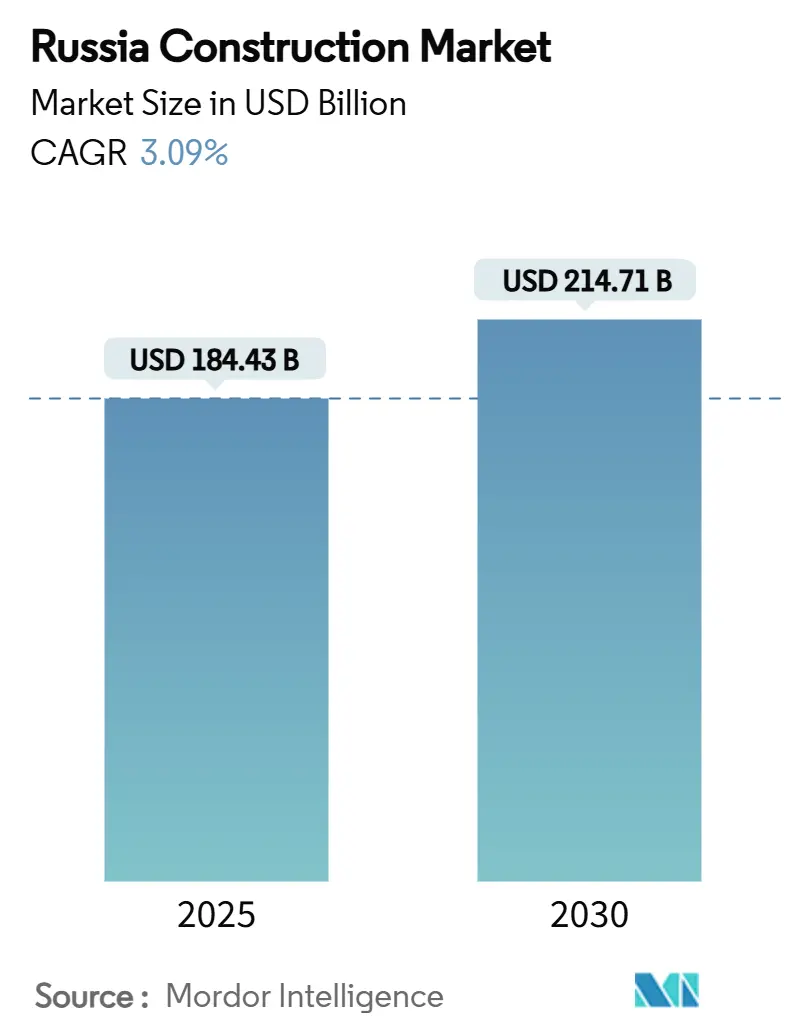

| Market Size (2025) | USD 184.43 Billion |

| Market Size (2030) | USD 214.71 Billion |

| Growth Rate (2025 - 2030) | 3.09% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Construction Market Analysis by Mordor Intelligence

The Russia construction market size stands at USD 184.43 billion in 2025 and is forecast to reach USD 214.71 billion by 2030, translating into a 3.09% CAGR over the period. Resilient public infrastructure spending, a pivot toward domestic supply chains, and reconstruction mandates in newly integrated territories keep the growth trajectory stable, even as sanctions restrict Western inputs. Mortgage rates at 30% dampen urban apartment demand, yet record individual housing completions and USD 285.6 billion in national-project funding underpin steady residential activity. Rapid industrial and logistics expansion tied to import substitution adds a fresh layer of demand, while labor shortages foster experimentation with prefabricated methods. Finally, the USD 11.1 billion-a-year rebuilding program in war-affected zones offers a counter-cyclical buffer.

Key Report Takeaways

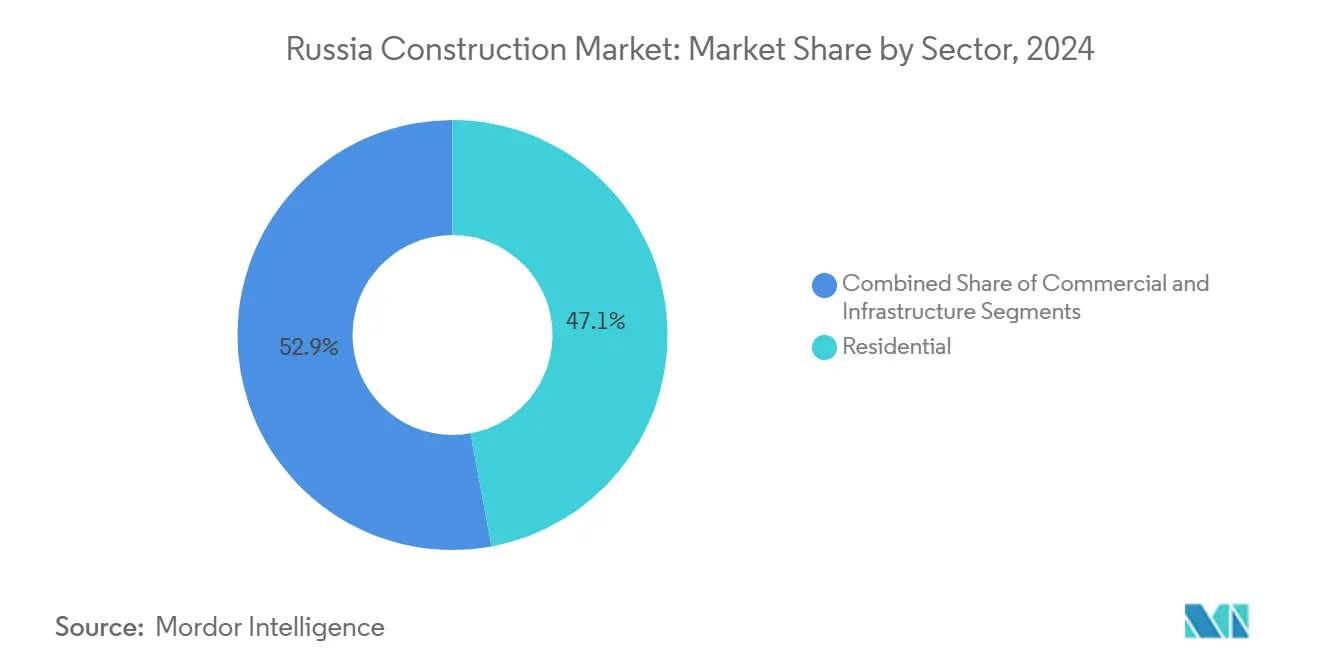

- By sector, residential construction held 47.1% of the Russia construction market share in 2024, while commercial construction is projected to expand at a 4.23% CAGR through 2030.

- By construction type, new builds accounted for 67.7% of the Russia construction market size in 2024, whereas renovation is advancing at a 3.91% CAGR to 2030.

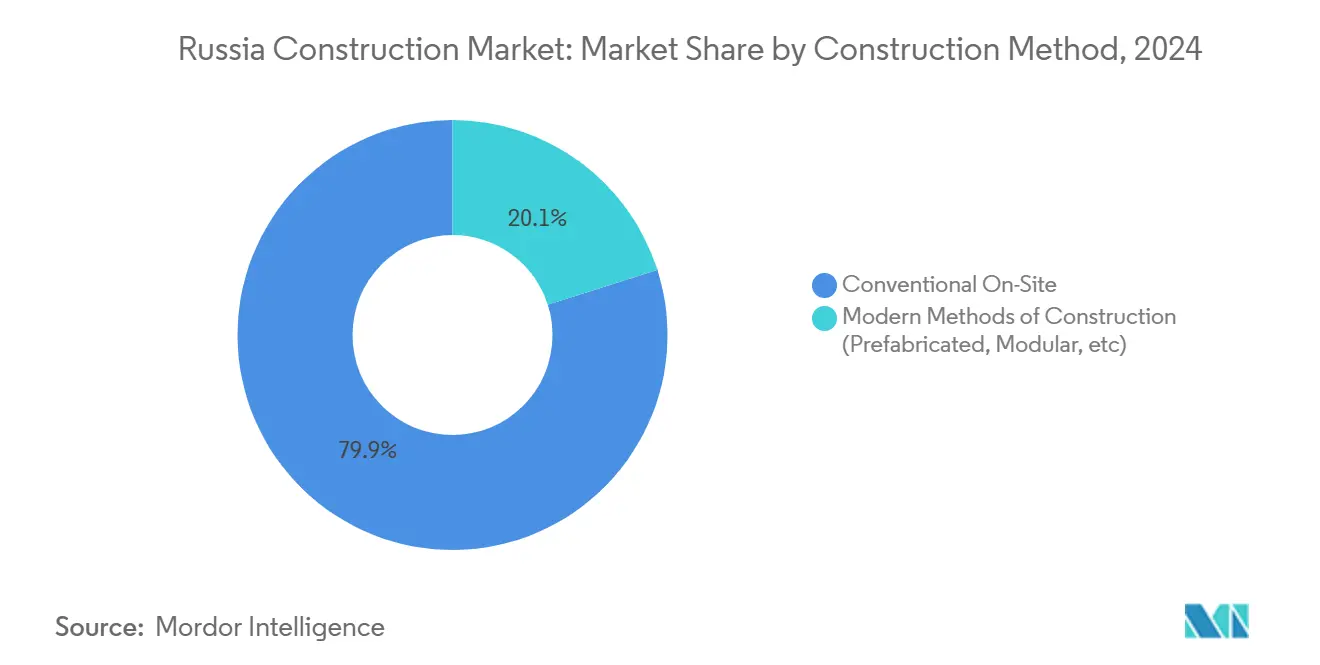

- By construction method, conventional on-site work commanded a 79.9% share in 2024; modern methods such as prefabrication are set to grow at a 4.11% CAGR.

- By investment source, private capital supplied 61.2% of 2024 spending, but public outlays are growing faster at a 3.67% CAGR on the back of national projects.

- By geography, the Central Federal District held 31.2% of the Russia construction market share in 2024, while the North-Western Federal District is projected to grow at a 4.47% CAGR through 2030.

Russia Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in public infrastructure investments | +0.9% | Central Federal District & major metros | Medium term (2-4 years) |

| Government housing initiatives and demand stimulus | +0.8% | Nationwide, focus on regional centers | Long term (≥ 4 years) |

| Economic reorientation fueling industrial & logistics construction | +0.6% | Volga & Southern districts | Medium term (2-4 years) |

| “Friendly” foreign partnerships and capital inflows | +0.5% | Nationwide strategic projects | Long term (≥ 4 years) |

| Modernization of aging infrastructure and housing stock | +0.3% | Central & North-Western districts | Long term (≥ 4 years) |

| Reconstruction in war-affected territories | +0.2% | Southern district & annexed areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Public Infrastructure Investments

Russia's commitment to enhancing its public infrastructure is evident through its ambitious funding initiatives. With a national-project funding commitment of USD 285.6 billion through 2030, the country is laying the groundwork for an expansive array of highways, metro extensions, and utility projects. Programs like “Infrastructure for Life” and “Effective Transport System” not only provide contractors with a clear, multi-year order visibility but also ensure smoother cash flows and incentivize capacity upgrades. Import-substitution rules favoring local inputs give a leg up to domestic suppliers of cement, steel, and equipment. The Leningrad-7 nuclear unit's early progress—two and a half months ahead of schedule—demonstrates the sector's adeptness at navigating complex tasks, even amidst sanctions. Ongoing federal support acts as a buffer, shielding the Russian construction market from immediate macroeconomic jolts. These developments underscore the resilience and forward momentum of Russia's infrastructure sector.

Government Housing Initiatives and Demand Stimulus

Addressing housing challenges remains a priority for the Russian government as it seeks to balance affordability and regional disparities. Facing record-low birth rates and regional housing shortages, the government has rolled out measures like DOM.RF loan subsidies and relaxed sanitary codes for schools. In 2024, individual housing starts reached 62 million m², counterbalancing a dip in high-rise sales driven by mortgage challenges. Extended deadlines for social facility completions shield contractors from penalties, and housing grants in the Arctic zone diversify activity beyond just Moscow and St. Petersburg. This comprehensive approach addresses both affordability and regional disparities, establishing a robust demand foundation for residential builders. Even with elevated rates, increased subsidies are poised to energize the Russian construction market. These initiatives reflect the government's commitment to fostering a sustainable and inclusive housing ecosystem.

Economic Reorientation Fueling Industrial & Logistics Construction

Russia's economic reorientation is driving significant growth in industrial and logistics construction. As firms pivot to localize manufacturing due to import-substitution policies, there's a surge in demand for factory shells, worker housing, and distribution centers. A case in point is the USD 50 million tractor plant in Vladimir, showcasing mid-sized industrial projects catering to domestic requirements. With Asian trade corridors expanding, warehouse construction is on the rise, and occupiers are leaning towards ownership over leasing as a hedge against currency fluctuations. This landscape allows industrial EPC specialists to carve out a larger share in the Russian construction market, while generalists are branching into logistics fit-outs, diversifying their portfolios, and softening the impact of residential slowdowns. These shifts highlight the adaptability and growth potential of the industrial and logistics construction segment.

“Friendly” Foreign Partnerships and Capital Inflows

International collaboration is playing a pivotal role in shaping Russia's construction landscape. Chinese and Indian financiers are stepping in where European banks once dominated, channeling both capital and technology into Russia's transport and energy megaprojects. A notable instance is a Russian developer collaborating with an Indonesian consortium, which boasts a hefty USD 22.2 billion in pledged funds. These cross-border joint ventures not only enhance local firms' BIM tools and modular capabilities but also prime them for intricate domestic and international contracts. Such collaborations not only trim financing expenses but also infuse innovation, bolstering the long-term trajectory of the Russian construction market. These partnerships underscore the importance of global cooperation in driving sustainable growth.

Restraints Impact Analysis*

| Restraints | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages and Demographic Pressures | -1.2% | National, with acute impact in Central and North-Western Federal Districts | Long term (≥ 4 years) |

| High Material Costs and Construction Price Inflation | -0.9% | National, with regional variations based on transport costs and supply chain access | Medium term (2-4 years) |

| Impact of Sanctions on Equipment and Supplies | -0.6% | National, with severe impact on specialized equipment and Western technology-dependent projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Demographic Pressures

The Russian construction market is facing significant challenges due to labor shortages and demographic shifts. By 2030, the industry is expected to encounter a shortfall of 11 million workers, driven by declining birth rates, which have dropped to 1.22 million, and the migration of skilled laborers to higher-wage markets. In Moscow, wage inflation and project delays are already evident in high-rise construction projects. To address volume demands, the industry increasingly relies on migrant workers, but this approach escalates costs associated with language barriers and training. While automation and prefabrication are gaining traction, smaller firms struggle with the high upfront capital expenditure required for these technologies. Without a substantial improvement in productivity, the labor shortage could severely constrain the achievable output of Russia's construction market over the next decade. Addressing these challenges will be critical to sustaining the market's growth and meeting future demands[1]Ministry of Labour and Social Protection, "Labour Market Demographics Report 2024," mintrud.gov.ru.

High Material Costs and Construction Price Inflation

The construction market in Russia is also grappling with elevated material costs and persistent price inflation. Despite the stability of the ruble, prices for essential materials such as rebar, glass, and lumber remain high due to energy price increases, logistical disruptions, and sanctions on specialty inputs. Domestic mills have reported an 11% decline in output as export channels diminish, forcing builders to pay premiums for substitute grades. Parallel imports have alleviated some shortages but have introduced additional freight and compliance costs. To mitigate currency fluctuations, contractors are now hedging their quotes in USD, which complicates the tendering process. These sustained high input costs are compressing profit margins and could deter private investment, potentially slowing the expansion of Russia's construction market. Proactive measures will be essential to address these cost pressures and ensure the market's resilience in the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Dominance Amid Commercial Upswing

Residential work captured 47.1% of 2024 spending, making it the clear anchor of the Russia construction market share. Mortgage constraints have shifted households toward self-built homes, pushing individual housing completions to a record 62 million m². Developers are substituting smaller apartments and co-living formats for stalled premium condos. Commercial builds are climbing at a 4.23% CAGR through 2030 on the back of warehouse demand tied to Asia-oriented logistics corridors. Retail footprints shrink, but data-center and cold-storage projects help offset, diversifying revenue streams for general contractors.

The Russia construction market size for commercial assets is forecast to swell as manufacturers localize production and occupy purpose-built plants. LSR Group has already pivoted 15% of its pipeline toward light-industrial sheds, while PIK Group leverages its design team to offer turn-key office-plus-factory campuses. Such strategic refocusing keeps overall sector activity balanced even when urban apartment sales slow.

By Construction Type: New Builds Lead but Renovation Accelerates

In 2024, ongoing investments in greenfield factories, highway infrastructure, and high-rise urban developments propelled new construction to account for 67.7% of total spending. Yet, the renovation segment is on the rise, expanding at a CAGR of 3.91%. This growth is largely due to regulatory mandates pushing for utility system upgrades and elevator replacements. Contractors focusing on façade overcladding, HVAC retrofits, and energy-efficient glazing are now enjoying premium daily rates. As capital construction registries start releasing phased funding tranches, the renovation-driven share of Russia’s construction market is poised for further growth, allowing for a more balanced distribution of project workloads throughout the year.

Renovation’s appeal also lies in lower permitting hurdles and shorter paybacks for landlords facing high vacancy rates. Government co-financing of elevator swaps covers up to 50% of costs, lifting take-up among HOA-run apartment blocks. As cost-inflated new builds struggle to hit presales thresholds, retrofit-heavy portfolios provide a cushion, reinforcing sector resilience[2]Association of Construction Materials Producers, "Industrial Construction Demand Analysis," stroymaterialy.ru.

By Construction Method: Conventional Dominance with Modern Acceleration

Conventional on-site techniques still represent 79.9% of the Russia construction market share. Brick-and-block masonry remains cheap and familiar, especially outside Moscow. Yet modern methods are expanding at a 4.11% CAGR due to labor shortages and stricter quality norms. Prefabricated wall panels trimmed Moscow tower cycle times by 15 days in 2024 tests, and modular dorms now house workers in Mariupol.

Domestic kiln and machinery makers are scaling up to replace sanctioned European lines, allowing Samolet Group to roll out a local prefab plant in Tula. As capacity jumps, cost parity with conventional builds draws nearer, accelerating adoption in industrial and social-infrastructure schemes.

By Investment Source: Private Capital Leads as Public Cash Gains Pace

Private funds supplied 61.2% of 2024 outlays, led by residential projects financed via escrow accounts. Nonetheless, public budgets are increasing at a 3.67% CAGR, powered by the USD 285.6 billion national-project envelope and USD 14.4 billion Mariupol rebuild. Public-private partnerships proliferate: Rosatom co-finances worker villages around the Leningrad-7 site while retaining operational control.

The Russia construction market size attached to purely state contracts thus widens, giving civil works heavyweights predictable cash flows. In contrast, rising rates have pushed private developers such as Samolet to cut dividend plans, redirecting liquidity toward project completion.

Geography Analysis

The Central Federal District held 31.2% of national construction activity in 2024, making it the clear focal point for building work in Russia. Its proximity to federal ministries and access to a highly skilled contractor base enable the swift execution of large-scale projects, including metro extensions and expressways. Moscow exemplifies this advantage, with developers planning to deliver 219 new residential skyscrapers between 2025 and 2027, reflecting a significant 26.6% increase in annual tower completions. The district also benefits from strong demand for premium properties, with luxury apartments priced at USD 33,300 per m² and business-class units accounting for nearly half of the new supply. However, rising land costs and a constrained labor market are encouraging some developers to explore opportunities beyond the capital’s ring road.

North-Western Russia is anticipated to experience the fastest growth, with a projected 4.47% CAGR through 2030, driven by energy and transportation projects. The region’s engineering capabilities are evident at the Leningrad-7 nuclear unit, which is progressing 2.5 months ahead of schedule with the support of 400 workers. In St. Petersburg, developers are shifting their focus from foreign tenants to domestic and Asian clients, ensuring continued activity in both office and residential developments. Investments in transport infrastructure and port modernization projects provide a steady stream of work, enabling local firms to secure long-term contracts. These factors collectively contribute to the region’s technical expertise and market resilience.

The Volga and Southern Federal Districts are increasingly emerging as alternative growth centers. In the Volga region, the construction of a USD 50 million tractor plant, designed to produce 10,000 units annually, underscores the region’s focus on manufacturing real estate. Meanwhile, in the Southern Federal District, reconstruction efforts in newly integrated territories allocate approximately USD 11.1 billion annually and engage 44,000 builders, making it one of the largest ongoing construction initiatives in the country. Both districts benefit from lower land and labor costs compared to Moscow, offering investors higher potential returns. Federal incentives targeting industrial development and reconstruction continue to attract contractors to these regions, gradually diversifying Russia’s traditionally Moscow-centric construction landscape.[3]Federal District Development Agency, "Regional Investment Priorities," minvr.gov.ru.

Competitive Landscape

In the face of shifting market dynamics, major players in the Russian construction market are recalibrating their strategies. PIK Group is moving away from its historical dependence on expansive land banks. Instead, it's turning to prefabricated construction methods, aiming to lessen its reliance on onsite labor and speed up project delivery. LSR Group is pivoting its investments towards industrial and logistics sectors, seizing the opportunity as e-commerce tenants migrate from central Moscow to outlying regions. On the other hand, Samolet Group is prioritizing cash flow stability. In response to a dip in residential demand, it has halted dividend distributions and adjusted its 2024 projections downward.

Regional players are leveraging reconstruction contracts to expand their presence. For example, Rostov-based Mostotrest has secured a multi-year bridge construction program in Mariupol, valued at USD 560 million. The adoption of advanced technologies is widening the competitive gap within the market. Companies implementing Building Information Modeling (BIM) and drone-based progress tracking are reducing pay-request processing times by two weeks, thereby improving cash flow efficiency. Additionally, equipment manufacturers such as Uralmash are expediting the development of sanctions-compliant tower cranes to support firms unable to access European brands.

New entrants are targeting specialized segments, including prefab modules and 3-D printed concrete façades, offering faster project completion timelines that appeal to state buyers under pressure to meet political deadlines. In response, established firms are forming joint ventures with Chinese fabricators, mitigating technology risks while securing yuan-denominated credit lines. The Russian construction market is increasingly favoring companies that can effectively combine local expertise with advanced efficiency tools sourced internationally.

Russia Construction Industry Leaders

-

PIK Group

-

LSR Group

-

Samolet Group

-

Etalon Group

-

MR Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PIK Group bought a 60% stake in prefabrication specialist Zodchiy for RUB 35 billion (USD 389 million), giving the developer in-house modular capacity for 1.5 million m² of annual housing output

- May 2025: LSR Group secured a RUB 24 billion (USD 267 million) EPC contract from Rosavtodor to widen and modernize a 137 km segment of the M-12 Moscow–Kazan expressway

- April 2025: Samolet Group and China State Construction Engineering formed a 70:30 joint venture to develop a mixed-use waterfront district in Krasnodar valued at RUB 65 billion (USD 722 million)

- March 2025: Mostotrest won a RUB 12 billion (USD 133 million) design-build contract from the Russian Transport Ministry to construct four river bridges within the Mariupol reconstruction program

Russia Construction Market Report Scope

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| Central Federal District (CFD) |

| Volga (Privolzhsky) Federal District |

| North-Western Federal District |

| Southern Federal District |

| Rest of Russia |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Federal District | Central Federal District (CFD) | |

| Volga (Privolzhsky) Federal District | ||

| North-Western Federal District | ||

| Southern Federal District | ||

| Rest of Russia | ||

Key Questions Answered in the Report

What drives future growth despite sanctions?

The Russia construction market size is USD 184.43 billion in 2025, heading toward USD 214.71 billion by 2030 at a 3.09% CAGR.

Which segment leads Russian construction spending?

Residential construction is the largest segment, accounting for 47.1% of 2024 outlays, supported by record individual housing completions.

What drives future growth despite sanctions?

USD 285.6 billion in national-project funding, industrial re-shoring, and an USD 11.1 billion-a-year reconstruction program underpin demand.

How are companies coping with labor shortages?

Firms are adopting prefabrication, automation, and migrant labor, while accelerating BIM-based workflows to offset an 11 million-person gap by 2030.

Which regions show the fastest expansion potential?

The Southern Federal District is poised for the highest CAGR due to large-scale reconstruction, while Volga benefits from industrial investments.

Are material costs expected to ease soon?

Significant relief is unlikely in the medium term because energy hikes, sanctions-driven supply issues, and parallel-import premiums keep prices firm.

Page last updated on: