Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 709.79 Billion |

| Market Size (2030) | USD 905.89 Billion |

| Growth Rate (2025 - 2030) | 5.00% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Construction Market Analysis by Mordor Intelligence

The Latin America Construction Market size is estimated at USD 709.79 billion in 2025, and is expected to reach USD 905.89 billion by 2030, at a CAGR of 5% during the forecast period (2025-2030).

The Latin American construction industry is experiencing significant transformation driven by urbanization and infrastructure construction modernization initiatives across the region. The hospitality sector has emerged as a particularly dynamic segment, with the region's total hospitality construction pipeline encompassing 555 projects and 90,496 rooms as of Q2 2022. This robust pipeline is complemented by accelerated project launches, with 40 new projects totaling 8,481 rooms breaking ground in the first half of 2022, demonstrating strong investor confidence in the sector's growth potential. The construction landscape is further enriched by innovative sustainable construction projects and urban renewal initiatives that are reshaping major metropolitan areas.

Foreign investment continues to play a crucial role in driving construction and development activity across Latin America, though patterns vary significantly by country. Guatemala, for instance, received USD 18 billion in remittances from the United States in 2022, representing 20.9% of its GDP and significantly influencing construction sector investments. The region is witnessing a notable shift toward sustainable and renewable energy infrastructure projects, exemplified by Total Eren's entry into Honduras with a 112 MW wind project in 2023, marking one of the largest foreign investments in renewable energy infrastructure in Central America.

Technological advancement and innovation are increasingly shaping the construction landscape, with countries across the region embracing modern construction technology methodologies and digital transformation. The establishment of LIFT's manufacturing innovation initiatives in Puerto Rico represents a significant step toward modernizing construction practices and developing a skilled workforce for advanced manufacturing processes. This transformation is accompanied by the integration of Building Information Modeling (BIM), modular construction techniques, and smart construction practices across major projects.

Infrastructure construction development remains a cornerstone of construction activity, with significant investments in water, transportation, and public facilities. The EPA's 2023 announcement of a USD 23 million investment in Puerto Rico's water infrastructure projects exemplifies the scale of infrastructure modernization efforts underway. New diplomatic construction projects, such as the US Embassy in Guatemala City, demonstrate the continued confidence of international stakeholders in the region's long-term growth prospects. These developments are characterized by advanced sustainable design features and resilient construction methodologies, setting new standards for future construction projects in the region.

Latin America Construction Market Trends and Insights

Government Infrastructure Investments & Policy Support

Latin American governments are making substantial infrastructure investments to drive construction sector growth. In Chile, the government has proposed an ambitious infrastructure plan including 48 grid infrastructure projects worth USD 1.45 billion, with the largest transmission line project estimated at USD 345 million scheduled to begin construction in 2025. Similarly, Puerto Rico has secured USD 23 million in federal funding for water infrastructure projects across multiple communities, demonstrating the government's commitment to essential infrastructure development. These public sector investments are creating significant opportunities for construction companies while addressing critical infrastructure needs.

The regulatory environment across Latin America has become increasingly supportive of construction activities, with governments implementing policies to stimulate both public and private sector development. Colombia's government has introduced comprehensive policies and subsidies to address the housing shortage, encouraging construction companies and investors to participate in residential construction projects. In Panama, liberal economic policies and political stability have created an exceptional business environment that has attracted substantial foreign investment in construction projects. These government initiatives, combined with streamlined approval processes and tax incentives, are providing a strong foundation for sustained growth in the construction sector.

Understand The Key Trends Shaping This Market

Download PDF

Growing Tourism & Hospitality Construction Demand

The expanding tourism sector across Latin America is driving significant construction activity in the hospitality segment. Mexico leads the region with a hotel supply ratio of 2.6 rooms per 1,000 inhabitants, while Chile is projected to add approximately 46,700 quality hotel rooms in the coming years, representing a 5.3% increase in supportable supply. This growth in tourism infrastructure is creating substantial opportunities for construction companies specializing in hospitality projects, from luxury resorts to business hotels. Peru has emerged as another key market showing remarkable growth in quality lodging supply, despite starting from a relatively smaller base.

The hospitality construction boom is particularly evident in strategic tourist destinations where developers are responding to increasing visitor numbers with new projects. Colombia's tourism sector growth has sparked significant construction activity, supported by special tax incentives for hospitality development. The trend extends beyond traditional hotels to include mixed-use developments incorporating retail spaces, restaurants, and entertainment facilities. This diversification in hospitality construction projects is creating multiple revenue streams for developers while meeting the evolving needs of both leisure and business travelers.

Foreign Direct Investment & Economic Stability

Latin America's construction sector is benefiting from strong foreign direct investment flows, particularly in economically stable countries. Panama's exceptional business environment has attracted investors from the United States, Europe, and Asia, leading to consistent price appreciation of 5-10% annually in real estate values. This steady influx of foreign capital is funding major construction projects across residential, commercial, and infrastructure segments, while also introducing international construction standards and technologies to the region. The stability of local currencies and favorable investment policies has made several Latin American countries attractive destinations for global construction firms and developers.

The region's improving economic fundamentals are encouraging both regional and international construction companies to expand their operations. Brazil's economic recovery has supported steady commercial construction activity, particularly in the commercial sector, while Chile's reputation as one of the region's most stable economies continues to attract long-term investment in construction projects. Colombia's emergence as a key business destination, despite challenges in specific sectors like petroleum, has created sustained demand for commercial and industrial construction projects. This economic stability, combined with urbanization trends and growing middle-class populations, is providing construction companies with a robust pipeline of projects across multiple segments.

Urbanization & Housing Demand

Rapid urbanization across Latin America is creating substantial demand for residential and commercial construction projects. Colombia's current housing shortage of more than 1.3 million homes exemplifies the scale of opportunity for construction companies in the residential construction sector. This deficit, combined with government support through subsidies and incentives, is driving significant construction activity in both affordable and middle-income housing segments. The trend is particularly evident in major urban centers where population growth and economic development are creating demand for new residential communities and supporting infrastructure.

The urbanization trend is also spurring development in the commercial and mixed-use segments. Brazil's office market, despite high availability rates, continues to see new development activity as companies seek modern, efficient spaces in prime locations. This urban development extends beyond traditional construction to include green building practices and smart city initiatives. The demand for urban housing and commercial space is further supported by rising income levels and changing lifestyle preferences among Latin American consumers, creating opportunities for innovative construction projects that integrate residential, commercial, and recreational facilities within planned communities.

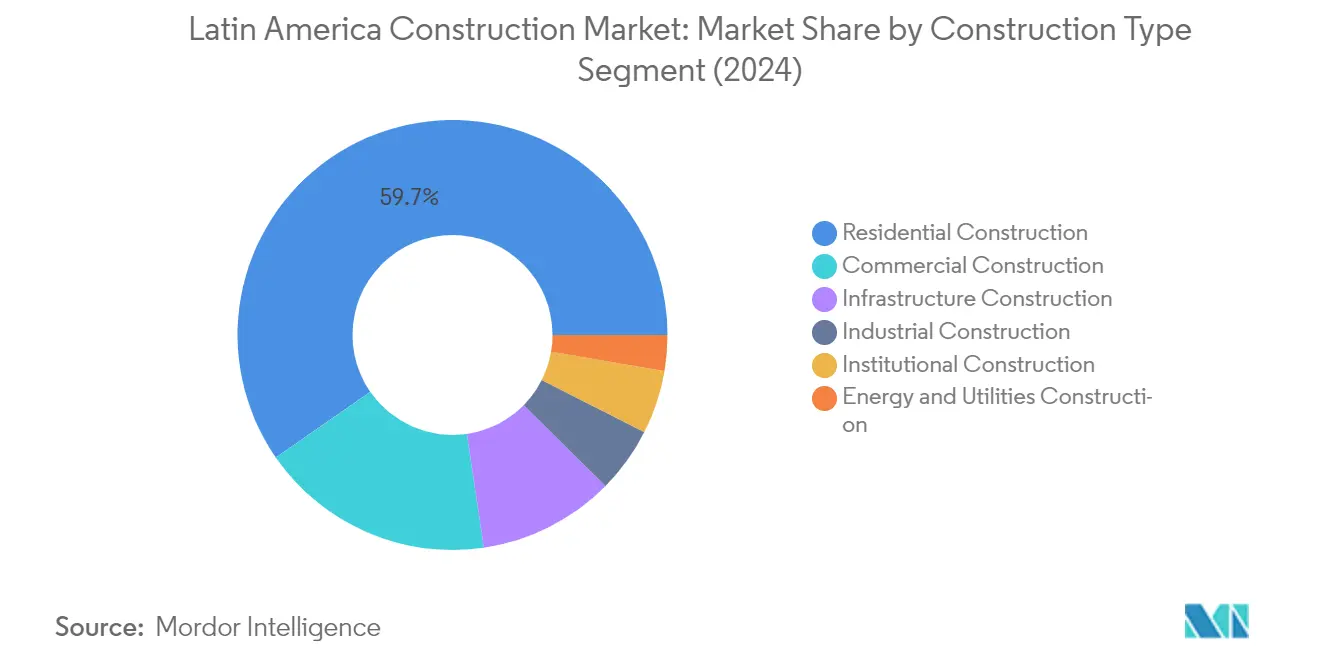

Segment Analysis: By Construction Type

Residential Construction Segment in Latin America Construction Market

The residential construction segment continues to dominate the Latin American construction market, holding approximately 60% market share in 2024. This segment's prominence is driven by increasing urbanization rates across major cities, growing housing demand from middle-class populations, and government initiatives supporting affordable housing projects. In Chile, which represents a significant portion of the regional market, residential construction accounts for nearly 7,222 billion CLP in 2024, reflecting strong domestic housing demand and urban development projects. The segment's robust performance is further supported by favorable mortgage rates, increasing foreign investment in residential real estate, and ongoing urban renewal programs across major metropolitan areas.

Energy and Utilities Construction Segment in Latin America Construction Market

The energy and utilities construction segment is emerging as the fastest-growing sector in the Latin American construction market, with a projected growth rate of approximately 4% during 2024-2029. This accelerated growth is primarily driven by increasing investments in renewable energy infrastructure, particularly solar and wind power projects. The segment's expansion is further supported by government initiatives promoting clean energy transition, modernization of existing power distribution networks, and growing demand for sustainable utility infrastructure. Major projects include large-scale solar installations, wind farms, and grid modernization initiatives across the region, particularly in countries like Chile where energy infrastructure development remains a key priority.

Remaining Segments in Latin America Construction Market

The other segments in the Latin American construction market include commercial construction, industrial construction, institutional, and infrastructure construction, each playing vital roles in the region's development. Commercial construction is driven by retail expansion and office space demand in urban centers. Industrial construction benefits from manufacturing sector growth and logistics facility development. The institutional segment focuses on healthcare facilities, educational institutions, and government buildings. Infrastructure construction encompasses transportation projects, including highways, bridges, and urban transit systems. These segments collectively contribute to the market's diversification and overall economic development across Latin America.

Latin America Construction Market Geography Segment Analysis

Construction Market in Dominican Republic

The Dominican Republic maintains its position as the dominant force in the Latin American construction sector, commanding approximately 35% market share in 2024. The country's construction industry benefits from its strategic location and robust infrastructure construction initiatives. The government's commitment to modernizing transportation networks, including ports and airports, has attracted significant private sector participation. The construction sector is particularly active in tourism-related infrastructure, with numerous resort and hospitality projects under development along the coastline. The country's focus on renewable energy infrastructure, including solar and wind power facilities, demonstrates its commitment to sustainable development. Additionally, the implementation of public-private partnerships has accelerated the execution of major infrastructure construction projects, particularly in urban areas. The sector's resilience is further strengthened by steady foreign direct investment and supportive government policies aimed at maintaining construction sector growth.

Construction Market in Guatemala

Guatemala's construction sector is experiencing remarkable growth, with projections indicating an impressive growth rate of approximately 8% during 2024-2029. The country's construction industry is undergoing a significant transformation, driven by extensive urban development projects and infrastructure modernization initiatives. The government's focus on improving transportation infrastructure, including highways and ports, has created numerous opportunities for construction companies. The residential construction segment has shown particular dynamism, supported by increasing urbanization and growing housing demand. Guatemala's commitment to sustainable construction practices is evident in its adoption of green building technologies and eco-friendly materials. The industrial construction sector is also expanding, with new manufacturing facilities and logistics centers being developed. Foreign investment in the construction sector has increased significantly, particularly in commercial and industrial projects, reflecting growing international confidence in Guatemala's economic prospects.

Construction Market in Chile

Chile's construction sector continues to demonstrate remarkable resilience and innovation in its approach to infrastructure construction development. The country's focus on sustainable construction practices and green building initiatives has positioned it as a regional leader in environmental consciousness. Significant investments in renewable energy infrastructure, including solar and wind power facilities, have created substantial opportunities for construction companies. The sector benefits from strong institutional frameworks and transparent regulatory policies, making it attractive for both domestic and international investors. Urban development projects, particularly in metropolitan areas, are driving demand for both residential and commercial construction. The industry's adoption of advanced construction technologies and digital solutions has improved project efficiency and quality. Additionally, Chile's commitment to earthquake-resistant construction standards has fostered specialized expertise in structural engineering and construction methodologies.

Construction Market in Costa Rica

Costa Rica's construction sector exhibits strong fundamentals driven by its stable political environment and growing tourism industry. The country's commitment to environmental sustainability has influenced construction practices, with a growing emphasis on green building techniques and eco-friendly materials. Infrastructure development focuses on improving connectivity between urban centers and tourist destinations, supporting economic growth. The commercial construction segment has shown particular dynamism, driven by demand for modern office spaces and retail developments. Costa Rica's strategic position in Central America has attracted international investors, particularly in hospitality and commercial real estate projects. The government's support for sustainable urban development has led to innovative construction projects that balance environmental protection with economic growth. The sector also benefits from skilled labor availability and established construction standards that promote quality and safety.

Construction Market in Other Countries

The construction markets in El Salvador, Honduras, and Puerto Rico each demonstrate unique characteristics and development trajectories. These markets are characterized by varying degrees of infrastructure development, regulatory frameworks, and economic conditions. El Salvador's construction sector focuses on urban development and infrastructure modernization, while Honduras emphasizes residential construction and tourism-related infrastructure. Puerto Rico's construction industry continues to evolve with a focus on resilient infrastructure and sustainable development practices. These markets share common challenges and opportunities, including the need for infrastructure modernization, sustainable construction practices, and improved housing solutions. The construction sectors in these countries benefit from government initiatives aimed at improving infrastructure quality and accessibility, though each market maintains its distinct characteristics based on local economic conditions and development priorities.

Competitive Landscape

Top Companies in Latin America Construction Market

The Latin American construction market features prominent players like Doka, Peri, Ulma Construction, Encofrados Alsina, SH Formwork, and Brand Industrial Services leading the industry. Companies are increasingly focusing on developing innovative formwork and scaffolding solutions to meet the growing demands of infrastructure and residential projects across the region. Strategic partnerships with local contractors and distributors have become essential for market penetration and expansion. Operational excellence is being achieved through investments in digital technologies and automated construction processes, while sustainability initiatives are gaining prominence in product development. Companies are also expanding their service offerings to include engineering consultancy, construction management, and specialized technical support to create additional value streams and strengthen client relationships.

Fragmented Market with Strong Local Presence

The Latin American construction industry exhibits a fragmented structure with a mix of global players and strong regional competitors operating across different segments. Local players maintain significant market share due to their established networks, understanding of regional construction practices, and ability to provide customized solutions for specific market needs. The market demonstrates moderate consolidation levels, with larger companies primarily focusing on high-value infrastructure and commercial projects while smaller players dominate the residential and small-scale commercial segments.

The industry has witnessed increased merger and acquisition activities, particularly as global players seek to strengthen their regional presence through strategic partnerships and acquisitions of local companies. These consolidation efforts are driven by the need to achieve economies of scale, expand geographic reach, and enhance technological capabilities. Companies are also forming joint ventures to pool resources and expertise for large-scale infrastructure projects, particularly in emerging markets within the region.

Innovation and Localization Drive Market Success

Success in the Latin American construction market increasingly depends on companies' ability to combine technological innovation with local market expertise. Incumbent players are strengthening their position by investing in research and development, particularly in sustainable construction technology solutions and digital transformation initiatives. Market leaders are also focusing on developing comprehensive service portfolios that include technical support, training programs, and after-sales services to create stronger barriers to entry and enhance customer loyalty.

New entrants and challenger companies can gain market share by focusing on underserved segments and developing specialized solutions for specific construction applications. The market presents opportunities for companies that can effectively address the growing demand for cost-effective and environmentally sustainable construction services. Success also depends on navigating complex regulatory environments across different countries, building strong relationships with local stakeholders, and maintaining flexibility to adapt to changing market conditions and customer preferences.

Latin America Construction Industry Leaders

Sigdo Koppers

Sacyr

MRV Engenharia

Carso Infraestructura y Construcción

Techint Ingeniería y construcción

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: Holcim acquires PASA®, a leading roofing and waterproofing solutions producer in Mexico and Central America, with pro forma net sales of USD 38 million. As a leader in innovation, sustainability, and quality, PASA® expands Holcim’s roofing and waterproofing offer and strengthens its regional business footprint. By integrating the existing PASA® distribution network with waterproofing solutions from its GacoFlex product range, Holcim will deliver more customer value with an enhanced supply chain.

- May 2023: Sika has acquired the MBCC Group, a leading global supplier of construction chemicals. With a focus on innovation and sustainability, MBCC Group has been at the forefront of driving positive change in the construction industry. By joining forces, Sika and MBCC Group have created a workforce of 33,000 experts and achieved net sales of more than CHF 12 billion (USD 13.21 billion).

Latin America Construction Market Report Scope

Construction includes any on-site physical work that involves erecting a structure, cladding, external finish, formwork, fixtures, installing services, unloading equipment, supplies, etc. A complete background analysis of the Latin America Construction Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Latin American construction market is segmented by sector (residential, commercial, industrial, infrastructure (transportation), energy, and utilities). The market size and forecast are provided in values (USD) for all the above segments.

By Type

| Residential |

| Commercial |

| Industrial |

| Infrastructure |

| Energy and Utilities |

| By Type | Residential |

| Commercial | |

| Industrial | |

| Infrastructure | |

| Energy and Utilities |

Key Questions Answered in the Report

How big is the Latin America Construction Market?

The Latin America Construction Market size is expected to reach USD 709.79 billion in 2025 and grow at a CAGR of 5% to reach USD 905.89 billion by 2030.

What is the current Latin America Construction Market size?

In 2025, the Latin America Construction Market size is expected to reach USD 709.79 billion.

Who are the key players in Latin America Construction Market?

Sigdo Koppers, Sacyr, MRV Engenharia, Carso Infraestructura y Construcción and Techint Ingeniería y construcción are the major companies operating in the Latin America Construction Market.

What years does this Latin America Construction Market cover, and what was the market size in 2024?

In 2024, the Latin America Construction Market size was estimated at USD 674.30 billion. The report covers the Latin America Construction Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Latin America Construction Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: