Canada Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

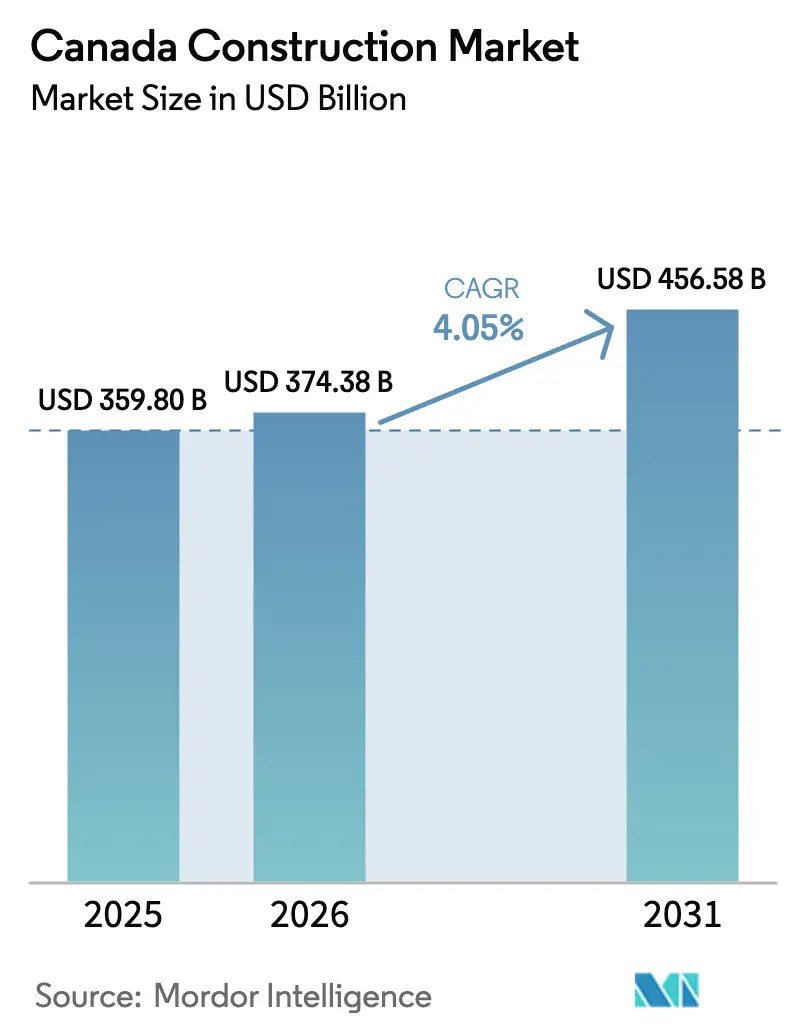

| Base Year Market Size (2025) | USD 359.80 Billion |

| Market Size (2026) | USD 374.38 Billion |

| Market Size (2031) | USD 456.58 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

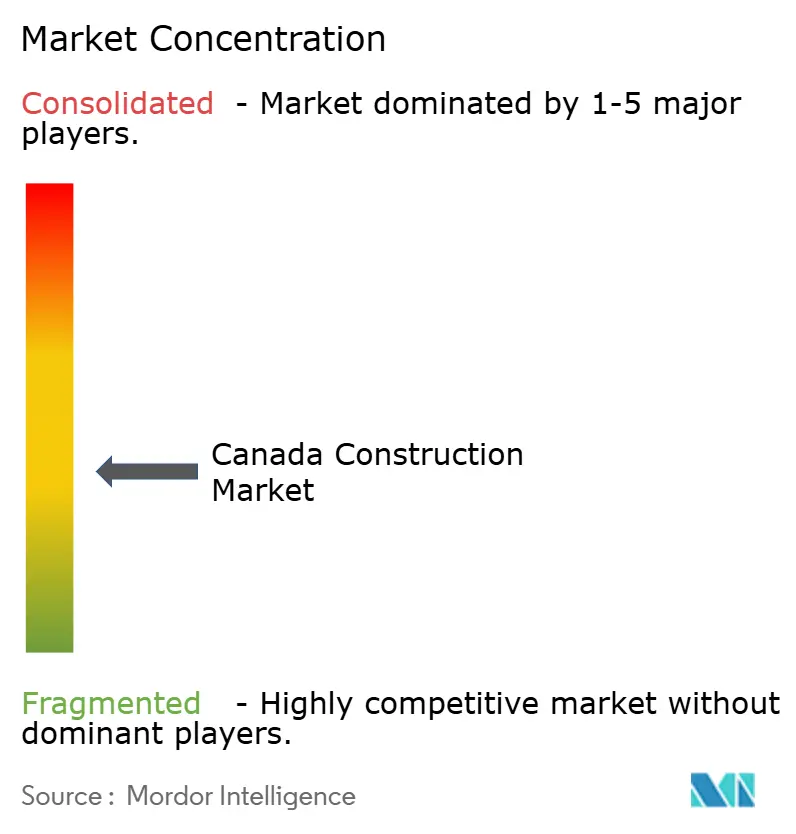

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Construction Market Analysis by Mordor Intelligence

Canada Construction Market size in 2026 is estimated at USD 374.38 billion, growing from 2025 value of USD 359.80 billion with 2031 projections showing USD 456.58 billion, growing at 4.05% CAGR over 2026-2031. Residential building activity, infrastructure modernisation, and industrial projects tied to the digital economy continue to anchor demand. Policy alignment between federal and provincial governments is accelerating low-carbon construction, while the C$180 billion Investing in Canada Plan (USD 133.2 billion) is sustaining a multi-year public works pipeline. Multi-family housing, data centres, and e-commerce logistics facilities are emerging as high-growth niches, and Indigenous-led partnerships are opening northern projects linked to critical mineral extraction. Competitive intensity remains high because 147,490 licensed firms operate nationwide, yet labour scarcity, rising finance costs, and volatile input prices are compressing margins.

Key Report Takeaways

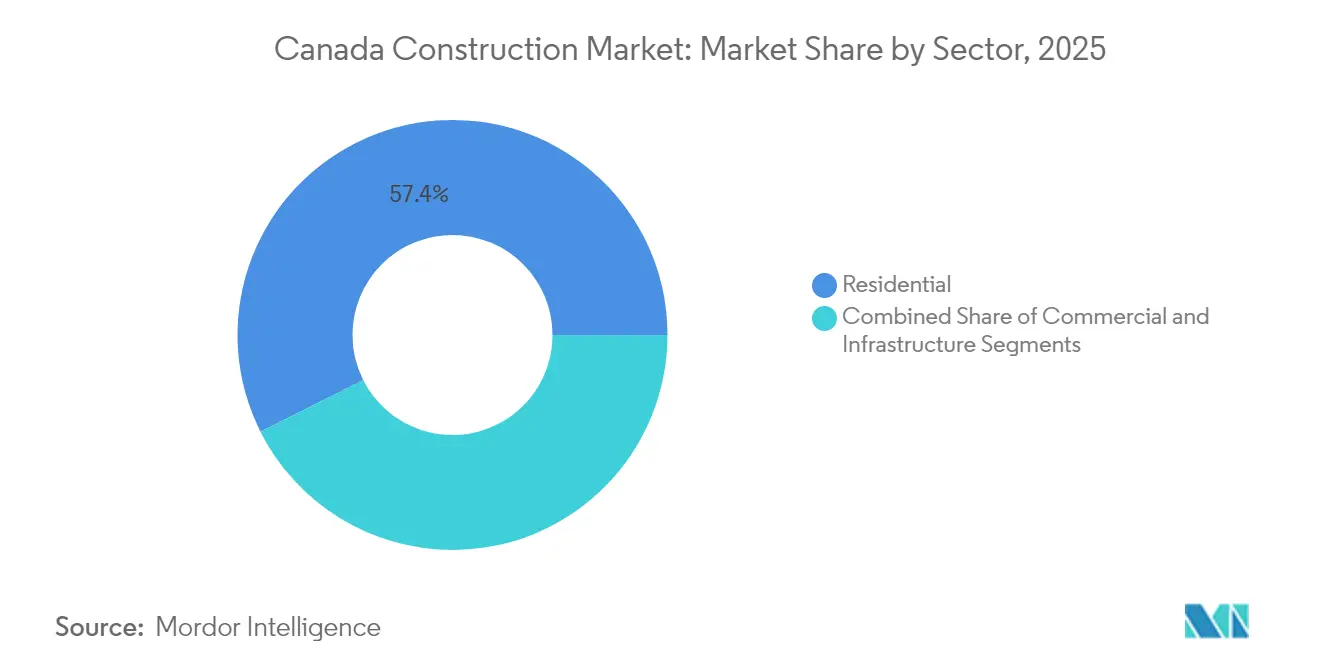

- By sector, residential construction held 57.42% of the Canada construction market share in 2025, whereas energy and utilities are projected to post the fastest 4.18% CAGR through 2031.

- By construction type, new construction accounted for 73.12% share of the Canada construction market size in 2025, while renovation and retrofit are expected to advance at a 4.27% CAGR to 2031.

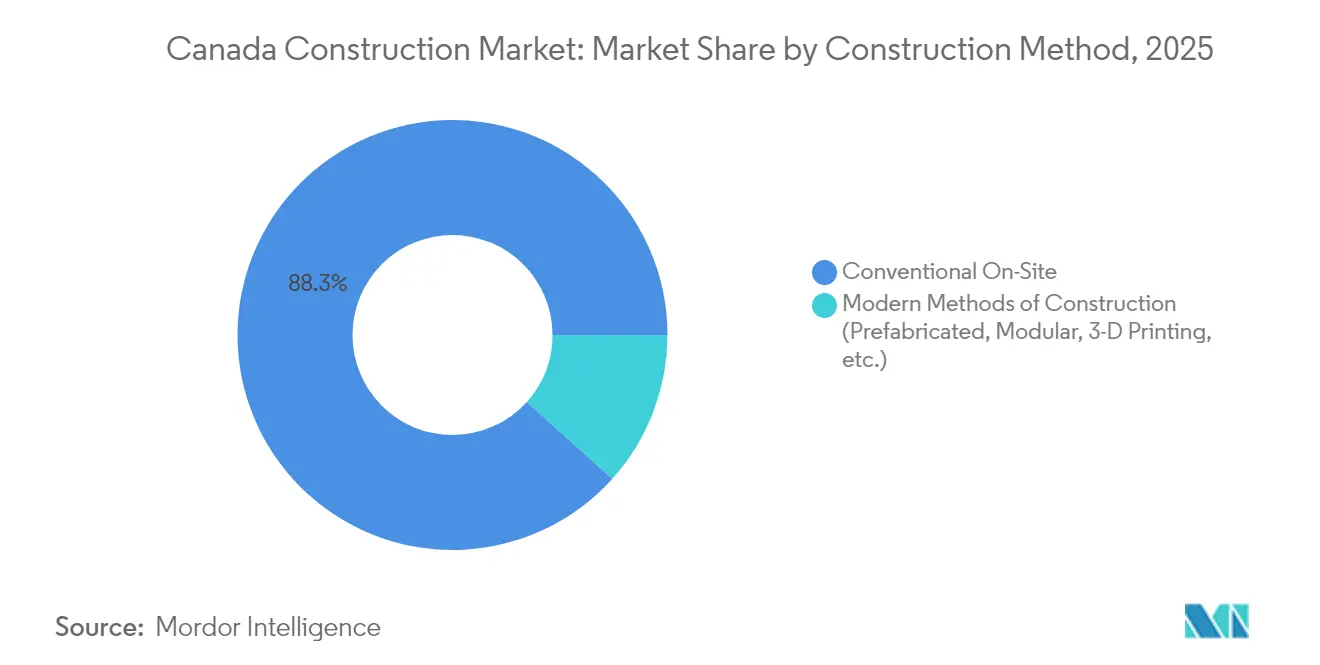

- By construction method, conventional on-site activity controlled 88.34% of the Canada construction market size in 2025, yet modern methods are forecast to climb at a 4.41% CAGR between 2026-2031.

- By investment source, private funding represented 69.12% of the Canada construction market size in 2025, whereas public-private partnerships are forecast to grow at a 4.22% CAGR through 2031.

- By province, Ontario led with 38.45% of the Canada construction market share in 2025, while Alberta is projected to log the fastest 4.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Investing in Canada Plan public-works pipeline | +1.2% | National, especially Ontario, Quebec and Alberta | Long term (≥ 4 years) |

| Housing affordability crisis stimulating multi-family supply | +0.9% | National, acute in Toronto, Vancouver and Montreal | Short term (≤ 2 years) |

| Federal and provincial green-building incentives | +0.8% | National with higher uptake in British Columbia, Ontario and Quebec | Medium term (2-4 years) |

| Demand for data centres and logistics hubs | +0.6% | Alberta, Ontario, Quebec and emerging in British Columbia | Medium term (2-4 years) |

| Code-mandated climate-resilience retrofits | +0.4% | National with focus on climate-vulnerable regions | Medium term (2-4 years) |

| Indigenous-led northern partnerships | +0.3% | Northern territories plus northern Ontario and Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Investing in Canada Plan public-works pipeline

The USD 133.2 billion plan is backing more than 500 major projects nationwide, including the Alto high-speed rail corridor, whose USD 2.9 billion first phase will support 51,000 construction jobs. Natural Resources Canada lists USD 468.1 billion in energy and resource builds at various stages, underscoring sustained heavy-civil demand. Public-private partnerships worth USD 56.2 billion introduce risk-sharing frameworks that reward firms with strong balance sheets. Mega-projects such as the Fraser River Tunnel replacement in British Columbia are embedding seismic technology and smart-traffic systems that raise the technical bar for bidders. The scale and diversity of this pipeline generate long-run visibility for contractors, equipment suppliers, and material producers.

Housing affordability crisis spurring multi-family and high-density projects

Canada requires 3.5 million additional homes by 2030, and policy tools now channel capital into rental and condominium towers instead of detached houses. The Apartment Construction Loan Program has expanded to USD 11.1 billion to reduce financing costs for large rental blocks. A USD 25 billion prefabricated-housing initiative is directing bulk orders to modular factories, shortening build times and lowering waste. Purpose-built rentals dominate priority lists across all 12 metropolitan areas reviewed by CMHC. Standardised design catalogues adopted by federal agencies encourage copy-and-paste site plans that accelerate approvals. This shift is reshaping contractor skill requirements toward vertical construction, crane logistics, and off-site assembly.

Federal and provincial green-building incentives accelerating adoption of low-carbon materials

The Greener Homes Initiative has financed more than 165,000 retrofits, cutting average household energy costs by USD 386 each year and stimulating private demand for advanced materials. Clean Economy Investment Tax Credits worth USD 68.8 billion over the decade are lowering project costs for heat pumps, hydrogen, and other technologies. Provincial programmes magnify these effects, illustrated by British Columbia’s Oil-to-Heat-Pump scheme, funded with USD 76.7 million in federal transfers. Federal procurement rules now prefer low-carbon concrete and steel, creating demonstration projects that influence private developers. Together, these incentives position the Canada construction market as a proving ground for exportable green-building solutions[1]David Paterson, “Canada Greener Homes Grant Program Overview,” Natural Resources Canada, nrcan.gc.ca

Surging demand for data centres and e-commerce logistics facilities

Alberta’s AI Data Centre Strategy targets USD 55.5-74 billion in digital-infrastructure investment by pairing low-cost power with streamlined permits. National industrial construction set a quarterly record in Q4 2024 with 16.3 million ft² delivered, yet vacancy still sat at just 4.3% in major hubs. Rents climbed 16% in Montreal as retailers and cloud providers competed for scarce space. Data centre projects require redundant power and sophisticated cooling, pushing contractors into mechanical-electrical specialisation. Continuous-operation requirements are raising workmanship standards that spill over into hospitals and transit hubs, broadening the influence of this niche.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortages and ageing workforce | -0.9% | National, severe in Alberta and Ontario | Medium term (2-4 years) |

| Tight monetary policy and elevated mortgage rates | -0.7% | National, acute in Toronto and Vancouver | Short term (≤ 2 years) |

| Volatile lumber and steel prices | -0.4% | National with supply-chain variations | Short term (≤ 2 years) |

| Lengthy environmental permitting timelines | -0.3% | National, felt most in energy and infrastructure builds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-labour shortages and ageing workforce

BuildForce Canada projects that 22% of the construction workforce will retire by 2032, removing critical experience. Immigration pathways favour university degrees, leaving gaps in trades such as carpentry and welding. Job vacancies fell from 991,680 in 2022 to 737,530 in 2023, yet the remaining openings reflect skills mismatches rather than labour surplus. Firms are recruiting abroad and investing in training centres, but productivity growth lags demand, especially in multi-family high-rise work. Unless vocational-training throughput improves, this restraint will shave almost one percentage point from potential growth over the medium term.

Tight monetary policy and elevated mortgage rates dampening new-home starts

Although the Bank of Canada lowered its policy rate from 5% to 3.25% in 2024, mortgage renewals on USD 222 billion worth of loans still strain household budgets. Delinquency doubled in Toronto and Vancouver to 0.20%, curbing the appetite for new purchases. Developers face higher carry costs, leading to project cancellations or smaller unit counts. Investor demand dipped as rental yields compressed against rising debt service. This restraint is expected to moderate within two years as inflation eases and rate cuts broaden affordability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential dominance faces an energy-transition challenge

Residential construction captured 57.42% of the Canada construction market size in 2025 as governments raced to alleviate housing shortages. Condo towers and purpose-built rentals now crowd skylines in Toronto and Vancouver, while modular factories secure bulk orders for northern Indigenous communities. The energy and utilities segment, although only 8.72% of 2025 output, is poised for a 4.18% CAGR through 2031 thanks to nuclear refurbishment at Pickering and grid-modernisation mandates. Contractors accustomed to wood framing are pivoting to concrete cores, prefabricated panels, and robotic rebar tying to meet tighter delivery timelines. Banks increasingly tier lending rates by project energy performance, nudging developers toward net-zero designs that blend rooftop solar with high-efficiency HVAC.

Commercial and institutional building demand is more nuanced. Offices face reduced leasing, but industrial warehouses tied to e-commerce enjoy brisk absorption. Hospital and school upgrades funded under the Investing in Canada Plan create steady institutional volume. The energy-utilities build-out introduces specialist packages such as turbine hall erection and transmission-line construction, drawing new entrants into the Canada construction market. Synergies emerge where mixed-use precincts integrate residential, retail, and transit infrastructure, enlarging the total contract value per site.

By Construction Type: Renovation acceleration signals market maturation

New construction retained a 73.12% share of the Canada construction market size in 2025. Even so, renovation and retrofit work is forecast to expand at a 4.27% CAGR, underpinned by the Greener Homes Initiative and National Building Code amendments. Aging apartment blocks require envelope insulation, low-emissivity glazing, and heat-pump retrofits. Owners of heritage properties tap federal grants that cover up to 30% of eligible costs, provided upgrades meet embodied-carbon thresholds. Contractors capable of night-shift work and tenant-occupied retrofits secure premium margins.

The line between new build and deep renovation is blurring. Projects such as the USD 2.1 billion Ville-Marie tunnel modernisation involve complete systems replacement yet keep the original structure, classifying as renovation in statistics. The retrofit wave encourages investment in diagnostic technologies like infrared thermography and 3D laser scanning. Financing flexibility also improves, with green bonds channeling capital into energy-efficiency packages that bundle multiple buildings for scale. Over the forecast horizon, renovation spend is likely to claim an incremental share during economic slowdowns when developers defer new starts.

By Construction Method: Modern techniques gain traction despite conventional dominance

Conventional on-site construction controlled 88.34% of 2025 revenues, but modern methods of construction are set for 4.41% CAGR growth. Modular apartment modules, panelised walls, and mass-timber components can cut schedules by 20-50%, a crucial advantage amid labour shortages. The federal Loan Program earmarks USD 370 million for builders adopting factory assembly lines, lowering interest rates by 50 basis points relative to standard loans. National Research Council code updates now allow 12-storey encapsulated mass-timber buildings, triggering taller wood projects such as Vancouver’s Burrard Exchange.

Regulatory harmonisation remains the chief bottleneck. CSA Standard A277 certification applies to volumetric modules, but municipalities differ on inspection procedures, forcing dual approvals that erode savings. Despite the setback of a major factory closure in 2024, new entrants backed by timber producers plan facilities near rail spurs in Ontario and Quebec. Adoption will accelerate where specialist lenders embrace pay-for-performance models, guaranteeing time and cost savings.

By Investment Source: PPP growth reflects infrastructure complexity

Private capital made up 69.12% of the Canada construction market size in 2025, reflecting robust housing and industrial activity. Public-private partnerships are on a steeper trajectory, with a 4.22% CAGR through 2031 as mega-projects exceed public balance-sheet capacity. The Alto high-speed rail consortium employs an availability-payment model that transfers ridership risk to the public sector while leaving cost overruns with the builder. Indigenous housing allocations of USD 4.3 billion adopt community-ownership structures that combine grant funding with revenue from natural resources.

For contractors, PPPs demand enhanced financial engineering and lifecycle-cost analysis. Lenders scrutinise operations-and-maintenance plans spanning 30 years, pushing bidders to form joint ventures with facility-management specialists. Projects in transport and healthcare dominate the pipeline because asset revenue streams are clearer. Smaller municipalities are testing mini-PPPs for water-treatment plants, signalling widening applicability.

Geography Analysis

Ontario commands 38.45% of current spending and is forecast to mirror the national 4.05% CAGR through 2031. Nuclear refurbishment at Pickering and the GO Rail Expansion anchor multi-year order books and create supply-chain synergies for turbine, switchgear, and tunnel suppliers. Provincial harmonisation with national codes removes 1,730 unique clauses, lowering compliance costs for firms that operate coast to coast. Condo-led densification in Toronto prompts significant investments in water mains and sewage treatment, linking civil and residential workflows within the Canada construction market. Indigenous partnerships on mining access roads around Timmins highlight inclusive procurement trends gaining traction across provinces.

Quebec benefits from mega-projects that showcase complex engineering. The USD 2.7 billion Île-d’Orléans cable-stayed bridge introduces seismic isolation bearings and wildlife corridors, setting design precedents. Long-duration tunnel renovations in Montreal ensure continuous employment for underground specialists and reinforce demand for prefabricated reinforcement cages. Indigenous ownership of an 85-kilometre transmission line demonstrates new governance models where communities capture recurring income from power tariffs. These examples cultivate local expertise in mass timber, prefabricated steel, and intelligent-transport systems, reinforcing Quebec’s reputation for engineering innovation.

Western Canada displays two distinct growth narratives. British Columbia leverages transport network modernisation with the USD 3 billion Fraser River Tunnel replacement, integrating seismic design suited to Pacific Rim fault lines. Data-centre clusters emerge near hydro-powered substations, reinforcing low-carbon branding. Alberta’s appeal lies in abundant land, competitive power prices, and provincial tax credits aligned with digital infrastructure, enabling the Canada construction market to attract hyperscale cloud providers. The Rest-of-Canada grouping gains visibility through Arctic corridor builds like the Grays Bay Road and Port, which enhances critical mineral supply security. Climate-resilient upgrades to Atlantic seawalls and prairie flood-control systems diversify regional demand and broaden contractor opportunity sets.

Competitive Landscape

The market remains highly fragmented, with no single firm holding a dominant share of overall national revenue. This fragmentation fosters price competition yet also nurtures nimble specialists that focus on mass-timber assembly, tunnel ventilation or nuclear decommissioning. Consortia form around megaproject tenders where bonding capacity exceeds the ability of individual firms. Procurement frameworks increasingly evaluate carbon footprints and Indigenous engagement plans, encouraging companies to invest in life-cycle assessment tools and cultural-competency training.

Strategic acquisitions are reshaping the mid-tier. Saint-Gobain added The Bailey Group for USD 880 million, capturing roll-formed steel supply in twelve plants and strengthening its vertical integration into gypsum and insulation systems. VINCI Construction’s purchase of Entreprises Marchand broadens its heavy-civil presence in Quebec. These moves signal renewed interest by global players in securing local labour pools and pre-existing project pipelines within the Canada construction market.

Technology adoption has become the defining competitive lever. BIM-driven clash detection, point-cloud surveying and predictive cost-control platforms reduce rework and enhance thin margins. Firms proficient in modular manufacturing partner with financiers to guarantee schedule savings, winning bids under value-for-money assessments. Prompt-payment legislation at the federal level improves cash-flow certainty, a boon to small contractors and suppliers. Together, these dynamics point toward gradual consolidation around digitally enabled, financially resilient firms that can meet exacting ESG and Indigenous-participation benchmarks.

Canada Construction Industry Leaders

PCL Construction

EllisDon Corporation

Aecon Group Inc.

Graham Construction & Engineering

Bird Construction Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Government of Canada advanced the Projet structurant de l’Est with ARTM overseeing early works ahead of an August 2025 collaborative-delivery launch.

- February 2025: Cadence was named preferred developer for the Alto rail corridor linking Quebec City and Toronto via a 1,000 km, 300 km/h network.

- February 2025: British Columbia awarded the USD 3 billion Fraser River Tunnel replacement to the Cross Fraser Partnership.

- January 2025: An Aecon–AtkinsRéalis joint venture secured a USD 1.1 billion Pickering Nuclear Generating Station refurbishment contract.

Canada Construction Market Report Scope

| Residential | Apartments / Condominiums |

| Villas and Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation / Retrofit |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, 3-D Printing, etc.) |

| Public |

| Private |

| Public-Private Partnership (PPP) |

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Sector | Residential | Apartments / Condominiums |

| Villas and Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation / Retrofit | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, 3-D Printing, etc.) | ||

| By Investment Source | Public | |

| Private | ||

| Public-Private Partnership (PPP) | ||

| By Province / Territory | Ontario | |

| Québec | ||

| British Columbia | ||

| Alberta | ||

| Rest of Canada | ||

Key Questions Answered in the Report

What is the current size of the Canada construction market?

The market reached USD 374.38 billion in 2026 and is forecast to climb to USD 456.58 billion by 2031.

What is the expected CAGR for the Canada construction market during 2026-2031?

A compound annual growth rate of 4.05% is projected for the 2026-2031 period.

Which construction segment holds the largest market share?

Residential projects led with 57.42% of market output in 2025.

Which segment is expected to grow the fastest?

The energy and utilities segment is forecast to expand at a 4.18% CAGR through 2031.

Which province commands the highest share of construction spending?

Ontario accounted for 38.45% of national construction value in 2025.

What is the main constraint facing Canadian builders today?

A looming skilled-labour shortfall—22% of the workforce is approaching retirement—remains the most significant headwind.

Page last updated on: