Organic Pet Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

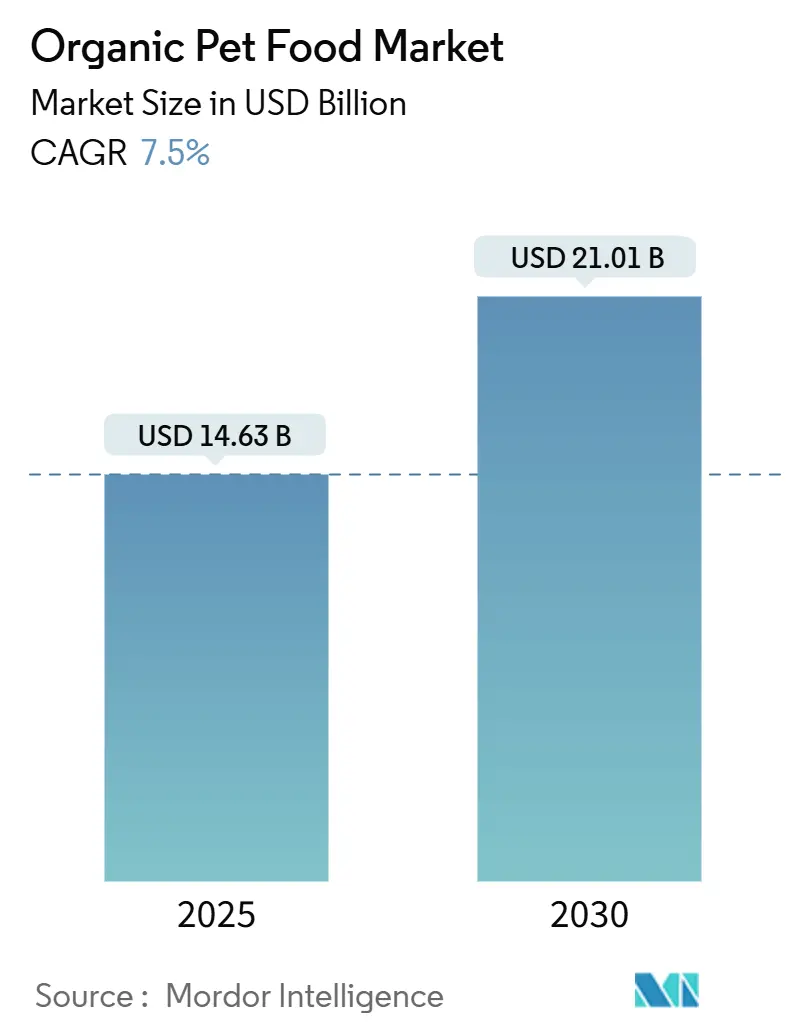

| Market Size (2025) | USD 14.63 Billion |

| Market Size (2030) | USD 21.01 Billion |

| Growth Rate (2025 - 2030) | 7.50% CAGR |

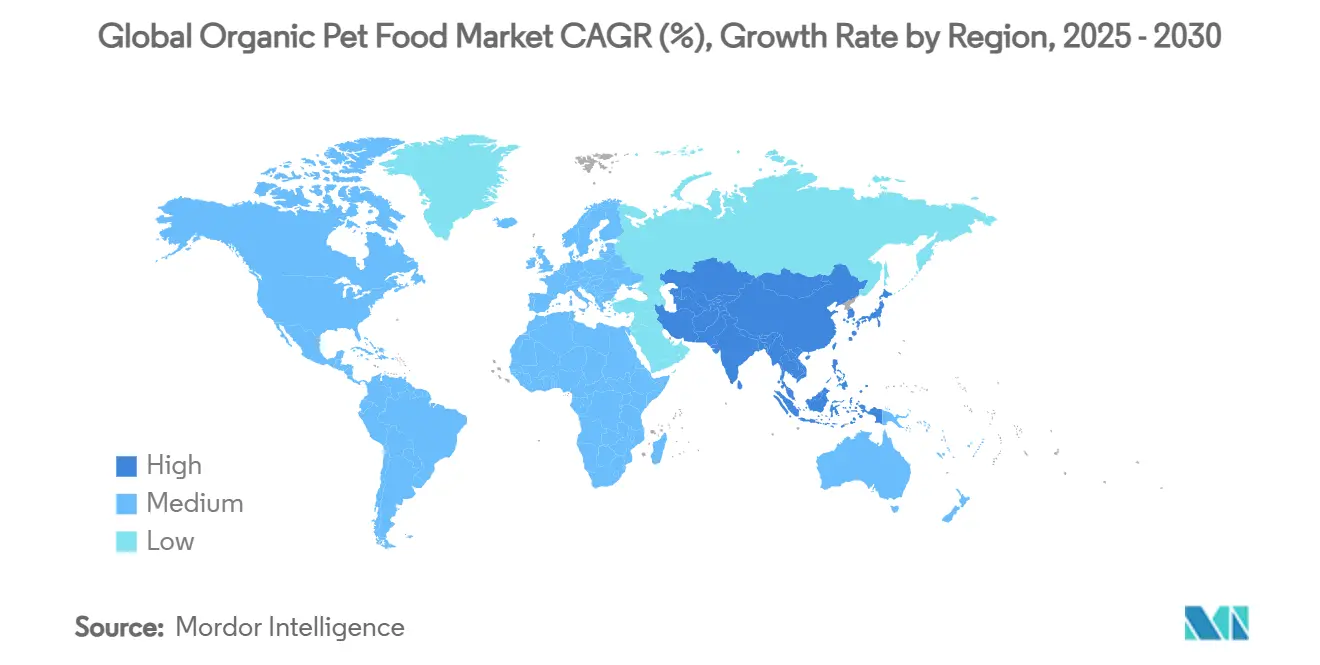

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Pet Food Market Analysis by Mordor Intelligence

The organic pet food market size stands at USD 14.63 billion in 2025 and is projected to reach USD 21.01 billion by 2030, registering a 7.5% CAGR during the forecast period. Demand accelerates as pet owners link diet quality with animal longevity[1]Source: U.S. Department of Agriculture, “China: Pet Food Market Update 2025,” USDA.gov, while the final United States Department of Agriculture (USDA) organic rules, published in December 2024, reduce certification ambiguity and open the door for functional ingredients, such as taurine [2]Source: U.S. Department of Agriculture, “National Organic Program; Market Development for Mushrooms and Pet Food,” Federal Register, USDA.gov . E-commerce subscriptions, premium treats, and novel proteins expand category reach beyond niche natural-food shoppers. North America retains value leadership due to a mature certification infrastructure, yet Asia-Pacific shows the fastest spending gains as urban millennials mirror Western pet-humanization habits. Competitive intensity rises as large packaged-food groups acquire premium start-ups to secure high-margin growth corridors.

Key Report Takeaways

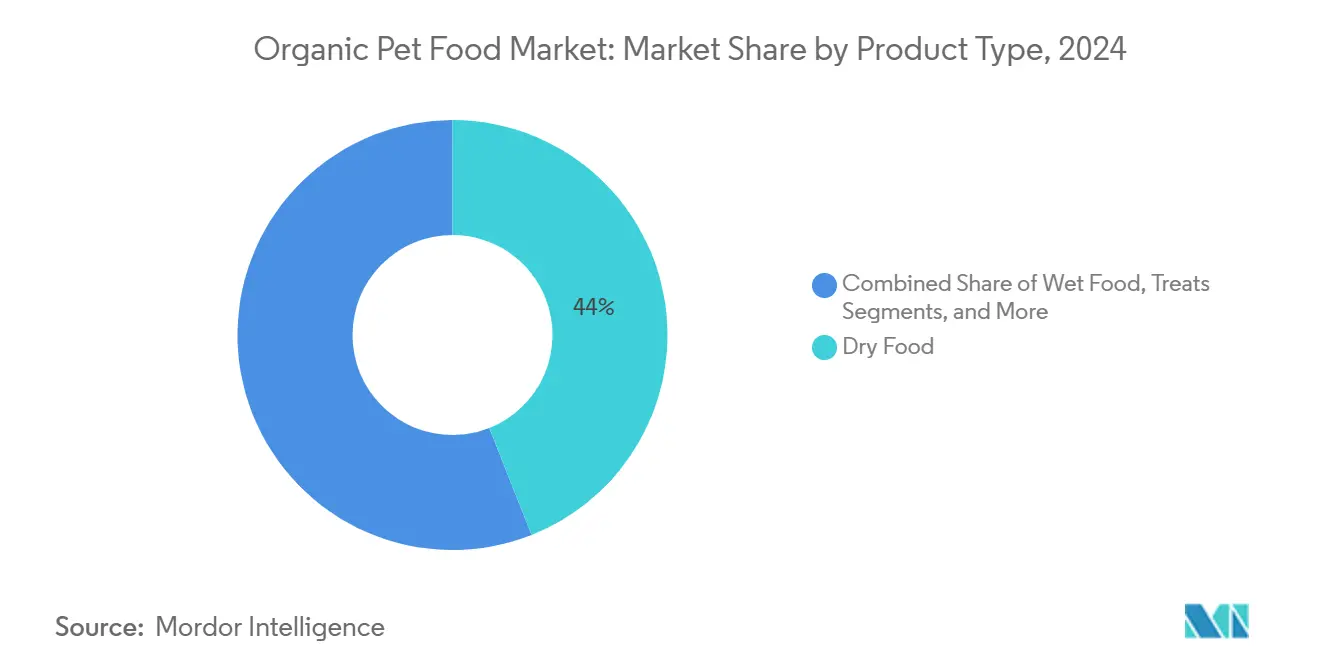

- By product type, dry formulations led with a 44% share of the organic pet food market in 2024, while meal toppers and mixers are forecast to expand at a 10.5% CAGR through 2030.

- By pet type, dog food accounted for a 63% share of the organic pet food market size in 2024, while cat food is projected to advance at a 9.2% CAGR to 2030.

- By packaging type, bags and pouches accounted for about 54% of the organic pet food market share in 2024, and Tetra Packs are projected to grow at a CAGR of 17.4% during the forecast period.

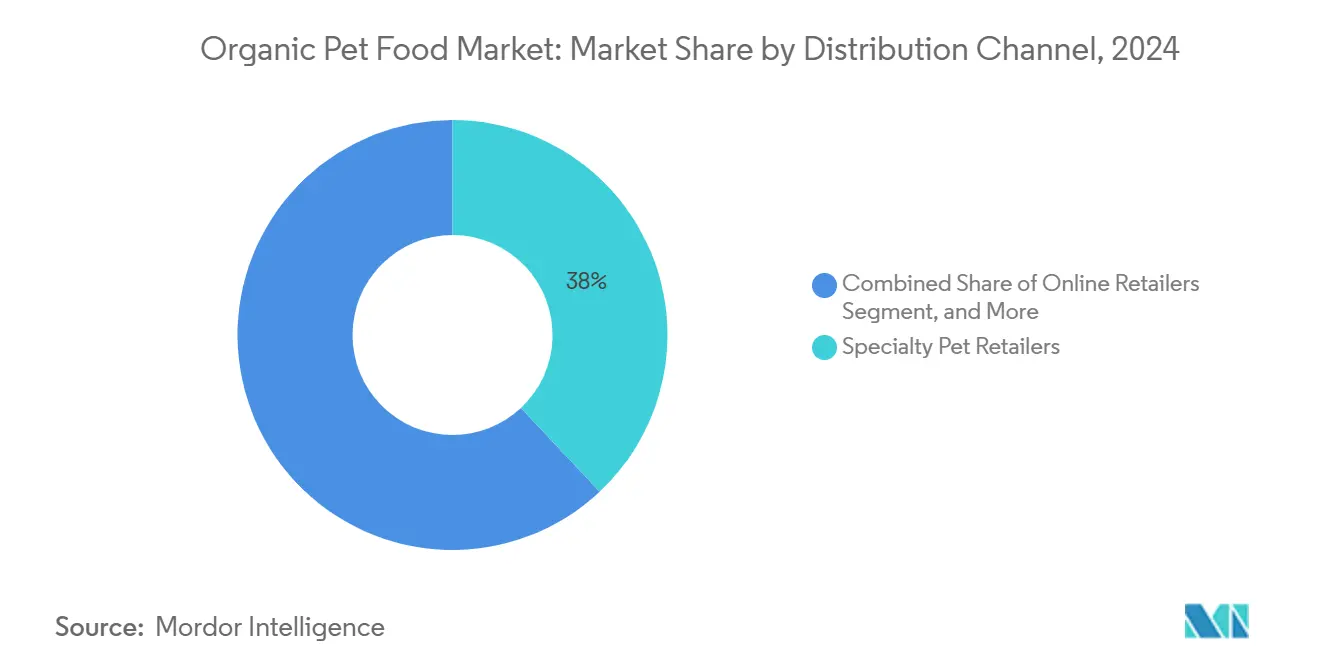

- By distribution channel, specialty retailers held a 38% share in 2024, whereas online retailers are projected to record a CAGR of 11.5% through 2030.

- By geography, North America commanded a 44% share in 2024, while the Asia-Pacific region recorded the fastest trajectory with a 15.6% CAGR.

- Major players include Nestlé Purina, Open Farm, Tender & True, Yarrah Organic, and Smallbatch Pets LLC, holding strong shares in 2024 yet leaving space for newcomers.”

Global Organic Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of pet diets | +3.2% | North America, Europe, and emerging in Asia-Pacific | Medium term (2–4 years) |

| Ingredient transparency from pet humanization | +2.8% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Expansion of organic certification programs | +2.1% | North America and European Union, scaling to Asia-Pacifica | Medium term (2–4 years) |

| Rapid e-commerce penetration | +1.9% | Global, highest in Asia-Pacific | Short term (≤ 2 years) |

| Ingredient Innovation: Novel Organic Proteins | +1.4% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Pet Obesity Concerns Elevating Demand for Clean Labels | +1.1% | Developed markets, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Pet Diets

Globally, premium positioning shifts the organic pet food market from fringe to mainstream as owners equate cost with nutrition quality. Nielsen consumption panels show premium lines will command 60% of the United States' spending by 2030. To justify higher price points, brands add superfoods, single-protein recipes, and recyclable paper-based packs pioneered by Wynn Petfood, responding to the 56% of consumers favoring environmentally responsible packaging. Premiumization also widens average order values in subscription channels, improving lifetime customer value for direct-to-consumer brands.

Ingredient Transparency from Pet Humanization

With 96% of pet owners now viewing pets as family members, organic pet food brands are increasingly adopting human-food vernacular, emphasizing terms like "human-grade," region-of-origin, and QR-code-enabled traceability. This shift reflects a deeper consumer demand for transparency and accountability. Rhodes Pet Science’s Smart Trace Technology exemplifies this trend by delivering lot-level sourcing data, appealing especially to millennial consumers who are skeptical of opaque supply chains. Such transparency not only builds trust but also helps sustain brand loyalty, even in the face of inflationary pressures, by reinforcing perceived product value and ethical alignment.

Expansion of Organic Certification Programs

Implementation of European Union Regulation 2023/2419 in May 2024 requires 95% agricultural inputs to be certified organic, streamlining entry for multinationals that already comply with USDA standards[3]Source: Legislative Train Schedule European Parliament, "Regulation on organic labelling of pet food In Agriculture and Rural Development - AGRI," europa.eu. Open Farm leveraged dual certification plus B Corp status to increase European listings by 22% in 2025. The harmonization of regulatory frameworks significantly reduces duplication in compliance audits, making international certification processes more efficient. This shift not only benefits larger players but also supports small and mid-sized brands by lowering operational barriers, thereby facilitating their export expansion into the European organic pet food market.

Rapid E-Commerce Penetration

Online share of the United States pet products climbed to 44% in 2024, and Asia-Pacific surpassed 50% in cross-border pet-food spend through marketplaces such as JINGDONG. Subscription services cut customer friction, with Stella & Chewy’s seeing a 28% reorder uplift after its 2024 site launch. These digital storefronts empower niche organic pet food labels to bypass traditional slotting fees, instead reinvesting in social media marketing and AI-powered personalization engines that tailor diet plans based on breed, age, and allergy profiles, enhancing both consumer engagement and product relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional food | -2.4% | Global, sharper in price-sensitive markets | Short term (≤ 2 years) |

| Limited organic ingredient capacity | -1.8% | Global, acute in novel proteins | Medium term (2–4 years) |

| Regulatory Patchwork Across Export Markets | -1.2% | International trade corridors, European Union, United States and Canada | Long term (≥ 4 years) |

| Nutritional Density Challenges in Organic Formulations | -0.9% | Global, affecting complete nutrition claims | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium Versus Conventional Food

Organic SKUs frequently command a price premium, often selling at two to three times the cost of conventional formulations, placing added pressure on household budgets, particularly during periods of inflationary volatility. In response, retailers are mitigating sticker shock through tactics such as smaller pack sizes and flexible "mix-and-match" bundle offers, designed to preserve trial and accessibility. On the supply side, manufacturers face difficult cost pass-through decisions, exacerbated by a 7% decline in organic soybean availability and the ongoing burden of freight surcharges, both of which compress margins and complicate pricing strategies.

Limited Organic Ingredient Capacity

Novel organic proteins, such as black soldier fly meal, offer sustainable potential but require specialized processing facilities, which remain limited and geographically concentrated. The implementation of the USDA's Strengthening Organic Enforcement (SOE) rule has introduced 4,000–5,000 additional supply chain certifications, further tightening the short-term availability of compliant raw materials. The American Trucking Association projects a 1.1 million driver shortfall by the end of the decade, fueling spot-rate volatility, especially for refrigerated freight used in organic distribution chains. Together, these dynamics underscore the structural complexities in scaling next-generation organic inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dry Food Retains Scale while Meal Toppers Surge

Dry foods held a 44% organic pet food market share in 2024, due to affordability, shelf stability, and familiarity. The dry food segment grew 6% year-over-year as brand owners fortified recipes with taurine and omega-3s to satisfy complete-nutrition guidelines. Meal toppers and mixers represent the fastest-growing niche, logging a 10.5% CAGR outlook as consumers adopt “build-a-bowl” routines that blend functional freeze-dried pieces with core kibble. The organic pet food market rewards such customization because it raises the average price per pound without burdening owners with full dietary shifts.

Muenster Milling expanded its production capacity with a new Texas facility, featuring 120,000 square feet of space and over 20 freeze-dryers to address increasing demand. Wet and canned organic pet foods maintain their premium positioning through enhanced palatability, particularly benefiting senior pets with dental concerns. The treats and chews segment mirrors human snacking patterns by incorporating functional ingredients such as hemp and turmeric, achieving price points above USD 15 per pound. Manufacturers across all processing methods emphasize gentle cooking techniques to maintain nutrient bioavailability while reinforcing the minimal processing principles of organic pet food production.

By Pet Type: Dogs Dominate Volume, Cats Drive Margin

Dog diets captured 63% of the organic pet food market size in 2024, supported by higher caloric requirements and ongoing premiumization of large-breed formulations. The segment benefits from hybrid feeding trends in which owners mix dry kibble with raw toppers to balance cost and nutrient density. Yet cat food posts the fastest 9.2% CAGR through 2030, powered by rising feline adoption among Gen Z apartment dwellers and the popularity of grain-free, hairball-control organic recipes.

Small-mammal nutrition, though niche, commands premium per-ounce pricing as owners seek soy-free, certified-organic hay blends and fortified pellets. Exotic pet keepers demand limited-ingredient organic formulas to mitigate allergy risks, an angle smaller brands exploit to enter the organic pet food market with minimal marketing budgets. These segments benefit from rising interest in clean-label, species-specific diets and are increasingly supported by online specialty retailers that simplify distribution for emerging brands. Additionally, organic formulations tailored for rabbits, guinea pigs, and reptiles are gaining visibility through influencer content and veterinary endorsements, expanding their reach beyond hobbyist circles.

By Distribution Channel: Specialty Expertise Meets Digital Disruption

Specialty pet retailers held 38% organic pet food market share in 2024, leveraging knowledgeable staff and in-store sampling to justify higher prices. Retail education remains critical for first-time organic buyers who seek feeding-transition guidance. Online retailers, however, are scaling at 11.5% CAGR as Chewy, Amazon, and brand-owned sites offer subscription savings and home delivery convenience that resonate with time-pressed owners.

Native Pet doubled its physical reach via Tractor Supply’s rural network while maintaining a direct-to-consumer storefront, exemplifying the omnichannel imperative. Supermarkets and Hypermarkets push “gateway” organic lines in remodelled natural-foods aisles, converting mainstream shoppers. Veterinary clinics build credibility for therapeutic organic diets targeting allergies and weight management, but shelf space remains limited. As cross-channel buying rises, loyalty shifts from retailer to brand, intensifying competition for search visibility and subscription retention within the organic pet food market.

By Packaging Type: Sustainability Shapes Purchase Decisions

Bags and pouches held 54% of the organic pet food market in 2024. This domination is because they optimize cost-to-protect ratio and handle high-throughput dry-food lines. In 2024, 56% of the United States owners indicated a willingness to switch brands for sustainable packaging, prompting Amcor’s launch of AmLite HeatFlex Recycle-Ready pouches that cut carbon footprint while preserving product freshness.

Tetra packs projected fastest at a CAGR of 17.4% during the forecast period. Wet-food cans guarantee hermetic sealing but face recycling skepticism. Innovators such as Wynn Petfood rolled out 100% paper packs for pâté-style meals, reducing metal reliance. The Pet Sustainability Coalition’s Packaging Pledge pushes brands to meet recycle-ready or compostable criteria by 2025. Bulk refill stations trialed in select European Union pet shops extend zero-waste solutions yet depend on stringent sanitation to maintain organic integrity. Across formats, clear labelling of bio-based inks and resealable closures communicates product safety and elevates brand equity inside the organic pet food market.

Geography Analysis

North America generated the highest revenue and accounted for about 44% of the organic pet food market size in 2024, aided by USDA certification clarity and premium-centric consumer behavior. The United States pet food exports reached USD 2.49 billion in 2024, and the region is forecast to expand through 2030 as suppliers embed regenerative-agriculture claims that resonate with climate-conscious buyers. The organic pet food market benefits from venture capital inflows targeting tech-enabled formulations and AI nutrition tools.

Asia-Pacific is the growth pacesetter with a 15.6% CAGR outlook. This rapid expansion is driven by rising pet humanization in urban centers, particularly in China, India, and Southeast Asia, where middle-class consumers are increasingly prioritizing premium, health-focused diets. The United States organic brands supplied 69% of imported niche diets, underscoring trust in Western safety standards. E-commerce accelerates rural penetration where physical organic assortments remain thin. Rising disposable income and pet-humanization rhetoric translate into premium spending, propelling further regional investments such as Real Pet Food Co.’s insect-protein launch in Australia.

Europe remains the leading market, supported by strong organic legislation that enhances consumer trust. The European Union’s 2023/2419 regulation simplifies labeling requirements, reducing administrative burdens for exporters. Germany, France, and the United Kingdom collectively account for more than half of Europe’s organic pet food sales. In South America, the market is growing rapidly as rising middle-class incomes drive demand for premium products. Local producers are collaborating with the United States co-manufacturers to expedite product launches. The Middle East and Africa are also experiencing steady growth, fueled by increasing expatriate populations and the expansion of specialized pet boutiques across Gulf Cooperation Council countries. This geographically diverse growth creates a complex and attractive opportunity matrix for the organic pet food market.

Competitive Landscape

The organic pet food market shows moderate consolidation, with top manufacturers holding a significant revenue share but still allowing room for emerging players. Nestlé Purina PetCare Company maintains a leading position through premium organic SKUs and partnerships focused on regenerative ingredient sourcing to reduce emissions. Yarrah Organic Petfood B.V., revitalized under new ownership, is expanding its product lines and adopting eco-friendly packaging across Europe. These moves reflect a broader shift toward sustainability-driven value propositions.

Challenger brands are fueling market momentum through innovation and ethical sourcing. Open Farm Pet Food Company Inc. is scaling regenerative agriculture partnerships and introducing plastic-neutral packaging to align with consumer sustainability expectations. Tender & True Pet Nutrition LLC continues to lead in certified organic offerings, now diversifying into heirloom grain and grain-free blends. Smallbatch Pets LLC specializes in organic, fresh-frozen meals and is now launching nutrient-enhanced variants like bone broth-infused recipes.

Regulatory uncertainty is growing, as proposals to rescind dedicated United States Department of Agriculture (USDA) organic pet food standards prompt pushback from leading brands. In response, companies are securing both United States and EU certifications and diversifying sourcing to mitigate risk. The market is also seeing new opportunities in hypoallergenic, ancient-grain formulations and carbon-labeled packaging. These trends support continued growth, innovation, and ESG-aligned differentiation in the organic pet food industry.

Organic Pet Food Industry Leaders

-

Nestlé Purina PetCare Company

-

Open Farm Pet Food Company Inc.

-

Tender & True Pet Nutrition LLC

-

Yarrah Organic Petfood B.V.

-

Smallbatch Pets LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Yarrah Organic Petfood launched recyclable packaging and upgraded organic recipes to reduce its carbon footprint and align with organic sustainability goals.

- July 2024: Open Farm Pet Food Company Inc. achieved B Corp certification, reinforcing its commitment to ethical sourcing and transparency in organic pet food production.

- April 2024: Nestlé Purina PetCare Company launched a USD 30 million regenerative agriculture initiative for organic grain sourcing for pet food manufacturing, supporting farmers transitioning to eco-friendly practices across North America and Europe.

Global Organic Pet Food Market Report Scope

Organic pet food is pet food made from certified organic ingredients produced without synthetic pesticides, chemical fertilizers, genetically modified organisms (GMOs), antibiotics, or artificial additives, and formulated to support pet health and overall nutrition.

The Organic Pet Food Market Report is segmented by Product Type (Dry Food, Wet/Canned Food, Treats and Chews, Meal Toppers and Mixers, and Others), Pet Type (Dogs, Cats, and Other Small Mammals), Distribution Channel (Specialty Pet Retailers, Supermarkets and Hypermarkets, Online Retailers, and Veterinary Clinics), Packaging Type (Bags and Pouches, Cans and Trays, Tetra Packs, and Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Dry Food |

| Wet/Canned Food |

| Treats and Chews |

| Meal Toppers and Mixers |

| Others |

| Dogs |

| Cats |

| Other Small Mammals |

| Specialty Pet Retailers |

| Supermarkets and Hypermarkets |

| Online Retailers |

| Veterinary Clinics |

| Bags and Pouches |

| Cans and Trays |

| Tetra Packs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Dry Food | |

| Wet/Canned Food | ||

| Treats and Chews | ||

| Meal Toppers and Mixers | ||

| Others | ||

| By Pet Type | Dogs | |

| Cats | ||

| Other Small Mammals | ||

| By Distribution Channel | Specialty Pet Retailers | |

| Supermarkets and Hypermarkets | ||

| Online Retailers | ||

| Veterinary Clinics | ||

| By Packaging Type | Bags and Pouches | |

| Cans and Trays | ||

| Tetra Packs | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the organic pet food market?

The organic pet food market size is USD 14.63 billion in 2025 and is projected to reach USD 21.01 billion by 2030.

Which product type leads the market?

Dry food leads with 44% market share in 2024, though meal toppers and mixers show the fastest growth at 10.5% CAGR.

Why is Asia-Pacific the fastest-growing region?

Rising disposable incomes, urban lifestyles, and strong e-commerce logistics drive a 15.6% CAGR for Asia-Pacific through 2030.

What factors restrain market expansion?

Price premiums over conventional food and limited certified-organic ingredient capacity currently dampen wider adoption.

Page last updated on: