Fish Based Pet Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

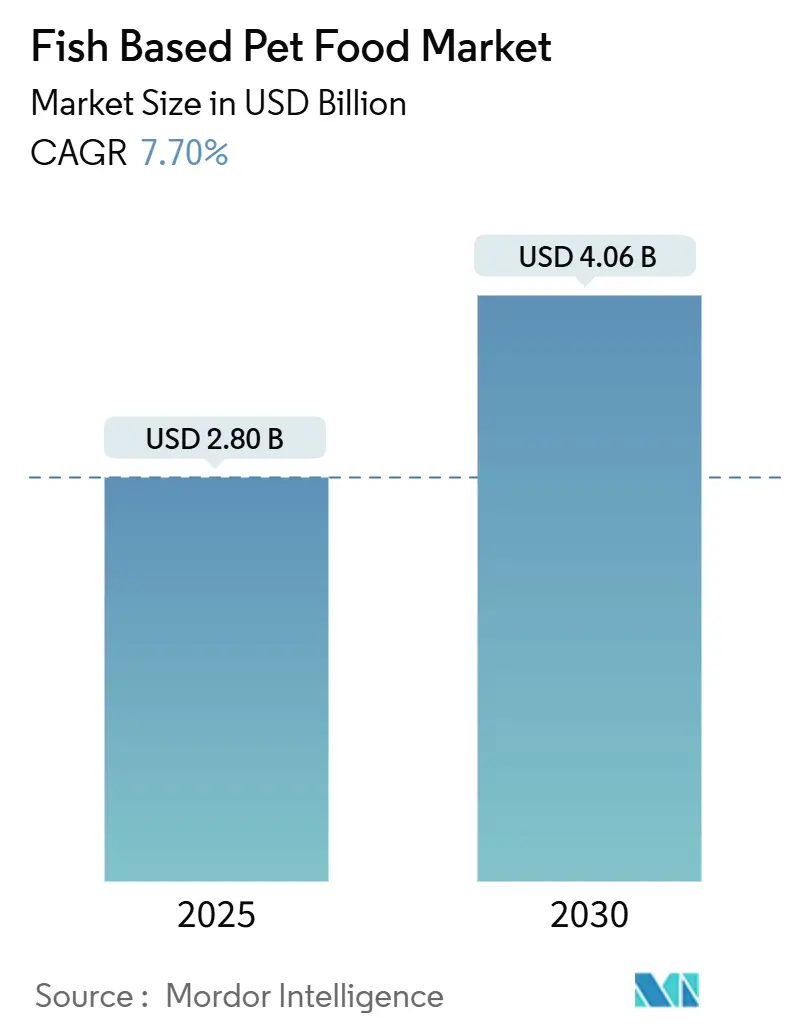

| Market Size (2025) | USD 2.80 Billion |

| Market Size (2030) | USD 4.06 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

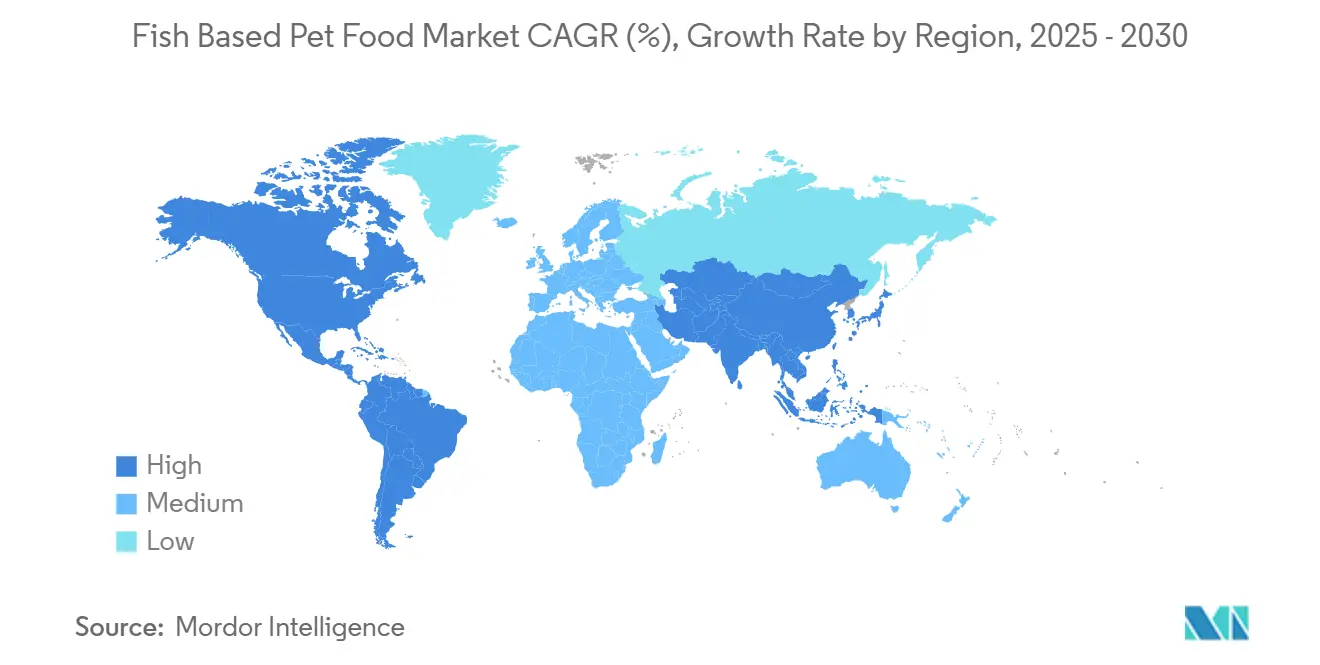

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fish Based Pet Food Market Analysis by Mordor Intelligence

The fish-based pet food market size reached USD 2.8 billion in 2025 and, at a forecast CAGR of 7.7%, is anticipated to advance to USD 4.06 billion by 2030. Momentum in the fish-based pet food market stems from rising omega-3 awareness, the premiumization wave that links pet nutrition to human-grade standards, and better marine-protein processing technologies. Salmon continues to anchor many formulations, yet sardine and herring adoption grows fastest on sustainability and cost advantages. Online channels accelerate the discovery of premium stock-keeping units (SKUs) while freeze-dried technology expands shelf life without preservatives. The regional growth disparity underscores a fundamental shift in global pet food consumption patterns, with emerging markets prioritizing health-focused formulations over traditional offerings. Alongside growth, firms manage supply volatility in Peru’s anchovy fishery and tightening biogenic-amine limits in China and Europe. The industry faces a critical inflection point where sustainable sourcing practices and technological innovation in fish protein processing will determine long-term market leadership positions.

Key Report Takeaways

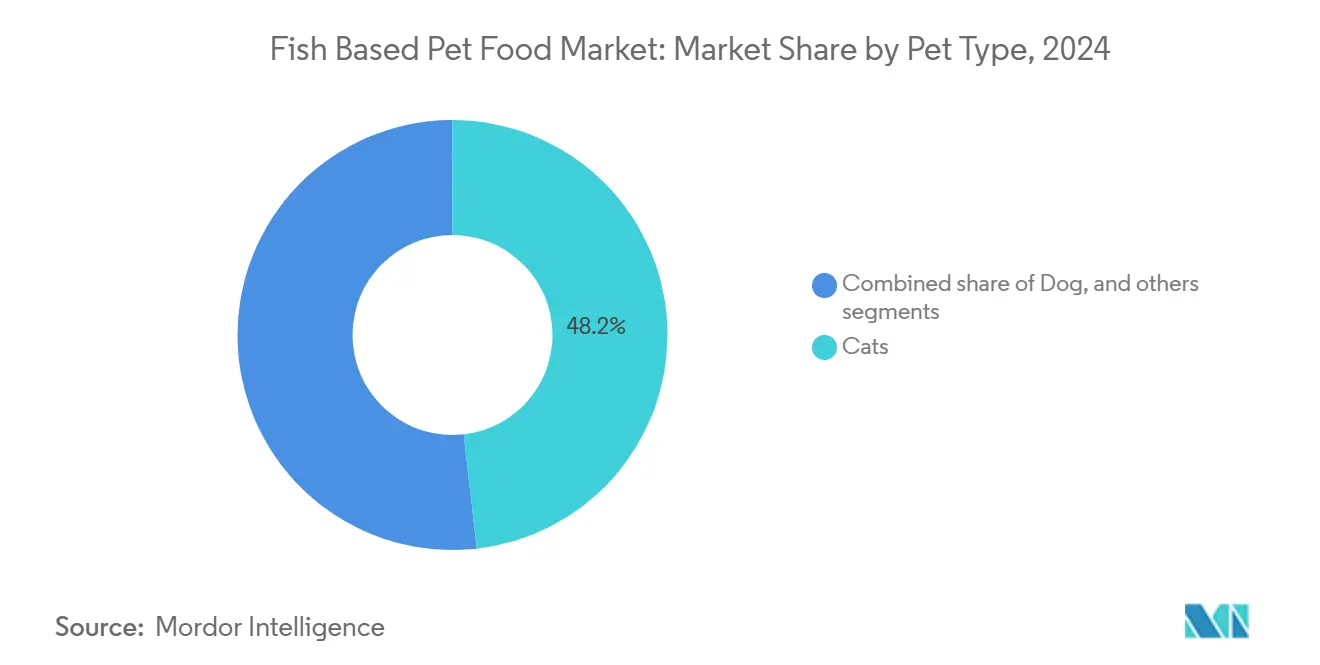

- By pet type, cats held 48.2% of the fish-based pet food market share in 2024, while the feline segment is projected to grow at an 8.5% CAGR through 2030.

- By product form, wet/canned items led with 42.3% revenue share in 2024, and refrigerated/fresh products are forecast to register a 20.2% CAGR between 2025 and 2030.

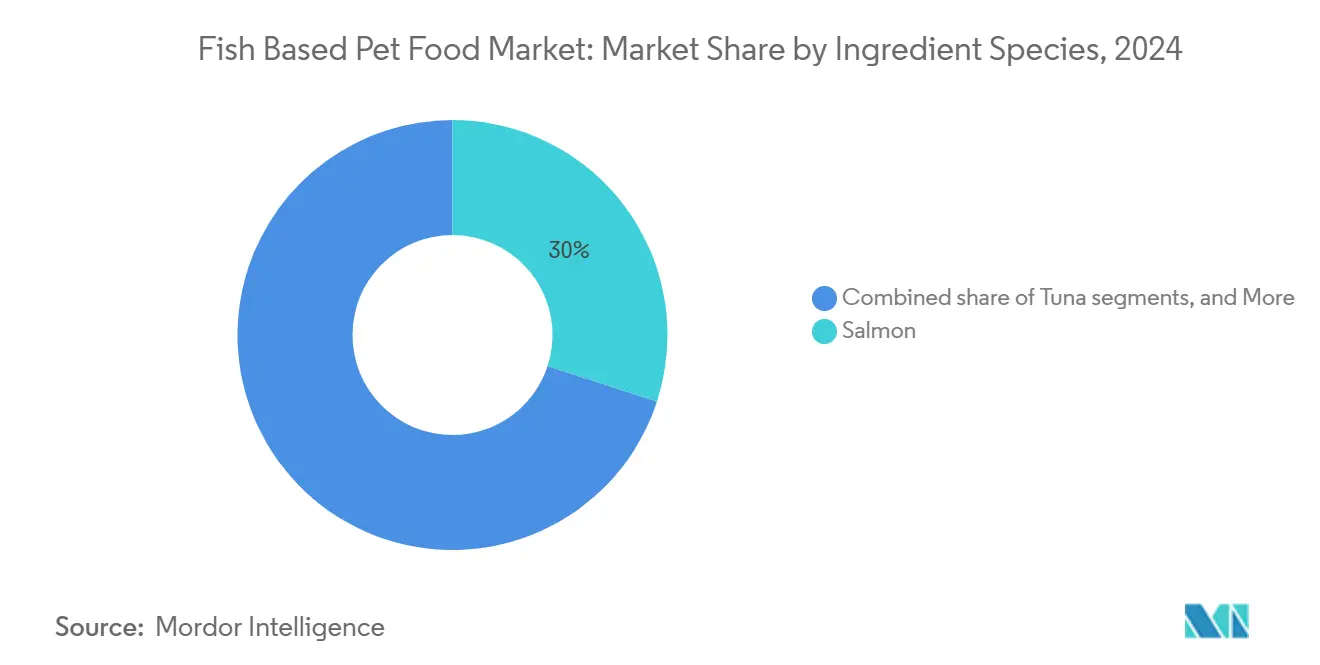

- By ingredient species, salmon accounted for 30% of the fish-based pet food market size in 2024, whereas sardine and herring are positioned for a 10.3% CAGR over the same horizon.

- By distribution channel, online/e-commerce captured 43.2% share of the market size in 2024 and is projected to post a 12.4% CAGR through 2030.

- By geography, North America accounted for 42.5% of the revenue in 2025, while the Asia-Pacific region is projected to expand at a 8.5% CAGR through 2030.

Global Fish Based Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for omega-3 rich diets for skin and coat health | +1.2% | Global, with premium focus in North America and Europe | Medium term (2-4 years) |

| Premiumization and human-grade ingredient trends | +1.8% | North America and Europe primary, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of wet cat food containing marine proteins | +1.5% | Global, particularly strong in developed markets | Short term (≤ 2 years) |

| Upcycling of fish processing by-products reduces raw-material cost | +0.9% | Global, with concentration in major fishing nations | Medium term (2-4 years) |

| Expansion of aquaculture by-product supply chains post-Peru quota reforms | +0.8% | Global supply impact, regional processing benefits | Long term (≥ 4 years) |

| Freeze-dried tech enabling longer shelf life for fish proteins | +1.1% | North America and Europe leading, and Asia-Pacific following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Omega-3 Rich Diets for Skin and Coat Health

Clinical evidence linking EPA and DHA intake to improved dermatological outcomes propels fish-based formulations into daily routines. Veterinarians increasingly specify marine-sourced omega-3s because of superior bioavailability versus plant substitutes. Owners, seeking functional solutions, accept premiums of 15-25% above conventional diets. This convergence elevates the fish-based pet food market as a go-to option for preventive care, reinforcing volume gains across both dry and wet platforms.

Premiumization and Human-Grade Ingredient Trends

Expenditure patterns mirror human food habits, fresh, minimally processed, traceable seafood inputs move from the dinner plate into the bowl. Premium dog and cat food sales rose 5% and 9% respectively, in 2024, while fresh and frozen categories registered 16.1% value growth[1]Source: Jordan Tyler, “Fundamental and functional uses for fats and oils in pet nutrition,” Pet Food Processing, petfoodprocessing.net. The fish-based pet food market benefits directly as brands promote wild-caught or sustainably farmed salmon, tuna, and whitefish that meet human-grade criteria. Start-ups leverage transparency to vie with universals like Mars, Incorporated and Nestlé S.A. (Purina), shifting competition toward storytelling and ingredient ethics.

Growth of Wet Cat Food Containing Marine Proteins

Wet cat food usage stood at 59% of owners in 2024. Taurine, arachidonic acid, and readily digested protein levels in fish validate the format’s biological fit for felines. Odor and texture hurdles that once constrained fish-based kibble are absent in canned products, allowing manufacturers to command 20-30% higher margins. Consequently, the fish-based pet food market records an outsized contribution from wet SKUs and sees ongoing innovation in gourmet textures, pates, and broth-rich recipes.

Upcycling of Fish Processing By-Products Reduces Raw-Material Cost

Turning heads, bones, and trimmings into premium meals boosts recovery rates up to 90% of whole-fish biomass. Brands report raw-material cost cuts of 12-18% after adopting full-stream utilization. Circular messaging resonates with eco-focused buyers, positioning the fish-based pet food market as a sustainability vanguard. Supply partners in Norway, Chile, and Thailand integrate vertically to secure by-product flows, fostering price stability and environmental credentials simultaneously. The trend accelerates as sustainability becomes a key purchasing criterion, with by-product utilization serving as a tangible differentiator in marketing communications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global fishmeal and fish-oil prices | -0.8% | Global, with acute impact on cost-sensitive markets | Short term (≤ 2 years) |

| Sustainability concerns over forage fish stocks | -1.2% | Global, particularly affecting premium segments | Long term (≥ 4 years) |

| Odor-related palatability issues in kibble manufacturing | -0.6% | Global, primarily affecting dry food segments | Medium term (2-4 years) |

| Stricter biogenic amine limits in Europe and China pet-food import rules | -0.9% | Europe and China primarily, spillover to exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Global Fishmeal and Fish-Oil Prices

Peruvian anchovy landings exceeded 4.8 million metric tons in 2024 after a weak 2023, swinging commodity prices sharply[2]Source: Chris Chase, “Peru doubles anchovy quota for first season of 2024,” SeafoodSource, seafoodsource.com. With Peru covering 15-20% of global fishmeal supply, pet food producers face hedge-or-absorb decisions every season. Sudden cost spikes strain premium SKUs where pricing elasticity is thin, challenging margin preservation in the fish-based pet food market. The challenge intensifies as premium pet food segments cannot easily absorb price increases without risking consumer defection to alternative protein sources, creating a strategic dilemma between profitability and market share preservation.

Sustainability Concerns Over Forage Fish Stocks

Growing environmental awareness among pet owners creates pressure for sustainable sourcing practices, with concerns over the depletion of forage fish potentially limiting long-term market expansion. Activist scrutiny drives retailers to conduct thorough sourcing audits, and regulators are eyeing stricter quotas. Brands respond by tapping certified fisheries, blending algae-derived DHA, or spotlighting low-trophic species. Meeting eco-criteria adds compliance costs yet also differentiates offerings within the fish-based pet food market. The emergence of alternative protein sources, including marine micro-algae for omega-3 production, offers potential solutions but requires significant investment in new supply chains and consumer education to achieve market acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Cats Drive Marine Protein Adoption

Cats accounted for 48.2% of the fish-based pet food market size in 2024, and with an 8.5% CAGR outlook, they anchor future demand. Taurine, DHA, and arachidonic acid, naturally abundant in fish, align with feline physiology, making marine ingredients a near-default option. Usage of wet cat food incorporating salmon, tuna, and sardines rose sharply, signaling sustained brand investment. Dogs retain a majority of volume but slower growth, relying on omega-3 positioning rather than species-specific necessity.

The cat-centric dynamic widens, and premiumization owners accept higher price points for arthritis relief, glossy coats, and reduced shedding. In the Asia-Pacific region, cultural affinity between cats and fish intensifies market penetration, with Japanese and Chinese processors tailoring sardine and mackerel pâtés for local taste expectations. Specialty boutiques highlight feline-only recipe lines, enhancing shelf differentiation across the fish-based pet food market.

By Product Form: Fresh Formats Challenge Traditional Leadership

Wet/canned goods held 42.3% of the fish-based pet food market share in 2024. However, refrigerated and fresh chubs, rolls, and patties are projected to grow at a 20.2% CAGR, signaling a shift in consumer preferences. In 2021, Freshpet’s USD 975.2 million in sales underscored category credibility, with fish-inclusive SKUs propelling the brand.

The transition to chilled cases reflects a humanization trend, where buyers seek short ingredient lists and are drawn to real salmon fillets visible through transparent packaging. Dry kibble still maintains a strong presence in the pantry for convenience, although the high fish load limits odor management. Freeze-dried chunks bridge the gap by offering shelf stability without compromising nutrient density, nudging incremental penetration in the fish-based pet food market.

By Ingredient Species: Salmon Dominance Faces Emerging Challengers

Salmon captured 30% of the fish-based pet food market size in 2024. Familiarity, fatty-acid density, and consistent supply keep it center stage across premium and mainstream lines. Yet sardine and herring track a 10.3% CAGR as sustainability metrics become purchasing filters. Their lower trophic level reduces ecological impact while delivering higher EPA/DHA ratios, enabling marketers to pitch “greener” omega-3 packages.

Tuna retains relevance in feline pouches, especially in the Asia-Pacific region. Whitefish variants, such as cod and pollock, serve value tiers without abandoning their marine positioning. Interest in novel species, such as mackerel, anchovy, or even invasive carp, signals proactive diversification to mitigate single-species exposure, a strategic hedge within the fish-based pet food market.

By Distribution Channel: E-commerce Transforms Market Access

Online platforms held 43.2% revenue in 2024 and posted the highest 12.4% CAGR forecast. Automatic reorder programs, ingredient explainers, and user reviews lower trial barriers for pricey fish SKUs. Specialty pet stores continue to showcase refrigerated ranges, leveraging consultative selling for therapeutic diets. Mass retail answers convenience seekers with combo offers bundling salmon kibble and wet toppers.

The United States online pet food sales already exceed USD 21 billion. In China, online penetration is headed toward 54% by 2025. Smaller labels exploit drop-shipping to niche audiences sensitive-skin or weight-management blends, tilting competitive parity across the fish-based pet food market.

Geography Analysis

North America commanded 42.5% of revenue in 2025, buoyed by premium willingness to pay and widespread vet endorsement of fish-based prescription diets. Robust logistics handle refrigerated SKUs, and e-commerce penetration tops global averages. The United States manufacturers also serve export demand, outbound shipments to Asia-Pacific climbed as Chinese tariffs eased[3]Source: Food and Agriculture Organization Correspondent, “Peruvian anchovy TAC highest since 2011,” Food and Agriculture Organization, fao.org. Canada mirrors preferences for salmon and trout, while Mexico’s rising middle class pushes adoption of tuna-infused recipes.

Asia-Pacific stands out with an 8.5% CAGR to 2030, underpinned by demographic and cultural forces. Regional processors in Thailand and New Zealand leverage abundant fisheries to export canned fish diets, amplifying supply chain agility within the fish-based pet food market. Europe offers a sophisticated yet regulation-heavy environment. Consumers scrutinize MSC labels and expect verified low biogenic-amine levels, especially in salmon pâtés.

Brands comply with rising sustainability benchmarks, often blending algae-derived DHA to offset forage fish pressure. Eastern Europe opens incremental volume as disposable income expands. South America, led by Brazil and Chile, benefits from local fishing economies, and chilled salmon rolls gain shelf space in high-end outlets. The Middle East and Africa display nascent but rising demand. Affluent Gulf households favor imported tuna mousse, while South Africa’s coastal fisheries feed local kibble production.

Competitive Landscape

The fish-based pet food market remains moderately consolidated, with Mars, Incorporated and Nestlé S.A. (Purina) dominating scale-driven procurement, alongside 22 United States firms that exceed USD 100 million in annual turnover. Vertical integration into fisheries and rendering plants secures access to raw materials and ensures biosafety control. Mars’ R&D hub in Thailand customizes palatability for Asian pets, testing recipes with 100 cats and 50 dogs in 2023. Nestlé S.A. (Purina) ramps launch cadence for salmon-rich Pro Plan LiveClear extensions targeting allergy-relief claims.

Mid-tier challengers, such as Freshpet, leverage refrigerated innovation, converting 27.2% sales growth into a USD 46.9 million net income in 2024. General Mills’ USD 1.45 billion pickup of Whitebridge adds fish broth and pate capabilities across Europe, underscoring consolidation aimed at premium niches. Ingredient suppliers like Pelagia and Cargill Incorporated expand fishmeal capacity, ensuring continuity for specialty recipes. Biotech start-ups collaborate on cultivated fish proteins, promising scalable, antibiotic-free inputs that could disrupt sourcing conventions inside the fish-based pet food market.

Strategic themes revolve around sustainability certification, transparent supply mapping, and technology that minimizes odor while preserving omega-3 potency. Brands differentiate through trace-back QR codes, single-species formulations for allergy management, and eco-packaging to meet retail mandates. Competitive intensity thus pivots from price toward values and science-backed functionality.

Fish Based Pet Food Industry Leaders

Thai Union Group PCL

Hill’s Pet Nutrition (Colgate-Palmolive)

Nestlé S.A. (Purina)

General Mills, Inc.

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ADM established a manufacturing facility in Yecapixtla, Mexico, with a USD 39 million investment. The plant produces wet pet food, including fish-based products. The company aims to meet 50% of Mexico's wet pet food demand through local production by 2025, reducing the country's dependence on French imports.

- June 2024: Mars, Incorporated's USD 1 billion digital investment aims to boost online premium pet food sales, including fish-based products, and drive growth in this segment.

- April 2024: Nestlé S.A. (Purina) approved a USD 195 million expansion at its Jefferson, Wisconsin, site, boosting wet food output for Pro Plan and Fancy Feast by nearly 50% and creating 100 jobs.

- July 2023: Hill's Pet Nutrition launched Science Diet Sensitive Stomach and Skin formulas containing Marine Stewardship Council (MSC) certified Alaskan Pollock. The wild-caught Alaskan Pollock provides protein and Omega-3s while aligning with environmental sustainability goals.

Global Fish Based Pet Food Market Report Scope

| Dogs |

| Cats |

| Other Companion Animals |

| Dry Kibble |

| Wet/Canned |

| Freeze-Dried and Air-Dried |

| Refrigerated/Fresh |

| Salmon |

| Tuna |

| Whitefish |

| Sardine and Herring |

| Other Fish Species |

| Specialty Pet Stores |

| Supermarkets and Hypermarkets |

| Online/E-commerce |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Other Companion Animals | ||

| By Product Form | Dry Kibble | |

| Wet/Canned | ||

| Freeze-Dried and Air-Dried | ||

| Refrigerated/Fresh | ||

| By Ingredient Species | Salmon | |

| Tuna | ||

| Whitefish | ||

| Sardine and Herring | ||

| Other Fish Species | ||

| By Distribution Channel | Specialty Pet Stores | |

| Supermarkets and Hypermarkets | ||

| Online/E-commerce | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

Which regions will add the most revenue to fish-based pet food between 2025 and 2030?

Asia-Pacific shows the fastest rise at an 8.5% CAGR, driven by pet humanization in China, Japan, and India.

How important is e-commerce to fish-focused pet food sales?

Online channels already hold 43.2% share and a 12.4% CAGR, making digital the primary growth engine for premium marine diets.

Why are sardine and herring gaining space versus salmon?

Higher omega-3 density, lower ecological impact, and cost advantages give sardine and herring a projected 10.3% CAGR through 2030.

What supply risk most affects manufacturers?

Volatile fishmeal and fish-oil prices linked to Peru's anchovy catch can compress margins in the short term.

How are brands addressing sustainability scrutiny?

Companies pursue MSC certification, integrate by-product upcycling, and explore algae or cultivated fish proteins to satisfy eco-driven buyers.

Page last updated on: