Pet Food Premix Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

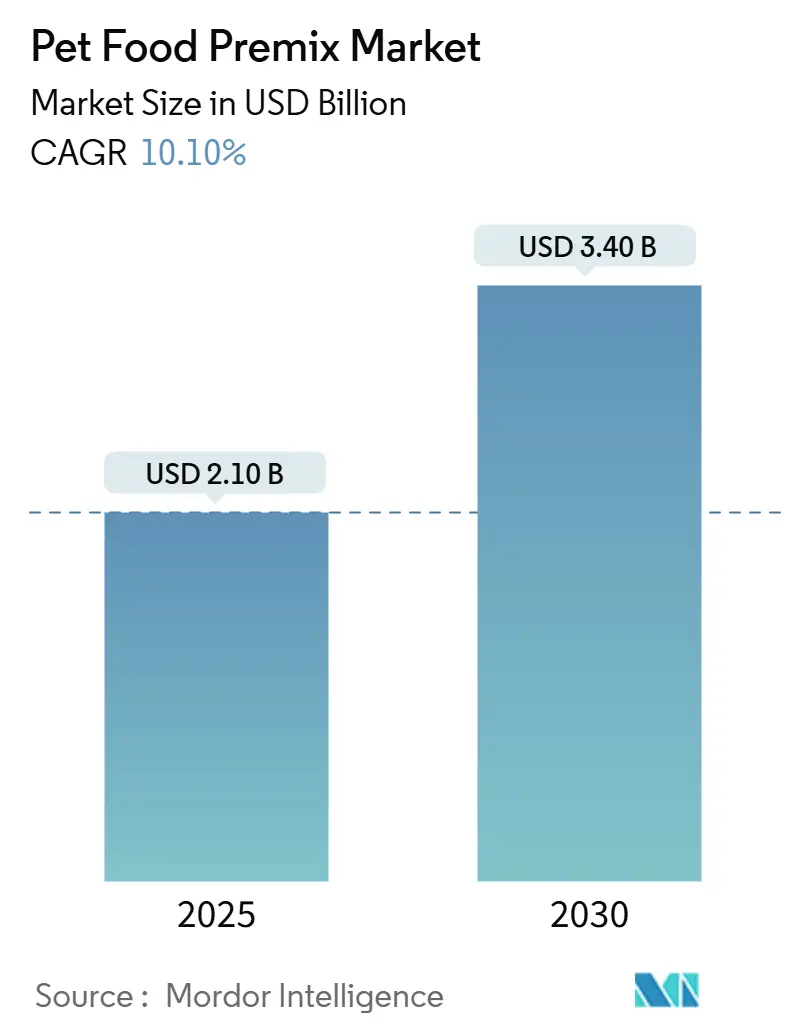

| Market Size (2025) | USD 2.10 Billion |

| Market Size (2030) | USD 3.40 Billion |

| Growth Rate (2025 - 2030) | 10.10% CAGR |

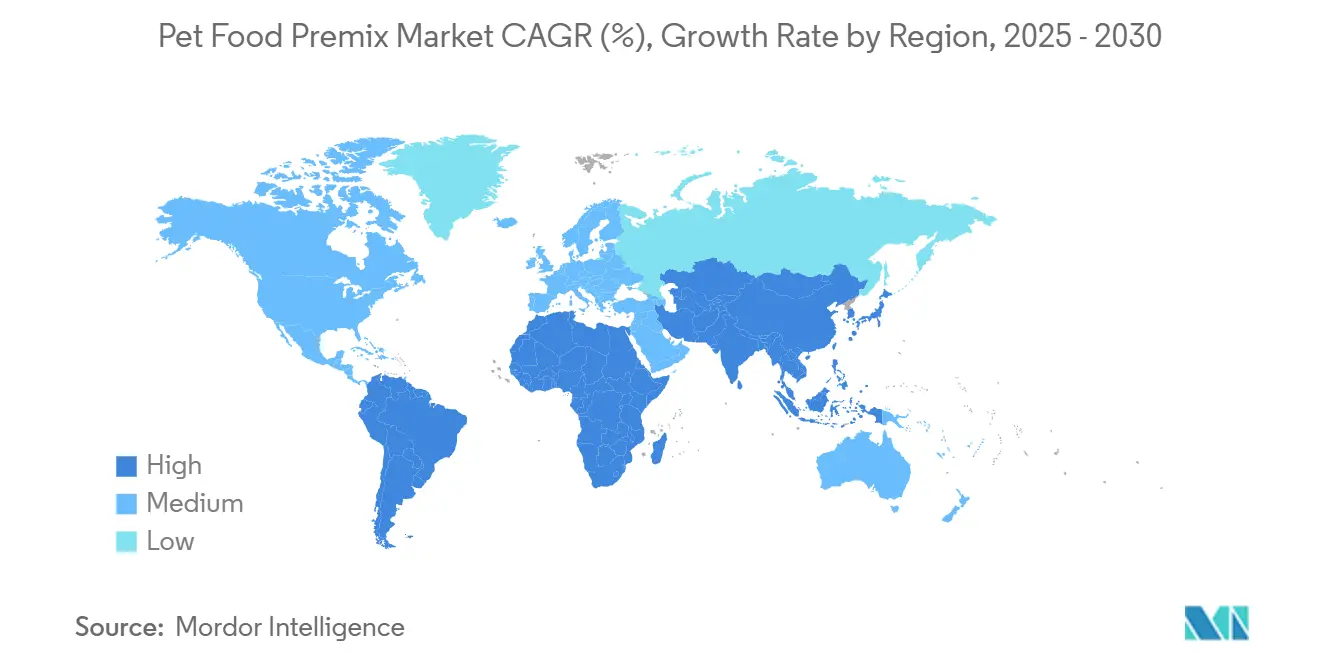

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pet Food Premix Market Analysis by Mordor Intelligence

The pet food premix market size reached USD 2.1 billion in 2025 and is projected to advance at a 10.1% CAGR to USD 3.4 billion by 2030. Growth comes from pet humanization, owner awareness of preventive health, and improved nutrient-stabilization technologies that allow premium micronutrients to survive extrusion. Owing to expanding middle-class pet ownership and rising disposable income Asia-Pacific region demonstrates an impressive growth rate. Vitamins and minerals provide an essential baseline, yet probiotics and prebiotics post the fastest uptake as manufacturers use advanced encapsulation to protect live cultures in dry kibble. Dogs remain the leading pet type, though cat formulations are expanding swiftly on the back of species-specific taurine and amino-acid requirements. Competitive advantage now hinges on proprietary stabilization technologies and regional blending capacity that keep micronutrients potent while reducing freight cost exposure.

Key Report Takeaways

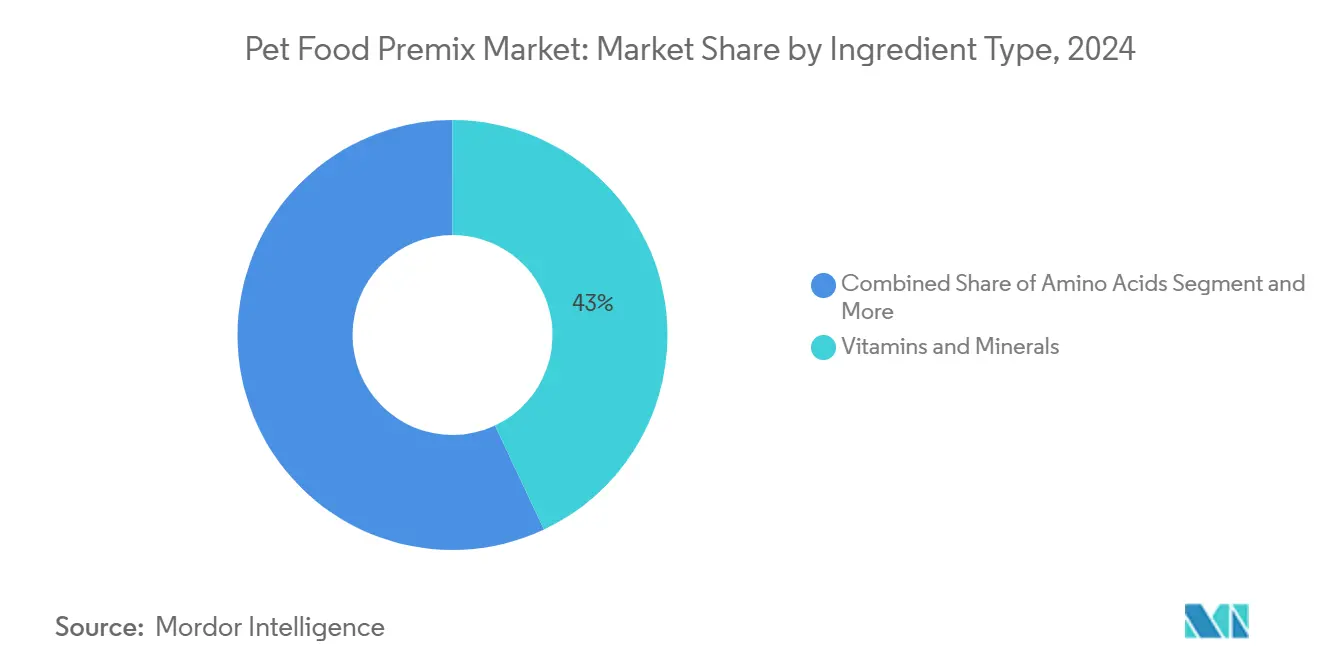

- By ingredient type, vitamins and minerals led with 43% revenue share in 2024, probiotics and prebiotics are forecast to expand at a 13.4% CAGR through 2030.

- By form, powder premixes captured 61% of the pet food premix market share in 2024, while liquid formulations recorded the highest projected CAGR at 11.8% through 2030.

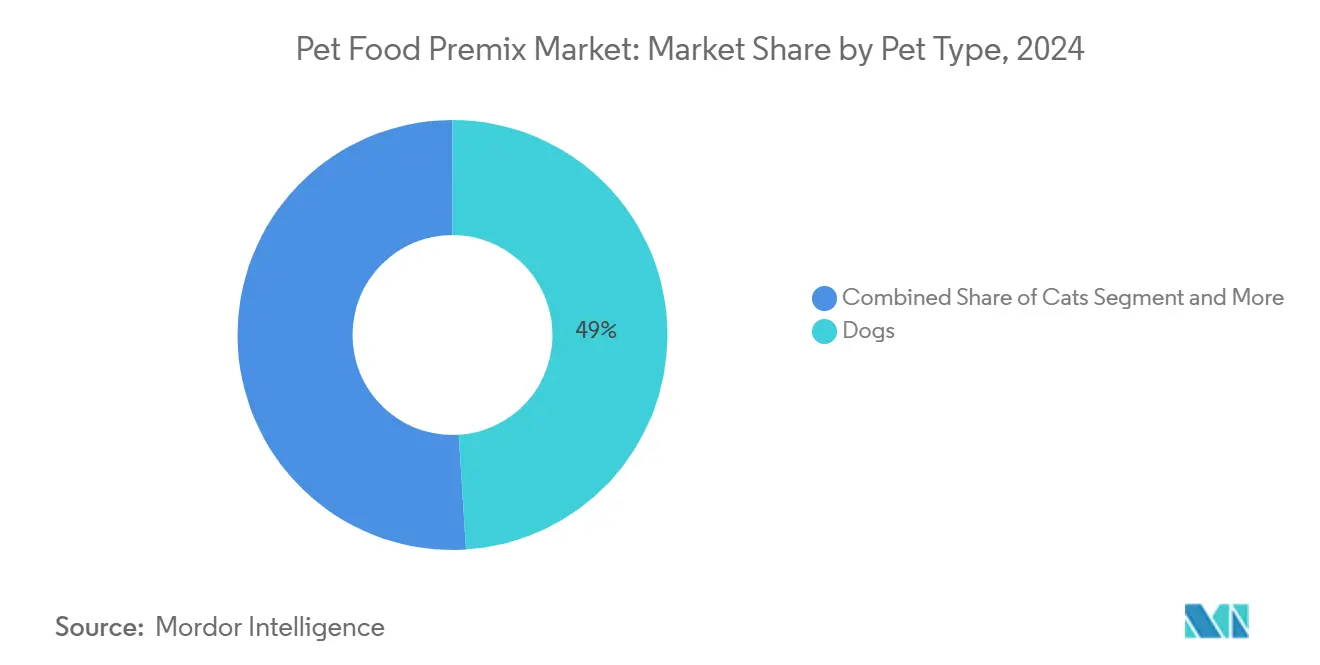

- By pet type, dogs commanded a 49% share of the pet food premix market size in 2024, and cats are advancing at a 12.2% CAGR through 2030.

- By functionality, digestive health premixes accounted for 32% of the market in 2024 and are projected to grow at a 14.7% CAGR to 2030.

- By geography, North America held 38% of 2024 revenue, while Asia-Pacific exhibits the fastest growth at 12.9% CAGR to 2030.

Global Pet Food Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization of pets driving demand for functional nutrition | +2.80% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of pet obesity and chronic diseases | +2.10% | North America and Europe primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward premium and natural formulations | +1.90% | Global, led by developed markets | Short term (≤ 2 years) |

| Rapid pet ownership growth in emerging economies | +1.70% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Demand for stability-enhanced probiotics in extruded kibbles | +1.20% | Global, with early adoption in North America | Medium term (2-4 years) |

| Expansion of private-label blending capacity | +0.80% | Europe primarily, with spillover to Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Humanization of Pets Driving Demand for Functional Nutrition

Pet owners increasingly treat animals like human family members, prompting interest in human-grade ingredients and clinically supported functional claims. Premix blends now combine omega-3s for cognition, antioxidants for aging support, and amino-acid profiles that match breed predispositions.[1]Source: ADM, “Five Trends Influencing Pet Nutrition Health and Wellness,” adm.com Packaging and marketing echo human dietary supplements, pushing premium price points close to 40% above mass formulations. Suppliers invest in research hubs that parallel human nutrition labs so that pet brands can substantiate structure-function messaging. Urban households with smaller family sizes pay for premium diets, accelerating spending in markets where pets substitute for traditional leading roles. This shift pivots demand away from basic vitamin-mineral blends and toward targeted health optimization that drives value capture for technological innovators in the pet food premix market.

Rising Prevalence of Pet Obesity and Chronic Diseases

More than 60% of dogs and cats in developed regions are overweight or obese, creating sustained demand for therapeutic nutrition. Premix suppliers formulate micronutrient ratios that support weight management and chronic-condition diets by incorporating chromium for glucose metabolism, glucosamine precursors for joints, and L-carnitine for fat oxidation. Therapeutic kibble commands 3-4 times the price of maintenance diets, offsetting higher ingredient and testing costs. Regulatory approval for veterinary nutrition remains lighter than pharmaceuticals, allowing quicker go-to-market timelines. An aging pet population assures continued volume growth as senior animals require intensive nutritional support throughout life stages.

Shift Toward Premium and Natural Formulations

Consumers scrutinize ingredient panels and prefer naturally derived micronutrients even when cost premiums reach 25-35%. Natural vitamin E extracted from vegetable oils is priced 3-5 times above synthetic but enables clean-label claims. Suppliers therefore secure specialty sourcing contracts and install analytical labs that verify isotopic signatures, confirming natural origin. Organic certification compounds complexity by mandating segregated lines and exhaustive documentation that small blenders struggle to finance. Freeze-dried and raw food segments intensify this trend because their gentle processing protects heat-sensitive natural vitamins.

Rapid Pet Ownership Growth in Emerging Economies

Urbanization and income growth across Asia-Pacific, South America, and Africa push double-digit pet population gains, especially in China and India. Early demand centers on affordable vitamin-mineral premixes that guarantee nutritional adequacy. As markets mature, consumers migrate toward functional formulations, unlocking margins for suppliers that invested early in localized production. Currency volatility and import tariffs heighten the importance of regional blending facilities able to deliver cost-optimized solutions with shorter lead times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in vitamin and amino-acid raw-material prices | -1.80% | Global, with highest impact in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent regulatory and labeling requirements | -1.20% | North America and Europe primarily | Medium term (2-4 years) |

| Limited shelf-life compatibility of novel fatty-acid premixes | -0.90% | Global, affecting premium segments | Long term (≥ 4 years) |

| Capacity bottlenecks for ultra-trace mineral blending | -0.70% | Global, concentrated in specialized facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Vitamin and Amino-acid Raw-material Prices

Vitamin B-complex and amino-acid costs swing 30-50% each year because supply remains concentrated in China, where periodic environmental shutdowns squeeze output. Suppliers must carry higher inventories to buffer shocks, yet pet food makers resist price hikes, compressing margins. Currency movements further complicate planning when purchases are denominated in USD but sales occur in local currencies. Some large players explore backward integration, although capital intensity restricts this path to a few global giants.

Stringent Regulatory and Labeling Requirements

Divergent rules across the Association of American Feed Control Officials (AAFCO) and the European Pet Food Industry Federation (FEDIAF) raise complexity and add six to twelve months to development cycles for functional ingredients that lack extensive safety dossiers. Compliance for a novel component can cost USD 100,000-500,000 per jurisdiction, elevating barriers for smaller blenders and delaying innovation rollouts. Multiple formulation variants are required to meet region-specific nutrient maximums and labeling protocols, reducing economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Functional Probiotics Outpace Core Vitamins

Vitamins and minerals supplied 43% of 2024 revenue and remain essential to baseline nutrition in every pet food premix market segment. Probiotics and prebiotics, though starting from a smaller base, are forecast to expand at a 13.4% CAGR as encapsulation methods now protect live cultures through extrusion, positioning digestive health as a mainstream benefit. Amino-acid blends held a significant share by addressing species-specific needs such as taurine for cats and arginine for canine cardiac support.

Competitive differentiation in this segment hinges on controlled-atmosphere logistics that maintain probiotic viability end-to-end, a capability possessed by only a few multinationals. Price volatility associated with vitamin and amino-acid inputs, especially those sourced from China, generates margin risk but also justifies diversification into higher-margin functional blends. Suppliers able to lock in multi-year contracts and manage cold-chain requirements gain bargaining power with brand owners that cannot afford nutrient failures in finished foods.

By Form: Liquid Premixes Gain Ground

Powder blends constituted 61% of 2024 sales within the pet food premix market because they integrate smoothly into dry kibble lines and maintain a long shelf life. Liquid premixes are set to grow 11.8% annually as wet pet foods extend their footprint and liquid carriers improve nutrient dispersion in high-moisture matrices. Base blends comprised the significant share, functioning as carriers that dilute ultra-potent actives before inclusion in final formulas.

Liquid progress reflects better bioavailability and ease of homogeneous mixing, especially for senior pet diets that demand pre-dissolved nutrients. Manufacturing requires stainless transfer lines, emulsification equipment, and microbiological controls not universally available. Only suppliers that invest in liquid-handling tanks, in-line homogenizers, and stringent cleaning validation can capture this growth, reinforcing moderate consolidation across the pet food premix industry.

By Pet Type: Cats Drive Future Revenue

Dogs dominated demand with 49% of global share in 2024, mainly due to higher feed volumes per animal. Cats register a 12.2% CAGR through 2030, reflecting apartment-friendly ownership trends and species-specific nutrient needs. Cat-focused premixes command premiums because formulas must supply biologically active vitamin A and high taurine levels.

Rising feline ownership in high-rise urban centers augments growth, pushing brand owners to partner with blenders that master these precise nutrient targets. Small mammal and avian segments remain niche yet profitable niches for companies that can tailor micro-batch runs of specialized blends.

By Functionality: Digestive Health Leads

Digestive health premixes held a 32% share and are set to expand 14.7% annually as gut microbiome science gains mainstream acceptance among pet owners. The digestive category benefits from clear clinical endpoints such as fecal quality and pathogen reduction, allowing robust marketing claims.

Probiotic inclusion in dry kibble elevates entry barriers, consolidating share among suppliers that command proprietary encapsulation. Immune blends gain momentum as pandemic-era consumer habits persist, encouraging formulations that combine antioxidants, colostrum, and functional mushrooms in a single premix.

Geography Analysis

North America commands the largest slice of the pet food premix market with a 38% share in 2024. High per-capita pet spending, consumer readiness to pay premiums for therapeutic formulas, and shorter regulatory timelines under AAFCO (Association of American Feed Control Officials) underpin ongoing momentum. Manufacturing clusters in the Midwest leverage proximity to grain processors and existing animal feed infrastructure, which helps contain logistics costs for national brands.

Europe holds a significant market share, as clean-label preferences gain traction among German, French, and British consumers. Eastern European toll blending offers 20-30% cost savings, allowing multinationals to redirect capital toward high-value functional premixes produced in Western plants. Harmonized European Union regulations simplify cross-border trade but lengthen approval cycles for novel actives, placing a premium on regulatory expertise.

Asia-Pacific is the fastest-rising territory, expanding at 12.9% CAGR on urbanization, middle-class expansion, and pet humanization in China and India. Domestic production capacity is scaling quickly because tariffs and foreign-exchange swings inflate landed costs for imported blends. Suppliers that entered early through joint ventures now enjoy entrenched relationships and brand loyalty, giving them a springboard as functional categories take off.

Competitive Landscape

The pet food premix market exhibits moderate concentration. DSM-Firmenich leads with a significant share, leveraging over forty plants worldwide and proprietary RoviPet stabilization that protects heat-labile micronutrients.[2]Source: DSM, “Pet Nutrition and Health Solutions,” dsm.comOther key players include Nutreco N.V. , Cargill, Incorporated, Nutra Blend LLC, and ADM's (Archer Daniels Midland) Wisium division. Competitive differentiation revolves around vertical integration, microencapsulation patents, and geographic reach that supports just-in-time delivery. ADM (Archer Daniels Midland) has expanded its pet nutrition capabilities by opening a new premix production line at its facility in Chierry, France, to address the growing demands of pet owners.[3]Source: ADM, "Premix Remix: New Pet Food Production Line Opens in France" adm.com

Strategic movements concentrate on regional capacity expansion. MIAVIT acquired a Serbian mixer to exploit cost arbitrage in Eastern Europe. Suppliers heavily invest in R&D to extend the shelf life of probiotics and omega-3s. The race to master ultra-trace mineral blending continues as demand grows for selenium and iodine inclusions tailored to senior pet and breed-specific formulas.

Private-label growth in Europe and North America spreads demand across both commodity and premium tiers, forcing suppliers to maintain flexible production lines that can switch between high-volume vitamin premixes and specialty micro-batches. Relentless raw-material volatility spurs some market leaders to explore backward integration into vitamin synthesis, though high capital outlays and regulatory hurdles deter smaller competitors.

Pet Food Premix Industry Leaders

-

DSM-Firmenich AG

-

Nutra Blend LLC (Land O’Lakes, Inc)

-

Cargill, Incorporated

-

Nutreco N.V.

-

ADM (Archer Daniels Midland)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: DSM announced plans to build a premix plant for the pet food industry in Tonganoxie, supported by the KC Animal Health Corridor.

- October 2022: ADM expanded its pet nutrition capabilities by opening a new premix production line at its facility in Chierry, France, to address the growing demands of pet owners.

Global Pet Food Premix Market Report Scope

| Vitamins and Minerals |

| Amino Acids |

| Probiotics and Prebiotics |

| Nucleotides |

| Specialty Botanicals |

| Powder Premix |

| Liquid Premix |

| Base Blend |

| Dogs |

| Cats |

| Fish and Aquatics |

| Birds and Small Mammals |

| Equine |

| Digestive Health |

| Immune Support |

| Joint and Mobility |

| Skin and Coat |

| General Wellness |

| North America | United States |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Ingredient Type | Vitamins and Minerals | |

| Amino Acids | ||

| Probiotics and Prebiotics | ||

| Nucleotides | ||

| Specialty Botanicals | ||

| By Form | Powder Premix | |

| Liquid Premix | ||

| Base Blend | ||

| By Pet Type | Dogs | |

| Cats | ||

| Fish and Aquatics | ||

| Birds and Small Mammals | ||

| Equine | ||

| By Distribution Channel | Digestive Health | |

| Immune Support | ||

| Joint and Mobility | ||

| Skin and Coat | ||

| General Wellness | ||

| Geography | North America | United States |

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the pet food premix market in 2025 and anticipated market size for 2030?

The pet food premix market size is USD 2.1 billion in 2025 and is anticipated to reach USD 3.4 billion by 2030.

Which region holds the largest share of premix demand?

North America leads with 38% of global revenue due to high pet spending and rapid functional-food adoption.

Why are probiotics driving growth in pet premixes?

Encapsulation advances allow live cultures to survive extrusion, making digestive-health claims feasible in dry kibble, which dominates pet food sales.

What is the fastest-growing ingredient category?

Probiotics and prebiotics are projected to rise at a 13.4% CAGR because owners seek gut-health benefits.

Page last updated on: