Plant Based Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

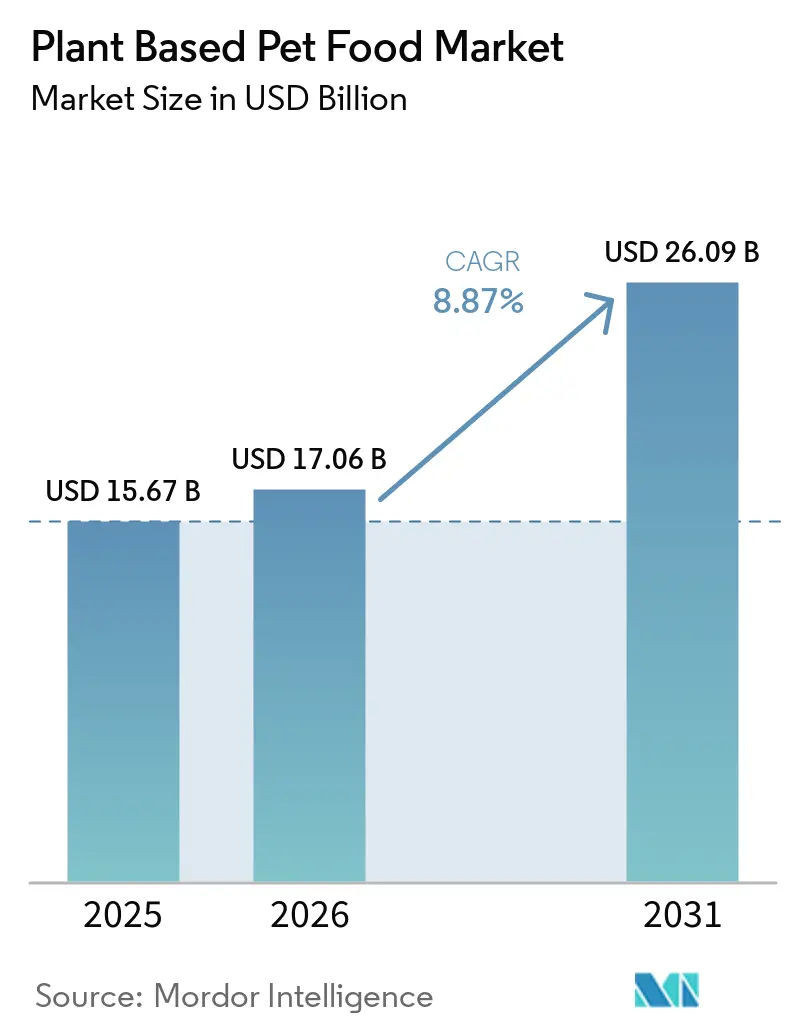

| Market Size (2026) | USD 17.06 Billion |

| Market Size (2031) | USD 26.09 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant Based Pet Food Market Analysis by Mordor Intelligence

The plant-based pet food market size is projected to expand from USD 15.67 billion in 2025 and USD 17.06 billion in 2026 to USD 26.09 billion by 2031, registering a CAGR of 8.87% during 2026-2031. The plant-based pet food market is moving forward as pet owners increasingly apply their own food standards to companion animals and seek cleaner labels, clearer ingredient disclosure, and products that align with personal values around health and sustainability. Demand is also widening because plant-based formulas are increasingly used for dogs with suspected meat allergies and sensitive stomachs, giving the plant-based pet food market a stronger clinical use case than it had a few years ago. A 12-month controlled feeding trial published in 2024 demonstrated that healthy adult dogs maintained normal clinical, hematological, and nutritional markers while consuming a commercial plant-based diet[1]Source: Annika Linde, Maureen Lahiff, Adam Krantz, Nathan Sharp, Theros T. Ng, and Tonatiuh Melgarejo, “Domestic Dogs Maintain Clinical, Nutritional, and Hematological Health Outcomes When Fed a Commercial Plant-Based Diet for a Year,” PLOS One, journals.plos.org. This finding is reducing hesitation among veterinarians and cautious pet owners. Veterinary acceptance is significant, as it often influences trial and repeat purchase rates in premium pet nutrition, particularly in categories where owners seek clear reassurance regarding nutritional adequacy. The plant-based pet food market also remains open to both large pet food companies and specialist brands, and long-term positions are likely to depend more on clinical credibility, ingredient innovation, and repeat digital engagement than on shelf presence alone.

Key Report Takeaways

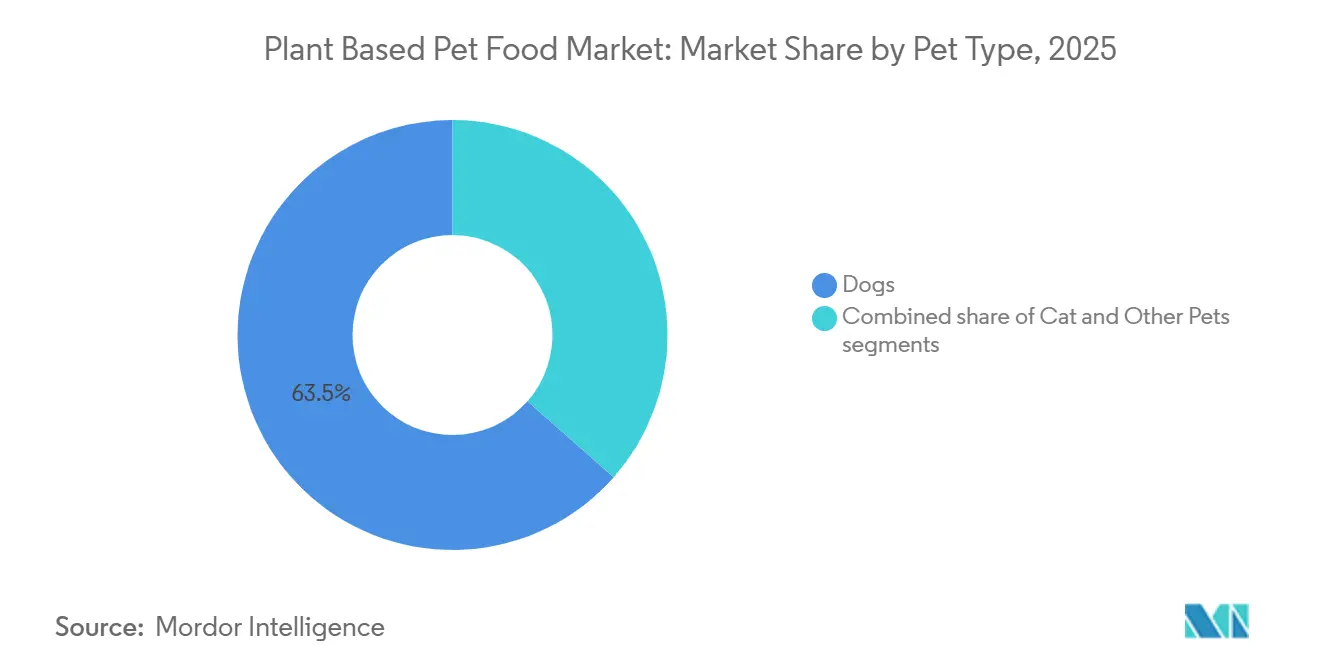

- By pet type, dogs were the largest segment with a 63.5% share in 2025 and also the fastest-growing segment with an anticipated 11.4% CAGR during 2026-2031.

- By food type, dry food accounted for 51.2% of the plant-based pet food market size in 2025, while treats and chews are the fastest-growing segment with a projected 12.8% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets accounted for 54.8% of the plant-based pet food market share in 2025, while online retail is anticipated to be the fastest-growing segment, with a projected 14.1% CAGR during 2026-2031.

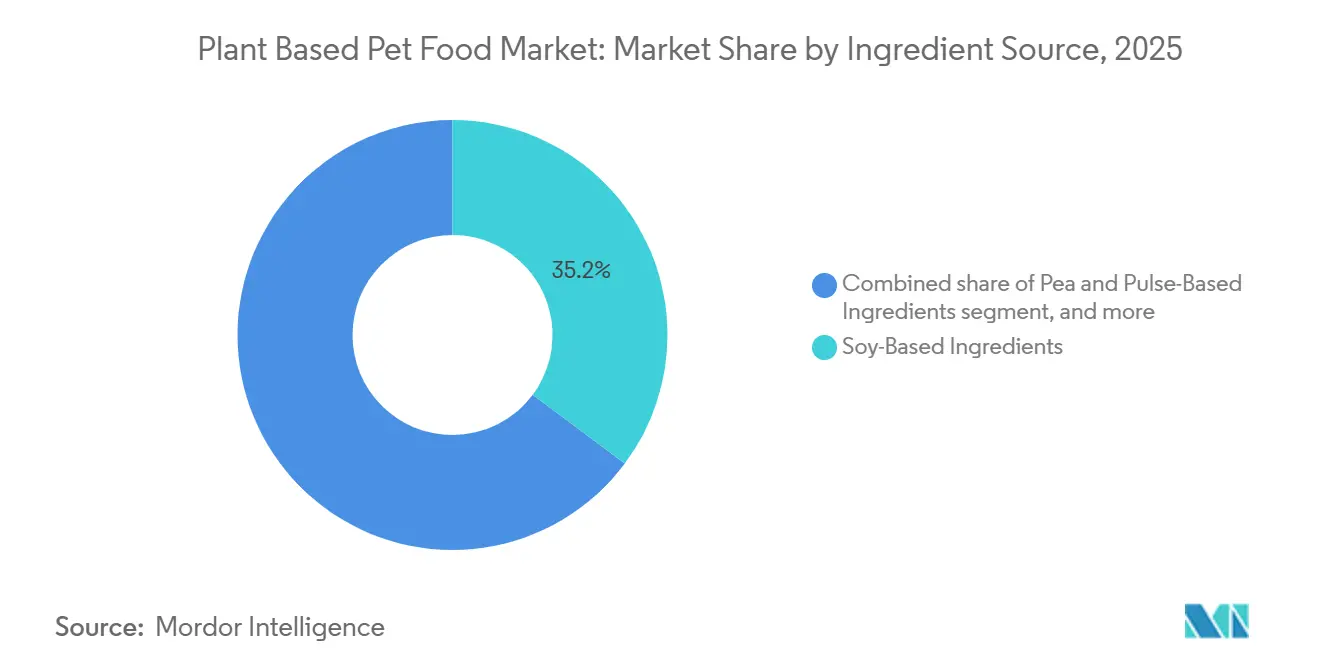

- By ingredient source, soy-based ingredients were the largest segment with 35.2% share in 2025, while yeast, algae, and fermentation-derived ingredients are the fastest-growing segment with a projected 13.5% CAGR during 2026-2031.

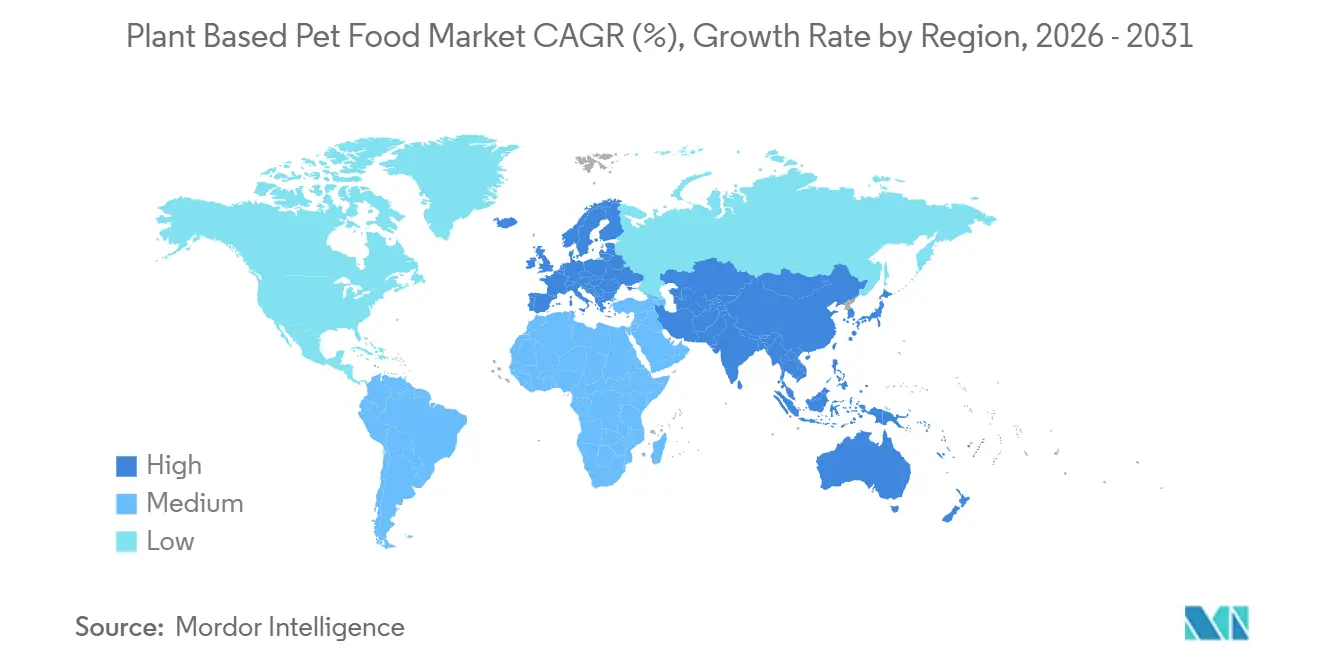

- By geography, Europe was the largest regional segment with 40.7% share in 2025, while Asia-Pacific will be the fastest regional segment with a projected 12.2% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plant Based Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumized human-grade positioning for dogs | +2.00% | Global, strongest in North America, Europe, and Australia where premium pet nutrition spending is more established | Short term (≤ 2 years) |

| Rising use for meat-allergy and sensitive-stomach cases | +1.50% | Strongest in North America and Western Europe where veterinary-led diet switching is more common | Medium term (2–4 years) |

| Climate and animal-welfare purchasing pull | +1.20% | Highest in Europe, with secondary relevance in North America due to stronger ethical and environmental purchasing behavior | Medium term (2–4 years) |

| Online and specialty shelf expansion | +1.80% | Global, especially strong in the United States, China, the United Kingdom, and Brazil due to rapid digital pet retail growth | Short term (≤ 2 years) |

| Yeast, algae, and precision-fermented proteins closing nutrient gaps | +1.00% | Strongest in North America and Europe where research activity and commercialization are advancing faster | Long term (≥ 4 years) |

| Retailer and investor carbon-accounting pressure favoring lower-impact formulas | +0.70% | Global, with stronger influence in the United States and Western Europe where sustainability screening standards are tightening | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumized Human-Grade Positioning for Dogs

Human-grade positioning has moved from a niche message to a core premium cue in dog nutrition, and this shift is supporting the plant-based pet food market among higher-income buyer groups. Many pet owners now judge dog food by the same standards they use for their own meals, which means ingredient traceability, cleaner labels, and fewer animal by-products matter more than before. A 2024 review in Frontiers in Veterinary Science found that vegan diets for dogs were associated with health outcomes comparable to or better than those of non-vegan diets across the reviewed studies, providing brands with stronger scientific support when speaking to cautious buyers. The plant-based pet food market is not driven just by price, and brands that communicate credible nutrition and transparent sourcing can continue to command a premium. Petaluma, Inc. reinforced that pattern in 2025 when it launched Whole Food Mixer as a shelf-stable complete dog food with 67% certified organic ingredients, showing how specialist brands are using formulation quality and product story to support premium pricing.

Rising Use for Meat-Allergy and Sensitive-Stomach Cases

The plant-based pet food market is also expanding as clinically motivated buyers enter the category, especially dog owners dealing with suspected protein allergies and digestive issues. This matters because veterinary-led switching tends to create a more durable demand base than lifestyle-led trial, and it can improve repeat purchase rates in the plant-based pet food market. A 2025 review titled “Nutritional analysis of commercially available, complete plant‑ and meat‑based dry dog foods in the UK” found that 31 commercially available dry dog foods in the United Kingdom showed plant‑based products to be broadly comparable to meat‑based equivalents across most macro‑ and micronutrients, although iodine and B vitamins were identified as gaps that can be supplemented. The Association of American Feed Control Officials (AAFCO) 2024 Model Regulations also continue to provide the framework for substantiating nutritional adequacy claims, which is important for brands seeking clinical credibility and veterinary acceptance [2]Source: Association of American Feed Control Officials, “Model Regulations for Pet Food and Specialty Pet Food Under the Model Bill,” Association of American Feed Control Officials, aafco.org. As more products meet both formulation standards and practical feeding expectations, the plant-based pet food market is likely to gain greater trust in allergy management and elimination-diet settings.

Climate and animal-welfare purchasing pull

Environmental and animal-welfare concerns are adding another layer of support to the plant-based pet food market, even if those concerns do not usually drive first purchase on their own. A 2026 analysis in Frontiers in Sustainable Food Systems reported that plant-based dry dog foods generated 2.82 kg carbon dioxide equivalent per 1,000 kcal, compared with 31.47 kg carbon dioxide equivalent for beef-based diets, providing brands with a measurable environmental argument rather than a broad claim[3]Source: Andrew Knight, “The Digestibility of Vegan and Vegetarian Diets for Dogs and Cats,” Animals, mdpi.com. The British Veterinary Association (BVA) also recognized the environmental case for plant-based feeding, while stressing that nutritional completeness remains essential, meaning sustainability claims work best when paired with sound formulation. Europe has been the clearest lead region for this driver, as buyers in the United Kingdom, Germany, the Netherlands, and Sweden show greater sensitivity to welfare and environmental factors in food purchasing. In practical terms, the plant-based pet food market rewards brands that can document both nutritional quality and a lower environmental impact, as retailers and consumers are becoming less willing to accept claims that lack evidence.

Online and Specialty Shelf Expansion

Online and specialty channels are lowering the trial barrier in the plant-based pet food market by giving brands more space to explain ingredients, feeding use cases, and nutritional logic. That is especially important in a category where buyers often need more information before moving away from conventional meat-based products. PawCo Foods, Inc. raised USD 2 million in seed funding in February 2024 to open a second production facility in Indiana and scale its artificial intelligence (AI)-optimized direct-to-consumer fresh dog food platform, which highlights how digital-first brands are building around both formulation and repeat purchase. Specialty pet stores also remain important because informed staff, curated assortments, and premium positioning help reduce buyer hesitation in the plant-based pet food market. In Asia-Pacific, high mobile commerce use and rising urban pet ownership are making online distribution even more effective, which is one reason the plant-based pet food market is set to grow faster there than in more mature regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Veterinary skepticism on nutritional completeness | -1.50% | Global, with especially strong influence in the United States, Canada, Germany, and the United Kingdom where veterinary guidance strongly affects premium pet food selection | Medium term (2–4 years) |

| Premium price gap versus conventional kibble | -1.20% | Strongest in Asia-Pacific, South America, and Africa where pet food purchasing remains more price sensitive | Short term (≤ 2 years) |

| Cat-specific taurine and arachidonic-acid formulation complexity | -0.80% | Global, with notable relevance in the United States, Canada, Germany, and Japan due to large cat ownership bases and stricter nutritional scrutiny | Long term (≥ 4 years) |

| Ultra-processed and greenwashing backlash risk | -0.70% | Most visible in Europe and North America where sustainability claims and labeling practices face stronger regulatory and consumer attention | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Veterinary Skepticism on Nutritional Completeness

Veterinary caution still limits the plant-based pet food market more than any other single factor because owners often rely on professional guidance when choosing a daily feeding product. The British Veterinary Association stated that well-formulated diets can meet canine nutritional needs, but it also noted that long-term independent evidence and nutrient consistency data remain limited across commercial products, and that feline evidence is much thinner [4]Source: British Veterinary Association, “BVA Companion Animal Feeding Working Group Report,” British Veterinary Association, bva.co.uk. A 2024 study in the Journal of Veterinary Internal Medicine found that 29% of English cocker spaniels in the study group had low blood taurine and that diet variables, including protein source type, were associated with taurine status. This keeps the plant-based pet food market under closer scrutiny than many adjacent premium pet nutrition categories, even when brands meet formal adequacy standards. It also means commercial progress depends not only on product launches but on stronger long-term data, post-launch monitoring, and continuing education for veterinarians.

Premium Price Gap Versus Conventional Kibble

The plant-based pet food market still carries a clear price premium over conventional kibble, which limits adoption in markets where pet food is bought on tighter household budgets. Small production runs, premium raw materials, novel ingredient systems, and higher consumer education costs all keep shelf prices higher than those of mainstream alternatives. The European Circular Bioeconomy Fund reported that younikat GmbH generated USD 10.8 million (EUR 10 million) in 2024 with 66% year-over-year growth, indicating that scale is possible but also highlighting the capital needed before operating leverage improves. Even in wealthier markets, the price issue can weaken repurchase after an initial trial if the perceived value case is not clear enough or if feeding plans are not easy to maintain. This means the plant-based pet food market needs subscription retention, better cost absorption, and broader scale before affordability becomes a weaker restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Anchor Volumes While Cat Formulations Advance

Dogs were the largest segment of the plant-based pet food market, and accounted for 63.5% of revenue in 2025. That position reflects the larger product range available for dogs and the stronger body of published evidence on canine nutritional adequacy with plant-based feeding. A 12-month PLOS One feeding trial published in 2024 found that healthy adult dogs maintained normal essential amino acid profiles, cardiac biomarkers, and vitamin D status on a commercial plant-based diet, which has become an important reference point in the plant-based pet food market. Cats were the second-largest segment, but growth has been slower because their nutrient requirements create greater formulation pressure and require greater precision in supplementation. Other pets, including small mammals and birds, still represent a niche in the plant-based pet food market, with limited current revenue contribution and fewer dedicated products.

Dogs are also the fastest segment and are projected to advance at an 11.4% CAGR during 2026-2031. Much of that momentum comes from allergy-management use cases, wider owner acceptance of premium plant-based feeding, and a growing mix of dry, fresh, and topper products built around dogs first. The dog segment of the plant-based pet food market also benefits from easier communication about completeness, as more clinical data are available and veterinarians have greater confidence discussing canine diets than feline diets. The cat segment is still moving forward, though mainly through targeted research on digestibility and supplementation. If companies can close the taurine and arachidonic acid gap at scale, the plant-based pet food market would gain access to a meaningful underserved customer base in feline nutrition.

By Food Type: Treats and Chews Drive Premiumization While Dry Food Anchors Volume

Dry food was the largest food type, and accounted for 51.2% of the plant-based pet food market size in 2025. Dry food holds that position because it is easier to store, ship, and distribute through large retail channels than fresh or wet formats. For many households, dry food also offers a lower cost per serving, which matters in a category where plant-based products often carry a price premium. Wet, fresh, and refrigerated formats are available in the plant-based pet food market, but they remain smaller because they require greater consumer commitment and often higher spending. Supplements and toppers play an important support role because they let owners test plant-based feeding with less risk than a full meal replacement.

Treats and chews are the fastest food type and are projected to grow at a 12.8% CAGR during 2026-2031. That growth is important because treats often serve as the first entry point into the plant-based pet food market, especially for buyers who are curious but not ready to switch to an entirely plant-based diet. A 2025 digestibility study published in Multidisciplinary Digital Publishing Institute Animals found that pumpkin-based plant protein diets delivered the highest organic matter digestibility (90.1%) among the tested oil mill by-product sources, supporting continued experimentation with plant-derived treat ingredients. Treats also give brands more frequent purchase occasions, which can build familiarity before owners move into complete feeding products. Soopa Pets Ltd. fits this pattern in the plant-based pet food market because its focus on natural chew positioning and clean ingredients supports premium pricing without relying on full-diet conversion at first purchase.

By Distribution Channel: Online Retail Is Reshaping Access While Supermarkets Hold Scale

Supermarkets and hypermarkets were the largest distribution channel, holding 54.8% of the plant-based pet food market share in 2025. This shows that the plant-based pet food market still depends heavily on physical retail for broad volume, especially in dry food, where mainstream shopping habits remain strong. Large-format retail helps normalize the category by placing plant-based options beside conventional products in regular shopping trips. Specialty pet stores remain important because their shoppers are more willing to read ingredients, compare formulas, and ask questions before purchasing. Veterinary clinics still account for a small share, but they matter because trust in that channel can influence both first-time and repeat purchases in the plant-based pet food market.

Online retail is anticipated to be the fastest-growing channel, with a 14.1% CAGR during 2026-2031. The plant-based pet food market lends itself well to online selling because buyers often want ingredient details, feeding guidance, and time to compare products, which digital pages can provide more effectively than a physical shelf tag. PawCo Foods, Inc. showed the strength of that model when it raised USD 2 million in 2024 to scale production and grow its artificial intelligence-enabled direct-to-consumer platform. Online selling also supports subscriptions, which are valuable in the plant based pet food market because they reduce churn and make premium pricing easier to manage over time. The next stage of channel competition will depend not only on reach but on whether brands can retain digital buyers after the first or second order.

By Ingredient Source: Fermentation-Derived Inputs Lead Innovation While Soy Stays Largest

Soy-based ingredients were the largest segment, and represented 35.2 percent of revenue in the plant-based pet food market in 2025. Soy remains the largest because it has a long commercial track record, a familiar amino acid profile, and supply chains that are already built for scale. Pea and pulse ingredients also hold a strong place in the plant-based pet food market, especially in dry kibble, where grain-free and novel-protein positioning still matter to some buyers. Grain, seed, and potato ingredients continue to support energy, texture, and fiber across a range of formulations. Other plant-derived ingredients, including roots and botanicals, are gaining attention among formulators seeking greater ingredient diversity or targeted nutritional functions.

Yeast, algae, and fermentation-derived ingredients were the fastest-growing sources and are projected to rise at a 13.5% CAGR during 2026-2031. A 2025 study in Frontiers in Animal Science found that fermented plant protein improved crude protein digestibility in dogs to 81.94% compared with 79.63% for a soybean meal control and also lowered wet fecal output, providing the plant-based pet food market with useful performance evidence. A 2025 review in Foods also noted that algal protein can contain 55-70% protein on a dry weight basis and can support docosahexaenoic acid (DHA) supply through microalgae rather than fish oil. A 2024 study in the Journal of Animal Science further showed that duckweed protein was viable as a replacement for pea protein in dog diets at up to 10% inclusion. Ingredient innovation of this kind is helping the plant-based pet food market improve nutritional credibility while also broadening the product story beyond soy and pea.

Geography Analysis

Europe was the largest regional segment, which held 40.7% of the plant-based pet food market in 2025. The region leads because it has more specialist brands, a stronger specialty retail infrastructure, and earlier buyer acceptance of alternative proteins in pet care. Germany remains especially important, and the Bundesvereinigung der Deutschen Ernährungsindustrie reported that the country’s ready-made pet food market reached USD 4.86 billion (EUR 4.5 billion) in 2025, with premiumization acting as a key driver. Germany-based younikat GmbH also underscored Europe’s momentum, reporting USD 10.8 million (EUR 10 million) in revenue and securing USD 9.8 million (EUR 9 million) in Series A funding in June 2025 to support expansion in Germany, Austria, Switzerland, and the Netherlands. The region also benefits from a stronger consumer focus on sustainability and animal welfare, which fits the value proposition of the plant-based pet food market.

North America remained the second-largest region in 2025 and continues to act as an important innovation center for the plant-based pet food market. The United States stands out for its active work in precision fermentation, premium direct-to-consumer models, and new regulatory pathways for novel ingredients. Growing consumer interest in sustainable and alternative proteins further reinforces the region’s role as an innovation hub. Canada adds demand through premium pet nutrition spending and expanding specialty retail, while Mexico is moving more gradually as urban pet ownership rises and organized pet retail improves.

Asia-Pacific was the fastest-growing regional segment and is projected to grow at a 12.2% CAGR during 2026-2031, driven by urbanization, pet ownership growth, and strong mobile commerce adoption, creating favorable conditions for online-led plant-based brands. Asia-Pacific growth is being supported by China, South Korea, Japan, and Australia, where digital buying behavior makes education-heavy products easier to sell. The plant-based pet food market is still less mature there than in Europe, but the speed of channel development is faster, creating room for quicker brand expansion. South America remains an emerging region, with Brazil and Chile showing the clearest early signs of organized distribution, while Argentina and Colombia remain more constrained by price sensitivity. The Middle East is developing through premium urban demand in the United Arab Emirates and Saudi Arabia, while Africa remains the smallest regional block and is led mainly by South Africa in the near-term opportunity. Across both the Middle East and Africa, the plant-based pet food market is likely to remain more dependent on imports until local manufacturing capability further develops.

Competitive Landscape

The plant-based pet food market remains moderately fragmented, leaving room for both multinational incumbents and specialist brands. The largest established names include Purina PetCare (Nestlé S.A.), Mars, Incorporated, Natural Balance Pet Foods, Inc. (Ethos Pet Brands), Halo, Purely for Pets, Inc., and Vegeco Ltd. These companies benefit from scale, distribution, procurement, and broader pet food operating experience, which gives them advantages in shelf access and supply continuity. The plant-based pet food market still allows specialist players such as Omni Pet Ltd., younikat GmbH, Petaluma, Inc., PawCo Foods, Inc., V-dog, Inc., and Amì Planet Srl to compete through product credibility and focused brand identity. A 2025 review in Foods highlighted growing patent activity around the use of microalgae biomass in restructured wet pet food formulations, showing how larger pet food companies are expanding into multiple alternative-protein technologies rather than relying on a single ingredient platform.

Competition in the plant-based pet food market is moving away from simple label claims toward evidence of digestibility, nutrient completeness, and ingredient quality. Petaluma, Inc., launched Whole Food Mixer dehydrated dog food in 2025, showing that premium shelf-stable meals can be positioned around organic sourcing and veterinary formulation rather than solely on conventional kibble economics. Hence, product strategy is becoming more specialized, with brands seeking defensible niches rather than relying solely on broad plant-based messaging.

The plant-based pet food market still has the clearest open space in feline nutrition, veterinary channel acceptance, and fermentation-derived ingredient systems. Acquisition-led entry is also appearing, as shown by Pets Choice Ltd., which acquired HOWND in 2024 to extend its reach in premium plant-based pet care. Better Choice Company, Inc. also reshaped its regional footprint in April 2025 by selling Halo’s Asia business for USD 8.1 million and then operating through a separate Asia strategy, which reflects how uneven regional maturity is influencing portfolio decisions. Smaller specialist brands can still compete well in the plant-based pet food market if they combine science-backed claims with strong digital retention and a clear product use case. Over the next few years, the most durable positions are likely to belong to companies that can make plant-based feeding feel nutritionally secure, practically easy, and distinct enough to justify repeat premium spending.

Plant Based Pet Food Industry Leaders

Mars, Incorporated

Purina PetCare (Nestlé S.A.)

Natural Balance Pet Foods, Inc. (Ethos Pet Brands)

Vegeco Ltd.

Halo, Purely for Pets, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bramble Pets expanded its plant-based, fresh dog food portfolio with the launch of The Wharf, a new recipe designed to strengthen its premium offerings and highlight the company’s focus on innovation and health-oriented formulations in the growing U.S. plant-based pet food market.

- April 2026: Symrise AG invested in United States-based Bond Pet Foods to accelerate the commercialization of precision-fermented proteins for pet nutrition applications. The partnership focused on scaling sustainable animal-free protein ingredients for next-generation dog and cat food formulations.

- June 2025: Younikat GmbH secured USD 9.8 million in Series A financing, led by the European Circular Bioeconomy Fund and Green Generation Fund, to support its expansion in the plant-based pet food market across Germany, Austria, Switzerland, and the Netherlands in 2026.

Global Plant Based Pet Food Market Report Scope

Plant-based pet food refers to nutritionally formulated pet food made primarily from plant-derived ingredients and non-meat alternative proteins. It includes complete meals, treats, toppers, and fresh or dry products designed for pets, mainly dogs and selected cat applications, with required nutrient supplementation where needed. The Plant-Based Pet Food Report is Segmented by Pet Type (Dogs, Cats, and Other Pets), by Food Type (Dry, Wet, Treats and Chews, Supplements and Toppers, and Fresh and Refrigerated), by Distribution Channel (Supermarkets and Hypermarkets, Specialty Pet Stores, Online Retail, Veterinary Clinics, and Other Retail Channels), by Ingredient Source (Soy-Based Ingredients, Pea and Pulse-Based Ingredients, Grain, Seed, and Potato-Based Ingredients, Yeast, Algae, and Fermentation-Derived Ingredients, and Other Plant-Derived Ingredients), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Dogs |

| Cats |

| Other Pets |

| Dry Food |

| Wet Food |

| Treats and Chews |

| Supplements and Toppers |

| Fresh and Refrigerated Food |

| Supermarkets and Hypermarkets |

| Specialty Pet Stores |

| Online Retail |

| Veterinary Clinics |

| Other Retail Channels |

| Soy-Based Ingredients |

| Pea and Pulse-Based Ingredients |

| Grain, Seed, and Potato-Based Ingredients |

| Yeast, Algae, and Fermentation-Derived Ingredients |

| Other Plant-Derived Ingredients |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Other Pets | ||

| By Food Type | Dry Food | |

| Wet Food | ||

| Treats and Chews | ||

| Supplements and Toppers | ||

| Fresh and Refrigerated Food | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Pet Stores | ||

| Online Retail | ||

| Veterinary Clinics | ||

| Other Retail Channels | ||

| By Ingredient Source | Soy-Based Ingredients | |

| Pea and Pulse-Based Ingredients | ||

| Grain, Seed, and Potato-Based Ingredients | ||

| Yeast, Algae, and Fermentation-Derived Ingredients | ||

| Other Plant-Derived Ingredients | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in plant based pet food?

Growth is being supported by pet humanization, allergy-management use cases in dogs, online retail expansion, and progress in fermentation-derived proteins. The market is projected to grow at an 8.87% CAGR during 2026-2031.

Which pet type contributes the most revenue?

Dogs are the fastest segment with an projected 11.4% CAGR during 2026-2031.

Why is Europe leading this space?

Europe held 40.7% of revenue in 2025 because it has stronger specialist brand presence, mature specialty retail, and earlier consumer acceptance of alternative proteins in pet nutrition.

Which sales channel is growing the fastest?

Online retail is the fastest channel with a projected 14.1% CAGR during 2026-2031 because digital platforms offer more room for feeding guidance, subscriptions, and ingredient education.

What is the biggest barrier to wider adoption?

Veterinary skepticism on nutritional completeness remains the main barrier, especially for cat nutrition where taurine and arachidonic acid requirements make formulation more difficult.

Which ingredient trend matters most for future product development?

Yeast, algae, and fermentation-derived inputs are the most important long-term trend. This segment is projected to grow at a 13.5% CAGR during 2026-2031 and is helping close nutrient and digestibility gaps.

Page last updated on: