India Pet Food Market Analysis by Mordor Intelligence

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban pet ownership upsurge | +3.5% | National, concentrated in Mumbai, Delhi NCR, Bangalore, Hyderabad, and Pune | Medium term (2-4 years) |

| Pet care spending surges amid rising incomes and humanization trends | +3.2% | National, strongest in metros and Tier 1 cities | Long term (≥ 4 years) |

| Expansion of e-commerce and quick-commerce delivery | +2.8% | National, early gains in metros, and spillover to Tier 2 cities | Short term (≤ 2 years) |

| Domestic extrusion capacity expansion lowers prices | +2.1% | National, manufacturing hubs in Maharashtra, Tamil Nadu, and Telangana | Medium term (2-4 years) |

| Pet-insurance rollout lifts premium-diet spending | +1.5% | National initial uptake in metros with veterinary density | Long term (≥ 4 years) |

| Functional ingredients sourced from food waste cut formulation cost | +1.2% | National pilot projects in Karnataka and Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Pet Ownership Upsurge

In 2024, India's pet-dog population hit 31 million, bolstered by an annual addition of 2 million companion animals from metro nuclear families, according to industry estimates based on veterinary clinic registrations and municipal licensing data. Millennials and Gen Z now represent 68% of first-time pet adopters, emphasizing emotional bonds over traditional guard roles, and fueling a demand for tailored nutrition. In urban settings, the trend of high-rise apartment living has led to a surge in small-breed ownership. Breeds like Shih Tzus, Beagles, and Labradors, now favorites among city dwellers, require calorie-rich kibbles suited for their indoor lifestyle. As pet ownership transitions from backyard kennels to living rooms, hygiene standards have risen. Many owners, deeming loose grains unhygienic, now see packaged food as essential. In June 2024, Mars introduced 85-gram breed-specific Pedigree SKUs for apartment residents who favor single-serve sizes. This packaging innovation led to a 22% increase in trial rates in the first quarter of its launch[1]Source: Mars Incorporated, “Royal Canin Opens Packaging Facility in Maharashtra,” mars.com.

Pet Care Spending Surges Amid Rising Incomes and Humanization Trends

Households in India's upper-middle class, earning over Rs 10 lakh (USD 12,000) annually, are increasingly investing in pet care, spending around Rs 5,000 (USD 60) monthly on premium diets, grooming, and veterinary services. This trend of pet humanization is evident as pet owners gravitate towards grain-free formulations, single-protein recipes, and functional treats enriched with probiotics or omega-3 fatty acids. While these categories had minimal shelf presence in 2020, they surged to represent 18% of specialty-store revenue by 2025. In June 2024, Heads Up For Tails unveiled 'Hearty', a super-premium pet food line boasting 60% real meat and 40% fresh vegetables. This launch targets discerning pet parents who scrutinize ingredient labels as meticulously as their own food. The brand anticipates revenue of Rs 500 crore (USD 60 million) within three years, highlighting urban consumers' willingness to pay three times the price of standard kibbles for assured transparency and traceability. Meanwhile, in April 2025, Godrej Pet Care made its debut in Tamil Nadu with 'Ninja', a mid-premium range enriched with 37 nutrients. Priced 25% lower than imported counterparts, 'Ninja' aims to attract households aspiring for premium products but with a keen eye on budget.

Pet Insurance Rollout Lifts Premium Diet Spending

In April 2024, HDFC ERGO unveiled "Paws n Claws," marking India's debut of a comprehensive pet insurance. This policy, tailored for dogs and cats aged 3 months to 10 years, encompasses surgical procedures, chronic illness management, and veterinary diet prescriptions. Annual premiums range between Rs 5,000 and Rs 15,000 (USD 60 to USD 180). Notably, the policy reimburses up to 80% for therapeutic diets, especially those prescribed for renal disease, diabetes, or obesity. This effectively subsidizes the premium pricing of Rs 800 to Rs 1,200 per kg (USD 9.60 to USD 14.40 per kg) for Hill's Prescription Diet and Royal Canin's Veterinary Range. Colgate-Palmolive's Hill's Pet Nutrition witnessed a 28% surge in Prescription Diet sales in India during the first half of 2025. The company attributes this uptick to the affordability brought by insurance and strong endorsements from veterinarians, which have proven more influential than retail promotions. This synergy between insurance coverage and the adoption of therapeutic diets has created a momentum. Claims data not only underscores the benefits of specialized nutrition but also bolsters veterinarian endorsements. This trend is poised to expand the market for veterinary diets, with the share of total pet-food revenue projected to increase from 4% to 12% by 2030.

Functional Ingredients Sourced from Food Waste Cut Formulation Cost

In 2025, String Bio, a Bangalore-based biotech startup, successfully piloted a project that converts methane captured from dairy-processing plants into fermented protein. This protein boasts a crude-protein content of 72%, is priced 40% lower than imported fish meal, and has a carbon footprint that's 60% smaller. Palatability trials with Labrador Retrievers and Beagles confirmed its digestibility, matching that of chicken meal. Now, the startup is ramping up production to 500 metric tons annually, targeting mid-tier kibble formulations. Meanwhile, Allana Group's Bowler's Nutrimax brand is turning a waste stream from its poultry-processing units into a valuable hydrolyzed feather meal. This digestible protein not only meets the Association of American Feed Control Officials (AAFCO) standards but also trims raw-material costs by Rs 12 per kg (USD 0.14 per kg) for the finished kibble. By valorizing by-products from the food industry, these companies tackle two major challenges, they counteract raw-material inflation influenced by global commodity trends and bolster brand differentiation through sustainability. This eco-friendly messaging strikes a chord with 42% of pet owners in India under 35, who prioritize environmental considerations in their purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity in Tier 2/3 cities | -2.5% | National, most acute in Uttar Pradesh, Bihar, Madhya Pradesh, and Rajasthan | Medium term (2-4 years) |

| Low packaged-food penetration vs homemade diets | -2.0% | National, strongest in rural areas and Tier 3 cities | Long term (≥ 4 years) |

| Dependence on imported wet food and specialty ingredients | -1.5% | National, affects the premium and super-premium segments | Short term (≤ 2 years) |

| Fragmented regulatory oversight slows feed-standard rollout | -1.0% | National compliance complexity in import clearance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Wet Food and Specialty Ingredients

In India, wet pet food is predominantly imported, with Thailand, the United States, and the European Union as the primary sources. This reliance subjects the segment to foreign exchange fluctuations, tariff modifications, and supply chain hiccups. As a result, retail prices for wet food soar by 20% to 30% compared to domestic kibbles. Specialty ingredients, including hydrolyzed proteins, chelated minerals, and freeze-dried meat toppings, are procured from suppliers in New Zealand, Australia, and the United States. This sourcing not only extends lead times by 8 to 12 weeks but also mandates sanitary import permits from the Food Safety and Standards Authority of India (FSSAI). Securing these permits for new SKUs can be a lengthy process, taking between 4 to 6 months. While industry giants Mars and Nestlé eye greenfield investments in wet-food plants, the hefty capital requirement of Rs 300 crore to Rs 400 crore (USD 36 million to USD 48 million) and an unpredictable payback period in a market sensitive to pricing have stalled their final investment decisions. Until domestic wet-food production ramps up, this segment is poised to remain a luxury for affluent urban households, curbing its potential impact on the broader market growth.

Fragmented Regulatory Oversight Slows Feed-Standard Rollout

In India, pet food regulation is split between the Food Safety and Standards Authority of India (FSSAI), which focuses on food safety and labeling, and the Department of Animal Husbandry and Dairying, which ensures the quality of animal feed [2]Source: Food Safety and Standards Authority of India, “Pet Food Regulations,” fssai.gov.in. This dual oversight leads to overlapping compliance requirements that differ by state, resulting in delays for product approvals. While FSSAI requires nutritional statements and ingredient labels, it doesn't set specific standards for pet food formulations. This oversight pushes manufacturers to self-certify based on guidelines from the Association of American Feed Control Officials (AAFCO) or the European Pet Food Industry Federation (FEDIAF). Such a gap not only erodes consumer trust but also leads to inconsistent enforcement. For imported wet food, brands must navigate a maze, securing a sanitary import permit from the Department of Animal Husbandry and Dairying (DAHD), obtaining a veterinary health certificate from the exporting country, and FSSAI clearance for each SKU. This lengthy process, taking 6 to 9 months, often deters brands from launching new flavors or pack sizes. Without a standardized pet food code, labeling requirements vary across states like Maharashtra, Tamil Nadu, and Karnataka. This inconsistency forces national brands to produce state-specific packaging, driving up inventory costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Food Dominance Drives Volume Growth

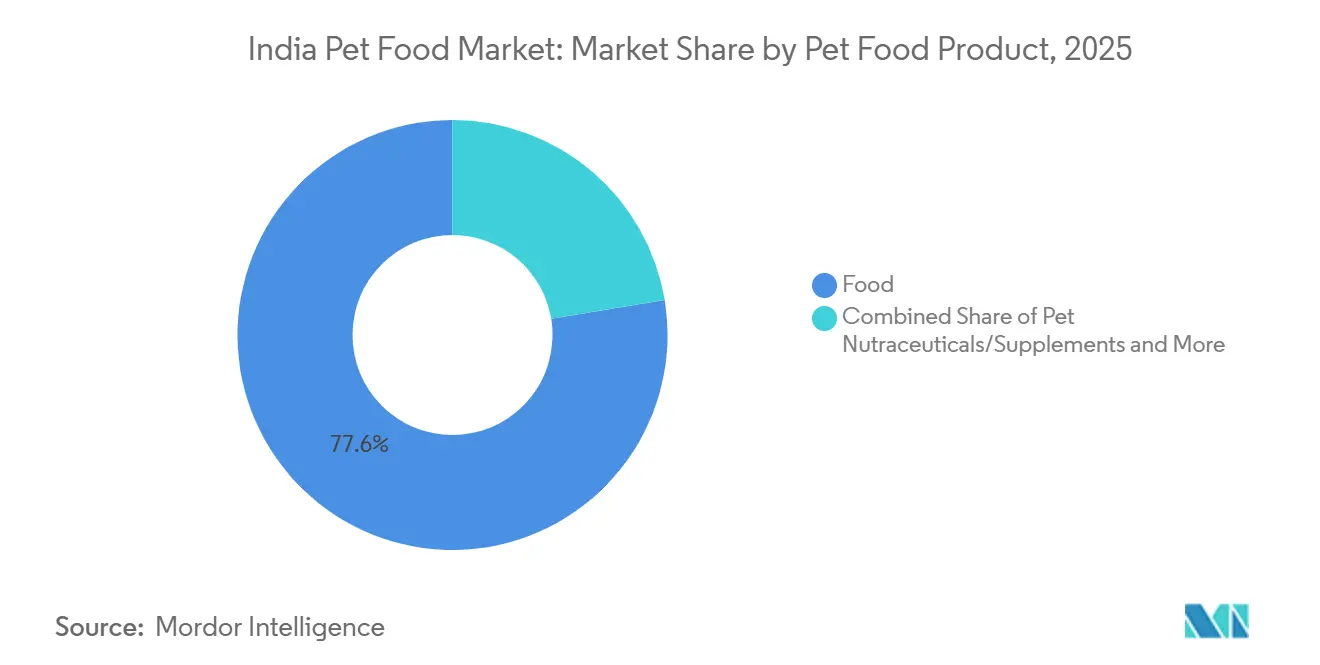

Food accounted for the largest share, representing 77.6% of the India pet food market size in 2025, and is also the fastest-growing segment, with a projected CAGR of 12.1% through 2031. Underscoring their fundamental role and the habitual purchasing behavior that ensures steady revenue for producers. Within the food category, dry pet food stands out as the top sub-segment, leveraging its longer shelf life and economical distribution methods to reach a broader audience. On the other hand, while wet pet food commands a premium price, it grapples with supply challenges stemming from its reliance on imports and the need for a cold chain.

Food products not only dominate but also lead the fastest-growing segment, this surge is bolstered by an increasing awareness among pet owners about the significance of quality nutrition and a noticeable pivot towards premium and specialized food offerings. Kibbles have secured their spot as the favored choice in the dry food category, owing to their cost-effectiveness, convenience, and nutritional adequacy. Meanwhile, wet pet food continues to entice with its moisture-rich content and taste appeal.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pet: Dogs Drive Volume, Cats Deliver Growth

Dogs dominate the India pet food market, accounting for 92.4% of the India pet food market share in 2025 and are also the fastest-growing segment, with a projected CAGR of 11.6% through 2031. Established feeding routines and a familiarity with commercial nutrition have solidified stable demand patterns in the dog food segment, enhancing both inventory planning and distribution efficiency. Factors such as urbanization, rising disposable incomes, and heightened awareness of pet nutrition among dog owners are propelling this growth. Notably, the segment's dominance is bolstered by a surge in demand for premium offerings, spanning dry pet food, specialized treats, and veterinary diets.

Within the dog food landscape, there's a clear bifurcation, economy kibbles are priced below Rs 300 per kg (USD 3.60), while super-premium, grain-free formulations command prices above Rs 700 per kg (USD 8.40). The mid-tier segment, ranging from Rs 400 to Rs 600 per kg (USD 4.80 to USD 7.20), is declining as consumers either opt for budget-friendly choices during inflationary times or elevate their purchases for perceived health benefits. Targeting this dynamic market, Godrej's Ninja, introduced in Tamil Nadu in April 2025, strategically positions itself at Rs 450 per kg (USD 5.40). With a formulation boasting 37 nutrients and probiotics, Ninja aims to attract households seeking premium nutrition without the imported brand price tag. Bolstering the segment's strength is the widening distribution network, complemented by a diverse product range accessible through specialty stores and online platforms.

By Distribution Channel: Specialty Stores Face Online Disruption

By distribution channel, specialty stores led the India pet food market in 2025 with a 34.1% market share and are anticipated to be the fastest-growing channel, expanding at a CAGR of 14.1% through 2031. Specialty stores leverage their product expertise and strong customer relationships to achieve premium positioning and engage in consultative selling. By offering expert advice, tailored product recommendations, and a wide range of premium and specialized pet foods, these stores have established themselves as essential destinations for pet owners. This segment is experiencing significant growth and is projected to expand further, supported by the rise of pet ecosystem stores and increasing demand for specialized pet diets.

Prominent specialty store chains, such as Heads Up For Tails, which operates 75 retail locations across India, are transforming the pet retail landscape. They achieve this by integrating product offerings with value-added services, including pet grooming and veterinary consultations. The success of specialty stores is driven by their customer-focused approach, knowledgeable staff, and the ability to stock both mainstream and niche pet food brands. This makes them the preferred choice for pet owners who prioritize quality and seek expert guidance in their purchasing decisions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

West India, anchored by the pet-friendly cultures of Mumbai and Pune, leads the regional market. The area's higher disposable incomes bolster the adoption of premium pet products. With a robust retail infrastructure and a swift embrace of e-commerce, West India offers numerous avenues for brands to engage consumers. Major players like Mars, Incorporated, and Royal Canin have set up manufacturing bases in Maharashtra, reaping supply chain benefits and expediting product launches. Furthermore, West India's regulatory framework, in sync with Food Safety and Standards Authority of India (FSSAI) standards, not only ensures product quality and safety but also bolsters consumer trust in packaged pet nutrition.

While Tier 2 cities like Jaipur, Lucknow, Coimbatore, and Visakhapatnam welcome 400,000 new pet-owning households each year, the penetration of packaged food lags below 20%. This is largely due to price sensitivities and limited retail access. Quick-commerce platforms are bridging this gap, offering specialty-store assortments directly to consumers without the need for physical storefronts. In rural India, where 48% of the nation's pet dogs reside, there's a stark absence of commercial food adoption. With homemade diets being the norm and veterinary services sparse, these areas present a long-term opportunity. Yet, realizing this potential hinges on rising incomes and targeted behavior-change campaigns. South India, buoyed by the tech-driven prosperity of Bengaluru and Chennai, is witnessing a surge in pet ownership. As nuclear families increasingly embrace pets, the region's online shopping habits and early adoption of subscription-based pet food deliveries are fostering brand loyalty and ensuring steady revenue. Moreover, South India's cultural acceptance of vegetarian pet food offers distinctive product opportunities, setting it apart from other regions.

Despite boasting sizable pet populations, the northern states of Uttar Pradesh, Bihar, and Madhya Pradesh account for a mere 12% of market revenue. This shortfall is attributed to lower per-capita incomes and a cultural tendency to feed pets household leftovers. As urbanization progresses and younger pet owners lean towards convenience, this dynamic is poised for a gradual shift. On the export front, the Agricultural and Processed Food Products Export Development Authority (APEDA) highlighted a burgeoning potential [3]Source: Agricultural and Processed Food Products Export Development Authority, “India’s Pet Food Export Potential,” apeda.gov.in. In 2024, pet-food shipments to Nepal, Bhutan, and the Middle East touched Rs 120 crore (USD 14.4 million), marking a 35% uptick from 2023. Indian manufacturers, capitalizing on their cost edge, are making inroads into neighboring markets. Yet, it's worth noting that these exports constitute less than 2% of total production and grapple with perception challenges in premium segments.

Competitive Landscape

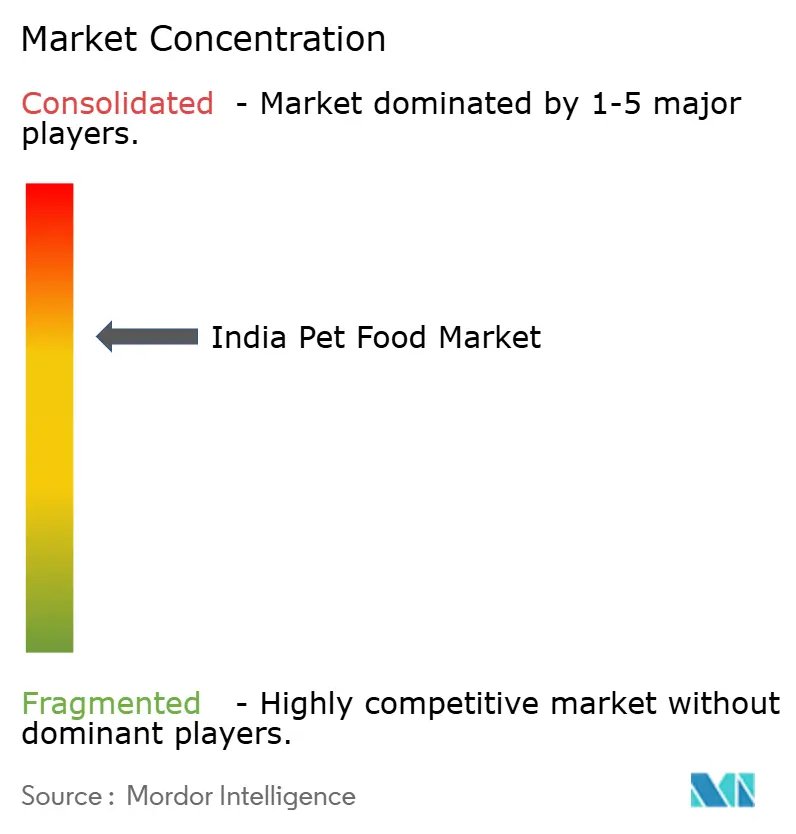

The top five players, including Mars, Incorporated, Nestle S.A. (Purina), Drools Pet Food Pvt. Ltd., Charoen Pokphand Group, and Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), dominate the India pet food market, which is highly consolidated. While local players are present, they mainly operate in specific regional markets or concentrate on particular product segments. The market features a blend of diversified conglomerates that include pet food in their broader portfolio and specialized companies dedicated solely to pet nutrition and wellness.

Domestic startups like Supertails and Pawfectly Made leverage direct-to-consumer models, sidestepping wholesale margins. Their digital platforms employ algorithmic recommendations and offer bundled services, such as grooming vouchers, to boost sales. Godrej Consumer Products is set to invest USD 60 million (INR 500 crore) over five years to penetrate the segment, leveraging its established FMCG supply chains and the Godrej Agrovet feed mill network. Meanwhile, Nestlé S.A. (Purina)’s minority stake in Drools underscores growing multinational interest and offers Drools capital for capacity enhancements.

To thrive in the India pet food market, companies must grasp local pet ownership trends and consumer preferences. They should develop products tailored to the nutritional needs of various pet breeds while keeping prices competitive. Forming robust ties with veterinarians and pet care experts is vital, given their influence on purchasing choices. An omnichannel strategy, spanning specialty stores, supermarkets, and e-commerce, is crucial for reaching a broad customer base. Additionally, firms should prioritize educating consumers on the advantages of commercial pet food compared to home-cooked meals.

India Pet Food Industry Leaders

Mars, Incorporated

Drools Pet Food Pvt. Ltd.

Charoen Pokphand Group.

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

Nestle S.A. (Purina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nestlé S.A. (Purina) made a minority financial investment in India pet food unicorn Drools, marking the global food giant's first strategic investment in India's pet care sector while maintaining Drools' operational independence.

- May 2023: Nestle S.A. (Purina) introduced new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

- April 2023: Mars, Incorporated opened its first pet food research and development center in Asia-Pacific. This new facility, called the APAC pet center, will support the company's product development.

Mordor Intelligence follows a four-step methodology in all our reports.

Key Questions Answered in the Report

What is the projected value of the India pet food sector by 2031?

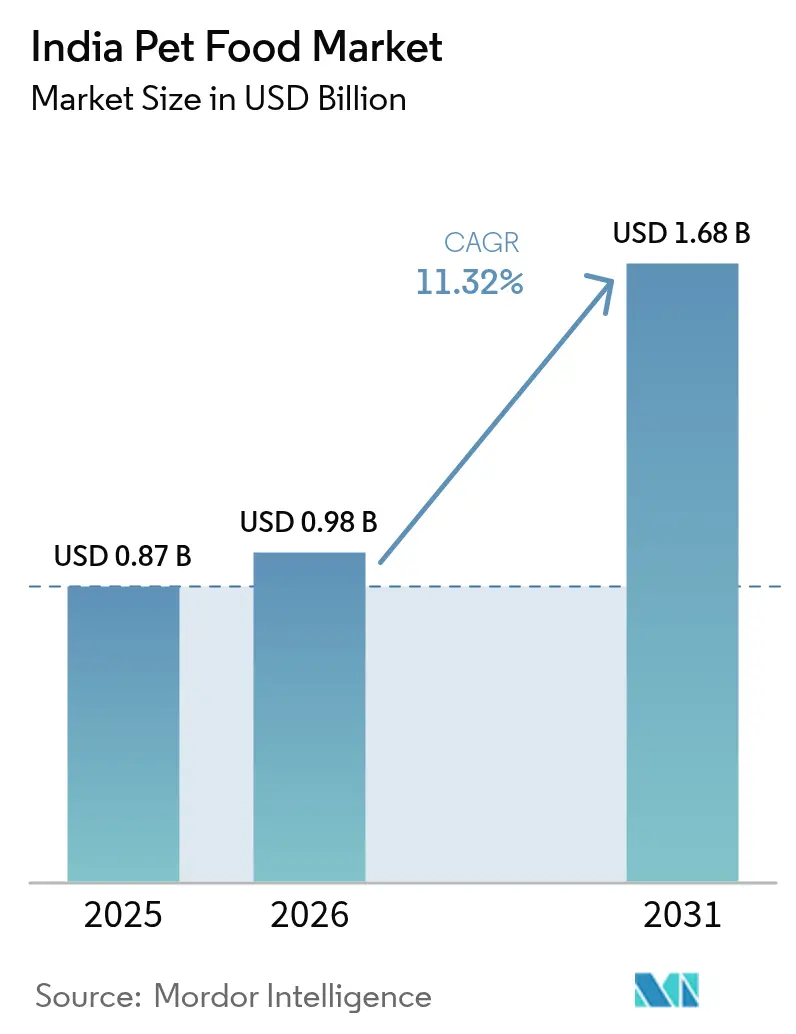

The India pet food market size was valued at USD 0.87 billion in 2025 and is projected to grow from USD 0.98 billion in 2026 to USD 1.68 billion by 2031, at a CAGR of 11.32% during the forecast period (2026-2031).

How fast will specialty channel sales of pet food expand in India over the forecast period?

Specialty store platforms are emerging as the fastest-growing channel in pet retail, with a (CAGR) of 14.1% through 2031.

Why is adoption of veterinary diets accelerating among Indian pet owners?

New pet-insurance policies reimburse up to 80% of therapeutic diet costs, making premium medical nutrition affordable for a wider base of insured pets.

Which pet type is projected to register the fastest demand growth?

Dog food is set to rise at a 11.6% CAGR through 2031, as apartment living and smaller household footprints favor feline adoption.

Page last updated on: