Petri Dishes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

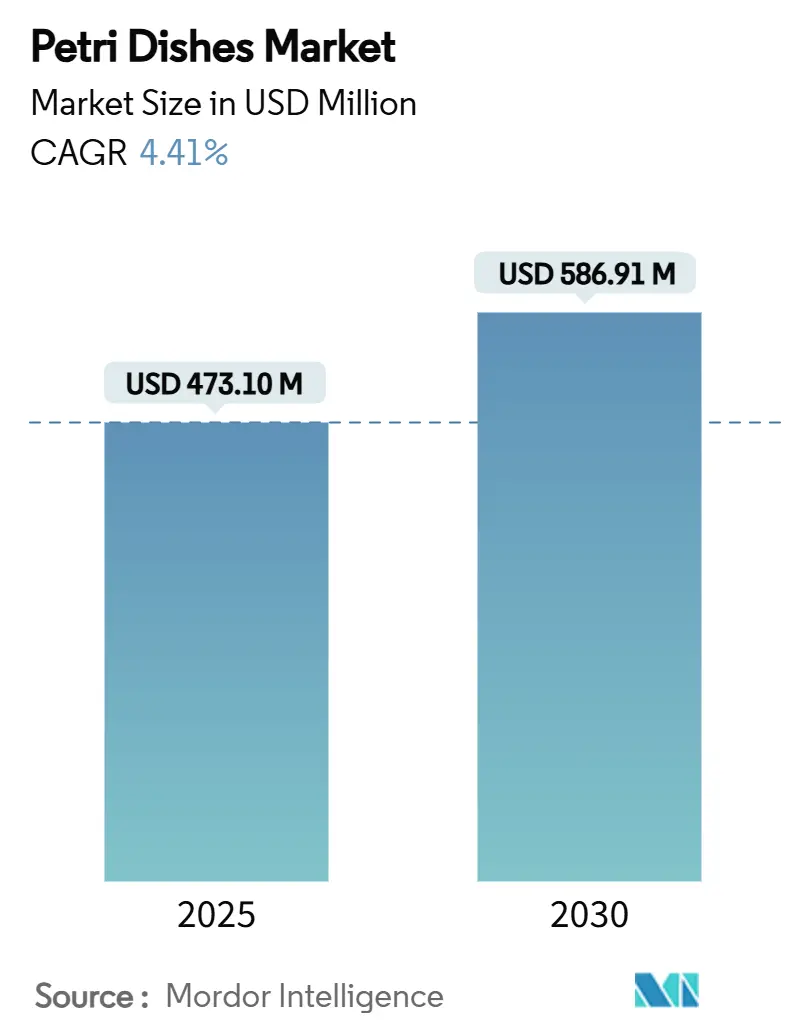

| Market Size (2025) | USD 473.10 Million |

| Market Size (2030) | USD 586.91 Million |

| Growth Rate (2025 - 2030) | 4.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Petri Dishes Market Analysis by Mordor Intelligence

The petri dishes market size stands at USD 473.10 million in 2025 and is forecast to climb to USD 586.91 million by 2030 at a steady 4.41% CAGR. Growth reflects the technology’s enduring role as the preferred culture platform in pharmaceutical R&D, diagnostic testing and basic research. Laboratories continue to favour single-use formats that mesh with automated workflows, while advances in surface chemistry are widening petri dish utility in 3-D organoid development, high-throughput screening and space biology. Regulatory scrutiny of sterility, rising funding for regenerative medicine and the spread of automation across Asia-Pacific laboratories create fertile demand, yet environmental restrictions on single-use plastics and volatile resin prices constrain profit margins. Competitive advantage now pivots on integrating material innovation with robotics-ready design and demonstrable sustainability credentials.

Key Report Takeaways

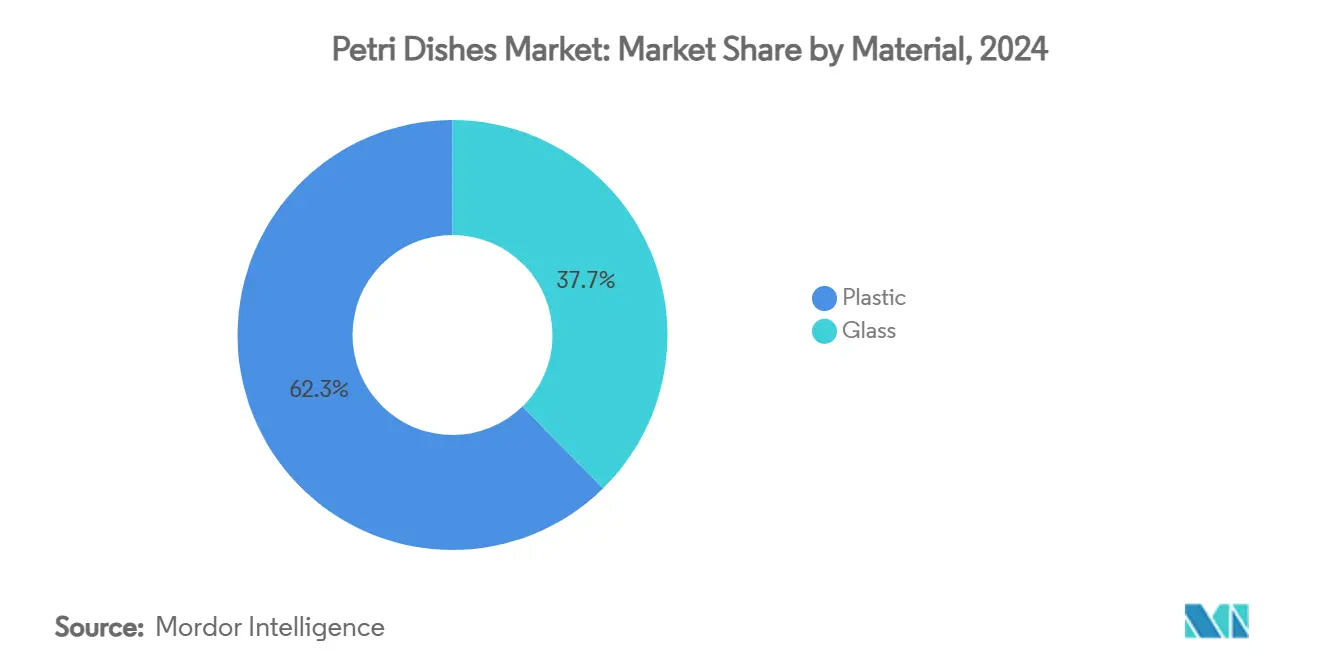

- Plastic materials led the material segment with 62.34% of petri dishes market share in 2024 and are projected to expand at 7.48% CAGR through 2030.

- Disposable single-use dishes accounted for 56.43% of the petri dishes market size in 2024, while the segment is forecast to grow 6.62% CAGR to 2030.

- By diameter, 90 mm formats captured 46.12% revenue share in 2024; dishes ≥120 mm are advancing at a 7.89% CAGR through 2030.

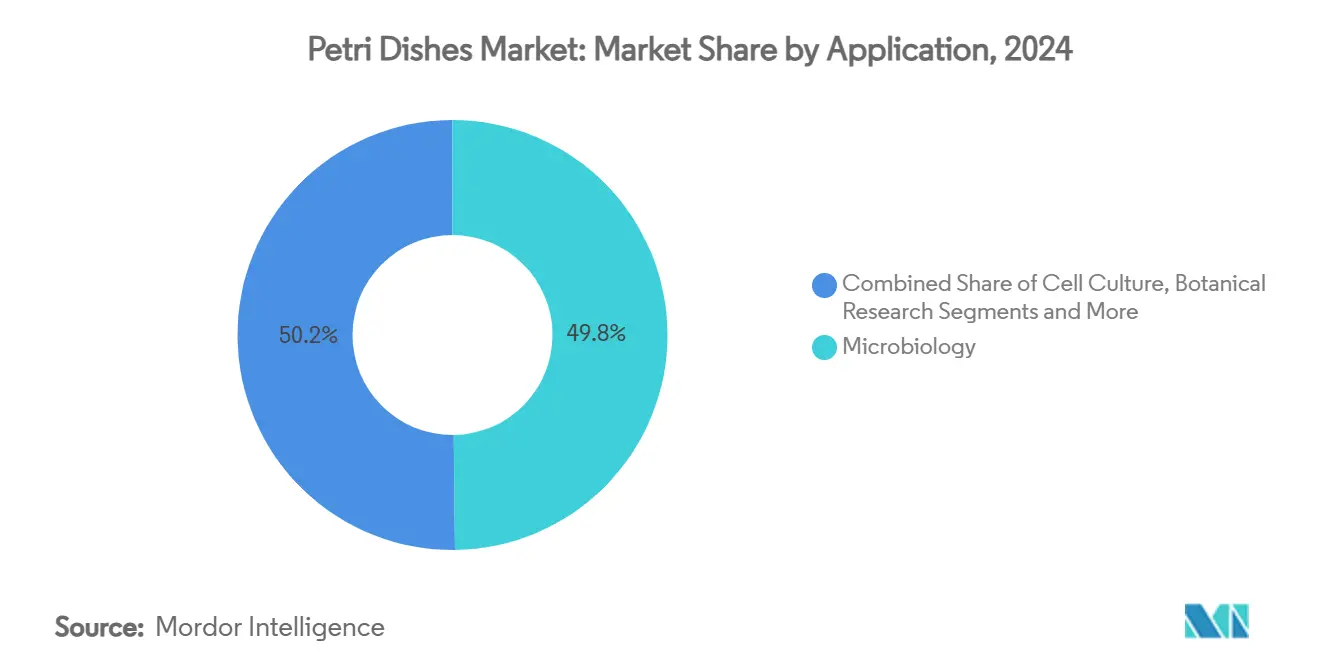

- In applications, microbiology retained 49.82% share of the petri dishes market in 2024, whereas cell culture is progressing at an 8.01% CAGR to 2030.

- By end user, pharmaceutical and biotechnology companies held 36.81% share of the petri dishes market in 2024; contract research organisations are recording the fastest 7.37% CAGR through 2030.

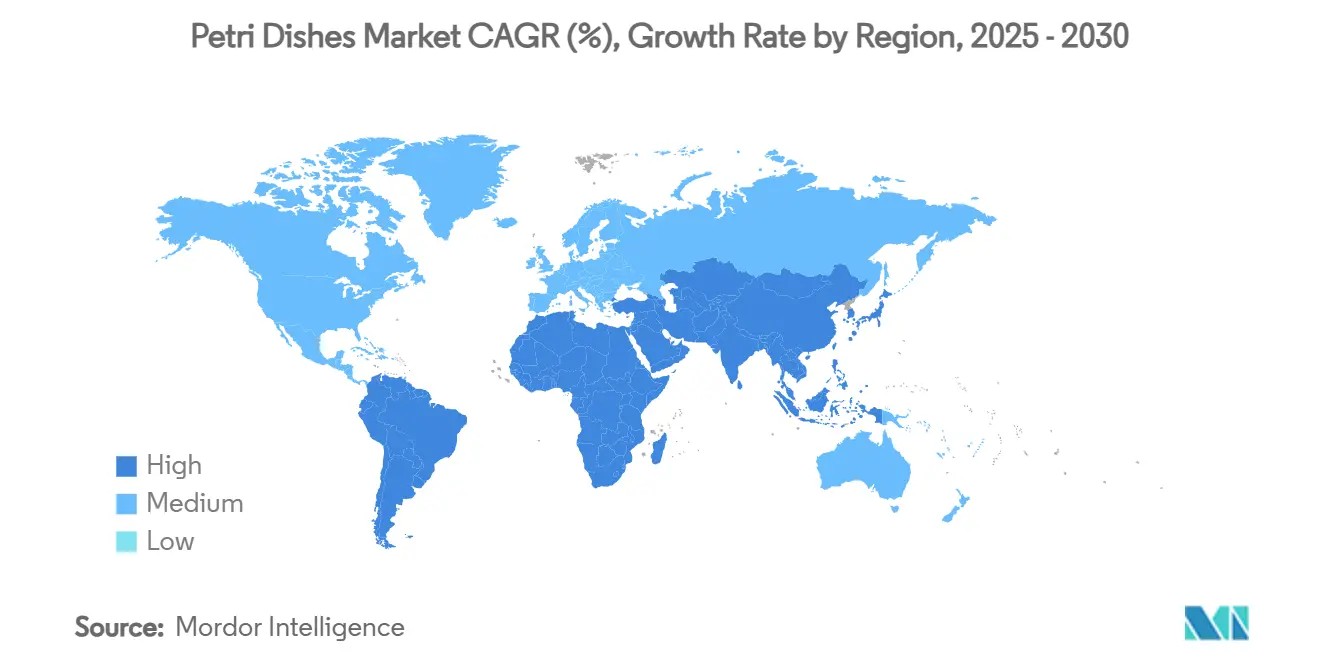

- By geography, North America controlled 31.28% of global revenue in 2024, while Asia-Pacific is rising at a 6.46% CAGR during the forecast horizon.

Global Petri Dishes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cell-culture demand in regenerative therapies | +1.2% | North America, Europe, expanding globally | Medium term (2-4 years) |

| Higher infectious-disease testing volumes | +0.8% | APAC and other emerging regions | Short term (≤ 2 years) |

| CRO expansion in cost-advantaged regions | +0.7% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Preference for single-use plasticware | +0.6% | North America, Europe, gradually worldwide | Medium term (2-4 years) |

| Clarity needs for automated imaging systems | +0.5% | North America, Europe, early adoption in APAC | Medium term (2-4 years) |

| Space-biology R&D funding | +0.3% | North America, Europe, nascent APAC participation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for cell culture in regenerative and personalised therapies

Organ-specific regenerative medicine is reshaping petri dish specifications as laboratories shift from 2-D monolayers to complex 3-D organoids that require precision-engineered surface chemistries. The FDA Modernization Act 2.0 has accelerated organ-on-chip adoption, triggering wider use of coated dishes such as Corning’s CellBIND that improve cell attachment via oxygen-rich functional groups. Hiroshima University recently demonstrated that aligned stem-cell sheets grown on treated surfaces doubled protein secretion, signalling how surface design can enhance tissue-engineering outcomes. AI-guided CRISPR optimisation for ovarian-ageing reversal further underscores the need for vessels that support precise micro-environments. NASA’s USD 2.3 million allocation for 11 space-biology projects is extending these demands to micro-gravity settings, forging a premium niche for advanced culture platforms.

Rising prevalence of infectious diseases boosting microbial testing volumes

Updated 2024 guidelines from the Infectious Diseases Society of America emphasize rapid diagnostics that still rely on confirmatory cultures, keeping petri dishes integral to clinical workflows.[1]J. Michael Miller, “Guide to Utilization of the Microbiology Laboratory for Diagnosis of Infectious Diseases: 2024 Update,” Clinical Infectious Diseases, pubmed.ncbi.nlm.nih.govMetagenomic sequencing adoption has paradoxically reinforced the need for culture validation in complex cases, especially for antibiotic-resistant ESKAPE pathogens identified via MALDI-TOF proteomics.[2]Yu Zhao, Wenhui Zhang & Xin Zhang, “Application of Metagenomic Next-Generation Sequencing in the Diagnosis of Infectious Diseases,” Frontiers in Cellular and Infection Microbiology, frontiersin.org Public-health surveillance, highlighted by the 2023 Utah E. coli outbreak traced to irrigation water, underscores how standardised culture vessels remain pivotal in outbreak response. Laboratories are pairing manual plating with automated colony counters that demand high-clarity, dimensionally precise dishes.

Rapid expansion of CROs in emerging markets

Asian CROs are scaling rapidly as multinational sponsors seek cost-efficient patient access. ICON’s network across 12 Asia-Pacific countries illustrates how regional infrastructure supports multi-regional clinical trials. WuXi AppTec’s ascent among the world’s top-ten CROs signals that the region’s capabilities now span discovery through manufacturing. The rise of decentralised trials and mRNA platforms demands robust cultureware that maintains sterility across disparate geographies, accelerating orders for automation-ready disposable dishes.

Shift toward single-use plasticware to mitigate cross-contamination

Research labs generate billions of pounds of plastic waste annually, yet sterility protocols still push facilities toward disposable dishes. Institutions now investigate recyclable or biodegradable polymers, and studies show that reusable borosilicate glass can match sterility while cutting individual researcher footprints by 105.92 kg CO₂e over 10 years.[3]Sriram Kalpana et al., “Antibiotic Resistance Diagnosis in ESKAPE Pathogens—A Proteomic Perspective,” Diagnostics, frontiersin.org The EU’s Packaging and Packaging Waste Regulation compels recyclability by 2030, forcing suppliers to redesign products for end-of-life recovery. Manufacturers therefore face a dual challenge: meeting sterility benchmarks and demonstrating circular-economy compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental regulations on single-use plastics | -0.9% | Europe leading, spreading to North America and APAC | Medium term (2-4 years) |

| Raw-material price volatility | -0.6% | Global, acute in production hubs | Short term (≤ 2 years) |

| Uptake of microfluidic culture chips | -0.4% | North America, Europe, gradual APAC | Long term (≥ 4 years) |

| Rising sterilisation-compliance costs | -0.3% | Regulated high-income markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental regulations limiting single-use plastics

Europe’s Regulation 2025/351 tightens impurity thresholds for polymer food-contact articles, and parallel rules govern laboratory vessels, forcing reformulation of polystyrene and polypropylene blends. The US General Services Administration now factors plastic-free packaging into federal procurement, nudging public research institutes toward alternative materials. Widespread PFAS bans add complexity, as 29 states and the EU review curbs on thousands of compounds, compelling suppliers to prove compliance throughout the value chain.

Raw-material price volatility

European polystyrene rose EUR 55 per metric ton in January 2025, following similar 2024 spikes in polyethylene and polypropylene markets. Ethylene-oxide sterilisation facilities face USD 313 million in mandatory upgrades under new EPA air-toxics norms, pushing conversion costs higher. Manufacturers must either absorb price swings or adjust contracts, pressuring margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: plastics consolidate leadership

Plastic commanded 62.34% of the petri dishes market in 2024 and is forecast to advance at 7.48% CAGR through 2030, extending its edge over glass as laboratories embrace single-use sterility and automation readiness. This dominance reflects plastics’ compatibility with robotic handlers, lower breakage risk and the maturing of surface-treatment chemistries that now rival glass in optical clarity and wettability. Advancements such as oxygen-enriched CellBIND coatings enhance cellular attachment while keeping extractables below critical thresholds, broadening plastics’ suitability for 3-D organoid culture and high-content imaging. Glass retains a foothold in corrosive chemical work and long-term archiving, yet performance parity from new copolymers is eroding this niche.

Manufacturers are shifting from commodity to application-specific resins, embedding RFID chips and robot-grip flanges that integrate with closed-loop QC platforms. Regulatory attention on recycling has catalysed biodegradable blends, but stringent sterility demands keep conventional polystyrene dominant until validated eco-grades scale. Cost volatility in styrenics underscores the value of diversified supply chains, prompting large suppliers to vertically integrate pellet production and gamma-irradiation capacity to protect margins and delivery reliability.

By Petri Dish Type: disposables dictate workflow design

Disposable single-use formats captured 56.43% of 2024 revenue and are growing 6.62% CAGR on the back of post-pandemic contamination control protocols. Laboratories calculate that the downstream cost of a failed experiment dwarfs the premium paid for pre-sterilised dishes, especially in cell-therapy production where batch value can exceed USD 1 million. Standard reusable glass or autoclavable plastic persists in teaching labs and small clinics, but repeated sterilisation cycles degrade dimensional tolerance, rendering them unsuitable for automated sorters and colony counters.

Automation is a decisive force: robots require uniform dish geometry that disposables guarantee, while embedded barcodes speed chain-of-custody documentation. Sustainability mandates push suppliers to introduce recyclable or bio-sourced polymers, yet adoption remains modest because validation data are still limited. Pricing gaps are narrowing as scale economies expand, effectively locking in disposables as the default choice for regulated and high-throughput environments.

By Diameter: size extremes create a bifurcated market

The 90 mm standard held the largest slice at 46.12% in 2024 because it balances culture area with incubator capacity for routine clinical microbiology. At the same time, dishes ≥120 mm are the fastest riser at 7.89% CAGR, driven by organoid research and multi-layer assays that need expansive growth surfaces. Smaller ≤60 mm formats serve cost-sensitive settings and space-constrained incubators, while the 70–100 mm tier meets niche needs for precise surface-area normalisation in quantitative toxicology screens.

Automation exerts a dual pull: high-throughput imagers favour larger dishes that minimise plate exchanges, whereas microfluidic add-ons push miniaturisation for reagent savings. Laboratories therefore keep mixed inventories, encouraging vendors to bundle diameter variants with common lids and stacking rings to streamline procurement. Future growth will hinge on which end-use—high-density screening or macro-scale tissue engineering—wins greater funding momentum.

By Application: cell culture unlocks premium value

Microbiology still contributed 49.82% of the petri dishes market in 2024, underscoring the enduring need for culture-based diagnostics even as molecular assays proliferate. Yet cell culture is expanding fastest at 8.01% CAGR, reflecting regenerative-medicine pipelines and organ-on-chip adoption that demand advanced surface treatments and optical consistency. Botanical studies, education and water testing form dependable low-margin channels that stabilise baseline demand.

The cell culture upswing pushes suppliers to add gas-permeable lids, integrated sensing films, and coating options tailored for stem-cell, spheroid, or suspension models. Parallel regulatory moves to reduce animal testing elevate ex vivo models, further tilting R&D budgets toward high-specification dishes. These upgrades support premium pricing, lifting overall petri dishes market size even in segments with modest volume growth.

By End-User: CROs narrow the gap with pharma leaders

Pharmaceutical and biotechnology firms retained 36.81% share of the petri dishes market in 2024, reflecting their sizeable R&D budgets and stringent QC protocols that favour high-specification consumables. Contract research organisations trail in absolute revenue but are logging 7.37% CAGR as sponsors outsource discovery and early-stage development to cost-advantaged hubs. Hospitals and diagnostic labs anchor steady demand for standard formats, while academic institutes drive experimentation with alternative materials and smart-dish prototypes.

CRO growth changes purchasing dynamics because these organisations buy in bulk across multiple geographies, imposing unified consumable standards and squeezing supplier lead times. Vendors that can guarantee global stocking, lot-to-lot consistency and electronic traceability gain preferred-supplier status. Downstream, food-and-beverage QA labs and environmental testing centres add incremental volume as regulatory surveillance intensifies—rounding out a demand profile that is broad but increasingly quality-differentiated.

Geography Analysis

North America retained 31.28% revenue share in 2024, buoyed by deep pharmaceutical pipelines and early adoption of robotics. Thermo Fisher’s USD 2 billion US capacity upgrade highlights sustained domestic demand for premium consumables. FDA sterility-information guidance and EPA ethylene-oxide rules tighten quality controls, rewarding suppliers with validated processes. The petri dishes market size gains further traction as AI-linked imaging platforms become standard in biopharma QC labs.

Asia-Pacific is the fastest-growing region at 6.46% CAGR, fuelled by China and India’s expanding biotech ecosystems and active government incentives. Initiatives supporting mRNA facilities, decentralised trials and stem-cell therapies translate into rising demand for high-specification cultureware. CRO proliferation magnifies this effect by centralising bulk purchasing of disposables compatible with high-throughput screens. Regional suppliers are scaling, yet many labs still rely on imported premium brands, preserving revenue for multinationals.

Europe hosts a mature yet regulation-driven market where environmental directives reshape product design. EU mandates for recyclability by 2030 catalyse R&D into closed-loop polymers and reusable dish systems. Sustainability positioning has become a procurement criterion for publicly funded institutes, benefiting firms that can document lifecycle emissions reductions. Simultaneously, high R&D intensity in Germany, France and the UK underpins steady turnover of premium, automation-ready formats.

Middle East & Africa and South America remain nascent but show accelerating uptake as hospital infrastructure and academic research funding expand. The adoption curve follows diagnostics capacity growth, with public health labs as lead customers. Currency fluctuations and import tariffs temper growth yet present opportunities for regional manufacturing investments.

Competitive Landscape

The petri dishes industry features moderate fragmentation: multinodal manufacturing capacity co-exists with innovation clusters in North America, Europe and East Asia. Thermo Fisher Scientific, Corning and BD leverage broad portfolios, validated sterilisation, and global distribution to hold substantial shares. Corning’s Ascent fixed-bed bioreactor and CellBIND surfaces illustrate an ongoing pivot toward specialty high-margin products, while BD’s acquisition of Olink expands adjacent proteomics integration.

Strategic moves emphasise vertical integration and digital enablement. BD plans to spin off diagnostics to sharpen focus on life-science consumables, and its new robotics solution automates single-cell research—an ecosystem pull-through for premium dishes. Sartorius’ Center for Bioprocess Innovation likewise embeds consumable trialing into client projects, fostering lock-in.

Emerging players pursue differentiation via sustainable materials and AI-enabled QC. Greiner Bio-One markets partially recycled polystyrene lines, while startups explore biodegradable PLA composites. Market entry barriers remain centred on sterility validation, dimensional precision and regulatory compliance, limiting rapid share displacement.

Petri Dishes Industry Leaders

Thermo Fisher Scientific Inc.

Corning Incorporated

Becton, Dickinson and Company

Greiner Bio-One International GmbH

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific pledged USD 2 billion over four years to expand manufacturing and R&D capacity in the United States.

- November 2024: Sartorius inaugurated a Center for Bioprocess Innovation in Marlborough, Massachusetts, featuring two GMP suites slated for 2025 clinical production.

Global Petri Dishes Market Report Scope

| Plastic |

| Glass |

| Standard (Reusable) |

| Disposable (Single-use) |

| ≤ 60 mm |

| 70 – 100 mm |

| ≥ 120 mm |

| Microbiology |

| Cell Culture |

| Botanical Research |

| Others (Education, Water Testing) |

| Hospitals & Diagnostic Labs |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Food & Beverage Industry |

| Environmental & Water Testing Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Plastic | |

| Glass | ||

| By Petri Dish Type | Standard (Reusable) | |

| Disposable (Single-use) | ||

| By Diameter | ≤ 60 mm | |

| 70 – 100 mm | ||

| ≥ 120 mm | ||

| By Application | Microbiology | |

| Cell Culture | ||

| Botanical Research | ||

| Others (Education, Water Testing) | ||

| By End-User | Hospitals & Diagnostic Labs | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Food & Beverage Industry | ||

| Environmental & Water Testing Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth rate of the global petri dishes market to 2030?

The market is forecast to expand at a 4.41% CAGR from 2025 to 2030.

Which material category commands the highest market share today?

Plastic petri dishes lead with 62.34% share in 2024 and are expected to post a 7.48% CAGR through 2030.

Why are laboratories increasingly opting for disposable petri dishes?

Single-use dishes minimise cross-contamination and deliver robot-ready dimensional consistency, benefits that outweigh their higher per-unit cost in high-value workflows.

Which geographic region is expanding fastest?

Asia-Pacific holds the highest growth momentum, advancing at a 6.46% CAGR on the back of biotechnology investment and CRO expansion in China and India.

How are environmental regulations affecting petri dish suppliers?

EU and US rules targeting single-use plastics and PFAS push manufacturers to reformulate polymers, validate recycling pathways and absorb higher compliance costs.

Page last updated on: