Cat And Dog Food Topper Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

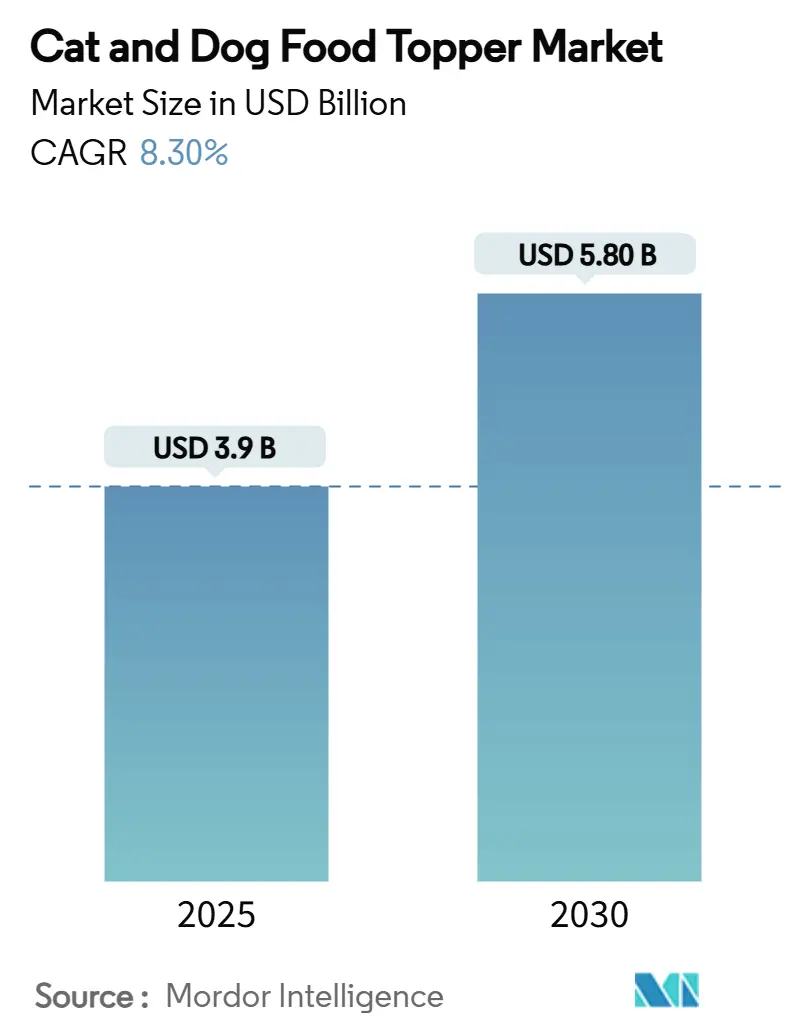

| Market Size (2025) | USD 3.9 Billion |

| Market Size (2030) | USD 5.80 Billion |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

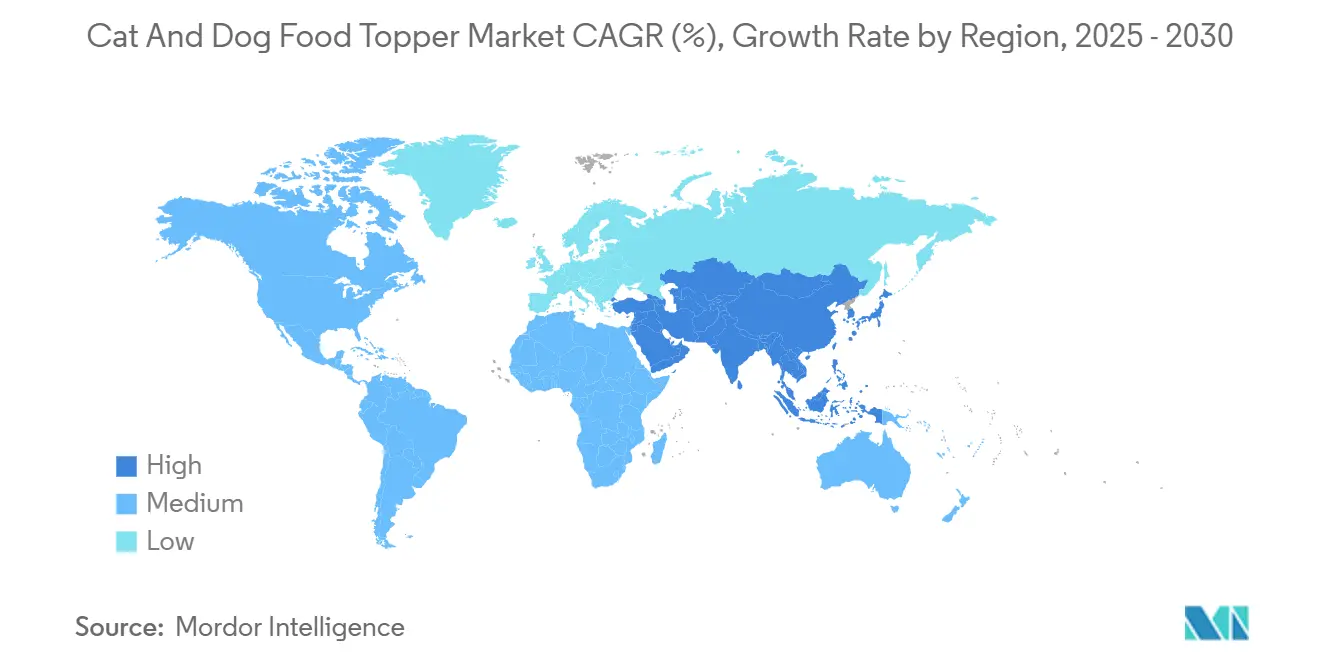

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cat And Dog Food Topper Market Analysis by Mordor Intelligence

The cat and dog food topper market size reached USD 3.9 billion in 2025 and is forecast to grow at an 8.3% CAGR, touching USD 5.8 billion by 2030. A sharp rise in pet humanization, greater interest in functional nutrition, and expanding e-commerce access collectively fuel this trajectory. Owners increasingly treat toppers as essential meal enhancers that deliver targeted health benefits, prompting brands to invest in novel protein sources, microbiome science, and freeze-drying technology. Specialty retailers remain influential due to staff expertise, yet online subscription services are reshaping replenishment habits and broadening geographic reach. Regulatory clarity in the United States and Canada is also boosting innovation, while sustainability concerns are steering ingredient choices toward insect protein and up-cycled meat co-products.

Key Report Takeaways

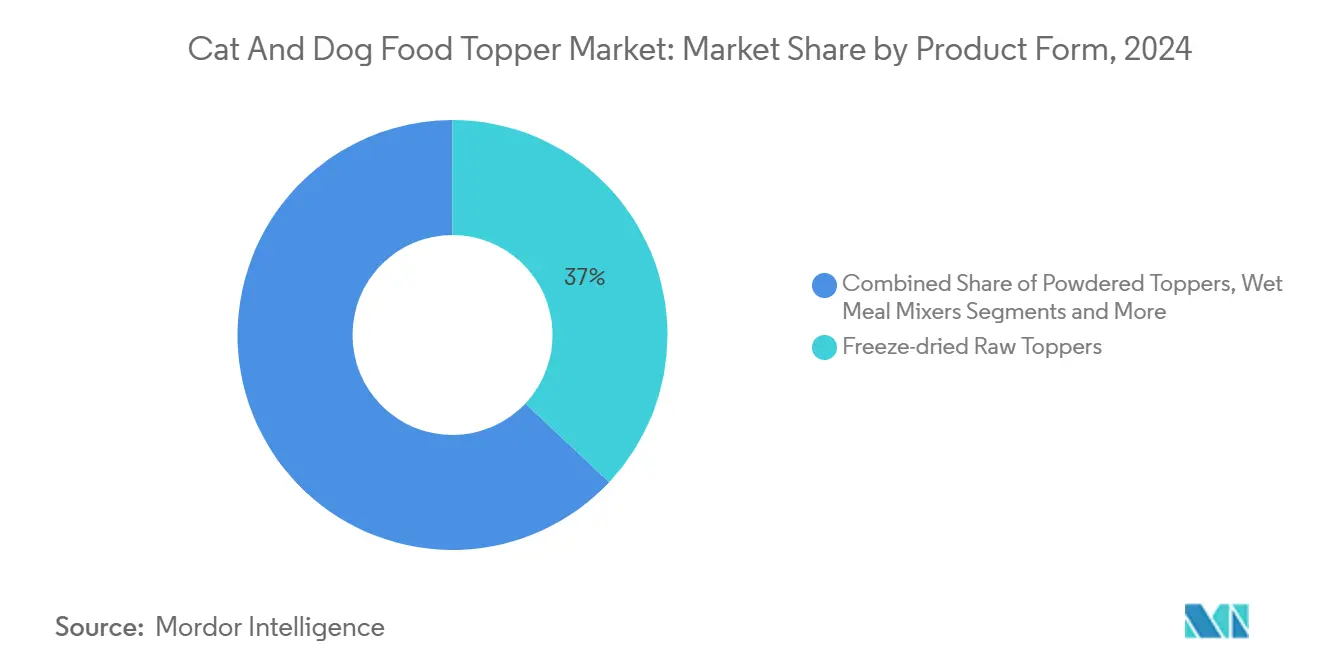

- By product form, freeze-dried raw toppers captured 37.0% of the cat and dog food topper market share in 2024. Powdered Toppers are the fastest-growing product form projected to expand at a 10.2% CAGR through 2030.

- By pet type, dogs held 60.0% of the 2024 pet-type segment, whereas cat-focused toppers are anticipated to grow at a 9.7% CAGR.

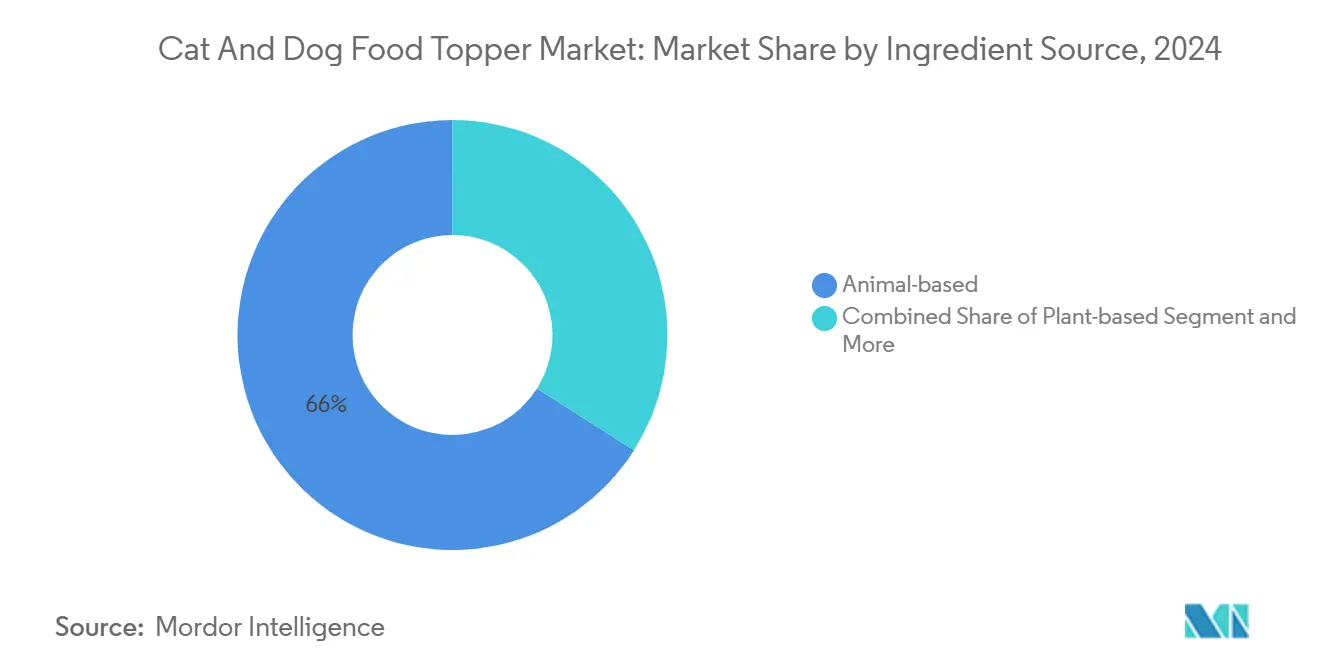

- By ingredient source, animal-based ingredients commanded 66.0% share of the cat and dog food topper market size in 2024, while insect-based lines are projected to grow at 11.2% CAGR.

- By sales channel, specialty pet stores retained a 52.5% share in 2024, while online retail is projected to rise at a 10.4% CAGR.

- By geography, North America led with a 43.1% share in 2024, while Asia-Pacific is anticipated to grow at a 10.6% CAGR in the forecast period.

Market Trends and Insights

Drivers Impact Analysis of Cat And Dog Food Topper Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid humanization of pets is elevating demand for premium meal enhancers | +2.1% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Accelerating shift from treats to functional nutrition boosters | +1.8% | Global, early adoption in developed markets | Short term (≤2 years) |

| Freeze-dried raw processing advances lowering price premiums | +1.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| E-commerce subscription models driving repeat topper purchases | +1.2% | Global , led by North America and urban Asia-Pacific | Short term (≤2 years) |

| Post-biotic and microbiome-targeted formulations are gaining traction | +0.9% | Developed markets first, emerging economies later | Long term (≥4 years) |

| Up-cycling of meat co-products into sustainable toppers | +0.7% | Europe and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Humanization of Pets is Elevating Demand for Premium Meal Enhancers

Pet parents increasingly emulate human dining experiences for their companions, driving premium topper adoption. Higher-income and millennial households show the strongest willingness to pay for functional claims that mirror their wellness routines. Premium positioning benefits from the perception that toppers transform basic kibble into gourmet fare, boosting palatability and variety. Veterinary endorsements of functional toppers reinforce consumer confidence and justify higher price points. This sentiment is most pronounced in North America and Western Europe, where per-pet spend remains unparalleled.

Accelerating Shift from Treats to Functional Nutrition Boosters

Consumers now favor toppers that deliver tangible health benefits rather than empty-calorie treats. Brands respond with formulations featuring antioxidants, postbiotics, and joint-support compounds that address specific conditions. Retailers merchandise these products in wellness sections, further re-framing toppers as daily health aids. The trend aligns with veterinarian advice on preventive nutrition, although over-supplementation risks persist. Demand is strongest in mature markets but quickly penetrates urban centers in the Asia-Pacific.

Post-Biotic and Microbiome-Targeted Formulations are Gaining Traction

Advances in gut-health science now focus on bacterial metabolites rather than live cultures, enabling shelf-stable functional toppers. Hill’s ActivBiome+ launch in 2025 set a benchmark for clinically backed digestive benefits. Post-biotics address sensitive stomachs and immune function, appealing to over 80% of owners who rank digestive health as a purchase driver. As research becomes mainstream, brands integrate specific strains and metabolites that differentiate Stock Keeping Units. Veterinary recommendations remain pivotal for widespread uptake.

Up-Cycling of Meat Co-Products into Sustainable Toppers

Circular-economy sourcing converts organ meats and bone meals into nutrient-dense ingredients, reducing waste and carbon footprint. Sustainability messaging resonates with 70% of European pet owners, supporting premium pricing. Processing innovations enhance palatability and safety, turning by-products into value-added inputs. The approach eases protein supply constraints amid rising demand and tightens cost control by leveraging existing meat streams. Regulatory bodies in Europe and North America encourage up-cycling through clearer labeling rules.

Restraints Impact Analysis of Cat And Dog Food Topper Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory gray-zone between treats and complete diets increases compliance risk | −1.3% | United States and European Union | Medium term (2-4 years) |

| Supply bottlenecks for human-grade novel proteins | −1.1% | Global premium supply chains | Short term (≤2 years) |

| Price sensitivity in emerging economies is limiting premium topper uptake | −0.8% | Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Potential over-supplementation leading to veterinarian push-back | −0.6% | Developed markets with strong veterinary networks | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Gray-Zone Between Treats and Complete Diets Increases Compliance Risk

Association of American Feed Control Officials 2024 Pet Food Label Modernization clarified many rules, yet left ambiguities around functional claims[1]Holland and Hart, “AAFCO Updates to Model Regulations,” hollandhart.com. Brands must now navigate nutrient adequacy testing if toppers approach meal-replacement territory. Mislabeling fines or product withdrawals can erode trust and inflate costs. Smaller firms without dedicated regulatory teams face higher barriers to entry. Harmonization efforts continue, but uncertainty will weigh on innovation timelines during the next two to four years.

Price Sensitivity in Emerging Economies is Limiting Premium Topper Uptake

Inflationary pressures reduce discretionary pet spending in markets such as Nigeria and Brazil. Consumers prioritize staple diets over add-ons toppers unless products demonstrate clear health paybacks. Brands introduce smaller pack sizes and value lines, but margins shrink in the process. Currency volatility further complicates pricing strategies and import costs. Despite rising pet ownership, premium topper uptake will lag until purchasing power stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cat And Dog Food Topper Market Segment Analysis

By Product Form:

Freeze-dried leadership with powdered toppers accelerationFreeze-dried raw toppers retained 37.0% of the cat and dog food topper market share in 2024, driven by superior nutrient preservation and shelf stability. Cost reductions from improved freeze-drying cycles have widened consumer access, while flavor diversity keeps the segment engaging. Liquid and broth toppers consolidate hydration benefits, appealing to older pets and owners concerned about water intake. Wet meal mixers and semi-moist gravies address texture preferences, especially for finicky eaters, fostering cross-selling with dry kibble. Powdered toppers, though smaller, are advancing at a 10.2% CAGR through 2030 as consumers seek portion control and lower price points. Brands differentiate powders with targeted functional additives such as collagen or postbiotics. Collectively, varied formats balance premium positioning with affordability, expanding household penetration.

Manufacturers increasingly offer multi-format packs that blend freeze-dried morsels with powdered nutrients to maximize convenience and health claims. Retailers' merchandise format-specific shelving alongside clear functional labeling guides shoppers toward tailored solutions. Private-label ranges now mimic premium features, intensifying competition on innovation rather than price. As cost curves keep falling, the cat and dog food topper market size for freeze-dried lines will likely maintain dominance, yet powdered toppers may outpace in unit velocity given their affordability. Long-term winners will integrate processing advances, palatability science, and transparent sourcing to sustain consumer trust.

By Pet Type:

Canine scale and feline momentumDogs accounted for 60.0% of 2024 consumption, underpinning volume leadership through higher per-serving needs. The large installed base and established treat routines simplify topper incorporation into daily feeding. Product innovation for dogs often centers on joint health, weight management, and high-protein energy formulas. Conversely, cat toppers are expanding at a 9.7% CAGR, propelled by heightened awareness of feline-specific amino acid requirements. Flavor innovation with fish, tuna, and taurine-rich profiles improves palatability for selective felines. This focus on cat-specific products aligns with global trends, as cat ownership exceeded dog ownership in 2024, with male owners (52%) outnumbering female owners (48%)[2]Mars, Incorporated, "Mars unveils the world’s largest pet parent study," mars.com.

Marketers leverage social media campaigns that highlight picky-eater transformations to convert cat owners. Smaller pack sizes accommodate portioning and freshness concerns unique to cats. Veterinary recommendations for urinary tract health and hydration also elevate topper relevance in feline diets. In the future, canine lines will continue to anchor portfolio revenues, yet the fastest incremental gains will stem from species-specific feline formulations that address wellness and sensory needs.

By Ingredient Source:

Animal dominance meets novel protein disruptionAnimal-based formulations led with 66.0% share of the cat and dog food topper market size in 2024, owing to palatability and established supply chains. Chicken, beef, and salmon remain staples, while organ meats deliver nutrient density and sustainability advantages. Plant-based toppers attract environmentally minded owners but require meticulous amino-acid balancing for obligate carnivores. Insect-based toppers, though niche, are scaling at an 11.2% CAGR due to favorable feed-conversion ratios and low land use. Functional additive-enhanced lines overlay antioxidants, glucosamine, or postbiotics onto base proteins, creating premium Stock Keeping Units that command higher margins.

Consumer education on black soldier fly larvae protein has improved, aided by transparent sourcing stories and third-party certifications. Up-cycled co-products further elevate sustainability credentials without compromising taste. Regulatory acceptance of novel proteins in North America and Europe is steadily advancing, smoothing market entry. Future share shifts will depend on the cost parity of insects and plant blends versus traditional meats, alongside consumer acceptance. Premiumization will remain strongest where ingredient stories combine health functionality with environmental responsibility.

By Sales Channel:

Specialty expertise and digital disruptionSpecialty pet stores preserved 52.5% channel share in 2024 by offering curated assortments and informed staff consultations. Their authority on nutrition fosters consumer confidence, especially for first-time topper users. Shelf placement alongside therapeutic diets encourages trial purchases. Meanwhile, online retail is expanding at a 10.4% CAGR as subscription services automate replenishment and widen geographic reach. Supermarkets and hypermarkets cater to value seekers with mainstream toppers, while veterinary clinics grow as gateways for condition-specific products.

Omnichannel strategies now dominate brand planning companies, harmonizing pricing and promotions across physical and digital shelves. Data from direct-to-consumer portals feed agile product development, narrowing time to market for functional innovations. Click-and-collect programs bridge convenience and expertise, allowing shoppers to pick up online orders at specialty stores. Over the forecast window, specialty outlets will keep authority status, but the bulk of incremental cat and dog food topper market growth will come from e-commerce efficiencies and personalized subscription models.

Geography Analysis

North America Cat And Dog Food Topper Market

North America held 43.1% of 2024 revenue as households maintained high per-pet spending and embraced functional nutrition. Mature distribution networks and consistent Association of American Feed Control Officials guidance underpin rapid innovation cycles. The United States drives volume through awareness campaigns and frequent veterinary visits that legitimize health-oriented toppers. Canada supports cross-border product flows via simplified supplement import regulations enacted in 2024. The region’s growth pace is accelerating, shifting from 6.8% CAGR in 2019-2024 to a projected 8.1% through 2030.

APAC and Oceania Cat And Dog Food Topper Market

Asia-Pacific is advancing at a 10.6% CAGR, the fastest globally, fueled by rising disposable incomes, urban lifestyles, and digital commerce penetration. Vietnam exemplifies breakout momentum with a projected 9.1% CAGR as middle-class owners adopt premium meal enhancers. China’s online marketplaces leverage influencer marketing to highlight ingredient transparency, attracting younger, educated consumers. Japan’s aging pet population spurs demand for senior-specific functional toppers, while Australia maintains steady premium uptake. Price sensitivity still restrains adoption in India and Indonesia, pushing brands to introduce trial-size packs.

Europe Cat And Dog Food Topper Market

Europe balances sustainability leadership with moderate volume growth. Western European consumers prioritize eco-friendly claims, prompting rapid uptake of insect-based and up-cycled meat toppers. Germany and the United Kingdom spearhead premium innovation, whereas France, Spain, and Italy see growing functional awareness. Inflation has expanded private-label offerings store brands gained a 25% share in late 2024 as shoppers traded down. Eastern Europe’s growth remains uneven amid currency volatility, yet long-term fundamentals are positive given rising pet ownership. Regulatory harmonization on novel proteins is improving, promising smoother pan-European rollouts.

Competitive Landscape

The cat and dog food topper market is moderately fragmented, with the top companies holding a significant combined share, leaving room for agile challengers. Global conglomerates such as Mars, Incorporated and Nestle Purina PetCare leverage scale, research budgets, and halo brands to defend shelf space. These leaders invest heavily in freeze-drying assets and microbiome research, underpinning premium positioning with science-backed claims. They also expand digital engagement, illustrated by Purina’s strong presence in e-commerce, which constitutes a major portion of Nestle Purina PetCare's online pet care sales.

Mid-tier companies gain ground by targeting niche health concerns or ethical sourcing gaps. Stella and Chewy’s, Primal Pet Foods, and Open Farm capitalize on raw nutrition expertise and transparent ingredient stories. Strategic partnerships with co-packers facilitate rapid line extension without heavy capital outlays. Vacuum-coating technology from suppliers such as Dinnissen enhances nutrient retention, offering smaller players performance parity with multinationals[3]Dinnissen, “Improving petfood safety and quality,” dinnissen.com. Acquisition appetite among large consumer-goods firms remains high, exemplified by General Mills’ USD 1.45 billion purchase of Whitebridge Pet Brands in 2025, which broadened its topper and supplement footprint.

Start-ups deploy direct-to-consumer models to bypass traditional retail and gather rich customer data. Subscription-based newcomers emphasize personalization algorithms that match topper functions to pet life stages and chronic issues. Investor interest continues as pet-tech solutions blur lines between nutrition and health monitoring. Competitive intensity overall is climbing, with more than 100 new topper Stock Keeping Units debuting at major trade shows in 2025 alone. Sustained differentiation now hinges on clinical validation, credible sustainability credentials, and omnichannel execution.

Cat And Dog Food Topper Industry Leaders

-

Mars, Incorporated

-

Nestle Purina PetCare (Nestle S.A.)

-

Blue Buffalo Company, Ltd. (General Mills Inc.)

-

Wellness Pet, LLC

-

Stella & Chewy's

- *Disclaimer: Major Players sorted in no particular order

Cat And Dog Food Topper Market Companies Covered in this Report

- Mars, Incorporated

- Nestle Purina PetCare (Nestle S.A.)

- Blue Buffalo Company, Ltd. (General Mills Inc.)

- Wellness Pet, LLC

- Stella & Chewy's

- The Honest Kitchen

- Primal Pet Foods (Primal Pet Group)

- Open Farm Inc.

- PetChef

- Rachael Ray Nutrish (The J. M. Smucker Company)

- Nature's Variety

- Instinct Pet Food (Agrolimen S.A.)

- Zesty Paws (H&H Group)

- Petcurean

- Solid Gold

Recent Industry Developments in Cat And Dog Food Topper Market

- May 2025: Pedigree introduced Drizzlers, a sauce that can be added to dog food to enhance flavor and texture. The product comes in four flavors and aligns with the increasing consumer demand for pet food enhancers and premium dining options for pets.

- April 2025: Natoo Pet Foods introduced four broth-based meal toppers for dogs and cats. The product line includes salmon with pumpkin and chicken with sweet potato and broccoli variants.

- March 2025: Natural Balance and Canidae unveiled over 100 new and reformulated toppers at Global Pet Expo.

- August 2024: Wellness Pet introduced Bowl Boosters Hearty Toppers at SUPERZOO 2024, offering nutritional and flavor enhancements for dog meals. The toppers feature varied textures and nutrient-dense ingredients to support overall canine health.

Global Cat And Dog Food Topper Market Report Scope

A cat and dog food topper is a supplementary product added to a pet’s regular meals to enhance flavor, nutrition, or health benefits.

The Cat and Dog Food Toppers Market Report is segmented by Product Form (Freeze-Dried Raw Toppers, Powdered Toppers, Liquid/Broth Toppers, Wet Meal Mixers, Semi-Moist/Gravy Toppers), Pet Type (Dog, Cat), Ingredient Source (Animal-Based, Plant-Based, Insect-Based), Sales Channel (Specialty Pet Stores, Supermarkets and Hypermarkets, Online Retail, Veterinary Clinics, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are provided in terms of Value (USD).

Segmentation Overview

| Freeze-dried Raw Toppers |

| Powdered Toppers |

| Liquid/Broth Toppers |

| Wet Meal Mixers |

| Semi-Moist/Gravy Toppers |

| Dog |

| Cat |

| Animal-based |

| Plant-based |

| Insect-based |

| Specialty Pet Stores |

| Supermarkets and Hypermarkets |

| Online Retail |

| Veterinary Clinics |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Form | Freeze-dried Raw Toppers | |

| Powdered Toppers | ||

| Liquid/Broth Toppers | ||

| Wet Meal Mixers | ||

| Semi-Moist/Gravy Toppers | ||

| By Pet Type | Dog | |

| Cat | ||

| By Ingredient Source | Animal-based | |

| Plant-based | ||

| Insect-based | ||

| By Sales Channel | Specialty Pet Stores | |

| Supermarkets and Hypermarkets | ||

| Online Retail | ||

| Veterinary Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the cat and dog food topper market be by 2030?

Projections place the market at USD 5.8 billion by 2030, reflecting an 8.3% CAGR from 2025.

Which product form currently leads sales?

Freeze-dried raw toppers held 37.0% share in 2024, the largest among all formats.

What is the fastest-growing sales channel for toppers?

Online retail is expanding at a 10.4% CAGR as subscriptions drive repeat purchases.

Which region shows the highest growth momentum?

Asia-Pacific leads with a 10.6% CAGR, propelled by rising incomes and digital commerce adoption.

Page last updated on: