Pet Food Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

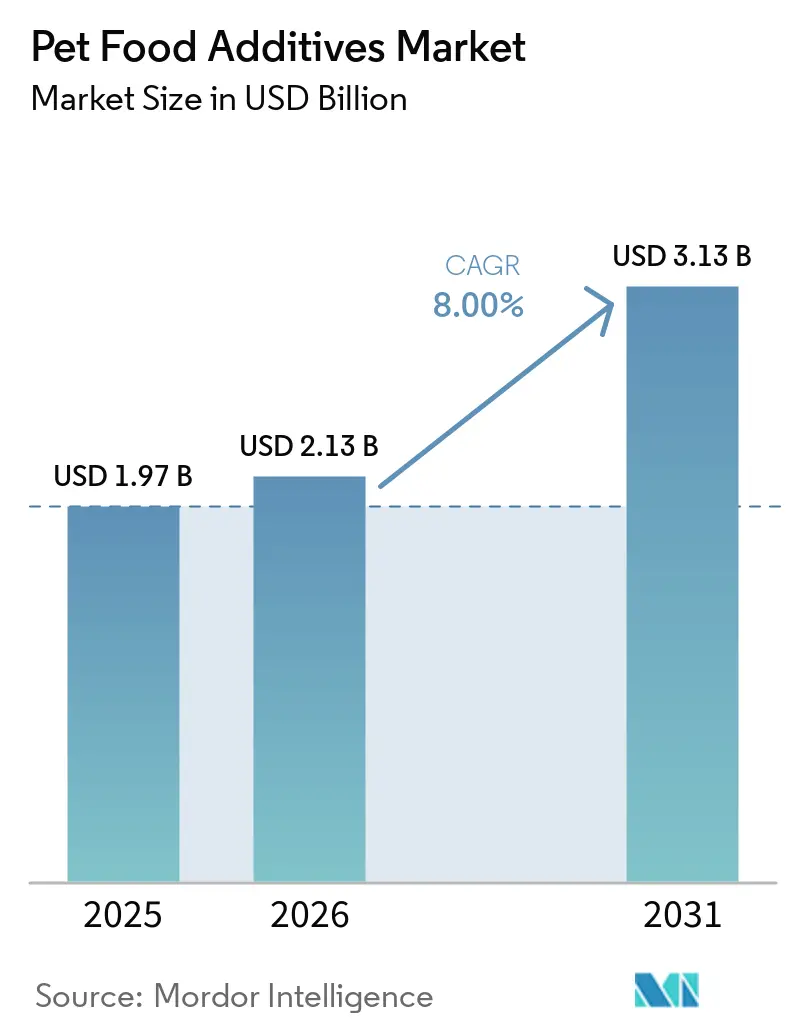

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 8.00% CAGR |

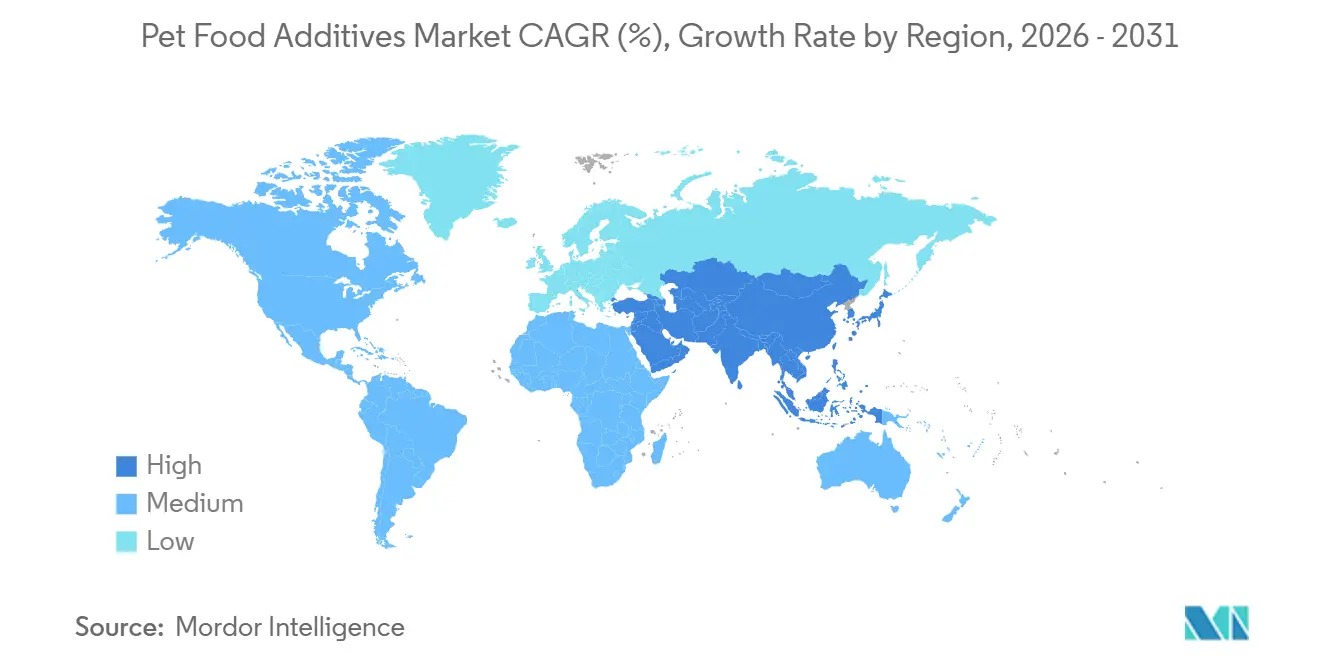

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Additives Market Analysis by Mordor Intelligence

The pet food additives market size is projected to expand from USD 1.97 billion in 2025 and USD 2.13 billion in 2026 to USD 3.13 billion by 2031, registering a CAGR of 8.0% between 2026-2031. Reformulation momentum is accelerating as brand owners position additive transparency as a proxy for pet wellness, catalyzing demand for functional vitamins, probiotics, enzymes, and clean-label antioxidants. Spending gravitates toward solutions that address gut health, joint support, and cognitive vitality, reflecting the convergence of companion-animal nutrition with mainstream human-wellness trends. Rapid adoption of encapsulation technologies allows manufacturers to protect heat-sensitive bioactives during extrusion, while digital B2B marketplaces lower sourcing barriers for emerging regional brands. Competitive vigor centers on speed-to-claim, with suppliers investing in peer-reviewed feeding trials to substantiate health benefits under Association of American Feed Control Officials and European Pet Food Industry Federation frameworks.

Key Report Takeaways

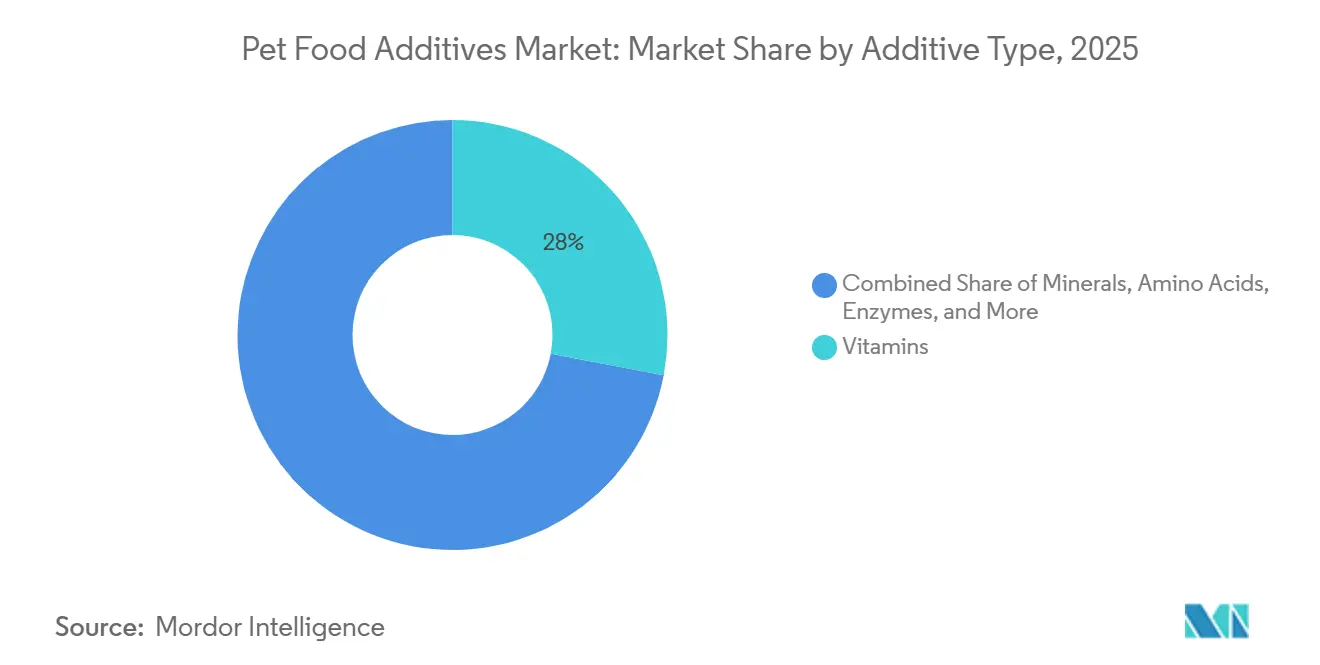

- By type, vitamins were the largest, capturing 28% of the pet food additives market share in 2025, whereas probiotics and prebiotics are projected to post the fastest 10.9% CAGR over 2026–2031.

- By pet type, the dog segment held the largest 46% share of the pet food additives market in 2025, while the cat segment is forecast to grow at the fastest 9.4% CAGR during 2026–2031.

- By form, dry additives were the largest category at 57% share in the pet food additives market size in 2025, and encapsulated formats are set for the fastest 12.8% CAGR through 2026–2031.

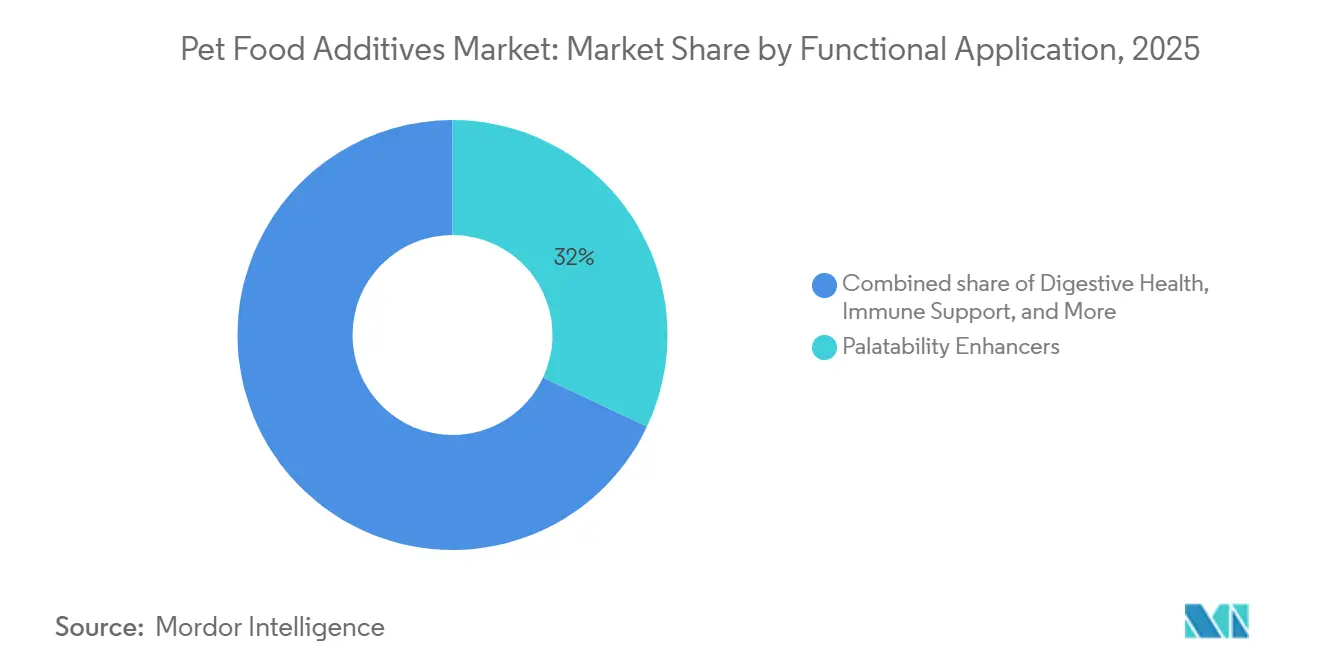

- By functional application, palatability enhancers held the largest 32% share of the pet food additives market size in 2025, while the digestive health solutions will achieve the fastest 11.2% CAGR over 2026–2031.

- By distribution channel, direct sales to pet food manufacturers accounted for the largest 64% share of the pet food additives market size in 2025, and the online B2B marketplaces will post the fastest 13.6% CAGR for 2026–2031.

- By geography, North America accounted for the largest 35% share of the pet food additives market size in 2025, whereas Asia-Pacific is projected to grow at the fastest 9.5% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing human-grade clean-label reformulations | +1.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Shift toward functional nutrition (gut, joint, cognitive health) | +1.6% | Global, prominent in North America and Asia-Pacific urban centers | Long term (≥ 4 years) |

| Escalating premiumization in emerging economies | +1.4% | Asia-Pacific core with spill-over to the Middle East and South America | Medium term (2-4 years) |

| Tailored additive blends for breed-specific diets | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Expansion of insect-protein based palatant systems | +0.7% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Circular economy demand for up-cycled co-product additives | +0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Human-Grade Clean-Label Reformulations

Manufacturers continue to replace generic animal-digest palatants with species-named hydrolysates and swap synthetic vitamins for whole-food concentrates, responding to consumers who now scrutinize ingredient panels as closely as their own food. In 2024, 41% of the United States dog owners bought premium formulations, a 5% jump from 2023, while premium cat-food penetration rose nine points to 38%, a signal that transparency carries a pricing premium in feline categories[1]American Pet Products Association, “The American Pet Products Association (APPA) Releases 2025 Dog & Cat Report,” americanpetproducts.org.. To capture this demand, DSM-Firmenich extended its Veramaris algal omega-3 line in 2025 with higher eicosapentaenoic acid concentration per dose, showcasing traceable microalgae inputs that bypass marine-fish supply risk. Regulatory clarity also improved after the United States Food and Drug Administration issued an enforcement update in 2024 that aligned label descriptors with Association of American Feed Control Officials definitions, enabling faster reformulation cycles.

Shift Toward Functional Nutrition (Gut, Joint, Cognitive Health)

Supplement adoption continues to surge as owners seek proactive health management. The United States dog-supplement usage reached 53% of owners in 2024, a 56% jump since 2018. Suppliers respond with evidence-based ingredients, such as Evonik Industries’ enhanced Ecobiol probiotic, released in 2025, which shows improved colonization in the pet gut. Joint-mobility blends combining glucosamine and collagen peptides gain traction for aging pets, whereas medium-chain triglycerides and phosphatidylserine address cognitive decline. Brands differentiate by underwriting peer-reviewed feeding trials that meet the European Pet Food Industry Federation's guidelines, reinforcing the scientific foundation for functional claims.

Escalating Premiumization in Emerging Economies

Higher disposable incomes in the Asia-Pacific and Middle Eastern markets compress the adoption curve for novel additives. According to the United States Department of Agriculture, China’s pet sector reached USD 43.4 billion in 2025, underpinned by urban millennials who treat pets as family and prefer products with visible quality cues, such as probiotic colony counts[2]United States Department of Agriculture Foreign Agricultural Service, “China Pet Food Market Update 2026,” fas.usda.gov.. Symrise addressed this surge in February 2026 by inaugurating a palatant plant in Querétaro, Mexico, that localizes high-intensity flavors and cushions tariff exposure for South American buyers. Harmonized standards across Southeast Asia, modeled on Codex Alimentarius, streamline cross-border ingredient flow, trimming compliance costs for multinational suppliers.

Tailored Additive Blends for Breed-Specific Diets

Data-driven personalization allows manufacturers to engineer nutrient packages calibrated for breed genetics and activity profiles. DSM-Firmenich opened a fully automated pet-only premix facility in Tonganoxie, Kansas (United States) in 2025, designed for small-batch production that supports breed-targeted recipes without lengthy lead times. Large-breed puppies benefit from controlled calcium and phosphorus to avert orthopedic disorders, while brachycephalic dogs require aroma-intense palatants to offset reduced olfactory ability. Direct-to-consumer platforms aggregate owner-reported data, then source flexible premixes from suppliers capable of rapid formulation pivots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory hurdles on novel feed ingredients | -0.8% | Global, acute in the European Union and China | Short term (≤ 2 years) |

| Price volatility of key micronutrients | -0.6% | Global, pronounced in import-dependent regions | Short term (≤ 2 years) |

| Consumer pushback on synthetic antioxidants | -0.5% | North America and Western Europe | Medium term (2-4 years) |

| Supply-chain vulnerability for specialty enzymes | -0.4% | Global, critical in tropical markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles on Novel Feed Ingredients

Authorization timelines in the European Union can exceed 2 years, delaying the commercialization of precision-fermented or insect-derived additives. China’s General Administration of Customs heightened this risk in 2024 by banning specific New Zealand avian-based inputs due to biosecurity concerns, abruptly halting shipments and stranding inventories[3]New Zealand Ministry of Foreign Affairs and Trade, “China Export Sector Update: Pet Food,” mfat.govt.nz.. Suppliers now pursue pre-submission consultations and Generally Recognized as Safe determinations in the United States to establish precedents that ease foreign approvals.

Price Volatility of Key Micronutrients

Concentrated upstream capacity for vitamins and trace minerals means a single plant outage can lift spot prices by 30%, creating margin instability for brands that lack long-term contracts. Evonik Industries raised MetAMINO DL-methionine prices by 10% in March 2026, demonstrating how raw-material inflation and tight supply quickly cascade into higher costs for pet food formulators. Vitamin A output is clustered among a handful of producers, so fires or regulatory shutdowns can erase capacity overnight and force smaller manufacturers to absorb cost shocks or pursue risky reformulations that threaten nutritional adequacy. Leading suppliers hedge exposure through multi-year agreements, diversified regional sourcing, and fermentation-based vitamin production, reducing reliance on petrochemical feedstocks susceptible to energy-price swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Probiotics Propel Category Expansion

Vitamins held the largest 28% market share of pet food additives in 2025, reflecting their mandatory role in complete-and-balanced recipes. Probiotics and prebiotics will deliver the fastest 10.9% CAGR during 2026-2031 as brand owners target gut-health claims supported by peer-reviewed trials. Together, the two segments illustrate how regulatory essentials and wellness trends drive complementary growth paths within the market size. Suppliers balance cost and efficacy by blending vitamin concentrates with strain-specific probiotics that withstand the heat of extrusion.

Minerals followed with a moderate share, buoyed by chelated trace elements that improve bioavailability in high-protein kibble. Antioxidants are shifting toward natural tocopherols and rosemary to replace synthetic options under clean-label pressure. Enzymes expand steadily as processors use phytase and protease to boost plant-protein digestibility. Flavors, sweeteners, colorants, and preservatives remain smaller niches yet are essential for palatability, shelf life, and visual consistency.

By Pet Type: Cat Nutrition Outpaces Canine Staples

Dog formulations captured the largest 46% pet food additives market share in 2025, supported by a broad global canine population and high per-animal spending. Cat-specific additives will post the fastest 9.4% CAGR for 2026-2031 as urban households in Asia-Pacific favor low-maintenance pets that require taurine-rich diets. The interplay of these two species defines near-term demand curves and guides R and D priorities. Brands enhance value propositions by tailoring palatants and nutrient blends to species-unique physiology.

Fish, bird, and small-mammal segments remain niche but profitable for suppliers of carotenoids, vitamin D3, and vitamin C. Each niche relies on specialized additives that address ornamental color, bone integrity, or endogenous synthesis gaps. Although volumes are lower, margin potential is attractive because owners of exotic pets pay premiums for targeted nutrition. Continuous education of specialty retailers supports incremental uptake across these smaller categories.

By Form: Encapsulation Unlocks Stability Advantage

Dry additives retained the largest 57% market share in 2025, owing to easy handling, long shelf life, and seamless integration into kibble processing. Encapsulated formats will log the fastest 12.8% CAGR from 2026-2031 as processors safeguard heat-sensitive probiotics, enzymes, and omega-3 oils during extrusion. This divergence underscores how stability concerns are reshaping the pet food additives market size by delivery technology. Coated beadlets and lipid-matrix microcapsules also enable controlled intestinal release, boosting efficacy.

Liquid additives are commonly utilized in wet foods and gravies due to their ability to evenly distribute flavors, oils, and functional ingredients throughout the formulation. Their use enhances palatability and ensures consistent nutrient delivery. However, they often necessitate the use of preservatives and temperature-controlled storage, leading to higher operational costs, particularly in humid regions. To mitigate these issues, manufacturers are introducing hybrid powder-in-oil formats, which integrate the benefits of liquid additives with the storage and handling advantages of dry ingredients. This development is encouraging increased investment in flexible formulations designed to support varied pet food production processes.

By Functional Application: Digestive Health Drives Demand Upswing

Palatability enhancers accounted for the largest 32% of the pet food additives market share in 2025, confirming that taste drives repeat purchases and minimizes food waste. Digestive-health additives will register the fastest 11.2% CAGR over 2026-2031 as strain-validated probiotics address stool quality and immune modulation. The contrast shows how sensory appeal and functional science jointly expand market size without cannibalizing each other. Manufacturers often co-dose palatants and prebiotics to achieve simultaneous acceptance and health outcomes.

Immune-support blends are becoming more prominent due to the inclusion of beta-glucans and antioxidant vitamins, which enhance innate immune defenses. Joint and mobility solutions are increasingly focused on senior pets, utilizing ingredients such as glucosamine, chondroitin, and collagen peptides. Skin and coat formulations emphasize balanced omega fatty acids and biotin. Cognitive health additives, while still an emerging category, are drawing increased research and development efforts as pet lifespans extend. Regulatory variations regarding health claims continue to impact formulation choices and marketing strategies across different regional markets.

By Distribution Channel: Digital B2B Platforms Accelerate Market Access

Direct sales to pet food manufacturers accounted for the largest 64% market share in 2025, owing to embedded technical service relationships and multi-year contracts. Online B2B marketplaces will post the fastest 13.6% CAGR during 2026-2031 as small brands source specialty enzymes and custom premixes with minimal inventory. This shift illustrates how digitalization and long-standing partnerships now coexist in shaping the size of the pet food additives market. Suppliers differentiate on documentation quality and just-in-time delivery to preserve customer loyalty.

Premix and contract manufacturers are essential in offering blending expertise, formulation support, and regulatory compliance services to brands without in-house production capabilities. Specialty ingredient distributors enhance geographic reach and provide localized technical support in regions where direct supplier operations are not cost-effective. Channel participants are increasingly required to meet demands for traceability, Certificates of Analysis, and compliance with Hazard Analysis and Critical Control Point (HACCP) standards.

Geography Analysis

North America captured the largest 35% pet food additives market share in 2025, supported by high pet ownership rates and a mature premium segment. The region benefits from clear United States Food and Drug Administration guidance that accelerates novel-ingredient approvals and lowers compliance uncertainty. Asia-Pacific will post the fastest 9.5% CAGR during 2026-2031 as rising household incomes and regulatory harmonization ease market entry for new additives. Together, these two regions set the pace for global demand by combining spending power with expanding product portfolios.

Europe, South America, the Middle East, and Africa collectively add meaningful volume and diversification. Europe maintains stable growth as consumers pay premiums for sustainability-certified additives such as Marine Stewardship Council approved krill meal. South America gains momentum as Brazil and Argentina invest in local premix blending to cut import reliance. Middle Eastern and African markets advance on the back of urbanization and growing pet ownership among younger demographics.

Regional ecosystems are projected to strengthen as suppliers localize production, expand cold-chain logistics, and collaborate with regulators on faster dossier reviews. Investment in flavor plants, premix facilities, and e-commerce distribution hubs shortens lead times and widens access to ingredients. Multinational companies leverage joint ventures to share technical know-how and reduce tariff exposure. These developments position all regions to unlock additional layers of the pet food additives market size through 2031 and beyond.

Competitive Landscape

The market is moderately fragmented, with the top five players, DSM-Firmenich AG, Cargill, Incorporated, Archer Daniels Midland Company, BASF SE, and Kemin Industries, together holding a majority share of the pet food additives market size in 2025. DSM-Firmenich AG leads by leveraging a fully automated Kansas premix plant that unites blending, quality control, and just-in-time delivery. Cargill, Incorporated followed closely and deepened its South American reach in 2025 by acquiring Mig-Plus, adding local premix capacity that trims freight costs. Both leaders pair vertical integration with sustainability programs that emphasize algae-based omega-3 oils and regenerative supply chains to defend premium pricing.

Archer Daniels Midland Company and BASF SE round out the top cohort by bundling amino acids, vitamins, and functional lipids into turnkey solution sets that shorten customer development cycles. Kemin Industries maintains a strong franchise and, in 2025, launched PALIVATE, a wet-food flavor system that masks the bitterness of functional additives. Evonik Industries AG and Novus International Inc. focus on fermentation-derived methionine and chelated minerals that reduce carbon intensity. Nutreco N.V., Alltech Inc., Symrise AG, Adisseo S.A.S., Lesaffre et Compagnie S.A., Lallemand Inc., Prinova Group LLC, and Aker BioMarine ASA compete through specialty niches such as insect proteins, yeast-based probiotics, krill phospholipids, and custom nutrient premixes.

Competitive momentum is projected to intensify as companies funnel capital into precision fermentation assets, artificial intelligence formulation engines, and region-specific production hubs. Strategic partnerships, such as the 2026 alliance between Archer Daniels Midland Company and Alltech Inc., signal a shift toward portfolio bundling that raises switching costs for pet food manufacturers. Suppliers also court regulatory bodies early to accelerate dossier approvals and secure first-mover advantage on novel claims. These actions position the competitive set to expand the overall pet food additives market by unlocking new health-focused use cases and penetrating untapped geographic markets.

Pet Food Additives Industry Leaders

Archer Daniels Midland Company

BASF SE

Kemin Industries

DSM-Firmenich AG

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSM-Firmenich has expanded its pet nutrition portfolio with the introduction of Veramaris O3 Max Pure, an algal omega-3 ingredient with a high concentration of Eicosapentaenoic Acid (EPA) and traceable microalgae-based sourcing. This product enables clean-label pet food formulations, reduces dependence on marine fish oils, and addresses sustainability challenges.

- April 2026: Symrise announced a strategic investment in Bond Pet Foods to scale precision fermentation technology for cultivated proteins, positioning the company to offer next-generation palatants derived from animal-cell cultures that deliver consistent flavor profiles without traditional rendering processes.

- October 2024: The United States Food and Drug Administration published an updated enforcement policy for Association of American Feed Control Officials-defined animal feed ingredients, replacing 1980 and 1995 compliance policy guides and providing clearer pathways for novel-ingredient approvals and labeling claims.

Global Pet Food Additives Market Report Scope

Pet food additives are substances deliberately included in pet food, such as preservatives, antioxidants, colorants, or flavor enhancers, to enhance taste, texture, safety, or shelf life. The pet food additives market report is segmented by additive type (vitamins, minerals, amino acids, enzymes, probiotics and prebiotics, antioxidants, flavors and sweeteners, colorants, preservatives, and other additives), by pet type (dog, cat, and other pets), by form (dry, liquid, and encapsulated), by functional application (palatability enhancers, digestive health, immune support, joint and mobility, skin and coat, and other applications), by distribution channel (direct to pet food manufacturer, premix and contract manufacturer, specialty ingredient distributor, and online B2B marketplace), and by geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Vitamins |

| Minerals |

| Amino Acids |

| Enzymes |

| Probiotics and Prebiotics |

| Antioxidants |

| Flavors and Sweeteners |

| Others |

| Dog |

| Cat |

| Other Pets |

| Dry |

| Liquid |

| Encapsulated |

| Palatability Enhancers |

| Digestive Health |

| Immune Support |

| Joint and Mobility |

| Skin and Coat |

| Others |

| Direct to Pet Food Manufacturer |

| Premix and Contract Manufacturer |

| Specialty Ingredient Distributor |

| Online B2B Marketplace |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Additive Type | Vitamins | |

| Minerals | ||

| Amino Acids | ||

| Enzymes | ||

| Probiotics and Prebiotics | ||

| Antioxidants | ||

| Flavors and Sweeteners | ||

| Others | ||

| By Pet Type | Dog | |

| Cat | ||

| Other Pets | ||

| By Form | Dry | |

| Liquid | ||

| Encapsulated | ||

| By Functional Application | Palatability Enhancers | |

| Digestive Health | ||

| Immune Support | ||

| Joint and Mobility | ||

| Skin and Coat | ||

| Others | ||

| By Distribution Channel | Direct to Pet Food Manufacturer | |

| Premix and Contract Manufacturer | ||

| Specialty Ingredient Distributor | ||

| Online B2B Marketplace | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current market size and long-term outlook?

The pet food additives market stands at USD 2.13 billion in 2026 and is projected to reach USD 3.13 billion by 2031, reflecting an 8.0% CAGR over 2026-2031.

What is driving the fastest growth in additive categories?

Probiotics and prebiotics will expand at 10.9% CAGR through 2026-2031, outpacing vitamins and minerals, as clinical evidence validates their role in digestive resilience and immune modulation.

Which region will lead the expansion over the forecast period?

Asia-Pacific will post a 9.5% CAGR to 2026-2031, propelled by rising incomes, urbanization, and regulatory harmonization that eases approvals for novel ingredients in China, India, and Southeast Asia.

How are regulatory hurdles affecting innovation timelines?

European Union novel-food authorization can exceed 24 months, delaying commercialization of precision-fermented and insect-derived additives, while China's import controls introduce abrupt market-access risk.

Which pet type is experiencing the fastest additive demand growth?

Cat-focused formulations will grow at a 9.4% CAGR through 2026-2031 as urban households in Asia-Pacific favor feline companionship and manufacturers develop taurine and arachidonic acid blends tailored to the physiology of obligate carnivores.

Page last updated on: