Fortified Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

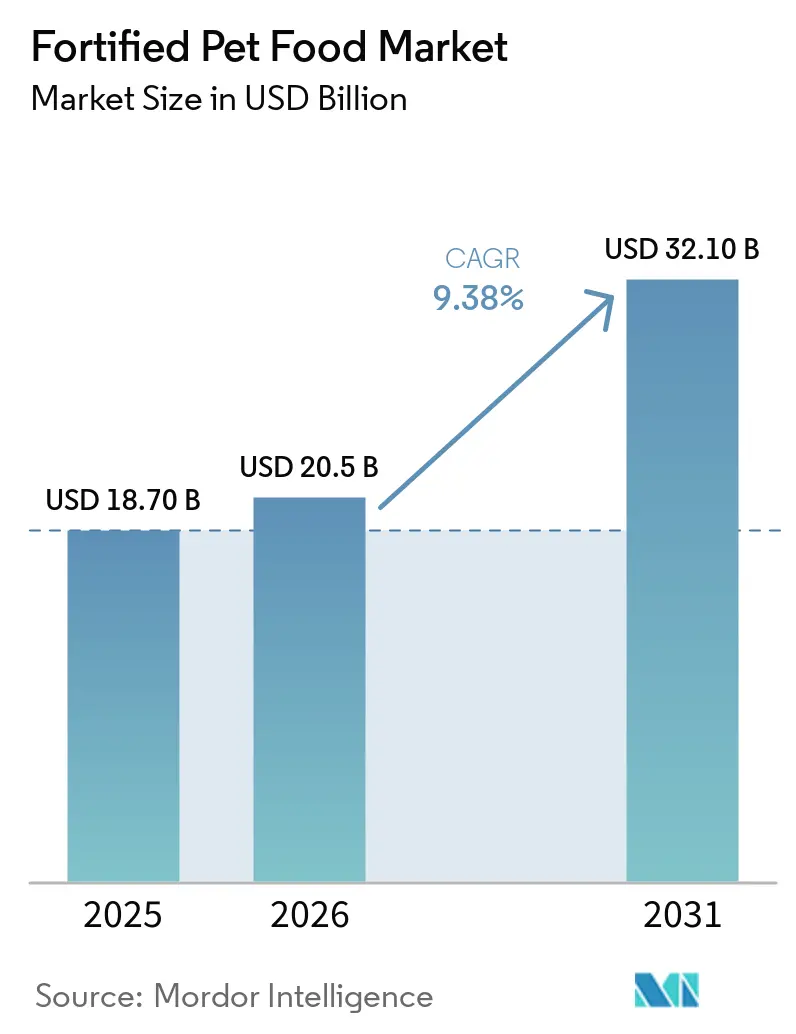

| Market Size (2026) | USD 20.5 Billion |

| Market Size (2031) | USD 32.10 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fortified Pet Food Market Analysis by Mordor Intelligence

The fortified pet food market size is anticipated to increase from USD 18.7 billion in 2025 to USD 20.5 billion in 2026 and reach USD 32.1 billion by 2031, growing at a CAGR of 9.38% over 2026-2031. Demand is propelled by pet humanization, clinical validation of functional ingredients, and rapid e-commerce penetration that makes premium fortified diets available beyond large metropolitan areas. Ingredient-level innovation, such as microencapsulation, is widening the fortification toolkit, while veterinary endorsement programs legitimize efficacy claims and lift willingness to pay. Regional momentum is shifting toward Asia-Pacific, where rising disposable incomes intersect with surging online retail, yet North America continues to dominate absolute spending through entrenched clinical channels and high per-patient outlays. Competitive strategies revolve around capacity expansion, fresh and hybrid formats, and data-enabled personalization that deepens brand stickiness inside the fortified pet food market.

Key Report Takeaways

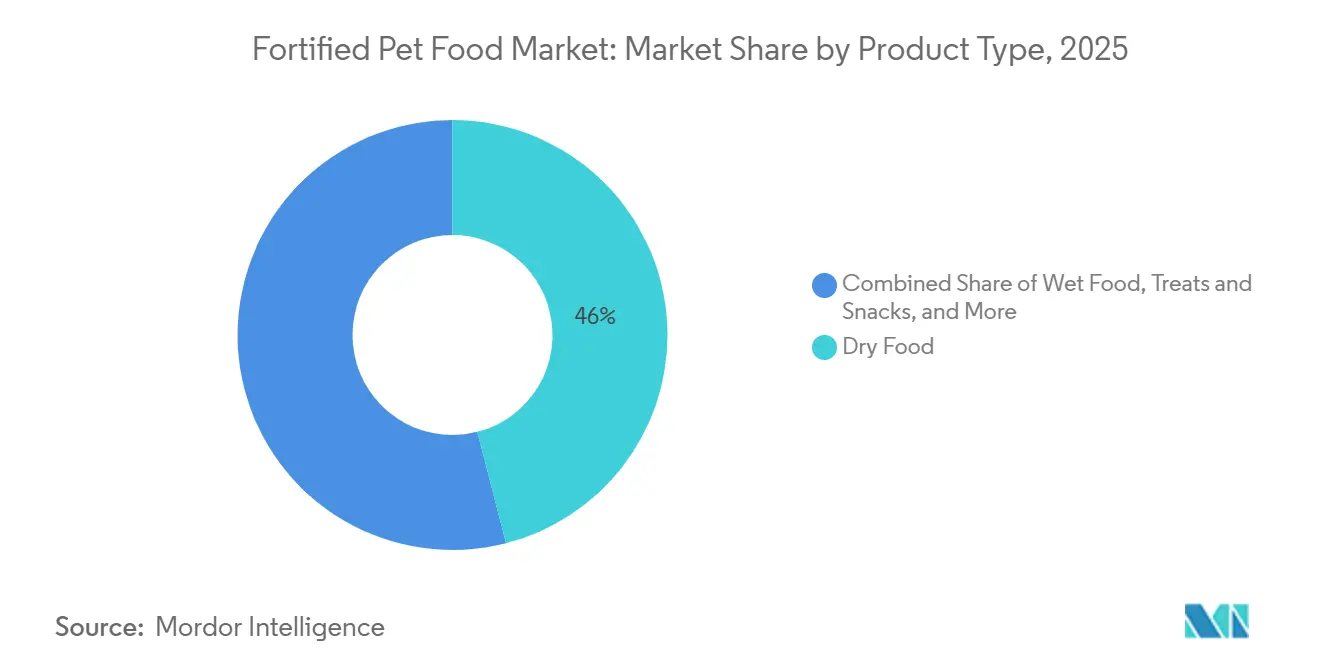

- By product type, dry food held the largest 46.0% share of the fortified pet food market size in 2025 value, whereas functional supplements are projected to post the fastest 13.8% CAGR over 2026-2031.

- By pet type, the dog segment captured the largest 58.0% fortified pet food market share in 2025 value, while cat formulations are projected to register the fastest 10.4% CAGR during 2026-2031.

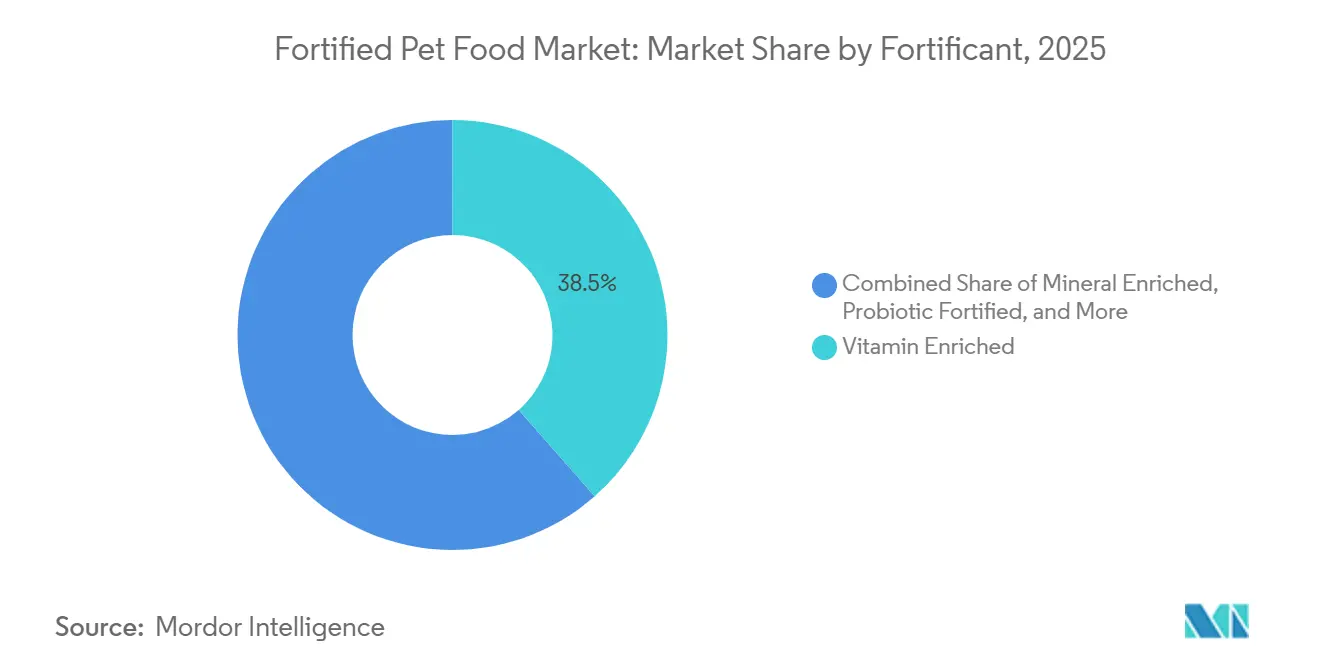

- By fortificant, vitamin-enriched diets accounted for the largest 38.5% fortified pet food market share in 2025 revenue, and probiotic fortified offerings are forecast to deliver the fastest 15.1% CAGR through 2026-2031.

- By distribution channel, supermarkets and hypermarkets commanded the largest 42.0% fortified pet food market share in 2025 value, whereas online retail is set to expand at the fastest 18.7% CAGR across 2026-2031.

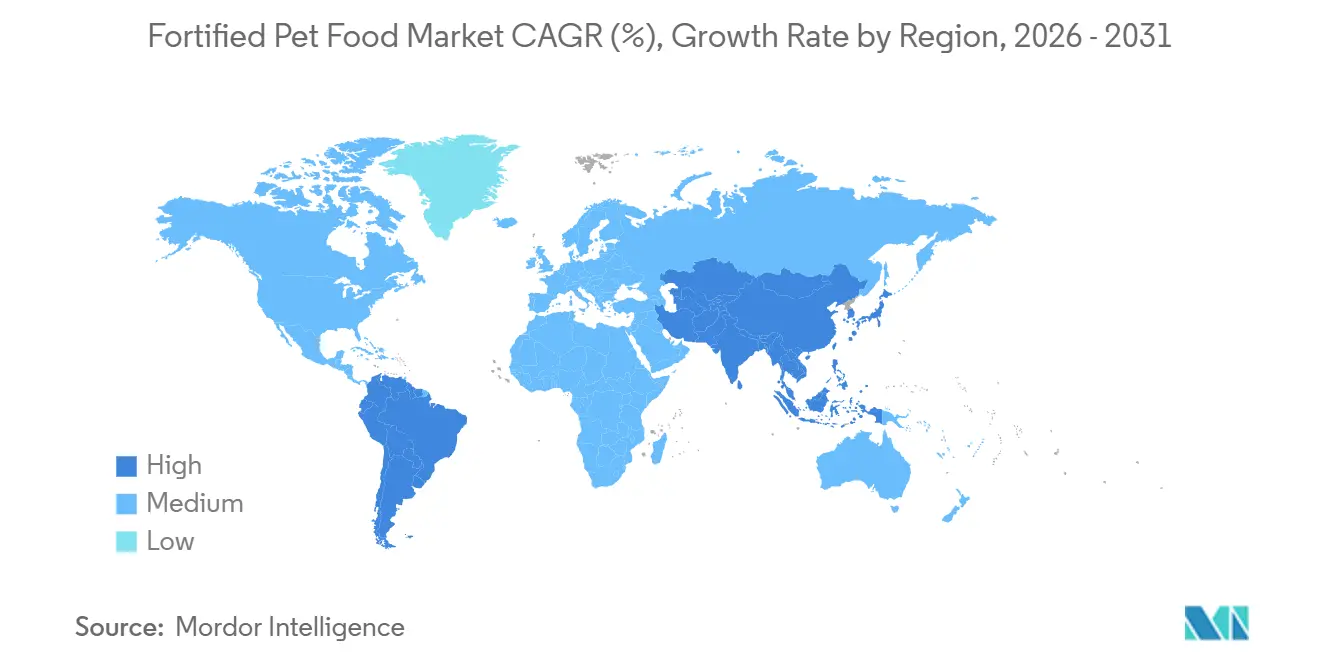

- By geography, North America retained the largest 35% fortified pet food market share in 2025 value, yet Asia-Pacific is poised for the fastest 11.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fortified Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Growth Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of pet diets | +2.1% | Global, with peak intensity in North America, Western Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Humanization trend in emerging markets | +1.8% | Asia-Pacific core, with spillover to the Middle East and South America | Long term (≥ 4 years) |

| Advancements in nutrient-microencapsulation | +1.3% | Global, led by North America and Europe's research and development hubs | Medium term (2–4 years) |

| Veterinary endorsement programs | +1.1% | North America and Europe, early adoption in Australia and New Zealand | Short term (≤ 2 years) |

| Rise of DNA-based personalized pet nutrition | +0.7% | North America and Western Europe early adopters | Long term (≥ 4 years) |

| Expansion of insect-based fortified proteins | +0.9% | Europe leading regulatory approvals, sustainability demand in the Asia-Pacific and South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Pet Diets

Upgrading to super-premium fortified formulas is a prominent trend reflecting the humanization of pets. According to the American Pet Products Association (APPA) 2025 State of the Industry Report, pet owner spending in the United States reached USD 158 billion in 2025[1]Source: American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” americanpetproducts.org.. Despite relatively stable pet food prices, this growth suggests that increased consumption volume, rather than inflation, is driving the fortified pet food market. Similar trends are emerging in other regions, where pet owners are increasingly opting for premium nutrition products enriched with functional ingredients such as omega-3 fatty acids, probiotics, and joint-support nutrients to enhance pet health and wellness.

Humanization Trend in Emerging Markets

Disposable income growth in China, India, and key Southeast Asian economies is driving stronger adoption of fortified pet food that mirrors human wellness trends. As reported in the China Pet Industry White Paper (2025), referenced by the State Council Information Office of China, the urban pet dog and cat market in the country reached CNY 300.2 billion (USD 41.3 billion) in 2024[2]Source: State Council Information Office of China, “China's Urban Pet Market Tops 300 Billion Yuan in 2024: Report,” english.scio.gov.cn.. This growth highlights the increasing expenditure on premium pet care products and specialized nutrition solutions. Comparable trends are observed in other developing markets, driven by rising pet ownership, higher disposable incomes, and the growth of e-commerce platforms. These factors are boosting demand for fortified pet foods containing functional ingredients aimed at enhancing overall pet health and wellness. Brands are introducing gently cooked fresh diets and kibble-wet hybrids that highlight whole-food ingredients, reflecting how human-grade cues are influencing the fortified pet food market.

Advancements in Nutrient-Microencapsulation

Heat-, moisture-, and oxygen-sensitive nutrients can now survive extrusion owing to microencapsulation that improves bioavailability and label-claim accuracy. According to a review published in the Frontiers in Nutrition journal in 2025, nanoencapsulation technologies help protect sensitive bioactive ingredients from degradation caused by heat, oxygen, moisture, and pH fluctuations. These technologies enhance the stability, solubility, and bioavailability of such ingredients. This is particularly significant for functional ingredients like probiotics, omega-3 fatty acids, vitamins, and antioxidants commonly used in fortified pet foods. By maintaining nutrient efficacy during processing and storage, microencapsulation allows manufacturers to include higher-value functional ingredients while ensuring consistent nutritional benefits. As demand for premium pet nutrition increases, these advancements are driving product innovation and growth in the fortified pet food market.

Veterinary Endorsement Programs

Clinic recommendations elevate consumer trust and accelerate the adoption of therapeutic fortified diets. Hill’s Prescription Diet remains the most recommended brand by United States veterinarians, leveraging practitioner education and in-clinic sampling. The Veterinary Oral Health Council list validates dental claims, steering shoppers toward enzyme-rich treats and foods[3]Source: Veterinary Oral Health Council, “Accepted Product List,” vohc.org . As Hill’s rolled its ActivBiome+ prebiotic system into mainstream Science Diet in 2025, the evidence-based halo expanded to wider price tiers. Brands that fund peer-reviewed trials secure durable advantages in the fortified pet food market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in specialty micronutrient costs | -1.4% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| Stringent fortification-labeling regulations | -0.9% | North America and Europe, limited impact in the Asia-Pacific | Medium term (2–4 years) |

| Limited shelf-life perception of probiotic formats | -0.6% | Global, stronger impact in North America and Western Europe | Medium term (2–4 years) |

| Ethical concerns around novel protein sources | -0.4% | North America and Europe have minimal impact in the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Specialty Micronutrient Costs

Peru reduced its 2026 anchovy quota by 36% to 1.91 million metric tons, cutting the primary raw material for fish oil that underpins omega-3 fortification and driving spot prices toward USD 5,000 per metric ton. Aquaculture accounts for over 70% of the global 1.2 million metric ton fish-oil supply, leaving pet food formulators to compete for shrinking residual volumes and expose them to sudden cost spikes. Vitamin premix pricing is equally erratic because environmental shutdowns at Chinese and Indian plants periodically constrict output and create supply gaps. Large manufacturers hedge through vertical integration and long-term contracts, whereas smaller brands must either raise retail prices or reformulate with alternative sources, such as krill oil from suppliers like Aker BioMarine, eroding competitiveness in premium segments.

Stringent Fortification Labeling Regulations

The Association of American Feed Control Officials Pet Food Label Modernization rules, effective January 2024, mandate a Pet Nutrition Facts box, stricter Complete criteria, and clear Purpose Statements, forcing brands to redesign packaging and validate nutrient profiles at high cost. Multinationals selling in Europe must also comply with nutrient-profile and health-claim verification protocols set by the European Food Safety Authority and the European Pet Food Industry Federation, which adds parallel documentation and testing layers. These combined frameworks raise entry barriers for start-ups that lack in-house regulatory expertise, effectively consolidating share among larger incumbents that can amortize compliance spending across wider portfolios. Over time, the stricter rules should improve consumer trust in functional claims, yet near-term they lengthen development timelines and delay launches of novel fortified recipes in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Supplements Lead Growth Velocity

Dry food held the largest share, accounting for 46.0% of the fortified pet food market size in 2025, but the fortified pet food market tied to dry kibble is projected to rise only modestly as consumers migrate toward fresh and wet textures. Functional supplements are forecast to grow at the fastest rate, with a 13.8% CAGR, catering to joint, gut, and immune needs that cannot be addressed by base diets alone. Treats and snacks benefit from daily-use dental products endorsed by the Veterinary Oral Health Council, reinforcing loyalty to fortified regimens. Wet food’s projected significant CAGR growth is underpinned by new capacity, such as the USD 85 million Brazilian plant Mars opened in 2025.

The fortified pet food market share commanded by functional supplements is likely to expand as owners layer chewables and toppers onto kibble, reflecting an unbundling of nutrition. Regulatory clarity under the 2024 labeling rules, which separate complete diets from supplements, should filter out exaggerated claims and steer spending toward clinically backed products. Dry food is unlikely to disappear, yet future success will hinge on palatability upgrades and microencapsulated inclusions that keep the segment relevant for value-conscious shoppers.

By Pet Type: Feline Fortification Gains Momentum

Dog held the largest share, accounting for 58.0% of the fortified pet food market in 2025, though obesity management formulas are showing faster momentum than general canine kibble. The cat segment has recorded a significant share, but rising apartment living and targeted urinary or hairball solutions are driving the fortified pet food market for feline offerings to grow at the fastest rate, with a 10.4% CAGR through 2026-2031. Others, covering small mammals and exotics, remain a sub-1% niche yet draw high spend per kilogram from dedicated owners.

Veterinary advocacy regarding feline-specific nutritional needs is contributing to the introduction of premium wet food and probiotic products aimed at addressing common health issues in indoor cats. Companies that integrate veterinary education efforts with online subscription-based distribution models are well-positioned to expand their market share. Meanwhile, canine-focused brands must enhance their product portfolios in areas such as dental care, mobility support, and weight management to maintain competitiveness. Failure to do so may result in increased investment in shelf space, product development, and innovation being directed toward the faster-growing feline segment within the fortified pet food market.

By Fortificant: Probiotics Surge on Gut Health Science

Vitamin-enriched formulas accounted for the largest share of 2025 revenue, with 38.5%, driven by regulatory mandates that anchor complete and balanced diets. In contrast, probiotic-fortified products are the fastest-growing subcategory, projected to grow at a 15.1% CAGR between 2026 and 2031 as clinical trials validate digestive and immune benefits. The coexistence of a mandatory baseline segment and a science-driven breakout category underscores how functional evidence is reshaping consumer priorities inside the fortified pet food market. Rising veterinary endorsements and microencapsulation technologies further accelerate the shift toward live-culture inclusions that differentiate premium labels.

Omega-3-fortified diets held a significant share, but supply-chain tensions around fish oil are pressuring formulation costs and spurring interest in algal and krill alternatives. Mineral-enriched recipes accounted for a limited share, limited by perceptions that basic minerals add little incremental value beyond compulsory levels. Multi-functional blends combining vitamins, probiotics, and omega-3s captured descent share of turnover and are growing rapidly as shoppers seek all-in-one convenience. Together, these remaining segments provide stepping-stone options for consumers transitioning from baseline nutrition to specialized fortification.

By Distribution Channel: E-Commerce Redefines Access

Supermarkets and hypermarkets held the largest share, accounting for 42.0% of the fortified pet food market size in 2025, driven by store traffic and impulse buying. Online retail is the fastest-growing channel, forecast to grow at 18.7% CAGR over 2026-2031, as subscription services and data-driven personalization expand the fortified pet food market. Physical shelf dominance is therefore giving way to digital discovery, particularly in emerging economies where e-commerce leapfrogs brick-and-mortar constraints. Brands that master cold-chain logistics for fresh fortified meals and integrate genetic or wearable data are poised to win in this high-velocity space.

Specialty pet stores accounted for a prominent share and are projected to grow rapidly, supported by knowledgeable staff and curated premium assortments that foster shopper trust. Veterinary clinics contributed a decent share and will grow at a decent CAGR as therapeutic diets maintain clinician endorsement despite a limited footprint. Farm and feed outlets, along with other channels, reflect growth as rural consumers rely on value offerings rather than premium fortification. Collectively, these channels illustrate a balanced ecosystem in which expertise-driven outlets bolster confidence while digital platforms unlock convenience and customization.

Geography Analysis

North America retained the largest market share at 35% of 2025 revenue, supported by high per-pet spending and entrenched veterinary endorsement programs. Capacity additions such as Mars’s USD 450 million Royal Canin plant in Ohio and Nestlé Purina’s USD 195 million Wisconsin upgrade expand therapeutic diet output and bolster supply resilience. Asia-Pacific is the fastest region, forecast to advance at an 11.8% CAGR over 2026-2031 as e-commerce penetration spreads fortified super-premium formulas into tier-2 and tier-3 cities. Rising disposable incomes and urban pet ownership in China and India reinforce the momentum of premiumization and drive greater uptake of functional supplements.

Europe is experiencing steady growth, supported by sustainability-focused consumers in Germany, the United Kingdom, and France. Additionally, the regulatory oversight of the European Food Safety Authority enhances claim credibility and promotes the development of scientifically formulated products. In South America, growth is driven by Brazil’s expanding middle class and the establishment of Mars’s new wet-food facility in São Paulo state, which is fostering the adoption of fortified diets. The Middle East is witnessing improved adoption rates, supported by high per-capita income in Saudi Arabia and the United Arab Emirates, as well as the ongoing expansion of modern retail channels. In Africa, the market remains underdeveloped. However, urbanization in South Africa and Nigeria is gradually increasing awareness of the advantages of functional pet nutrition.

Collectively, these regional dynamics diversify revenue streams and cushion suppliers against localized economic shocks. Manufacturing investments in high-demand geographies shorten lead times and reduce foreign-exchange exposure, supporting further expansion of the fortified pet food market. Digital platforms that transcend brick-and-mortar limitations allow brands to harmonize product launches and marketing across continents. As clinical validation of functional ingredients gains global visibility, each region is projected to deepen its contribution to overall category growth through 2031.

Competitive Landscape

The fortified pet food market is moderately concentrated, with the top five suppliers, including Mars, Incorporated, Nestlé Purina PetCare (Nestlé S.A.), Hill’s Pet Nutrition, Inc. (Colgate-Palmolive Company), Blue Buffalo Pet Products, Inc. (General Mills, Inc.), and United Pet Group, Inc. (Spectrum Brands Holdings, Inc.). Mars, Incorporated leverages vertically integrated manufacturing, multi-billion-dollar capacity projects, and data-enabled service platforms to reinforce leadership in super-premium and therapeutic segments. Nestlé Purina PetCare (Nestlé S.A.) is aligning with this pace by establishing new factories in the United States, expanding its Pro Plan and ONE fortified product lines, and allocating significant research and development budgets toward probiotic science and fresh product formats. Both companies leverage veterinary channel influence and genomic data partnerships to enhance brand loyalty and drive innovation within the broader industry.

Hill’s Pet Nutrition, Inc. (Colgate-Palmolive Company) defends its share through clinician-backed Prescription Diet and Science Diet ranges that translate university research into label-backed therapeutic claims. Blue Buffalo Pet Products, Inc. (General Mills, Inc.) has diversified beyond kibble by absorbing Whitebridge Pet Brands and Edgard and Cooper, which strengthen its premium wet food and treat presence in North America and Europe. United Pet Group, Inc. (Spectrum Brands Holdings, Inc.) concentrates on specialty supplements and aquatics, providing a portfolio hedge that positions the company for cross-category wellness bundles. Collectively, these three players complement the giants by emphasizing veterinary trust, acquisition-driven portfolio expansion, and niche fortificant leadership.

Across the landscape, incumbents are scaling direct-to-consumer subscriptions, cold-chain logistics, and wearables-driven personalization that elevate switching costs and grow lifetime value. Ongoing investments in insect protein alliances, algal omega-3 sourcing, and microencapsulation technology are broadening ingredient arsenals and insulating supply chains against volatility. Regional footprint expansions in Brazil, Eastern Europe, and Southeast Asia shorten delivery lead times and align capacity with the fastest-demand nodes. These moves indicate that the leading companies intend to expand category reach and accelerate overall expansion of the fortified pet food market through 2031.

Fortified Pet Food Industry Leaders

Mars, Incorporated

Nestlé Purina PetCare (Nestlé S.A.)

Hill’s Pet Nutrition, Inc. (Colgate-Palmolive Company)

Blue Buffalo Pet Products, Inc. (General Mills, Inc.)

United Pet Group, Inc. (Spectrum Brands Holdings, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nestlé Purina PetCare (Nestlé S.A.) introduced Purina Pro Plan AdvantEDGE, a new range of probiotic-enhanced nutrition designed for adult and senior dogs and cats, expanding its portfolio of fortified pet foods aimed at supporting digestive and overall health.

- April 2026: Globe Buddy launched new insect-protein dog treats, Luxx Easy and Luxx Energy, featuring black soldier fly larvae protein combined with functional ingredients such as L-tryptophan, L-carnitine, electrolytes, minerals, and botanicals. These products aim to promote calmness, energy, and recovery in dogs. This development underscores the growing demand in the fortified pet food market for nutritionally enhanced and functional pet nutrition products that utilize alternative proteins and provide targeted health benefits.

- April 2025: Hill’s Pet Nutrition, Inc. (a subsidiary of Colgate-Palmolive Company) expanded its Hill’s Science Diet portfolio by introducing ActivBiome+ Multi-Benefit Technology. This microbiome-focused innovation is designed to support digestive health, immune function, and overall well-being in dogs and cats. The launch reinforces the company's position in the probiotic-fortified and multi-functional blend segments of the fortified pet food market.

Global Fortified Pet Food Market Report Scope

Fortified pet food is formulated to supply essential vitamins, minerals, and nutrients that may be lost during processing or absent in raw ingredients, ensuring a complete and balanced diet. The fortified pet food market report is segmented by product type (dry food, wet food, treats and snacks, functional supplements, and other products), by pet type (dog, cat, and other pets), by fortificant (vitamin enriched, mineral enriched, probiotic fortified, omega 3 fortified, and multi-functional blend), by distribution channel (supermarkets and hypermarkets, specialty pet stores, veterinary clinics, online retail and other distribution channel), and by geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Dry Food |

| Wet Food |

| Treats and Snacks |

| Functional Supplements |

| Others |

| Dog |

| Cat |

| Others |

| Vitamin Enriched |

| Mineral Enriched |

| Probiotic Fortified |

| Omega-3 Fortified |

| Multi-functional Blend |

| Supermarkets and Hypermarkets |

| Specialty Pet Stores |

| Veterinary Clinics |

| Online Retail |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Dry Food | |

| Wet Food | ||

| Treats and Snacks | ||

| Functional Supplements | ||

| Others | ||

| By Pet Type | Dog | |

| Cat | ||

| Others | ||

| By Fortificant | Vitamin Enriched | |

| Mineral Enriched | ||

| Probiotic Fortified | ||

| Omega-3 Fortified | ||

| Multi-functional Blend | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Pet Stores | ||

| Veterinary Clinics | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the fortified pet food market be by 2031?

The fortified pet food market size is anticipated to reach USD 32.1 billion in 2031, advancing at a 9.38% CAGR from 2026 to 2031.

Which product type is expanding the fastest?

Functional supplements are forecast to post a 13.8% CAGR through 2026 to 2031, outstripping growth in kibble, wet food, and treats, based on Mordor Intelligence data.

What region will lead growth momentum?

Asia-Pacific is anticipated to deliver the highest regional CAGR at 11.8% from 2026 to 2031, driven by rising incomes and strong e-commerce adoption.

Which fortificant shows the highest CAGR?

Probiotic-fortified recipes are forecast to grow at a 15.1% CAGR to 2031, underpinned by growing veterinary endorsement and robust clinical evidence.

How are regulations influencing product development?

New Association of American Feed Control Officials labeling rules introduce mandatory nutrition facts boxes and stricter Complete claims, raising compliance costs but also standardizing fortified product disclosures.

Page last updated on: