Pet Food Microalgae Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

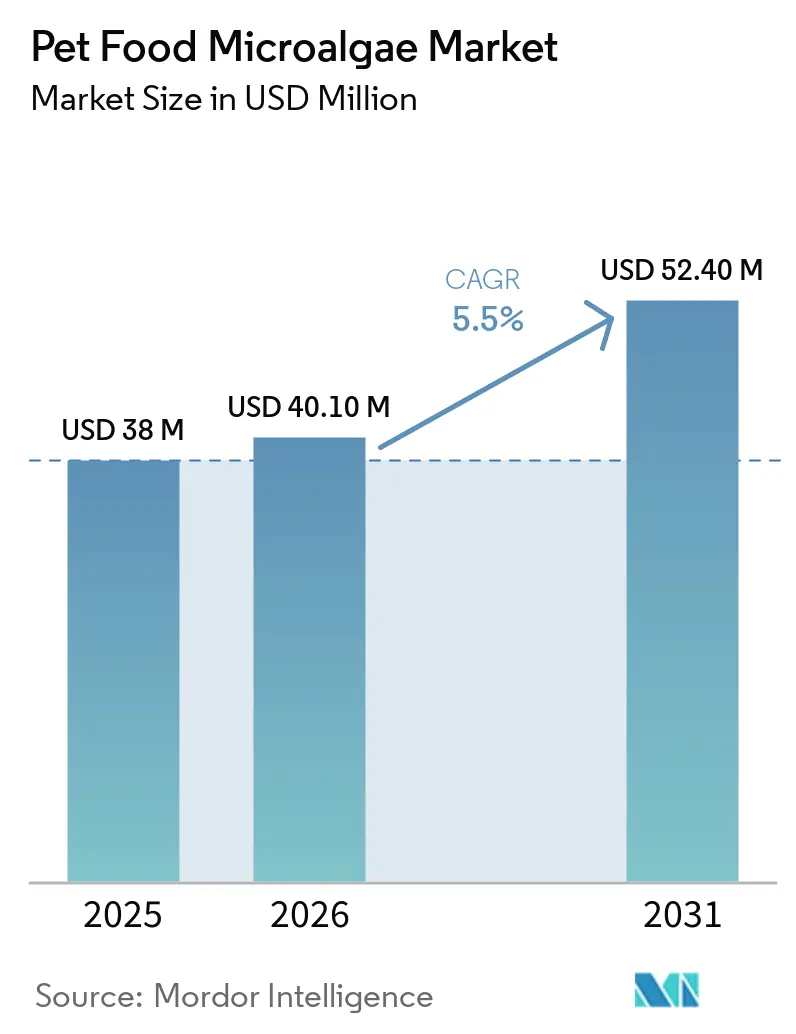

| Market Size (2026) | USD 40.10 Million |

| Market Size (2031) | USD 52.40 Million |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Microalgae Market Analysis by Mordor Intelligence

The pet food microalgae market is projected to grow from USD 38.0 million in 2025 to USD 40.1 million in 2026 and USD 52.4 million by 2031, registering a CAGR of 5.5% between 2026 and 2031. The increasing consumer demand for traceable omega-3 and hypoallergenic proteins is driving the commercialization of pet food microalgae, despite the higher ingredient costs compared to conventional soy or fish oil inputs. The rapid adoption of functional pet supplements in Asia and the growth of premium pet food sales through online channels are contributing to the wider acceptance of algae-based ingredients. Furthermore, regulatory modernization efforts by the Association of American Feed Control Officials (AAFCO) and the United States Food and Drug Administration (FDA) are streamlining approval processes for novel animal feed ingredients, facilitating faster commercialization and ongoing innovation in microalgae-based pet nutrition products.

Key Report Takeaways

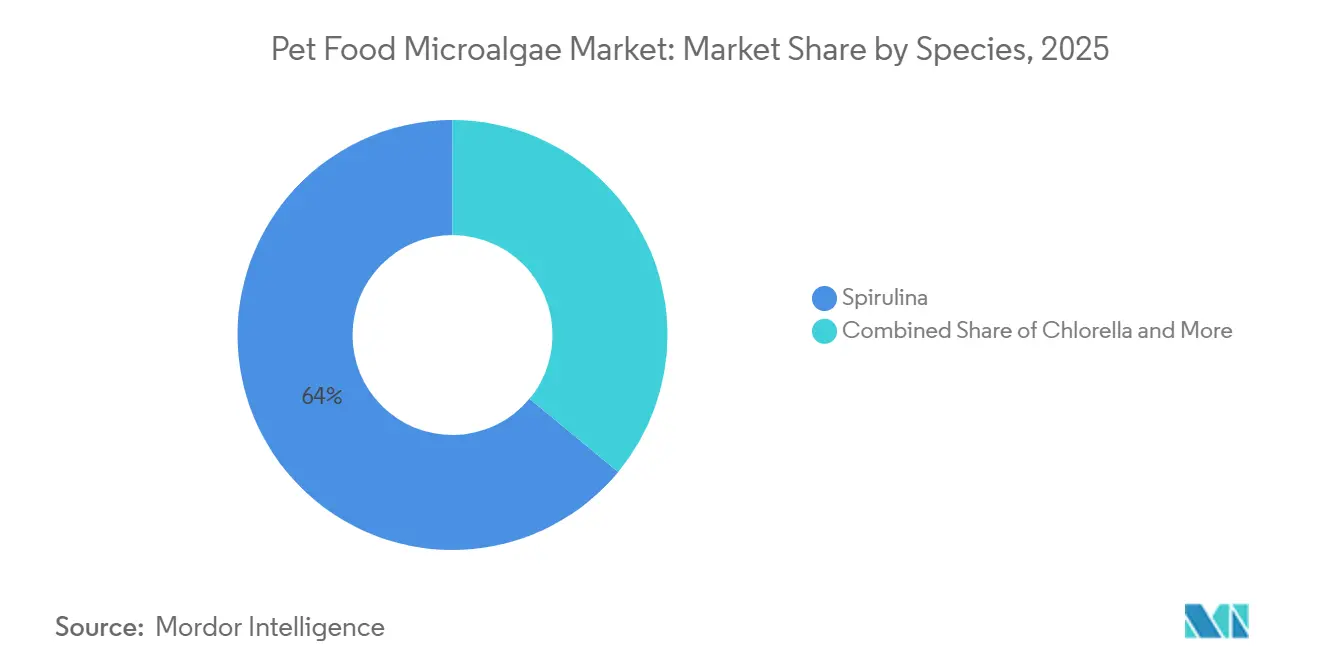

- By species, Spirulina held the largest 64% of the pet food microalgae market share in 2025, while the Haematococcus market size is projected to grow at the fastest 9.1% CAGR from 2026 to 2031.

- By source, freshwater microalgae accounted for the largest 85% of the pet food microalgae market share in 2025, whereas the pet food microalgae market size for the marine microalgae segment is projected to expand at the fastest 8% CAGR from 2026 to 2031.

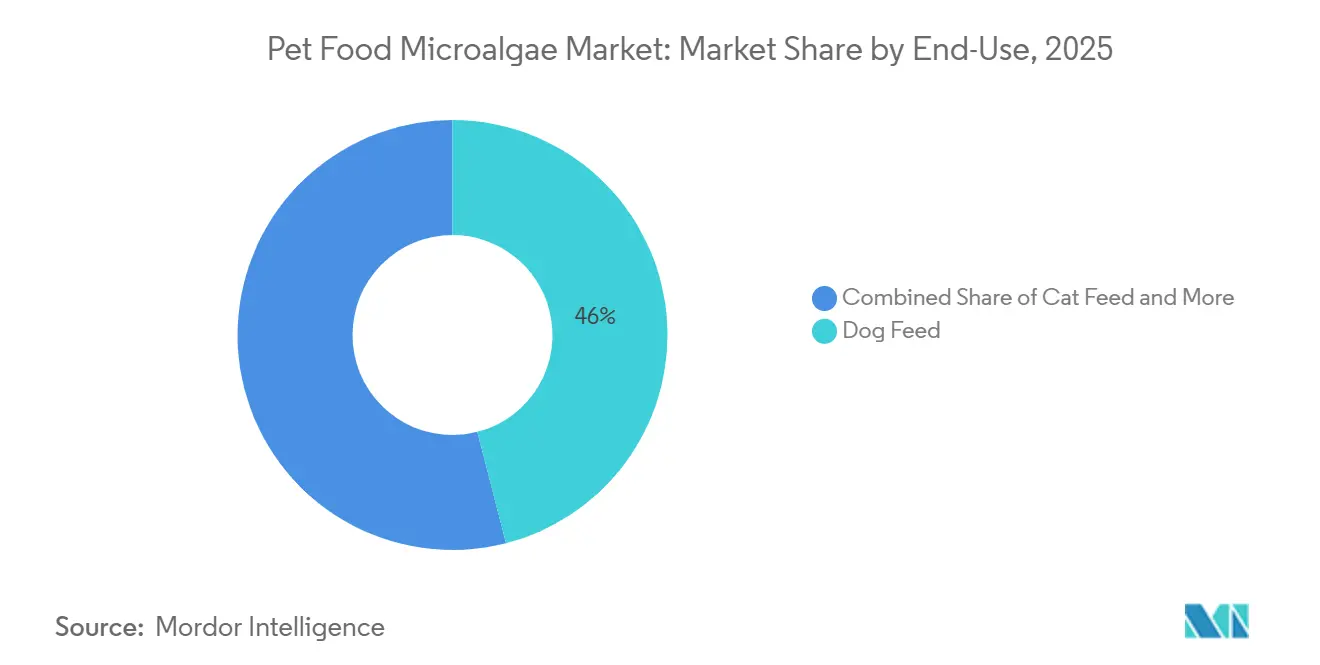

- By end-use, dog feed represented the largest 46% of the pet food microalgae market share in 2025, whereas the small-pet feed and treats market size is projected to grow at the fastest 7.7% CAGR from 2026 to 2031.

- By form, powder form captured the largest 71% of the pet food microalgae market share in 2025, while the oil form market size is anticipated to grow at the fastest 8.8% CAGR from 2026 to 2031.

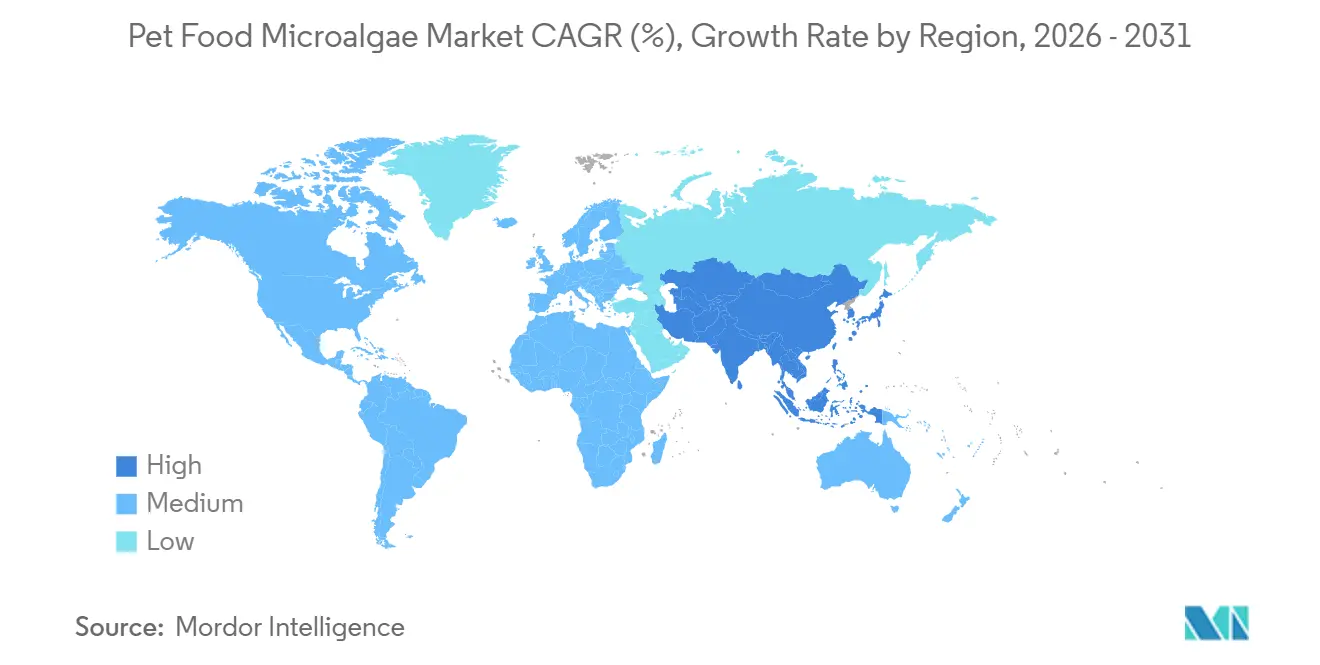

- By geography, Asia-Pacific commanded the largest 52% of the pet food microalgae market share in 2025, while the market size is forecast to grow at the fastest 6.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Microalgae Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization driving demand for functional ingredients | +1.2% | Global, with strongest adoption in North America, Western Europe, and urban China | Medium term (2–4 years) |

| Sustainability shift replacing fish oil omega-3 with microalgae | +1.5% | North America and Western Europe lead, while Asia-Pacific aligns through regulation | Long term (≥ 4 years) |

| Rising pet allergies increasing demand for alternative proteins | +0.8% | Global, with heightened awareness in North America and Western Europe | Medium term (2–4 years) |

| Growth in premium pet food e-commerce channels | +0.7% | Global, with acceleration in India, Southeast Asia, and South America | Short term (≤ 2 years) |

| Waste heat integration reducing microalgae cultivation energy costs | +0.5% | Regional clusters near industrial facilities in Scotland, Netherlands, and coastal Portugal | Long term (≥ 4 years) |

| Streamlined regulatory pathways supporting novel algae strains | +0.6% | North America and European Union, with spillover to Asia-Pacific and South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization Driving Demand for Functional Ingredients

Urban pet owners are increasingly treating companion animals as family members, leading to a greater willingness to invest in ingredients that provide measurable health benefits. According to the American Pet Products Association, in 2025, 95 million United States households owned at least one pet[1]Source: American Pet Products Association (APPA), 2025 State of the Industry Report, americanpetproducts.org . This widespread ownership fosters stronger emotional bonds and drives increased spending on functional and condition-specific nutrition. The use of advanced microalgae fermentation enhances traceability and sustainability, making it particularly appealing to premium buyers. As a result, this trend is driving higher demand for microalgae-based ingredients, contributing to overall market growth.

Sustainability Shift Replacing Fish Oil Omega-3 with Microalgae

Growing sustainability concerns about marine resources are driving a shift away from fish oil-based omega-3s toward alternative sources. According to the Food and Agriculture Organization (2025), 35.5% of global fishery stocks are overfished, underscoring the increasing strain on traditional marine inputs [2]Source: Food and Agriculture Organization, FAO Releases the Most Detailed Global Assessment of Marine Fish Stocks to Date, 2025, fao.org. This challenge is fostering the adoption of microalgae-derived omega-3, which provides a stable, scalable, and land-based alternative. Furthermore, advancements in technology and regulatory support are enhancing its commercial viability. Consequently, the focus on sustainability is boosting the demand for alternative omega-3 sources, contributing to long-term market growth.

Rising Pet Allergies Increasing Demand for Alternative Proteins

The increasing prevalence of pet allergies is driving the demand for alternative protein sources with low allergenic potential. According to Trupanion, allergy-related pet insurance claims rose by 42% in North America in 2024, underscoring the growing incidence of diet-related sensitivities and skin conditions in companion animals. This trend is prompting pet food manufacturers to explore novel proteins that minimize exposure to common allergens while meeting specific nutritional needs. Microalgae-based proteins are gaining traction as a viable option due to their controlled production processes, consistent nutritional composition, and lack of common antigen triggers. Additionally, their functional stability and sustainable sourcing are contributing to their growing use in premium and specialized pet nutrition products.

Growth in Premium Pet Food E-commerce Channels

The growth of premium pet food e-commerce channels is transforming the distribution of specialized nutrition products. Online platforms enable niche brands to overcome traditional retail constraints and directly engage consumers seeking functional, high-quality formulations. Subscription-based models enhance demand predictability, enabling suppliers to streamline production planning and minimize inventory costs. Additionally, digital content and platform-driven education increase consumer awareness of ingredient benefits, boosting purchase intent for advanced nutrition products. However, challenges such as high return rates and platform-related costs, including slotting fees, can impact margins, particularly for premium ingredients. This creates a growth environment that is both challenging and opportunity-filled.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus conventional proteins | -1.8% | Global, with strongest effect in price-sensitive South America and Asia-Pacific mass-market segments | Long term (≥ 4 years) |

| Palatability challenges, especially in feline diets | -1.0% | Global, with acute impact in cat-dominant markets such as Japan and Western Europe | Medium term (2–4 years) |

| Trace-metal accumulation risk in closed systems | -0.4% | Regions with strict feed safety enforcement, including the European Union and North America | Long term (≥ 4 years) |

| Volatile supply of food-grade carbon dioxide for indoor cultivation | -0.3% | Landlocked production sites and areas lacking industrial carbon dioxide infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost Versus Conventional Proteins

High production costs relative to conventional proteins continue to be a significant constraint, limiting adoption beyond premium market segments. According to the United States Department of Agriculture (2025), soybean meal prices are projected at USD 310 per short metric tons (approximately USD 0.34 per kg), underscoring the cost advantage of traditional protein sources. In contrast, microalgae production incurs higher cultivation, harvesting, and processing costs, resulting in a structural price disparity. While premium formulations can accommodate these higher costs, widespread market penetration remains limited, sustaining this challenge throughout the forecast period.

Palatability Challenges, Especially in Feline Diets

Palatability challenges continue to pose a significant barrier, particularly in feline diets, where taste sensitivity and neophobia impact food acceptance. Cats often show reluctance toward unfamiliar ingredients, leading to inconsistent consumption when microalgae are incorporated into formulations. Although certain species of microalgae are better accepted, the overall response remains variable, further complicating formulation. Efforts to enhance flavor using masking agents and palatants can improve acceptance but also increase production costs. Furthermore, physical attributes such as moisture sensitivity can influence texture and shelf stability in dry product formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Spirulina Leads While Haematococcus Accelerates

Spirulina accounted for the largest 64% of the pet food microalgae market share in 2025. Its leading position is attributed to its high protein content and regulatory clarity under feed standards, which facilitate its scalable adoption in pet nutrition formulations. Spirulina remains cost-effective compared to other microalgae due to its compatibility with open-pond cultivation methods and lower input requirements. In contrast, Haematococcus serves a specialized role due to its astaxanthin content, which supports joint and eye health in aging pets. This functional differentiation enables premium product positioning, while other species, such as Chlorella and Schizochytrium, contribute to diversification in protein and omega-3 applications.

The pet food microalgae market size for the Haematococcus segment is projected to grow at the fastest CAGR of 9.1% from 2026 to 2031. This growth is driven by rising demand for antioxidant-rich ingredients in premium pet formulations. Schizochytrium also supports market expansion due to its high docosahexaenoic acid (DHA) content, which serves as a replacement for fish oil in omega-3 supplementation. Meanwhile, Chlorella offers mid-range protein functionality with stability under processing conditions, making it suitable for inclusion in extruded pet foods. These complementary roles enhance product segmentation strategies, where bulk protein sources coexist with high-value functional extracts.

By Source: Freshwater Dominates as Marine Species Gain Momentum

Freshwater microalgae accounted for the largest 85% of the market share in 2025. This dominance is attributed to the long-established production of Spirulina and Chlorella in regions such as China, India, and the southwestern United States. The lower salinity requirements reduce the need for corrosion-resistant infrastructure and simplify wastewater management, keeping capital expenditure relatively low for large-scale operations. Additionally, freshwater cultivation benefits from favorable climatic conditions in high-insolation regions, enabling cost-efficient production. These factors support its widespread adoption in protein-focused formulations, establishing freshwater microalgae as the primary supply base.

The marine microalgae market size is projected to grow at the fastest 8.0% CAGR from 2026 to 2031. This growth is driven by increasing demand for sustainable omega-3 sources, particularly Schizochytrium oils, which serve as alternatives to fish oil in nutritional applications. Advances in fermentation technologies have enabled inland production using synthetic seawater, reducing reliance on coastal infrastructure. However, higher salinity control requirements and the need for trace-mineral inputs increase production costs, positioning marine microalgae in premium market segments. Regulatory frameworks also play a role, with clearer approvals for marine species facilitating commercialization, while freshwater variants face additional review processes in certain regions.

By End-Use: Dog Feed Anchors Demand, Small-Pet Treats Surge

Dog food accounted for 46% of the market share in 2025. This leadership is supported by higher consumption volumes and strong acceptance of functional ingredients, such as omega-3s and joint-health additives, in canine nutrition. Formulators increasingly combine microalgae-derived protein and oil to create integrated health-focused blends, sustaining consistent demand. The segment benefits from an established premium product base where consumers prioritize nutritional enhancements, reinforcing stable adoption. In contrast, other pet categories remain smaller but are gradually expanding as awareness of advanced nutrition solutions increases across diverse companion animal segments.

Small-pet feed and treats are projected to grow at the fastest 7.7% CAGR from 2026 to 2031. Growth is driven by rising interest in natural color enhancers and nutrient-dense formulations for herbivorous and ornamental species. Bird feed shows strong uptake due to visible benefits such as improved plumage, while small mammals benefit from high-protein supplementation. Cat feed presents growth potential but remains constrained by palatability challenges and selective eating behavior. Expanding applications across multiple pet types support portfolio diversification, enabling suppliers to distribute production costs and strengthen overall demand across varied end-use segments.

By Form: Powder Still Reigns While Oils Accelerate

Powder accounted for the largest 71% of the market share in 2025. This dominance is attributed to its ease of incorporation into dry pet food, stable shelf life, and compatibility with large-scale manufacturing processes. Whole-biomass powders also align with consumer preferences for clean-label and functional ingredients, supporting natural product positioning. Their visual appeal and versatility across various formulations make them a preferred choice in mainstream applications. These factors make powder formats the primary delivery form, particularly in cost-sensitive, high-volume product segments where efficiency and stability are essential.

The oil form is projected to grow at the fastest CAGR of 8.8% from 2026 to 2031, the fastest among all formats. This growth is driven by the demand for precise omega-3 delivery in wet food, supplements, and functional treats. Liquid formats offer accurate dosing and improved bioavailability while avoiding the texture and flavor limitations associated with powders. Extracts and concentrates cater to ultra-premium applications but require specialized storage conditions. Alternative formats, such as frozen pastes, remain niche due to logistical challenges. These advancements provide formulators with the flexibility to balance functionality, cost, and consumer appeal across various product categories.

Geography Analysis

Asia-Pacific commanded the largest 52% of the market share in 2025. This dominance is attributed to established microalgae cultivation infrastructure, favorable climate conditions, and robust growth in domestic pet food demand. Key countries such as China and India lead production due to cost advantages and large-scale freshwater microalgae operations. Increasing urbanization and premiumization trends are driving demand for functional pet nutrition, while digital retail platforms are improving accessibility. Regulatory frameworks in major countries are evolving to balance domestic production support with safety compliance, further reinforcing the region's leadership in both supply and consumption.

The Asia-Pacific region is projected to grow at the fastest 6.7% CAGR from 2026 to 2031. This growth is driven by rising disposable incomes, rapid urban pet adoption, and the expansion of e-commerce channels for premium pet food. Consumer preferences are increasingly shifting toward health-focused and natural ingredients, accelerating the adoption of functional additives such as microalgae-based nutrition. Furthermore, strong regional production capabilities reduce reliance on imports, enhancing supply chain efficiency. While some developing markets face infrastructure challenges, digital-first distribution strategies and localized manufacturing are anticipated to sustain growth, solidifying the region's position as both a production hub and a high-growth consumption market.

North America and Europe are established markets with robust regulatory frameworks and high adoption rates of premium pet nutrition products. These regions benefit from well-defined approval processes and heightened consumer awareness of sustainability and pet health, which drive the adoption of advanced ingredients such as microalgae. Additionally, well-developed supply chains and innovation ecosystems support consistent demand for functional pet food formulations. In contrast, South America is experiencing selective growth, fueled by increasing pet ownership and premiumization trends. According to Brazil’s Federal Senate, the country had approximately 150 to 160 million pets in 2024, contributing to the growing demand for high-quality and functional pet nutrition products [3]Source: Brazilian Federal Senate, Brazil has the third largest pet population in the world, 2024, senado.leg.br.

Competitive Landscape

The market is moderately concentrated, with key players such as Corbion N.V., Veramaris V.O.F. (DSM-Firmenich), Alltech, Inc., Cyanotech Corporation, and MiAlgae Limited driving technological advancements and scalability. These companies utilize proprietary fermentation and cultivation methods to deliver consistent quality and functionality, particularly in omega-3 and protein applications. Operational efficiencies are achieved through closed bioreactor systems, waste-heat recovery, and integrated nutrient cycles, providing cost advantages over traditional production methods and enabling scalable output of premium pet nutrition products.

Market growth is being driven by three key strategies. Integrated feed producers are expanding upstream to secure supply chains and improve production predictability. Industrial symbiosis models are becoming more prevalent, utilizing byproducts as feedstock to lower input costs and enhance sustainability. Furthermore, modular photobioreactor systems are allowing mid-sized companies to develop production capabilities with reduced capital investment. These strategies are increasing accessibility, optimizing cost structures, intensifying competition across the value chain, and supporting the adoption of advanced ingredient solutions.

White-space opportunities exist in areas such as feline palatability, ornamental bird pigmentation, and specialized diet formats. Limited progress in addressing taste sensitivity in cats highlights potential for innovation in flavor masking technologies. In bird nutrition, visible benefits like enhanced plumage drive demand for carotenoid-rich ingredients. Processing advancements, such as freeze-drying, improve nutrient retention but remain cost-intensive. These gaps present opportunities for differentiation, encouraging new market entrants and partnerships, while influencing future competitive dynamics and product development strategies.

Pet Food Microalgae Industry Leaders

Corbion N.V.

Veramaris V.O.F. (DSM-Firmenich AG and Evonik Industries AG)

Alltech, Inc.

Cyanotech Corporation

MiAlgae Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSM-Firmenich, through Veramaris V.O.F., introduced Veramaris O3 Max Pure at Petfood Forum 2026. This product features a native 3:2 EPA:DHA ratio, designed to replicate the performance of fish oil in pet nutrition.

- February 2026: Alltech Inc. and Archer Daniels Midland Company have launched Akralos Animal Nutrition, integrating their feed operations across North America to enhance specialty nutrition offerings. The joint venture focuses on advancing innovation in functional ingredients, such as microalgae-based nutrition solutions for premium pet food applications.

- December 2025: MiAlgae Limited has initiated an expansion of its facility in Scotland, increasing production capacity by more than 10 times. The company will utilize whisky byproducts as feedstock for sustainable microalgae production.

Global Pet Food Microalgae Market Report Scope

Pet food microalgae involves incorporating algae-based ingredients, such as spirulina and schizochytrium, into canine diets to supply protein, omega-3 fatty acids, and antioxidants. These components contribute to functional benefits, including improved joint health, better skin condition, and enhanced immune support, while serving as a sustainable alternative to conventional animal-based ingredients. The pet food microalgae market report is segmented by species (spirulina, chlorella, haematococcus, dunaliella, and schizochytrium), by source (freshwater microalgae and marine microalgae), by end-use (dog feed, cat feed, bird feed, and small-pet feed and treats), by form (powder, oil, whole biomass, and extract/concentrate), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Spirulina |

| Chlorella |

| Haematococcus |

| Dunaliella |

| Schizochytrium |

| Freshwater Microalgae |

| Marine Microalgae |

| Dog Feed |

| Cat Feed |

| Bird Feed |

| Small-Pet Feed and Treats |

| Powder |

| Oil |

| Whole Biomass |

| Extract / Concentrate |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Kenya |

| South Africa | |

| Rest of Africa |

| By Species | Spirulina | |

| Chlorella | ||

| Haematococcus | ||

| Dunaliella | ||

| Schizochytrium | ||

| By Source | Freshwater Microalgae | |

| Marine Microalgae | ||

| By End-Use | Dog Feed | |

| Cat Feed | ||

| Bird Feed | ||

| Small-Pet Feed and Treats | ||

| By Form | Powder | |

| Oil | ||

| Whole Biomass | ||

| Extract / Concentrate | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Kenya | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the pet food microalgae market in 2026 and where is it headed?

The pet food microalgae market size stands at USD 40.1 million in 2026 and is projected to reach USD 52.4 million by 2031, registering a 5.5% CAGR from 2026 to 2031.

Which species accounts for the bulk of current demand?

Spirulina leads with the largest 64% of pet food microalgae market share in 2025.

Which geography is growing the fastest?

Asia-Pacific shows the fastest growth at a 6.7% CAGR from 2026 to 2031, helped by rising disposable income and strong e-commerce penetration in tier-one cities.

What level of heavy-metal testing is now standard for commercial Spirulina lots?

European Union safety guidance requires every batch to undergo inductively linked plasma mass spectrometry screening for cadmium, lead, mercury, and arsenic before release.

Page last updated on: