Animal-based Pet Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

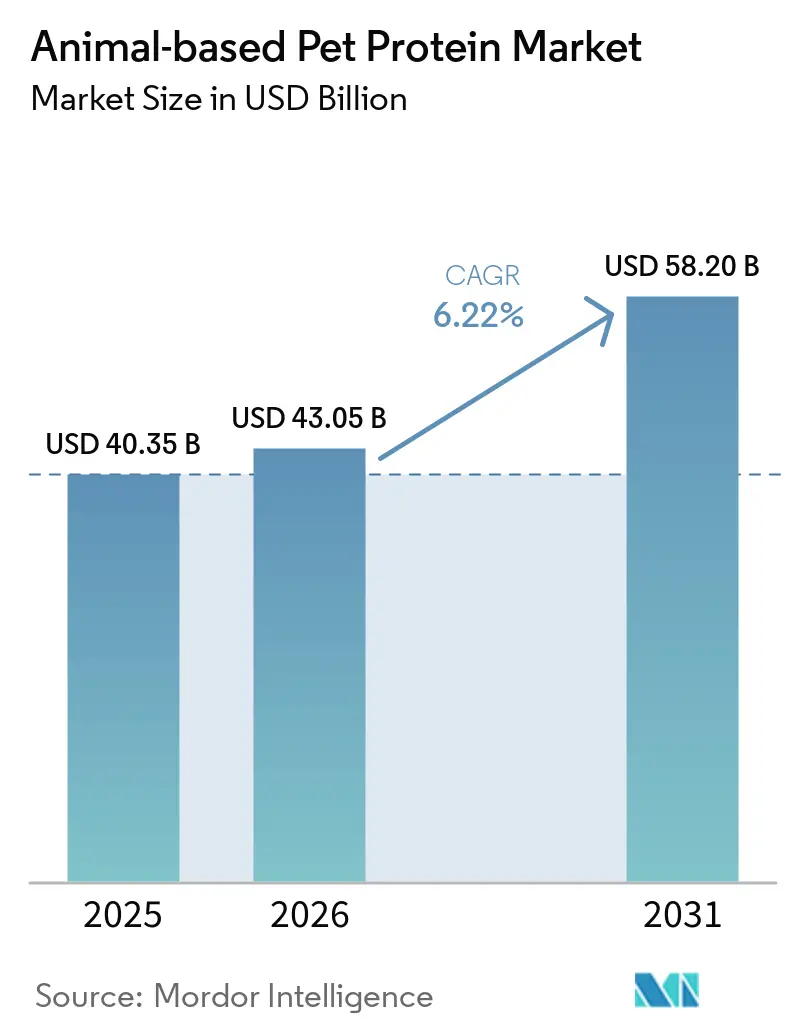

| Market Size (2026) | USD 43.05 Billion |

| Market Size (2031) | USD 58.20 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal-based Pet Protein Market Analysis by Mordor Intelligence

The animal-based pet protein market size is projected to grow from USD 40.35 billion in 2025 and USD 43.05 billion in 2026 to USD 58.20 billion by 2031, registering a CAGR of 6.22% from 2026 to 2031. This growth is driven by increased scrutiny of protein quality, premiumization trends, and the positioning of products as human-grade, reflecting pet owners' growing tendency to treat companion animals as family members. Factors such as label transparency, segmented life-stage nutrition, and vertical integration strategies are contributing to value growth outpacing volume gains. In North America, manufacturers benefit from economies of scale, while processors in emerging markets are expanding capacity to meet rising middle-class demand. Competitive dynamics are influenced by sustainability audits, regulatory changes on the use of animal by-products, and investments in cold-chain infrastructure. Additionally, market consolidation continues as large food conglomerates acquire niche brands to capitalize on opportunities in frozen-raw and single-protein product segments.

Key Report Takeaways

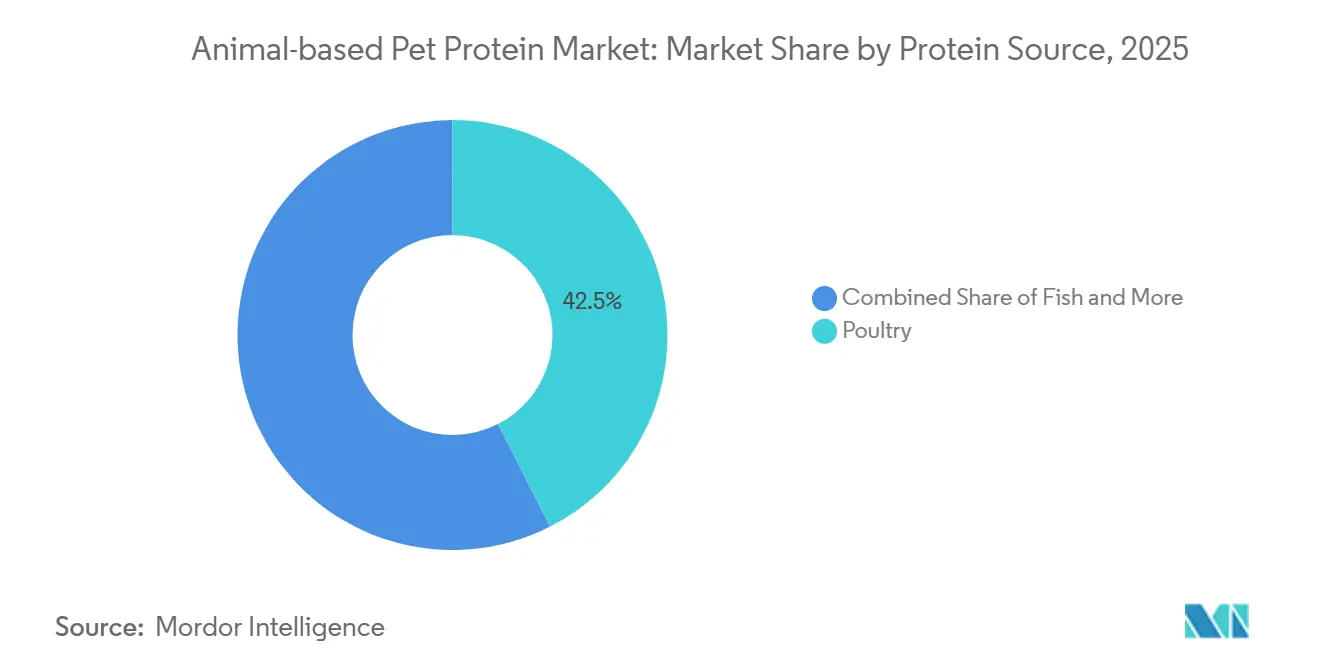

- By protein source, poultry accounted for the largest 42.5% of the animal-based pet protein market share in 2025, whereas the animal-based pet protein market size for the fish segment is projected to grow at the fastest 9.3% CAGR from 2026 to 2031.

- By pet type, dogs captured the largest 61.0% of the animal-based pet protein market share in 2025, while the cat market size is anticipated to expand at the fastest 8.0% CAGR from 2026 to 2031.

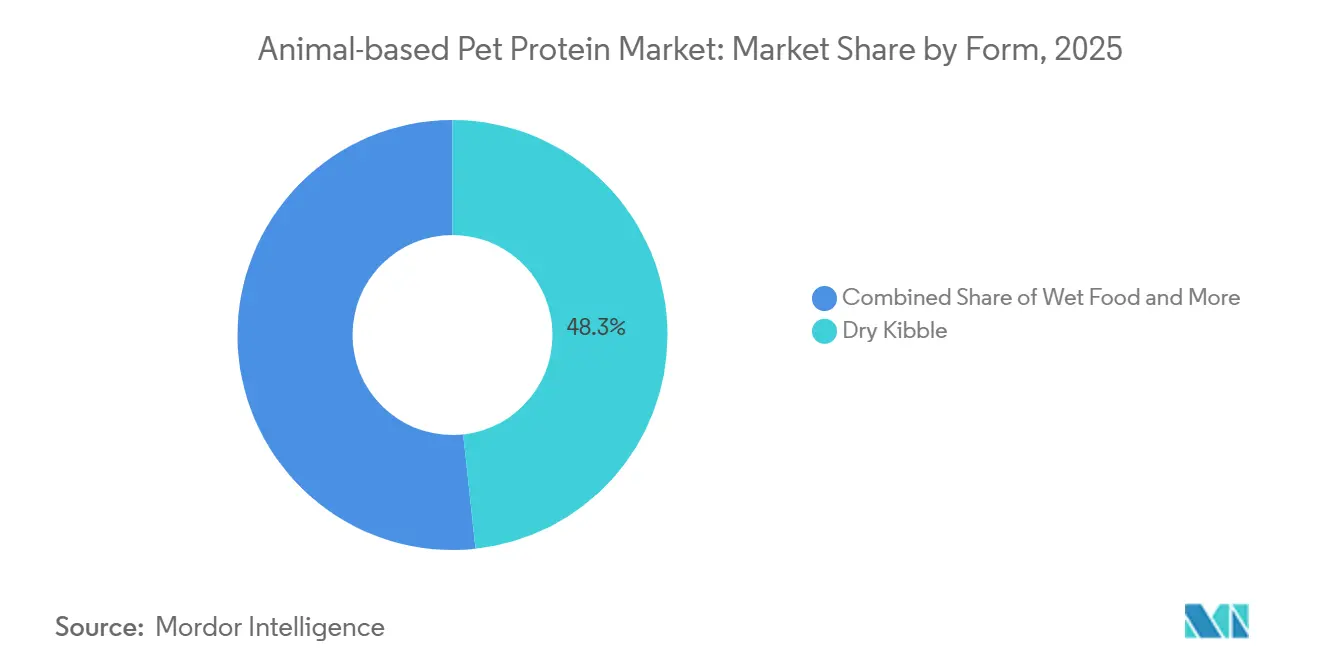

- By form, dry kibble held the largest 48.3% of the animal-based pet protein market size in 2025, whereas frozen/raw formats are projected to grow at the fastest 11.9% CAGR from 2026 to 2031.

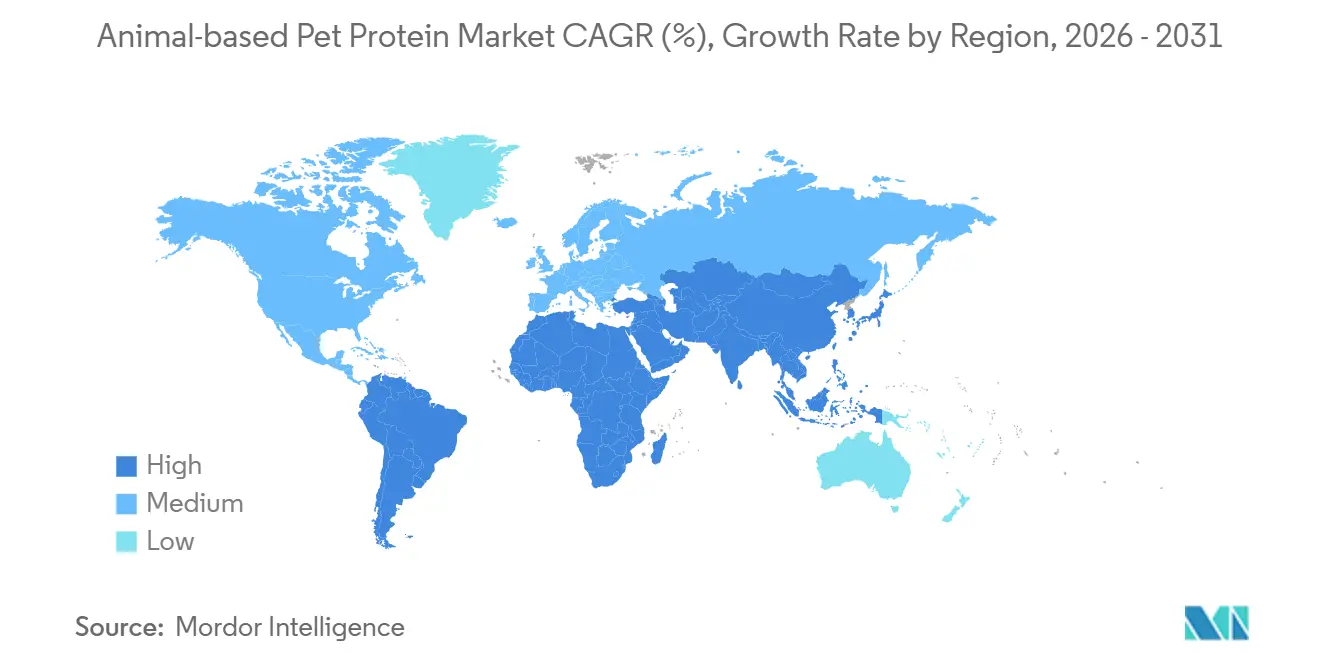

- By geography, North America commanded the largest 37.8% of the animal-based pet protein market share in 2025, while the Asia-Pacific market is projected to grow at the fastest 10.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Animal-based Pet Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization of pets driving premium protein diets | +1.8% | Global, strongest in North America and Western Europe | Medium term (2–4 years) |

| Rising global pet ownership in emerging economies | +1.5% | Asia-Pacific core plus Middle East and South America | Long term (≥ 4 years) |

| Perceived nutritional superiority over plant proteins | +1.2% | North America and Europe, early urban Asia-Pacific | Medium term (2–4 years) |

| Demand for high-protein senior-pet formulations | +0.9% | North America and Europe, gains in Japan and Australia | Short term (≤ 2 years) |

| Regulatory green-light for broader animal by-product use | +0.7% | North America and select Asian markets | Long term (≥ 4 years) |

| Insect-fed livestock improving digestibility profile | +0.5% | Europe and North America pilots, scaling Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Humanization of Pets Driving Premium Protein Diets

According to the American Pet Products Association, 41% of dog owners and 38% of cat owners purchased premium pet food in 2024 [1]Source: American Pet Products Association (APPA), “Research Insights on Premium & Functional Pet Foods,” americanpetproducts.org. This trend highlights the growing humanization of pets, with owners prioritizing quality, ingredient transparency, and health benefits in pet nutrition. Premium pet food products, often made with high-quality, named animal-based protein sources such as chicken, beef, and fish, are becoming more popular. The shift toward premium diets reflects a focus on nutrition rather than basic feeding, leading to higher spending per pet. This behavior is driving demand for animal-based protein ingredients and contributing to value-driven growth in the animal-based pet protein market.

Rising Global Pet Ownership in Emerging Economies

According to the United States Department of Agriculture Foreign Agricultural Service in 2024, China’s pet population reached 124.1 million, comprising 52.6 million dogs and 71.5 million cats. This represents an increase of 1.6% and 2.5%, respectively, compared to the previous year, highlighting the rapid growth of pet ownership in emerging economies [2]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “Pet Food Market Update 2024 – China,” fas.usda.gov. This expansion is attributed to urbanization, rising disposable incomes, and changing lifestyles in major cities. The increase in pet ownership has led to higher spending on pet food, with a growing preference for commercial and nutritionally balanced diets. As pets are increasingly regarded as companions, there is a rising demand for high-quality, protein-rich formulations, particularly those containing animal-based proteins.

Perceived Nutritional Superiority Over Plant Proteins

According to the Merck Sharp and Dohme (MSD) Veterinary Manual (2024), dogs require ten essential amino acids in their diet, while cats need an additional amino acid, taurine, obtained through their diet. This underscores the importance of complete, bioavailable protein sources in pet nutrition. Animal-based proteins naturally provide a comprehensive range of essential amino acids, including taurine, whereas plant-based proteins often require supplementation to fulfill these nutritional requirements. Consequently, pet owners and manufacturers increasingly favor animal-derived protein formulations due to their efficiency in meeting dietary needs and promoting overall pet health. This nutritional benefit enhances the demand for animal-based proteins and supports their premium positioning in the animal-based pet protein market.

Demand for High-Protein Senior-Pet Formulations

As pets age, their metabolic efficiency decreases, particularly in protein utilization, creating a greater need for high-quality, easily digestible protein sources. This has led to a shift in pet food formulations toward protein-rich diets designed to support muscle maintenance, mobility, and overall health in aging animals. Animal-based proteins are commonly used in these formulations due to their complete amino acid profile and higher bioavailability. Consequently, the growing number of senior pets is driving demand for specialized, high-protein diets, underscoring the importance of animal-based protein ingredients in the premium and therapeutic pet food segments of the animal-based pet protein market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shift toward plant-based and alternative proteins | −0.8% | North America and Western Europe, low in Asia-Pacific | Medium term (2–4 years) |

| Meat and poultry price volatility | −1.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Retail carbon-footprint audits on animal proteins | −0.6% | Europe and North America, signals in Australia | Medium term (2–4 years) |

| European Union welfare rules limiting organ-meat supplies | −0.4% | Europe, indirect global effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Shift Toward Plant-Based and Alternative Proteins

Consumer preference for sustainable, environmentally friendly pet food products is posing a notable challenge for the animal-based pet protein market. Growing awareness of the environmental impact of livestock production, along with rising interest in plant-based and alternative protein ingredients, is prompting pet food manufacturers to explore formulations beyond traditional animal-derived proteins. The growth of vegan, plant-based, and cultivated protein pet food products in developed markets is gradually shaping purchasing decisions among environmentally conscious consumers. Furthermore, increased investments in alternative protein innovation and broader product availability across retail channels are heightening competition for traditional animal-based protein products.

Meat and Poultry Price Volatility

According to the United States Department of Agriculture Economic Research Service, the national composite wholesale broiler price rose to 132.45 cents per pound (USD 1.32 per pound) in April 2024 before declining to approximately 124 cents per pound (USD 1.24 per pound) in the later quarters of 2024 [3]Source: United States Department of Agriculture Economic Research Service (USDA ERS), “Livestock, Dairy, and Poultry Outlook-May 2024,” ers.usda.gov. This highlights significant price fluctuations within a short timeframe. These changes in poultry prices directly impact the cost of animal-based raw materials used in pet food production, as pet food manufacturers depend on the same meat and poultry supply chains for protein sourcing. Fluctuating input costs reduce pricing predictability, complicate procurement planning, and may force manufacturers to adjust formulations or raise product prices. As a result, volatility in meat and poultry prices serves as a restraint on the animal-based pet protein market by increasing uncertainty in raw material costs and exerting pressure on profit margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Source: Fish Momentum Challenges Poultry Dominance

Poultry accounted for the largest 42.5% of the animal-based pet protein market share in 2025, supported by its cost efficiency, high palatability, and wide acceptance across both dog and cat diets. Its dominance is further reinforced by established supply chains and consistent availability of poultry by-products from the meat industry. Poultry-based formulations remain the preferred choice for mass-market pet food products due to their balanced amino acid profile and affordability, enabling manufacturers to maintain competitive pricing while meeting nutritional standards across various pet food categories globally.

The animal-based pet protein market size for the fish segment is projected to grow at the fastest 9.3% CAGR from 2026 to 2031, driven by increasing demand for functional nutrition and hypoallergenic formulations. Fish-based ingredients are gaining traction for their omega-3 fatty acid content and digestive benefits, particularly among pets with sensitivities. Premiumization trends and rising awareness of skin, coat, and joint health are supporting this shift. Manufacturers are expanding marine-based product lines to capture higher-margin segments, positioning fish proteins as a key growth driver within specialized and therapeutic pet nutrition offerings.

By Pet Type: Cats Accelerate on Obligate-Carnivore Needs

Dogs captured the largest 61.0% of the animal-based pet protein market share in 2025, primarily due to higher food consumption volumes and a larger global pet population. Dog food products require higher caloric intake and protein content across various life stages, driving consistent demand for animal-based protein ingredients. This segment benefits from a diverse range of product offerings, including dry, wet, and functional diets, tailored to different breed sizes, activity levels, and health conditions, thereby maintaining its leading position in overall market consumption.

The animal-based pet protein market for the cat segment is anticipated to grow at the fastest 8.0% CAGR from 2026 to 2031, driven by cats' obligate carnivorous nature, which necessitates greater reliance on animal-based proteins. Growing awareness of feline-specific nutritional needs, such as taurine and essential fatty acids, is boosting demand for meat-rich formulations. Additionally, urbanization and the increasing adoption of cats as companion animals, particularly in smaller living spaces, are contributing to this growth. These factors position the cat segment as a significant area for expansion in specialized protein-based pet food products.

By Form: Frozen/Raw Disrupt Shelf-Stable Staples

Dry kibble held the largest 48.3% share of the animal-based pet protein market in 2025, supported by its affordability, longer shelf life, and ease of storage and feeding. It remains the preferred choice among pet owners due to its cost-effectiveness and suitability for bulk purchasing. Manufacturers are focusing on innovations in this segment by improving nutritional profiles and incorporating high-quality animal protein sources, ensuring its continued dominance in both developed and emerging markets.

The frozen/raw market is projected to grow at the fastest 11.9% CAGR from 2026 to 2031, driven by increasing demand for minimally processed and natural pet food products. These formats are increasingly popular among consumers seeking fresh, high-protein diets that align with ancestral feeding patterns. The expansion of cold-chain infrastructure and premium retail channels is enhancing accessibility, allowing manufacturers to target high-value consumer segments with differentiated, protein-rich offerings.

Geography Analysis

North America commanded the largest share of the animal-based pet protein market in 2025, at 37.8%, driven by high pet ownership rates and elevated per-pet spending. The region benefits from a well-established pet food manufacturing infrastructure and an abundant supply of animal-based raw materials from the livestock industry. Additionally, advanced retail networks and veterinary-driven product recommendations support the demand for high-protein formulations. The presence of major industry players and ongoing product innovation, particularly in premium and therapeutic diets, further reinforces the region's market leadership.

The Asia-Pacific market is projected to grow at the fastest 10.8% CAGR from 2026 to 2031, supported by rising pet ownership and increasing disposable incomes among urban populations. Expanding middle-class demographics and evolving lifestyles are fostering the adoption of commercial pet food, especially protein-rich diets. The growth of organized retail and e-commerce channels is enhancing product accessibility. Regional manufacturers are also strengthening supply chains through partnerships and investments in processing capabilities, enabling higher production of animal-based protein ingredients to meet the growing demand.

In Europe, evolving sustainability frameworks are promoting the use of lower-emission animal proteins, such as poultry and fish, which continue to drive demand for animal-based ingredients. In South America, rising pet ownership and enhanced production capabilities are contributing to market growth, with Argentina and Chile bolstering fishmeal supply for premium pet food formulations. According to the International Trade Centre (ITC) Trade Map data (2024), Saudi Arabia imported 28,000 metric tons of dog and cat food in 2024, which is 35% higher compared to the previous year, indicating increasing demand for commercial pet food in the Middle East. Africa remains an emerging market, with gradual adoption supported by improving distribution networks.

Competitive Landscape

The market is moderately concentrated, with key players such as Mars, Incorporated, Nestlé Purina PetCare Company, Hill's Pet Nutrition Inc., Blue Buffalo Company, Ltd. (General Mills, Inc.), and Diamond Pet Foods Inc. (Schell & Kampeter Inc.) maintaining strong positions. These companies leverage diversified product portfolios and extensive distribution networks to sustain their market presence. Efforts are focused on expanding production capacity and securing raw material supply chains to ensure a steady availability of animal-based protein ingredients.

Competition is intensifying as companies emphasize product innovation, particularly in high-protein, functional, and minimally processed formulations. Manufacturers are prioritizing sourcing transparency and ingredient quality to align with consumer expectations. Strategies such as expansion into emerging markets and strengthening supply chain infrastructure are being adopted to capitalize on growth opportunities. Additionally, private-label and regional players are gaining market share by offering cost-competitive alternatives, contributing to a dynamic and competitive landscape across global and local markets.

Nestlé Purina PetCare Company has announced an investment of CHF 370 million (USD 470 million) to expand its pet food manufacturing facility in Vargeão, Brazil. The expansion aims to increase wet pet food production capacity and support sustainable operations powered by renewable energy. This initiative is designed to address the growing demand for high-protein, animal-based pet food products in Latin America. Additionally, the investment is projected to improve supply chain efficiency and regional distribution capabilities, strengthening the company's competitive position through enhanced capacity and sustainability-focused production practices.

Animal-based Pet Protein Industry Leaders

Mars, Incorporated

Nestlé Purina PetCare Company

Hill's Pet Nutrition Inc.

Blue Buffalo Company, Ltd. (General Mills, Inc.)

Diamond Pet Foods Inc. (Schell & Kampeter Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mars, Incorporated allocated CAD 180 million (USD 131 million) to upgrade and expand its manufacturing facilities in Ontario, Canada. This investment aims to enhance pet nutrition production capacity and improve operational sustainability.

- July 2025: Mars, Incorporated invested USD 2 billion in the United States to bolster its manufacturing network. This includes expanding its Royal Canin production facility to increase capacity for animal-based pet food and enhance supply chain efficiency.

- June 2025: General Mills, Inc. expanded its premium pet food offerings by launching Blue Buffalo Company, Ltd.’s “Love Made Fresh” range. Additionally, it introduced Edgard & Cooper products to the United States through a retail partnership with PetSmart, strengthening its position in the fresh, animal-protein-based pet nutrition market.

Global Animal-based Pet Protein Market Report Scope

Animal-based pet protein refers to protein obtained from animal sources, including poultry, fish, beef, pork, and lamb, used in pet food formulations. It supplies essential amino acids and nutrients necessary for pet growth, muscle development, and overall health. These proteins are commonly utilized in commercial pet food products due to their superior digestibility and nutritional completeness compared to plant-based options. The animal-based pet protein market report is segmented by protein source (poultry, fish, beef, pork, lamb, and other protein sources), by pet type (dogs, cats, and other pets), by form (dry kibble, wet food, semi-moist, frozen/raw, and powder/concentrate), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Poultry |

| Fish |

| Beef |

| Pork |

| Lamb |

| Others |

| Dogs |

| Cats |

| Others |

| Dry Kibble |

| Wet Food |

| Semi-Moist |

| Frozen/Raw |

| Powder/Concentrate |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Protein Source | Poultry | |

| Fish | ||

| Beef | ||

| Pork | ||

| Lamb | ||

| Others | ||

| By Pet Type | Dogs | |

| Cats | ||

| Others | ||

| By Form | Dry Kibble | |

| Wet Food | ||

| Semi-Moist | ||

| Frozen/Raw | ||

| Powder/Concentrate | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the animal-based pet protein market today?

The animal-based pet protein market size was valued at USD 40.35 billion in 2025.

Which protein source is growing fastest in companion-animal diets?

Fish proteins market size is projected to register the fastest 9.3% CAGR from 2026 to 2031.

What share do dog foods hold within the Animal-based pet protein market?

Dogs captured the largest 61.0% of the Animal-based pet protein market share in 2025.

Which geographic region will lead future growth?

Asia-Pacific is forecast to grow at the fastest 10.8% CAGR from 2026 to 2031.

Page last updated on: