Pet Food Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

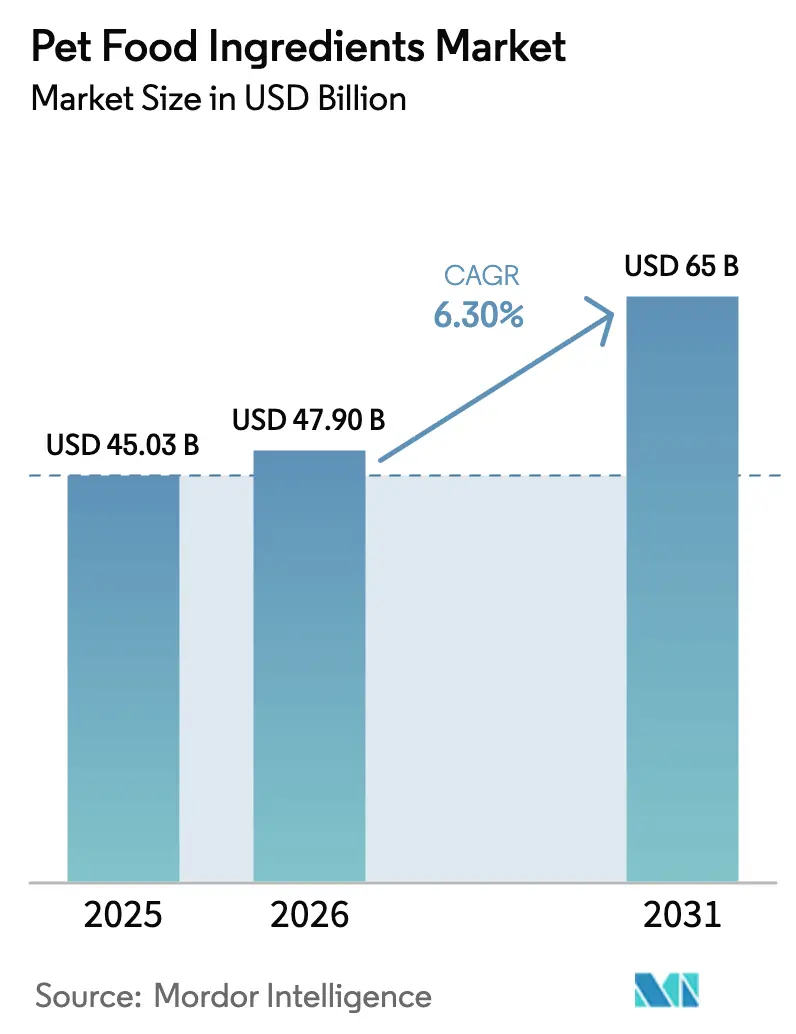

| Market Size (2026) | USD 47.90 Billion |

| Market Size (2031) | USD 65 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

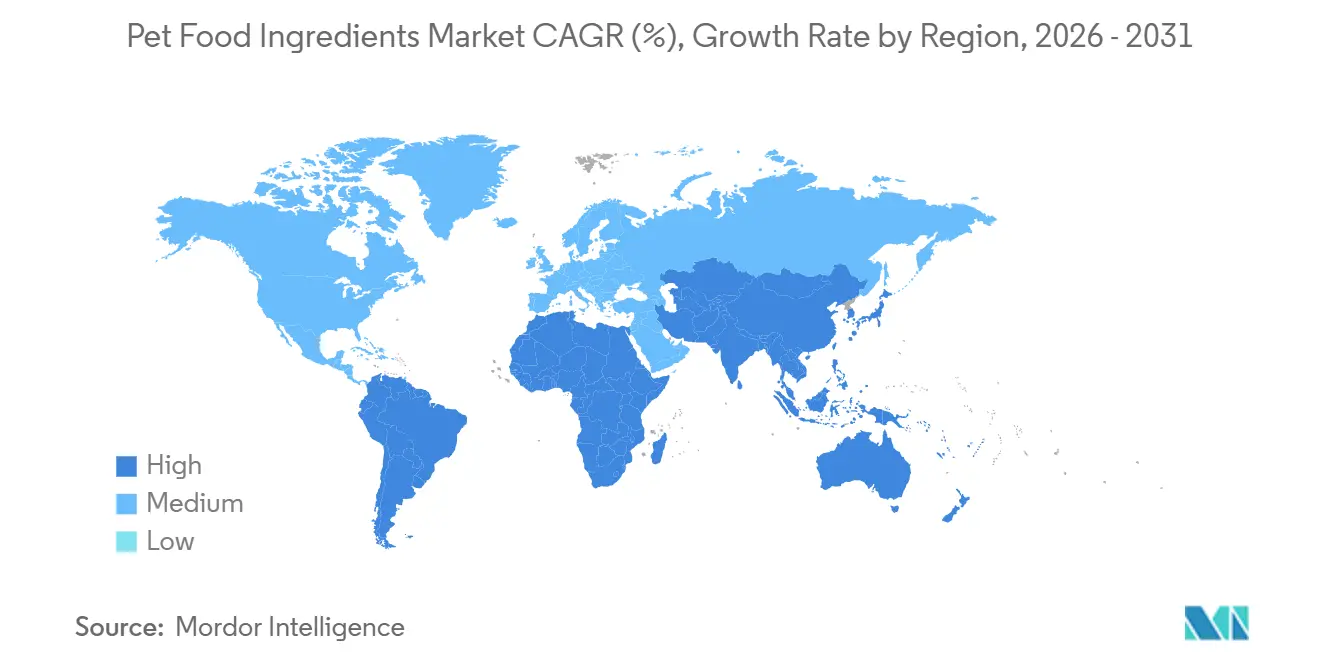

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

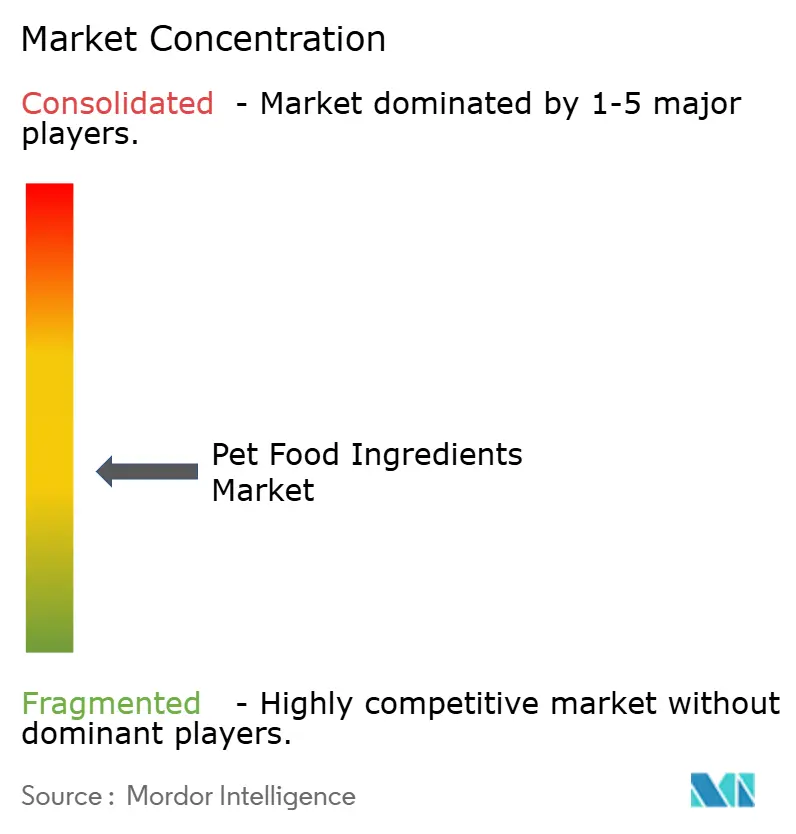

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Ingredients Market Analysis by Mordor Intelligence

The Pet Food Ingredients Market size was valued at USD 45.03 billion in 2025 and is estimated to grow from USD 47.90 billion in 2026 to reach USD 65 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031). Robust premiumization, expanding regulatory clearances for novel proteins, and supply-chain shifts toward traceable inputs are pushing revenue higher. North America remained the revenue leader in 2025 as consumers favored human-grade solutions, yet Asia-Pacific is setting the growth pace due to rising incomes, modernized safety codes, and rapid e-commerce adoption. Ingredient suppliers are re-engineering sourcing models around clean-label claims that resonate with younger pet owners, while cost volatility for grains and rendered meals continues to drive interest in insect, pulse, and precision-fermented alternatives. Competitive intensity is moderate, leaving open lanes for niche innovators targeting exotic pets, functional additives, and direct-to-consumer fresh diets.

Key Report Takeaways

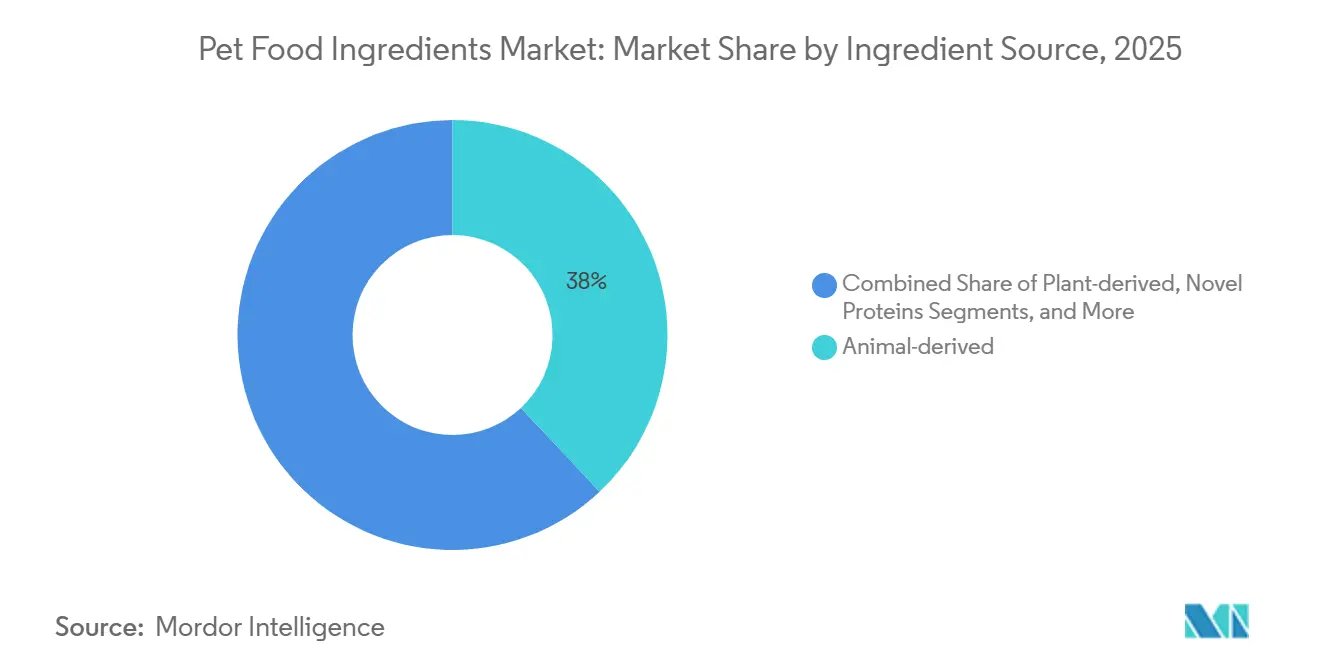

- By ingredient source, animal-derived proteins led with 38% of the pet food ingredients market share in 2025, while insect-based novel proteins are forecast to expand at a 12.4% CAGR through 2031.

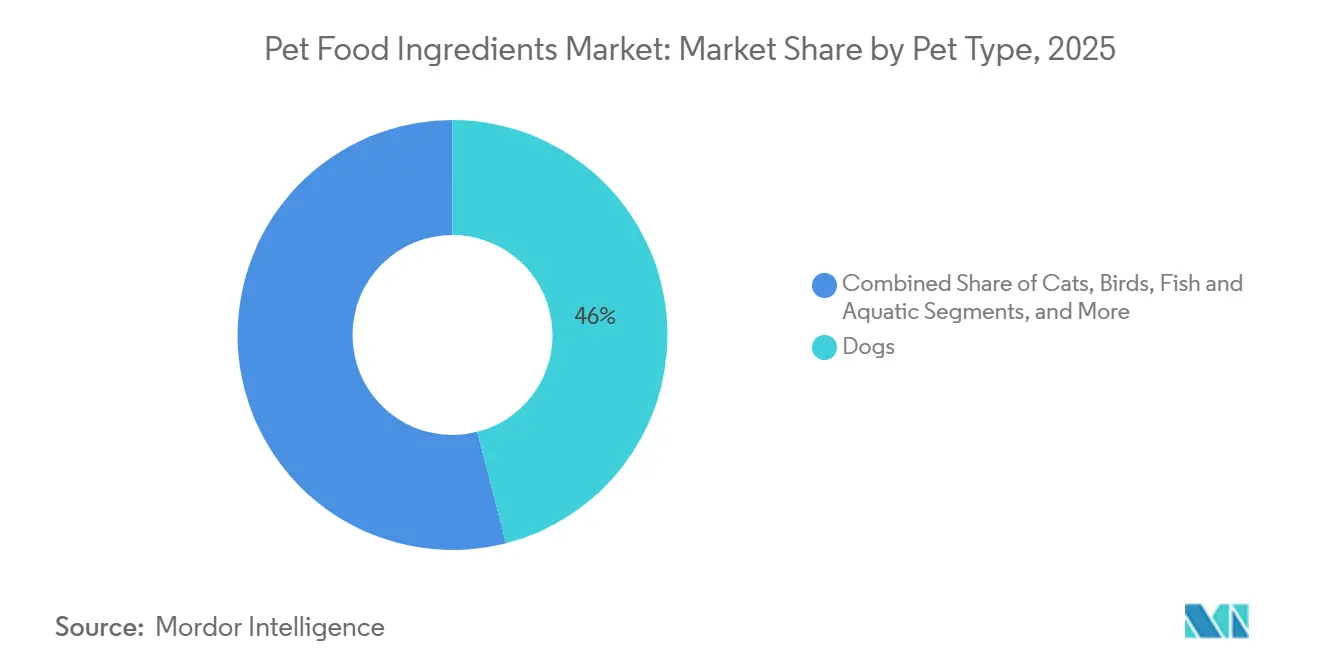

- By pet type, dogs accounted for 46% of the pet food ingredients market size in 2025, while reptiles and exotics are projected to rise at a 9.7% CAGR through 2031.

- By application, dry kibble accounted for 42% of the pet food ingredients market size in 2025, while raw, fresh, and freeze-dried formats are projected to progress at a 11.2% CAGR through 2031.

- By geography, North America captured a 34% revenue share in 2025, while the Asia-Pacific region is advancing at an 8.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in premium and human-grade pet food launches | +1.2% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Accelerated shift toward direct-to-consumer fresh diets | +0.9% | North America core, expanding to Western Europe | Short term (≤ 2 years) |

| Expansion of render-free clean label supply chains | +0.7% | North America and Europe, limited adoption in emerging markets | Medium term (2-4 years) |

| Increased venture funding for novel protein scale-up | +1.0% | Global, with concentration in Europe and North America | Long term (≥ 4 years) |

| Regulatory easing for insect-based pet food in United States and Europe | +1.1% | Europe and North America, early pilots in Asia-Pacific | Medium term (2-4 years) |

| Adoption of precision fermentation to lower amino-acid cost curves | +0.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Premium and Human-Grade Pet Food Launches

Pet owners increasingly treat companion animals like family and demand ingredients that mirror human food standards. Brands such as The Honest Kitchen and Open Farm purchase USDA-inspected meats and organic vegetables, bypassing rendered by-products. This strategy forces suppliers to provide audit trails, secure Non-GMO Project and USDA Organic seals, and invest in blockchain systems that validate origin from farm to bowl. A 2025 survey showed 62% of U.S. dog owners now rank ingredient transparency above price, up 14 points from 2020[1]Source: American Pet Products Association, “Pet Industry Market Size and Ownership Statistics,” americanpetproducts.org . Premium formulas typically retail 20% to 30% higher than mass-market alternatives, motivating ingredient vendors to create segregated supply chains that guarantee clean labels and traceable provenance. Documentation requirements raise barriers for low-cost commodity suppliers and create white-space for specialized processors that handle small-batch, human-grade inputs. As transparency becomes table stakes, brands that prove end-to-end integrity strengthen loyalty and reinforce pricing power.

Accelerated Shift Toward Direct-to-Consumer Fresh Diets

Subscription brands, notably The Farmer’s Dog, Ollie, and Nom Nom, deliver chilled meals that rely on minimally processed meats, vegetables, and functional powders intolerant to extrusion heat. Ingredion reported a 40% year-over-year jump in sales of cold-processed starches in 2025, underscoring format momentum. Fresh diets’ shorter shelf lives favor regional suppliers with refrigerated networks, redistributing margin away from global commodity renderers toward nearby poultry processors and vegetable co-packers. Emerging automation in small-footprint kitchens enables city-adjacent production hubs that meet fast turnaround times and reduce transport emissions. The format’s nutritional positioning enhances weight-management and digestibility claims, sharpening the competitive edge over traditional kibble.

Expansion of Render-Free Clean-Label Supply Chains

Premium brands increasingly reject meat meals and animal by-products, procuring whole-muscle cuts and organs directly from USDA-inspected facilities. Tyson Foods entered the segment in 2025 by launching deboned chicken breast and liver lines for pet formulators. Render-free models add 15% to 25% to ingredient costs, yet marketing narratives around single-source proteins justify premiums among affluent consumers. Eliminating “mystery meat” improves label clarity, a critical differentiator in e-commerce channels where customers scrutinize ingredient panels. Suppliers that secure multi-species slaughterhouse partnerships gain volume advantages and can flex supply between human and pet demand swings. However, higher raw-material costs pressure margin and necessitate careful portion sizing to meet target retail prices.

Regulatory Easing for Insect-Based Pet Food in United States and Europe

The European Food Safety Authority cleared yellow mealworm, house cricket, and black soldier fly for pet food use, and the United States Food and Drug Administration granted Generally Recognized as Safe (GRAS) status. These approvals unlock addressable markets exceeding USD 3 billion annually across the two regions. Insect proteins require 90% less land and 80% less water than beef, helping brands achieve corporate carbon goals. Compliance with Association of American Feed Control Officials nutrient profiles ensures insects can deliver complete diets, quelling formulation concerns. Regulatory momentum encourages contract manufacturers to add dedicated insect-handling lines, further reducing barriers for emerging brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Uncertainty in Poultry By-Products Post-AI (Avian Influenza) Outbreaks | -0.8% | North America and Europe, sporadic impact in Asia-Pacific | Short term (≤ 2 years) |

| Volatility in grain prices impacting plant derivatives | -0.6% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Regulatory ambiguity around cultured protein labeling | -0.4% | North America and Europe, minimal impact in Asia-Pacific | Medium term (2-4 years) |

| Consumer skepticism of genetically modified microbial proteins | -0.5% | North America and Europe, less pronounced in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Uncertainty in Poultry By-Products Post-AI (Artificial Intelligence) Outbreaks

Avian influenza outbreaks in 2024 and 2025 cut poultry by-product supply, prompting substitution with higher-priced pork or fish meals. The U.S. Department of Agriculture confirmed H5N1 across 15 states, leading to the culling of over 20 million birds[2]Source: U.S. Department of Agriculture, “Avian Influenza,” aphis.usda.gov. Darling Ingredients reported a 12% drop in poultry fat volumes in 2025 as biosecurity protocols restricted plant access. Commodity kibble makers felt the margin squeeze most acutely because rendered poultry meals underpin low-cost formulations. Premium brands that use diversified proteins or novel insects absorbed shocks more easily, highlighting the value of flexible sourcing contracts. Periodic outbreaks every three to five years pose recurring risks and encourage inventory buffers or forward contracts to mitigate shortages.

Volatility in Grain Prices Impacting Plant Derivatives

Wheat and corn futures climbed 18% and 22%, respectively, from January 2024 to December 2025, driven by Argentine drought and Russian export curbs. ADM disclosed delayed pet food orders in Q3 2025 as clients avoided locking into inflated cereal contracts. Rising costs flow through to wheat gluten and corn gluten meal, compressing margins for grain-heavy kibble producers. Legume concentrates like pea and chickpea offer partial hedges due to lower correlation with cereal markets, yet reformulating requires digestibility testing and palatability adjustments that slow adoption. Companies with vertical grain integration or multiyear hedging programs weather volatility better than spot buyers, underscoring the importance of supply-chain discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Source: Novel Proteins Disrupt Cost Curves

Animal-derived inputs anchored the pet food ingredients market at 38% share in 2025, buoyed by poultry meals that deliver cost-efficient protein. The pet food ingredients market size tied to insect-based novel proteins is forecast to expand at a 12.4% CAGR to 2031 as regulatory clearances and venture funding accelerate scale. Protix and Innovafeed are commissioning black soldier fly campuses that slash production costs and shorten lead times. Plant-derived ingredients, including pea and chickpea concentrates, are favored for their lower carbon intensity and compatibility with grain-free claims. Functional additives such as prebiotics, probiotics, and krill-derived omega-3s receive outsized attention because digestive and skin health remain leading purchase drivers.

Commodity beef and pork meals satisfy price-sensitive kibble but struggle with negative “mystery meat” perceptions among premium shoppers. Marine oils from Aker BioMarine and Omega Protein provide high levels of EPA and DHA for senior and therapeutic diets. Dairy by-products, vegetable oils, and fruit powders round out formulations by supplying flavor, essential fatty acids, fiber, and antioxidants. As costs for rendered meals fluctuate with disease outbreaks, formulators increasingly weigh novel proteins not solely on sustainability merits but on improved cost predictability. The pet food ingredients market increasingly bifurcates into a value tier optimizing for price and a premium tier leveraging transparent, multifunctional inputs to justify mark-ups.

By Application: Freeze-Dried Formats Capture Premium Wallets

Dry kibble accounted for 42% of 2025 revenue due to shelf stability and low cost. Wet or canned meals held significant share, primarily serving cats and older dogs that require softer textures. The pet food ingredients market size tied to raw, fresh, and freeze-dried applications is projected to grow 11.2% annually to 2031, propelled by brands like Stella and Chewy’s and The Farmer’s Dog that promote minimally processed, high-protein diets. Treats and snacks comprised a notable share of the market, while veterinary diets posted strong growth by addressing obesity, renal, and allergen issues under clinical guidance.

Freeze-drying preserves nutrients without synthetic preservatives, satisfying clean-label mandates and allowing convenient shelf storage before rehydration. Supplements and toppers, including bone-broth powders and krill oils, continue to expand as owners customize base diets with functional boosts. Format diversification lets manufacturers segment pricing ladders, drawing first-time buyers with treats before upselling to complete fresh meals. As cold-chain logistics improve and subscription services normalize, raw and fresh diets will erode kibble share in affluent urban centers, although mass-market retailers will still rely on extruded formats for entry-level price points.

By Pet Type: Exotic Categories Drive Niche Growth

Dogs captured 46% of 2025 demand, reflecting their larger caloric intake and cultural popularity. Cats followed as the next largest segment, but exotic pets, including reptiles, amphibians, and invertebrates, are growing 9.7% per year through 2031. Owners of bearded dragons and leopard geckos demand insect-rich diets fortified with vitamin D3 and calcium, a specification tailor-made for black soldier fly meal suppliers. Bird owners focus on seed blends enhanced with omega-3s and carotenoids to support plumage, while fish enthusiasts purchase krill and spirulina supplements that enhance coloration. Small mammals such as rabbits and guinea pigs need high-fiber pellets that include timothy hay, an application benefiting from Ingredion’s binding starches.

Margin expansion opportunities lie in specialty segments where fewer competitors command higher prices, such as reptile or ornamental fish formulas. Online forums and social media groups amplify niche requirements, creating rapid feedback loops that favor agile brands able to tweak formulations. Dogs and cats will continue to anchor volume, yet diversified portfolios mitigate risk and tap into rising urban preferences for smaller, low-maintenance companions. The trend aligns with demographic shifts toward apartment living and delayed parenthood, factors that elevate ownership of exotics that require less space and noise management.

Geography Analysis

North America accounted for 34% of 2025 sales, underpinned by the United States’ large companion-animal population and well-defined FDA and AAFCO regulations[3]Source: U.S. Food and Drug Administration, “Animal Food and Feeds,” fda.gov. Growth concentrates in premium and novel-protein segments as human-grade and fresh subscription brands scale urban distribution. Canada mirrors these trends, while Mexico remains price sensitive, relying on dry kibble manufactured with local cereals. The region’s forecast compound annual growth rate through the forecast period reflects a mature base supplemented by upscale category gains rather than volume explosions. Europe held significant share in 2025, supported by high per-capita pet ownership in Germany, the United Kingdom, and France. European Food Safety Authority (EFSA) approvals catalyzed insect-protein adoption, enabling Protix and Ynsect to market black soldier fly and yellow mealworm meals at a commercial scale[4]Source: European Food Safety Authority, “Insect Protein Approvals,” efsa.europa.eu .

Asia-Pacific is the fastest-growing region, advancing at 8.9% annually through 2031. China’s updated 2024 pet food safety codes tightened labeling and ingredient standards, encouraging foreign investment and domestic up-branding. Japan’s aging pet demographic favors joint-support additives like glucosamine, while South Korea’s millennial owners adopt freeze-dried diets at rising rates. India and Southeast Asia show early-stage adoption curves with strong upside as disposable incomes climb. The region’s fragmented distribution and regulatory diversity require localized strategies but offer outsized gains to suppliers that navigate complexity.

South America is forecast to climb strongly, led by Brazil’s recovering economy and rising dog ownership. Ingredient imports expose manufacturers to foreign-exchange swings, incentivizing regional pulse and animal protein production. Middle Eastern markets are expanding steadily, propelled by growing expatriate communities and easing cultural attitudes toward pets. Africa’s compound annual growth rate stems from urbanization and emerging middle classes in South Africa, Nigeria, and Kenya, though cold-chain gaps keep dry kibble dominant.

Competitive Landscape

The pet food ingredients market shows moderate concentration. Cargill Incorporated, Archer Daniels Midland Company, and Darling Ingredients leverage livestock rendering networks and global commodity trading to maintain cost leadership. Specialty players BASF SE, DSM-Firmenich AG, and Symrise occupy high-margin niches in vitamins, carotenoids, and palatants, using formulation know-how and technical service to create lock-in. Venture-backed disruptors Protix and Innovafeed are scaling insect protein rapidly, challenging incumbent cost structures and winning sustainability-focused contracts.

Strategic maneuvers include vertical integration as Tyson Foods launched pet-grade deboned chicken to capture value that previously flowed to renderers. Horizontal consolidation continued as Cargill Incorporated acquired Veramaris in 2024 to secure algae-based omega-3 oils for aquaculture and pet applications. Patent filings cluster around fermentation and insect rearing, with Evonik holding key microbial lysine patents. Incumbents’ regulatory expertise and ability to finance feeding trials serve as barriers that smaller peers mitigate through partnerships with contract research organizations.

Future competition will focus on traceability platforms, cold chain optimization, and the development of functional ingredients. Companies that blend sustainability metrics with tangible health benefits such as krill-derived phospholipids for joint health will gain pricing power. Conversely, suppliers tied exclusively to commodity-rendered meals may cede share as disease outbreaks and consumer perception challenges undermine their value proposition.

Pet Food Ingredients Industry Leaders

Cargill Incorporated

Darling Ingredients

Tyson Foods

BASF SE

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BioCraft Pet Nutrition has obtained EU registration for cell-cultured mouse meat, marking the first commercial use of lab-grown ingredients in cat food within Europe.

- December 2024: General Mills acquired Whitebridge Pet Brands to enhance its ingredient sourcing capabilities and expand its premium product offerings.

- April 2024: Wilbur-Ellis Nutrition, LLC, a provider of animal nutrition solutions, partnered with Bond Pet Foods, Inc., a Boulder, Colorado-based company specializing in fermentation-based animal protein production, to develop ingredients for pet food applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pet food ingredients market as the worldwide value of animal, plant, and synthetic raw materials, proteins, fats, carbohydrates, functional additives, and palatants, supplied to commercial pet food makers during the base year.

We exclude finished pet foods, retail veterinary diets, and feed additives used solely for livestock.

Segmentation Overview

- By Ingredient Source

- Animal-derived

- Poultry proteins and fats

- Meat meals (beef, pork)

- Fish and marine ingredients

- Dairy derivatives and whey

- By-products and trimmings

- Plant-derived

- Cereals and cereal derivatives

- Pulses and legumes concentrates

- Oilseeds and vegetable oils

- Fruit and vegetable powders

- Novel Proteins

- Insect-based proteins

- Cultured/cell-based proteins

- Microbial and algae proteins

- Functional Additives

- Prebiotics and probiotics

- Vitamins and minerals

- Specialty fats and oils

- Flavors and palatants

- Animal-derived

- By Pet Type

- Dogs

- Cats

- Birds

- Fish and Aquatic

- Small Mammals

- Reptiles and Exotics

- By Application

- Dry Kibble

- Wet/Canned

- Treats and Snacks

- Raw/Fresh and Freeze-dried

- Veterinary Diets

- Supplements and Toppers

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed rendering executives, plant-protein formulators, premix blenders, and procurement managers across North America, Europe, and Asia. These talks validated inclusion rates, contract lead times, and the pace at which novel proteins enter mainstream recipes.

Desk Research

We began with public sources such as USDA GATS shipment data, FAO STAT commodity balances, Eurostat feed material codes, AAFCO ingredient lists, and Pet Food Institute cost trackers to size volumes and establish typical price corridors. Company 10-Ks, investor decks, and trade press provided revenue splits and capacity clues. Paid libraries like D&B Hoovers (company financials) and Dow Jones Factiva (deal news) helped fill ownership and pricing gaps. The sources named here are illustrative; numerous additional open datasets supported data checks and clarifications.

Market-Sizing & Forecasting

We apply a top-down construct that starts with global pet food output in tonnes, multiplies by ingredient cost share, and adjusts for regional formulation mixes. Supplier roll-ups and ASP × volume samples act as bottom-up sense checks. Key variables include dog and cat population growth, meat-meal price indices, starch substitution ratios, protein innovation adoption curves, and currency movements. A multivariate regression extends these drivers to 2030, while bounded scenarios agreed with experts bridge patchy bottom-up data.

Data Validation & Update Cycle

Outputs pass variance screens against trade statistics and listed-company segment revenue. Senior reviewers sign off, reports refresh every twelve months, and interim flashes follow material events so clients always receive the latest view.

Why Mordor's Pet Food Ingredients Baseline Commands Reliability

Published estimates often diverge because each firm selects different ingredient cut-offs, price references, and refresh cadences.

Divergence widens when agricultural by-products destined for biofuel are counted, when distributor mark-ups are folded in, or when the base year shifts. Mordor aligns strictly with ingredients entering pet food factories in 2025 and recalibrates exchange rates quarterly, which keeps our benchmark steady yet current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 50.5 B (2025) | Mordor Intelligence | |

| USD 60.48 B (2023) | Global Consultancy A | Includes supplements for treats and two-year older base |

| USD 34.2 B (2023) | Global Consultancy B | Counts only additives, omits core proteins |

| USD 66.8 B (2024) | Industry Journal C | Mixes distributor mark-ups and partial double counting |

The comparison shows that Mordor's disciplined scope selection, annual refresh, and multi-layer validation deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the pet food ingredients market?

The market stands at USD 47.90 billion in 2026.

How fast is the pet food ingredients market anticipated to grow?

It is projected to expand at a 6.30% CAGR from 2026 to 2031.

Which ingredient segment shows the fastest growth potential?

Insect-based novel proteins are forecast to rise at a 12.4% CAGR through 2031.

Why are direct-to-consumer fresh diets influencing ingredient demand?

Fresh diets avoid high-temperature extrusion, spurring demand for human-grade meats, cold-process starches, and functional powders.

How did avian influenza outbreaks affect ingredient sourcing?

Outbreaks reduced poultry by-product availability, raising costs and encouraging formulators to adopt alternative proteins.

Page last updated on: