Pet Dietary Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

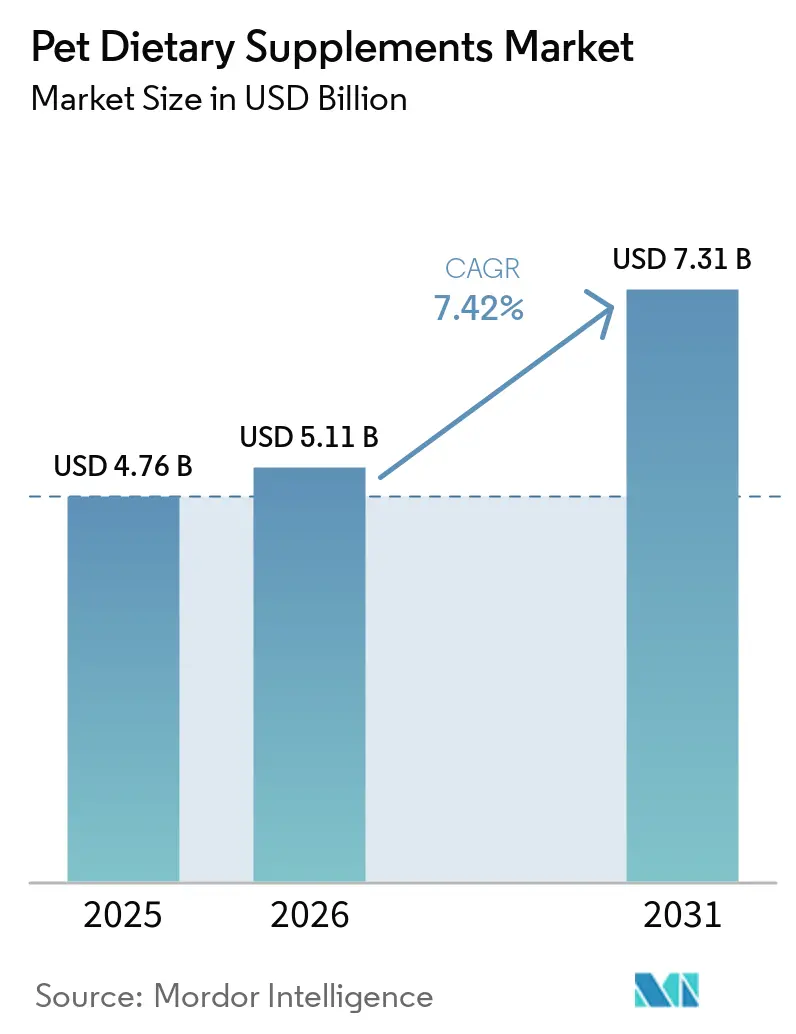

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 7.31 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Dietary Supplements Market Analysis by Mordor Intelligence

The pet dietary supplements market is projected to expand from USD 4.76 billion in 2025 and USD 5.11 billion in 2026 to USD 7.31 billion by 2031, registering a CAGR of 7.42% between 2026 to 2031. Growth is propelled by rising pet humanization, the strengthening of links between preventive care and nutrition, and digital sales models that convert one-time purchases into repeat orders. Veterinary endorsement of clinically backed formulations is elevating trust, while AI platforms deliver microbiome-based customization that lifts lifetime value. Soft-chews remain the compliance workhorse, but powders are tracking double-digit growth as subscription brands favor their dosing flexibility. Regionally, North America remains the leader, yet Asia is the fastest-growing market as urban households allocate more discretionary income to companion-animal wellness.

Key Report Takeaways

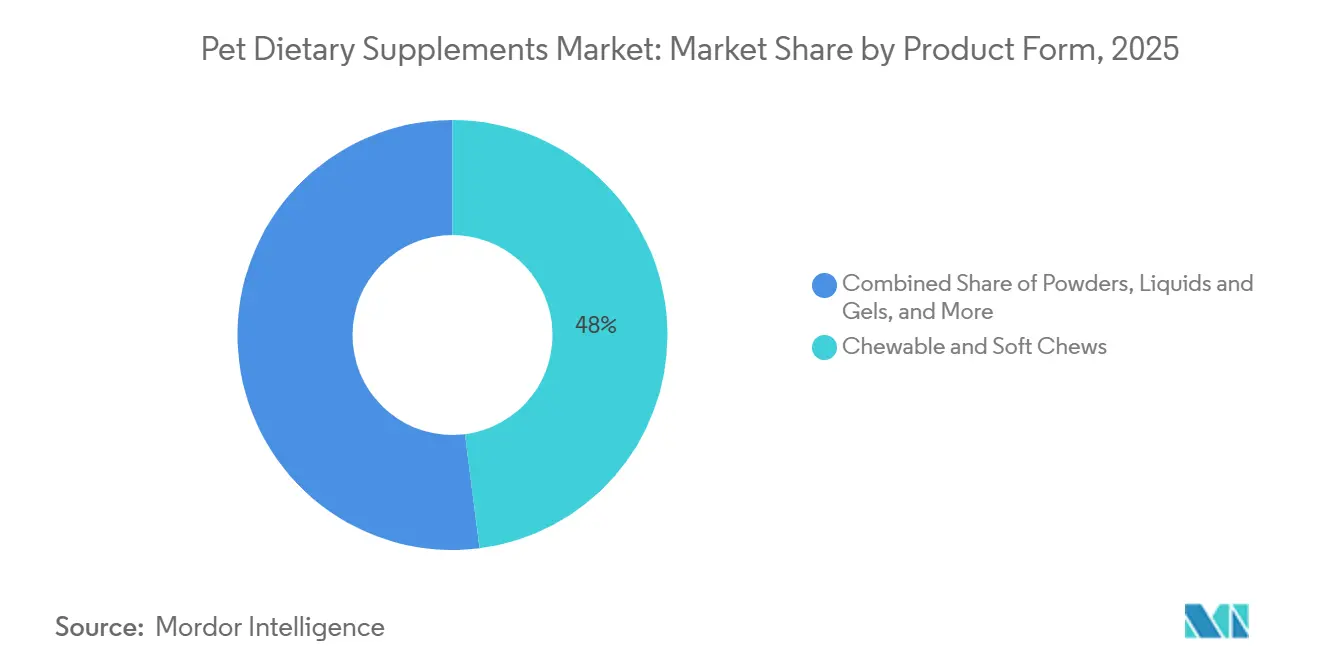

- By product form, chewable and soft chews captured 48% of the pet dietary supplements market size in 2025, and powders are forecast to grow at an 11.2% CAGR through 2031.

- By supplement type, multivitamins held 36% of the pet dietary supplements market size in 2025, whereas probiotics and prebiotics are projected to expand at a 10.5% CAGR to 2031.

- By function, hip and joint formulas accounted for 28% of the 2025 total, and digestive health products are set to rise at an 11.8% CAGR through 2031.

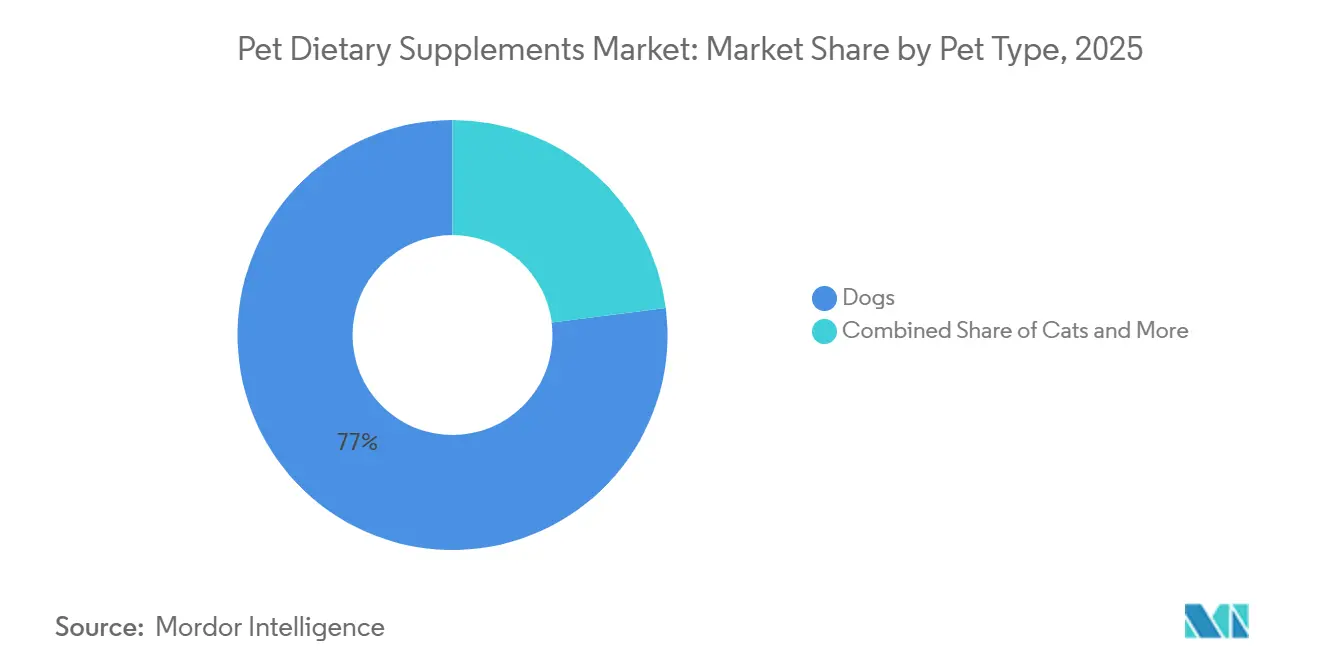

- By pet type, dogs captured 77% of the pet dietary supplements market share in 2025, while feline-focused lines are advancing at a 9.5% CAGR through 2031 due to innovations in urinary and renal care.

- By distribution channel, specialty stores held a 42.3% share of the pet dietary supplements market in 2025, and online channels are projected to record the highest CAGR at 12.6% through 2031.

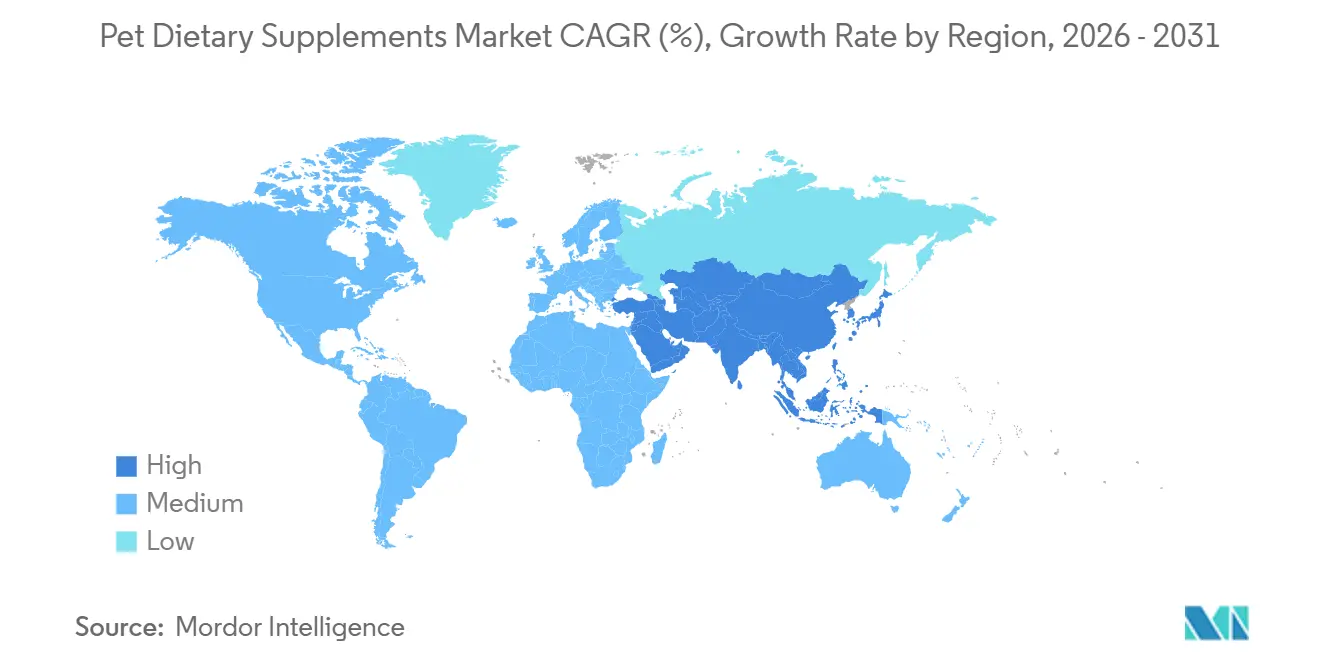

- By geography, North America accounted for 48.4% of global revenue in 2025, while the Asia-Pacific region is projected to grow at a CAGR of 7.4% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Dietary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for multivitamin soft-chews | +1.2% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Veterinary endorsement of probiotic formulas | +1.5% | North America and Europe, expanding in Asia | Long term (≥ 4 years) |

| Subscription-based Direct-To-Consumer (DTC) e-commerce expands Average Order Value (AOV) | +1.3% | North America, Western Europe, urban Asia | Short term (≤ 2 years) |

| AI-driven personalized microbiome blends | +0.8% | North America and select European markets | Long term (≥ 4 years) |

| Algae-derived omega-3 cost parity with fish oil | +0.6% | Global, with plants in Europe and the United States | Medium term (2-4 years) |

| Postbiotic stability enables ambient logistics | +0.5% | Global, critical in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multivitamin Soft-Chews

Palatability drives compliance in daily supplement regimens, and soft-chews have emerged as the dominant delivery format because they mimic treats rather than medication. Pet owners report higher adherence rates with chewable formats compared to tablets or capsules, a behavioral insight that has prompted manufacturers to invest in flavor-masking technologies and texture optimization. Zesty Paws, a subsidiary of H&H Group, is expanding its distribution network by increasing the number of retail stores. The company is focusing on bacon-flavored and peanut-butter soft chews formulated for voluntary consumption by dogs [1]Source: H&H Group, “Investor Relations,” hhgroupholding.com. The format's success has also attracted private-label entrants, as retailers recognize that soft-chews command premium shelf prices while generating repeat purchases. Manufacturers are responding by exploring pectin-based vegan alternatives, though these formulations require additional stabilizers to match the chewability of animal-derived gelatin.

Veterinary Endorsement of Probiotic Formulas

Veterinarians function as gatekeepers in the pet supplement market, and their willingness to recommend specific products directly influences retail adoption rates. Clinical evidence supporting the use of probiotics for gastrointestinal health has reached a tipping point, with peer-reviewed studies demonstrating that strains such as Enterococcus faecium and Bifidobacterium animalis reduce the duration of diarrhea and improve fecal consistency in dogs. A 2024 study published in the Journal of Veterinary Internal Medicine found that dogs receiving Visbiome Vet experienced a 42% reduction in acute diarrhea episodes compared to dogs in the placebo group. Purina's FortiFlora, which holds the largest share of the veterinary probiotic segment, benefits from decades of clinical trials and a sales force that educates practitioners on microbiome science.

AI-Driven Personalized Microbiome Blends

Algorithmic customization represents the next frontier in pet nutrition, moving beyond breed-based recommendations to individual microbiome profiles. Nestle (Purina)'s Petivity Microbiome Analysis Kit, launched in April 2024, collects fecal samples and sequences bacterial DNA to identify dysbiosis patterns, then formulates powder sachets with targeted probiotic strains and prebiotic fibers. Ollie's acquisition of DIG Labs in October 2024 brought machine-learning capabilities that analyze pet health records, activity data, and genetic markers to predict nutrient deficiencies before clinical symptoms appear. These platforms charge premium prices, with Petivity kits retailing at USD 99 for the initial analysis and USD 79 per month for customized supplements, positioning them as luxury offerings for affluent pet owners.

Algae-Derived Omega-3 Cost Parity with Fish Oil

Sustainability concerns and supply-chain volatility in marine omega-3 sources have accelerated investment in algal oil production. Veramaris, a joint venture between DSM, Firmenich, and Evonik, operates a fermentation facility in Nebraska that produces EPA and DHA from marine microalgae, thereby bypassing the need for wild-caught fish. The company reported that its algal oil achieved cost parity with fish oil in 2024 for bulk pet-food applications, driven by economies of scale and reduced purification steps compared to krill-oil processing. Algae-derived omega-3 also appeals to vegan pet owners, addressing concerns about ocean depletion, although palatability remains a challenge, as some pets reject the earthy flavor profile. In 2024, Nordic Naturals and NOW Foods introduced algae-based omega-3 supplements for pets, marketing them as eco-friendly alternatives that deliver equivalent bioavailability to fish oil.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Food and Drug Administration (FDA) and Association of American Feed Control Officials (AAFCO) claim regulations | -0.9% | North America with export spillovers | Long term (≥ 4 years) |

| Price sensitivity among first-time buyers | -0.7% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Volatile krill-oil supply chain | -0.4% | Global, premium omega-3 lines | Medium term (2-4 years) |

| Counterfeit products on cross-border marketplaces | -0.5% | Asia-Pacific and South America, growing in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Among First-Time Buyers

Pet supplements occupy an ambiguous position in household budgets, perceived as beneficial but not essential, which makes them vulnerable to discretionary spending cuts during economic downturns. First-time buyers, who often enter the category through veterinary recommendations or social media advertising, exhibit high price elasticity, with conversion rates dropping 40% when products exceed USD 30 per month, according to internal data from digital-native brands. This sensitivity is most pronounced in emerging markets, where per-capita pet spending remains a fraction of the levels in North America. Brands have responded by introducing starter packs and trial sizes priced below USD 15, though these formats erode gross margins and complicate inventory management. The challenge for premium brands lies in communicating value propositions beyond price, such as clinical validation, veterinary endorsements, and transparent supply chains, to justify higher price points.

Counterfeit Products on Cross-Border Marketplaces

Gray-market platforms and unregulated e-commerce sites have become conduits for counterfeit pet supplements, undermining brand equity and posing safety risks. The Food and Drug Administration (FDA) Operation Pangea, a coordinated international enforcement action, seized over 1,200 shipments of counterfeit pet medications and supplements in 2024, yet the volume of illicit products continues to grow as counterfeiters exploit lax platform moderation and cross-border shipping loopholes [2]Source: U.S. Food and Drug Administration, “AFIC Guidance,” fda.gov . Counterfeit supplements often contain incorrect active-ingredient levels, undeclared fillers, or contaminants, such as heavy metals, leading to adverse events that damage the category's credibility. Brands have invested in authentication technologies such as QR codes and blockchain-based provenance tracking, but these measures require consumer engagement and add 2% to 4% to unit costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Soft-Chews Dominate Through Compliance Engineering

Chewable and soft chews captured 48% of the pet dietary supplements market size in 2025, a dominance rooted in behavioral psychology rather than nutritional superiority. Pet owners struggle with pill administration, and chewable formats eliminate the friction of forcing tablets down reluctant pets' throats. Regulatory influence remains minimal in product-form selection, as the Food and Drug Administration (FDA) focuses on ingredient safety rather than delivery mechanisms. The European Food Safety Authority has raised concerns about certain gelling agents used in soft chews, prompting manufacturers to reformulate with European Food Safety Authority (EFSA)-approved alternatives, such as carrageenan and agar. The shift toward soft-chews reflects broader humanization trends, as pet owners increasingly demand products that mirror their own supplement routines in format and flavor.

Powders are forecasted to grow at an 11.2% CAGR through 2031, driven by their compatibility with personalized dosing algorithms and lower per-unit manufacturing costs, which enable competitive pricing. Powders benefit from the rise of personalized nutrition platforms that ship custom-blended sachets, although they require pet owners to mix supplements into their pet's food, adding a compliance hurdle. Other forms, including topical sprays and transdermal patches, occupy niche segments but are gaining traction for joint-pain relief where oral bioavailability is suboptimal.

By Supplement Type: Probiotics Surge on Clinical Validation

Multivitamins accounted for 36% of the pet dietary supplements market size in 2025, benefiting from their broad appeal and veterinary recommendations for general wellness. Cannabidiol (CBD) regulatory uncertainty hinders mainstream adoption, as manufacturers opt to avoid interstate commerce to circumvent federal enforcement, thereby limiting distribution to state-licensed dispensaries and online direct-to-consumer channels. Herbal extracts, such as turmeric and ashwagandha, are marketed for their anti-inflammatory and calming benefits, although the Food and Drug Administration (FDA) has issued warning letters to companies making disease-treatment claims without substantiation.

Probiotics and prebiotics are projected to expand at a 10.5% CAGR to 2031, as clinical evidence mounts for their role in digestive and immune health. The probiotic surge reflects a convergence of scientific validation and veterinary advocacy. A 2024 meta-analysis published in Frontiers in Veterinary Science reviewed 28 randomized controlled trials and concluded that multi-strain probiotic formulations reduced gastrointestinal symptoms in 67% of dogs with chronic enteropathies [3]Source: Frontiers in Veterinary Science, “Meta-Analysis of Probiotic Efficacy,” frontiersin.org. Prebiotics, which nourish beneficial gut bacteria, are increasingly bundled with probiotics in synbiotic formulations that enhance colonization rates.

By Function: Digestive Health Accelerates on Microbiome Insights

Hip and joint formulas accounted for 28% of the 2025 total, reflecting the aging pet demographic and high prevalence of osteoarthritis in large-breed dogs. The maturity of the dog segment has led brands to adopt micro-segmentation strategies, focusing on breeds susceptible to specific conditions, such as hip dysplasia in German Shepherds and brachycephalic airway syndrome in Bulldogs. In contrast, cat supplements present distinct formulation challenges due to cats being obligate carnivores with low tolerance for plant-based ingredients and heightened sensitivity to taste. Advanced formulations incorporating UC-II collagen, green-lipped mussel, and Boswellia serrata are increasingly replacing traditional glucosamine-only products, supported by clinical studies that show improved pain reduction outcomes.

Digestive health products are set to rise at an 11.8% CAGR through 2031, propelled by microbiome research that links gut health to immune function and behavior. Skin and coat health products benefit from visible outcomes that drive repeat purchases, while immune support supplements gained traction during the COVID-19 pandemic and have sustained elevated demand. The digestive health acceleration stems from veterinary recognition that gastrointestinal disorders underlie a range of systemic conditions, from allergies to anxiety. Probiotics, such as Enterococcus faecium and Lactobacillus acidophilus, have demonstrated efficacy in reducing the duration of diarrhea and improving fecal quality, while prebiotics, such as fructooligosaccharides, enhance probiotic colonization.

By Pet Type: Feline Formulations Gain Traction

Dogs captured 77% of the pet dietary supplements market share in 2025, reflecting their larger population and higher per-capita supplement spending. The dog segment's maturity has prompted brands to pursue micro-segmentation strategies, targeting breeds prone to specific conditions such as hip dysplasia in German Shepherds or brachycephalic airway syndrome in Bulldogs. Dental supplements face skepticism, as mechanical plaque removal remains the gold standard, yet enzymatic formulas that disrupt biofilm formation are gaining veterinary endorsements.

Cats represent the fastest-growing segment, with a 9.5% CAGR through 2031, as manufacturers develop feline-specific formulations that address urinary, renal, and dental health. Cat supplements face unique formulation challenges, as felines are obligate carnivores with limited tolerance for plant-based ingredients and heightened sensitivity to palatability. Small mammal supplements, including those for rabbits and guinea pigs, are expanding as exotic pet ownership rises, though regulatory frameworks for non-traditional companion animals remain underdeveloped.

By Distribution Channel: Specialty Stores Hold, Online Channels Surge

Specialty stores held a 42.3% share of the pet dietary supplements market in 2025, leveraging knowledgeable staff and in-store veterinary clinics to drive sales of supplements. Supermarkets and hypermarkets offer convenience and competitive pricing, but they often lack the specialized knowledge required to effectively assist first-time buyers, resulting in lower conversion rates for premium products. Veterinary clinics play a crucial role in dispensing prescription-grade supplements and products that require professional guidance, although their market share is declining as online retailers offer similar formulations at lower prices. Convenience stores have a minimal role, primarily offering mass-market multivitamins with a limited range of SKUs.

Online channels are projected to record the highest CAGR at 12.6% through 2031, as Autoship programs lock in recurring revenue and reduce customer acquisition costs. Online retailers' recommendation engines cross-sell supplements based on pet profiles and purchase history, increasing basket size and attachment rates.

Geography Analysis

North America accounted for 48.4% of global revenue in 2025, driven by high disposable incomes, mature veterinary infrastructure, and cultural norms that treat pets as family members. The United States dominates regional revenue, with California, Texas, and Florida accounting for 42% of national sales due to high pet ownership rates and the concentration of digital-native brands. Canada's bilingual labeling requirements and stricter import regulations add complexity for cross-border distribution, though the market's affluence and veterinary channel strength support premium pricing. Mexico represents an emerging opportunity, with urbanization and rising middle-class incomes driving the adoption of pet supplements, although counterfeit products and unregulated distribution channels constrain growth.

The Asia-Pacific region is projected to grow at a CAGR of 7.4% through 2031, the fastest regional growth rate, fueled by urbanization, nuclear family structures, and e-commerce penetration in China, Japan, and South Korea. China's pet supplement market is concentrated in tier-1 cities such as Beijing, Shanghai, and Shenzhen, where disposable incomes exceed USD 15,000 per capita, and pet ownership is viewed as a status symbol. Tmall and JD.com dominate online distribution, leveraging livestream commerce and influencer partnerships to drive supplement sales. Japan's aging pet population mirrors its human demographic trends, with 40% of dogs over 10 years old, creating demand for senior-specific formulations targeting joint health and cognitive function. India represents a nascent market with high growth potential, though price sensitivity and limited veterinary infrastructure constrain premium segment adoption.

Europe is projected to grow with Germany, the United Kingdom, and France leading regional revenue. The European Food Safety Authority's rigorous novel-ingredient approval process delays product launches but enhances consumer trust in supplement safety and efficacy. Germany's preference for natural and organic products has driven demand for herbal supplements and algae-based omega-3, while the United Kingdom veterinary channel strength supports prescription-grade formulations. France's regulatory environment mandates veterinary oversight for certain supplement categories, limiting direct-to-consumer distribution but ensuring professional guidance. Southern Europe, including Italy and Spain, exhibits lower supplement penetration due to cultural norms that prioritize fresh-food diets over processed supplements.

Competitive Landscape

Major consumer packaged goods companies, veterinary pharmaceutical firms, and private equity investors are driving consolidation in the market. Nestle (Purina), Mars Incorporated (Mars Petcare), Colgate-Palmolive Company (Hill’s Pet Nutrition), General Mills Inc. (Blue Buffalo), and H&H Group (Zesty Paws) collectively held a significant market share in 2025. These companies are pursuing targeted acquisitions to address capability and ingredient gaps. For instance, General Mills acquired Whitebridge Pet Brands for USD 1.45 billion in 2024. Clinical validation has become a critical factor for retail placement, leading companies to publish peer-reviewed research on the efficacy of their ingredients.

H&H Group (Zesty Paws) expanded its weight-management product portfolio by launching an obesity-focused canine supplement in April 2025. Virbac reported a 13.6% revenue increase in 2025, driven by strong demand for dental and dermatology products supported by veterinary endorsements. Patent protection, such as Mars' US 10709156 B2 for probiotic tablets, allows companies to secure competitive positions in condition-specific segments.

The competitive landscape is also shaped by vertical integration strategies, with companies such as Zoetis and Elanco leveraging their pharmaceutical expertise to develop veterinary-exclusive formulations that command higher margins. Patent activity is concentrated in delivery technologies, such as microencapsulation for probiotic stability and sustained-release coatings for joint-health actives, rather than novel active ingredients, which are typically derived from natural sources and difficult to patent.

Pet Dietary Supplements Industry Leaders

Mars Incorporated (Mars Petcare)

Colgate-Palmolive Company (Hill’s Pet Nutrition)

General Mills Inc. (Blue Buffalo)

Nestle (Purina)

H&H Group (Zesty Paws)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: H&H Group (Zesty Paws) introduced New Vet Strength, a canine obesity supplement that supports fat metabolism, digestion, and satiety in dogs. The product contains scientifically formulated ingredients designed to support weight management.

- February 2025: Fera Pets introduced a dental support powder for pets, incorporating botanical ingredients and postbiotics. The product, called Fera Pets Dental Support, addresses oral health concerns through internal supplementation. Its formulation features three primary components Oravestin, Bactase Pet, and a clinically tested postbiotic.

- December 2024: General Mills completed its acquisition of Tyson Foods' pet treat business for USD 1.2 billion, expanding its Blue Buffalo portfolio with manufacturing capacity and distribution channels that enable cross-selling of supplements alongside treats. The transaction reflects consolidation trends as large food conglomerates seek to capture adjacencies in the pet-care category.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pet dietary supplements market as value generated from nutritionally active products, vitamins, minerals, fatty acids, probiotics, botanicals, and functional blends, administered orally to companion animals to enhance specific health outcomes such as joint mobility, skin condition, digestive balance, and anxiety relief. Products sold as complete pet foods, prescription therapeutics, or livestock feed additives sit outside this scope.

Scope exclusion: Remedies formulated exclusively for food-producing animals or licensed veterinary drugs are not counted in our model.

Segmentation Overview

- By Product Form

- Tablets and Capsules

- Chewable and Soft Chews

- Powders

- Liquids and Gels

- Capsules

- Other Forms

- By Supplement Type

- Multivitamins

- Probiotics and Prebiotics

- Omega-3 and Essential Fatty Acids

- Glucosamine and Chondroitin

- CBD and Hemp Derivatives

- Antioxidants

- Herbal and Botanical Extracts

- Other Supplement Type

- By Function

- Urinary Tract Health

- Hip and Joint Health

- Diabetes Management

- Heart and Renal Health

- Skin and Coat Health

- Immune System Support

- Digestive Health

- Calming and Anxiety Relief

- Dental and Oral Care

- Metabolic/ Weight Management

- Senior/Cognitive Support

- Other Specialty Needs

- By Pet Type

- Dogs

- Cats

- Other Pets

- By Distribution Channel

- Convenience Stores

- Online Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Other Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We speak with veterinarians, e-commerce category managers, specialty-store buyers, contract manufacturers, and ingredient formulators across North America, Europe, and Asia-Pacific. These conversations test desk-research assumptions, surface average selling prices, and reveal regional uptake rates that our desk work alone cannot capture.

Desk Research

We begin by stitching together foundational numbers from tier-one public sources such as the US FDA Center for Veterinary Medicine, the American Pet Products Association, Eurostat trade codes for HS 2309 feed preparations, and peer-reviewed journals tracking ingredient efficacy. To refine regional flow, we review pet population data from national veterinary associations, customs import records for glucosamine and fish-oil concentrates, and retail scanner updates.

Next, our team taps paid databases, D&B Hoovers for company revenue splits and Dow Jones Factiva for launch news, to benchmark supplier footprints and price movements. Company 10-Ks, investor decks, and high-circulation press articles provide additional checkpoints. The secondary source list is illustrative; numerous other documents inform data collection, validation, and clarification.

Market-Sizing & Forecasting

We reconstruct demand using a top-down pet population and supplement penetration pool, which is then cross-checked through selective bottom-up supplier roll-ups and sampled average selling price × volume calculations. Key variables include dog and cat ownership counts, supplement penetration per pet, average retail price shifts by form factor, veterinary visit frequency, e-commerce share of supplement sales, and NASC/FDA registration data. A multivariate regression links these indicators to historical spending, while scenario analysis tests sensitivity to regulatory or raw material shocks before numbers are locked. Data gaps in bottom-up estimates are bridged with channel checks and price band medians.

Data Validation & Update Cycle

Model outputs flow through automated variance scans, peer review, and a senior analyst sign-off. We rerun the model annually, with interim refreshes triggered by regulatory changes, major recalls, or mergers. A last-minute sense check ensures clients receive the latest view.

Why Mordor's Pet Dietary Supplements Baseline Earns Trust

Published estimates often diverge because firms weigh geography, product forms, and pricing windows in distinct ways. Our disciplined variable selection and annual refresh cadence narrow these gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.70 Bn (2025) | Mordor Intelligence | - |

| USD 2.50 Bn (2024) | Global Consultancy A | Includes herbal nutraceutical treats and equine supplements |

| USD 2.95 Bn (2024) | Business Intelligence Firm B | Uses one North American ASP and inflates globally |

| USD 2.62 Bn (2024) | Industry Analytics Group C | Pet population base year set to 2022 with no mid-cycle update |

Taken together, the comparison shows that Mordor Intelligence presents a balanced, transparent baseline anchored to verifiable pet population counts, current pricing, and clearly stated inclusions, giving stakeholders a dependable starting point for strategic planning.

Key Questions Answered in the Report

How fast is the pet dietary supplements market projected to grow between 2026 and 2031?

It is projected to record a 7.42% CAGR, moving from USD 5.11 billion in 2026 to USD 7.31 billion by 2031.

Which product form currently leads sales?

Soft-chews dominate with 48% of 2025 revenue owing to treat-like palatability.

Why are probiotics gaining momentum in companion animals?

Clinical studies and growing veterinary endorsements link specific strains to better digestive and immune outcomes.

What channel is expanding the fastest?

Online subscriptions are rising at a 12.6% CAGR through 2031 as Autoship programs lock in recurring demand.

Page last updated on: