Pet Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

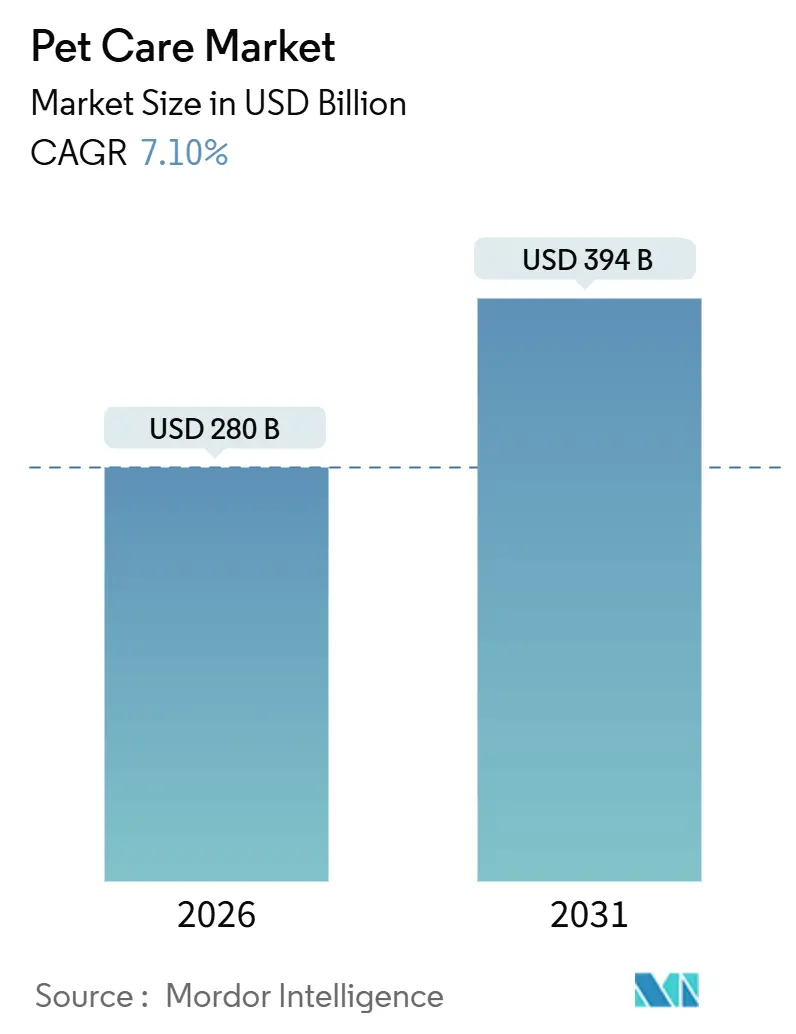

| Market Size (2026) | USD 280 Billion |

| Market Size (2031) | USD 394 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Care Market Analysis by Mordor Intelligence

The pet care market size was USD 280 billion in 2026 and is projected to climb to USD 394 billion by 2031, reflecting a 7.1% CAGR through the period. Younger owners, particularly Generation Z households with multiple pets, are redefining consumption by prioritizing wellness, sustainability, and convenience in their purchase decisions. These shifts underpin premiumization in nutrition, healthcare, and services, while data-driven e-commerce models turn one-off transactions into long-term subscriptions. At the same time, scale advantages in procurement and distribution keep barriers high for new entrants, even as functional-ingredient challengers press incumbents for market share. Raw material price fluctuations, stricter labeling regulations, and risks of counterfeiting continue to pose challenges. However, these factors are unlikely to significantly hinder the projected growth of the pet care market over the next five years.

Key Report Takeaways

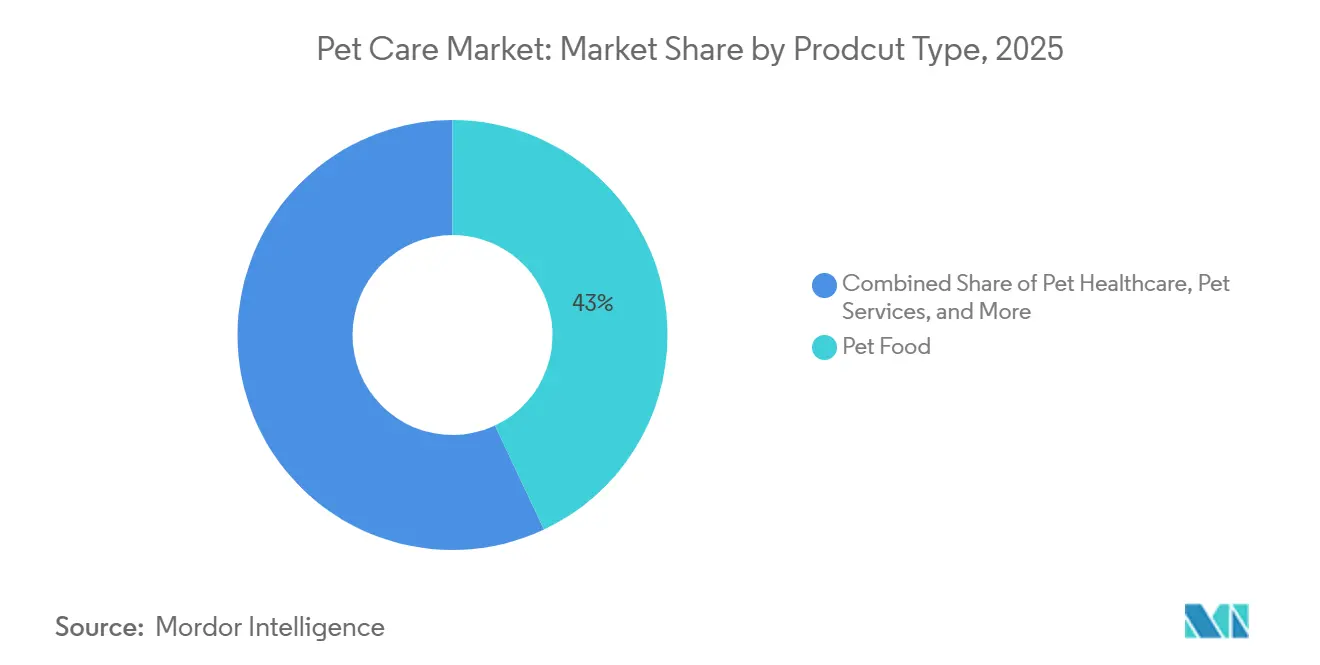

- By product type, Pet Food accounted for 43% of the pet care market size in 2025, and Pet Services is forecast to expand at a 10% CAGR through 2031.

- By animal type, Dogs captured 46% pet care market share in 2025, while Cats are advancing at an 8.4% CAGR to 2031.

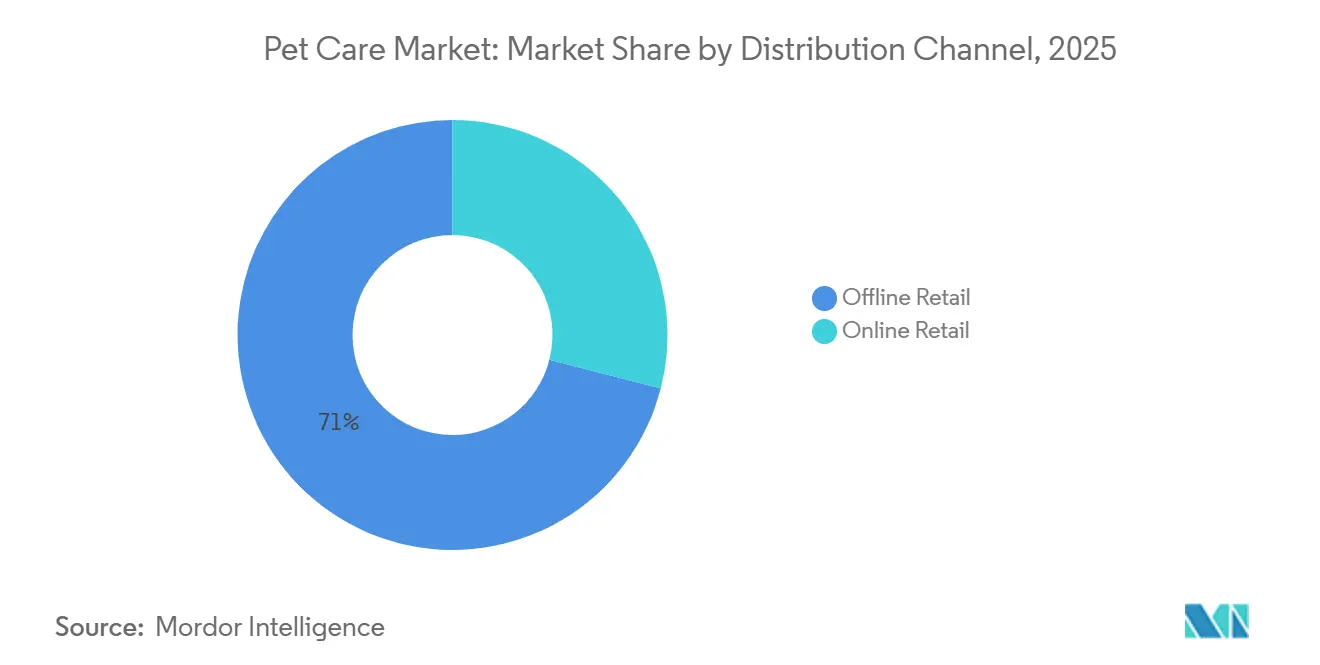

- By distribution channel, Offline Retail held a 71% share in 2025, whereas Online Retail is projected to reach an 11.8% CAGR through 2031.

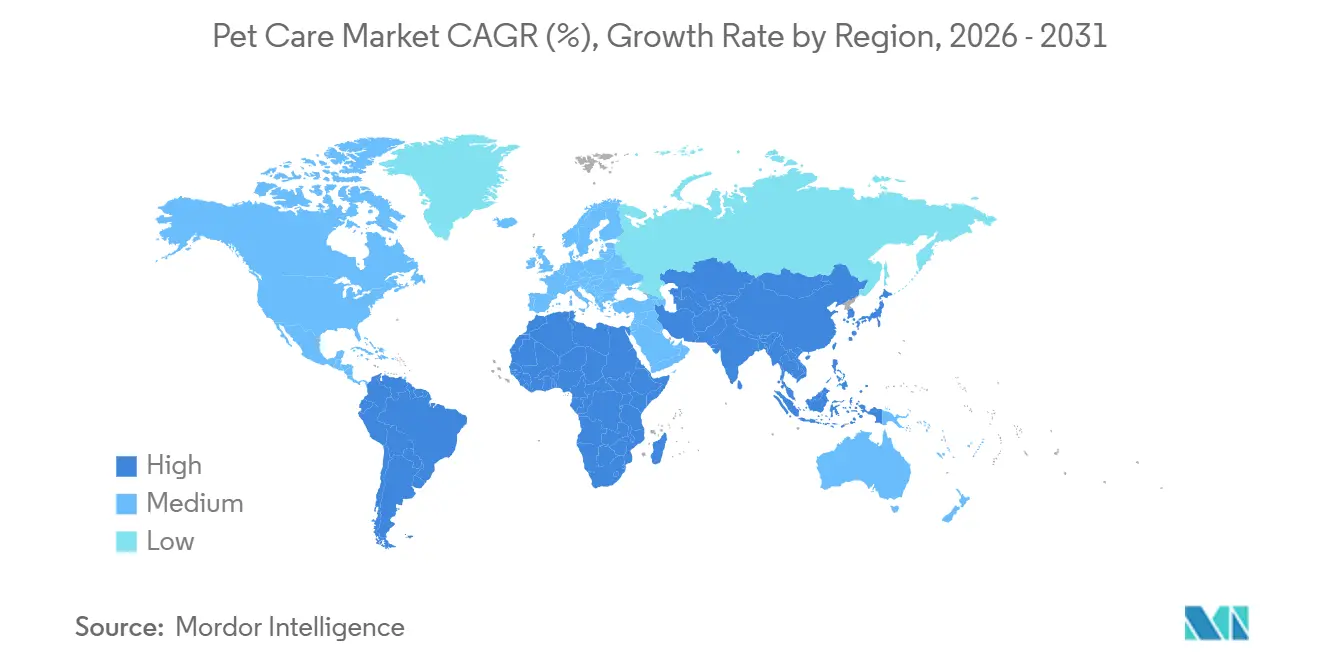

- By geography, North America accounted for 39% of global revenue in 2025, and the Asia-Pacific region is projected to rise at a 9.6% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization of pets fueling premiumization | +1.80% | Global, highest in North America and Western Europe | Medium term (2-4 years) |

| Rising pet adoption among millennials and Generation Z | +1.50% | Urban centers worldwide | Short term (≤ 2 years) |

| Growth of online pet product retail | +1.30% | Global, especially North America and China | Short term (≤ 2 years) |

| Increasing spend on preventive veterinary care and insurance | +0.90% | North America and Europe core | Medium term (2-4 years) |

| Rapid urbanization of secondary Asian cities | +0.80% | Asia-Pacific core | Long term (≥ 4 years) |

| Integration of functional ingredients into food lines | +0.60% | North America and Europe lead | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Humanization of Pets Fueling Premiumization

Owners regard animals as family, so they willingly pay premiums for grain-free recipes, fresh meals, and wellness supplements. Freshpet’s refrigerated range grew 27.2% year-over-year to USD 975.2 million in 2024, proving strong price elasticity for minimally processed products. In Western markets, the trend extends to grooming, apparel, and pet-friendly travel, widening revenue pools for retailers and service providers. Cross-category willingness to spend depends on stable labor markets, recessions historically cause trading down to value tiers. Nonetheless, premium SKUs continue to outgrow mainstream alternatives, anchoring long-term value creation in the pet care market.

Rising Pet Adoption Among Millennials and Generation Z

Generation Z households reached 18.8 million in 2024, representing a 43.5% increase from the previous year, and 70% of these homes contained two or more pets in the United States[1]Source: Association of American Feed Control Officials, “Model Regulations for Pet Food,” aafco.org. Digital natives favor transparent sourcing, carbon-neutral packaging, and auto-ship subscriptions, prompting brands to adopt omnichannel ecosystems. Chewy’s 20.3 million active customers and 75% auto-ship mix validate the model’s lock-in economics[2]Source: Chewy, “2024 Annual Report,” investor.chewy.com. In Asia, delayed family formation is redirecting discretionary income toward companion animals, strengthening the demographic factors driving growth in the pet care market.

Increasing Spend on Preventive Veterinary Care and Insurance

Gross written premiums (GWP) reached USD 4.7 billion in 2024, representing an annual increase of 21.4%, yet penetration was only 3.9% of the eligible pets in the United States [3]Source: Chewy, “2024 Annual Report,” investor.chewy.com. Average veterinary outlays per dog reached USD 598 and per cat USD 529, driven by routine diagnostics and the management of chronic diseases [4]Source: North American Pet Health Insurance Association, “2024 State of the Industry,” naphia.org. Zoetis Services LLC and Elanco Animal Health Inc. are rolling out broader vaccine and parasiticide portfolios, while insurers highlight flexible deductible options to attract first-time buyers. With Sweden’s 40% penetration serving as a benchmark, insurers see a large upside in North America and Asia as awareness improves.

Rapid Urbanization of Secondary Asian Cities

China’s cat population climbed to 62.3 million in 2023, exceeding its dog count for the first time, driven by apartment constraints that favor smaller species. Japan exhibits a similar pattern, with 9.1 million cats compared to 6.8 million dogs in 2023. Manufacturers such as Unicharm are expanding their litter and feline-specific nutrition lines to capitalize on the trend. Smaller pets generate lower tickets per purchase but expand the consumer base, giving the pet care market fresh volume momentum.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices for meat and grains | -0.9% | Global, most acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent regulations on labeling and claims | -0.5% | North America and Europe core | Medium term (2-4 years) |

| Counterfeit and low-quality products online | -0.4% | Global, and highest where enforcement is weak | Short term (≤ 2 years) |

| Limited cold-chain infrastructure in emerging markets | -0.3% | Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices for Meat and Grains

Chicken, beef, corn, and wheat account for up to 70% of production cost. Price spikes in 2022–2024 squeezed margins as many brands lacked hedging capacity. Large players offset volatility through vertical integration, but mid-tier firms either reformulated or absorbed losses, risking consumer backlash or cash-flow strain. Geopolitical events, such as export bans and avian flu outbreaks, perpetuate uncertainty, hindering long-term capital expenditures in the pet care market.

Stringent Regulations on Labeling and Claims

Food and Drug Administration (FDA) rules require descending weight ingredient lists, guaranteed analyses, and substantiated nutritional adequacy, while the European Union (EU) Regulation 767/2009 adds traceability mandates. Enforcement actions surrounding grain-free diets demonstrate a rising level of scrutiny, extending product development cycles, and increasing compliance costs. Smaller brands without dedicated regulatory teams face disproportionate burdens.

Segment Analysis

By Product Type: Services Outpace Food Growth

Pet Food dominated the pet care market with a 43% market share in 2025, anchored by dry kibble’s affordability and shelf stability. However, Pet Services' grooming, boarding, daycare, and training are projected to post a robust 10% CAGR to 2031 as busy urban owners treat professional care as a non-negotiable line item. Higher labor inputs and lower price sensitivity grant services the richest margins in the pet care industry. Healthcare is another bright spot, buoyed by growing awareness of preventive care and insurance reimbursements. Dry kibble remains the volume engine, yet fresh and refrigerated SKUs, although constrained by cold-chain gaps, are growing multiples faster. Combined, these dynamics ensure that the pet care market size will tilt progressively toward higher-value offerings over the forecast horizon.

The expansion of services is reshaping competitive strategy. Incumbents utilize loyalty programs and bundled wellness packages to foster customer loyalty, while start-ups leverage technology to offer app-based booking and real-time pet monitoring. The profit pool is attracting non-traditional players such as hotels that retrofit unused space into daycare suites. In the food industry, functional claims for digestive health, joint support, and anxiety relief differentiate premium lines, while Association of American Feed Control Officials (AAFCO) guidance on ingredients such as probiotics sharpens the competitive field. Treats and supplements leverage parallels with human wellness trends, enabling price premiums that reduce the volume disparity with staple pet food. Product-type segmentation reveals a dual opportunity where brands need to maintain their scale in commodity categories while creating value in service-oriented and functional niches to enhance their share of the pet care market.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Cats Gain on Dogs

Dogs accounted for 46% of the pet care market size in 2025, however, cats are forecast to grow at an 8.4% CAGR through 2031, driven by urban households seeking low-maintenance companions. Emerging Asian cities are at the epicenter, where apartment size, noise restrictions, and dual-income lifestyles favor felines. Cat owners are upgrading to odor-control litter, urinary-health diets, and subscription toy boxes, expanding the pet care market size for feline-specific products. Birds, fish, small mammals, and reptiles remain niche but benefit from space constraints and the desire for unique home aesthetics. Each species carries distinct accessory needs, including filters, heaters, habitats, and specialized margin streams for retailers.

Dogs still account for high-ticket spending because food, professional training, and boarding days eclipse feline outlays. Nevertheless, discerning cat owners pay premiums on a per-pound basis for vet-authorized diets. Fish enjoy popularity in offices for their calming effect, supporting a long tail of consumables such as water conditioners and decorative aquascapes. Small mammals appeal to first-time parents, teaching responsibility, while reptiles anchor enthusiast communities that spend heavily on habitat technology. This widening species spread diversifies revenue beyond traditional dog-centric categories, ensuring the pet care market maintains balanced growth even if any single animal category experiences a slowdown.

By Distribution Channel: Online Gains Share

Offline Retail retained a 71% share in 2025, driven by pet specialty stores, veterinary clinics, and mass merchants that offered tactile product sampling and expert advice. Yet, Online Retail is projected to record an 11.8% CAGR through 2031, increasing its share of the pet care market as subscription convenience and personalized algorithms lock in repeat orders. Chewy’s auto-ship penetration at 75% of 2024 revenue exemplifies sticky e-commerce economics. Physical stores are fighting back with buy-online-pick-up-in-store options, same-day local delivery, and in-store experiences such as self-service dog washes. Veterinary clinics enjoy quasi-regulated moats by dispensing prescription food and medicines that require professional authorization, thereby protecting a stable, if specialized, profit pool.

Counterfeits and delivery damages continue to be challenges for pure-play e-commerce. However, serialization and blockchain tools are showing progress in addressing these issues. Geographic differences play a significant role. North America and Western Europe benefit from well-established last-mile networks, facilitating faster online adoption. In contrast, emerging regions rely more on brick-and-mortar models due to underdeveloped logistics and digital payment systems. Supermarket chains leverage loyalty fuel points and cross-category promotions to retain pet care purchases within weekly grocery trips, particularly appealing to value-conscious consumers. Ultimately, an omnichannel approach is projected to shape distribution, with each channel serving distinct shopper needs, driving sustained growth in the pet care market regardless of channel preference.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 39% of the pet care market size in 2025. The prevalence of premium fresh meals, comprehensive insurance plans, and on-demand services contributes to steady growth in consumer spending. The United States leads in the early adoption of veterinary telemedicine, while Canada’s bilingual labeling requirements introduce minor compliance costs without creating significant structural barriers. The region also boasts the highest online penetration, driven by advanced logistics systems and strong consumer confidence.

The Asia-Pacific region, projected to grow at a 9.6% CAGR through 2031, is the fastest-growing territory in the pet care market. China’s apartment culture, India’s rising middle class, and Southeast Asia’s urbanization collectively build a vast new consumer base. Cold-chain gaps hinder the distribution of refrigerated products, yet dry and wet formats continue to flourish, alongside the expansion of grooming and hospital chains into secondary cities. Japan, South Korea, and Australia showcase mature spending per pet, emphasizing wellness and functional diets. Momentum hinges on continued infrastructure investments to unlock premium-product tiers.

Europe is anticipated to grow steadily, driven by Germany, France, and the United Kingdom. In these countries, factors such as sustainability, traceability, and ingredient transparency are prompting consumers to opt for premium pet care products. Meanwhile, Southern Europe remains more value-focused but is gradually aligning with the broader market as income levels improve. However, strict labeling and regulatory requirements, while fostering consumer trust, tend to slow the introduction of new innovations. South America and Africa are projected to exhibit relatively faster growth. In South America, rising urban pet adoption in countries like Brazil and Argentina supports market expansion despite economic volatility. In Africa, emerging demand in markets such as South Africa and Egypt is bolstered by increasing awareness and the growth of e-commerce in major cities. These factors contribute to long-term pet care market growth, despite challenges related to infrastructure and affordability.

Note: Segment share of all individual segments available upon report purchase

Competitive Landscape

The pet care market is moderately concentrated, with Mars, Incorporated, Nestlé S.A. (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), The J. M. Smucker Company, and Spectrum Brands, Inc. collectively accounting for the majority of the market size in 2025. Leading companies, such as Mars, Incorporated, and Nestlé S.A., are expanding vertically into veterinary services and fresh food manufacturing to access higher-margin revenue streams beyond traditional dry pet food. Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) maintains a strong competitive position in therapeutic diets, supported by extensive veterinarian endorsement networks that are challenging for mass-market brands to replicate. Mid-sized competitors rely on brand heritage and retail visibility but face growing pressure to enhance their digital and direct-to-consumer capabilities.

Innovation opportunities are increasingly focused on functional nutrition, condition-specific diets, and personalized meal plans delivered directly to consumers. Freshpet Inc. has demonstrated the potential of refrigerated and fresh formats to command premium pricing without depending on traditional wholesale channels. In response, established players are accelerating acquisitions, partnerships, and investments in fresh and functional nutrition, leveraging their regulatory expertise as a defensive advantage within complex approval frameworks.

Barriers to entry remain significant due to high raw material sourcing costs, retail slotting fees, and increasing digital marketing expenses. However, niche segments such as aquatic care, functional supplements, and environmentally friendly pet products present opportunities for differentiated growth. Overall, competition is increasingly divided between scale-driven multinational corporations and specialized value-added players. Success in the market depends on omnichannel reach, ingredient transparency, and clinically supported product positioning.

Pet Care Industry Leaders

Mars, Incorporated

Nestle S.A.(Purina)

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

The J. M. Smucker Company

Spectrum Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mars, Incorporated has introduced AI-powered pet health tools, including the GREENIES Canine Dental Check, which utilizes image analysis to aid in the early detection of dental issues. This initiative underscores the role of artificial intelligence in enhancing preventive care, personalization, and digital engagement within the pet care market.

- December 2024: General Mills, Inc. completed the USD 1.45 billion acquisition of Whitebridge Pet Brands’ North American premium cat feeding and pet treats business, enhancing its position in high-value pet care segments.

- January 2024: Ÿnsect obtained approval from the United States Association of American Feed Control Officials (AAFCO) for dried mealworm meal, marking the first insect-protein clearance for pet food in the United States. This development is projected to enhance market competition and drive innovation in insect-based pet food products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the pet care market as all revenue generated from products and services that keep companion animals fed, healthy, groomed, entertained, and insured. This includes packaged food, treats, veterinary medicines, routine veterinary services, grooming and hygiene products, training and boarding services, smart accessories, and pet insurance sold across physical and digital channels worldwide.

Scope Exclusions: livestock feed, equine sports nutrition, and laboratory-animal supplies remain outside this boundary.

Segmentation Overview

- By Product Type

- Pet Food

- Pet Healthcare

- Pet Grooming Products

- Pet Accessories

- Pet Services

- By Animal Type

- Dogs

- Cats

- Other Pets

- By Distribution Channel

- Offline Retail

- Supermarkets and Hypermarkets

- Pet Specialty Stores

- Veterinary Clinics

- Online Retail

- Offline Retail

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed veterinarians, specialty retailers, online subscription platforms, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. The conversations tested adoption curves for premium food, tele-health uptake, and average service tickets, which helped us validate secondary numbers and fine-tune model assumptions.

Desk Research

We first gathered baseline figures from public sources such as the American Pet Products Association expenditure survey, USDA animal ownership files, FEDIAF pet population dashboards, Eurostat household spend data, and Japan Pet Food Association statistics, complemented by news archives in Dow Jones Factiva and company 10-K filings. These provided pet population counts, spend per pet, channel splits, and cost indices that anchor the demand pool. D&B Hoovers supplied revenue breakouts that guided price tiers and category shares. The sources listed illustrate our approach and are not exhaustive; many additional datasets were reviewed to confirm trends and fill gaps.

Market-Sizing & Forecasting

A top-down construct converts country pet populations into spend pools through average outlay per dog, cat, fish, or small mammal, which are then reconciled with supplier roll-ups and sampled online ASP × volume checks before finalizing totals. Key variables include pet adoption rates, disposable income per capita, inflation-adjusted product prices, veterinary cost index, and e-commerce share of specialty pet goods. Five-year forecasts rely on exponential smoothing supported by multivariate regression for price and population drivers that our expert panel endorsed. Where channel data were incomplete, sampled retailer panels bridged the gap.

Data Validation & Update Cycle

Outputs move through variance scans against historical spend curves, peer benchmarks, and currency checks, followed by senior analyst review. We refresh every twelve months and trigger interim reruns when mergers, disease outbreaks, or regulatory shifts materially alter demand.

Why Mordor's Pet Care Baseline Earns Trust

Published figures differ because firms pick varied product mixes, channels, and update cadences.

Our disciplined scope, iterative cross-checks, and annual refresh give decision-makers a stable yet timely anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 380 B (2025) | Mordor Intelligence | - |

| USD 273.42 B (2025) | Global Consultancy A | Omits grooming devices and most insurance lines and applies slower premiumization growth |

| USD 200 B (2024) | Trade Journal B | Captures only retail food and accessories, excludes veterinary and services revenue |

| USD 159.1 B (2022) | Industry Association C | Early base year and limited country set with no online channel inflation adjustment |

These contrasts show that when scope narrows or price updates lag, totals swing widely. By capturing the full commercial chain and re-validating every year, Mordor Intelligence delivers a balanced, transparent baseline that planners can replicate and defend.

Key Questions Answered in the Report

How big is the pet care market in 2026?

The pet care market size reached USD 280 billion in 2026, setting the base for a 7.1% CAGR through 2031.

Which product category is growing fastest?

Pet Services show the strongest trajectory with a projected 10% CAGR, supported by grooming, boarding, and daycare demand.

What animal type is gaining share most rapidly?

Cats are advancing at an 8.4% CAGR as urban owners in Asia and younger United States demographics favor lower-maintenance companions.

How quickly is online pet retail expanding?

Online Retail is forecast to grow at 11.8% CAGR, far outpacing offline channels thanks to subscription and same-day delivery perks.

Which region will add the most new spending?

Asia-Pacific, set for a 9.6% CAGR, will add the largest incremental dollars as middle-income households embrace pet ownership.