Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

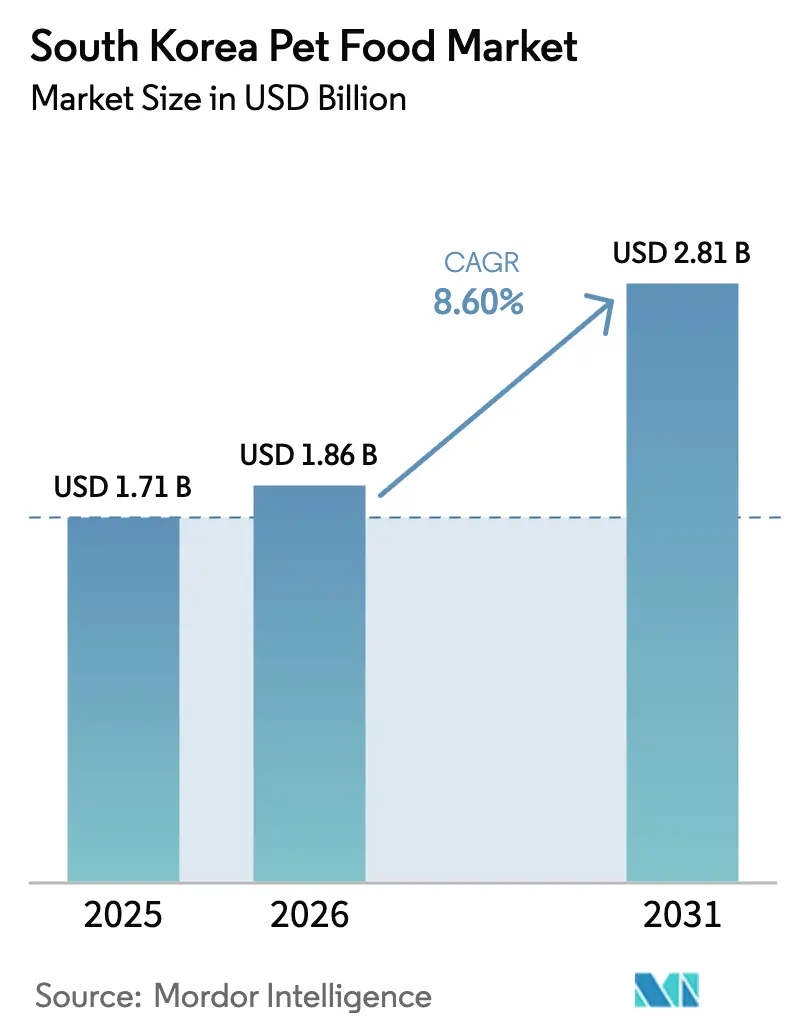

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Pet Food Market Analysis by Mordor Intelligence

The South Korea pet food market size is projected to expand from USD 1.71 billion in 2025 and USD 1.86 billion in 2026 to USD 2.81 billion by 2031, registering a CAGR of 8.6% between 2026 to 2031. This expansion reflects profound changes in household structures, especially the rise of single-person households that now represent more than 30% of the population and increasingly treat pets as family members rather than accessories. The parliamentary ban on dog-meat consumption, with the full ban coming into effect in February 2027, has removed a cultural barrier and is estimated to boost dog ownership, while apartment-dwelling millennials are driving cat adoption, leading to the fastest growth in feline ownership. Premiumization and functional nutrition are expanding margins as owners prioritize gut health, joint care, and human-grade ingredients. At the same time, rapid e-commerce adoption, supported by same-day delivery in more than 80% of Seoul, is redistributing value away from hypermarkets toward digital channels. Global incumbents are defending share through veterinary-clinic partnerships, but domestic challengers leverage vertical poultry integration to compete on price and trust, signaling a two-tier market split between cost-focused dry kibble and high-margin functional formats.

Key Report Takeaways

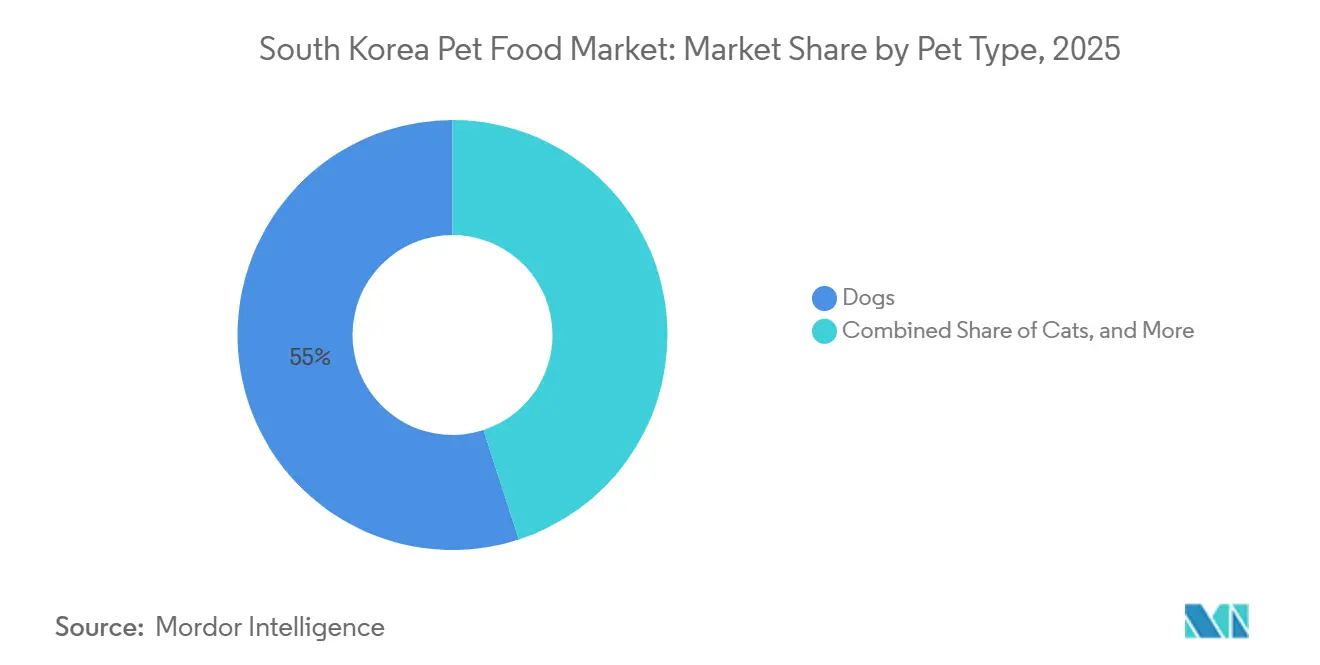

- By pet type, dogs led with 55% of South Korea's pet food market share in 2025, while cats are advancing at a 9.9% CAGR through 2031.

- By product type, dry pet foods captured 52.5% of the South Korean pet food market size in 2025, treats and snacks are expanding at a 12.1% CAGR through 2031.

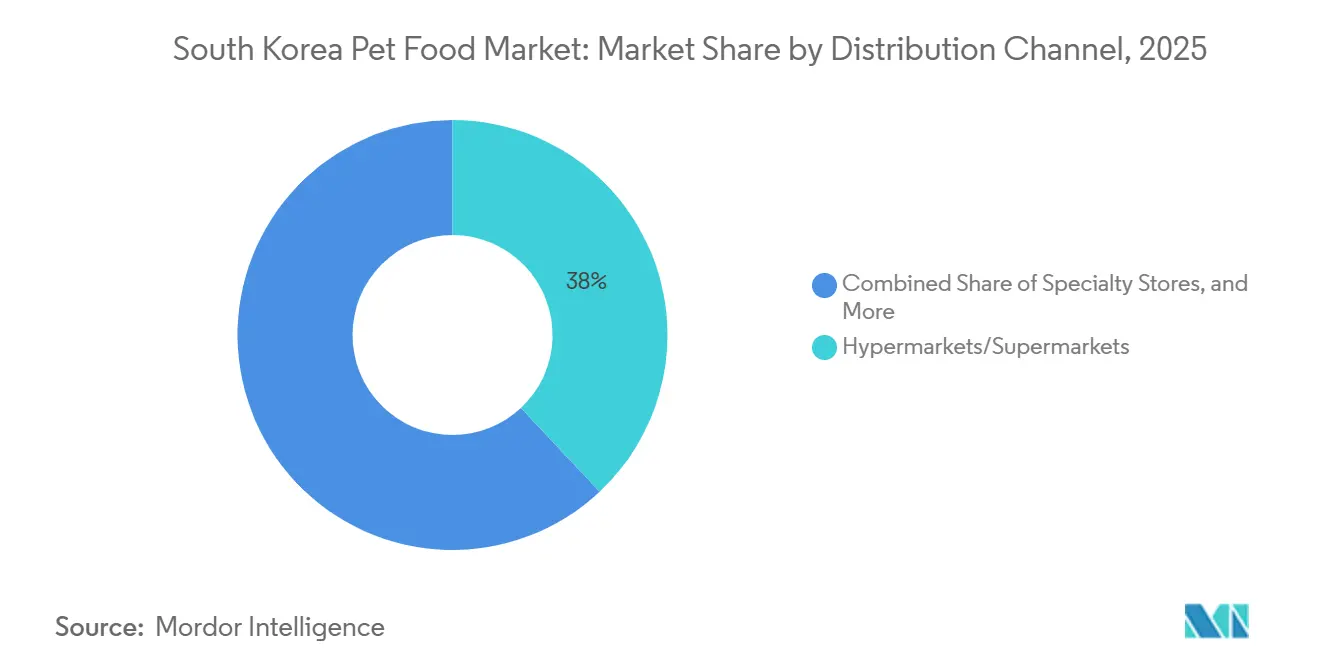

- By distribution channel, hypermarkets and supermarkets held 38% share of the South Korea pet food market size in 2025, whereas online channels are growing at a 17.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pet ownership and pet humanization | +1.50% | National, concentrated in Seoul, Busan, and Incheon | Medium term (2-4 years) |

| Premium and functional nutrition demand surge | +1.80% | National, early adoption in Seoul and Gyeonggi Province | Short term (≤ 2 years) |

| Rapid e-commerce and last-mile delivery expansion | +1.40% | National, Seoul metro coverage >80% | Short term (≤ 2 years) |

| Government ban on dog-meat spurring dog adoptions | +0.90% | National, stronger shift in urban centers | Long term (≥ 4 years) |

| Commercialization of insect-protein supply chain | +0.70% | National, pilot farms in Gyeongsangbuk-do | Medium term (2-4 years) |

| AI-driven personalized diet platforms adoption | +0.60% | National, Seoul and Gyeonggi early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Pet Ownership and Pet Humanization

Single-person households exceeded 30% and are driving a ‘fur-baby’ culture in which pets enjoy birthday parties, premium grooming, and even insurance policies. A significant share of the population keeps pets and allocates a notable portion of monthly household spending to their care[1]Source: KB Financial Group, “Korean Pet Report 2023,” kbfg.com. Rising cat ownership is particularly noticeable among apartment dwellers who prefer lower-maintenance companions. Government statistics anticipate a strong expansion in pet food sales over the coming years. Together, these factors cement consistent volume growth for the South Korea pet food market. Consumers are increasingly seeking brands that adhere to human-grade ingredient standards, reinforcing the trend of premiumization. As household sizes continue to shrink, per-pet spending is estimated to increase, thereby deepening the market’s revenue pool. Consequently, manufacturers that embed emotional and lifestyle narratives into product marketing are winning market share.

Premium and Functional Nutrition Demand Surge

Functional formats that address joint health, digestive wellness, and senior vitality sold at premiums of more than 30% over standard kibble, yet velocity remained robust. Hill’s Pet Nutrition’s ActivBiome+ range, distributed mainly through veterinary clinics, has become a staple for digestive and immune support. Harim Pet Food’s The Real line, which excludes synthetic preservatives and uses human-grade inputs, achieved strong sales performance and a 6.0% operating margin. Owners accept higher prices, fearing that switching brands may upset pets’ digestion, which reduces price sensitivity and supports margin expansion. South Korea pet food market stakeholders are therefore channeling R&D funds toward science-backed claims that justify sustained premiums. This demand dynamic also incentivizes new ingredient innovations, including probiotics and post-biotics, that can be patented to secure differentiation. Premiumization ultimately widens the revenue gap between functional SKUs and commoditized kibble.

Rapid E-Commerce and Last-Mile Delivery Expansion

Online channels are expanding at a faster rate than brick-and-mortar, supported by same-day delivery networks that now cover a significant share of Seoul. Subscription models, pioneered by Dongwon F&B’s Nutri Plan, lock in predictable recurring revenue. Cargill’s large Pyeongtaek facility supports rapid fulfillment for both retail and digital orders, ensuring products remain in stock during peak promotions. Influencer marketing on Naver and Kakao simplifies product discovery and accelerates category penetration. Logistics providers are extending same-day reach to secondary cities, widening nationwide access to imported and premium brands. Data analytics from online transactions allow precise targeting, helping startups scale quickly with minimal marketing spend. Taken together, e-commerce infrastructure is a powerful catalyst for South Korea’s pet food market growth.

Commercialization of Insect-Protein Supply Chain

Pilot-scale black-soldier-fly farms in Gyeongsangbuk-do achieved sufficient output to appear in hypoallergenic kibble. Insect meal offers a 90% smaller carbon footprint than conventional meat proteins, aligning with rising environmental consciousness. Cargill entered a joint venture to secure proprietary supply, signaling serious industrial commitment. Regulatory approval of insect ingredients resolved prior uncertainty and enabled commercialization. European brands already include insect meal at up to 15% inclusion rates[2]Source: International Platform of Insects for Food and Feed, "Edible Insects on the European Market: Market Factsheet", ipiff.org, offering a roadmap that South Korean firms are increasingly following. Early adopters enjoy first-mover advantage in exports to Japan and China, markets that monitor Korean innovations closely. Sourcing insect protein domestically also reduces foreign-exchange risk, an added benefit amid currency volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependence and foreign-exchange-linked cost volatility | -1.20% | National, importers sourcing USD-denominated ingredients | Short term (≤ 2 years) |

| Complex labeling compliance regime | -0.80% | National, Ministry of Food and Drug Safety jurisdiction | Medium term (2-4 years) |

| Trust crisis following cat-food toxicity cases | -0.60% | National, concentrated in wet-food segment | Short term (≤ 2 years) |

| Nutrient-deficiency risk in fresh diets | -0.40% | National, urban centers with higher fresh-diet adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Dependence and Foreign-Exchange-Linked Cost Volatility

Functional ingredients are largely dollar-denominated, leaving manufacturers exposed when the won weakens. The currency experienced a notable decline against the dollar, forcing difficult choices between absorbing costs and raising retail prices during a period of elevated inflation. Some manufacturers partially offset pressure through domestic poultry integration, but brands reliant on imported salmon oil, glucosamine, and probiotics felt the squeeze. Pet-specific inflation ran at roughly double the national consumer index, yet demand proved sticky because owners fear negative health outcomes if they down-trade. Persistent currency swings delay new product launches that rely on specialty imports and favor domestically sourcing firms, narrowing supplier options and curbing the pace of innovation across the South Korea pet food market.

Complex Labeling Compliance Regime

The Ministry of Food and Drug Safety updated regulations, mandating allergen panels, origin statements, and batch traceability codes. Small and medium enterprises now face additional legal review and design work before products can reach store shelves. Penalties for non-compliance represent a material burden for new entrants. While consumers appreciate stronger labeling following contamination incidents, the added rigor raises barriers to entry and discourages smaller importers. Domestic players with established regulatory teams navigate the system more efficiently, gaining a relative advantage. Over-disclosure has become prevalent as companies prioritize compliance, leading to packaging filled with information that may confuse consumers. In aggregate, compliance costs weigh on the South Korea pet food market, particularly for innovative, smaller brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Cats Narrow the Gap

Dogs commanded 55% of the South Korea pet food market size in 2025, followed by cats, while small mammals and birds shared the remaining portion of the market. The ranking reflects historical dog ownership and mature product portfolios that cater to different life stages. Cat food, however, is closing in quickly as millennials and Gen Z apartment dwellers appreciate low-maintenance felines. Other pets, including rabbits and hamsters, remain minor due to limited SKUs and low per-pet spending.

Cats are growing at a 9.9% CAGR through 2031, the fastest among all pet types, while dogs and other pets are projected at lower rates. The parliamentary dog-meat ban supports steady dog gains, yet saturation in urban ownership tempers upside. Small-pet categories exhibit stable but modest growth, reflecting limited marketing attention and shelf space. These differing trajectories illustrate why manufacturers diversify across species while prioritizing feline innovations to capture incremental volume and value.

By Product Type: Treats Outpace Core Nutrition

Dry foods led with 52.5% of South Korea's pet food market share in 2025, followed by treats, wet foods, veterinary diets, and various other specialty products. Dry kibble remains dominant due to shelf stability and cost efficiency, but treats and snacks exhibit outsized momentum driven by functional claims. Wet foods lag after the toxicity shock, while prescription diets hold a defensible share via clinic channels.

Treats and snacks are expanding at a 12.1% CAGR, ahead of veterinary diets, dry foods, wet foods, and other formats. Functional treat innovation, such as Harim’s lactose-free frozen dog ice cream, accelerates category velocity. Prescription diets benefit from rising chronic conditions in aging pets. In contrast, wet food’s recovery depends on sustained transparency efforts, and commoditized dry kibble faces mounting price competition, narrowing margins.

By Distribution Channel: Online Gains Accelerate

Hypermarkets and supermarkets took 38% of 2025 sales, followed by specialty stores, online channels, and other outlets. Physical big-box stores appeal to shoppers who value in-person label inspection and instant gratification. Specialty retailers and vet clinics maintain authority in therapeutic and premium segments.

Online channels are posting the fastest 17.3% CAGR, followed by specialty stores, hypermarkets, and other outlets. Same-day delivery and data-driven personalization underpin e-commerce momentum. Specialty stores sustain relevance through consultative selling, yet some traffic migrates online. Hypermarkets retain bulk-purchase shoppers but must renovate pet aisles to remain competitive. Overall, channel diversification continues to reshape revenue streams across the South Korea pet food market size landscape.

Geography Analysis

Sales are heavily concentrated in Seoul, Gyeonggi Province, and Busan, collectively accounting for the majority of national revenue. Higher disposable income, dense vet networks, and ample specialty retailers drive this clustering. Single-person households flourish in these areas, propelling premium cat and small-dog ownership. Rural provinces rely on hypermarkets and agricultural cooperatives, hampering access to imported or niche products and keeping the value tier prominent.

E-commerce coverage provides extensive same-day reach in Seoul but is significantly lower in Daegu and Gwangju in 2025. Logistics investments aim to narrow this gap by 2028, yet economics favor dense urban areas first. Cultural acceptance of the dog-meat ban (effective February 2027) is strongest in cities, where dog adoptions spike, while rural regions transition more slowly. The geographic split guides marketing spend, with brands tailoring urban campaigns to premium SKUs and rural campaigns to value formats.

Ingredient sourcing clusters around Jeollabuk-do and Gyeongsangbuk-do, where Harim and CJ CheilJedang operate vertically integrated plants. Insect-protein farms in Gyeongsangbuk-do benefit from provincial subsidies, positioning the region as a sustainability hub. Meanwhile, AI-driven subscription services gain traction in Seoul, leveraging 95% smartphone penetration, before rolling out to secondary markets. Overall, regional disparities in income, logistics, and culture create a mosaic of opportunities and challenges across the South Korea pet food market.

Competitive Landscape

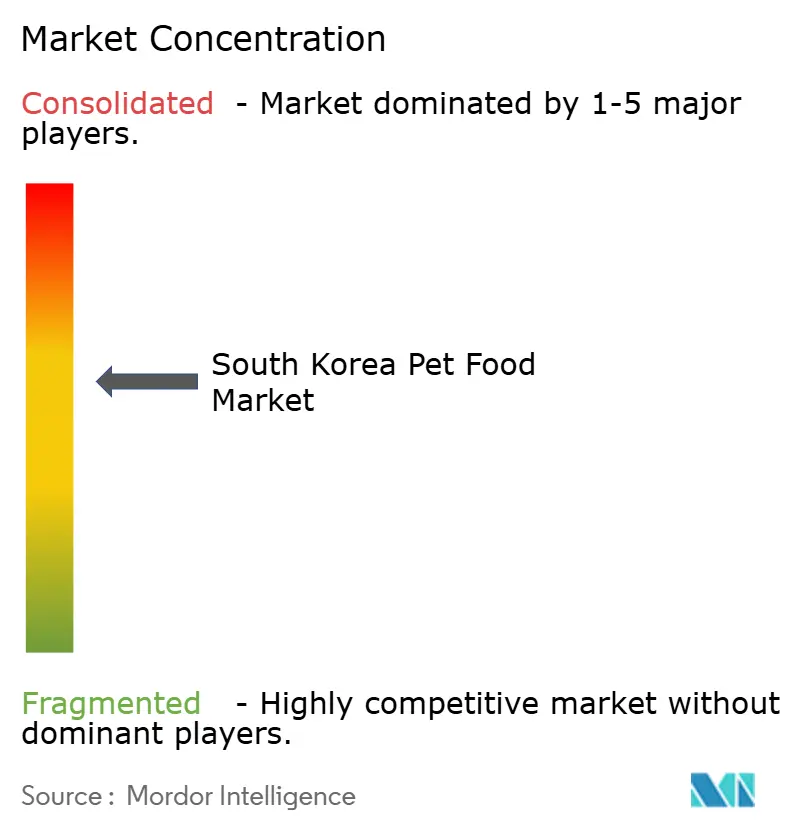

The top five vendors controlled a substantial share of market revenue, resulting in a moderate level of market concentration. Mars, Incorporated and Nestle (Purina) jointly hold a significant portion of the market, leveraging global research capabilities and veterinary partnerships to defend share. Domestic firms such as CJ CheilJedang Corporation and Harim Group (Jeil Feed) leverage local poultry integration to offer competitive pricing without sacrificing quality. Harim’s margins improved after eliminating synthetic preservatives and emphasizing human-grade inputs[3]Source: Harim Holdings Co., Ltd, “Financial Information”, harimholdings.com.

White-space segments include functional cat treats and insect-protein kibble, where first movers can command 30-40% premiums. Digital-native startups bypass retail gatekeepers via AI-based meal subscriptions, potentially eroding incumbent share. Hill’s Pet Nutrition expanded its vet-clinic footprint significantly in 2025, reinforcing professional endorsement loops that secure loyalty at higher price points. As the South Korea pet food market bifurcates, scale and cost leadership underpin the value tier, whereas speed in innovation and digital engagement dictate success in premium niches.

Strategic moves underline intensifying rivalry. CJ CheilJedang increased cat-specific SKUs by 20% in 2025, while Harim launched experiential pop-up stores to promote frozen treats. Cargill’s insect-protein joint venture signals upstream investment to secure sustainable differentiation. The result is a dynamic landscape where global giants, vertically integrated locals, and agile startups all contest share.

South Korea Pet Food Industry Leaders

-

Mars, Incorporated

-

Nestle (Purina)

-

Unicharm Corporation

-

CJ CheilJedang Corporation

-

Colgate-Palmolive (Hill's Pet Nutrition, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: H&H Group has officially launched its pet supplement brand, Zesty Paws, in South Korea. The products are now available on major online platforms, including Coupang, Naver, Cafe24, and Bite Me, and will gradually be introduced at select offline locations such as grooming salons and training centers.

- March 2025: Nestle (Purina) launched independent pet food operations in South Korea, transitioning away from its joint venture with Lotte Wellfood to establish direct market presence through Purina PetCare, signaling increased commitment to the Korean market despite challenging competitive dynamics.

- July 2024: Harim Pet Food opened a The Real Ice Cream pop-up at Starfield Hanam, offering lactose-free frozen dog treats positioned as 100% human-grade.

- July 2024: Kormotech has become the first company from Ukraine to export pet food to South Korea. Kormotech’s super-premium dog and cat food brand, Optimeal, and the premium brand, Club 4 Paws, are now available on specialized online platforms in South Korea.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea pet food market as all commercially packaged feed and treats formulated for dogs, cats, and other companion animals, measured in retail value at point of sale. It embraces dry kibble, wet or canned meals, veterinary diets, and snack formats sold through online and offline channels.

Scope exclusion: livestock feed, pet supplements sold as pharmaceuticals, and unprocessed raw meat purchased directly from butchers are outside this scope.

Segmentation Overview

-

By Pet Type

- Dogs

- Cats

- Other Pets

-

By Product Type

- Dry Pet Foods

- Wet Pet Foods

- Veterinary Diets

- Treats and Snacks

- Other Product Types

-

By Distribution Channel

- Hypermarkets/Supermarkets

- Specialty Stores

- Online Channels

- Others Distribution Channels

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed nutritionists, veterinary clinicians, online marketplace managers, and store buyers across Seoul, Busan, and four second-tier cities. These discussions helped us verify average selling prices, brand mix shifts, and emerging functional claims, which we then contrasted with survey responses from urban pet owners on purchase frequency and channel preference.

Desk Research

We begin with published data sets from the Ministry of Agriculture, Food and Rural Affairs, Korea Customs Service import-export records, Statistics Korea household expenditure tables, and trade association newsletters such as the Korea Pet Food Association. Those sources anchor pet population trends, spending per pet, and shipment volumes. Additional context is taken from peer-reviewed veterinary journals, investor filings, reputable business press, and paid databases like D&B Hoovers and Dow Jones Factiva that clarify company revenues and retail footprints. The sources mentioned illustrate the range consulted; many further documents supported fact-checking and gap filling.

Market-Sizing & Forecasting

A top-down model starts with national pet population and average calorie demand, which are then married to import receipts, retail scanner sales, and e-commerce order volumes to estimate 2024 consumption. Selective bottom-up checks, such as leading suppliers' revenue roll-ups and channel audits, fine-tune totals. Key variables include dog-to-cat ownership ratio, premium price index, import duty changes, online penetration, and veterinarian clinic visit rates because they directly sway spending. Forecasts use multivariate regression backed by expert consensus to project how these drivers evolve under baseline, optimistic, and cautious scenarios. Where data gaps appear, we interpolate using three-year moving averages that are later validated against primary feedback.

Data Validation & Update Cycle

Before sign-off, senior analysts run variance screens, compare output with external shipment dashboards, and reconfirm any swings with at least one primary contact. The model is refreshed annually and revisited mid-cycle if policy shocks or disease outbreaks materially affect pet numbers.

Why Mordor's South Korea Pet Food Baseline Commands Confidence

Published estimates often differ because firms choose dissimilar product scopes, pricing bases, and refresh cadences. Our disciplined selection of variables and yearly recalibration minimize those gaps for decision-makers.

Key gap drivers typically arise when other publishers bundle supplements, apply factory gate prices, or project growth from pre-pandemic trend lines without testing post-COVID channel shifts, whereas Mordor adjusts for import substitution and real retail prices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.71 bn (2025) | Mordor Intelligence | - |

| USD 1.15 bn (2022) | Global Consultancy A | excludes e-commerce surge, uses factory-gate values |

| USD 1.51 bn (2023) | Trade Data Provider B | retail only, omits veterinary diets |

| USD 2.50 bn (2024) | Regional Consultancy C | adds supplements and grooming products |

Taken together, the comparison shows that when scope creep or outdated baselines are removed, Mordor's balanced, transparent model delivers a reliable reference grounded in verifiable Korean market fingerprints.

Key Questions Answered in the Report

What is the current value of the South Korea pet food market?

The South Korea pet food market size is USD 1.86 billion in 2026.

How fast is the market growing?

The market is forecast to expand at an 8.6% CAGR, reaching USD 2.81 billion by 2031.

Which pet type is growing the quickest?

Cat food is advancing at a 9.9% CAGR through 2031, outpacing all other segments.

Which product category is expanding fastest?

Treats and snacks lead with a 12.1% CAGR due to functional and indulgent innovations.

What channel is gaining share most rapidly?

Online platforms are growing at a 17.3% CAGR, driven by same-day delivery and subscriptions.

Page last updated on: