Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

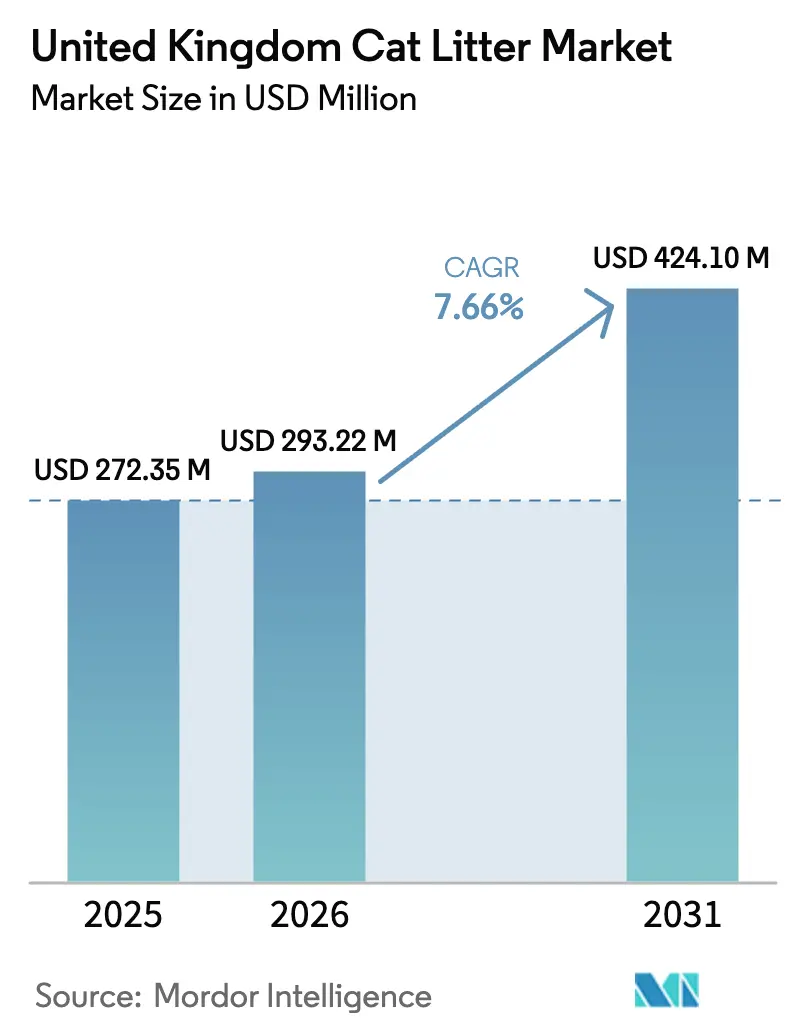

| Base Year Market Size (2025) | USD 272.35 Million |

| Market Size (2026) | USD 293.22 Million |

| Market Size (2031) | USD 424.1 Million |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

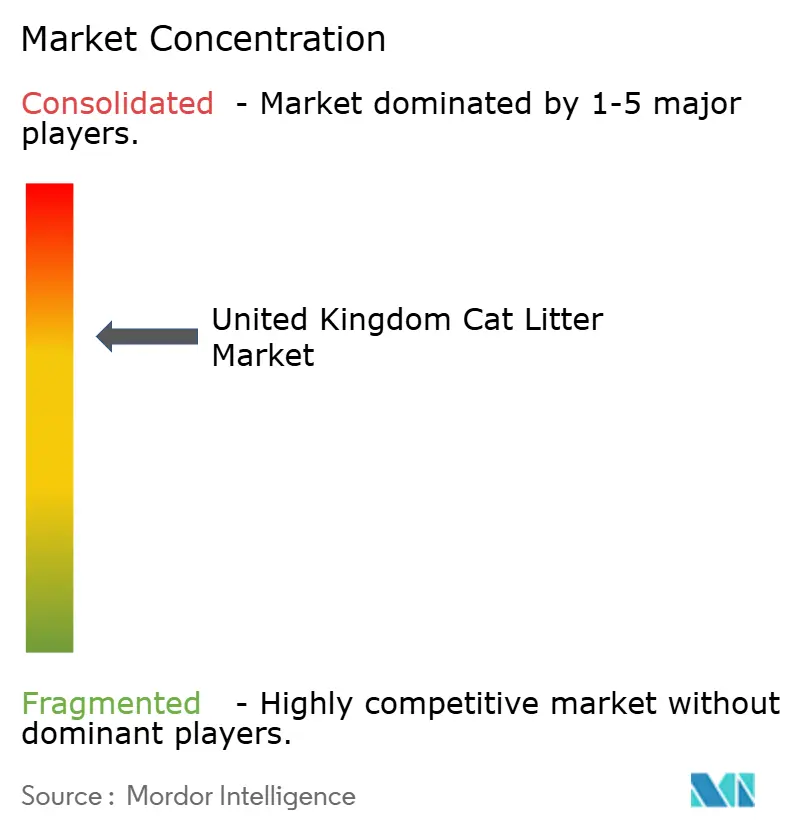

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Cat Litter Market Analysis by Mordor Intelligence

The United Kingdom cat litter market size is expected to grow from USD 272.35 million in 2025 to USD 293.22 million in 2026 and is forecast to reach USD 424.1 million by 2031 at 7.66% CAGR over 2026-2031. The market demonstrates consistent demand due to substantial household penetration, with 10.6 million cats present in 25% of the United Kingdom households. The considerable proportion of indoor cats (36%) contributes to increased daily litter consumption and purchase frequency[1]Source: Cats Protection, “Cats Report 2024,” catsprotection.org. Digital commerce has established itself as a significant growth driver, with subscription services and automated replenishment accounting for approximately 10% of category revenue for major omnichannel retailers. These services minimize inventory shortages and improve customer retention rates. Premium product segments continue to expand as younger pet owners invest in advanced formulations featuring low-dust, odor-control, and antibacterial properties to enhance both feline comfort and household air quality. Economic pressures have prompted 49% of cat owners to express concerns about product affordability, resulting in market adaptations through value-tier products and expanded private-label offerings to maintain market share.

Key Report Takeaways

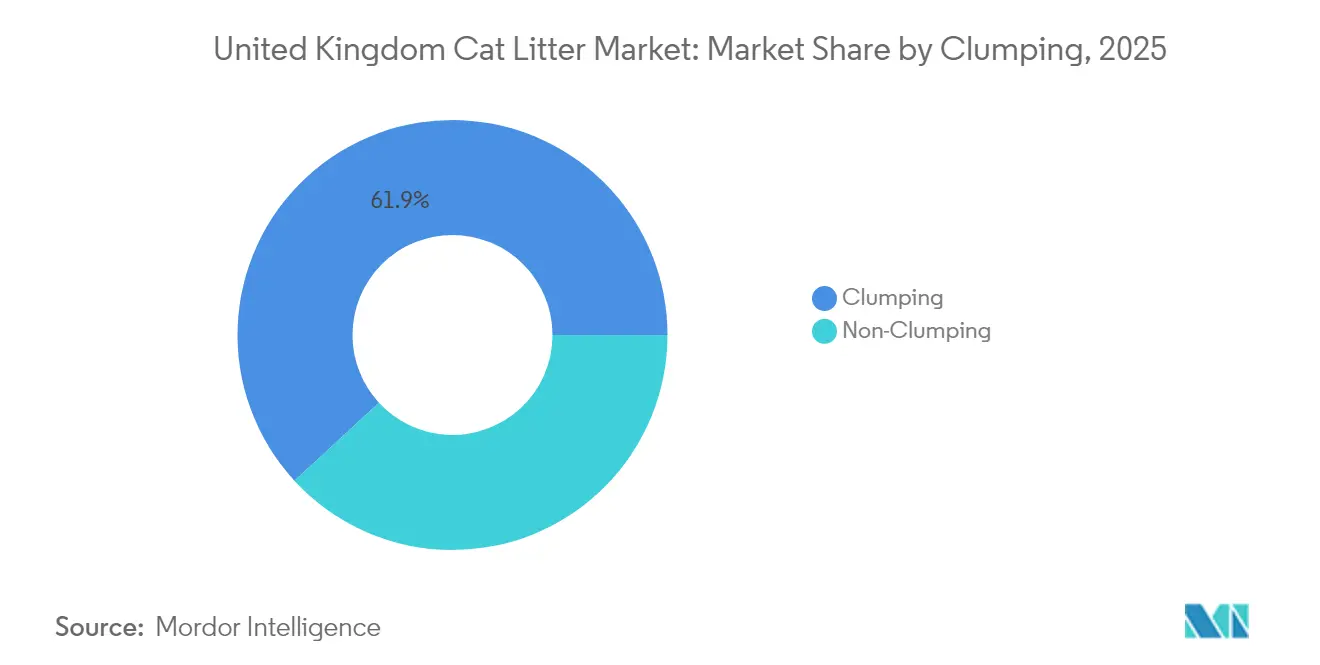

- By product type, clumping litter captured 61.85% of the United Kingdom cat litter market share in 2025, and is projected to expand at an 8.07% CAGR through 2031.

- By raw material, clay-based accounted for 67.55% of the United Kingdom cat litter size in 2025, whereas plant-based and biodegradable are projected to expand at a 9.72% CAGR through 2031, the fastest rate among raw material segments.

- By distribution channel, hypermarkets and supermarkets held 47.95% of the market revenue in 2025, while internet sales recorded the highest projected CAGR at 9.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Cat Litter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated pet-humanization trend | +1.1% | National, strongest in urban centers | Medium term (2-4 years) |

| Accelerating e-commerce penetration | +1.5% | Nationwide | Short term (≤ 2 years) |

| Premiumization of pet-care spend | +1.4% | England and Scotland | Medium term (2-4 years) |

| Shift toward sustainable/biodegradable litters | +1.7% | United Kingdom, led by London and Edinburgh | Long term (≥ 4 years) |

| Retailer private-label expansion via data analytics | +0.9% | Supermarket channels across the country | Short term (≤ 2 years) |

| Subscription-based delivery models gaining traction | +1.0% | High-density urban areas, extending to suburb | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Pet-Humanization Trend

The strengthening emotional connection between owners and pets is influencing purchasing decisions in the cat litter market. Research shows that 85% of cat owners engage in daily physical contact with their pets, while 65% maintain regular play schedules, indicating that cats are increasingly viewed as family members. This shift in perception has led to increased consumer willingness to purchase premium cat litter products that offer low-dust, hypoallergenic, and odor-control features to protect both cat health and home environment. The growth in pet insurance coverage and veterinary wellness plans has further emphasized the importance of quality products in maintaining feline health. Marketing messages have evolved from basic sanitation benefits to focus on overall cat wellbeing. As a result, the United Kingdom cat litter market is experiencing increased demand for premium products that offer comprehensive benefits, creating opportunities for higher revenue and product upgrades in retail channels.

Accelerating E-Commerce Penetration

Over 90% of United Kingdom households have internet access, with 73% regularly shopping on mobile devices. Cat litter bags are heavy and difficult to transport, making home delivery an appealing option for consumers through digital channels. Retailers use artificial intelligence systems to customize reorder timing based on customer usage patterns, which increases customer retention and order sizes. Pets at Home's Easy Repeat subscription service demonstrates this trend, with in-store subscription sign-ups matching online enrollment rates, showing successful integration across channels[2]Source: Pets at Home Group Plc, “FY24 Preliminary Results,” petsathome.co.uk. Online-only retailers focus on millennials by offering user-friendly interfaces and flexible subscription management. The United Kingdom cat litter market shows a shift in purchasing channels rather than replacement, as e-commerce complements traditional retail stores instead of replacing them.

Premiumization of Pet-Care Spend

Cat comfort remains a top spending priority for 52% of surveyed owners, ranking above entertainment and apparel despite inflation. Pedigree cats, which account for 45% of new pet acquisitions, require specialized products, driving demand for antibacterial and low-tracking clumping litter varieties. Indoor cat households show a strong preference for products featuring odor control, antimicrobial properties, and natural fragrances. In response, retailers have increased shelf space for premium products with functional benefits. This shift toward higher-value products has enabled the United Kingdom cat litter market to maintain revenue growth despite price sensitivity concerns.

Shift Toward Sustainable/Biodegradable Litters

The United Kingdom generates 774 million liters of cat litter waste annually, leading to increased environmental concerns. The government's plan to prohibit biodegradable waste in landfills by 2028 creates incentives for transitioning from bentonite clay to renewable materials such as wood pellets, corn, and recycled paper[3]Source: Department for Environment, Food and Rural Affairs, “Biodegradable Waste Consultation,” defra.gov.uk. Metropolitan areas with established curbside organic collection systems show higher adoption rates of sustainable alternatives. Manufacturers obtain Forest Stewardship Council certification for wood products and ISO 14001 certification for manufacturing processes to validate their environmental claims. Ongoing research has improved sustainable cat litter performance to match traditional clay-based products. The United Kingdom cat litter market expects sustainable products to increase market share while maintaining clumping effectiveness, driving continued product innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw material costs | -1.6% | United Kingdom, import-reliant clusters | Short term (≤ 2 years) |

| Environmental scrutiny of clay-mining operations | -0.8% | Global supply chains influencing United Kingdom | Long term (≥ 4 years) |

| Post-pandemic pet relinquishment dampening demand | -0.7% | Urban hubs | Medium term (2-4 years) |

| Brexit-linked logistics cost inflation | -1.1% | Nationwide, Europe trade routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Costs

The United Kingdom imports bentonite clay primarily from Greece, Hungary, and Bulgaria. Currency fluctuations and energy costs in mining operations led to a 6% increase in landed costs in 2025 compared to the previous year. Oil-Dri Corporation identifies freight and labor costs as key factors contributing to higher production expenses. The domestic landfill tax increased from USD 112 to USD 137 per metric ton in April 2025, further increasing costs for clay-based litter manufacturers[4]Source: Bywaters, “UK Recycling Trends 2025,” bywaters.co.uk. While producers implement hedging strategies and pursue multi-year supply agreements, transferring these costs to consumers remains difficult in the competitive retail market. The resulting margin pressure limits companies' ability to invest in innovation.

Brexit-linked Logistics Cost Inflation

The United Kingdom pet-care supply chain incurs administrative costs of USD 65 million annually through Export Health Certificates, customs inspections, and rule-of-origin documentation[5]Source: UK Pet Food, “Brexit Cost Implications,” ukpetfood.org. Extended lead times at Channel ports necessitate higher inventory levels and increased working capital requirements from distributors. While domestic manufacturers benefit from local production operations, raw material imports remain susceptible to currency fluctuations, affecting cost forecasting accuracy. These combined factors increase landed costs and influence competitive pricing in the United Kingdom cat litter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clumping Dominance Drives Innovation

Clumping litter accounts for 61.85% of the United Kingdom cat litter market share in 2025, with a projected CAGR of 8.07% through 2031. This segment generates the majority of category revenue due to its moisture-activated agglomeration properties, which facilitate daily maintenance and odor control. Major manufacturers have enhanced particle technology to improve absorption rates and minimize tracking. Mars, Incorporated has dedicated a portion of its USD 1 billion investment in digital and research and development to enhance the clumping granule composition, incorporating antibacterial properties and natural fragrances to support its premium wellness strategy. The segment's market dominance has spurred innovations in packaging design, with a focus on user convenience and environmental responsibility. The predictable consumption pattern of clumping litter aligns well with subscription services, strengthening customer retention and enabling product diversification within the United Kingdom cat litter market.

Non-clumping litter maintains its market presence among price-conscious consumers, particularly in households with multiple cats or those with outdoor access, where longer tray durability compensates for the increased maintenance requirements. While manufacturers offer dust-free crystal options and fragranced products to distinguish themselves from basic varieties, economic factors favor clumping litter as production efficiencies reduce cost differences. The non-clumping segment is anticipated to experience a slight decrease in market share through 2031.

By Raw Material: Clay Dominance Faces Sustainable Pressure

Clay-based products account for 67.55% of the United Kingdom cat litter market size in 2025, facing increased scrutiny regarding environmental impact and disposal costs. While bentonite offers superior clumping and cost advantages, its mining-related emissions and landfill impact pose challenges to sustainability objectives. Imerys Minerals Ltd., Oil-Dri Corporation of America, and regional miners supply the United Kingdom converters, with transportation requirements further affecting carbon emissions. Upcoming regulatory changes, including landfill restrictions planned for 2028, indicate a shift away from non-renewable materials.

Plant-based and biodegradable alternatives are experiencing rapid growth, with a projected 9.72% CAGR through 2031. Wood pellets appeal to environmentally conscious consumers by utilizing Forest Stewardship Council-certified forestry residue and natural pine fragrance, eliminating the need for artificial scents. Recycled paper granules offer flushable options where plumbing regulations permit, while corn- and wheat-based litter matches clay in terms of clumping effectiveness. Investment in local pellet production reduces import dependency and supports rural employment. Manufacturers demonstrating reduced carbon footprints are well-positioned for upcoming Extended Producer Responsibility fee adjustments. Silica gel maintains its premium market position, serving customers who value extended usage periods and effective odor control. Despite being non-biodegradable, silica's longer use duration results in reduced overall waste volume. While high prices and limited consumer awareness restrict widespread adoption, silica gel contributes to product diversification and margin enhancement.

By Distribution Channel: Internet Sales Transformation Accelerates

Hypermarkets and supermarkets hold 47.95% of the United Kingdom cat litter market share in 2025. These retailers capitalize on regular grocery shopping patterns through strategic product placement, including end-cap displays and in-aisle sampling. Their market position strengthens through data-driven shelf optimization, customized planograms, and expanded store formats that accommodate large product sizes. Private label offerings across price points help maintain customer loyalty through point-based reward systems.

Internet sales show the highest growth rate at 9.05% CAGR, driven by improved logistics and increasing consumer preference for home delivery. Major platforms, including Amazon, retail websites, and specialized pet care companies, offer real-time stock updates and rapid delivery options. Subscription services combine cat litter with other pet care products and services. Distribution centers implement automated packaging systems and sustainable protective materials to enhance operational efficiency and meet regulations. While veterinary clinics and convenience stores continue to serve immediate purchase needs, their combined market share is declining as e-commerce expands.

Geography Analysis

England leads the United Kingdom cat litter market, with its dominance attributed to a population of 9 million resident cats and a higher average household disposable income. London and the South East regions demonstrate the highest per-capita spending, influenced by concentrated indoor living that requires effective odor control and dust suppression products. The retail network is well-established, with Pets at Home operating over 450 stores across the country, with 50% located in England, offering integrated click-and-collect services that meet the needs of digital consumers.

Scotland maintains a prominent position in the market due to high indoor cat ownership rates, driven by adverse weather conditions and the prevalence of urban apartment living in cities such as Glasgow and Edinburgh. The region shows strong adoption of sustainable products, with biodegradable litter comprising 22% of Scottish sales compared to 14% nationally. The Scottish Government's Circular Economy Bill supports this consumer behavior, prompting retailers to expand their eco-friendly product ranges. The region also demonstrates high e-commerce adoption, supported by efficient parcel delivery networks and a concentrated population in the Central Belt.

Wales and Northern Ireland maintain a small but consistent market share, with growth driven by increasing private-label adoption and improved rural broadband connectivity. Welsh regions record the United Kingdom's highest recycling rates, supporting the adoption of compostable litter products that align with green-waste collection systems. Northern Ireland's post-Brexit trading status creates supply chain challenges, but its proximity to the Republic of Ireland ports provides alternative transportation routes, reducing mainland congestion impact. Both regions are projected to achieve steady mid-single-digit growth as disposable income levels align with national averages.

Competitive Landscape

The market maintains moderate consolidation, with five companies - Mars, Incorporated, Nestlé S.A. (Purina), Church & Dwight Co., Inc., The Clorox Company, and Pets Choice Ltd. (Pettex Limited) holding the majority market share in 2024. Mars, Incorporated maintains market leadership through its Catsan brand and strengthened market presence via veterinary clinic partnerships and loyalty programs. Nestlé's Purina division holds a significant market share, emphasizing premium features such as bacterial control and mild fragrances. Church & Dwight Co., Inc. maintains its position through Arm & Hammer's established baking soda technology and operates a Folkestone facility that produces over 500 SKUs for both domestic and export markets.

Industry consolidation continues through strategic acquisitions. Pets Choice acquired Pettex in April 2025, integrating the established litter brand into its diverse pet product portfolio and expanding multichannel distribution capabilities. Inspired Pet Nutrition's acquisition of Butcher's Pet Care in 2024 established a USD 380 million revenue operation, enabling vertical integration and expanded cat-specific production. Digital companies such as Tippaws and VanCatUK target specific market segments through sustainability initiatives and direct-to-consumer sales. Private label products from retailers, including Tesco's Everyday Value and Sainsbury's, Hypoallergenic impact pricing dynamics and shelf placement, affecting branded product margins.

Market participants prioritize investments in environmental material development, AI-based demand prediction, and recyclable packaging to meet Extended Producer Responsibility requirements. Marketing strategies increasingly incorporate social media influencers to connect with online cat owner communities, measuring engagement through digital metrics. The United Kingdom cat litter market reflects a competitive environment where market position depends on operational scale, regulatory compliance, and digital capabilities.

United Kingdom Cat Litter Industry Leaders

Mars, Incorporated

Nestlé S.A. (Purina)

Church & Dwight Co., Inc.

The Clorox Company

Pets Choice Ltd. (Pettex Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pets Choice Ltd acquired Pettex Ltd, incorporating their cat litter and small animal business operations. The Pettex cat litter brands joined Pets Choice's portfolio of pet brands, which includes Webbox, Bob Martin, Felight, Tastybone, and B-Calm. The acquisition enables customers and retailers to access Pettex Cat Litter products through Pets Choice's distribution network.

- March 2025: Oil-Dri Corporation of America showcased its cat litter products at the 2025 Global Pet Expo in Orlando, Florida. The company presented its Cat's Pride, Jonny Cat, and Ultra brands, along with private label options.

- March 2024: Kent Pet Group, a subsidiary of Kent Corporation and the maker of World's Best Cat Litter, partnered with Little Big Brands, a New York-based brand design firm, for a comprehensive brand redesign. The initiative included a new logo, packaging design, and visual identity.

United Kingdom Cat Litter Market Report Scope

Cat litter is an essential supply for all indoor cats and is used by cats to bury their urine and feces. The report covers cat litter brands and sales statistics in the United Kingdom and is segmented by product type (clumping and non-clumping), raw material (clay and silica), and distribution channels (specialized pet shops, internet sales, hypermarkets, and other distribution channels). The report offers market sizes and forecast values (USD) for all the above segments.

By Product Type

| Clumping |

| Non-Clumping |

By Raw Material

| Clay-based |

| Silica gel |

| Plant-Based and Biodegradable |

By Distribution Channel

| Specialized Pet Shops |

| Internet Sales |

| Hypermarkets/Supermarkets |

| Other Channels (Veterinary Clinics, Convenience Stores) |

| By Product Type | Clumping |

| Non-Clumping | |

| By Raw Material | Clay-based |

| Silica gel | |

| Plant-Based and Biodegradable | |

| By Distribution Channel | Specialized Pet Shops |

| Internet Sales | |

| Hypermarkets/Supermarkets | |

| Other Channels (Veterinary Clinics, Convenience Stores) |

Key Questions Answered in the Report

How large is the United Kingdom cat litter market in 2026?

The United Kingdom cat litter market size reached USD 293.22 million in 2026 and is projected to grow at a 7.66% CAGR through 2031.

Which product type holds the biggest share?

Clumping formulations captured 61.85% of United Kingdom cat litter market share in 2025 due to superior odor control and convenience.

Which raw-material segment is growing the fastest?

Plant-based and biodegradable litters are forecast to post a 9.72% CAGR between 2026 and 2031, the fastest among all material types.

Which companies lead the competitive landscape?

Mars Incorporated, Nestlé Purina, and Church & Dwight Co., Inc. top the market, while Pets Choice Ltd. is expanding through acquisitions.

Page last updated on: