Pesticide Inert Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

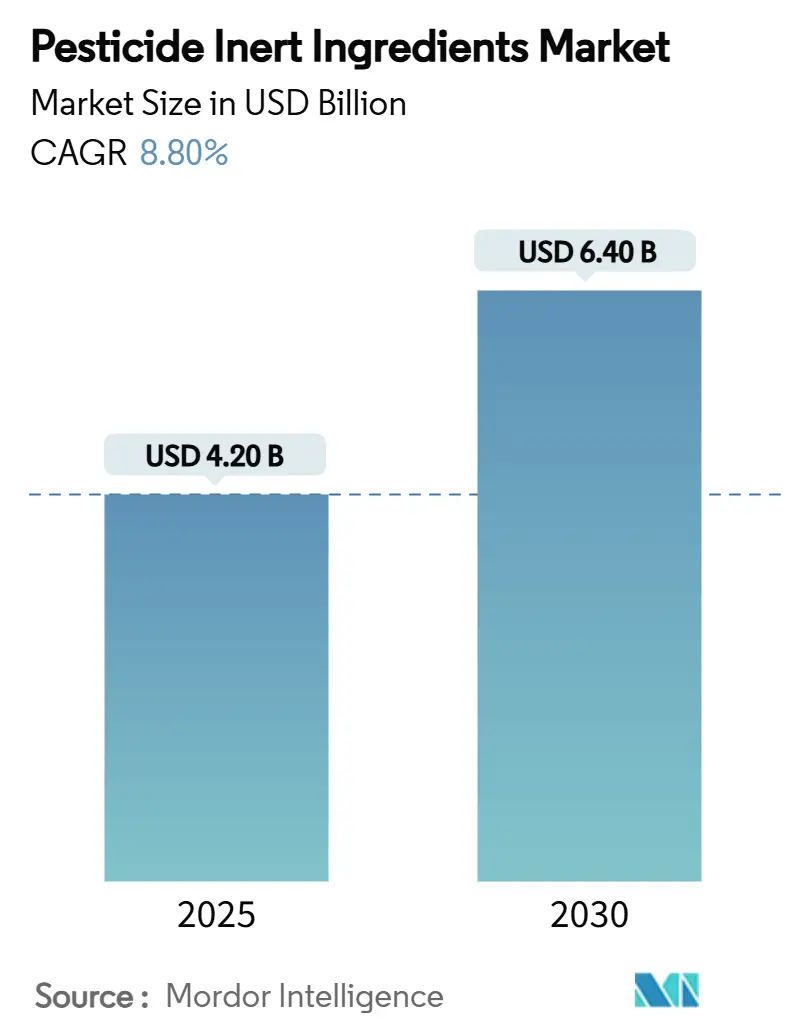

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 6.40 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pesticide Inert Ingredients Market Analysis by Mordor Intelligence

The pesticide inert ingredients market size is valued at USD 4.2 billion in 2025 and is projected to reach USD 6.4 billion by 2030, reflecting an 8.8% CAGR over the forecast period. Sustained demand for sustainable formulation technologies, rapid uptake of precision-spraying tools, and tighter disclosure rules position inert substances as active performance enhancers rather than passive carriers. Nano-carrier systems and sensor-compatible adjuvants now enable real-time field analytics, supporting higher input efficiency and lower environmental load[1]Source: Staff Writer, “Nano-Carrier Technologies Boost Agrochemical Efficiency,” ScienceDaily, sciencedaily.com. North America retains its volume leadership, while the Asia-Pacific region shows the fastest growth, driven by large-scale agricultural modernization and the adoption of tank-mixes that counter herbicide resistance. Substantial investments in bio-based surfactants, driven by rising restrictions on Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) and polyethoxylated tallow amines (POEAs), are focused on R&D towards fermentation-derived chemistries with transparent supply chains.

Key Report Takeaways

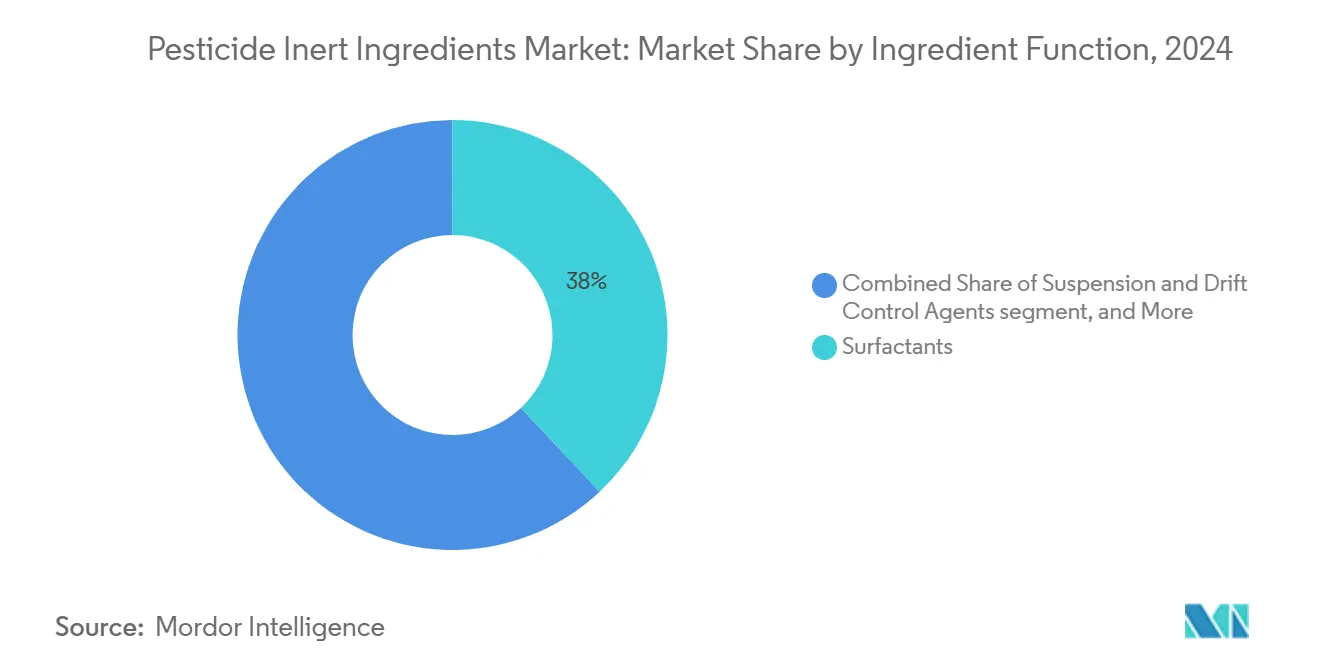

- By ingredient function, surfactants led with 38% of the pesticide inert ingredients market share in 2024, while suspension and drift control agents are projected to advance at a 9.4% CAGR through 2030.

- By source, synthetic products accounted for a 67% share of the market in 2024, while bio-based products are projected to expand at a 11.5% CAGR through 2030.

- By form, liquid formulations accounted for a 72% share of the pesticide inert ingredients market size in 2024, with solid formats projected to register a 6.8% CAGR through 2030.

- By pesticide type, herbicides dominated the pesticide inert ingredients market, accounting for nearly 50% of the market in 2024. In contrast, fungicide-linked inert demand is poised to grow at the highest CAGR of 9.2% from 2024 to 2030.

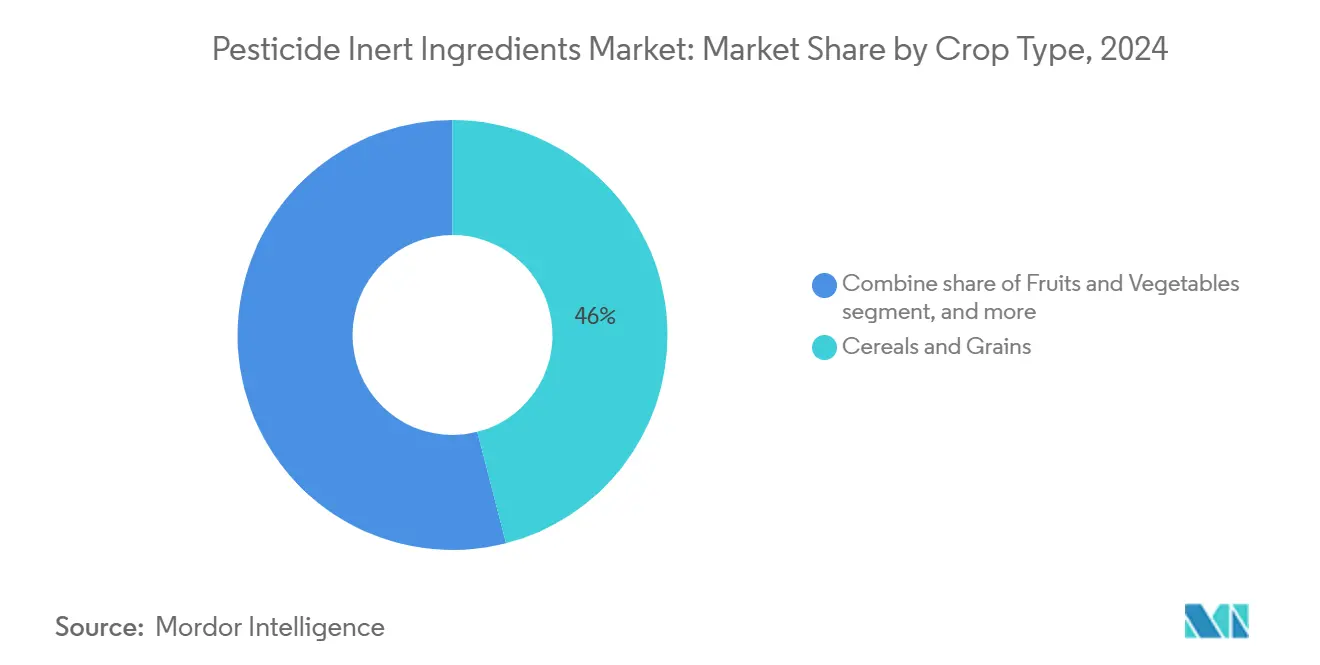

- By crop type, cereals and grains contributed 46% revenue in 2024, and the fruits and vegetables are forecast to post an 8.9% CAGR until 2030.

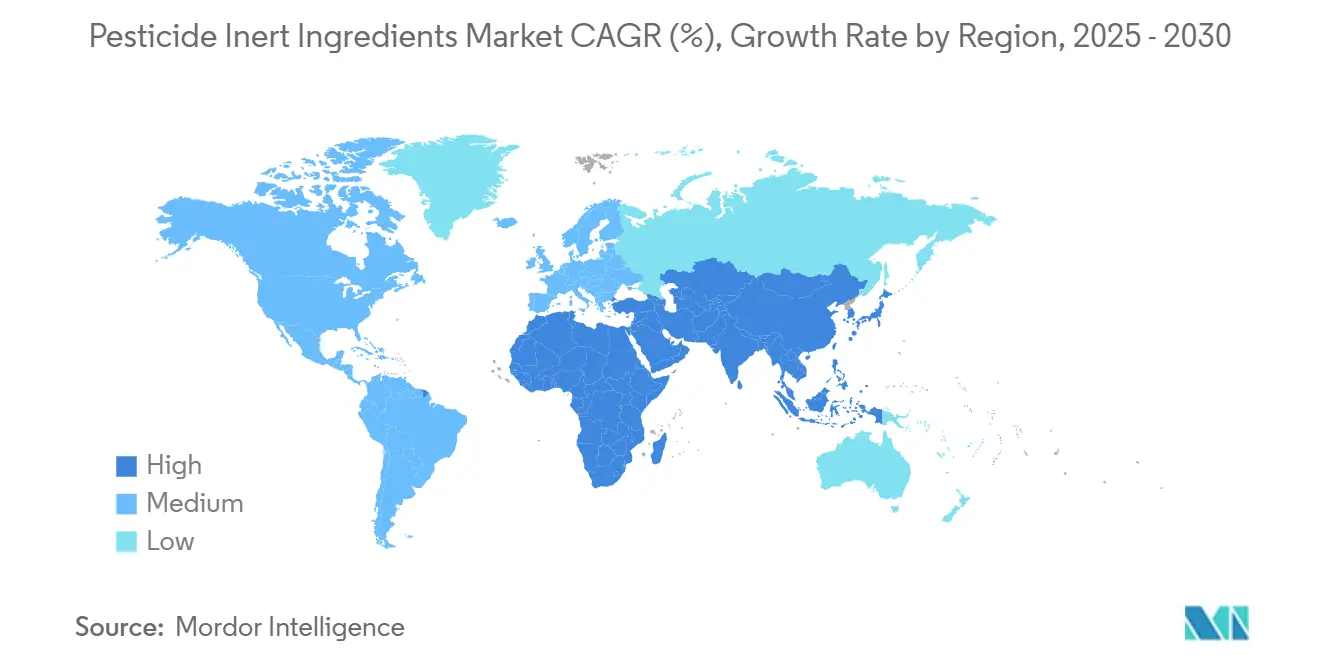

- By geography, North America accounted for 41% share of the revenue in 2024, and Asia Pacific is projected to register a 10.7% CAGR until 2030.

- BASF SE, Dow Inc., Solvay SA, Clariant AG, and Croda International, held a 50.7% collective share in 2024, underscoring a moderately concentrated competitive field.

Global Pesticide Inert Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surfactant dominance in modern pesticide formulations | +1.8% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Rising precision-spraying and drift-reduction mandates | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| Expansion of bio-based inert ingredient pipelines | +1.3% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Growth of tank-mix adjuvants for herbicide resistance management | +1.1% | Global, especially North and South America | Medium term (2–4 years) |

| Nano-carrier innovation improving active-ingredient uptake | +0.9% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Sensor-ready smart adjuvants enabling real-time field analytics | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surfactant Dominance in Modern Pesticide Formulations

Non-ionic surfactants underpin colloidal stability, wetting, and penetration for glyphosate and glufosinate programs. Polyether-modified polysiloxanes reduce surface tension to below 20 mN/m, aiding canopy coverage during drone spraying. Performance criteria now cover droplet diameter uniformity and drift index scores, spurring demand for multifunctional surfactants with built-in antifoam properties. Environmental pressure accelerates the switch to biodegradable options derived from castor and palm kernel feedstocks. Higher unit prices for premium grades offset slower volume growth, keeping revenue expansion on track for the pesticide inert ingredients market.

Rising Precision-Spraying and Drift-Reduction Mandates

The United States Environmental Protection Agency’s 2024 Herbicide Strategy mandates drift-reducing technologies for 900 protection zones, raising formulation thresholds for drift indices below 10%[2]Source: Environmental Protection Agency, “Herbicide Strategy 2024,” EPA, epa.gov. Polymer-based drift control agents now deliver higher viscosity at low shear, preserving nozzle performance, and supporting aerial spraying windows previously off-limits[3]Source: MDPI Editorial Board, “Spray Drift Mitigation Techniques,” MDPI, mdpi.com. Similar rules are advancing in the European Union, prompting parallel adoption of electrostatic sprayers that require highly conductive adjuvants. The regulatory-compliance premium is widening, creating a differentiated segment within the pesticide inert ingredients market.

Expansion of Bio-Based Inert Ingredient Pipelines

Fermentation-based glycolipids and sophorolipids match conventional ethoxylates in spreading efficacy while curbing ecotoxicity, driving an 11.5% CAGR for the bio-based segment. Castor-bean traceability programs certify over 100,000 metric tons of seed annually, supplying plant-derived C12-C18 chains for green wetting agents with 57% yield improvement for smallholders. Rising organic acreage in Europe and North America offers premium pricing channels, strengthening margins for early movers in the pesticide inert ingredients market.

Growth of Tank-Mix Adjuvants for Herbicide Resistance Management

Multifunctional adjuvants stabilize dicamba and 2,4-D premixes, improving control of resistant Amaranthus species by up to 25 percentage points over single-mode programs. Compatibility agents prevent antagonism between contact and systemic actives, reducing re-spray costs. University of Florida field trials report 33% fewer clogging incidents when growers adopt surfactant-based acidic buffers. These efficiency gains reinforce the adoption of premium tank-mix enhancers inside the pesticide inert ingredients market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory disclosure of full formulations | -1.2% | Europe and North America, expanding globally | Medium term (2–4 years) |

| Acute toxicity findings for polyethoxylated tallow amines | -0.8% | Global, strongest in Europe and North America | Short term (≤ 2 years) |

| Supply volatility of specialty vegetable oils | -0.6% | Global, particularly bio-based segment | Medium term (2–4 years) |

| Emerging bans on Per- and polyfluoroalkyl substances (PFAS)-containing fluorosurfactants | -0.7% | Europe and North America, with potential global spread | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Disclosure of Full Formulations

The shift toward full formulation disclosure marks a significant change in pesticide regulation. The European Union and several United States jurisdictions have introduced requirements that remove the traditional protection of inert ingredient identities as trade secrets. This regulatory change compels manufacturers to reformulate products using ingredients that are publicly acceptable, often resulting in higher costs and potential compromises in performance. These requirements pose challenges for companies with proprietary surfactant blends and specialized adjuvant systems, which are the result of substantial R&D investments.

Acute Toxicity Findings for Polyethoxylated Tallow Amines

Recent toxicological studies have linked polyethoxylated tallow amines (POEAs) to bee mortality and disruptions in aquatic ecosystems, prompting regulatory reviews and voluntary phase-outs by major manufacturers in the United States. These actions have led to supply chain disruptions and formulation challenges. The Environmental Protection Agency (EPA)'s acknowledgment of POEA toxicity concerns has intensified scrutiny of surfactant ingredients. Manufacturers are making significant investments in alternative surfactant technologies, such as plant-based ethoxylates and synthetic alternatives, which aim to address toxicity concerns while maintaining performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Function: Surfactants Extend Performance Leadership

Surfactants retained a 38% share of the pesticide inert ingredients market size in 2024, underlining their pivotal role in penetration, wetting, and drift control. Sophisticated polyether-modified polysiloxanes achieve contact angles below 10 degrees, boosting uptake in waxy leaf crops. In addition, biodegradable alkyl polyglucosides now match their synthetic counterparts in terms of spreading speed, thereby widening their adoption in certified sustainable programs. Moving forward, the push to replace POEAs accelerates niche opportunities for natural glycolipids, especially in organic farming.

Emulsifiers ensure the stable dispersion of multi-active formulations for resistance management. Oil-based concentrates, largely methylated seed oils, contribute to efficacy gains in post-emergence herbicides. Suspension and drift control agents are projected to advance at a 9.4% CAGR through 2030, as drone and electrostatic spraying enlarge application windows. Buffers and water conditioners help reduce hard-water antagonism in the pesticide inert ingredients market. Hybrid multifunctional products are blurring category lines, encouraging suppliers to position systems solutions rather than single-function additives.

By Source: Bio-Based Momentum Builds

Bio-based inputs are projected to approach parity with synthetics by 2030. A robust 11.5% CAGR reflects regulatory incentives, lower carbon footprints, and farmer preferences for greener labels. Fermentation-derived sophorolipids achieve a 1:1 substitution ratio compared to petroleum ethoxylates, resulting in up to a 65% reduction in greenhouse gas emissions.

Synthetic ingredients still account for a significant share of the volume, at 67% due to their scale and cost advantages. Yet, restrictions on Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) and public disclosure rules raise compliance expenses, prompting many formulators to test hybrid blends that combine synthetic performance with bio-based appeal. Pilot plants in Germany and Brazil are scaling enzymatic esterification routes, promising further cost parity by 2027.

By Form: Liquids Maintain Dominance

Liquid preparations accounted for 72% of the pesticide inert ingredients market size in 2024, due to their compatibility with high-pressure booms and autonomous drones. Formulators fine-tune rheology to 200–300 cP to secure uniform droplet diameters under variable nozzle pressures. Smart liquids embedding conductive polymers generate real-time viscosity data to field consoles, reducing misapplication episodes by 6%.

Solid formats, including wettable powders and water‑dispersible granules projected to grow at a 6.8% CAGR through 2030, driven by improved handling stability and compatibility with low‑volume application technologies. These excel in humid tropics where storage temperatures breach 30 °C. The nano-encapsulated gels and microemulsion concentrates remain a niche. Despite small volume, these high-margin formats are the fastest expanders, attracting venture investment into the pesticide inert ingredients market.

By Crop Type: Cereals and Grains Stay at the Forefront

Cereals and grains captured 46% of revenue because extensive acreage and weed pressure keep adjuvant spend high. Drone spraying of rice in Asia utilizes ultra-low-volume emulsions, which require higher surfactant loadings for uniform leaf wetting. Fruits and vegetables are poised for an 8.9% CAGR through 2030, propelled by residue-sensitive programs that value low-toxicity bio-based carriers.

The use of oilseeds and pulses is increasing as the biodiesel policy boosts planted areas and thus adjuvant demand for waxy cuticle penetration. Specialty and horticultural crops filled the remaining niche, where targeted applications and smart-release systems are gaining traction. Collectively, evolving crop mixes diversify the revenue base of the pesticide inert ingredients market while offering premium niches for technology-oriented suppliers.

By Pesticide Type: Herbicides Drive Volume

Herbicide formulations constituted roughly 50% of inert consumption in 2024, reflecting continued reliance on post-emergence weed control amid escalating resistance. Dicamba-tolerant cropping systems use diverse adjuvant packages to balance volatility, uptake, and off-target risk. Insecticide-linked inert demand has been increasing consistently, with a focus on cuticular penetration enhancers for resistant pests in cotton and soy.

Fungicides are poised for the highest 9.2% CAGR to 2030, bolstered by systemic actives that rely on xylem mobility, aided by nano-carriers. Precision soil-borne nematicide delivery shows strong upside. The shift to integrated pest management enhances cross-functional adjuvants that can serve multiple pesticide classes, thereby expanding wallet share per hectare in the pesticide inert ingredients market.

Geography Analysis

North America generated 41% of global revenue in 2024, aided by extensive precision-spraying infrastructure and Environmental Protection Agency (EPA) drift-reduction mandates that favor premium adjuvants. State-level Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS) disclosure rules intensify reformulation activity, stimulating demand for fluorine-free wetting agents. Public–private programs in the United States and Canada support drone-ready adjuvant trials across 300,000 acres of row crops, creating an early-mover advantage for local manufacturers.

Asia-Pacific recorded the fastest 10.7% CAGR outlook to 2030, supported by modernization programs in China, India, and Southeast Asia. India’s 416 new pesticide registrations in H1 2024 unlock downstream adjuvant opportunities. Government-backed drone subsidies encourage liquid adjuvant demand, especially for rice and cotton. Market participants must navigate fragmented regulations yet benefit from high adoption elasticity as farm incomes rise.

Europe's demand is driven by stringent sustainability targets and the most transparent ingredient disclosure regime worldwide. The European Commission’s multi-year renewal of key active approvals provides product planning stability, while funding under Horizon Europe accelerates research on low-carbon emulsifiers[4]Source: Analysts, “EU Renewal of Pesticide Approvals,” Foresight, foresight.org. Despite slower hectare growth, premiumization continues to drive the expansion of the pesticide inert ingredients market through value gains. South America, the Middle East, and Africa collectively represent the remaining share, with Brazil’s soybean expansion driving demand for compatibility agents that stabilize multi-mode herbicide tanks. African horticultural exports have fostered interest in residue-minimizing, bio-based surfactants. Middle Eastern date and citrus growers are adopting water-conditioning buffers to offset the high bicarbonate content in their irrigation water, highlighting climate-specific needs within the pesticide inert ingredients market.

Competitive Landscape

The top five companies, BASF SE, Dow Inc., Solvay SA, Clariant AG, and Croda International, held a 50.7% collective share in 2024, signaling moderate concentration. BASF SE leads as the market leader, leveraging its integrated castor programs and a broad range of emulsifiers. Dow Inc., another major player, is emphasizing process innovation, exemplified by its hydrogen peroxide-to-propylene glycol route, which was launched in collaboration with Evonik Industries in 2025. Solvay SA, Clariant AG, and Croda International complete the group with specialized surfactants and polymeric drift agents. Fragmentation below the top tier leaves room for regional producers and biotech start-ups to carve niches in bio-based sophorolipids and nano-carriers.

Strategically, players pursue vertical integration and technology alliances. Dow Inc.’s tie-up with Evonik Industries reduces water use by 95% in propylene glycol production, positioning both firms for lower-carbon supply chains. BASF SE’s Pragati program secures feedstock while granting farmers a 57% yield bump, reinforcing social license and supply security. Smaller innovators partner with drone OEMs to preload adjuvants into application software, creating lock-in advantages.

Regulatory expertise and transparent sourcing increasingly dictate success. Companies invest in digital formulation libraries compliant with global hazard communication standards, cutting registration time. Intellectual property shifts toward process and application methods as ingredient disclosure grows. Together, these dynamics maintain brisk innovation while preserving a balanced competitive field within the pesticide inert ingredients market.

Pesticide Inert Ingredients Industry Leaders

BASF SE

Solvay SA

Clariant AG

Croda International

Dow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Environmental Protection Agency's (EPA) proposed registration of ten isocycloseram-based products will boost demand for compatible inert ingredients across diverse use sites. This is projected to accelerate innovation in surfactants, carriers, and formulation aids for next-gen insecticides.

- January 2025: Syngenta Group Co.’s Crop Protection division divested its FarMore Technology vegetable seed treatment platform to Gowan SeedTech, broadening access to precision coating systems. This is projected to spur innovation in binders, polymers, and carriers within the pesticide inert ingredients market.

- June 2024: Nutrien Ltd's subsidiary, Nutrien Ag Solutions, has acquired Suncor’s AgroScience assets, a move that is set to drive demand for inert ingredients compatible with chlorin-based photosensitizers. This supports advancements in formulation stability and delivery systems ahead of Environmental Protection Agency (EPA) registration by 2026.

Global Pesticide Inert Ingredients Market Report Scope

Pesticide inert ingredients are non-active substances in pesticide formulations that support functions such as mixing, spreading, stabilizing, and preserving, but do not directly control pests. The Pesticide Inert Ingredients Market is segmented by ingredient function (surfactants, Oil-based Oils and Methylated Seed Oils, Emulsifiers, Suspension and Drift Control Agents, Buffers and Water Conditioners), source (synthetic and bio-based), form (liquid and solid), pesticide type (herbicides, insecticides, fungicides and others), crop type (cereals and grains, fruits and vegetables, Oilseeds and Pulses and Others), and geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market forecasts are presented in value terms (USD).

| Surfactants |

| Oil-based Oils and Methylated Seed Oils |

| Emulsifiers |

| Suspension and Drift Control Agents |

| Buffers and Water Conditioners |

| Synthetic |

| Bio-based |

| Liquid |

| Solid (Powders & Granules) |

| Herbicides |

| Insecticides |

| Fungicides |

| Others (Rodenticides, Nematicides) |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Other Crops |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Ingredient Function | Surfactants | |

| Oil-based Oils and Methylated Seed Oils | ||

| Emulsifiers | ||

| Suspension and Drift Control Agents | ||

| Buffers and Water Conditioners | ||

| By Source | Synthetic | |

| Bio-based | ||

| By Form | Liquid | |

| Solid (Powders & Granules) | ||

| By Pesticide Type | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Others (Rodenticides, Nematicides) | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Other Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the pesticide inert ingredients market, and how fast is it growing?

The pesticide inert ingredients market size stands at USD 4.2 billion in 2025 and is forecast to reach USD 6.4 billion by 2030, reflecting an 8.8% CAGR.

Which ingredient function holds the largest share in the pesticide inert ingredients market?

Surfactants lead with 38% share in 2024 because they enhance wetting, penetration, and drift control in modern formulations.

Why are bio-based inert ingredients gaining traction?

Fermentation-derived surfactants offer competitive performance and help meet tightening sustainability and disclosure regulations, resulting in an 11.5% CAGR for the bio-based segment.

Which region is projected to grow the fastest through 2030?

Asia-Pacific is projected to record a 10.7% CAGR, driven by rapid precision-agriculture adoption and expanding crop protection capacity.

Page last updated on: