Biorational Pesticides Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

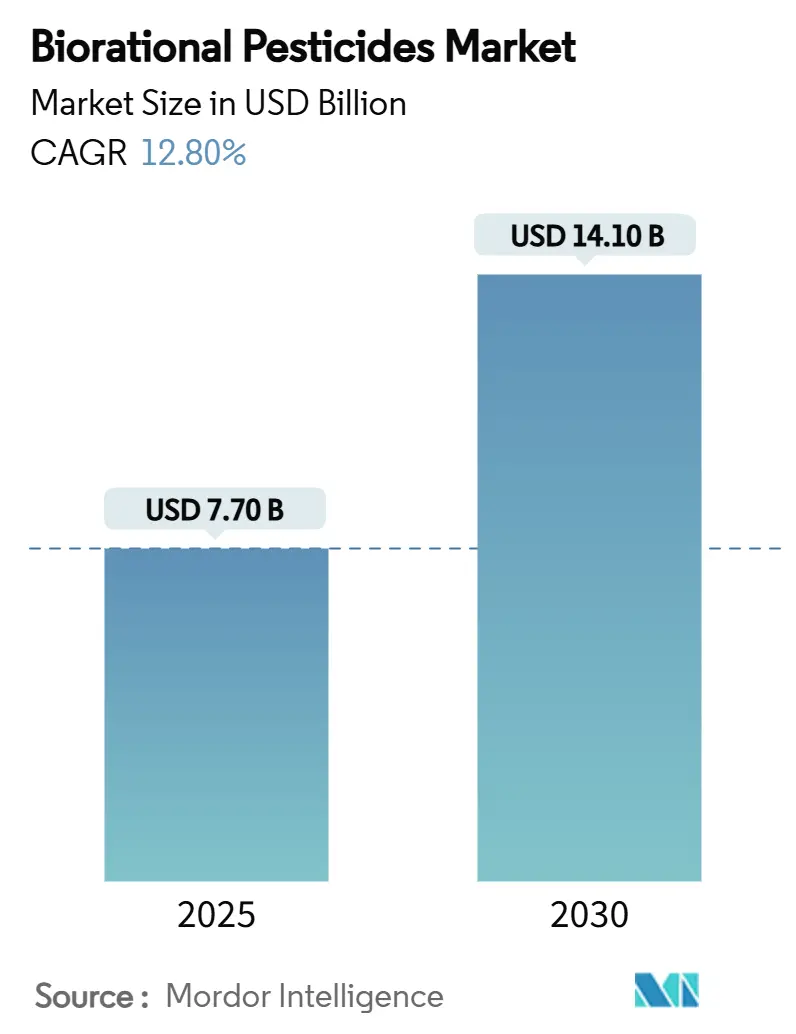

| Market Size (2025) | USD 7.70 Billion |

| Market Size (2030) | USD 14.10 Billion |

| Growth Rate (2025 - 2030) | 12.80% CAGR |

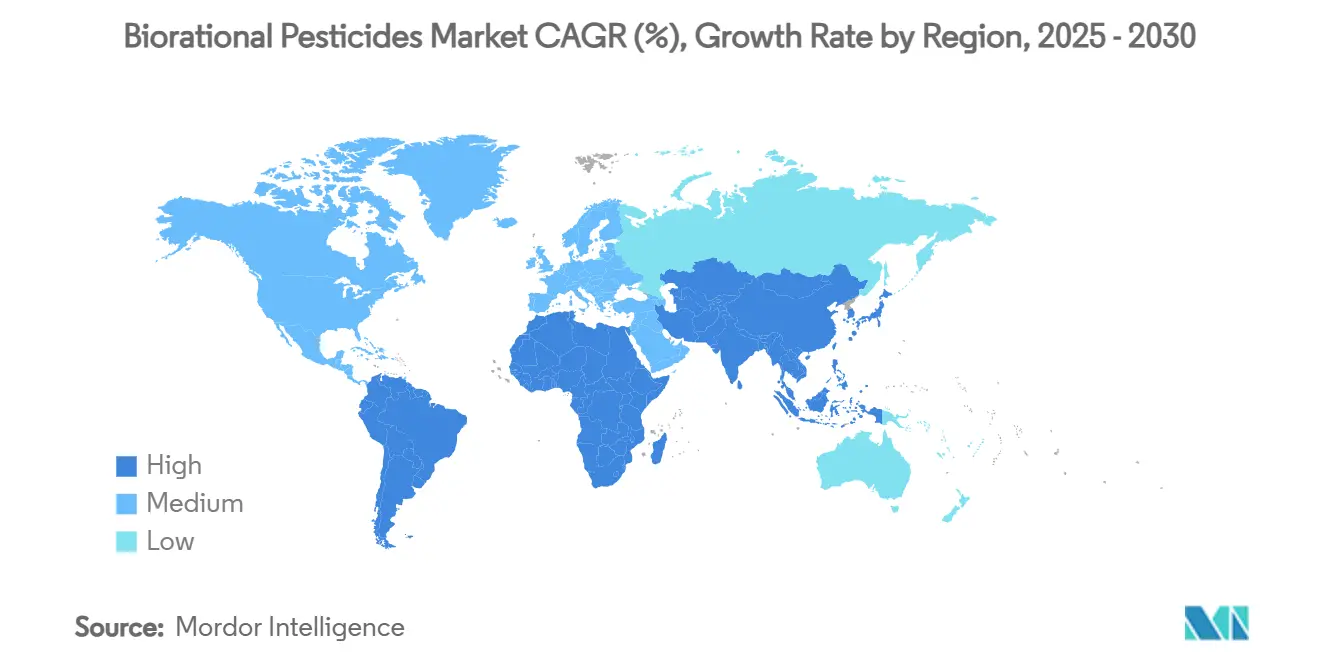

| Fastest Growing Market | South America |

| Largest Market | North America |

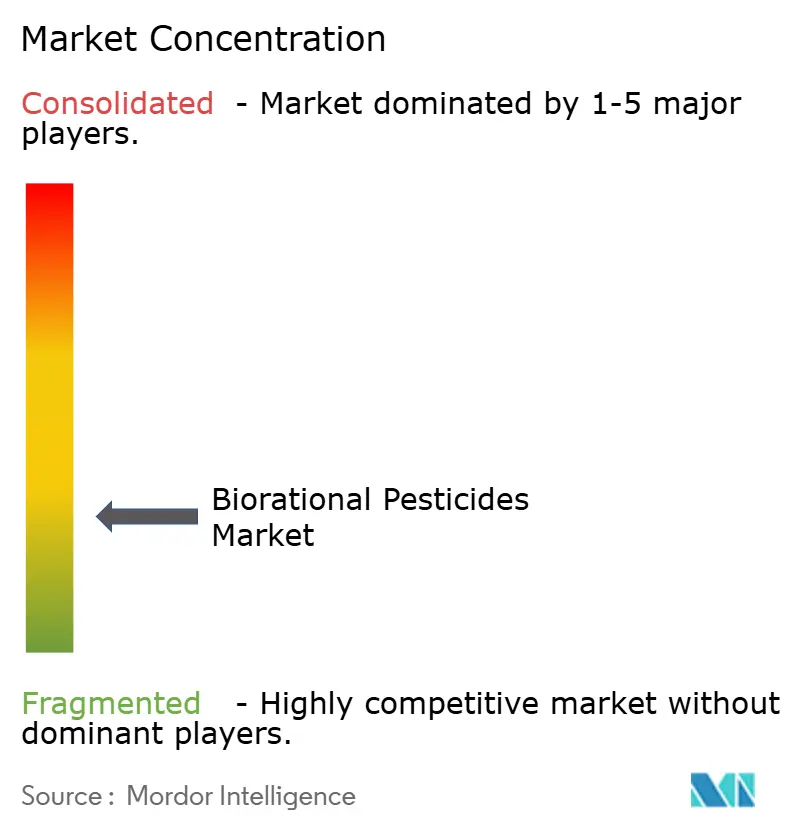

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biorational Pesticides Market Analysis by Mordor Intelligence

The biorational pesticides market size is USD 7.7 billion in 2025 and is projected to reach USD 14.1 billion by 2030, growing at a CAGR of 12.8%. Stringent global residue regulations, expansion of organic farming acreage, and advancing bio-innovation pipelines drive this growth.[1]European Food Safety Authority, “Updated Peer Review of the Pesticide Risk Assessment of the Active Substance Spinosad,” EFSA Journal, efsa.europa.euRegulatory changes, specifically the European Union's Farm to Fork strategy targeting a 50% reduction in synthetic pesticide use by 2030, are transforming crop protection approaches toward biological alternatives. The market development is further supported by venture capital investments that enable commercial scaling of RNA interference technologies and microbiome-based products. North America maintains its market leadership due to advanced agricultural infrastructure and efficient United States Environmental Protection Agency (EPA) registration processes, while South America demonstrates the highest growth potential through supportive regulatory frameworks and large-scale farming operations. The microbial ingredient segment dominates the market, with biochemical platforms showing rapid adoption rates due to advances in synthetic biology and peptide discovery that reduce development timelines. The market's fragmented nature increases merger and acquisition opportunities, particularly for specialized innovators who integrate proprietary active ingredients with digital agricultural decision-making tools.

Key Report Takeaways

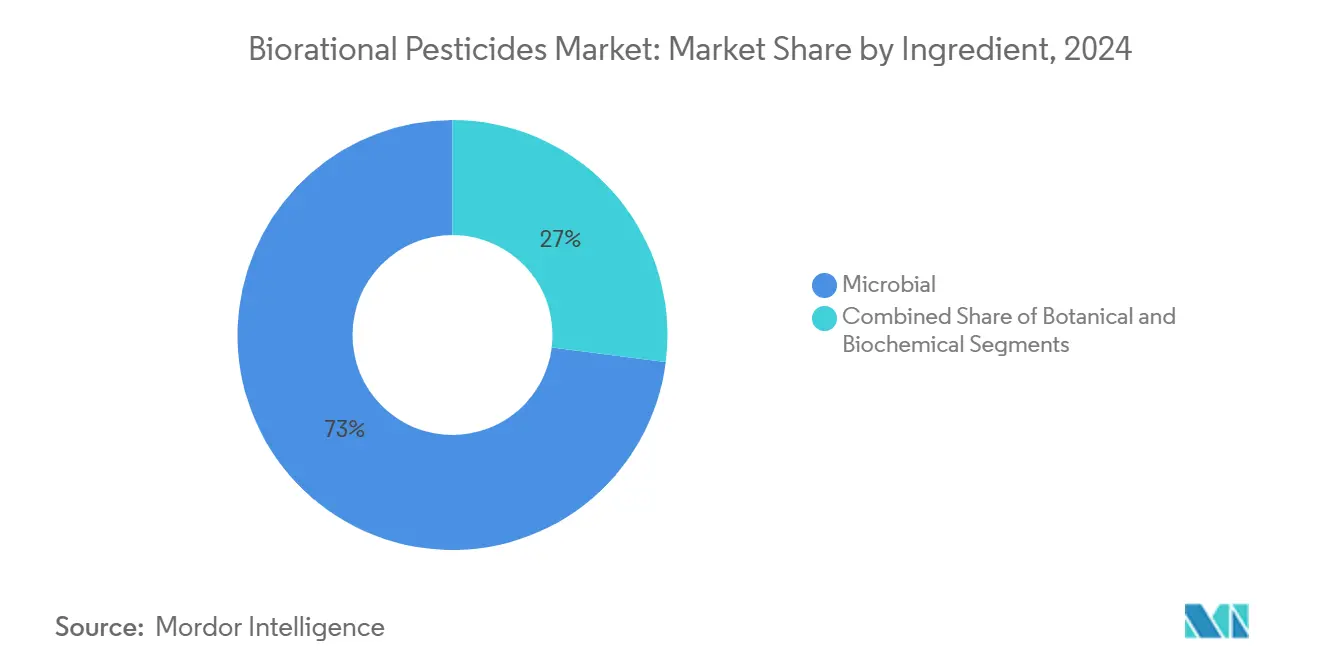

- By ingredient, the microbial segment dominated with 73% of the biorational pesticides market share in 2024, while biochemical products are projected to grow at 16.7% CAGR through 2030.

- By product type, bioinsecticides generated 48% of market revenue in 2024, with bionematicides projected to achieve the highest growth rate at 19.1% CAGR through 2030.

- By crop type, fruits and vegetables held 33% of the market size in 2024. The oilseeds and pulses segment is forecast to grow at 18.9% CAGR between 2025 and 2030.

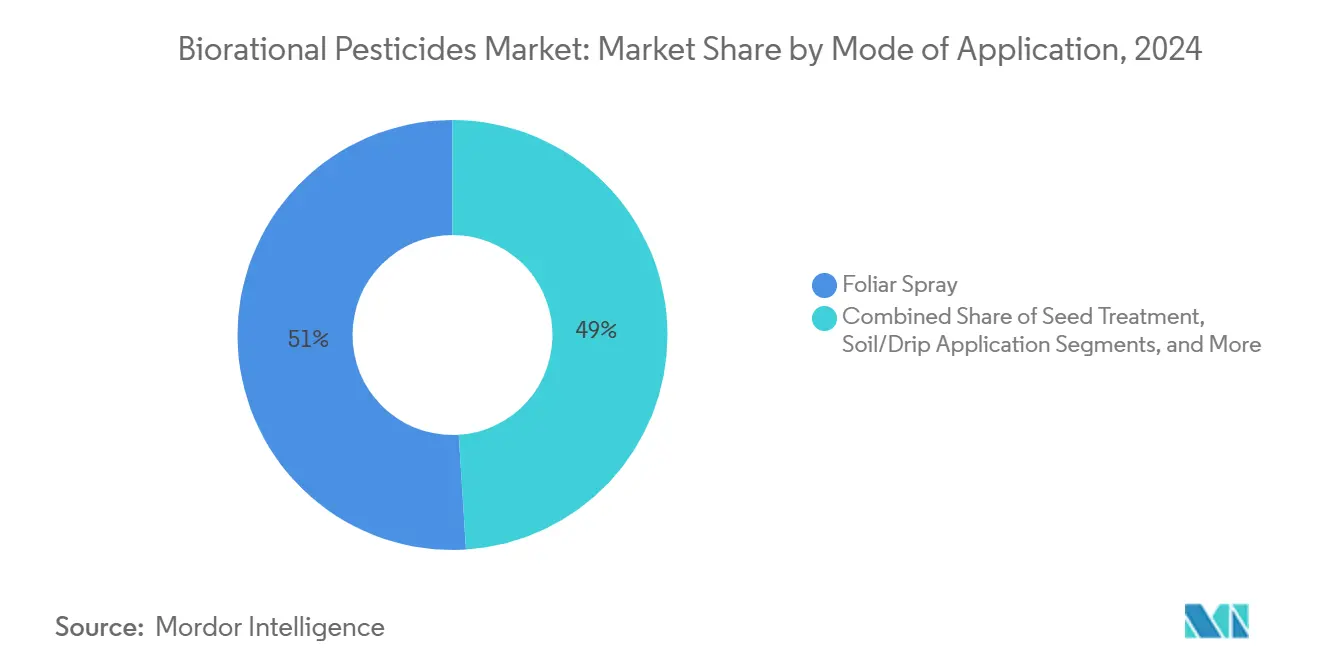

- By mode of application, foliar sprays dominated with 51% revenue share in 2024. Seed treatments are projected to grow at a 19.8% CAGR through 2030.

- By formulation, liquid held the dominant position with a 58% revenue share in 2024. The dry formulation segment is anticipated to grow at a CAGR of 14.5% through 2030.

- By geography, North America maintained market leadership with a 35% share in 2024, while South America is anticipated to grow at a 15.0% CAGR through 2030.

- The market remains fragmented, with Valent BioSciences (Sumitomo Chemical Co., Ltd.), Bayer AG, Syngenta AG, BASF SE, and Certis Biologicals (Mitsui & Co., Ltd) collectively holding 34% market share in 2024.

Global Biorational Pesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global maximum residue limits and pesticide bans | +2.1% | Global; Europe and Japan at the forefront | Medium term (2–4 years) |

| Rapid growth of organic acreage and premium food demand | +1.8% | North America and Europe; spreading to Asia-Pacific | Long term (≥4 years) |

| Post-patent pipeline shift of majors toward bio-innovation | +1.5% | Global; Research and Development hubs in North America and Europe | Medium term (2–4 years) |

| Venture-backed RNA-interference bio-actives reaching field scale | +1.2% | North America and Europe; pilot programs in Brazil | Short term (≤2 years) |

| Soil-microbiome digital twins optimizing bio-pesticide efficacy | +0.9% | Advanced markets in North America, Europe and Australia | Medium term (2–4 years) |

| Carbon-credit monetization for biological crop-protection practices | +0.8% | Global; early uptake in California, Europe and Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Maximum Residue Limit and Pesticide Bans

Global regulators are implementing stricter residue limits, leading growers to adopt biological alternatives. The European Union removed more than 200 chemical active ingredients following the 2024 regulations, while Japan's positive-list import system creates additional compliance requirements. Developing countries are adopting similar restrictions - Chile prohibited 58 active ingredients and Mexico restricted glyphosate use, aligning their export requirements with stringent international standards. Export-focused farmers are increasingly using biorational products to safeguard against potential future restrictions. This regulatory alignment is permanently changing product portfolios and intensifying research efforts toward residue-free solutions.

Rapid Growth of Organic Acreage and Premium Food Demand

Global certified organic farmland reached 96.4 million hectares in 2024, with organic food sales reaching EUR 141 billion (USD 152.3 billion).[2]Agence BIO, “Organic Sector Worldwide,” AGENCE BIO, agencebio.org This expansion drives demand for biorational pesticides, as organic regulations prohibit synthetic chemicals while requiring crop protection. The price premiums for organic produce offset the higher costs of biological inputs. The emergence of pesticide-free labels in Europe creates an additional market segment by providing an intermediate sustainability option. Consumer willingness to pay higher prices for residue-free produce continues to support grower adoption of biological solutions, despite their variable performance.

Post-Patent Pipeline Shift of Majors Toward Bio-Innovations

Major agrochemical companies are shifting their research and development focus due to the expiration of key synthetic patents and lengthening chemical approval timelines, which now exceed 10 years. The integration of Lavie Bio Ltd.'s computational biology platform by ICL Group Ltd. in 2025 demonstrates the industry's move toward rapid, biology-based innovation. Biological products typically receive market approval within 3-5 years, enabling companies to update their product portfolios efficiently while fulfilling sustainability commitments. Large companies now utilize their established distribution networks and regulatory expertise to commercialize biological products at scale, intensifying competition for startups with limited market access.

Venture-Backed RNA-Interference Bio-actives Reaching Field Scale

RNA interference (RNAi) platforms secured over USD 100 million in venture funding in 2024. The EPA's approval of a double-stranded RNA (dsRNA) solution for controlling the Colorado potato beetle demonstrated the technology's commercial viability.[3]United States Environmental Protection Agency, “Biopesticide Registration Program,” epa.gov Field trials indicated 70-85% pest control effectiveness with minimal impact on non-target organisms, resolving previous performance concerns. Improved fermentation processes have reduced manufacturing costs, while new encapsulation methods enhance dsRNA stability in field conditions. Initial applications in potato, corn, and specialty crop cultivation show decreased pest resistance development, establishing RNAi as an effective component of integrated pest management strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent field-level performance vs. synthetics | –1.5% | Global; especially regions with high weather variability | Short term (≤2 years) |

| Limited shelf-life and cold-chain gaps | –1.2% | Emerging markets lacking refrigerated infrastructure | Medium term (2–4 years) |

| Complex, region-specific biological registration processes | –0.8% | Global; notable delays in Asia-Pacific and South America | Long term (≥4 years) |

| Rising cross-resistance to single-strain microbials | –0.6% | Intensive production zones with high biological adoption | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Field-Level Performance vs. Synthetics

The efficacy of microbial pesticides varies between 40% and 90%, influenced by temperature, humidity, and pest pressure, which affects farmer confidence. Microbial viability decreases by 30-50% within 48 hours under unfavorable field conditions, making application timing crucial. The lack of standardized label instructions and limited agricultural extension support hinders widespread adoption. While formulation research, weather prediction tools, and targeted application protocols help address these challenges, consistent field performance remains a work in progress.

Limited Shelf-Life and Cold-Chain Gaps

Biological products require storage at 2-8°C and have a shelf life of 12-24 months, while synthetic products remain stable for 3-5 years. Cold chain infrastructure limitations in Africa and parts of Asia increase distributor costs by up to 25% and restrict retail inventory levels. Recent encapsulation technologies have extended stability to 36 months, though higher production costs reduce pricing flexibility. Kapsera's biodegradable microfluidic carrier extends product shelf life but lacks large-scale manufacturing capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Microbials Sustain Leadership Amid Biochemical Acceleration

Microbial products accounted for 73% of the biorational pesticides market share in 2024, supported by an extensive application history and established regulatory frameworks. The market relies on proven strains of Bacillus, Trichoderma, and Beauveria, which have demonstrated a safe record, enabling multi-crop applications. While the biorational pesticides market continues to show steady revenue growth in the microbial segment, its expansion rate is lower compared to emerging chemical alternatives due to limited opportunities for new label expansions.

Biochemical products are projected to grow at a 16.7% annual rate through 2030, driven by advances in synthetic biology for producing complex plant-derived molecules and pheromone blends. Investment activities by major players demonstrate strong market confidence in peptides, alkaloids, and signaling compounds, which provide high efficacy without leaving residues. The expedited approval process for non-living active ingredients shortens time-to-market, enabling faster commercialization. The accelerated approval process for non-living active ingredients reduces time-to-market, allowing new competitors to gradually gain market share from established microbial products.

By Product Type: Bioinsecticides Maintain Scale While Bionematicides Surge

Bioinsecticides accounted for 48% of revenue in 2024, primarily targeting lepidopteran and coleopteran pests in fruits, vegetables, and row crops. Their established field performance and comprehensive label coverage make them essential components of integrated pest-management programs. The segment maintains volume through new RNA-i and peptide-based products designed to manage resistance development.

The bionematicides market is projected to grow at 19.1% annually through 2030, driven by increased recognition of nematode-related crop losses. Microbial consortia for soil application and biochemical seed coating technologies protect crucial early growth phases. Market expansion is supported by growing soybean cultivation in South America and increased pulse production in India, where synthetic nematicide options are restricted or being eliminated.

By Crop Type: High-Value Produce Drives Premium Adoption

Fruits and vegetables held a 33% share of the biorational pesticides market in 2024, driven by strict residue limits and quality standards. Retailers' "no detect" requirements have made biological products essential for pre-harvest applications. The consistent urban demand for fresh berries, grapes, and leafy greens maintains regular application patterns.

The oilseeds and pulses segment is projected to grow at a CAGR of 18.9%, as farmers increase their use of biological seed treatments for early crop protection and improved germination rates. The growth in rapeseed and pea cultivation across Europe, combined with double-cropped soybean production in South America, provides the volume needed for efficient biological seed coating applications that work alongside nitrogen-fixing organisms.

By Mode of Application: Foliar Sprays Hold Ground; Seed Treatments Gain Momentum

Foliar sprays accounted for 51% of revenue in 2024, as growers continued using conventional boom sprayers due to familiarity and low switching costs. The immediate visible results of treatments in fruits and vegetables contribute to high repeat purchase rates. New adjuvant formulations improve leaf adhesion and UV protection, which reduces the need for repeated applications.

Seed treatment applications are projected to grow at 19.8% annually, driven by precision planting equipment and polymer coating technologies that enable accurate dosing and protect microorganisms during planting. Combined seed treatments containing both inoculants and biological pest control agents improve root development and crop establishment. Digital tracking systems using batch codes monitor product effectiveness, highlighting the importance of technology integration.

By Formulation: Liquids Dominate but Dry Technologies Extend Access

Liquid formulations hold 58% market share in 2024, driven by their ease of dilution and compatibility with existing equipment. Cold-chain storage requirements limit their distribution in regions with poor infrastructure. Manufacturers incorporate UV-blocking stabilizers and oxygen scavengers to extend shelf life, though these additions increase production costs.

Dry formulations, including wettable powders and water-dispersible granules, are growing at a 14.5% CAGR during 2025-2030. These forms offer 24-36 months of stability at ambient temperatures. Biodegradable granules enable controlled release in soil, supporting long-term nematode suppression. Manufacturers focus on developing encapsulation carriers that decompose after active ingredient release, addressing environmental concerns and improving logistics efficiency.

Geography Analysis

North America contributed 35% of 2024 revenue, with the United States as the primary market. The Environmental Protection Agency's biopesticide registration division provides accelerated review timelines, reducing the process by half compared to synthetic pesticides. The region's market strength stems from high-value specialty crops in California, Washington, and Florida, combined with extensive implementation of precision agriculture, which supports higher biological product pricing. Canada's market growth is driven by organic transition grants that provide subsidies for microbial applications in prairie grain rotations.

Europe represents the second-largest market, driven by the Farm to Fork strategy that requires a 50% reduction in chemical pesticide usage by 2030. Germany, France, and the Netherlands demonstrate high adoption rates through established extension networks and public-private pilot projects that assess effectiveness in temperate climates. The market expansion is further supported by pesticide-free production certifications in Scandinavian and Central European countries, which create new opportunities in the mid-price sustainability segment.

South America demonstrates the highest growth rate at 15.0% CAGR, with Brazil's approval of over 600 biological active ingredients over the past five years and their integration into large-scale soybean and sugarcane production. Argentina's soybean market expansion and Chile's fruit export industry drive biological adoption due to residue concerns. The Asia-Pacific region shows varied adoption patterns, with Japan's strict residue regulations driving demand, while India's small-scale farmers require integrated biological and extension service packages. Australia combines carbon-credit incentives with digital platforms to measure emission reductions from biological applications. The Middle East and Africa markets remain early-stage, with promising developments in South African table grape production and Kenyan horticulture, supported by cold-chain infrastructure improvements.

Competitive Landscape

The industry remains fragmented, with the top five suppliers players including Valent BioSciences (Sumitomo Chemical Co., Ltd.), Bayer AG, Syngenta AG, BASF SE, and Certis Biologicals (Mitsui & Co., Ltd), holding a combined 34% market share in 2024. Valent BioSciences maintains the largest share through its proprietary fermentation facilities and extensive Bacillus product portfolio. Syngenta AG and Bayer AG maintain strong positions through their global distribution networks and multi-crop product registrations, while BASF SE and Certis Biologicals complete the top five manufacturers. This fragmentation creates opportunities for innovative companies, as demonstrated by AgroSpheres, which secured USD 37 million in Series B financing in late 2024 to advance its AgriCell encapsulation technology for improved biological persistence in field conditions.

The competitive landscape is evolving through strategic partnerships between established companies and emerging firms. Corteva's investment in Micropep provides access to peptide discovery libraries and streamlines product registration through shared data. ICL's 2025 acquisition of Lavie Bio demonstrates the integration of computational biology with formulation expertise, reflecting chemical companies' transition toward biological solutions.

Investment in biological crop protection remains robust, with over USD 500 million invested in ventures during 2024. Biobest secured USD 82.4 million in January 2025 to expand its global insectary operations, while Koppert Biological Systems obtained EUR 140 million (USD 151.2 million) to expand its bumblebee pollination and microbial products in Asia and South America. This capital influx enables specialized companies to expand manufacturing capabilities, manage regulatory requirements, and pursue strategic acquisitions to consolidate market position.

Biorational Pesticides Industry Leaders

Valent BioSciences (Sumitomo Chemical Co., Ltd.)

Bayer AG

Syngenta AG

BASF SE

Certis Biologicals (Mitsui & Co., Ltd)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ICL Group Ltd. has completed the acquisition of Lavie Bio Ltd.'s computational biology activities from Evogene, integrating predictive design capabilities into its biological crop protection research and development.

- March 2025: Syngenta Group launched NETURE, a biological insecticide that helps farmers manage insects affecting the productivity of soybean and corn crops. The bioproduct provides effective and residual control of corn leafhopper and other sap-sucking pests, including stink bugs, whiteflies, and sugarcane leafhopper.

- December 2024: SOLASTA Bio secured USD 14 million in Series A funding to accelerate the development of its peptide-based bioinsecticides. The company's nature-inspired products represent the first such bioinsecticides developed globally.

- November 2024: Kapsera completed a USD 4.4 million Series A round to advance biodegradable microfluidic encapsulation for biological inputs.

Global Biorational Pesticides Market Report Scope

| Microbial |

| Botanical |

| Biochemical and Semiochemical |

| Bioinsecticide |

| Biofungicide |

| Bioherbicide |

| Bionematicide |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Other Crops (Turfs and Ornamentals, and Commercial Crops) |

| Foliar Spray |

| Seed Treatment |

| Soil/Drip Application |

| Post-Harvest |

| Liquid |

| Dry (WP, WG, Granules) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Israel | |

| Iran | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Africa |

| By Ingredient | Microbial | |

| Botanical | ||

| Biochemical and Semiochemical | ||

| By Product Type | Bioinsecticide | |

| Biofungicide | ||

| Bioherbicide | ||

| Bionematicide | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Other Crops (Turfs and Ornamentals, and Commercial Crops) | ||

| By Mode of Application | Foliar Spray | |

| Seed Treatment | ||

| Soil/Drip Application | ||

| Post-Harvest | ||

| By Formulation | Liquid | |

| Dry (WP, WG, Granules) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Israel | ||

| Iran | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current biorational pesticides market size?

The biorational pesticides market size is USD 7.7 billion in 2025 and is projected to reach USD 14.1 billion by 2030.

Which ingredient type leads the biorational pesticides market?

Microbial products hold 73% of 2024 revenue, reflecting mature regulatory pathways and broad crop adoption.

Which region is growing fastest in the biorational pesticides market?

South America is projected to post the quickest 15.0% CAGR through 2030, led by Brazil’s supportive regulatory environment.

Why are seed treatments gaining traction in biological crop protection?

Seed treatments deliver precise doses, shield microbes during planting and are forecast to grow at a 19.8% CAGR through 2030.

How fragmented is the competitive landscape?

The top five players capture only 34% share, indicating ample room for consolidation and start-up disruption.

What role do carbon credits play in adoption?

Emerging carbon markets can add USD 15–30 per ha in revenue, improving biological paybacks by up to 35% and encouraging wider use.

Page last updated on: