Microencapsulated Pesticides Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

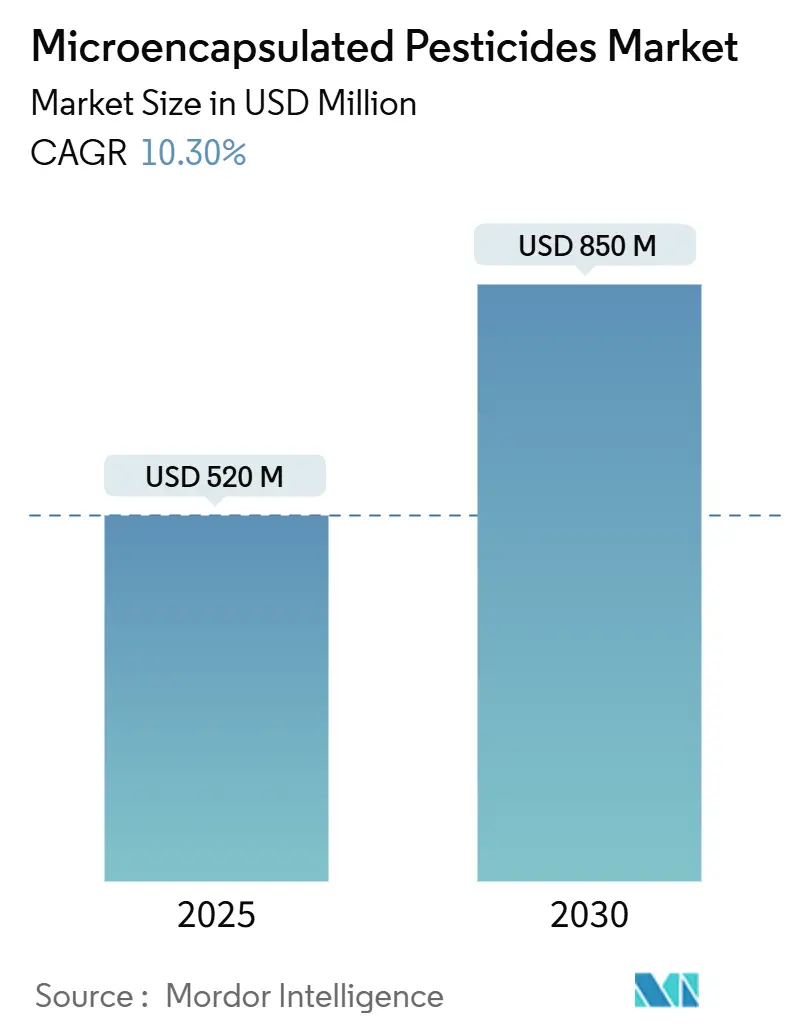

| Market Size (2025) | USD 520 Million |

| Market Size (2030) | USD 850 Million |

| Growth Rate (2025 - 2030) | 10.30% CAGR |

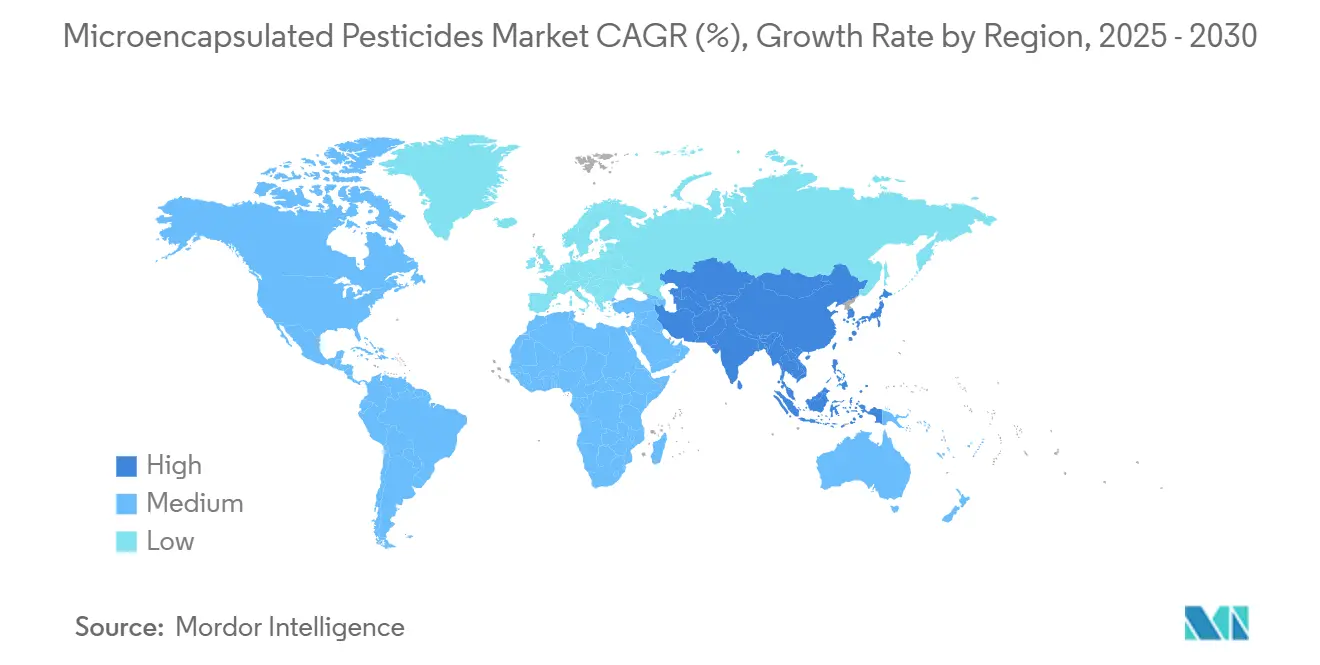

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

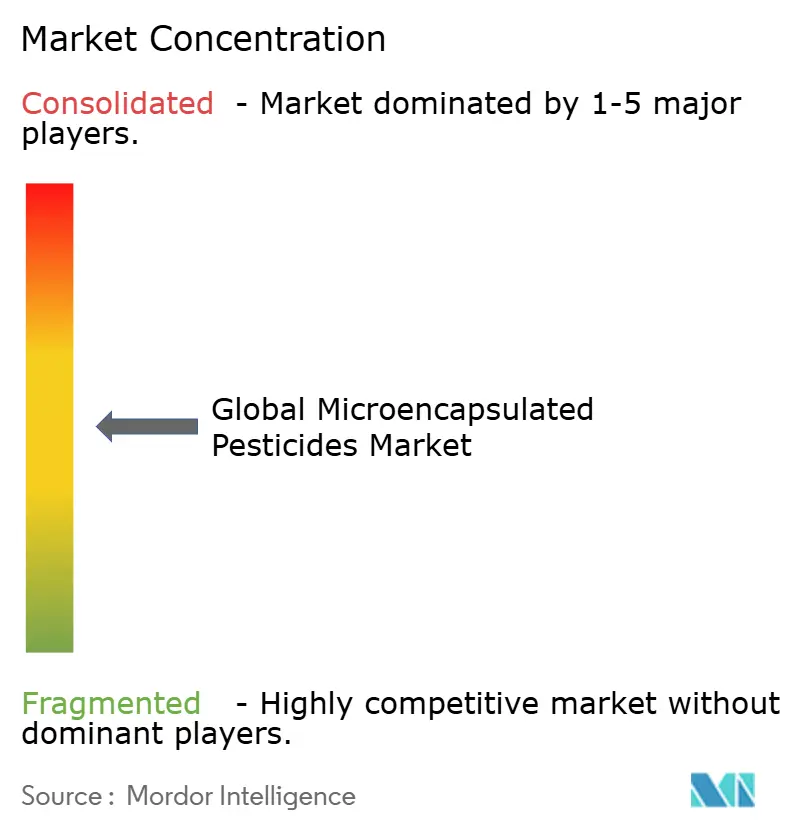

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microencapsulated Pesticides Market Analysis by Mordor Intelligence

The microencapsulated pesticides market size is projected to reach USD 850 million by 2030, reflecting a robust 10.3% CAGR that underscores the sector’s alignment with precision agriculture goals and tightening residue regulations. Growth momentum in the microencapsulated pesticides market is driven by controlled-release technology, which reduces off-target drift by up to 80%, meets stringent maximum residue limits, and addresses labor constraints through fewer spray passes. Early adopters who integrate drone-based variable-rate spraying with capsules report 20-30% savings on active ingredients, alongside stable yields, which strengthens the economic narrative for adoption. The integration of drone-based application systems with microencapsulated formulations is particularly promising, enabling variable-rate applications that optimize capsule placement and reduce labor costs by up to 40% in large-scale operations.

Key Report Takeaways

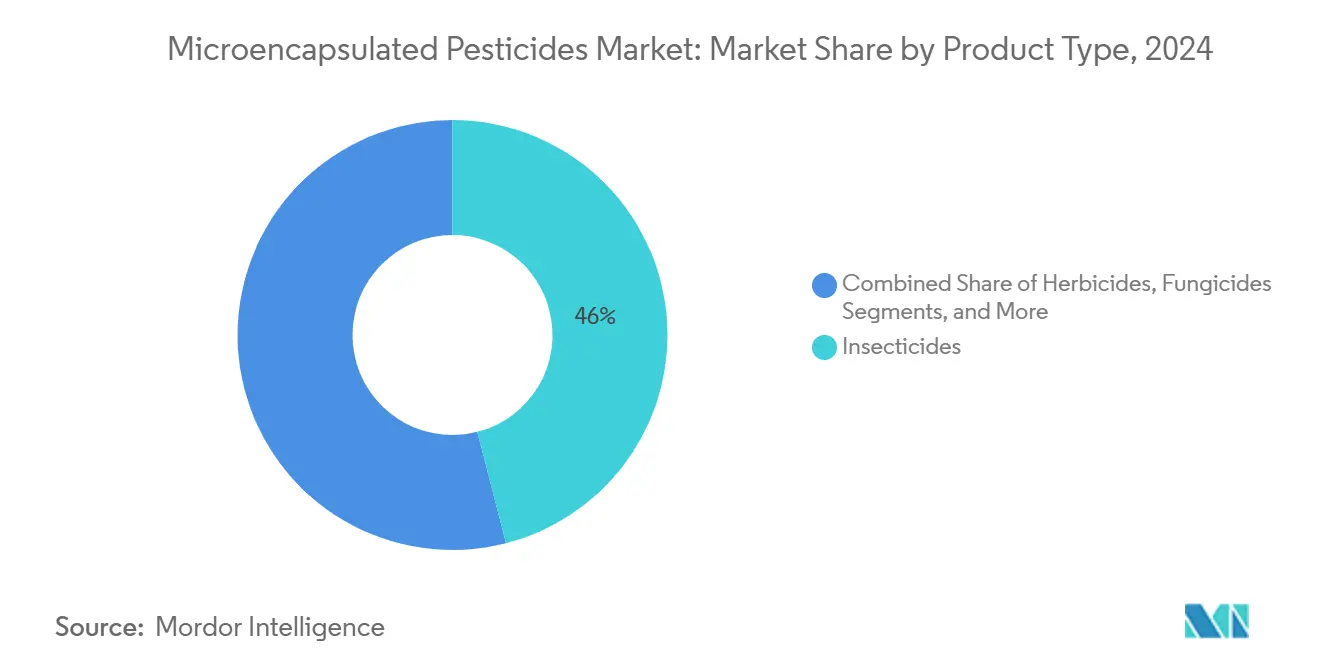

- By product type, insecticides captured 46% of the microencapsulated pesticides market share in 2024, while herbicides are projected to log a 12.4% CAGR through 2030.

- By technology, polymer coating held 51.2% of the microencapsulated pesticides market value in 2024, whereas fluidized-bed coating is forecast to expand at an 11.5% CAGR to 2030.

- By crop, cereals and grains accounted for 39.4% of the 2024 microencapsulated pesticides market size, while fruits and vegetables will grow at a 9.5% CAGR during 2025-2030.

- By capsule size, 50-250 µm particles represented 57.1% of the microencapsulated pesticides market size in 2024, and less than 50 µm capsules are positioned for a 10.4% CAGR through 2030.

- By region, North America led with 37.5% microencapsulated pesticides market share in 2024, and Asia-Pacific is slated for the fastest 12.1% CAGR to 2030.

Global Microencapsulated Pesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent pesticide-use regulations favoring controlled-release formulations | +2.1% | Global and strongest in North America and Europe | Medium term (2-4 years) |

| Shift toward integrated pest-management programs | +1.8% | Global and accelerating in Asia-Pacific | Long term (≥4 years) |

| Rising demand for residue-free produce by global retailers | +1.6% | Global and led by North America and Europe | Short term (≤2 years) |

| Increasing adoption in seed-treatment formulations | +1.4% | Global and strongest in Asia-Pacific | Medium term (2-4 years) |

| Emergence of biodegradable polymer shells | +1.2% | Global and early adoption in Europe | Long term (≥4 years) |

| AI-guided precision spraying boosting microencapsulation ROI | +1.0% | North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Pesticide-Use Regulations Favoring Controlled-Release Formulations

Most advanced farming economies are amplifying pressure on conventional chemistries. The European Union’s Farm to Fork pathway seeks a 50% cut in pesticide volumes by 2030, while the United States Environmental Protection Agency is phasing out tolerances on more than 200 actives [1]Source: Environmental Protection Agency, “Receipt of Pesticide Petitions,” federalregister.gov . Microencapsulated pesticides address those directives by slowing release rates so that growers can reduce total active load 20-40% yet maintain control levels. Capsules also limit drift, enabling 60-80% reductions in aquatic-toxicity metrics, which expedites product registrations. Specialty-crop exporters gain an extra hedge because controlled release enables near-zero residues that match supermarket specifications and avoid load-rejection penalties.

Shift Toward Integrated Pest-Management Programs

As of 2024, more than 70% of large grower cooperatives in North America and Europe employed formal Integrated Pest-Management (IPM) schemes, and national extension services in China and India are accelerating similar adoption. Microencapsulated pesticides align seamlessly with threshold-based decision-making, as extended residual windows support beneficial predators and biologicals. Field studies show that IPM regimes deploying capsules cut overall pesticide volume 25-35% while sustaining yields, which is crucial in high-value crops. Capsules also dovetail with remote-sensing alerts, allowing variable-rate microdosing once pest thresholds are trigger.

Rising Demand for Residue-Free Produce by Global Retailers

Retail chains including Walmart, Tesco, and Carrefour enforce private residue standards that are tighter than statutory ceilings, driving a premium channel for farms that deliver residue-free produce. Controlled-release formulations reduce harvest-time residues 70-85% compared with conventional sprays. Export-oriented fruit and vegetable producers thus capture 15-25% price lifts, while non-compliant shipments risk 30% rejection. Consequently, growers shift their budget toward microencapsulated pesticides even when the cost per liter is higher because revenue protection outweighs price premiums.

Increasing Adoption in Seed-Treatment Formulations

Microencapsulated seed treatments account for over 40% of new global registrations, driven by the requirement to incorporate systemic active ingredients into kernels without causing phytotoxicity. The encapsulation technology enables increased loading rates and controlled release for up to six weeks after emergence, protecting seedlings during their critical growth period. Bayer AG, Syngenta Group, and Corteva Agriscience invest more than USD 200 million annually in developing temperature-sensitive encapsulation technology that releases active ingredients as soil temperature increases. Results from extensive corn trials demonstrate that seed-treatment encapsulation reduces early stand loss by 15-20%, leading to increased adoption across row-crop areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial manufacturing costs of microencapsulation | -1.8% | Global and acute in price-sensitive markets | Short term (≤2 years) |

| Regulatory ambiguity for nano-capsule registration | -1.4% | Global and strongest in Europe and Asia-Pacific | Medium term (2-4 years) |

| Limited farmer awareness in price-sensitive economies | -1.2% | Asia-Pacific, Africa, and South America | Long term (≥4 years) |

| Scalability challenges for bio-based wall materials | -0.9% | Global and early-stage impact | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Initial Manufacturing Costs of Microencapsulation

Building a commercial capsule plant demands dedicated reactors, precision droplet generators, and rigorous in-line analytics. Capital expenditure ranges USD 25-40 million, while operating costs run 20-30% above conventional pesticide lines due to high-grade polymers and stringent QC. Many manufacturers, therefore, target premium segments capable of paying 15-25% per-liter price premiums, leaving bulk commodity crops underserved. Continuous-processing pilots promise to shave 25-35% off production expense by 2027, yet near-term economics still force cautious capacity expansion.

Regulatory Ambiguity for Nano-Capsule Registration

Capsules under 100 nm are often subject to fragmented oversight. Europe’s Biocidal Products Regulation imposes nano-specific dossiers, costing USD 1-3 million per active substance, and can extend approval timelines by 18-36 months. Similar uncertainty surrounds proposed guidance in China and India, prompting several firms to sideline nano-programs despite superior biological performance. The Organisation for Economic Co-operation and Development (OECD) is piloting harmonized nano-test guidelines, yet universal uptake remains years away, keeping risk perceptions high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Herbicides Accelerate While Insecticides Dominate

In 2024, insecticides accounted for 46% of the microencapsulated pesticides market share, reflecting their central role in Integrated Pest Management (IPM) strategies, where prolonged residual control helps restrain resistant insect populations. Capsules enable flexible spray schedules, protect beneficial species, and align with residue rules in specialty crops. Herbicides, however, post the fastest 12.4% CAGR as conservation tillage demands season-long pre-emergence control without multiple passes. Precision-spray capsules address concerns about drift associated with glyphosate and other broad-spectrum actives, thereby extending their use window under regulatory scrutiny.

Broader portfolios also gain from multi-active capsules that combine insecticidal and fungicidal modes to tackle complex pest complexes in a single shot, as shown in Bayer AG’s 2024 field trials [2]Source: Bayer AG, “Multi-Active Field Trials,” bayer.com . Fungicides continue to experience steady uptake, especially in grapes and tree fruits, where capsules maintain surface protection during rain events. Nematicide, rodenticide, and Plant Growth Regulators (PGR) niches remain small but attractive for innovators using shell chemistry to modulate challenging actives.

By Technology: Fluidized-Bed Coating Gains Ground Against Polymer Leaders

Polymer coating retained 51.2% in the global microencapsulated pesticides market revenue share in 2024 as the baseline platform for high-volume actives, owing to mature continuous lines and broad polymer libraries. Yet fluidized-bed coating is charting an 11.5% CAGR because it yields narrower size distributions and fewer wall defects, which translates into more predictable release curves and lower rejection rates. The upgrade matters in premium horticulture where misfires hurt yields.

Polymer-encapsulated granules dominate soil-applied herbicides, especially in rice and sugarcane fields where waterlogging complicates foliar sprays. Interfacial polymerization and coacervation remain niche but indispensable for pH-sensitive biologicals. Across approaches, automated in-line NIR monitoring and digital twins are trimming scrap, pushing all technologies toward cost parity in the microencapsulated pesticides market.

By Crop: Fruits and Vegetables Drive Premium Growth

Cereals and grains accounted for 39.4% of the 2024 microencapsulated pesticides market size, given extensive acreage and established seed-treatment channels. Capsules slash early-season passes, cutting labor and fuel 40% in Midwest corn rotations. Fruits and vegetables, however, outpace the market with a 9.5% CAGR, as residue-free compliance is non-negotiable in export chains. California strawberry growers, for instance, rely on microencapsulated pyrethroids to meet European Union Maximum Residue Levels (MRLs) without yield losses.

Oilseeds and pulses utilize capsules to manage soilborne pests in reduced-tillage systems. Sugarcane and plantation crops in tropical zones increasingly demand granular capsules that withstand monsoon rains yet release actives slowly, ensuring season-long protection without reentry hazards.

By Capsule Size: Less than 50 µm Capsule Innovation Accelerates

Capsules measuring 50-250 µm remain mainstream at 57.1% of the microencapsulated pesticides market value, balancing pumpability with consistent coverage. They fit most tractor-boom filters and maintain homogeneous distribution in tank mixtures. Less than 50 µm capsules, however, are gaining 10.4% CAGR because they penetrate waxy leaf layers and biofilms, enabling rate reductions of 25-30% without efficacy loss. Nano-scale particles also improve rainfastness, critical in tropical monsoon zones.

Capsules more than 250 µm retain importance in soil granules used for nematode control or plantation-crop slow release. Recent process controls have achieved a coefficient-of-variation below 10%, ensuring field-level uniformity across all size classes, thereby strengthening user confidence in the microencapsulated pesticides market.

Geography Analysis

North America anchors the microencapsulated pesticides market with a 37.5% share in 2024, driven by early uptake of precision-spray rigs and EPA approvals that streamline controlled-release dossiers. Adoption curves flatten as the region matures, but upside continues through product replacement cycles and biodegradable shell upgrades. Field studies show 25-35% efficiency gains when capsules integrate with prescription maps.

The Asia-Pacific region grows at the fastest rate of 12.1% CAGR in the global microencapsulated pesticides market, driven by China’s USD 2 billion precision farming budget and India’s efforts to increase yields per hectare under strict Maximum Residue Levels (MRLs) for exports. Although capsule penetration lags at below 20%, climbing awareness and subsidy aid are turning the tide, especially in cotton, rice, and horticulture. Europe sustains with Green Deal mandates and circular-economy incentives that favor biodegradable walls [3].Source: European Commission, “Implementing Regulation 2025/152,” europa.eu In South America, the Middle East, and Africa, governments are inching upward as they weave sustainability grants into crop-protection schemes, yet price sensitivity continues to dampen smallholder uptake.

The microencapsulated pesticides market in South America is growing at a significant rate, driven by the region’s strong export-oriented agriculture and increasing need to comply with stringent international residue limits. Farmers in Brazil and Argentina, which together account for a significant share of global soybean, maize, and sugarcane exports, are adopting encapsulated formulations that release active ingredients in a controlled manner, reducing overall pesticide use and ensuring compliance with European Union and Asian market standards. In 2024, Brazil’s Ministry of Agriculture announced new incentives for precision farming technologies, including low-drift and controlled-release pesticide applications, which have prompted multinational firms such as BASF SE and Syngenta Group to expand their encapsulation-focused product portfolios in the region.

Competitive Landscape

The microencapsulated pesticides market is moderately consolidated, with the top five firms controlling around 46.8% market share in 2024. BASF SE leads with the strength of its formulation libraries and global warehousing footprint. Syngenta Group’s Zeon platform, recently upgraded to biodegradable shells, positions the firm for premium horticulture alleys. FMC Corporation’s USD 85 million purchase of AgroSpheres adds temperature-triggered polymers to its toolkit.

Rivalry intensifies as digital agriculture converges with chemistry. John Deere and Syngenta Group co-developed variable-rate algorithms that adjust capsule discharge on the fly, integrating hardware, software, and chemistry into a single ecosystem. Patent activity surpassed 200 filings in 2024, with a primary focus on bio-based walls, multi-active payloads, and sensor-responsive release triggers. Mid-size specialists exploit white space in biodegradable capsules and crop-specific blends, charging price premiums that compensate for scale gaps.

Sustainability credentials serve as key differentiators. BASF SE and Sumitomo secured third-party verifications of life-cycle emission cuts for new polymer lines, while Eden Research became the first to win biodegradable registration in Brazil. Market entrants must now pair efficacy data with environmental metrics to secure shelf space in tight procurement rosters.

Microencapsulated Pesticides Industry Leaders

BASF SE

Bayer AG

FMC Corporation

Syngenta Group

UPL Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: FMC Corporation and AgroSpheres collaborated to develop microencapsulation solutions for sustainable agriculture, focusing on biodegradable polymer systems that address environmental persistence concerns while maintaining controlled-release performance characteristics.

- October 2024: Syngenta Group has introduced INZAK ZEON, a new insecticide in Brazil, targeting sucking pests such as the brown stink bug and whitefly on soybeans, corn, cotton, and beans. It combines acetamiprid and lambda‑cyhalothrin in ZEON microencapsulated formulation, offering rapid knockdown and sustained residual control through gradual release. The systemic action via contact and ingestion aims to boost farmer profitability while supporting environmental management.

- July 2023: UPL Ltd obtained an exclusive, long-term global license from the University of Arkansas System Division of Agriculture for patented seed treatment technology that combines Fenclorim with micro-encapsulated herbicides. This technology protects rice and other grass crops from Group 15 herbicides while ensuring crop safety.

Global Microencapsulated Pesticides Market Report Scope

| Insecticides |

| Herbicides |

| Fungicides |

| Others |

| Polymer Coating |

| Polymer-Encapsulated Granules |

| Fluidized Bed Coating |

| Other Technologies |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Other Crops |

| Less than 50 µm |

| 50–250 µm |

| More than 250 µm |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Insecticides | |

| Herbicides | ||

| Fungicides | ||

| Others | ||

| By Technology | Polymer Coating | |

| Polymer-Encapsulated Granules | ||

| Fluidized Bed Coating | ||

| Other Technologies | ||

| By Crop | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Other Crops | ||

| By Capsule Size | Less than 50 µm | |

| 50–250 µm | ||

| More than 250 µm | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the microencapsulated pesticides market by 2030?

The microencapsulated pesticides market size is forecast to reach USD 850 million by 2030.

Which region grows fastest in the microencapsulated pesticides market?

Asia-Pacific posts the fastest growth at a 12.1% CAGR between 2025 and 2030.

Why are herbicidal capsules gaining traction?

Herbicidal capsules offer season-long residual control in conservation-tillage systems, driving a 12.4% CAGR.

How do biodegradable capsules improve sustainability metrics?

Capsules made from chitosan or alginate degrade within 90 days, slash microplastic risk, and pass regulatory reviews faster.

Page last updated on: