Household Insecticides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

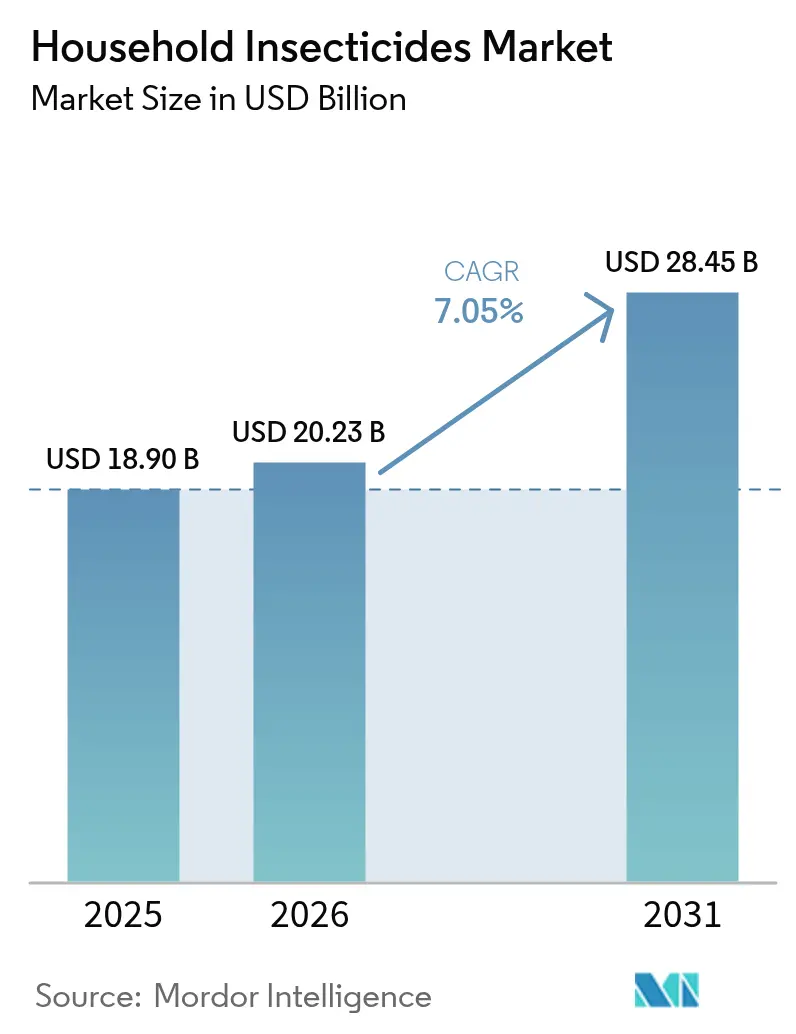

| Market Size (2026) | USD 20.23 Billion |

| Market Size (2031) | USD 28.45 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

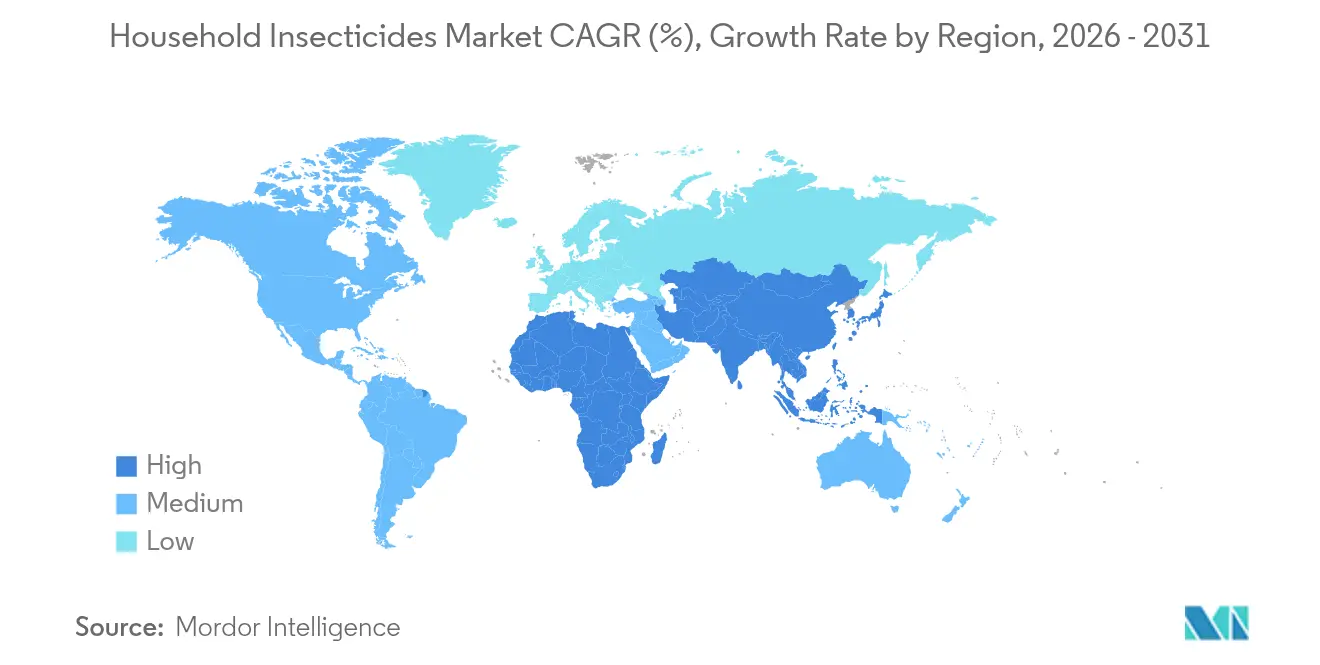

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

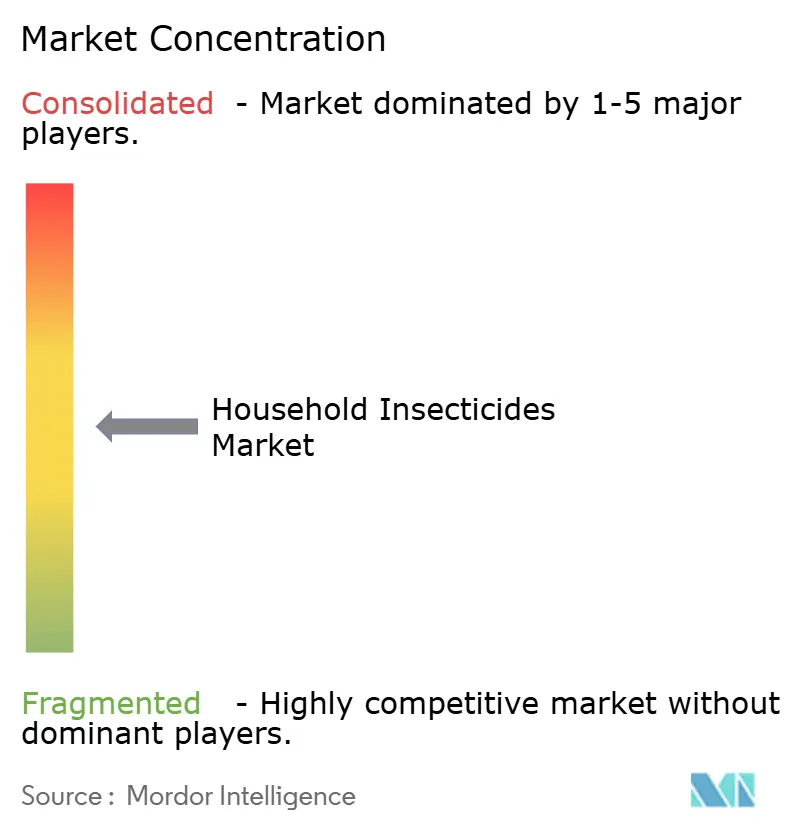

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household Insecticides Market Analysis by Mordor Intelligence

The household insecticides market size in 2026 is estimated at USD 20.23 billion, growing from 2025 value of USD 18.9 billion with 2031 projections showing USD 28.45 billion, growing at 7.05% CAGR over 2026-2031. Intensifying vector-borne disease outbreaks, rapid urbanization, and regulatory incentives for low-toxicity actives drive this expansion within the household insecticides market. Escalating dengue fever cases, which rose to 12.4 million in 2024, underscore the public health urgency that fuels premium demand for mosquito and fly control solutions[1]Source: World Health Organization, “Disease Outbreak News – Dengue Global Situation,” WHO, who.int. Regulatory agencies are expediting approvals for bio-based ingredients while tightening scrutiny on synthetic pyrethroids, prompting manufacturers to accelerate natural portfolio development[2]Source: U.S. Environmental Protection Agency, “Pesticide Registration,” EPA, epa.gov. Asia-Pacific holds the largest household insecticides market share at 40.0% due to dense cities that favor vector breeding, and the region’s players are debuting indigenous molecules to counter local resistance patterns. Meanwhile, e-commerce platforms widen global reach and enable data-rich, direct-to-consumer models that reward brands with strong digital engagement. Supply chain volatility in raw materials adds cost pressure, but premium outdoor living segments and smart IoT-enabled devices open new revenue pathways.

Key Report Takeaways

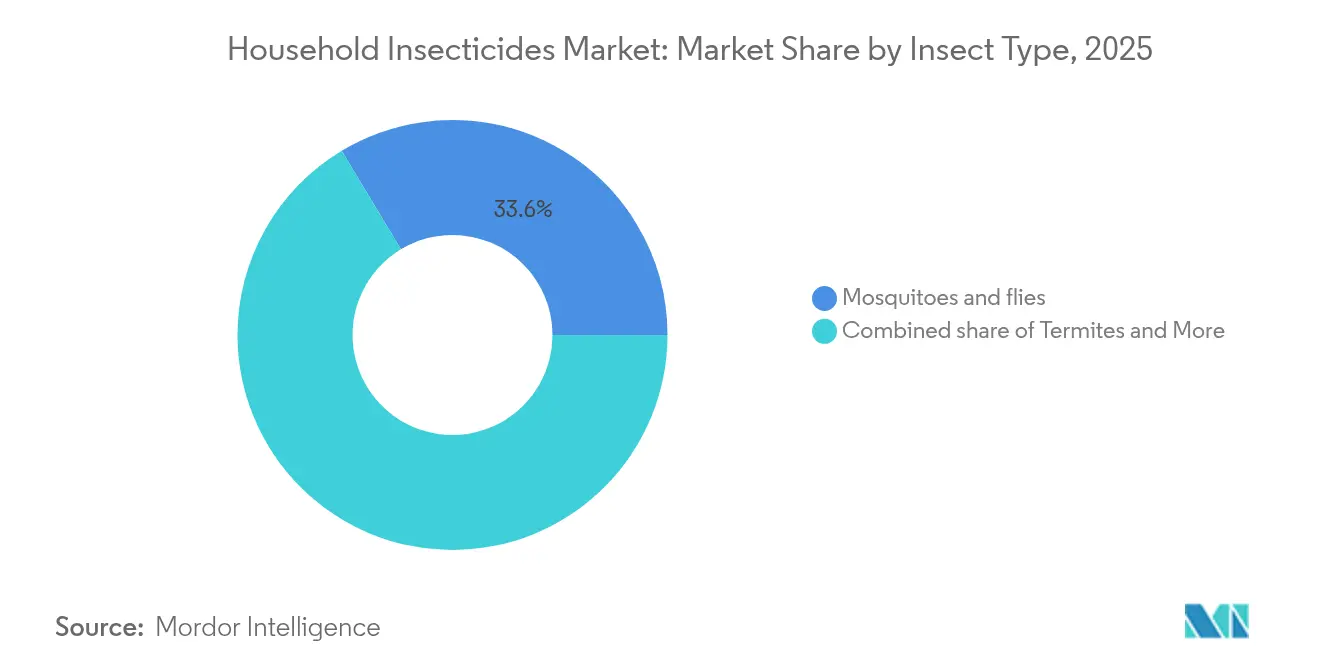

- By insect type, mosquitoes and flies led with 33.62% of the household insecticides market share in 2025. By insect type, bedbugs and beetles are advancing at a 9.41% CAGR through 2031.

- By chemical type, natural formulations commanded 51.35% share of the household insecticides market size in 2025 and are expanding at 8.42% CAGR.

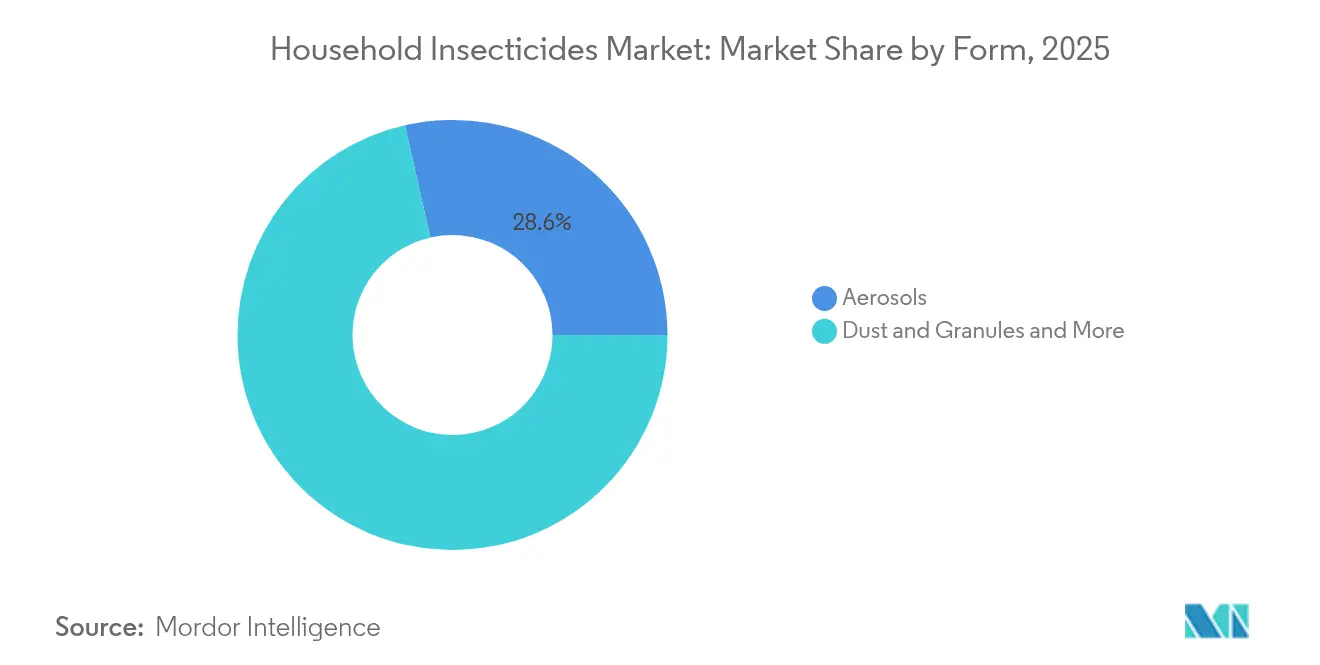

- By form, aerosol sprays retained a 28.55% share of the household insecticides market size in 2025, while creams and lotions exhibited the fastest growth at an 7.92% CAGR.

- Asia-Pacific accounted for 39.58 % of the revenue share of the household insecticides market size in 2025, and is projected to rise at a 7.12% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Household Insecticides Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of insect-borne diseases | +2.1% | Global, with peak impact in Asia-Pacific and Africa | Medium term (2-4 years) |

| Expansion of modern retail and e-commerce channels | +1.8% | North America and Europe are leading; Asia-Pacific is catching up | Short term (≤ 2 years) |

| Rapid urbanization and population density growth | +1.5% | Asia-Pacific core; spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Regulatory shift toward low-toxicity bio-based actives | +1.2% | North America and the EU are leading, with gradual global adoption | Medium term (2-4 years) |

| Emergence of smart/IoT-enabled insect-control devices | +0.8% | North America and developed Asia-Pacific markets | Long term (≥ 4 years) |

| Outdoor living trend boosting demand for patio/yard solutions | +0.7% | North America and Europe are primary; emerging in urban Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Insect-Borne Diseases

Dengue, malaria, and chikungunya outbreaks are surging far beyond historical baselines, making disease prevention the primary purchase trigger in the household insecticides market. Global dengue incidence jumped 230% from 2023 to 2024, propelling consumers toward continuous protection products that command premium price points. Climate change lengthens mosquito breeding seasons and expands Aedes aegypti into temperate zones, which opens new sales pockets in Europe and North America. Governments subsidize spray and coil purchases for vulnerable communities, especially in South America, where the dengue burden threatens economic productivity[3]Source: Brazilian Ministry of Health, “Dengue Surveillance Report 2024,” Government of Brazil, gov.br. Brands leveraging medical endorsements and scientific messaging enjoy stronger household penetration, as insecticides shift from convenience goods to essential health safeguards. Brazil’s record dengue year drove innovation in long-lasting formulations, reinforcing the link between epidemiological pressure and research and development focus.

Expansion of Modern Retail and E-commerce Channels

Digital platforms now outpace traditional hardware stores for do-it-yourself pest control. Amazon alone moved USD 1.3 billion of pest control products in Germany during 2024, dwarfing specialty retail volumes. Online availability elevates product transparency, letting challengers compete with incumbents through content-rich listings and review engines. Subscription models lock in replenishment, increasing customer lifetime value and smoothing demand seasonality in the household insecticides market. Data captured from clickstream and purchase histories guides targeted promotions and informs formulation tweaks. The channel shift accelerates cross-border expansion because brands bypass legacy wholesalers, although complex labeling laws still require localized packaging. Millennial and Gen Z shoppers lead the online cohort, purchasing insect repellents 60% more often via mobile than older consumers.

Rapid Urbanization and Population Density Growth

Urban centers with inadequate sanitation create persistent insect breeding sites, lifting per-capita consumption of sprays, coils, and vaporizer mats. United Nations studies show megacities above 10 million residents consume household insecticides at triple rural rates, driven by year-round heat island effects and dense housing[4]Source: UN-Habitat, “Urban Development and Pest Control Correlations,” United Nations, unhabitat.org. High-rise apartment complexes facilitate pest migration through vents and plumbing lines, bolstering demand for residual aerosol formulations. City dwellers pay premiums for odorless or low-smoke products that preserve indoor air quality. Informal settlements, where garbage management lags population growth, sustain constant vector pressure that eliminates seasonal dips in consumption. As more consumers occupy micro-apartments, compact delivery systems such as smart dispensers gain traction.

Regulatory Shift Toward Low-Toxicity Bio-based Actives

The Environmental Protection Agency’s streamlined pathway for natural ingredients trims time to market while stricter reviews on pyrethroids add testing layers that raise synthetic compliance costs by up to USD 100 million per molecule[5]Source: European Chemicals Agency, “REACH Registration Requirements,” ECHA, echa.europa.eu. European REACH regulations mirror this direction, compelling global players to maintain dual formulations or to pivot portfolios toward botanical extracts[6]Source: Environmental Health Perspectives, “Pyrethroid Exposure Studies,” National Institute of Environmental Health Sciences, ehp.niehs.nih.gov. Natural products attract 20-30% price premiums, offsetting typically lower kill rates relative to synthetics. Smaller botanical specialists partner with larger firms to leverage distribution muscle. Still, weaker intellectual property protection on naturally derived actives challenges long-term exclusivity, pushing companies to focus on delivery system patents and brand equity.

Restraints Impact Analysis of Household Insecticides Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global and national chemical regulations | -1.4% | Europe and North America are primary expanding globally | Medium term (2-4 years) |

| Health and environmental toxicity concerns | -1.1% | Global with the highest impact in developed markets | Short term (≤ 2 years) |

| Tariff-driven volatility in raw-material supply chains | -0.8% | Global impact, highest in import-dependent regions | Short term (≤ 2 years) |

| Rising pest resistance reducing product efficacy | -0.6% | Global, variant by pest species | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global and National Chemical Regulations

REACH registration fees and testing costs now exceed EUR 50 million (USD 54 million) annually for leading suppliers. Pyrethroid re-evaluations delay launches by up to two years. Smaller firms lack the capital to clear such hurdles, leading to potential consolidation and reduced innovation diversity. Divergent national rules force brands to maintain multiple formulations, pushing operational costs 15-20% higher than under harmonized regimes. The precautionary principle fuels uncertainty, making long-horizon research and development investments riskier.

Health and Environmental Toxicity Concerns

Peer-reviewed studies linking pyrethroid exposure to pediatric neuro issues gained mainstream media traction, slashing sales of certain aerosols by double digits. Social channels can amplify incomplete science, prompting retailers to de-shelve suspect items overnight. Brands respond with child-resistant packaging, updated safety labels, and influencer campaigns to rebuild trust, inflating marketing budgets by up to 30%. Natural products enjoy halo effects despite narrower efficacy windows, creating market distortion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Household Insecticides Market Segment Analysis

By Insect Type:

Disease Vectors Drive Market LeadershipMosquitoes and flies controlled 33.62% of the household insecticides market share in 2025, propelled by dengue and malaria fears and boosted by continuous spray and coil adoption. The household insecticides market size attributable to these vectors will maintain leadership as climate change widens endemic zones. Godrej’s renofluthrin launch directly tackles pyrethroid-resistant mosquitoes and underscores how vector pressure guides research and development focus. Bedbugs and beetles climb fastest at 9.41% CAGR because resurgent travel accelerates urban infestations; landlords in dense cities purchase residual aerosols to avert tenant turnover. Termite treatments remain regionally important in the tropics, sustaining premium pricing tied to property damage prevention. Rodent control plateaus but gains incremental volume in high-rise complexes where food waste collection lags, prompting hybrid bait and snap systems.

Consumer spending patterns reveal a hierarchy that favors health protection over property preservation. Vector control products tolerate 10–15% price premiums even when active ingredient costs are similar. Marketing increasingly highlights disease statistics to reinforce urgency. As travel rebounds, luggage-compatible bedbug sprays and laundry additives enter big box chains. Utility corridors in apartment towers serve as superhighways for cockroaches and ants, elevating demand for residual formulations and smart monitoring traps that alert maintenance staff before infestations spread building-wide.

By Chemical Type:

Natural Formulations Gain Regulatory AdvantageNatural formulations secured 51.35% of the household insecticides market share in 2025 and are set to expand at an 8.42% CAGR. The regulatory tailwind and consumer perception of safety partially offset efficacy gaps versus synthetics. Citronella remains the flagship but faces durability limits in heavy pest pressure, prompting blends with geraniol and lemongrass for wider spectrum coverage. Synthetic stalwarts such as DEET still dominate personal repellents but face stiff competition from picaridin thanks to better odor and fabric compatibility. Pyrethroids endure heavier compliance costs and negative press, yet remain essential for severe infestations. The household insecticides market size for synthetics may shrink modestly, but will persist due to performance advantages in professional settings.

Manufacturers seek compromise through hybrid formulations that combine rapid-knockdown synthetic actives with natural synergists to lower total load. Delivery innovation also improves naturals. Micro-encapsulation extends citronella vapor release, giving six-hour protection in laboratory tests. Firms invest in botanical supply chains, securing vertical integration to hedge raw material volatility and guarantee consistent terpene profiles.

By Form:

Aerosol Innovation Sustains Market LeadershipAerosols retained 28.55% of the household insecticides market size in 2025 due to one-hand convenience, broad availability, and continual nozzle technology upgrades that improve spray plume geometry and reduce propellant volume. Smart dispensers such as Godrej’s HIT Spray Matic pair Bluetooth timing algorithms with traditional canisters to curb overuse without sacrificing kill rate. Creams and lotions rise fastest at 7.92% CAGR because consumers favor targeted skin applications for outdoor activities, reinforced by the outdoor living trend. Dusts and granules become niche as consumers shy away from messy indoor treatments. Liquids stay relevant in professional services and refill stations. Coils dominate humid Asian evenings despite smoke concerns, while vaporizer mats capture consumers seeking plug-and-play overnight protection. Electronic ultrasonic devices hold niche appeal amid inconsistent efficacy evidence, yet gain in pet-friendly households seeking chemical-free alternatives.

Aerosol sustainability pressures are triggering propellant shifts from hydrofluorocarbons to hydrofluoroolefins and compressed air. Packaging designers explore post-consumer recycled aluminum to offset tariff impacts. Portable devices for travel use USB-C charging to match electronics ecosystems. Lotion makers integrate moisturizers and SPF additives to broaden utility. Delivery format choice increasingly hinges on lifestyle fit and regional infrastructure; vaporizer mats need reliable electricity, whereas coils serve off-grid rural users. Retailers highlight form-factor variety through planogram segmentation, aiding shopper navigation and upselling combination packs for layered protection.

Geography Analysis

APAC Household Insecticides Market

Asia-Pacific commanded a 39.58% share of the household insecticides market size in 2025 and is projected to rise at a 7.12% CAGR driven by megacity sprawl, high disease burden, and year-round warmth. India leads volume as Godrej pioneers indigenous actives and leverages vast distribution across general trade outlets. China’s expanding middle class channels spending into premium natural coils and smart devices, while Japan’s Earth Corporation sustains dominance through patented cockroach baits and recorded sales of JPY 139 billion (USD 930 million) in 2024 EARTH.JP. Southeast Asia shows the fastest incremental growth owing to government dengue campaigns that subsidize aerosol purchases.

North America Household Insecticides Market

The United States sees naturals encroaching on synthetic market share amid heightened chemical scrutiny, yet DEET remains entrenched for camping and hiking. Canada’s stricter labeling laws slow new product launches but reinforce consumer trust in approved brands. Mexico emerges as a high-growth pocket as dengue spreads northward and retail infrastructure modernizes. Regional e-commerce penetration above 40% makes direct-to-consumer subscriptions the norm for urban households.

Europe Household Insecticides Market

REACH compliance burdens and shorter pest seasons in temperate zones restrain Europe's market expansion. Southern Europe, from Spain to Greece, exhibits higher per-capita usage due to extended summers. Germany leads unit sales through DIY chains and online platforms, whereas the United Kingdom market pivots heavily toward pet-safe fume-free sprays following high press coverage of asthma concerns.

Competitive Landscape

The household insecticides market remains moderately concentrated as the top five players capture the majority share in market revenue. SC Johnson has a leading share in the market owing to the company's diversified product range and further investment of USD 100 million over ten years in malaria prevention manufacturing in Kenya, signaling a bet on emerging markets.

Reckitt Benckiser’s intention to divest Mortein by 2025 could reshuffle rankings and attract private equity or regional specialists. Godrej leverages local research and development to release renofluthrin and IoT dispensers, solidifying leadership in South Asia. Earth Corporation dominates Japan with a major share in cockroach traps and maintains aggressive patent filings. Spectrum Brands gains EPA approval for a longer shelf-life pyrethroid, aiding retail relationships.

Innovation intensity rises as patents for novel actives and delivery hardware climb 40% since 2024. Bio-based specialists strike licensing deals with conglomerates to scale faster, while giants acquire regional distributors to fortify last-mile reach, exemplified by Rollins acquiring Clark Pest Control in November 2024. Supply chain resilience becomes a differentiator; firms with dual sourcing or local manufacturing hedge tariff shocks better. Marketing budgets pivot toward digital storytelling to win over skeptical consumers, highlighting lab data and medical endorsements. Competitive pivots emphasize smart devices and preventative subscription models to lock in recurring revenue and valuable usage data.

Household Insecticides Industry Leaders

SC Johnson & Son, Inc. (private)

Reckitt Benckiser Group plc

Godrej Consumer Products Ltd. (Godrej Group)

Spectrum Brands Holdings, Inc.

Sumitomo Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Household Insecticides Market Companies Covered in this Report

- SC Johnson & Son, Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Ltd.

- Spectrum Brands Holdings, Inc.

- Sumitomo Chemical Co., Ltd.

- Henkel AG & Co. KGaA (Combat)

- Bayer AG

- BASF SE

- FMC Corporation

- Central Garden & Pet Company

- Rentokil Initial plc

- Rollins, Inc.

- Ecolab Inc.

- UPL Limited

- Dabur India Limited

Recent Industry Developments in Household Insecticides Market

- March 2025: BASF invested EUR 25 million (USD 27 million) to expand German production of bio-based actives, answering European natural demand.

- December 2024: Earth Corporation reported household product sales of JPY 139 billion (USD 930 million), sustaining a 90% share in Japanese cockroach traps through new actives.

- September 2024: Godrej Consumer Products launched HIT Spray Matic smart dispenser with IoT connectivity, the first of its kind in India.

Global Household Insecticides Market Report Scope

Home insecticides are products used to kill or control insects within and around the home. They are typically used to control common household pests such as ants, roaches, spiders, and flies. Home insecticides come in various forms, such as sprays, baits, powders, and traps, and are formulated with different active ingredients that target specific types of insects.

The household insecticides market is segmented by insect type into mosquitoes and flies, termites, bedbugs and beetles, and other insect types, by chemical type into synthetic and natural, by form into dust and granules, liquids, aerosol sprays, and other forms, and by geography into North America, Asia-Pacific, Europe, South America, and Africa. The market sizing is provided in value terms (USD) for all the above-mentioned segments.

Segmentation Overview

| Mosquitoes and Flies |

| Rats and Other Rodents |

| Termites |

| Bedbugs and Beetles |

| Other Insect Types |

| Synthetic | DEET |

| Picaridin | |

| Other Synthetic Chemicals | |

| Natural | Citronella Oil |

| Geraniol Oil | |

| Other Natural Oils |

| Dust and Granules |

| Liquids |

| Aerosol Sprays |

| Coils and Vaporizers |

| Creams and Lotions |

| Other Forms |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Insect Type (Value) | Mosquitoes and Flies | |

| Rats and Other Rodents | ||

| Termites | ||

| Bedbugs and Beetles | ||

| Other Insect Types | ||

| By Chemical Type (Value) | Synthetic | DEET |

| Picaridin | ||

| Other Synthetic Chemicals | ||

| Natural | Citronella Oil | |

| Geraniol Oil | ||

| Other Natural Oils | ||

| By Form (Value) | Dust and Granules | |

| Liquids | ||

| Aerosol Sprays | ||

| Coils and Vaporizers | ||

| Creams and Lotions | ||

| Other Forms | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current global value of the household insecticides market?

The household insecticides market size is estimated at USD 20.23 billion in 2026 and is projected to hit USD 28.45 billion by 2031.

Which region leads in household insecticide consumption?

Asia-Pacific holds 39.58% of global revenue thanks to dense urban populations and year-round vector pressure.

How is technology reshaping pest control at home?

Smart IoT traps and automated dispensers enable real-time monitoring and targeted spraying, cutting chemical use while improving efficacy.

What challenges stem from raw material supply chains?

Tariffs and currency swings create double-digit cost volatility for key actives such as benzalkonium chloride, squeezing margins and prompting sourcing diversification.

Page last updated on: