Carbamate Insecticide Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 320 Million |

| Market Size (2030) | USD 391 Million |

| Growth Rate (2025 - 2030) | 4.10% CAGR |

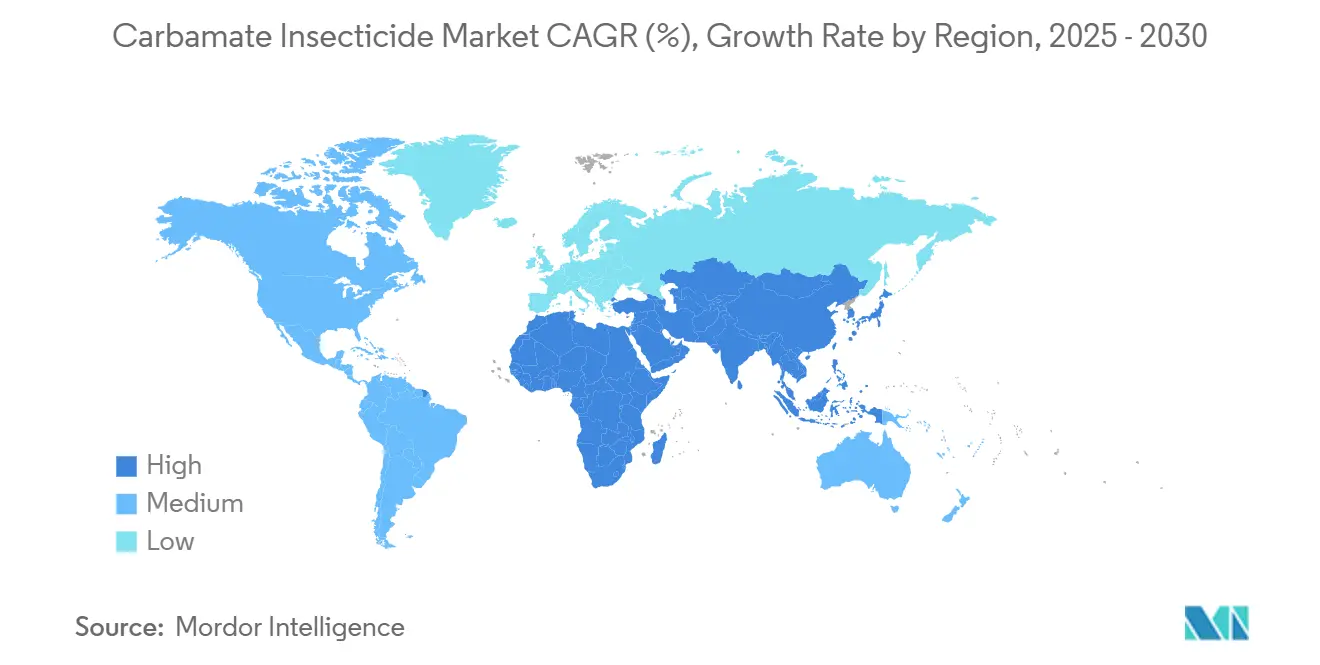

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

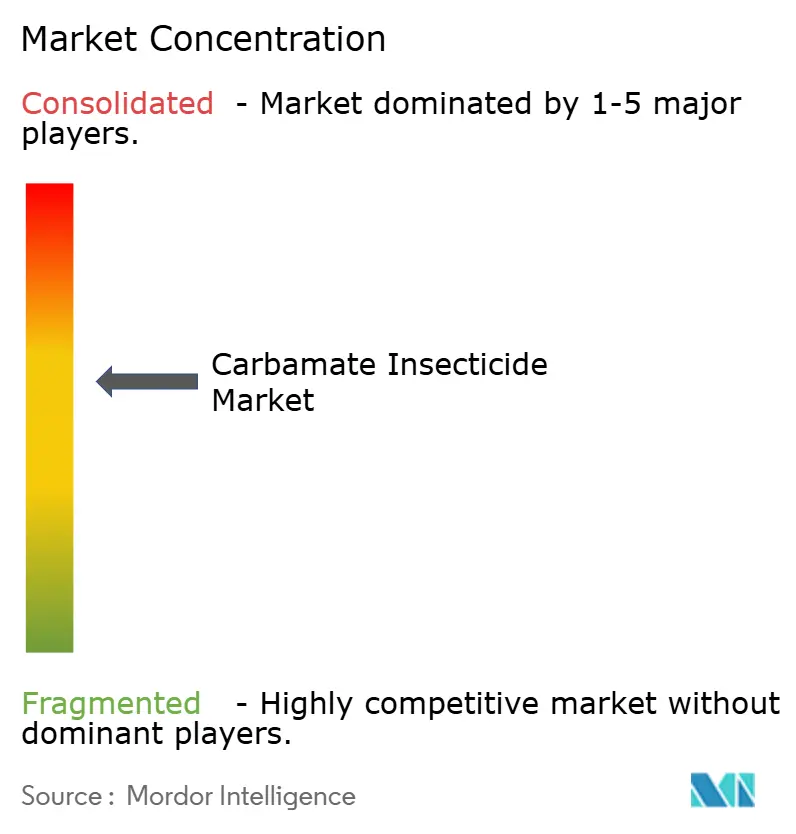

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbamate Insecticide Market Analysis by Mordor Intelligence

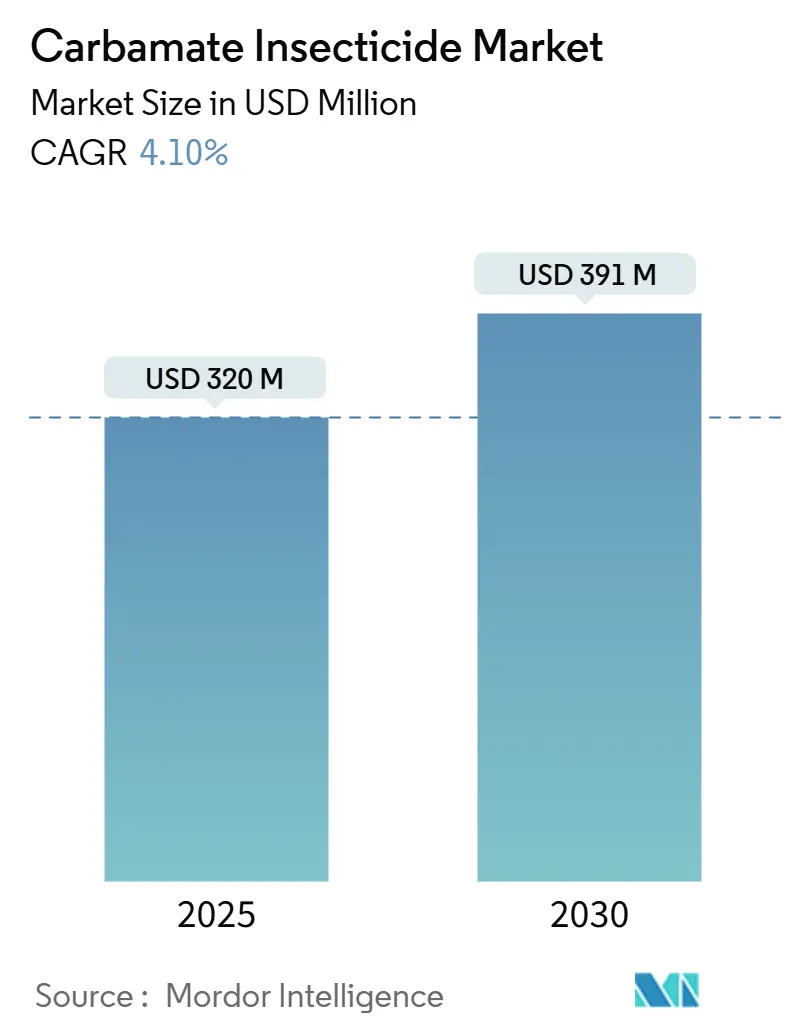

The carbamate insecticide market size is USD 320 million in 2025 and is forecast to reach USD 391 million by 2030, advancing at a 4.1% compound annual growth rate (CAGR). Within this growth path, emergency stockpiling for desert locust control, the mainstreaming of Integrated Pest Management (IPM) programs across major grain economies, and rapid uptake of drone-enabled ultra-low-volume spraying anchor near-term demand. Longer-term expansion is tied to N-methyl carbamate innovations that enhance target specificity and reduce environmental persistence, investor interest in nano-encapsulation technologies, and sustained government funding for food-security pesticide reserves in Africa and the Middle East. Competitive intensity is rising as leading firms bundle chemical efficacy with digital agronomy and precision-application services, while medium-sized regional manufacturers leverage fast regulatory approvals to fill localized supply gaps. The carbamate insecticide market continues to benefit from its role as an essential rotation partner in resistance-management schemes that protect the longevity of newer active-ingredient classes.

Key Report Takeaways

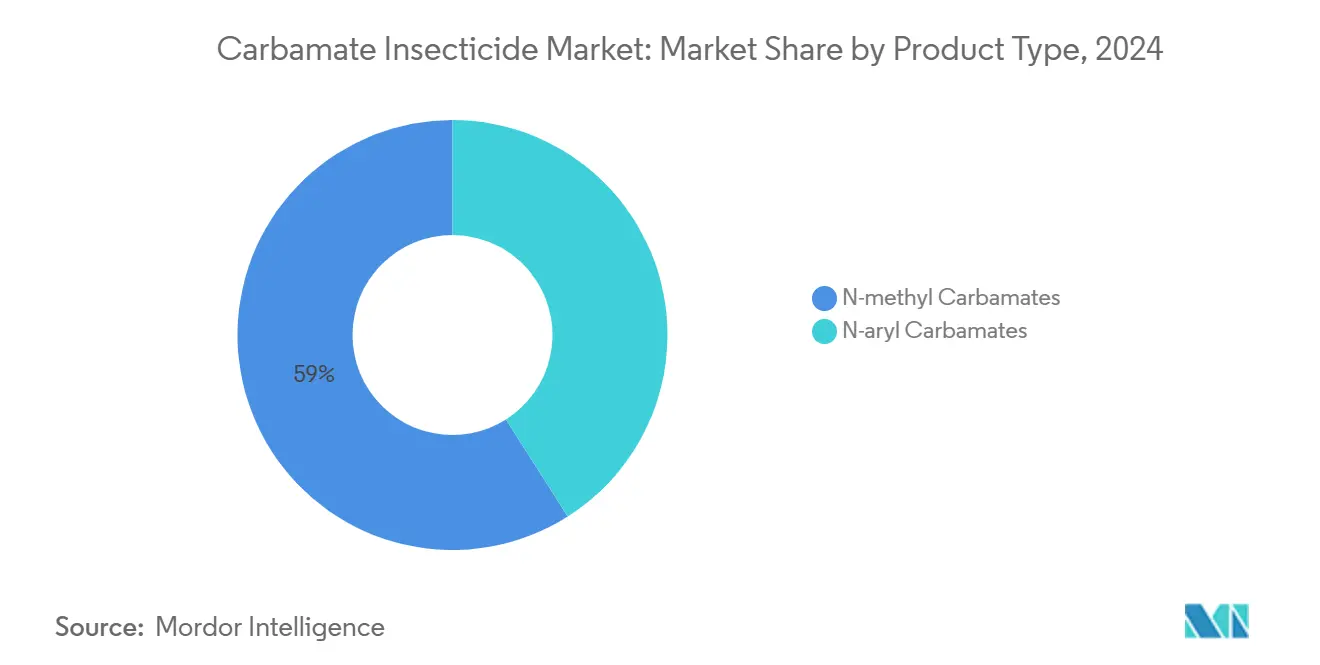

- By product type, N-methyl carbamates commanded a 59.0% carbamate insecticide market share in 2024 and are projected to register a 6.4% CAGR to 2030.

- By crop type, fruits and vegetables captured 38.5% of the carbamate insecticide market in 2024, while the oilseeds and pulses are set to grow the fastest at a 5.9% CAGR through 2030.

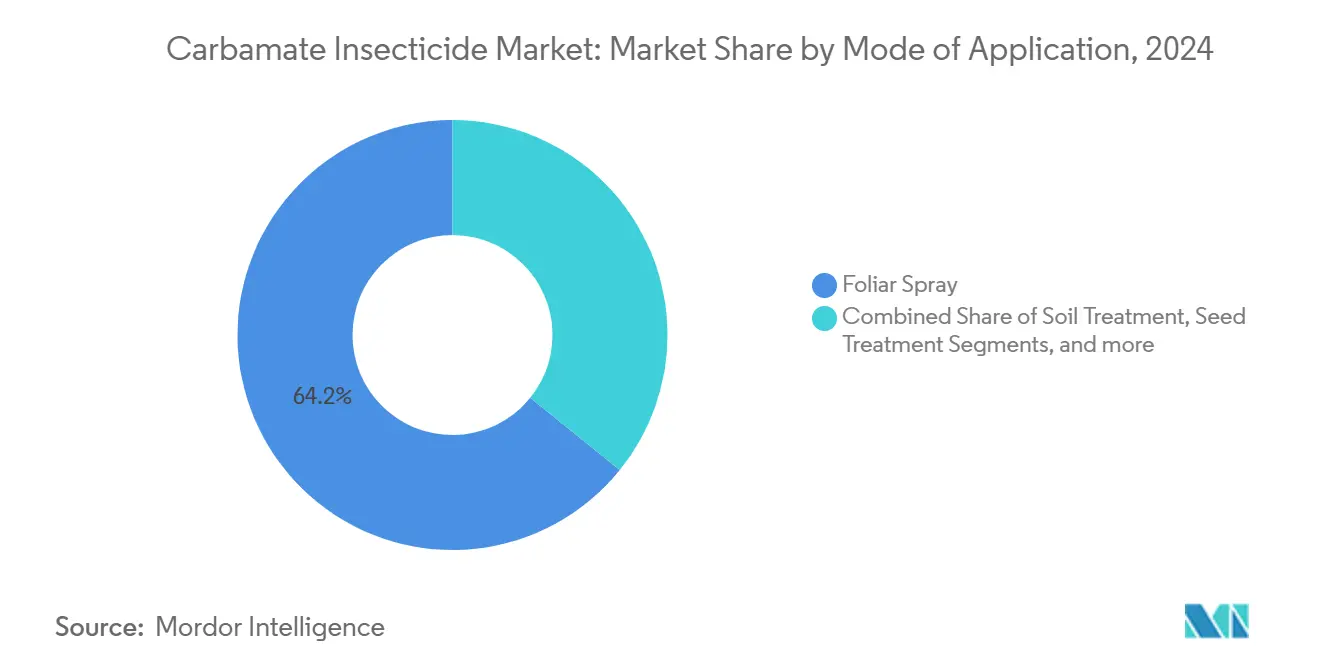

- By mode of application, foliar spray dominated delivery with 64.2% share of the carbamate insecticide market size in 2024, whereas seed treatment is forecast to expand at a 7.4% CAGR between 2025 and 2030.

- By geography, Asia-Pacific accounted for the largest market share of 44.0% of the carbamate insecticide market in 2024, and the Middle East is advancing at a 5.5% CAGR, making it the fastest-growing geography to 2030.

- Bayer AG, BASF SE, Syngenta Group, FMC Corporation, and UPL Limited collectively held 67.2% of the market share in 2024, indicating a moderately concentrated competitive landscape.

Global Carbamate Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Resistance-Management Requirements from Key Manufacturers Led Stewardship Programs | +1.2% | North America and Asia-Pacific, with spill-over globally | Medium term (2-4 years) |

| Rapid Expansion of Integrated Pest Management (IPM) Acreage in Asia-Pacific Cereals and Grains | +0.9% | Asia-Pacific, with influence in Africa and South America | Long term (≥ 4 years) |

| Emergence of Proprietary Oxime-Carbamate Combinations for Seed Treatment in Soybeans | +0.7% | North America and South America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Adoption of Drone-Enabled Ultra-Low-Volume Foliar Spraying in Field Crops | +0.6% | South America, pilot trials in Asia-Pacific | Short term (≤ 2 years) |

| Resurgent Locust Outbreaks in Eastern Africa and the Middle East Accelerating Emergency Pesticide Stockpiles | +0.5% | Africa and the Middle East, global supply implications | Short term (≤ 2 years) |

| R&D Breakthroughs in Nano-Encapsulated Methomyl Formulations Reducing Mammalian Toxicity | +0.4% | Developed markets first, global adoption later | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Resistance-Management Requirements from Key Manufacturers Led Stewardship Programs

Manufacturer-led stewardship programs now integrate carbamate rotation protocols that slow target-site resistance, allowing growers to preserve the efficacy of other chemistries by at least three years[1]Source: Insecticide Resistance Action Committee, “Mode of action classification 2025,” irac-online.org. Structured rotation elevates predictable reorder cycles for carbamates and positions suppliers as partners in sustainable agriculture solutions. Extension agencies in the United States require documented rotation plans for subsidy eligibility, creating institutional pull for carbamate usage that offsets price erosion in commodity pesticide markets. Research funded by the United States Department of Agriculture (USDA) shows that cotton fields applying carbamates within rotation strategies recorded 18% lower resistance allele frequencies in Helicoverpa armigera populations than fields relying solely on pyrethroids[2]Source: United States Department of Agriculture, “Integrated pest management monitoring report 2025,” usda.gov. Leading manufacturers provide digital rotation planners and in-season resistance surveillance, locking in customer loyalty and reinforcing premium positioning in the carbamate insecticide market.

Rapid Expansion of Integrated Pest Management (IPM) Acreage in Asia-Pacific Cereals and Grains

Government-funded IPM programs in China, India, and Vietnam encourage selective carbamate use as biological-friendly “clean-up” sprays that complement parasitoid releases and pheromone traps. The Food and Agriculture Organization (FAO) reports that rice growers under its Regional Pest Control initiative reduced overall pesticide load by 25% while maintaining yields when carbamates replaced organophosphates in rotation schedules. Precision weather prediction platforms notify growers of pest pressure windows, prompting timely carbamate applications that optimize efficacy and minimize non-target impacts. Subsidies for IPM adoption in Indonesia cover up to 40% of the carbamate purchase cost, expanding the addressable base for branded suppliers. This structural policy support ensures sustained volume growth in Asia-Pacific, the largest demand center within the carbamate insecticide market.

Emergence of Proprietary Oxime-Carbamate Combinations for Seed Treatment in Soybeans

Patent-protected seed coatings combining oxime carbamates with systemic fungicides extend early-season protection from 21 days to 45 days, justifying a 15-20% price premium over generic seed treatments. The United States Environmental Protection Agency (EPA) approved Acceleron 26FI in October 2024, validating regulatory pathways for multi-mode formulations. Soybean acreage adopting treated seeds across the Midwest reached 32 million hectares in 2024, lifting baseline demand for oxime carbamates. Multinational grain exporters now specify treated seed protocols to secure consistent emergence, creating pull-through demand in Brazil and Argentina. Seed treatment’s double-digit margin profile attracts formulators seeking insulation from post-patent price compression in foliar carbamate products.

Adoption of Drone-Enabled Ultra-Low-Volume Foliar Spraying in Field Crops

Brazilian sugarcane producers using unmanned aerial vehicles (UAVs) lowered carbamate volumes by 30% yet retained equivalent pest knockdown compared to tractor-mounted boom sprayers, according to field trials published in Frontiers in Nutrition. Application cost per hectare fell from USD 15.4 to USD 8.9, improving grower return on investment and accelerating technology adoption. Drift-reducing adjuvants optimized for UAVs bring environmental benefits that satisfy tightening application buffer regulations. South America’s rapid uptake is spilling into Thailand’s cassava sector, where pilot projects cover 12,000 hectares with ultra-low-volume carbamate regimes. Formulators that tailor droplet-size profiles for electric drone nozzles gain a first-mover advantage in this fast-scaling delivery channel within the carbamate insecticide market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Regulatory Phase-Outs in the European Union and Canada | -1.1% | Europe and North America, spill-over globally | Short term (≤ 2 years) |

| Growing Pest Resistance to First-Generation N-Methyl Carbamates | -0.8% | Intensive agriculture regions worldwide | Medium term (2-4 years) |

| Supply Disruptions of Key Intermediates (Methyl Isocyanate) From China Specialty-Chemical Plants | -0.6% | Global manufacturing footprint | Short term (≤ 2 years) |

| Investor-Led ESG Divestment from High-Toxicity Chemistries, Limiting Capital for New Facilities | -0.4% | Developed capital markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Regulatory Phase-Outs in the European Union and Canada

The revised Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) Annex XVII list, effective September 2025, tightens carcinogenic, mutagenic, and reproductive toxin thresholds that several carbamates fail to meet. Parallel amendments to Canada’s Pest Control Products Act align Maximum Residue Limits (MRLs) with stricter European levels, compelling multinational suppliers to withdraw or reformulate products. The European Union exported 81,615 metric tons of pesticides banned domestically in 2022, a practice that will cease under a 2025 export-ban regulation. Reformulation costs divert R&D budgets from new-mode chemistry, potentially slowing innovation. Regional producers able to upgrade toxicology profiles swiftly will exploit vacated shelf space, but overall volumes in the carbamate insecticide market face near-term contraction.

Growing Pest Resistance to First-Generation N-Methyl Carbamates

Field monitoring in Vietnam and Thailand showed that brown planthopper populations exhibited 45% lower sensitivity to carbofuran in 2024 compared to 2010 baselines[3]Source: MDPI Editors, “Field resistance in rice planthopper populations,” mdpi.com. Cross-resistance to oxydemeton-methyl compounds reduces rotation options, forcing growers to adopt expensive insect growth regulators. Resistance management protocols limit application frequency to two sprays per season, curbing volume throughput for generic N-methyl carbamates. Multinational companies intensify extension services and farm-level diagnostics to protect existing product franchises, yet efficacy erosion remains a structural drag on carbamate insecticide market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: N-Methyl Carbamates Sustain Leadership Through Broad-Spectrum Utility

N-methyl carbamates captured 59.0% of the carbamate insecticide market share, while growing at a CAGR of 6.4% through 2030. Their dominance as the primary sub-class within this chemical group stems from broad-spectrum efficacy, rapid pest knockdown, and low production costs, making them essential for large-acreage crop protection, particularly in row crops such as maize, sugarcane, cotton, and paddy. The compounds maintain a strong presence in Asia-Pacific, South America, and Sub-Saharan Africa, where farmers depend on cost-effective solutions to control economically damaging pests like borers, cutworms, planthoppers, and beetles. Key active ingredients include carbaryl, carbofuran, and methomyl, which have established registration portfolios and extensive distribution networks. The manufacturing of N-methyl carbamates benefits from efficient processes and existing infrastructure, enabling producers to maintain competitive volumes despite stricter regulatory requirements.

N-aryl carbamates occupy a low-volume, high-value segment focused on precision pest control in horticulture, floriculture, and controlled-environment agriculture (CEA). Their market share remains modest but consistent, supported by their selective mode of action, which aids resistance management strategies in crops such as tomatoes, cucumbers, grapes, and greenhouse vegetables. Growth in this segment concentrates in regions with strict MRL (maximum residue limit) enforcement and export-oriented value chains, particularly in Southern Europe, Israel, and specific United States specialty crop regions such as California's Central Valley. N-aryl carbamates integrate effectively within IPM protocols, complementing biologicals and reducing chemical usage while maintaining control effectiveness.

By Crop Type: Fruits and Vegetables Command Largest Share

Fruits and vegetables accounted for 38.5% of the carbamate insecticide market share in 2024, reflecting growers' willingness to invest in the shape and color perfection required by fresh-produce buyers. Strict retailer residue specifications favor carbamates over organophosphates, keeping demand firm despite competition from biologicals. Oilseeds and pulses represent the fastest-growing segment at a 5.9% CAGR, driven by global protein demand and the expansion of soybean acreage in Brazil and India, which leads to input intensification. Cereals and grains form a substantial yet mature foundation. Their role shifts toward precision resistance management rather than volume front-line defense.

The Food and Agriculture Organization’s fall armyworm advisories promote carbamate spot treatments in maize, offering targeted spray opportunities that support margin protection [4]Source: Food and Agriculture Organization, “Fall armyworm management guide 2024,” fao.org . In cotton and sugarcane, application frequency correlates with pest flare-ups tied to climate anomalies, creating episodic demand surges. Locally important crops such as cacao and mangoes in West Africa and Southeast Asia attract specialized carbamate formulations, enabling suppliers to exploit premium niches outside mainstream commodity systems.

By Mode of Application: Foliar Spray Transform Delivery

Foliar spray maintained a 64.2% portion of the carbamate insecticide market size in 2024 due to its entrenched equipment base and broad label coverage. Yet seed treatment is expanding at a 7.4% CAGR as early-season seedling protection minimizes stand losses in soybeans, corn, and pulses. Drone-enabled ultra-low-volume foliar spraying marries spray accuracy with cost savings, driving adoption in aerial-application-friendly geographies such as Brazil, Argentina, and Thailand. Soil treatments and post-harvest fumigation occupy specialized roles where the systemic activity or rapid knockdown of carbamates is uniquely valuable.

Environmental Protection Agency (EPA) approvals of stacked-active seed treatments validate regulatory confidence in sophisticated chemistries, encouraging further investment. Adoption barriers include initial capital expenditure for treatment equipment. Custom-treated seed offerings bypass on-farm investment requirements. Application-method diversity affords formulators multiple revenue streams, insulating them from single-channel demand volatility and strengthening their strategic footprint inside the carbamate insecticide market.

Geography Analysis

The Asia-Pacific region held the largest share of the carbamate insecticide market at 44.0% in 2024, primarily due to extensive cultivation of rice, cotton, and horticultural crops. Subsidized IPM adoption, high pest pressure, and supportive government procurement keep baseline volumes robust. China’s Regional Pest Control initiative reported a 25% pesticide cost reduction alongside stable yields from 2014 to 2024 once carbamates replaced organophosphates within rotations, reinforcing structural demand. India registered 416 pesticide agendas in the first half of 2024, of which 48 involved carbamate actives, demonstrating ongoing regulatory openness.

The Middle East logs the fastest forecast CAGR at 5.5% as desert locust surveillance and crop expansion programs in Saudi Arabia and Turkey heighten emergency preparedness budgets. Locust breeding-hotspot monitoring around the Red Sea prompts forward carbamate purchases that can represent a year’s supply executed within a six-week window, creating periodic demand peaks. Precision irrigation and drone spraying platforms enable dosage optimization under arid conditions, making premium formulations economically viable.

North America remains a mature yet strategically important market, where environmental regulations are driving demand toward low-toxicity oxime carbamates. The United States Environmental Protection Agency requires endangered-species mitigation labeling on carbaryl by August 2025, introducing compliance costs but also granting label exclusivity to companies that meet new buffer-zone requirements. South America expands briskly through Brazil’s adoption of drone applications in sugarcane and soybean systems, while Africa’s demand profile tracks locust response funding cycles and commercialization of large-scale farming enterprises from Nigeria to Kenya. In Europe, most carbamate insecticides are banned under European Union regulations, with remaining market activity largely confined to Russia. Across regions, local regulatory frameworks, climatic variability, and crop-mix evolution shape nuanced growth patterns within the carbamate insecticide market.

Competitive Landscape

The top five manufacturers control 67.2% of the global revenue, indicating a moderately concentrated competitive landscape for the carbamate insecticide market. Bayer AG leads through its extensive seed-treatment offerings and integration of digital agronomy platforms. BASF SE maintains a strong position, supported by sustained investment in active-ingredient innovation, backed by an annual R&D budget of EUR 900 million (approximately USD 973 million). Syngenta Group has strengthened its foothold with its 2024 acquisition of DuPont Professional Products. UPL Limited and FMC Corporation complete the top tier, leveraging strategic acquisitions and localized manufacturing capabilities.

Competitive differentiation is shifting toward formulation technology and service bundling. Drone-compatible products, nano-encapsulated actives, and digital decision-support tools strengthen customer retention and premium positioning. FMC Corporation’s 2024 divestiture of Global Specialty Solutions for USD 350 million enabled reinvestment in biological partnerships, such as its distribution agreement with Ballagro Agro Tecnologia Ltda. for fungi-based crop protection. Albaugh Europe’s takeover of Industrias Afrasa expanded Mediterranean reach with 350 registered products, positioning the company to exploit upcoming European generic gaps created by REACH phase-outs.

Patent filings for synergistic carbamate-phosphonate blends grew by 18% year-on-year, reflecting sustained innovation despite genericization pressures. Mid-tier firms like Coromandel International Limited and Sipcam Oxon SpA invest in capacity expansions and geographical acquisitions to hedge regulatory risk and capture growth in Africa and Eastern Europe. ESG scrutiny accelerates the shift toward safer formulations, rewarding companies with transparent sustainability metrics and advanced toxicology data. Competitive interplay therefore hinges on a dual mandate: meeting evolving regulatory demands while delivering agronomically superior and cost-efficient solutions for growers seeking risk mitigation in pest-management programs.

Carbamate Insecticide Industry Leaders

BASF SE

FMC Corporation

UPL Limited

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: According to the Food and Agriculture Organization, Asian rice output is projected to increase by approximately 0.9% in 2025, contributing to a global cereal production rise of 3.4%, primarily driven by Asia. This increase supports higher application of carbamates in intensive farming systems across the region.

- May 2025: India is projected to achieve harvests of 149 million metric tons of rice and 117.5 metric tons of wheat, according to Indian government estimates. This production increase drives the usage of broad-spectrum carbamates (such as carbaryl and methomyl) for crop protection.

- September 2024: Sulfoxamyl, an oxime carbamate active ingredient developed by Ningxia HugeRise Chemical Co., Ltd., received provisional approval from ISO for its common name, with final approval anticipated in early 2025. The pesticide targets nematode control applications.

- August 2024: The California Department of Pesticide Regulation classified carbaryl as restricted-use effective August 1, 2025, impacting over 190 residential products.

Global Carbamate Insecticide Market Report Scope

Carbamate insecticides are chemical pesticides that target and control insect pests by inhibiting their nervous systems, commonly used on crops such as cereals, fruits, and vegetables for broad-spectrum protection. The Carbamate Insecticide Market Report is segmented by product type (N-Methyl Carbamates and N-Aryl Carbamates), by crop type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables and Other Crops), by mode of application (Foliar Spray, Soil Treatment, Seed Treatment, and Post-Harvest Fumigation), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| N-methyl Carbamates |

| N-aryl Carbamates |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Other Crops |

| Foliar Spray |

| Soil Treatment |

| Seed Treatment |

| Post-Harvest Fumigation |

| North America | United States |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Russia |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | N-methyl Carbamates | |

| N-aryl Carbamates | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Other Crops | ||

| By Mode of Application | Foliar Spray | |

| Soil Treatment | ||

| Seed Treatment | ||

| Post-Harvest Fumigation | ||

| By Geography | North America | United States |

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Russia | |

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the carbamate insecticide market in 2025, and what is its growth outlook?

The carbamate insecticide market size is USD 320 million in 2025 and is projected to reach USD 391 million by 2030, reflecting a 4.1% CAGR.

Which product category is growing fastest within carbamate insecticides?

N-methyl carbamates are expanding at a 6.4% CAGR through 2030 due to their broad-spectrum efficacy, rapid pest knockdown, and low production costs.

Why is Asia-Pacific the leading region for carbamate demand?

Intensive rice and horticulture systems, government-sponsored IPM programs, and high pest pressure keep Asia-Pacific the largest consumer of carbamate products.

What factors constrain carbamate growth in Europe?

Accelerated phase-outs under the European Union’s REACH Regulation and stricter residue limits reduce market access and force reformulations.

How are drone applications influencing carbamate usage?

Unmanned aerial vehicles enable ultra-low-volume spraying that cuts chemical costs by up to 30% while maintaining efficacy, driving adoption in Brazil and other large-scale agriculture regions.

Page last updated on: