Miticides Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

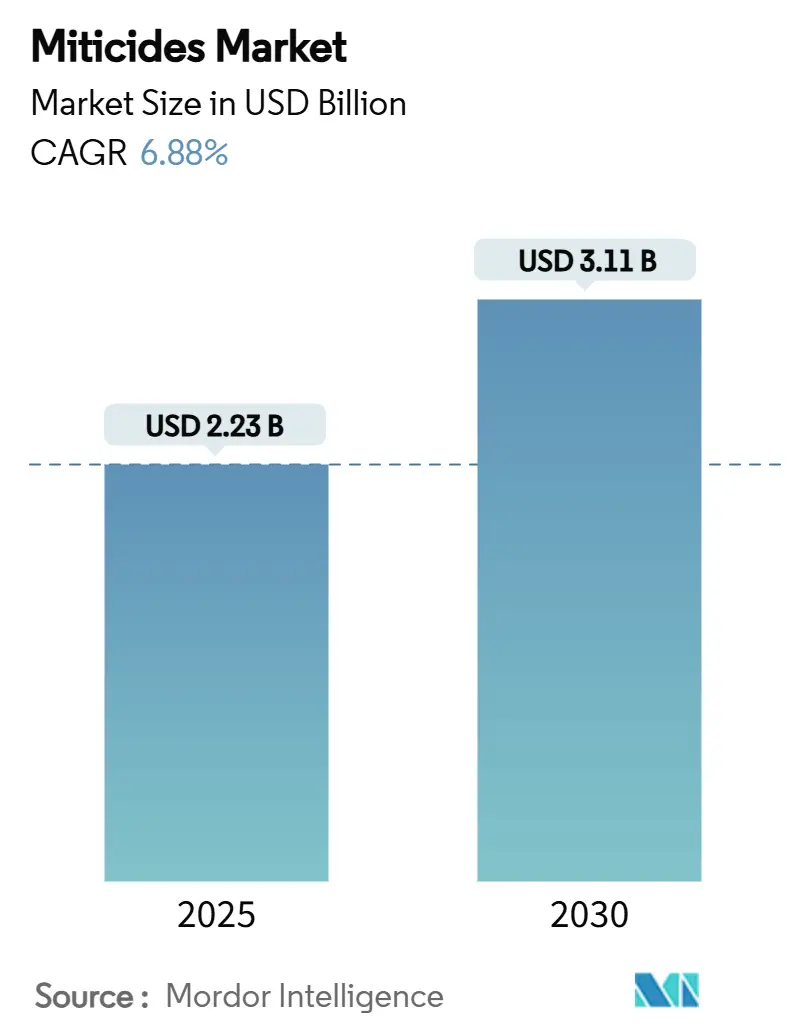

| Market Size (2025) | USD 2.23 Billion |

| Market Size (2030) | USD 3.11 Billion |

| Growth Rate (2025 - 2030) | 6.88% CAGR |

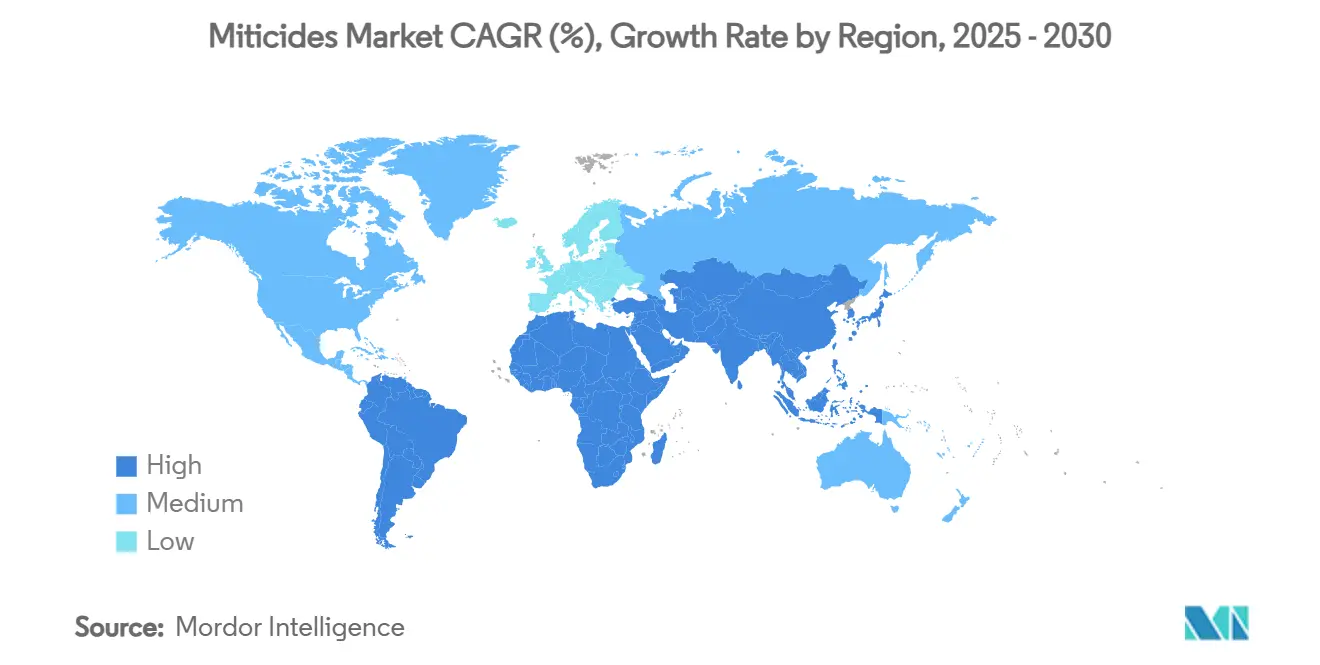

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Miticides Market Analysis by Mordor Intelligence

The miticides market size is USD 2.2 billion in 2025 and is projected to reach USD 3.1 billion by 2030, growing at a CAGR of 6.88% with an absolute growth of USD 880 million. The market shows annual growth of USD 176 million, exceeding the growth rates of traditional crop protection segments. The market expansion is driven by climate-related mite infestations, increased development of protected agriculture systems, and broader implementation of precision application methods. While chemical miticides remain the primary revenue source, biological alternatives are experiencing significant growth, reflecting the industry's shift toward products that address residue limits and resistance management. The increasing use of drone technology and aerosol ultra-low-volume application methods demonstrates a technological evolution that enables improved effectiveness with reduced chemical application. The market structure shows moderate concentration among multinational companies that maintain steady research and development, while also allowing regional specialists and biotech companies to establish market presence.[1]United States Environmental Protection Agency, “Pesticide Tolerances,” EPA.gov

Key Report Takeaways

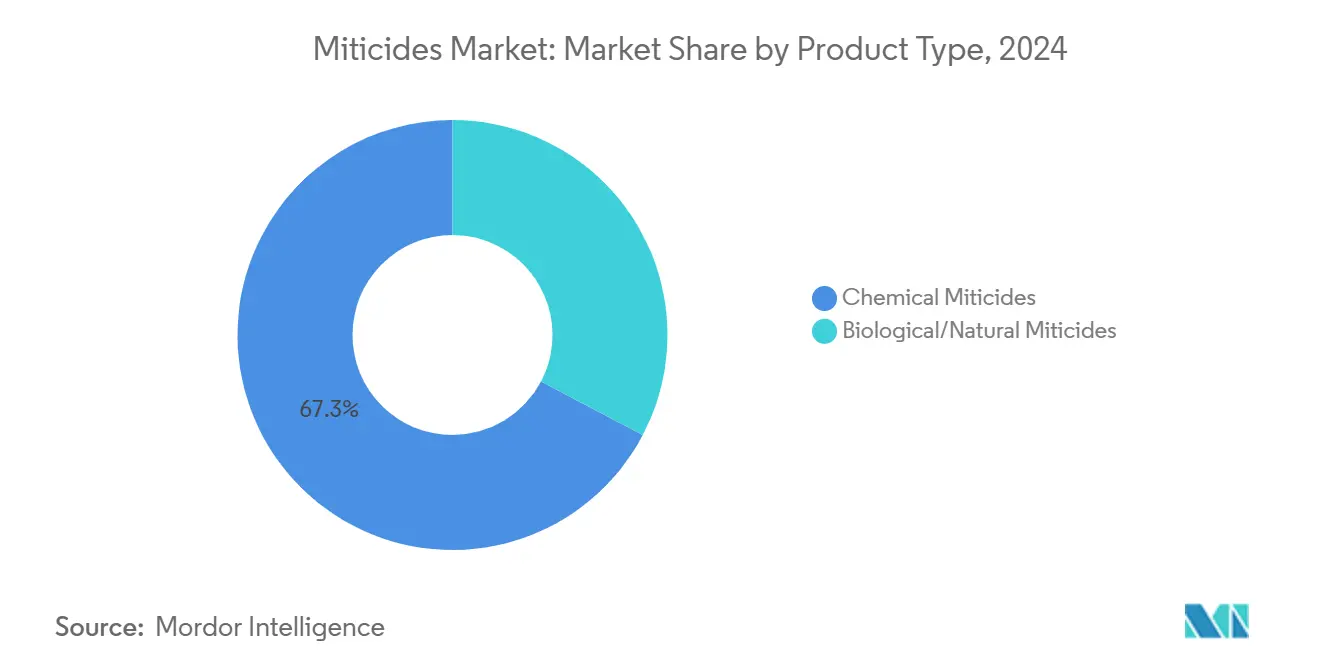

- By product type, chemical miticides dominated with a 67.3% revenue share in 2024, while biological and natural products are projected to grow at a 12.0% CAGR through 2030.

- By formulation, liquid concentrates held 40% of the miticides market share in 2024, with suspension concentrates anticipated to grow at a 10.1% CAGR through 2030.

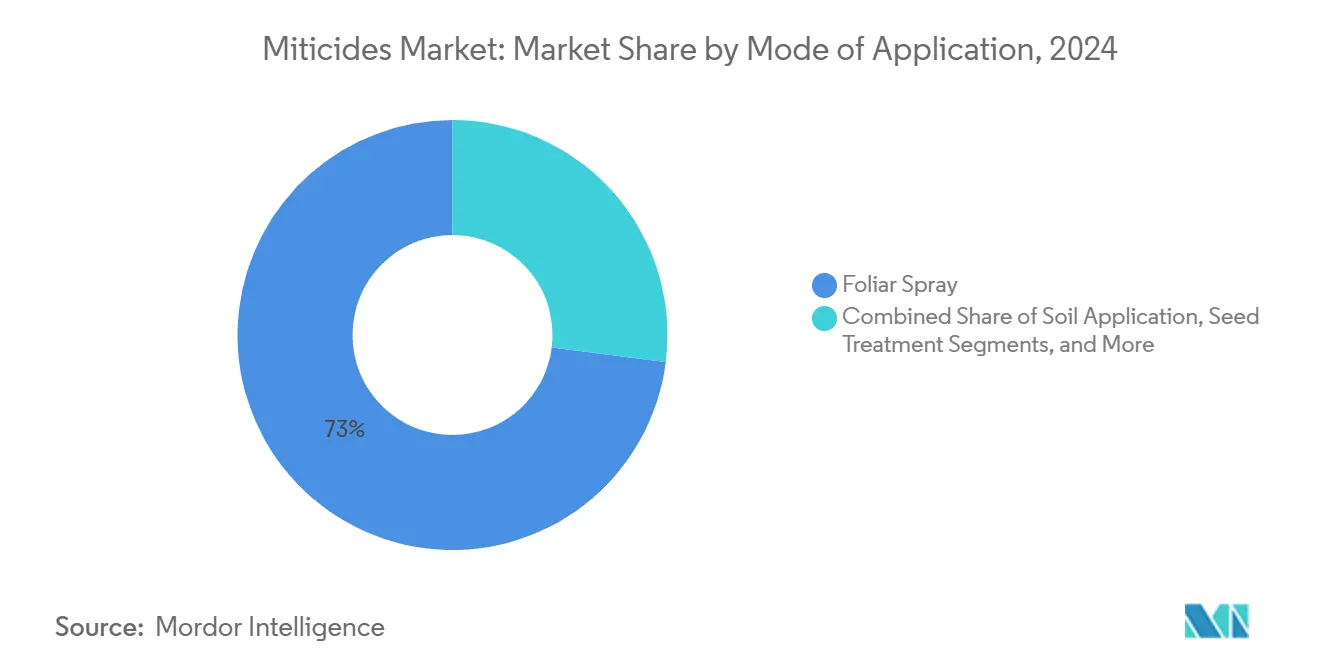

- By mode of application, foliar spray maintained a 73% share of the miticides market size in 2024, while aerosol and drone ultra-low-volume methods are projected to grow at a 13.1% CAGR through 2030.

- By crop type, fruits and vegetables accounted for 46.2% of 2024 revenue, with ornamental and turf uses growing at a 9.5% CAGR through 2030.

- By geography, North America captured a 34% market share in 2024, while Asia-Pacific is emerging as the fastest-growing region with an 8.0% CAGR through 2030.

- The market maintains moderate consolidation, with BASF SE, Bayer AG, Syngenta Group, FMC Corporation, and UPL Ltd. together holding 53% market share in 2024.

Global Miticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mite infestations in major crops | +1.2% | North America and Europe | Medium term (2-4 years) |

| Explosive growth of protected-cropping systems | +1.0% | Asia-Pacific, Middle East, and Africa | Long term (≥4 years) |

| Climate-change-induced spider-mite outbreaks | +0.9% | Arid and semi-arid zones worldwide | Long term (≥4 years) |

| Export market compliance drives late-season miticide applications | +0.8% | North America, Europe, and South America | Short term (≤ 2 years) |

| Novel technologies drive premium product development | +0.7% | Developed markets worldwide | Medium term (2-4 years) |

| Growing adoption of advanced aerial and drone-based application systems | +0.6% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mite Infestations in Major Crops

Spider mite populations thrive in temperatures between 27-30°C, which occur more frequently in major agricultural crops including chili, brinjal, cowpea, and beans. Their reproductive cycle has shortened to 7-10 days, requiring more frequent pesticide applications to prevent widespread infestations. Agricultural producers now implement rotation programs with multiple active ingredients, increasing miticide usage. Uncontrolled infestations reduce photosynthetic efficiency, increase vulnerability to secondary pathogens, and lower crop grades, potentially compromising export agreements. These factors encourage preventative treatment approaches and the use of premium formulations with proven long-term effectiveness.

Explosive Growth of Protected-cropping Systems

The expansion of greenhouse facilities in Asia-Pacific and the Middle East enables year-round production but creates enclosed environments where mite populations can be three to five times higher than in open fields.[2]M. Sharma, “Trends in Greenhouse Production Technology with Special Reference to Protected Cultivation of Horticultural Crops,” International Journal for Multidisciplinary Research, ijfmr.comGreenhouse operators require miticides that provide long-lasting protection, minimal plant damage, and compatibility with beneficial insects. The higher price tolerance in protected cultivation, typically two to three times that of open-field agriculture, drives the development of specialized formulations and package sizes suited for regular, small-volume applications. Biological oils and microbial products align with integrated pest management protocols in greenhouse systems and receive regulatory approvals more quickly.

Climate-change-induced Spider-mite Outbreaks

Rising temperatures and extended drought periods enable spider mites to reproduce twice as fast when temperatures near 30°C, while typical rainy season population control diminishes.[3]E.C. Silva, “Hydroxyethyl Cellulose-Based Hydrogel as a Novel Delivery System for Eucalyptus Globulus Essential Oil and Beauveria Bassiana Conidia for the Control of Poultry Red Mite,” BMC Veterinary Research, biomedcentral.com The demand for miticides increases in areas experiencing new persistent mite infestations, changing spray schedules, and increasing product use during off-seasons. High temperatures reduce the effectiveness of many conventional pesticides, driving the shift toward heat-stable active ingredients and encapsulated plant-based products that withstand UV exposure. Manufacturers providing performance data in high-temperature conditions gain market advantages.

Export Market Compliance Drives Late-Season Miticide Applications

Importers consistently enforce stricter maximum residue limits, requiring growers to use late-season miticides with zero-day pre-harvest intervals and exemption status. Entry into premium retail channels requires mandatory record-keeping and residue certificates, which drives supply chains to adopt low-residue products, regardless of domestic regulations. This shift increases the market presence of biological sprays, botanical oils, and fast-degrading synthetic alternatives in distribution networks. The rising compliance costs across the value chain strengthen the demand for low-risk solutions, despite their higher prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising resistance in key mite species impacts product effectiveness and costs | −1.1% | Intensive production zones worldwide | Short term (≤2 years) |

| Stringent residue and re-entry regulations | −0.8% | North America and Europe globally expanding | Medium term (2-4 years) |

| Regulatory restrictions drive shift toward lower-dose pesticides | −0.6% | Developed markets worldwide | Long term (≥4 years) |

| Proliferation of low-cost generics | −0.4% | Price-sensitive markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Resistance in Key Mite Species Impacts Product Effectiveness and Costs

The development of cross-resistance to organophosphates, carbamates, and pyrethroids reduces effective control options within two to three growing seasons of intensive pesticide use. Companies are developing multi-component formulations and alternative chemical compounds, which increases research and development costs. Farmers need to increase treatment frequency or dosages, leading to higher operational costs and potential acceleration of resistance development. The scarcity of new chemical modes of action creates an urgent need for biological control methods with different target mechanisms.

Stringent Residue and Re-entry Regulations

The reduction in maximum residue limits across major import markets is leading to the discontinuation of multiple active ingredients. Extended re-entry intervals are disrupting harvest schedules and requiring additional investments in protective equipment and compliance monitoring. Growers are adopting the most stringent international standards to streamline documentation processes, which increases chemical monitoring requirements across all markets. While these challenges accelerate the adoption of biological control methods, they also reduce profit margins for low-value crops where higher costs cannot be easily recovered through price increases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologicals Challenge Chemical Dominance

Chemical miticides held a 67.3% share of the miticides market size in 2024, with organophosphates and carbamates being primary solutions for high-volume field crops. However, increasing pest resistance and stringent residue regulations are driving biological and natural products to grow at a 12.0% CAGR through 2030. Botanical oils, fatty acid salts, and microbial metabolites are becoming more prevalent in protected cultivation environments where compatibility with beneficial insects and residue-free requirements are essential. In specialty crops, micro-encapsulated organosulfur and amidine active ingredients maintain the relevance of chemical solutions by providing rapid pest control during high infestation periods.

The industry's shift toward biological alternatives reflects risk-management strategies that prioritize sustainable resistance management over immediate cost benefits. The development of dsRNA sprays targeting specific mite gene pathways represents a significant advancement in biological control methods. Despite challenges in production costs and regulatory approval processes, successful adoption in premium greenhouse operations and export-oriented markets demonstrates the commercial viability of these solutions.

By Formulation: Liquid Concentrates Dominate Despite Innovation

Liquid concentrates maintain a 40% share of the miticide market due to their compatibility with tractor-mounted and aerial application equipment. Suspension concentrates are anticipated to grow at a 10.1% CAGR through 2030, driven by advanced particle-size engineering that enhances leaf retention and prevents settling. Wettable powders remain essential in regions with limited liquid storage and cold-chain infrastructure. Granular formulations serve a specialized role in perennial orchards, providing long-term control for soil-based applications.

Advanced formulation technologies include micro-encapsulation, which extends the effectiveness of volatile botanical ingredients, and oil-dispersion systems that protect essential oils from UV degradation. Ready-to-use aerosols address the needs of greenhouse operations requiring rapid and uniform application with minimal labor. The range of formulation options enables manufacturers to adapt to equipment requirements while complying with regulations on carrier volume reduction.

By Mode of Application: Precision Technologies Transform Delivery

Foliar sprays maintain market dominance, accounting for 73% of the miticides market share in 2024, primarily due to established application practices and readily available equipment. Drone and aerosol ultra-low volume (ULV) applications, while representing a smaller market segment, are growing at a 13.1% CAGR through 2030. Soil drench applications remain prevalent in orchard systems, providing systemic protection, while seed treatments offer early-stage crop protection. Chemigation methods incorporate miticide application through drip irrigation systems, optimizing distribution efficiency and reducing labor requirements.

The market for drone-based miticide applications continues to expand as precision agriculture advances through sensor-guided operations and digital documentation systems. Manufacturers are developing concentrated formulations suitable for low-volume applications, featuring improved suspension properties and resistance to nozzle blockage. These developments support agricultural sustainability initiatives by reducing per-acre chemical usage.

By Crop Type: Ornamental and Turf Crops Drive Premium Demand

Fruits and vegetables account for 46.2% of the market share, as their high economic value justifies regular treatment applications. The ornamental and turf grass segment shows the highest growth rate at 9.5% CAGR, driven by increased urban landscaping activities and golf course development. While cereals and grains primarily use cost-effective bulk chemicals, the growing adoption of integrated pest management encourages the testing of biological products in trial plots. The oilseeds and pulses segment benefits from government sustainability initiatives that provide subsidies for low-residue agricultural inputs.

Protected horticulture, particularly in berry and leafy green production, leads to a higher adoption of biological products, with per-acre expenditures significantly exceeding those for traditional field crops. The expansion of organic certification further supports this trend, requiring Organic Materials Review Institute (OMRI)-listed ingredients and verifiable supply chains. Companies that provide comprehensive data demonstrating product effectiveness in controlled environments gain competitive advantages in this market segment.

Geography Analysis

North America dominated the miticides market with a 34% revenue share in 2024. The region's strength stems from intensive greenhouse vegetable production in Mexico, apple orchards in the United States Pacific Northwest, and berry tunnels in Canada, which create high-value acreage supporting premium miticide solutions. The United States-European Union fresh produce trade requirements necessitate regular residue monitoring, facilitating the adoption of biological alternatives. The United States specialty crop sector shows rapid drone technology integration, with providers implementing pay-per-acre programs that include digital documentation.

Asia-Pacific shows the highest growth potential with an 8.0% CAGR in the miticides market. China and India's government support expands greenhouse vegetable production, while Southeast Asia experiences increased ornamental plant demand due to higher disposable income. Australia and New Zealand's fruit export sectors implement stricter residue standards than Codex requirements, increasing demand for rapidly degrading chemical solutions. Regional manufacturers focus on developing micro-emulsion and suspension concentrate products suitable for humid storage environments.

South America's market growth is supported by Brazil's expanding crop protection industry and Chile's fruit exports. The adoption of weather-based spray scheduling applications reduces unnecessary treatments, allowing budget allocation for advanced miticides during high-pressure periods. The Middle East and Africa regions show increasing potential through the development of drip-irrigated desert farming and urban rooftop gardens, creating demand for temperature-resistant formulations.

Competitive Landscape

The miticides market shows moderate concentration, with five major companies, BASF SE, Bayer AG, Syngenta Group, FMC Corporation, and UPL Ltd., accounting for 53% of market revenue in 2024. This concentration enables significant investments in research, field testing, and regulatory compliance while maintaining space for specialized companies to develop innovative technologies. Analysis of registration data indicates manufacturers are developing dual-action formulations that combine rapid pest control with biological enhancers to address resistance issues and meet residue requirements.

Strategic acquisitions and development partnerships characterize industry activity. In July 2024, Syngenta's partnership with Intrinsyx Bio provides access to endophytic strains that improve nutrient efficiency, enhancing their miticide portfolio with plant health capabilities. UPL's collaboration with Aarti Industries focuses on securing specialty amine supplies for advanced miticide components, strengthening their supply chain position. These strategic moves reflect an industry shift toward integrated capabilities and biological product development.

Biotechnology companies are establishing market presence through RNA interference and pheromone disruption technologies. They collaborate with formulation experts to expand production of dsRNA products, while utilizing Asia-Pacific contract manufacturers for cost-effective encapsulation. Digital solutions combining pest monitoring analytics with product recommendations serve as competitive advantages, improving customer retention and generating resistance monitoring insights.

Miticides Industry Leaders

BASF SE

Bayer AG

Syngenta Group

FMC Corporation

UPL Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nufarm forecasts revenue of USD 3.8-3.9 billion by FY26 in its crop protection segment, driven by projected price recovery through increased demand and inventory optimization. The company is strengthening its product portfolio with new miticide developments.

- November 2024: UPL Limited reported strong volume growth in fungicides and insecticides, including miticides, during Q2 FY25, with particular strength in Europe and Brazil markets. The company highlighted continued expansion in biocontrols and biostimulants portfolio despite pricing pressures impacting overall contribution margins across the agricultural chemicals sector.

- July 2024: Gowan Company launched Magister SC, a foliar miticide in the quinazoline chemical class effective against spider mites, broad mites, flat mites, and eriophyid mites. The product demonstrates knockdown activity within 24 hours and maintains excellent residual effects while being soft on beneficial insects.

- June 2024: Rovensa Next introduced OROWET Technology, utilizing advanced surfactants and natural extracts to enhance agricultural spraying results. The technology aims to improve miticide effectiveness through optimized application and performance in field conditions.

Global Miticides Market Report Scope

| Chemical Miticides | Organophosphates |

| Carbamates | |

| Pyrethroids | |

| Organosulfur | |

| Organochlorine | |

| Propargite | |

| Amidines | |

| Others (Fenpyroximate, Fenazaquin, Chlorfenapyr, Fluacrypyrim, Hexythiazox, Clofentezine, and Others) | |

| Biological/Natural Miticides | Botanical Oils |

| Microbial Based | |

| Fatty Acid Salts | |

| Others (Mineral and Inert Dusts, dsRNA/RNA-interference Sprays, Biopesticide Blends, and Others) |

| Liquid Concentrate |

| Emulsifiable Concentrate |

| Wettable Powder |

| Granules |

| Suspension Concentrate |

| Others (Micro-encapsulated suspension (CS), Oil-dispersion (OD), Micro-emulsion (ME), Ready-to-use aerosols/smokes, and Others) |

| Foliar Spray |

| Soil Application |

| Seed Treatment |

| Chemigation |

| Aerosol/Drone ULV |

| Fruits and Vegetables |

| Cereals and Grains |

| Oilseeds and Pulses |

| Ornamental and Turf |

| Others (Commercial Crops, and Others) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Chemical Miticides | Organophosphates |

| Carbamates | ||

| Pyrethroids | ||

| Organosulfur | ||

| Organochlorine | ||

| Propargite | ||

| Amidines | ||

| Others (Fenpyroximate, Fenazaquin, Chlorfenapyr, Fluacrypyrim, Hexythiazox, Clofentezine, and Others) | ||

| Biological/Natural Miticides | Botanical Oils | |

| Microbial Based | ||

| Fatty Acid Salts | ||

| Others (Mineral and Inert Dusts, dsRNA/RNA-interference Sprays, Biopesticide Blends, and Others) | ||

| By Formulation | Liquid Concentrate | |

| Emulsifiable Concentrate | ||

| Wettable Powder | ||

| Granules | ||

| Suspension Concentrate | ||

| Others (Micro-encapsulated suspension (CS), Oil-dispersion (OD), Micro-emulsion (ME), Ready-to-use aerosols/smokes, and Others) | ||

| By Mode of Application | Foliar Spray | |

| Soil Application | ||

| Seed Treatment | ||

| Chemigation | ||

| Aerosol/Drone ULV | ||

| By Crop Type | Fruits and Vegetables | |

| Cereals and Grains | ||

| Oilseeds and Pulses | ||

| Ornamental and Turf | ||

| Others (Commercial Crops, and Others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the miticides market?

The miticides market size is USD 2.23 billion in 2025 and is projected to reach USD 3.11 billion by 2030.

Which segment is growing the fastest in the miticides market?

Biological and natural miticides post the fastest growth with a 12.0% CAGR through 2030.

Which region offers the highest growth potential for miticides suppliers?

Asia-Pacific shows the highest growth, estimated at an 8.0% CAGR over 2025-2030, fueled by greenhouse expansion and integrated pest management adoption.

Why are drone and Ultra-Low Volume (ULV) applications gaining importance in mite control?

Drone and Ultra-Low Volume (ULV) techniques deliver precise canopy coverage, reduce chemical use per acre, and generate digital application records that aid export compliance.

How are resistance issues shaping product development in the miticides industry?

Accelerating spider mite resistance drives investment in novel modes of action, RNA interference technologies, and combination formulations to preserve long-term efficacy.

Which companies lead the global miticides market?

BASF SE, Bayer AG, Syngenta Group, FMC Corporation, and UPL Limited are the top five players, together holding 53% of revenue in 2024.

Page last updated on: