Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

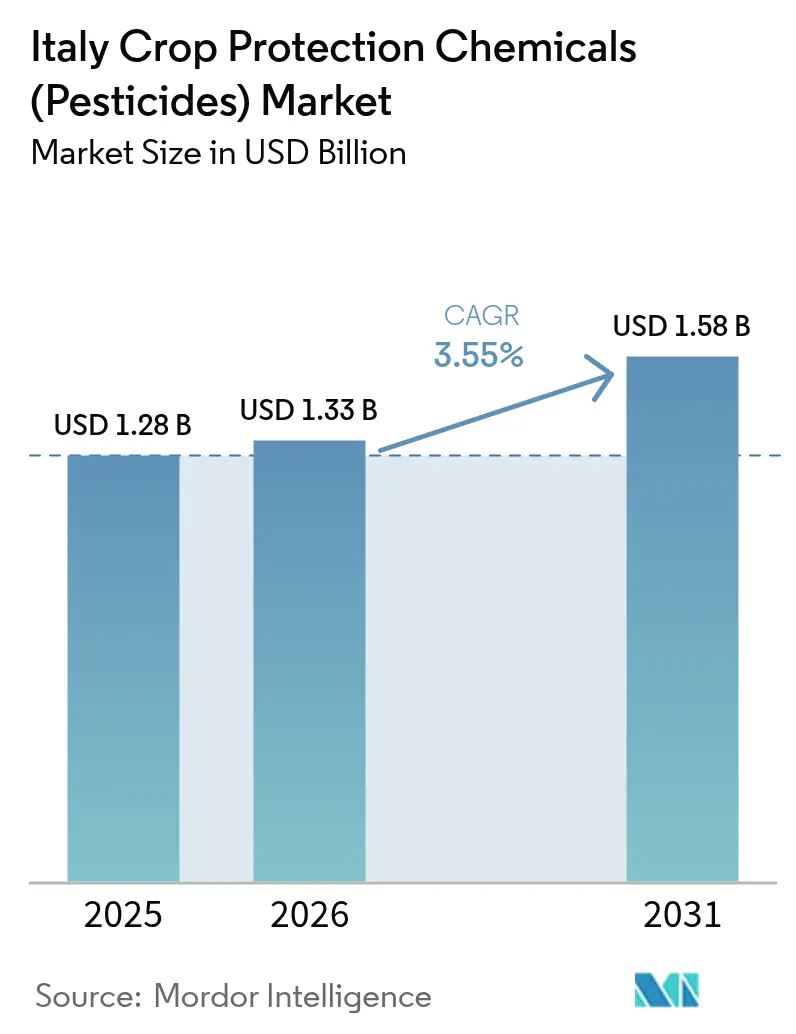

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Crop Protection Chemicals (Pesticides) Market Analysis by Mordor Intelligence

The Italy crop protection chemicals (pesticides) market size is expected to grow from USD 1.28 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at 3.55% CAGR over 2026-2031. Rising pest pressure, climate volatility, and export‐driven specialty crops keep demand resilient, even as the European Union Farm to Fork Strategy aims to cut synthetic pesticide use by 50% by 2030. Fungicides maintain dominance because vineyards, tomatoes, and fresh produce require season-long disease suppression, while drone spraying and seed treatments gradually diversify application methods. Biological products gain momentum under retailer zero-residue programs, offsetting revenue lost to active-ingredient non-renewals and counterfeit imports. Competitive intensity rises as generics and parallel imports pressure pricing, yet innovation in high-potency formulations, digital decision support, and resistance management preserves value for leading multinationals.

Key Report Takeaways

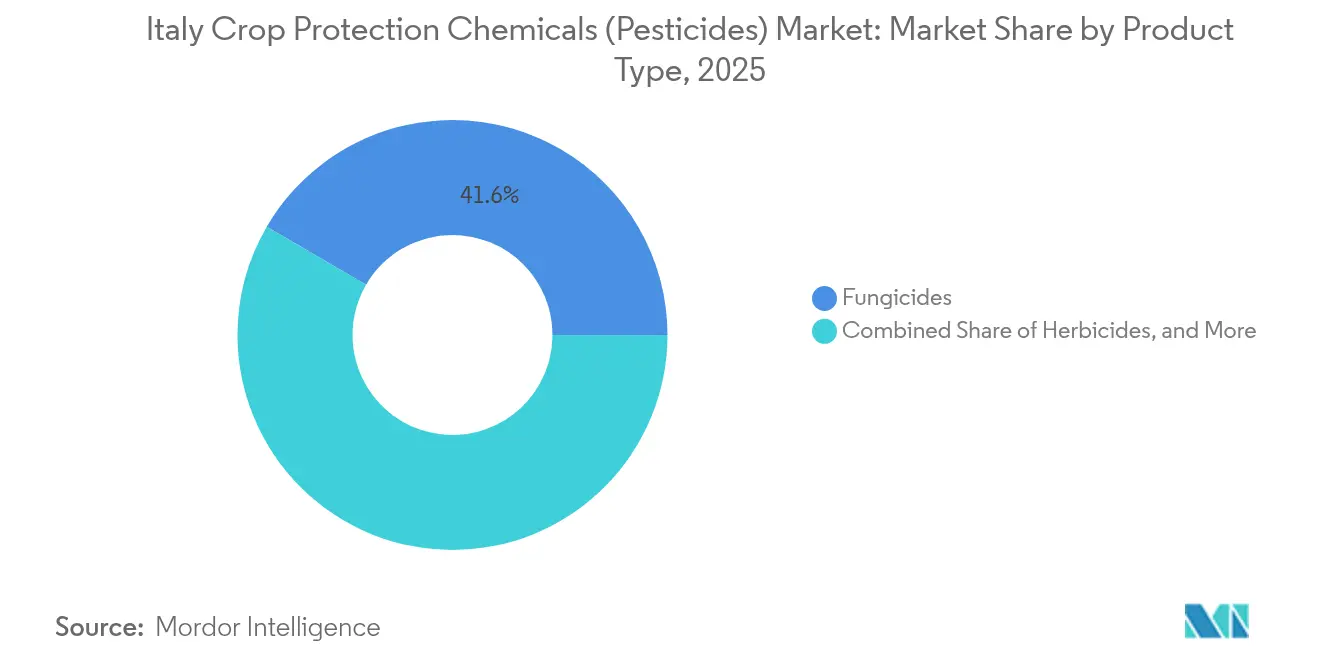

- By Product Type, fungicides held 41.60% of the Italy crop protection chemicals (pesticides) market share in 2025, and are forecast to expand at a 9.15% CAGR through 2031.

- By Application, foliar sprays led with 53.70% of the Italy crop protection chemicals (pesticides) market size in 2025, whereas seed treatment is projected to grow fastest at an 8.57% CAGR to 2031.

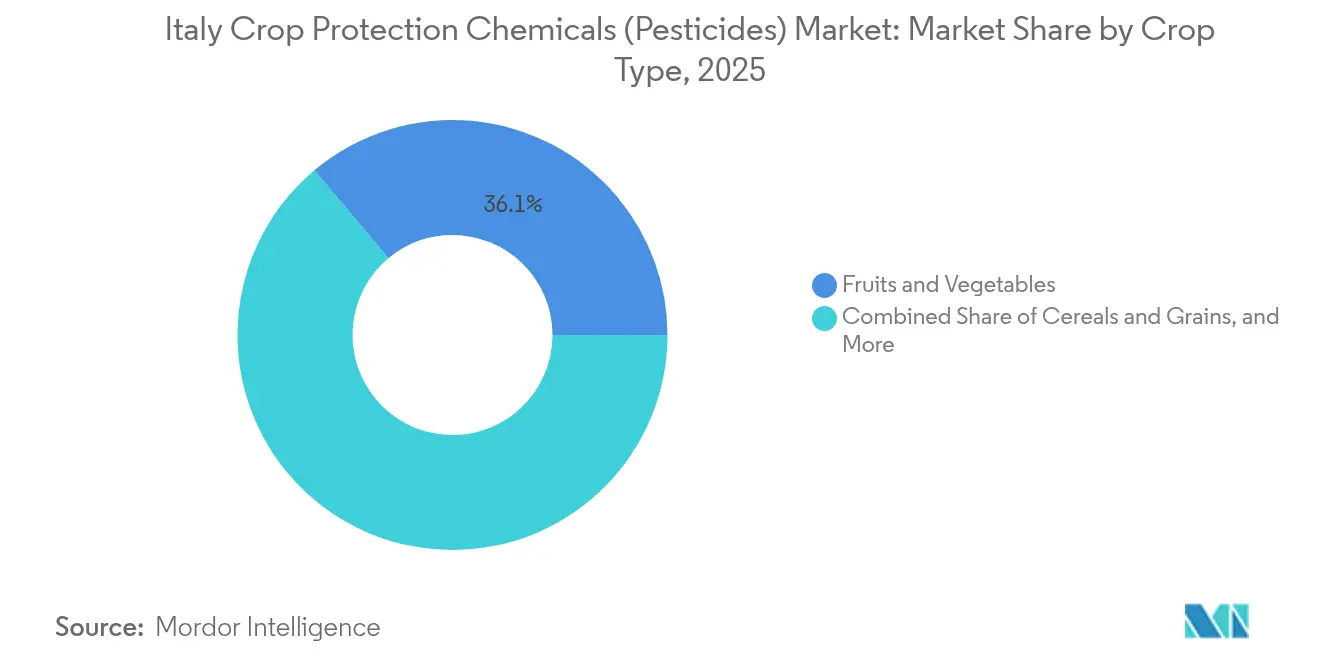

- By Crop Type, fruits and vegetables captured 36.10% of the crop protection chemicals market in 2025, and commercial crops are advancing at a 7.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Crop Protection Chemicals (Pesticides) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for food and agricultural productivity | +0.8% | Po Valley cereals and southern fruit belts | Medium term (2-4 years) |

| Increasing pest and disease outbreaks driven by climate volatility | +1.2% | Nationwide, early spikes in Veneto and Puglia | Short term (≤ 2 years) |

| Growing herbicide-resistant weed populations | +0.6% | Northern cereal basins spreading to vineyards | Long term (≥ 4 years) |

| Expansion of export-oriented fruit and vegetable production clusters | +0.7% | Sicily citrus, Campania tomatoes, Trentino apples | Medium term (2-4 years) |

| Specialty vineyard growth boosting premium fungicide demand | +0.5% | Veneto, Piedmont, Tuscany | Long term (≥ 4 years) |

| Rapid adoption of drone-based spot-spraying favoring high-potency formulations | +0.4% | National roll-out, fast uptake in vineyards | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Food and Agricultural Productivity

Per-capita consumption of fresh vegetables climbed 3.2% a year between 2020 and 2024, locking growers into volume contracts with northern European retailers that penalize supply shortfalls. Shrinking farm labor prompts heavier reliance on crop protection chemicals market tools to avoid field losses that can reach 40% in untreated processing tomatoes. Extreme weather caused USD 8.9 billion in crop damage during 2024, much of it linked to fungal and bacterial outbreaks that overwhelmed basic integrated pest management practices [1]Source: ISTAT, “Italian Agricultural Statistics 2024,” istat.it. These forces keep budget allocations for proven fungicides and herbicides inelastic despite cost pressures.

Increasing Pest and Disease Outbreaks Driven by Climate Volatility

Since 2015, warmer winters added three weeks to the downy mildew season in vineyards, forcing two extra fungicide rounds that cost EUR 150 (USD 157) per hectare. The brown marmorated stink bug now infests 80% of hazelnut and pear acreage, raising insecticide rotations and straining the crop protection chemicals market. Xylella fastidiosa has destroyed one-third of Puglia’s olives, yet growers still spray insect vectors and copper, illustrating chemistry’s residual role under biological stress [2]Source: European Food Safety Authority, “Xylella fastidiosa in the European Union: Scientific Updates,” efsa.europa.eu. BASF’s Serifel biological fungicide secured 2024 approval as a copper alternative, showing how resistance pressure accelerates new product uptake.

Growing Herbicide-Resistant Weed Populations

Rigid ryegrass resistant to glyphosate and acetolactate synthase inhibitors now infests 18% of wheat and barley fields, doubling herbicide spending above EUR 120 (USD 126) per hectare. Horseweed resistant to glyphosate spreads in vineyard inter-rows, steering the crop protection chemicals industry toward higher priced residual products [3]Source: Istituto Superiore per la Protezione e la Ricerca Ambientale, “National Report on Pesticides in Waters 2022,” isprambiente.gov.it. Corteva’s Arylex captured 8% of Italian cereal herbicide demand within two years by offering a resistance-breaking mode of action, despite a 25% price premium. Confirmed resistant weed species rose from nine to fourteen between 2019 and 2024, underlining long-term growth for innovation in the crop protection chemicals market.

Expansion of Export-Oriented Fruit and Vegetable Production Clusters

Fresh produce exports grew significantly in 2023, with residue limits below European Union standards driving demand for premium crop protection chemical solutions. In 2024, Sicily’s citrus belt expanded further, however, growers are required to transition to biological insecticides, such as spinosad, to meet residue limits that have been halved by Asian buyers. In Campania, San Marzano tomato processors face narrow application windows, which compress fungicide programs into shorter time frames, increasing per-hectare usage intensity. Meanwhile, precision tools used in Trentino apple cultivation reduced spray counts while maintaining high efficacy, demonstrating that technology can align export standards with yield security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union and national pesticide regulations | −1.1% | Strongest in Trentino-Alto Adige and Veneto | Medium term (2-4 years) |

| Heightened health and environmental risk concerns among consumers | −0.7% | High in organic-intensive Tuscany and Marche | Long term (≥ 4 years) |

| Rising inflow of counterfeit or parallel-import pesticides | −0.4% | Southern distribution hubs | Short term (≤ 2 years) |

| Retailer zero-residue standards reducing conventional chemical use | −0.6% | Nationwide, earliest in Coop Italia and Esselunga chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent European Union and National Pesticide Regulations

The Farm to Fork Strategy continues to aim for a significant reduction in pesticide use by 2030, despite the withdrawal of the Sustainable Use Regulation in February 2024. Italy has seen a decline in pesticide distribution over recent years. However, per-hectare usage among remaining growers has remained consistent, suggesting that regulation alone does not reduce usage intensity. In recent years, several active ingredients have lost approval, limiting disease control options to fewer chemical solutions and increasing the risk of resistance. In Trentino, buffer zones around schools have restricted aerial or drone spraying on a portion of apple acreage, resulting in notable sales losses for the Italy crop protection chemicals (pesticides) market.

Heightened Health and Environmental Risk Concerns Among Consumers

A 2024 consumer survey revealed that a significant percentage of respondents were willing to pay a premium for zero-residue produce, showing an increase compared to 2020. This trend has led to stricter pesticide thresholds in retail contracts. ISPRA reported the presence of pesticides in surface-water sites, intensifying media attention and public concerns about contamination. Organic farmland has expanded, accounting for a notable share of national farmland, which has directly reduced the demand for conventional crop protection chemicals. Additionally, regional subsidies in Tuscany are supporting the adoption of biological methods, redirecting budgets from synthetic chemicals to biocontrol solutions and contributing to a long-term decline in synthetic pesticide sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fungicides Sustain the Core of Demand

Fungicides delivered 41.60% of the Italy crop protection chemicals (pesticides) market share in 2025, as 640,000 hectares of vineyards and 1.3 million hectares of tomatoes demanded season-long disease control. The fungicides expand at a 9.15% CAGR as copper limits and retailer mandates move growers toward Bacillus amyloliquefaciens or Trichoderma formulas priced 100% higher than synthetics. Herbicides follow because cereal rotations rely on glyphosate and pendimethalin, though uncertainty around glyphosate renewal after 2025 elevates interest in Corteva’s Arylex and BASF’s Luximo premium entrants. Insecticides demand is driven by Mediterranean fruit fly and brown marmorated stink bug, while molluscicides and other minor products share the remaining.

The Italy crop protection chemicals (pesticides) market size tied to fungicides will keep expanding as high-value grapes and greenhouse vegetables offset acreage loss in cereals. Biological fungicides win incremental share, but cost headwinds limit penetration outside audited chains. Herbicide growth stays modest given regulatory risk, yet resistance pressure supplies a floor for new mode-of-action launches. Insecticide demand pivots toward drone-ready suspensions with rapid knockdown, a niche where multinationals hold formulation advantages.

By Application: Foliar Sprays Dominate but Seed Coatings Grow Fast

Foliar treatments generated 53.70% of the Italy crop protection chemicals (pesticides) market size in 2025, reflecting the grower's need for rapid, visible symptom suppression, especially in fruits and vegetables that cannot risk a 14-day disease incubation. Soil fumigation and chemigation each occupy smaller shares, but they remain critical in greenhouse beds plagued by Fusarium or root-knot nematodes. Seed treatment rises at an 8.57% CAGR as neonicotinoid bans redirect protection into systemic coatings that avert spray drift and satisfy pollinator safeguards.

Through 2031, seed-applied products will become the second-largest method in the crop protection chemicals market as maize, sunflower, and soybeans expand under biofuel demand. Foliar volumes level off but retain value because drone delivery improves coverage and reduces waste. Chemigation scales with protected cultivation, where labor scarcity makes drip-line inputs attractive. Overall, application-method diversification cushions revenue even as total kilogram use declines in response to European Union policy.

By Crop Type: Fruits and Vegetables Anchor Spending

Fruits and vegetables represented 36.10% of the Italy crop protection chemicals (pesticides) market in 2025 as Sicily citrus, Veneto vineyards, and Emilia-Romagna tomatoes trusted intensive programs to meet export residue caps. Commercial crops record the fastest 7.48% CAGR as energy incentives and cannabidiol extraction boost hemp and maize acreage. Grains and cereals have a significant share; however, low wheat prices curb sprays beyond essential herbicides and one fungicide for Fusarium. Oilseeds, pulses, and turf combine for the residual share, but they remain high-margin niches for low-toxicity formulations.

Fruits, vegetables, and vineyards will continue to dictate product innovation because residue limits and climate-driven pathogens demand new modes of action and biological tools. Biomass crop expansion injects incremental volumes for herbicides and insecticides where regulatory barriers are looser. Cereals stay price sensitive and lean on generic chemistry, squeezing margins unless resistance forces change. The Italy crop protection chemicals (pesticides) market thus tilts toward specialty horticulture for value growth and toward biomass acreage for volume buffers.

Geography Analysis

Northern Italy dominated spending with a significant share of the Italy crop protection chemicals (pesticides) market in 2025, powered by 3.2 million hectares of cereals and 24,000 hectares of Prosecco vineyards that require up to 15 fungicide rounds each season. High-value orchards in Veneto and Trentino push per-hectare chemical outlays to USD 1,260, double the national average. Southern Italy is the fastest-growing region and is projected to advance in line with the 7.48% CAGR posted by its expanding commercial biomass crops, such as industrial hemp and energy maize. Intensifying insect pressure from Mediterranean fruit fly and Xylella fastidiosa keeps fungicide and insecticide programs robust in Sicily and Puglia, cementing the region’s growth trajectory.

Central Italy, covering Tuscany, Umbria, Lazio, and Marche, accounted for roughly one-fifth of national sales as 320,000 hectares of premium vineyards and 180,000 hectares of olives blended systemic triazoles with copper and sulfur for scab and anthracnose control. Tuscany’s 17.4% organic land share curbs synthetic volumes yet boosts biological values, while Lazio’s glyphosate buffer zones near schools shift growers toward mechanical weeders and pricier pre-emergence herbicides. Northern alpine foothills such as Lombardy’s Franciacorta now support commercial viticulture for the first time, adding incremental fungicide use where none existed a decade ago. Across all central provinces, retailer residue audits spur precision-spray investments that keep spending resilient despite fewer kilograms applied.

Looking forward, regional demand will keep tilting toward specialty crops and precision technology. Drone spraying already covers 30% of vineyard hectares nationwide and is spreading southward, encouraging adoption of high-potency microencapsulated formulations that preserve value even as volumes decline. Government subsidies for electronic spray logs and precision farming equipment favor well-capitalized growers in the north, yet southern cooperatives leverage cost-competitive off-patent products to maintain momentum. As climate shifts push pests north and export markets tighten residue limits, every region is projected to intensify integrated programs that blend biologicals with low-dose synthetics, expanding the overall crop protection opportunity despite regulatory headwinds.

Regulatory Landscape

Italy regulates plant protection products under the EU framework, notably Regulation (EC) No 1107/2009 (placing products on the market) and Regulation (EC) No 396/2005 (maximum residue levels), with sustainable-use requirements under Directive 2009/128/EC implemented nationally via Legislative Decree 150/2012. The Ministero della Salute is the competent authority for national product authorizations and maintains the official database for registered plant protection products, while coordination spans other ministries (including MASAF and MASE), regional health structures, and enforcement bodies such as the Carabinieri Command for Health Protection.

Recent compliance focus has tightened around residue-limit and authorization upkeep. In January 2026, the Ministero della Salute updated operational guidance linked to changing MRL requirements and the need to re-check product uses as EU rules evolve, and in February 2026 it issued a circular addressing procedures for renewing certain authorizations. Alongside EU and national sustainability targets, these updates reinforce dossier, labeling, and use-condition discipline for suppliers and distributors, and they raise demand for formulations and programs aligned with integrated pest management and reduced-risk profiles, particularly in high-audit fruit, vegetable, and vineyard supply chains.

Competitive Landscape

Syngenta Group and Bayer CropScience AG anchor Italy’s crop protection sector, leveraging deep technical teams and decades of local trial data to align products with vineyard and vegetable disease profiles. Syngenta’s TYMIRIUM fungicide commands a EUR 45 (USD 47) per-hectare premium, yet growers accept the price because it breaks triazole resistance and delivers a 21-day residual window that cuts curative sprays. Bayer CropScience AG maintains a broad reach through glyphosate, pendimethalin, prothioconazole, and fluopyram while embedding its Climate FieldView decision platform on 120,000 hectares, which locks in repeat sales via data-driven recommendations.

BASF SE, Corteva Inc, and UPL Ltd round out the top tier with complementary strengths that chip away at the leaders’ head start. BASF SE couples premium vine fungicides such as Serifel with a new USD 26 million Bacillus plant in Spain that will supply zero-residue chains starting in 2026. Corteva Inc rides Arylex herbicide uptake in resistant cereals and pairs Zorvec fungicide with recently acquired biostimulants, enabling bundled offers that resonate with cash-tight mixed farms. UPL Ltd competes on price through an off-patent range averaging 20 to 30% below branded equivalents and is expanding its Ozzano dell’Emilia site to launch drone-ready suspensions and water-dispersible granules by 2026 UPL Ltd.

Growth prospects revolve around biological fungicides and precision-application formats that reward companies with formulation know-how and strong agronomic support. Retailer zero-residue programs create headroom for Bacillus and Trichoderma products, a niche where BASF SE and emerging specialists like Koppert aim to scale. Drone spraying already covers 30% of vineyard hectares and favors high-potency microencapsulated actives, tilting competitive advantage toward firms such as BASF SE and FMC Agro Italia S.r.l. that invest in polymer-coating technology. As Italy’s mandatory electronic registry raises compliance costs, smaller farms consolidate, and the remaining operators increase per-hectare spending, allowing established suppliers to deepen their share even as generic competition persists.

Italy Crop Protection Chemicals (Pesticides) Industry Leaders

Syngenta Group

BASF SE

Corteva Inc

UPL Ltd

Bayer CropScience AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two near-term opportunity areas are expanding around compliance-enabled services and biological portfolios. Italy has mandated the shift of professional pesticide usage registers to a mandatory electronic format by December 31, 2026 (MASAF implementation tied to EU requirements), which creates demand for farm-level digital tools, advisory workflows, and supplier-supported stewardship programs that help growers and cooperatives standardize records across multi-crop operations. Authorization management is also becoming more dynamic as MRL definitions change, and the Ministero della Salute has required timely national adjustments for affected products (including submission steps following EU publications), favoring companies with strong regulatory affairs capacity and distributor networks able to execute rapid label and portfolio updates.

Biocontrol and integrated programs also offer an evidence-backed expansion lane. In April 2026, Agrofarma (Federchimica) and FederBio presented a Manifesto for Biocontrol that calls for a clearer regulatory definition and more streamlined national authorization pathways for biocontrol, aligning with retailer and export-driven residue constraints highlighted across Italian horticulture and viticulture value chains. At the EU level, Implementing Regulation 2026/748 set multiannual residue control programs for 2027-2029 with ongoing monitoring requirements in 2026, reinforcing the premium placed on verifiable residue management and pushing product development and go-to-market toward biologicals, resistance-management rotations, and precision-application compatibility, including drone-ready, low-dose formulations already gaining traction in Italian vineyards.

Recent Industry Developments

- July 2026: Syngenta Italia reported results tied to its sustainability commitments in Italy, including farmer training on safe use practices and regenerative agriculture initiatives implemented across 52,000 hectares in 2025. The activity supports tighter on-farm stewardship and documentation routines that increasingly influence retailer and cooperative purchasing decisions for crop protection programs.

- May 2026: BASF commissioned a new fermentation plant (BioHub) at Ludwigshafen with a high double-digit million-euro investment to produce biological crop protection products, including Serifel and Inscalis. The additional fermentation capacity strengthens supply reliability for microbials and supports scale-up of biological solutions used in residue-sensitive horticulture and vineyards, including Italy-focused programs.

- April 2024: Adama launched Sonavio, a PPO herbicide based on bifenox, for use in additional vegetables in Italy. The expansion broadens chemical weed-control options for specialty crops where rotation flexibility matters, while growers and advisors balance efficacy with tightening sustainability and residue requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of crop protection chemical pesticides sold for agricultural use in Italy, across the main pest control functions used to protect yields and crop quality through the season.

Scope exclusions: We exclude fertilizers, soil conditioners, adjuvants sold as stand-alone products, farm equipment services, and on-farm application labor charges.

Segmentation Overview

- By Product Type

- Herbicides

- Insecticides

- Fungicides

- Molluscicides

- Other Product Types

- By Application

- Chemigation

- Foliar

- Fumigation

- Seed Treatment

- Soil Treatment

- By Crop Type

- Grains and Cereals

- Oilseeds and Pulses

- Fruits and Vegetables

- Commercial Crops

- Turf and Ornamental

Data Sources, Market Sizing, and Validation

Desk Research

To set up the market boundary and keep the inputs aligned with Italian agriculture, we start with public data that reflects crop area, output, and pesticide use conditions. Sources used include Eurostat for crop area and output, the Italian Ministry of Agriculture and related national statistics, ISTAT datasets, and FAOSTAT series for longer time comparisons. For product and regulatory context, we also review publications from the European Commission and EFSA, since approvals and withdrawals can shift volumes from one active category to another.

On the commercial side, we extract signals from company annual reports, investor presentations, and reputable press coverage on pricing, channel shifts, and formulation trends. Where needed, we use paid subscriptions covering company financials and a paid patent database to cross-check supplier exposure and innovation activity without relying on any single disclosure. The sources listed here are illustrative, and many other public references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions and to fill gaps that public data does not answer well, especially around price realization, mix changes, and channel stocking. We spoke with manufacturers, distributors, cooperatives, agronomists, and large farm buyers across Italy, and then we re-checked any outlier feedback with follow-up calls so the final model stayed consistent. When a variable moved the totals materially, we kept it only after it matched at least two independent viewpoints from the field.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | |

| Mid tier: 45% | Functional/Unit leaders: 30% | |

| Smaller Players: 20% | Managers: 58% |

Market-Sizing & Forecasting

The sizing starts with a top-down build that reconstructs demand from Italy crop area and crop mix, typical treatment intensity by crop, and observed shifts in pest pressure and seasonality. We then normalize pricing in USD for the base year.

Once the demand pool was created, we apply product mix splits that reflect common farmer programs (pre-emergence versus post-emergence, foliar windows, and seed treatment adoption), so the value total is not driven by one broad average.

To keep the model grounded, we also use selective bottom-up approximations, such as sampled supplier revenue exposure to Italy, distributor channel checks on volume movement, and sanity checks using implied average price per treated hectare for key crop groups. Input variables that matter most include hectares under major crops, spray frequency and dose patterns, the balance between generic and branded products, the share of higher value formulations, and regulatory-driven substitutions across active groups. For forecasting, we apply scenario analysis, with the base case guided by interview consensus on expected crop area stability, price progression, and the pace of product replacement under EU regulatory decisions. Where bottom-up information is incomplete, we use conservative ranges and then adjust only after the implied per-hectare spend aligns with field feedback.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including cross-checks versus crop area movements, season-driven demand swings, and year-to-year pricing logic. Any large variance between the top-down result and the bottom-up checks triggers a second review, and then assumptions are corrected or explicitly constrained to avoid overstating growth.

Before sign-off, the model and narrative go through multi-step analyst review so calculation links, conversions, and scope rules are applied consistently. Reports are refreshed annually, and if a material event occurs, such as a major active withdrawal or an unexpected crop disease year, an interim update is prepared. Right before delivery, we do a final pass to confirm the latest public indicators and field notes are reflected.

Mordor Intelligence's Italy Crop Protection Pesticides Market Size Versus Other Published Estimates

Published estimates for Italy crop protection pesticides can differ even when the topic sounds the same, because the scope boundary and the pricing logic are often not aligned. The spread typically comes from what is counted as pesticides, how crop and use-case coverage is handled, and whether the year used is a true base year or a forecasted stepping stone.

The key gap drivers are usually whether biological products are folded into the same total, whether distribution markups and on-farm service charges are mixed into the value, and how currency conversion timing is treated when prices are collected across a season. Some publications also anchor on a single year value and then apply a fixed CAGR, which can miss regulatory changes and a high or low disease year that temporarily moves treatment intensity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.28 B (2025) | |

| Global Consultancy A | USD 1.03 B (2024) | Uses an earlier base year and a different growth window, and the value basis can lean more on stated revenues by broad product groups, which may understate in-season price and mix shifts. |

| Industry Publisher B | USD 0.87 B (2028) | Focuses on a narrower agrochemical product basket and reports in EUR with a light-growth outlook, which can compress totals when converted and when newer formulations are not fully reflected. |

The table shows a clear spread by year and by what is treated as in-scope value, and in Mordor Intelligence's model the total is limited to crop protection chemical pesticides sold into agricultural use, with pricing normalized to the base-year season rather than a single point-in-time quote. Once the scope and price timing are aligned, the remaining differences usually come down to how treatment intensity and product mix are adjusted for regulation and pest pressure, which we keep traceable to simple, repeatable inputs.

Key Questions Answered in the Report

What is the 2026 value of Italy crop protection chemicals (pesticides) market?

The market is valued at USD 1.33 billion in 2026.

Which product type captures the largest share of Italian spending?

Fungicides lead with 41.60% of 2025 revenue.

Which application method is gaining ground most quickly?

Seed treatment is projected to grow at an 8.57% CAGR during the 2026-2031 forecast horizon.

How will drone spraying influence demand?

Drone adoption reduces volumes by 30–40% but increases demand for high-potency formulations, reshaping supplier advantages.

Page last updated on: