US Insecticide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.98 Billion |

| Market Size (2026) | USD 8.34 Billion |

| Market Size (2031) | USD 10.49 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Insecticide Market Analysis by Mordor Intelligence

The US insecticide market size was valued at USD 7.98 billion in 2025 and is estimated to grow from USD 8.34 billion in 2026 to reach USD 10.49 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031). The market is advancing on the back of diamide chemistry adoption, accelerating RNA interference (RNAi) product approvals, and the ongoing phase-out of high-toxicity organophosphates that is reshaping product portfolios. Neonicotinoid restrictions in several states are pushing retailers toward alternative seed-treatment actives, while specialty-crop expansion is widening the addressable acreage for selective formulations that leave minimal harvest residues. Growers are also investing in digital decision tools that time applications precisely, which is lifting demand for premium products with narrow spray windows. Together these factors are supporting value growth that outpaces treated-acreage expansion, even as input price inflation levels off relative to 2025 peaks.

Key Report Takeaways

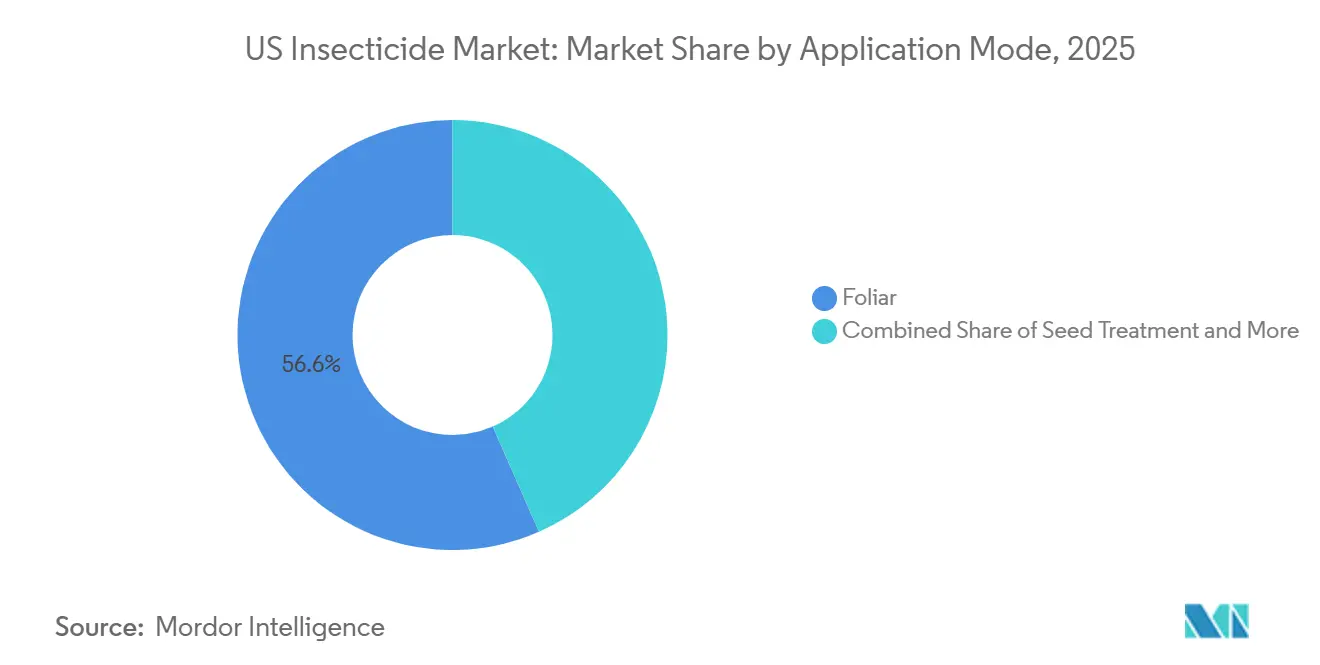

- By application mode, foliar sprays led with 56.6% of the US insecticide market share in 2025, whereas seed treatment posted the fastest growth at a 4.9% CAGR from 2026-2031.

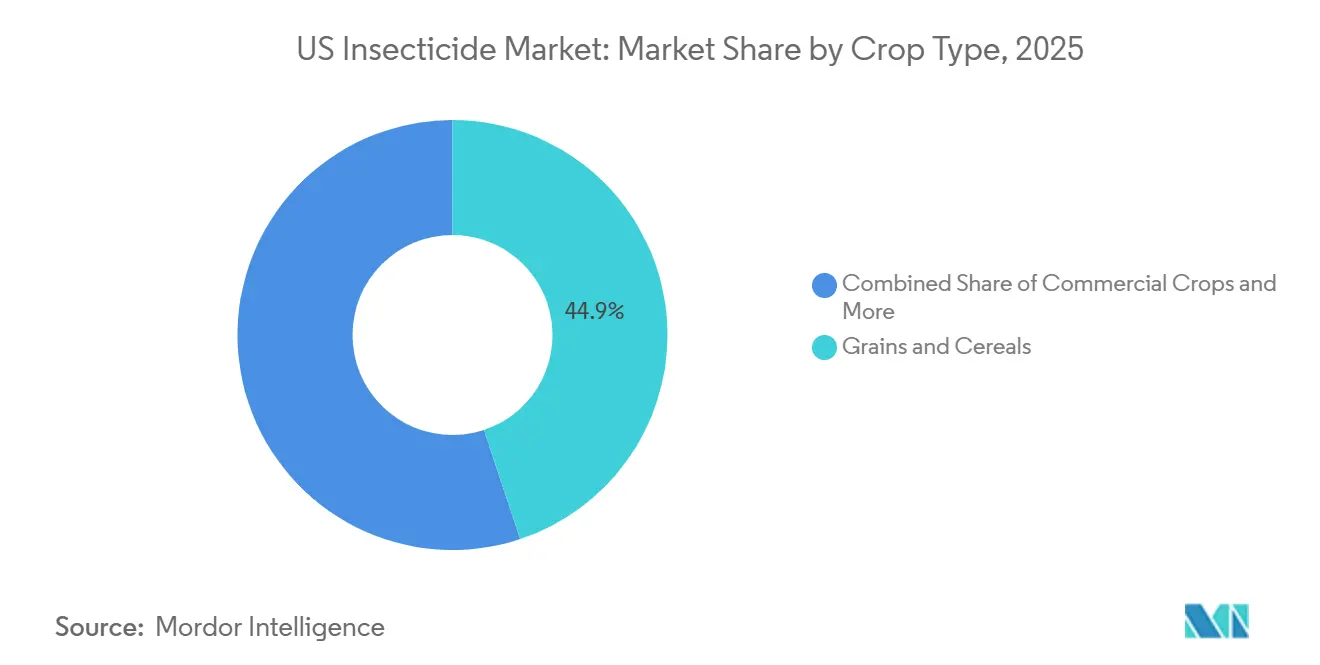

- By crop type, grains and cereals accounted for 44.9% of the US insecticide market size in 2025 and are expanding at the fastest growth of 5.1% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialty-crop acreage expansion requiring selective synthetic chemistries | +0.8% | California, Florida, and Pacific Northwest | Medium term (2-4 years) |

| Resistance management needs in insect populations | +1.2% | Corn Belt, Cotton Belt, and National | Long term (≥ 4 years) |

| Growth in seed-treatment adoption for systemic control | +0.7% | Midwest and Great Plains | Short term (≤ 2 years) |

| Advancements in synthetic chemistry screening accelerating discoveries | +0.4% | National, Delaware, North Carolina, and Missouri | Medium term (2-4 years) |

| Carbon-credit monetization for IPM adopters | +0.3% | California, Arizona, and Controlled environments | Long term (≥ 4 years) |

| Farm-level AI advisory platforms optimizing spray timing | +0.5% | Large-scale operations and Midwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Specialty-Crop Acreage Expansion Requiring Selective Synthetic Chemistries

Protected-environment vegetable, almond, and citrus hectares rose steadily in 2024 and 2025, and these high-value crops demand residue-free harvests that satisfy export inspection protocols. The differential in per-acre insecticide spend now exceeds a five-to-one ratio relative to Midwest field corn, prompting manufacturers to tailor low-PHI (Pre-Harvest Interval) formulations that secure premium pricing. Specialty crops often deliver three-to-five-fold higher gross returns relative to grains, so growers willingly adopt high-priced, reduced-risk formulations that protect both yield and quality. California growers are transitioning from broad-spectrum organophosphates to selective chemistries, such as cyantraniliprole, following the federal chlorpyrifos ban. Similar trends in Arizona and Florida are reinforcing a long-term volume and value tailwind for the US insecticide market.

Resistance Management Needs in Insect Populations

Widespread cross-resistance of the Western corn rootworm to multiple Bacillus thuringiensis (Bt) traits has impacted millions of acres, leading to a significant increase in the use of soil-applied organophosphates and foliar diamides. In 2024, the United States Environmental Protection Agency (EPA) issued regulatory guidance mandating refuge planting and chemistry rotation[1]Source: Environmental Protection Agency, “Chlorpyrifos Final Rule,” EPA.gov. This requirement has reinforced insecticide spending in resistance-prone areas, such as those affected by corn rootworm and cotton bollworm. As a result, portfolio depth has become a critical factor for suppliers, enabling them to meet entire seasonal demands and secure greater market share. Additionally, structured rotation has driven the development of formulations that combine multiple active ingredients, offering both insecticidal and fungicidal protection in a single application, thereby ensuring compliance and reducing labor costs. These factors collectively support consistent growth in the US insecticides market, as growers adopt diverse modes of action to maintain yield stability.

Growth in Seed-Treatment Adoption for Systemic Control

Seed-applied insecticides captured an increased share of total active-ingredient volume in 2024 and continued to climb through 2025 as growers favored root-zone delivery that minimizes pollinator exposure. Bayer’s LumiGEN and Corteva’s Lumiderm platforms combine neonicotinoids or diamides with biological additives, delivering double-digit yield gains in multi-state trials. The US insecticide market benefits because early-stage protection curbs costly re-sprays and anchors integrated pest management plans. The United States Environmental Protection Agency (EPA) issued dust-off mitigation guidance in 2025 that mandates closed-transfer systems, a move that boosts equipment investment but also entrenches adoption of premium coated seed. Service providers further enhance uptake through bundled seed plus treatment offerings that simplify grower procurement. As a result, seed treatments remain one of the fastest scaling revenue pools within the US insecticides market.

Farm-Level AI Advisory Platforms Optimizing Spray Timing

Digital agronomy systems, including Climate FieldView, FMC’s Arc, and Syngenta’s Cropwise, have significantly improved returns on insecticide investments by providing real-time pest pressure analytics. Algorithms recommending narrower spray windows have increased sales of higher-priced formulations with shorter residual curves, while also documenting chemical savings for carbon accounting purposes. Autonomous vision technologies, such as John Deere’s See and Spray, are anticipated to reduce active ingredient volumes through spot treatment. Collectively, these advancements enhance the data-driven competitive advantage of suppliers operating in the US insecticides market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Protection Agency (EPA) mandated withdrawals and use restrictions on select organophosphate and carbamate insecticides | -0.90% | National, California, Florida, and Pacific Northwest | Short term (≤ 2 years) |

| Pollinator-health pressures restricting neonicotinoid use | -0.60% | Agricultural regions with pollinator-dependent crops | Medium term (2-4 years) |

| Insurance premium surcharges on high insecticide intensity | -0.30% | National, Iowa, Illinois, Nebraska, and Kansas | Long term (≥ 4 years) |

| Shrinking custom-applicator labor pool | -0.4% | National, Great Plains and Delta states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Protection Agency (EPA) mandated withdrawals and use restrictions on select organophosphate and carbamate insecticides

The federal ban on chlorpyrifos in food production eliminated a significant amount of active ingredient annually, prompting users to shift to more expensive alternatives such as diamides and spinosyns. Additionally, updated registration reviews for malathion and diazinon now require costly closed-system mixing equipment, increasing compliance expenses for custom applicators. Companies are investing heavily in developing reformulated alternatives; however, commercial launches are delayed due to ongoing efficacy testing. The removal of existing chemistries in the near term reduces market volume while increasing cost pressures in the US insecticide market.

Insurance Premium Surcharges on High Insecticide Intensity

Pilot programs in the Midwest now tie crop-loss policy pricing to recorded insecticide-application intensity, with farms above the median load paying eight-to-fifteen percent higher premiums. Early actuarial work by the USDA Risk Management Agency shows that excessive foliar passes correlate with greater yield volatility due to disrupted beneficial insect populations. Growers consequently weigh insurance economics alongside chemistry choices, a calculus that can dampen volume growth in high-intensity segments of the US insecticide market. Data standardization gaps still slow nationwide rollout but the direction of travel is clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Seed Treatment Widens Systems Advantage

Foliar sprays led with a market share of 56.6% of the US insecticide market size in 2025, whereas seed treatment posted the fastest growth at a 4.9% CAGR from 2026-2031, anchored by their versatility across crop systems. The shift is driven by grower demand for labor-efficient systemic protection and state-level restrictions on in-season neonicotinoid foliar sprays, which increase the relative importance of treated seed. Platforms like Bayer’s LumiGEN and Corteva’s Lumiderm integrate neonicotinoids or diamides with biological coatings, delivering significant yield improvements in corn and soybean trials[2]Source: Bayer Crop Science, “LumiGEN Launch Press Release,” Cropscience.bayer.us. The success of seed treatments is further supported by the upcoming EPA requirement for planter dust-mitigation upgrades, which necessitate the use of premium closed-system equipment, encouraging the adoption of coated seeds. Regulatory pressure also favors closed-system seed coaters that reduce applicator exposure.

Chemigation is gaining traction in irrigated specialty crops because drip lines can distribute systemic actives at one-third lower rates than broadcast sprays. It is gaining traction where irrigation infrastructure permits, especially in water-limited regions aiming for simultaneous pest and moisture management. Fumigation retains a niche in strawberry beds and nursery stock but exhibits minimal growth. Soil treatments remain important in perennial orchards where root-zone protection is critical. Together, these trends illustrate the diversified pathway through which the US insecticide market accommodates evolving agronomic and labor realities.

By Crop Type: Row Crops Underpin Chemical Demand

Grains and cereals commanded 44.9% of the market share in the US insecticide market size in 2025 revenue and are projected to grow at a fastest rate of 5.1% CAGR from 2026-2031. Soybean seed treatments containing neonicotinoids are widely adopted due to their effectiveness in reducing the need for in-season spray applications. Wheat producers, particularly in certain regions, are expanding neonicotinoid use to address Hessian fly infestations, though potential regulatory restrictions may limit this growth. Variable-rate technology fine-tunes application density, aligning input spend with soil pest hotspots. The US insecticide market share for grains surged during the 2025 fall armyworm outbreak, underscoring pest volatility as a revenue lever.

Fruits and vegetables remain the most lucrative on a per-acre basis, with residue compliance dictating frequent use of low-dose formulations. California almonds and pistachios are migrating from banned organophosphates to selective spinosyn and diamide options, raising treated-acre value mix. Commercial crops such as cotton and sugarcane still depend on insecticides despite near-saturation trait adoption because refugia and resistance mitigation require complementary chemistry. Pulses and oilseeds witness steady growth as plant-based protein demand expands, encouraging acreage in the Northern Plains. Turf and ornamentals offer margin upside through premium labels tailored to aesthetic quality standards, although volumes are smaller. Collectively, these crop-specific patterns confirm the depth and breadth of the US insecticide industry’s end-user base.

Geography Analysis

The Midwest corn and soybean belt, encompassing key states, accounted for a significant portion of national volume in 2025. This growth was driven by widespread western corn rootworm resistance, necessitating both soil-applied and foliar interventions. Adoption of data-driven application timing has supported the use of premium narrow-window products. Despite stable planted areas, the insecticides market in the Midwest continues to grow due to rising per-acre expenditures.

California leads in specialty-crop value, with crops like almonds, grapes, citrus, and greenhouse vegetables generating the highest per-acre insecticide expenditures. Regulatory changes have accelerated the transition to selective diamides, increasing application costs while improving residue compliance for export markets. Protected agriculture acreage in California and neighboring regions has expanded, sustaining a premium for molecular innovations. Florida’s citrus sector remains a high-value cluster due to disease pressures requiring systemic trunk injections[3]Source: United States Department of Agriculture, “Citrus Fruits Report 2025,” USDA.gov.

The Southeast’s cotton and peanut systems rely heavily on foliar diamides to address bollworm resistance, resulting in a notable increase in diamide volumes. In the Delta rice and soybean region, the spread of fall armyworm has added late-season spray passes per crop cycle. The Pacific Northwest potato and vegetable sector has adopted precision chemigation and spot-spray robotics, a trend that may limit volume growth but increase unit pricing. Regional variations ensure that the US insecticide market continues to evolve in response to differing regulatory frameworks and pest pressures.

Competitive Landscape

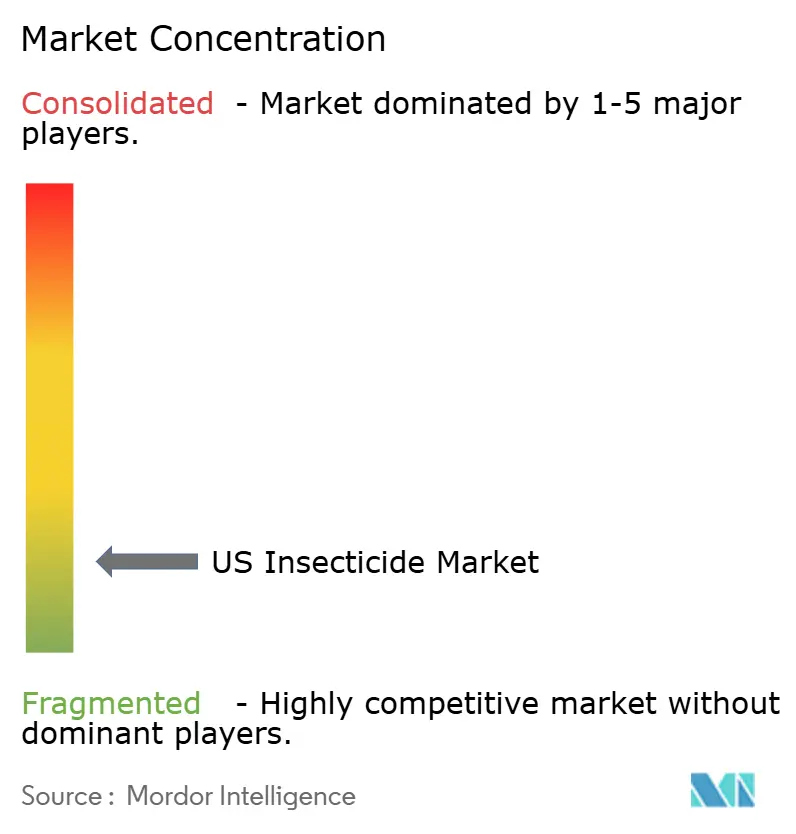

The US insecticide market exhibits low concentration in 2025, while numerous mid-tier and niche participants occupy the balance. BASF SE, Bayer AG, FMC Corporation, Syngenta Group, and Corteva Agriscience hold a significant market share. FMC Corporation, bolstered by its anthranilic diamides, Rynaxypyr and Cyazypyr, holds a notable share in the market. The company has expanded its reach by acquiring a majority stake in Nutrien’s retail network, adding several outlets that cater to numerous growers. Syngenta Group, leveraging thiamethoxam and lambda-cyhalothrin, holds a strong position in the market. Meanwhile, Corteva Agriscience, with its offerings of chlorantraniliprole and spinetoram, trails closely. Notably, these two products alone generated substantial domestic sales in 2024.

Bayer AG maintains a leading position in neonicotinoid seed treatments, though potential pollinator-related restrictions pose risks and have driven its focus on RNAi solutions. BASF SE is supported by the anticipated registration of meta-diamide broflanilide for use in rice and vegetables. Mid-tier companies such as Nufarm Ltd, UPL Ltd, and Sumitomo Chemical Company, Limited are leveraging their generic product portfolios to gain volume in cost-sensitive segments of the US insecticide market.

Leading players in the US insecticide market are prioritizing next-generation modes of action and precision application technologies. Bayer achieved a significant milestone with EPA approval for its RNAi seed treatment targeting western corn rootworm. This product is set to launch at a premium compared to conventional treatments. Meanwhile, FMC Corporation is increasing its diamide manufacturing capacity to meet anticipated growth in specialty crop demand. These strategic initiatives highlight the critical role of innovation in maintaining a competitive edge in the market.

US Insecticide Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BASF SE obtained EPA approval for isocycloseram, a broad-spectrum contact insecticide. The product targets lepidopteran pests and other insects affecting specialty crops.

- July 2025: ADAMA Ltd has officially rolled out Trinalor, a chlorantraniliprole-based insecticide. Specifically formulated for tree nuts and fruits, Trinalor targets pests like the navel orangeworm (NOW), codling moth, and leafrollers. The insecticide boasts a rapid knockdown effect and offers ingestion-based protection lasting up to three weeks.

- November 2023: FMC Corporation launched its next-generation seed treatment platform combining three active ingredients in a single formulation, reducing application complexity while providing comprehensive protection against soil-dwelling and early-season foliar pests in corn production systems.

US Insecticide Market Report Scope

Insecticides are chemical agents used in agriculture to control, repel, or eliminate insects that harm crops. These substances are intended to protect plants from pests such as beetles and aphids, thereby enhancing crop yield and ensuring food security. Insecticides function through contact, ingestion, or systemic action.

The US insecticide market report provides a comprehensive analysis of the industry, categorizing it by application mode and crop type. By application mode, the market includes chemigation, foliar, fumigation, seed treatment, and soil treatment. By crop type, it covers commercial crops, fruits and vegetables, grains and cereals, pulses and oilseeds, and turf and ornamental. Market estimates and forecasts are presented in both value (USD) and volume (metric tons).

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| By Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| By Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms