Insect Repellent Active Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

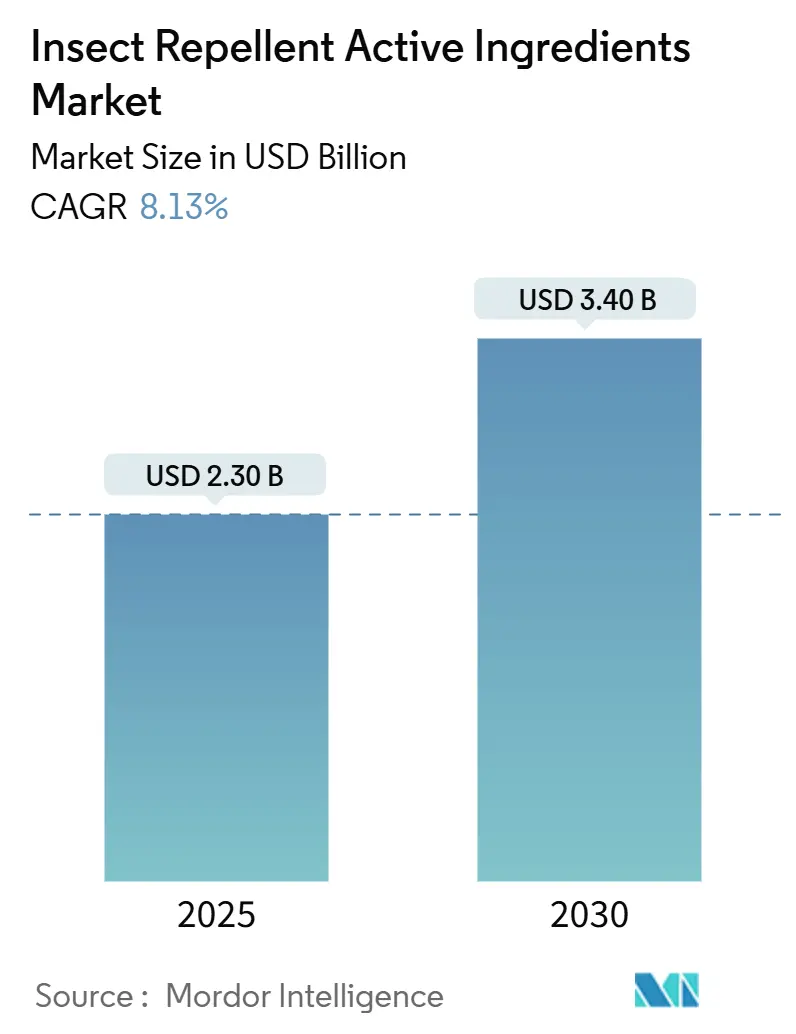

| Market Size (2025) | USD 2.30 Billion |

| Market Size (2030) | USD 3.40 Billion |

| Growth Rate (2025 - 2030) | 8.13% CAGR |

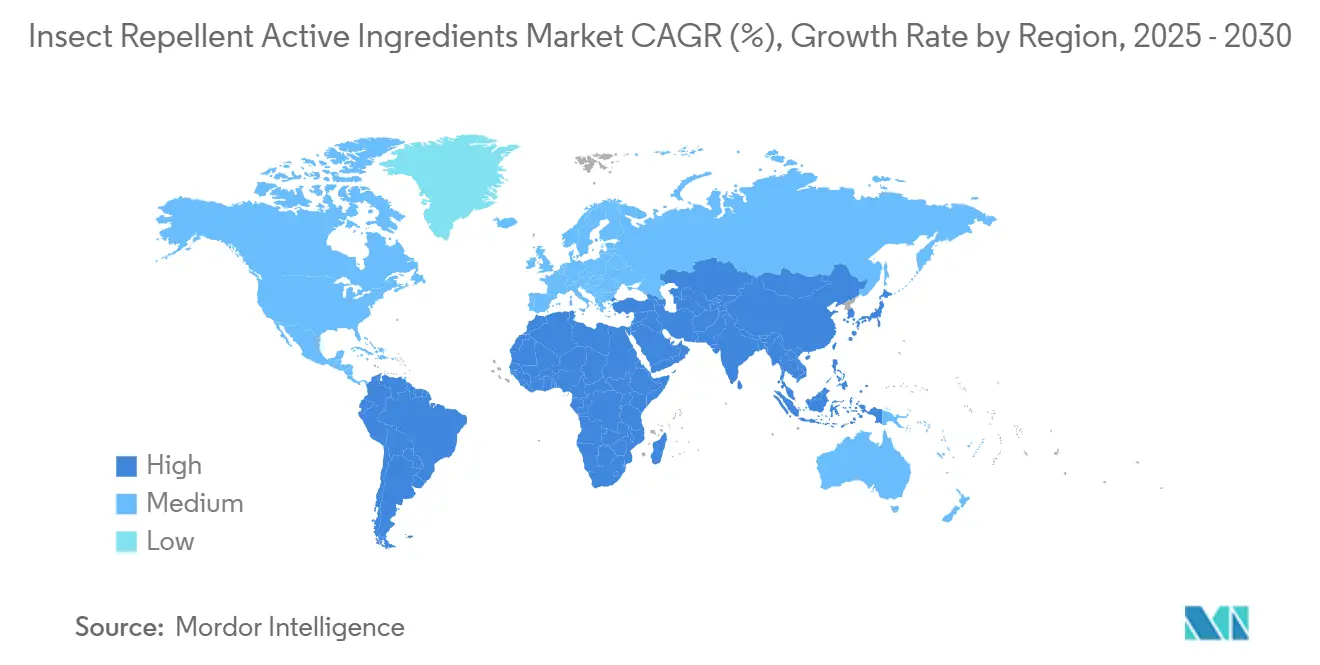

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insect Repellent Active Ingredients Market Analysis by Mordor Intelligence

The insect repellent active ingredients market size for agriculture is valued at USD 2.30 billion in 2025 and is forecast to reach USD 3.40 billion by 2030, advancing at an 8.13% CAGR during the period 2025-2030. Growth stems from rising pest resistance, tighter residue rules, and rapid adoption of precision formulations that lengthen efficacy windows at lower application rates. Climate-driven pest range expansion forces growers to seek dual-mode chemistries able to control both endemic and invasive species, while nanocarrier platforms help address labor shortages by cutting spray frequency. Bio-based terpene discovery pipelines accelerate as regulators favor natural products with benign eco-profiles, and regional modernization programs in Asia-Pacific drive uptake of advanced delivery technologies. Strategic collaborations between large multinationals and specialty innovators further shape the insect repellent active ingredients market through the co-development of proprietary slow-release systems and peptide-based biocontrols.

Key Report Takeaways

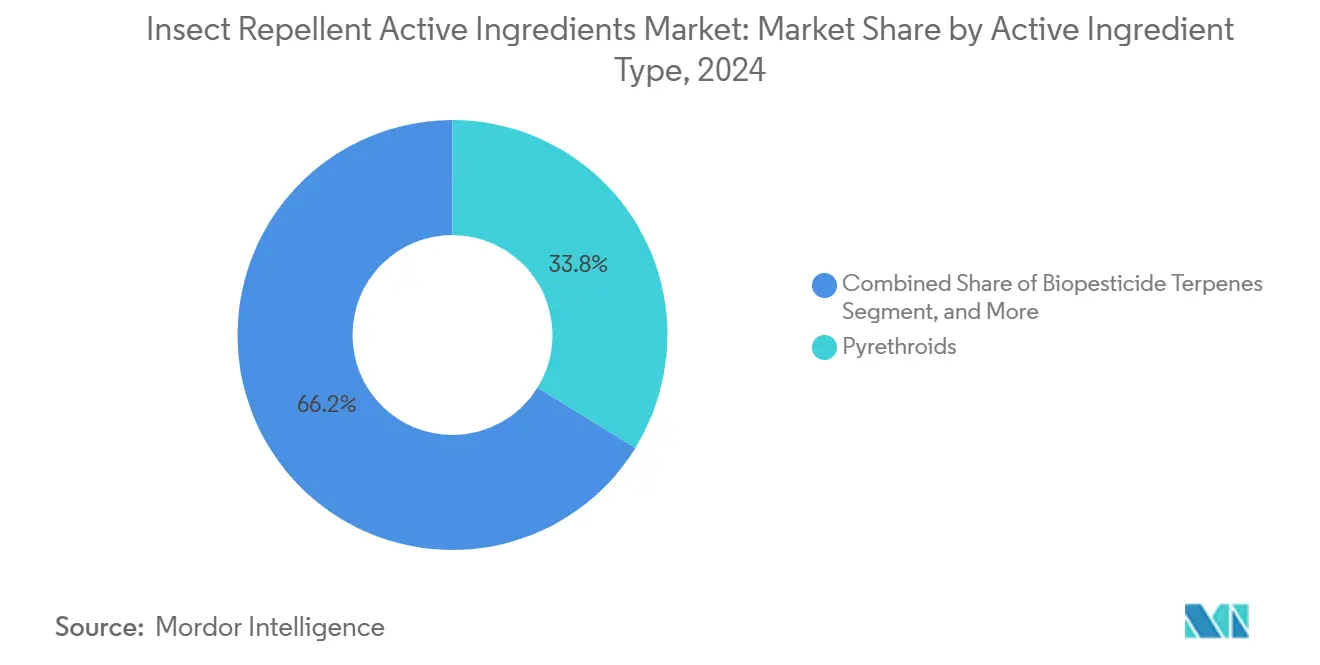

- By active ingredient type, pyrethroids led with 33.8% insect repellent active ingredients market share in 2024, whereas biopesticide terpenes are projected to expand at a 10.9% CAGR to 2030.

- By formulation form, emulsifiable concentrates held 37.5% in the insect repellent active ingredients market size in 2024, while nano-emulsions post the highest projected CAGR at 11.0% through 2030.

- By mode of application, foliar sprays accounted for 42.6% of the insect repellent active ingredients market value in 2024, and seed treatment repellents are advancing at a 9.1% CAGR through 2030.

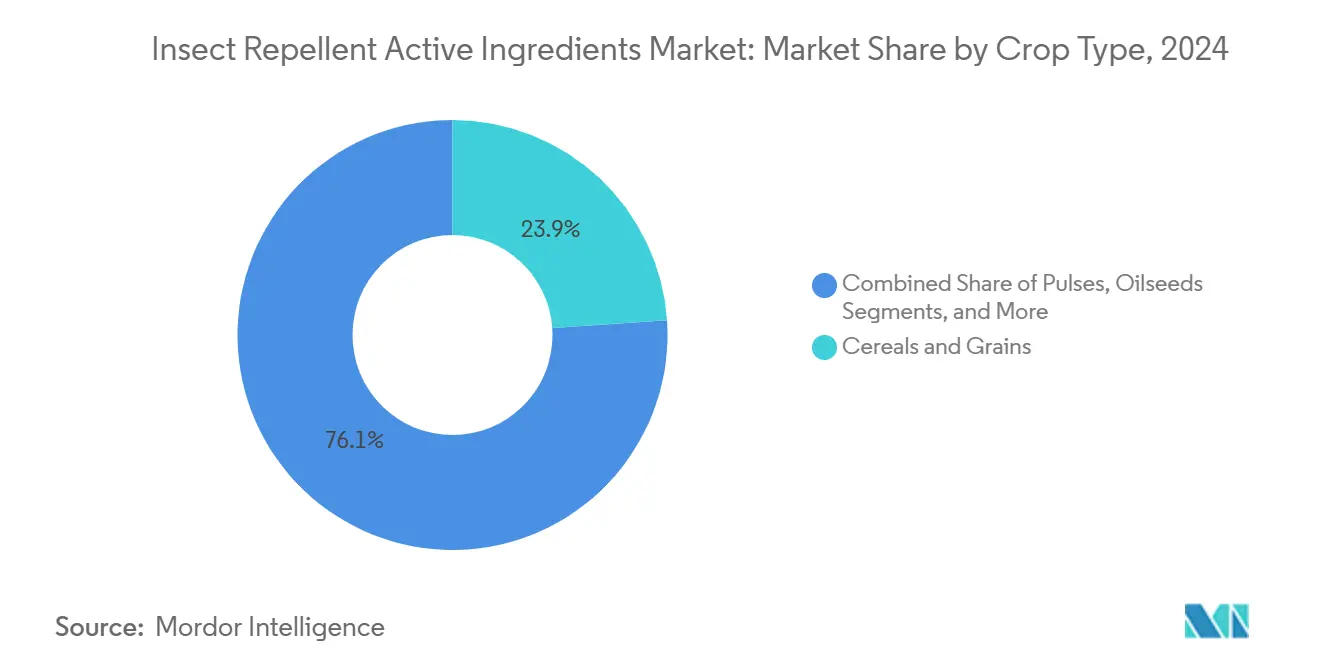

- By crop type, cereals and grains captured a 23.9% share in 2024; fruits and vegetables are forecast to grow at an 11.6% CAGR to 2030.

- By geography, North America commanded 32.5% of the 2024 value, while Africa records the fastest regional CAGR at 9.4% through 2030.

- By competitive position, the five largest suppliers controlled 42.5% market share in 2024, creating a moderately fragmented field with room for regional specialists.

Global Insect Repellent Active Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-based terpene discovery pipelines | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Nanocarrier-enabled slow-release actives | +1.5% | North America, Europe, and Asia-Pacific core markets | Medium term (2-4 years) |

| Proliferation of regenerative farming practices | +1.2% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Increasing regulatory approvals for dual-mode chemistries | +1.0% | North America, Europe, and select Asia-Pacific markets | Short term (≤ 2 years) |

| Climate-driven expansion of pest pressure zones | +0.9% | Global, with highest impact in tropical and subtropical regions | Long term (≥ 4 years) |

| Farm labor shortages accelerating aerial application demand | +0.7% | North America, Europe, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bio-based Terpene Discovery Pipelines

Plant-derived terpenoids now anchor the fastest-growing branch of the insect repellent active ingredients market, helped by regulatory incentives and consumer demand for eco-safe inputs. Research shows geraniol achieves 100% mortality against scabies mites at only 6.25% concentration within 15 minutes. Microwave and ultrasonic extraction raise yields without degrading bioactivity, lowering costs for commercial scale. Companies are mapping terpene synthase genes in crops such as Lanxangia tsaoko, uncovering 42 enzymes that collectively open hundreds of new molecular leads. These discoveries enable resistance-breaking formulations that fit organic, regenerative, and export-oriented systems. Investors fund dedicated fermentation lines that standardize supply and tame raw-material volatility. As approvals accelerate, terpenes migrate from niche fruit and vegetable uses into broad-acre cereals, reinforcing their strategic weight in the insect repellent active ingredients market.

Nanocarrier-Enabled Slow-Release Actives

Nanotechnology upgrades traditional spray chemistry by improving solubility, shielding actives from UV degradation, and metering release over weeks rather than days. Core-shell fibers loaded with plant volatiles deliver attraction cues for up to 80 days with 78% encapsulation efficiency, eclipsing commercial benchmarks. Sodium-alginate microcapsules preserve 89.5% of Beauveria bassiana conidia viability, raising diamondback moth mortality to 83.1%, versus 64.8% for conventional dusts. Drone-optimized nano-emulsions achieve uniform droplet sizes below 44 nanometers, improving canopy coverage and cutting active dose by 30%. Together, these advances lower labor needs, align with aerial delivery, and underpin premium pricing across the insect repellent active ingredients market.

Proliferation of Regenerative Farming Practices

Growers pursuing soil health and biodiversity now seek chemistries compatible with beneficial insects and microbial communities. Landscape complexity studies reveal that diversified field margins narrow organic yield gaps by supporting native predators. Adaptive multi-paddock grazing increases arthropod guild diversity without boosting pest counts, encouraging selective interventions over blanket sprays. Pollinator-safe terpene blends enable dual insect control and pollination services, generating economic gains even when yield impacts are modest. Digital twin platforms extend regenerative logic by optimizing the timing and placement of low-impact actives with 88% prediction accuracy. These factors elevate demand for targeted, residue-light solutions that define the future insect repellent active ingredients market.

Increasing Regulatory Approvals for Dual-Mode Chemistries

Authorities expedite reviews for active ingredients offering new modes of action and resistance management benefits. The US EPA accepted applications for Bacillus thuringiensis strain RTI545 seed treatments in 2024, signaling readiness to green-light biologicals at commercial scale [1]Source: Environmental Protection Agency, “Receipt of Applications for New Active Ingredients,” federalregister.gov . Syngenta’s isocycloseram secured registrations in 40 countries within three years, a pace once reserved for blockbuster herbicides. BASF invested USD 981 million annually in molecule discovery, with heteroaryl compounds now patent-protected for broad invertebrate control. This regulatory tailwind compresses time-to-market, supports premium pricing, and strengthens the pipeline feeding the insect repellent active ingredients market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicology data gaps delaying registrations | -1.3% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Volatility of terpene raw-material feedstocks | -1.1% | Global, with concentration in regions dependent on natural extraction | Medium term (2-4 years) |

| Cross-resistance with existing insecticides | -0.9% | Global, with highest impact in intensive agriculture regions | Long term (≥ 4 years) |

| Stringent maximum residue limits in export markets | -0.8% | Global, with particular impact on export-oriented agriculture | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicology Data Gaps Delaying Registrations

Comprehensive risk assessments for next-generation actives test capacity at many firms. EPA biological evaluations found that dinotefuran threatened 75% of listed species and 78% of habitats, prompting new mitigation measures [2]Source: Environmental Protection Agency, “Biological Evaluations of Dinotefuran and Acetamiprid,” epa.gov. EFSA cut the acceptable daily intake for acetamiprid after developmental neurotoxicity concerns, requiring fresh chronic studies [3]Source: EFSA, “Toxicological Properties of Acetamiprid,” efsa.europa.eu . For natural terpenes, existing protocols often fail to capture novel pathways, forcing extensive in-house method development. Smaller innovators face multi-million-dollar testing bills and multi-year delays that can erode patent life. Supply chains stall while waiting for definitive residue, ecotoxicity, and endocrine data. Consequently, promising solutions may miss peak pest windows, slowing near-term growth in the insect repellent active ingredients market.

Volatility of Terpene Raw-Material Feedstocks

Most industrial terpenes still rely on plant distillation or solvent extraction, processes vulnerable to weather shocks and land-use change. Extreme heat reduces essential oil yields in mint and eucalyptus by up to 25%, inflating input costs and disrupting contract manufacturing. Competing demand from cosmetics and aromatherapy markets tightens supply during peak agricultural seasons. Currency swings in producer countries add pricing noise, while phytosanitary incidents can provoke temporary trade bans. These fluctuations complicate long-term offtake agreements and discourage growers from switching out of predictable synthetic options. Although fermentation and synthetic biology offer stability, scale-up timelines stretch beyond the forecast horizon, tempering adoption of terpene-heavy products within the insect repellent active ingredients market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Active Ingredient Type: Biopesticides Challenge Synthetic Dominance

The insect repellent active ingredients market represents a 33.8% share for pyrethroids in 2024. Yet, regulatory scrutiny over aquatic toxicity and mounting resistance in fall armyworm populations intensifies pressure on this long-standing leader. Biopesticide terpenes, while smaller today, post a 10.9% CAGR, the highest within the taxonomy, as brands capitalize on fast-track approvals and favorable consumer perception. Organophosphates occupied a significant share through entrenched usage in developing regions, even as phased bans edge forward in Europe. Neonicotinoids retreat under bee health concerns, though seed-treatment formulations preserve a toehold in cereals. DEET derivatives and assorted chemistries serve livestock and specialty crops, commanding premium prices but modest volumes, underscoring the diverse, yet shifting, competitive terrain of the insect repellent active ingredients market.

Ongoing R&D pours into encapsulated essential oils that extend field life, such as β-cyclodextrin complexes that enhance fennel and basil oil stability. Bacillus-based products gain durability from sulfur quantum dot UV shields, lifting spore viability above 57% over four days of midday sun. These gains validate biologicals for broad-acre use and encourage portfolio balancing among multinationals. Investors recognize that diversified pipelines help hedge resistance liabilities and meet tightening residue limits in export markets. As trials document equivalent efficacy with improved safety, purchasing managers view terpenes and microbial toxins as risk-mitigating complements rather than fringe options, anchoring long-run rebalancing of the insect repellent active ingredients market.

By Formulation Form: Nano-Emulsions Drive Innovation

Emulsifiable concentrates command 37.5% of the global insect repellent active ingredients market size due to mature manufacturing assets and compatibility with a wide array of sprayers. However, nano-emulsions deliver the fastest 11.0% CAGR because droplet sizes below 50 nanometers improve cuticular penetration and rainfastness, reducing re-spray events by up to one-third. Microencapsulated suspensions, being one of the major segments by formulation form, employ polymeric walls that modulate release and minimize off-target drift, aligning with buffer-zone rules in Europe. Wettable powders and water-dispersible granules remain fixtures for regions lacking cold-chain logistics, though their shares gradually shrink as liquid systems dominate drone fleets. Firms race to engineer hybrid formulations that suspend nano-emulsified terpenes inside biodegradable capsules, uniting the best of both worlds and pushing formulation science to the strategic core of the insect repellent active ingredients market.

Ultrasonic processing enables solvent-free nano-emulsions of Cananga odorata oil with droplet uniformity that closely tracks commercial synthetic benchmarks. Metal-oxide nanoparticles, such as zinc and copper actives, emerge as dual insecticide and micronutrient inputs, easing formulation loadings and field handling. Industry investment shifts toward pilot-scale reactors capable of continuous inline emulsification, supporting just-in-time customization for local pest spectra. These technology leaps help meet the aerial application boom by supplying thermally stable, low-viscosity fluids that resist nozzle clogging. Collectively, formulation innovation redefines value capture, elevating chemistry plus delivery as inseparable levers inside the insect repellent active ingredients market.

By Mode of Application: Seed Treatments Gain Momentum

Foliar sprays still dominate at 42.6% of the insect repellent active ingredients market size in 2024 because growers value visual coverage and rapid knockdown. Yet seed-applied repellents are scaling quickly with 9.1% CAGR as they protect seedlings during their most vulnerable phase and limit farmworker exposure. Electrostatically charged coats raise active deposition threefold, with residue assays confirming 147.63 ng µL¹ versus 47.37 ng µL¹ under conventional dressing. Livestock formulations, although niche, see renewed interest for pasture insects after Mustang Max earned zero-day grazing intervals from the EPA in July 2025. Soil drenches maintain relevance where root feeders threaten stands, particularly in tropical horticulture, but face substitution as systemic seed technologies mature. These shifts reinforce the alignment between precision placement and sustainable stewardship, guiding the insect repellent active ingredients market.

Seed-treatment pioneers refine polymer binders that release actives synchronously with radicle emergence, reducing dust-off and safeguarding pollinators. In the United States, neonicotinoid coatings add measurable yield in corn, especially in warmer southern belts where soil insects proliferate. Meanwhile, Syngenta’s divestment of FarMore vegetable platform to Gowan SeedTech illustrates portfolio pruning that tightens focus on proprietary actives while outsourcing application know-how. Integration of biologicals into seed coatings accelerates as companies co-formulate peptides, microbes, and terpenes into multipurpose pelleting slurries. Such advances place seed treatments at the nexus of yield insurance and environmental compliance inside the insect repellent active ingredients market.

By Crop Type: Specialty Crops Drive Premium Pricing

Cereals and grains secure a 23.9% insect repellent active ingredients market share by virtue of acreage dominance, yet growth slows as commodity margins compress and adoption of GM traits stabilizes. Fruits and vegetables, registering 11.6% CAGR, command high residual control standards and reward residue-compliant actives with specialty pricing. Oilseeds at 18.4% share battle insects like soybean looper that increasingly withstand historical chemistries, spurring demand for dual-mode seed treatments and foliar stacks. Pulse crops and miscellaneous categories collectively represent a strategic frontier for biological blends that deliver both insect suppression and plant health benefits, aligning with smallholder needs across Asia and Africa. These crop-specific dynamics weave a tapestry of micro-markets that collectively shape the tactical allocation of R&D budgets within the insect repellent active ingredients market.

Apple orchards adopting integrated pest management increase natural enemy density while maintaining economic thresholds, although some yield penalties arise in suboptimal seasons. Okra growers combining plant-based sprays with entomopathogenic fungi secure 8.97 t/ha yields and improved returns, proof that biologicals can meet high-value crop standards. Digital decision aids that simulate pest outbreaks raise profits by 20% in greenhouse peppers, illustrating how data fusion augments chemical stewardship. These examples highlight the differentiated yet converging criteria that producers weigh when selecting actives, affirming the nuanced segmentation inside the insect repellent active ingredients market.

Geography Analysis

North America leads the insect repellent active ingredients market with a 32.5% share in 2024, underpinned by robust R&D ecosystems and a regulatory landscape that balances innovation with stewardship. Adoption of drone spraying surged, catalyzing uptake of nano-emulsion concentrates optimized for aerial delivery. The region’s growth slows through 2030 as saturation in broad-acre cereals tempers upside, though ongoing pest resistance challenges sustain demand for dual-mode products. Climate change extends pest pressure northward, compelling maize and soybean growers in Canada to trial seed-applied bio-insecticides for fall armyworm.

Africa leads regional growth rates at 9.4% CAGR, reflecting agricultural development initiatives and increasing food security concerns that create demand for effective pest management solutions. Asia-Pacific exhibits the fastest 9.1% CAGR as mechanization and digital farming penetrate China, India, and Southeast Asia. Biopesticide consumption rises as local governments prioritize rural health and food safety. China stabilizes chemical pesticide usage around 245,000 metric tons, yet grows Bacillus-based output for domestic and export vegetable markets. India posted 416 pesticide product approvals in 2024, indicating a dynamic regulatory environment open to innovation. Parallel growth in drone fleets, especially in Japan and China, elevates demand for thermally stable nano-emulsions. These trends cement the region as the growth epicenter of the insect repellent active ingredients market. The Middle East follows closely at 8.3% CAGR, while South America registers 7.9% growth driven by expanding agricultural production and export market development.

Europe's insect repellent active ingredients market is fueled by stringent maximum residue mandates that propel bio-based solutions and precision equipment. Approval cycles for novel actives accelerate under the EU sustainable pesticide regulation draft, yet the farm-to-fork objective capping chemical use at 50% by 2030 tightens compliance requirements. Regional growth indicates maturity, though regenerative agriculture subsidies and carbon credit schemes create incentives for eco-friendly actives. Multinationals pilot low-dose terpene seed dressings in France and Spain to secure export market access under shifting MRL ceilings.

Competitive Landscape

The insect repellent active ingredients market is moderately fragmented, with the top five companies, such as Corteva Agriscience, Syngenta AG, Bayer AG, BASF SE, and FMC Corporation, holding 42.5% market share in 2024. Corteva Agriscience leads the market, bolstered by a broad cereal portfolio and recent peptide biocontrol alliance with Micropep that accelerates entry into biological segments. Syngenta follows owing to the rapid global rollout of isocycloseram, a dual-mode insecticide that aligns with resistance-management mandates. Bayer leverages trait stacks and targeted seed coatings, while BASF funnels USD 981 million annually into new molecules, including heteroaryl compounds with novel binding sites free of cross-resistance.

Mid-tier firms such as Sumitomo Chemical Co., Ltd, UPL, and PI Industries capitalize on region-specific registrations and cost-effective manufacturing. Emerging specialists exploit white spaces in climate-adaptive formulations and regenerative farming aids. Strategic moves include Syngenta’s divestiture of FarMore seed technology to Gowan SeedTech, facilitating focus on proprietary chemistries while empowering partners to extend application reach.

FMC’s EPA-cleared Mustang Max pyrethroid for pasture illustrates niche expansion through label extensions. Overall, competition hinges on capacity to bundle chemistry with digital decision tools, residue stewardship, and flexible manufacturing with capabilities increasingly critical for navigating the evolving insect repellent active ingredients market.

Insect Repellent Active Ingredients Industry Leaders

Corteva Agriscience

Syngenta AG

Bayer AG

BASF SE

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: FMC has introduced Ethos Elite LFR, an at‑plant premix combining bifenthrin with two proprietary Bacillus strains (B. velezensis RTI301 and B. subtilis RTI477). It was launched in the United States market, which offers broad-spectrum control against early-season soil pests (e.g., rootworms, wireworms) and diseases (e.g., Fusarium, Pythium), while promoting seedling vigor and root development.

- May 2023: BASF introduced Axalion Active (active ingredient: dimpropyridaz), the first novel IRAC Group 36 mode‑of‑action for piercing and sucking insects since 2015. This unique chemistry disrupts insect sensory chordotonal organs, offering farmers a potent tool against resistant pests while being safe for beneficial species.

- May 2023: BASF introduced Cimegra, a pesticide containing the active ingredient broflanilide, which is registered under IRAC Group 30. The product launched in Indonesia, following its earlier releases in China and India. Cimegra provides broad-spectrum protection against various pests, including thrips, Spodoptera, Plutella, diamondback moth, wireworms, and Colorado potato beetle. The product's unique mode of action shows no known cross-resistance and delivers rapid pest control.

Global Insect Repellent Active Ingredients Market Report Scope

| Pyrethroids |

| Organophosphates |

| Neonicotinoids |

| Biopesticide Terpenes |

| DEET Derivatives |

| Other Chemistries |

| Emulsifiable Concentrates |

| Wettable Powders |

| Microencapsulated Suspensions |

| Nano-Emulsions |

| Water-Dispersible Granules |

| Other Forms |

| Seed Treatment Repellents |

| Foliar Sprays |

| Livestock Repellents (Cattle, Poultry) |

| Soil Treatments |

| Cereals and Grains |

| Pulses |

| Oilseeds |

| Fruits and Vegetables |

| Other Crops |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Spain | |

| Italy | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Vietnam | |

| Philippines | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Active Ingredient Type | Pyrethroids | |

| Organophosphates | ||

| Neonicotinoids | ||

| Biopesticide Terpenes | ||

| DEET Derivatives | ||

| Other Chemistries | ||

| By Formulation Form | Emulsifiable Concentrates | |

| Wettable Powders | ||

| Microencapsulated Suspensions | ||

| Nano-Emulsions | ||

| Water-Dispersible Granules | ||

| Other Forms | ||

| By Mode of Application | Seed Treatment Repellents | |

| Foliar Sprays | ||

| Livestock Repellents (Cattle, Poultry) | ||

| Soil Treatments | ||

| By Crop Type | Cereals and Grains | |

| Pulses | ||

| Oilseeds | ||

| Fruits and Vegetables | ||

| Other Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Spain | ||

| Italy | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Vietnam | ||

| Philippines | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the insect repellent active ingredients market?

The insect repellent active ingredients market size stands at USD 2.30 billion in 2025 and is projected to reach USD 3.40 billion by 2030.

Which active ingredient segment is growing the fastest?

Biopesticide terpenes record the quickest expansion, posting a 10.9% CAGR on regulatory preference for natural chemistries.

Why are nano-emulsions gaining traction in agricultural insect control?

Nano-emulsions boost bioavailability and rain fastness while enabling drone spraying, driving an 11.0% CAGR for this formulation type.

How does climate change influence demand for insect repellent actives?

Warming temperatures expand pest ranges, creating sustained demand for dual-mode chemistries able to protect crops in new pressure zones.

Page last updated on: