Morocco Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

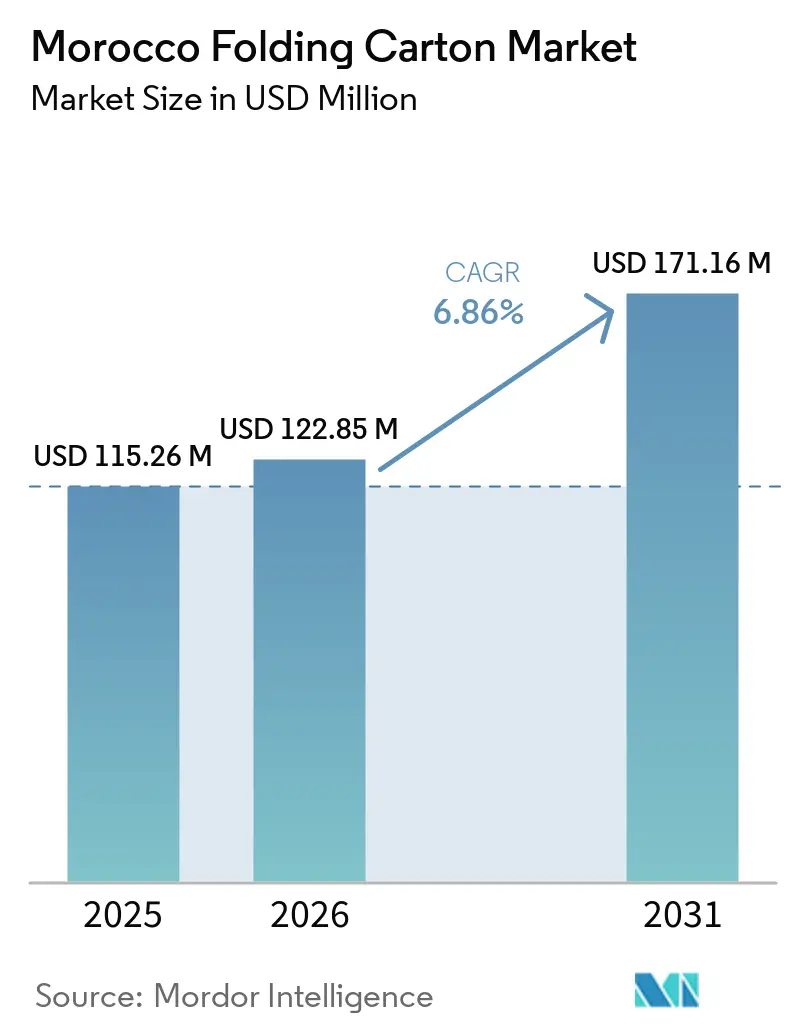

| Base Year Market Size (2025) | USD 115.26 Million |

| Market Size (2026) | USD 122.85 Million |

| Market Size (2031) | USD 171.16 Million |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

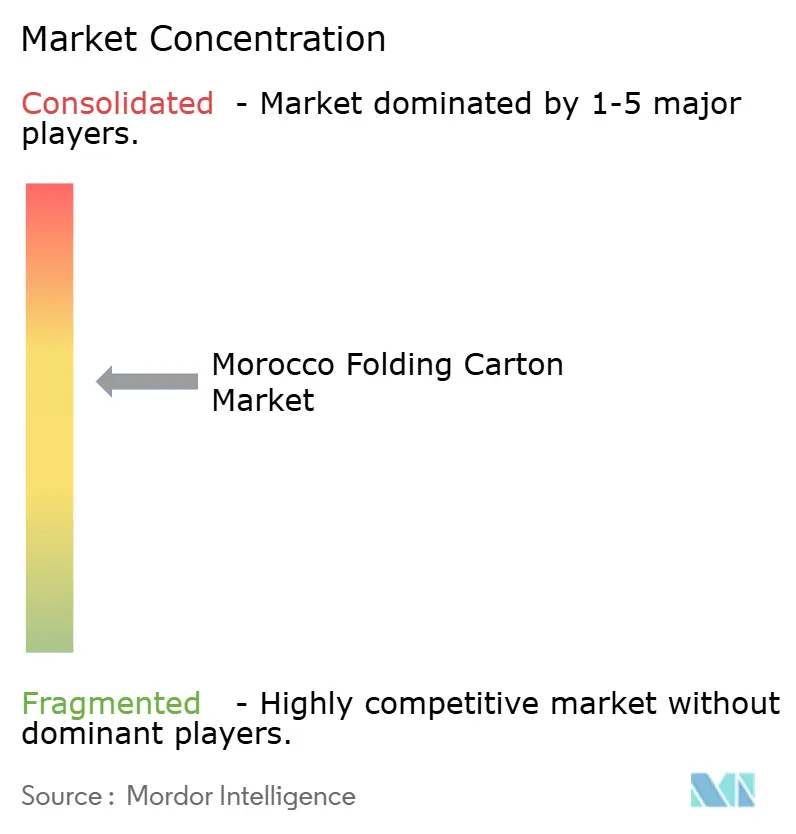

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Folding Carton Market Analysis by Mordor Intelligence

The Morocco folding carton market size is projected to expand from USD 115.26 million in 2025 to USD 122.85 million in 2026 and reach USD 171.16 million by 2031, registering a 6.86% CAGR between 2026 and 2031. Morocco has become the region’s low-cost export hub for paper-based packaging, shipping 21,000 tonnes of board in 2024 at an average free-on-board price of USD 745 per tonne, well below MENA peers. Private and multilateral capital is accelerating equipment upgrades, with EU-backed green-transition grants and the EBRD Green Value Chain facility steering converters toward energy-efficient presses and recycled-fiber lines. Demand is also buoyed by Morocco’s fruit-and-vegetable export boom, where high-value tomato, citrus, and red-fruit cartons require moisture barriers and digital traceability. At the same time, organized grocery chains, e-commerce platforms, and cosmetics brands are tightening graphics specifications and sustainability targets, driving sustained uptake of premium substrates and digital print formats.

Key Report Takeaways

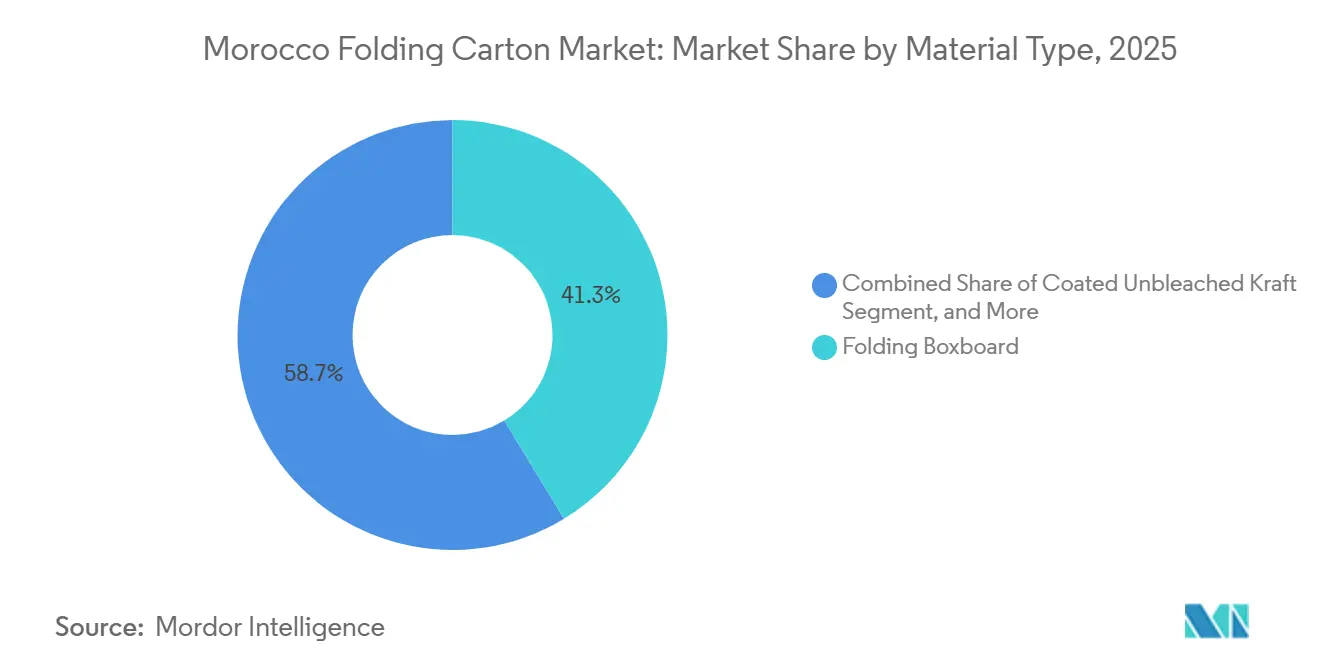

- By material type, folding boxboard captured with 41.32% of the Morocco folding carton market share in 2025.

- By printing technology, the Morocco folding carton market size for digital printing is projected to grow at a 8.73% CAGR to 2031.

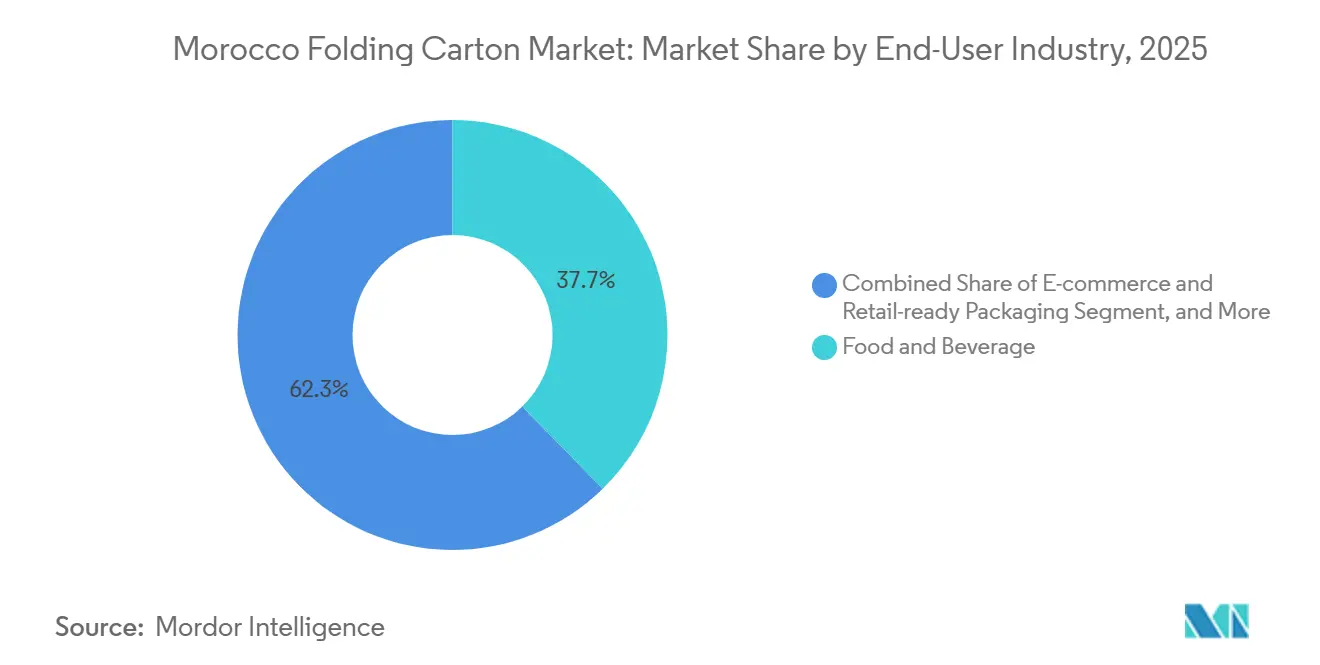

- By end-user industry, the food and beverage industry captured 37.69% of the Morocco folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Morocco's Export-Oriented Agri-Food Sector | +1.8% | National, Souss-Massa, Gharb, Fès-Meknès | Medium term (2-4 years) |

| Government Ban on Single-Use Plastic Bags Accelerating Carton Shift | +1.2% | National, organized retail zones | Short term (≤ 2 years) |

| Rapid Growth of Organized Retail Chains | +1.4% | Casablanca, Rabat, Marrakech, Tangier | Medium term (2-4 years) |

| Rising E-commerce Fulfillment Centers Around Casablanca-Settat | +1.1% | Casablanca-Settat core | Long term (≥ 4 years) |

| Investments in Offset Litho Presses by Local Converters | +0.7% | Industrial zones nationwide | Medium term (2-4 years) |

| EU-Morocco Green Packaging Compliance Grants | +0.6% | Export-oriented converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Morocco's Export-Oriented Agri-Food Sector

Higher-value tomato cultivars, citrus, and red fruits now dominate outbound produce, with tomato shipments hitting a record 745,000 tonnes in the 2024-2025 season. Premium 10 kg cartons featuring moisture-resistant liners and digital branding replace generic corrugated cases, boosting substrate and ink consumption. Export volumes rose 15% between 2023 and 2025, but tighter EU pricing is compressing packer margins, heightening demand for lightweight, cost-optimized carton designs.[1]Ayoub Arhzaf and Fadoua Eljai, “Moroccan exports of fruits and vegetables,” Agricultural Economics Review, aer.web.auth.gr Non-compliant labels accounted for over half of US border rejections of Moroccan produce, so converters offering FDA- and EU-ready cartons gain a commercial edge. FAO-EBRD technical support is channeling subsidies into citrus and avocado value chains, steering growers toward certified folding carton solutions.

Government Ban on Single-Use Plastic Bags Accelerating Carton Shift

Law 77-15 bans thin plastic carrier bags, with 742 tonnes seized at borders and 3,000 tonnes in commerce since 2016. Enforcement gaps remain, but modern retailers have largely switched to shelf-ready carton multipacks. The Ministry of Industry earmarked MAD 200 million (USD 20.2 million) for converter upgrades, while non-woven polypropylene bags surged to 3.2 billion units, indicating loopholes that still help carton demand inside supermarkets. Informal souks continue to rely on illicit plastics, creating a two-tier market where folding carton penetration tracks retail formalization.

Rapid Growth of Organized Retail Chains

Modern grocery outlets expanded 11% in 2024, outpacing regional peers. Label’Vie’s 179 Carrefour-branded stores generated nearly MAD 16 billion (USD 1.56 billion) in sales and raised USD 100 million in bonds for further expansion. BIM added 144 stores in 2025, bringing its total nationwide to 1,000. Casino will inject MAD 1 billion (USD 97.5 million) to open 210 Franprix and Monoprix units by 2035. These chains demand standardized shelf-ready cartons, private-label artwork, and logistics-friendly footprints, lifting long-run litho and flexo volumes.

Rising E-Commerce Fulfillment Centers Around Casablanca-Settat

Online sales hit USD 1.7 billion in 2025 and could reach USD 3.5 billion by 2029. Mobile transactions account for 68% of payments, driving increased demand for small-format cartons for apparel, electronics, and beauty products. Fulfillment clusters in Casablanca-Settat drive 24-hour delivery promises, so converters near the metro benefit from just-in-time orders and return-ready designs. Cash-on-delivery’s share fell to 52%, signaling maturing payment rails that enable higher order frequency and standardized pack sizes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Imported Pulp Prices | -0.9% | Import-dependent converters | Short term (≤ 2 years) |

| Limited Domestic Virgin Fiber Availability | -0.6% | Nationwide | Long term (≥ 4 years) |

| Skilled Press Operator Shortage Outside Urban Hubs | -0.4% | Secondary cities | Medium term (2-4 years) |

| Port Congestion Impact on Lead Times | -0.5% | Casablanca, Tanger Med | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Imported Pulp Prices

Morocco imported MAD 308.6 million (USD 37.6 million) of pulp in 2014 before sliding to recent lows, underscoring its exposure to global price swings. Local eucalyptus mills supply just 125,000 tonnes of virgin fiber, most exported, obliging converters to buy European board at spot rates denominated in euros, amplifying currency risks. GPC’s MAD 300 million (USD 36.6 million) recycling plant in Kénitra will capture waste fiber, yet recycled stock cannot replace virgin Solid Bleached Sulfate in premium pharma cartons. Until upstream capacity deepens, pricing volatility will curb margin visibility and capex appetite.

Port Congestion Impact on Lead Times

Casablanca and Tanger Med handled 11.1 million TEU in 2025, brushing 98% of design capacity. Q1 2026 storms and Red Sea diversions pushed January cargo arrivals out to May, forcing importers to divert to Spanish ports. Carriers levied war-risk surcharges of USD 1,500-3,300 per box, while demurrage climbed to USD 10,000 per vessel day. Delayed board and ink inflows idled converter lines, stalled agricultural exports, and raised inventory finance costs. Marsa Maroc’s USD 49 million quay-deepening project, due in 2028, will help, but near-term logistics risks persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Substrates Gain as Exports Climb

Folding Boxboard captured 41.32% of the Morocco folding carton market in 2025, anchored in cost-sensitive baked goods, snacks, and dairy cartons demanded by expanding supermarket chains. Solid Bleached Sulfate, however, is on an 8.27% CAGR trajectory to 2031, reflecting stricter EU food-contact rules and the rise of moisture-resistant tomato and red-fruit cartons. The Morocco folding carton market size for high-barrier substrates is therefore set to widen alongside agricultural premiumization. GPC’s Mohammedia plant, equipped with Africa’s first digital-flexo hybrid, now prints short-run, high-definition labels on SBS boards for export-grade produce, ramping run-and-change cycles from hours to minutes.

Rising EU sustainability metrics reward FSC-certified and traceable substrates, nudging exporters toward SBS and specialty laminates despite import premiums. Domestic recycled-fiber investments ease price pressure in mid-grade cartons, yet virgin board demand remains sticky where odor, brightness, and hygiene matter. The Morocco folding carton market continues to split along value lines: Folding Boxboard dominates domestic FMCG displays, while Solid Bleached Sulfate gains in export produce, cosmetics, and pharma, generating margin uplift for converters that master both supply chains.

By Printing Technology: Digital Gains Traction for Export Customization

Lithographic presses held a 45.88% share in 2025 because high-volume cereal and confectionery cartons still favor offset’s unit economics. Digital printing, however, is growing at 8.73% CAGR as exporters embrace QR-coded traceability and country-of-origin branding. Converters adopting hybrid lines can swap between flexo solids and digital variable graphics without plating downtime, cutting make-ready waste by up to 20%. That agility anchors the Morocco folding carton market size allocated to export-grade short runs.

Offset’s installed base in Casablanca, Rabat, and Tangier secures medium-term volumes, yet offset press investments are shifting toward automated plate mounting and closed-loop color controls to defend cost competitiveness. Flexography remains dominant for brown corrugated cases for bulk tomatoes and citrus, whereas gravure serves cigarette and liquor cartons that require long-run metallic fidelity. As brands favor multi-SKU promotions, digital’s share will rise, but hybrid offset-digital workflows will bridge the cost-quality gap for converters straddling domestic and EU clients.

By End-User Industry: E-Commerce Outpaces Traditional Retail

Food and Beverage accounted for 37.69% of 2025 revenue, tied to Morocco’s USD 11.6 billion packaged-food sector, which is expanding at a 21.6% CAGR to USD 14.9 billion by 2028. Yet E-commerce and Retail-ready Packaging will clock the fastest 8.85% CAGR as online baskets proliferate. The Morocco folding carton market share devoted to e-commerce protective cartons is therefore set to climb, particularly for apparel, electronics, and beauty-care segments.[2]Hongli Wang, “Market overview – Morocco,” agriculture.canada.ca Return-ready locks, tamper seals, and branded interiors now headline bid specifications, favoring converters with CAD-driven design and drop-test labs.

Healthcare and Pharmaceuticals deepen demand for small-format SBS cartons printed with DataMatrix codes for anticounterfeit compliance. Personal Care and Cosmetics, buoyed by USD 111 million in online beauty sales, favors luxury embellishments, lifting hot-foil and spot-UV usage. Electrical and Electronics cartons must absorb shock and static, while tobacco and household goods offer steady but slower-growing volumes. Collectively, end-user diversification cushions the Morocco folding carton industry from agri-seasonality and positions converters to ride the e-commerce wave.

Geography Analysis

Most folding cartons are consumed domestically, yet export orientation is rising. Morocco shipped 21,000 tonnes of board in 2024, accounting for 56% of MENA flows, while importing 7,400 tonnes of premium grades. Rabat-Salé-Kénitra and Tangier-Tétouan-Al Hoceima follow, aided by free-zone tax incentives and proximity to ports.[3]Alexandre Bazillac, “Morocco is struggling to structure and develop its plastic recycling sector,” circemed.org Casablanca-Settat hosts the largest converting cluster, anchored by GPC’s Mohammedia hub and fast-growing Kénitra recycling complex.

Inland, GPC’s MAD 200 million (USD 20 million) Meknès Agropolis plant, 50% complete, will slash haulage costs for Fès-Meknès citrus exporters and improve carton lead times. Southern expansion is visible in Dakhla, where a new 35,000-tonne plant will triple carton exports to West Africa. Organized retail is likewise spreading: Marjane’s new Ouarzazate hypermarket, powered by rooftop solar, and JYSK’s inland store pipeline are spreading demand into secondary cities.

Rising purchasing power in Fez, Meknes, Agadir, and Tangier increases per-capita carton consumption and prompts regional fulfillment centers to source near-site packaging. The Moroccan folding carton market, therefore, exhibits a two-node geography: export-driven coastal corridors and nascent interior growth pockets tied to retail formalization. The growing demand for sustainable packaging solutions further influences market dynamics.

Competitive Landscape

The Morocco folding carton market is moderately fragmented. GPC commands more than half of industrial packaging and 35% of agricultural cartons, but international groups such as Mondi, International Paper, and Graphic Packaging selectively supply premium grades via imports or alliances. Mondi’s European upgrade program (USD 1.32 billion) expands specialty containerboard supply into North Africa. Domestic players verticalize: GPC’s Kénitra recycling mill cuts virgin-fiber imports, and its upcoming IPO aims to fund digital presses and energy-efficient lines.

Private equity is active: Mediterrania Capital Partners acquired Amcor Flexibles Mohammedia in April 2026, with plans to implement operational upgrades and diversify its product range. Technology adoption is the new battleground. GPC’s USD 55 million hybrid digital line and USD 3.7 million EBRD-financed automatic corrugator cut energy use 35% and CO2 by 27%.[4]European Bank for Reconstruction and Development press office, “A paper and cardboard packaging producer boosts output with high-performance automatic line,” ebrdgeff.com Smaller converters leverage EU grants of EUR 115 million (USD 126.5 million) for eco-equipment and EUR 50 million (USD 55.0 million) for clean energy to modernize plants.

Competitive intensity is set to climb as organized retailers consolidate procurement and EU Extended Producer Responsibility rules tighten specifications. Converters able to certify fiber origin, embed QR-based traceability, and offer agile digital print runs will secure export contracts, while laggards risk margin erosion. The Morocco folding carton industry therefore sits at an inflection: capital-rich leaders are scaling capacity and sustainability metrics, whereas sub-scale firms may become acquisition targets or niche regional specialists.

Morocco Folding Carton Industry Leaders

Mondi plc

International Paper Company

Mayr-Melnhof Karton AG

Huhtamäki Oyj

Tetra Pak Egypt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GPC announced its MAD 200 million (USD 20 million) Agropolis Meknès expansion, which is over 50% complete and will supply digital-printed citrus and red-fruit cartons, with commissioning by end-2026.

- April 2026: Mediterrania Capital Partners agreed to acquire 100% of Amcor Flexibles Mohammedia, aiming to diversify its dairy, pharma, and personal-care packaging portfolio.

- March 2026: Severe congestion at Casablanca and Tanger Med delayed January imports until May, forcing temporary diversions to Spanish ports and disrupting packaging operations.

- March 2025: Casino and H&S Invest Holding partnered to roll out 210 Franprix and Monoprix stores nationwide by 2035.

Morocco Folding Carton Market Report Scope

The scope of this report covers the analysis of the folding carton market in Morocco. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, personal care, pharmaceuticals, and others. These cartons are lightweight, customizable, and recyclable, making them a preferred choice for sustainable packaging. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future prospects.

The Morocco Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Morocco folding carton market?

The Morocco folding carton market size is estimated at USD 122.85 million in 2026, according to Mordor Intelligence.

Which material segment is growing fastest within Morocco’s folding cartons?

Solid Bleached Sulfate boards are forecast to advance at an 8.27% CAGR through 2031 as exporters adopt premium, moisture-resistant packaging.

How are e-commerce trends influencing carton specifications?

Online sales growth favors small-format, return-ready cartons with branded interiors and tamper seals, driving adoption of digital and hybrid print technologies.

What impact does Law 77-15 have on carton demand?

The plastic-bag ban pushes organized retailers toward shelf-ready folding cartons, increasing demand despite enforcement gaps in informal markets.

Who holds the largest share of Morocco’s industrial and agricultural carton output?

GPC commands more than 50% of industrial and roughly 35% of agricultural folding carton volumes, while international suppliers focus on premium imports.

Page last updated on: